Bambang Leo Handoko*![]() | Dinda Sabrina Indrawati

| Dinda Sabrina Indrawati![]() | Salsabila Rafifa Putri Zulkarnaen

| Salsabila Rafifa Putri Zulkarnaen![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The impact of technological developments has now led to a transformation in the preparation of financial statements. By applying machine learning, auditors can easily increase anomalies detection. The purpose of this study is to determine the effect of optimism, innovativeness, perceived usefulness, and perceived ease of use on auditors’ intention to use machine learning. Data were collected using an online questionnaire and analyzed using the Structural Equation Modeling-Partial Least Square (SEM-PLS). The sample in this study used a nonprobability sampling and has a sample size of 100 respondents from auditors who work in a Public Accounting Firm in DKI Jakarta and Tangerang areas. The results of testing this study using SmartPLS 4 are optimism has a significant effect on perceived usefulness and perceived ease of use, while innovativeness only has a significant effect on perceived ease of use. In addition, perceived ease of use has a significant effect on perceived usefulness. This study implies that auditors' perception of the usefulness can influence the intention to use machine learning. However, perceived ease of use does not affect the intention to use machine learning. Therefore, we suggest that audit firms could establish training programs to enhance digital skills for auditor.

machine learning, auditing, anomalies, technology acceptance model, technology readiness index

In this era of industrial revolution 4.0, technological developments have become increasingly advanced, considerable by the emergence of Artificial Intelligence. The existence of the industrial revolution 4.0 affects all entities including the accounting field, especially in the audit process. Audit is an activity that has experienced developments in information technology, including Big Data. Big data has five characteristics consisting of Velocity, Volume, Value, Variety and Veracity. In accordance with one of the characteristics of big data, which is Volume, auditors are currently dealing with very large data information. With the use of big data analytics systems in audits, auditors will cover data, identify risks, complete audits quickly and at a higher level of quality so that clients get better insights [1]. Therefore, the application of technology in the audit process can assist auditors in analyzing data to find anomalies so as to provide more relevant audit results.

AI (Artificial Intelligence) is a machine concept that has been programmed automatically which aims to make work more efficient and reduce human error. The use of artificial intelligence is essential in the audit process as it provides the necessary tools for auditors to improve the effectiveness and efficiency of their work. The purpose of the audit process is mainly detecting anomalies, providing scope in AI to improve quality such as reducing error rates and efficiency by automating tasks such as detecting fraud from the audit process. A part of Artificial Intelligence, machine learning, is successfully applied to detect fraud and anomalies in data. Data anomalies are financial statement irregularities that usually occur due to errors in recording transactions. Anomalous data is a symptom of financial statement fraud because it has an unreasonable nominal value compared to established accounting standards. Algorithms from machine learning can analyze large amounts of data, identify suspicious patterns, and predict outcomes. Therefore, machine learning can contribute to preventing anomalies in financial reporting so as to provide good audit quality results.

In conducting research on auditors' readiness to adopt the use of machine learning, researchers used the Technology Readiness and Acceptance Model (TRAM) model. TRAM is a combined model between Technology Readiness Index (TRI) and Technology Acceptance (TAM). TRAM can explain from the point of view of personal opinion (TRI) and the impact on the intended and actual use of technology (PU and PEU) on adoption in their use life (ITU). This research only uses positive dimensions of the TRI variable including Optimism and Innovativeness. The positive dimensions of TRI lead to increased levels of PU and PEU [2]. In addition, PU and PEU effectively mediate the link between individuals’ beliefs about technology (TRI) and their intention to adopt and use that technology [3]. By using the TRAM model, researchers can test the level of technology readiness (TRI) for auditors and the construction of machine learning adoption (TAM), so that companies can prepare for the use of machine learning technology for the audit process in the future. This research can also provide insight into the new technology skills required for auditors in the future.

There are several preliminary studies that discuss the use of AI in the auditor's environment, for example, Al-Ateeq et al. [4] examined the impacts of using two dimensions of the technology acceptance model (TAM), using perceived usefulness and perceived ease of use on the adoption of big data analytics in auditing. Hayek et al. [5] also examined the external auditor’s perceptions of the ease of use and usefulness of machine learning in auditing in the UAE. However, until now there has been no research that examines the impacts of using the TRAM framework on the auditor's intention to use machine learning. Therefore, this study aims to determine the effect of using two positive dimensions of the TRAM which is optimism and innovativeness, while perceived usefulness and perceived ease of use as intervening variables on auditor’s response in readiness to use machine learning.

2.1 Theoretical background

Machine learning is the process of analyzing data using algorithms, finding implicit patterns, and applying the patterns found to make predictions about the future. Several studies have employed machine learning approaches in affecting the quality of financial reports. Aly et al. [6] investigated the relationship between machine learning algorithms and auditors’ assessments of the risks of material misstatement and restatement. The results showed machine learning techniques have a positive significant effect on the intentional misstatements. El Gawad [7] examined the effect of machine learning algorithms on the prediction accuracy of going concern opinion. From the result, El Gawad [7] recommended that auditors should be interested in developing their skills to be able to use machine learning in issuing audit opinions.

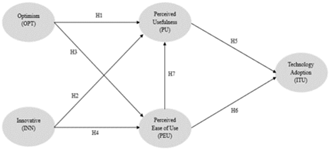

TRAM (Technology Readiness and Acceptance Model) is a combination of the concepts from TAM (Technology Acceptance Model) and TRI (Technology Readiness Index) which emphasizes how an individual’s level of readiness can impact their ability to interact, experience, and use new technology [8]. Optimism and innovation are the two variables that influence technology readiness. These factors affect the TAM-derived variables that affect the user’s intention to use the technology, that is Perception of Usefulness and Perception of Ease of Use [9].

Figure 1. Research model

In this study, we mainly focus on the positive dimension (Optimism and Innovative) that positively influence auditors’ intention to use of machine learning. Optimism is a positive dimension of technology users where the user of technology can optimistically increase efficiency by adopting new technology. When technology improves human life and presents convenience, individuals will be more positive about it, which will lead to a positive view of technology and generate the intention to use it [10]. We presented the research model in Figure 1.

As for innovative, it is a positive attribute that states an individual’s willingness to experiment with technology and take the lead in utilizing the newest systems based on technology [11]. This variable is an indicator that provides positive self-confidence and optimism, as a result of which users are motivated and interested in experimenting with the presence of technology in trying the new technology-based systems or services.

The studies [12, 13] defined Perceived Ease of Use as the user’s perception of the effort in using a system or technology. Based on these perceptions, it indicates individual beliefs by using information technology systems will neither be complicated nor require a lot of effort in using the technology because when someone has the belief that technology can be easily used, a person’s intention will increase to use technology [14].

Perceived Usefulness is a user's subjective view of how much the use of a system can improve their performance [15]. The belief of someone who thinks that if an individual uses a certain information technology system, the performance of the work performed will increase [16]. The extent to which a person thinks that using the system can improve performance at their work [17]. Perceived usefulness refers to the utilization of specific computer systems that will enhance these systems’ functionality.

Intention to use is an individual’s level of enthusiasm to use information technology consistently, assuming they’ve got access to information technology, is referred to as their interest in using information technology [18]. Technology readiness is the presence of positive personal feelings that encourage the use of new technology. Therefore, TRAM Framework has been used by many study as it provides an excellent theoretical basis for analyzing the user’s intention to use the technology in the audit process.

2.2 Hypothesis development

Optimism relates to a positive view towards technology and trust that it will offer people more efficiency, flexibility and control [10]. Moreover, Innovativeness is defined as the willingness to be a pioneer of a technology. Innovative users are interested in exploring the attributes of machine learning so as to accept the value and utility of machine learning. Previous related research [19] has found that optimism has a significant effect on perceived usefulness of digital health technology. This result encourages older adults to use digital health technology and obtain health benefits from it. Al-Adwan et al. [20] has found that innovativeness has significantly positively affects perceived usefulness. A similar study [21] indicated that technology readiness positively influences the accountants’ and auditors’ perceived usefulness. In the context of machine learning, optimistic and innovative users have a positive view of the functions provided by machine learning and tend to believe that machine learning can be more efficient in the audit process. Therefore,

H1: Optimism (OPT) has a significance effect on Perceived Usefulness (PU) of Machine Learning.

H2: Innovative (INN) has a significance effect on Perceived Usefulness (PU) of Machine Learning.

Ease of use, based on the study [16], is the extent to which a user feels that using a particular technology requires to be free from effort. Auditors who have an interesting and enthusiastic attitude in adopting new technology such as machine learning will tend to further understand the mechanism of a technology so that the user's perception will increasingly feel the ease of use of the machine learning. An individual’s enthusiasm to use technology increases when they think it can be utilized effortlessly or with little effort. Measuring an individual's interest in experimenting with technology and their willingness to be innovative in testing out the newest technology-based products or services [22].

Recently, Hassan et al. [23] examined the impact of innovation and customer optimism on the ease of using self service technologies, and the results indicated that innovation and optimism has a significant effect on perceived ease of use. Thus, the increase in innovative and optimism is associated with a rise in the perceived ease of self service technology use. Another significant effect was found in the study [24] that auditors; optimistic and innovative attitudes have a positive and significant influence on their perceived ease of use of CAATs and their perception improved performance when utilizing CAATs in conducting audits. Therefore,

H3: Optimism (OPT) has a significance effect on Perceived Ease of Use (PEU) of Machine Learning.

H4: Innovative (INN) has a significance effect on Perceived Ease of Use (PEU) of Machine Learning.

Changes in the level of perceived usefulness will affect the level of auditor interest in using machine learning. With the influence of perceived usefulness positively and significantly, using technology will have an impact such as improving performance, working effectively and usefully. Arachchi and Samarasinghe [25] identified significant and positively impact perceived usefulness related to AI and attitudes towards technology on impulse purchase intention. More recently, Sudaryanto et al. [26] conducted a study on accounting students and found that perceived usefulness significantly influence the application of AI technology in work,

H5: Perceived Usefulness (PU) has a significance effect on Auditor Acceptance of Machine Learning (ITU).

Perceived ease of use refers to how accessible potential users expect the system would be. Perceived Ease of Use expresses a person's belief that using an information technology system does not cause problems in its use [12]. The ease of use perceived by the auditor will affect the interest in using machine learning technology. TAM shows that there is a positive relationship between perceived ease of use and perceived usefulness. The studies [21, 27] provided results that perceived ease of use positively influences perceived usefulness. It is evident that users who find it easy to use technology tend to perceive usefulness. Therefore,

H6: Perceived Ease of Use (PEU) has a significance effect on Perceived Usefulness (PU) of Machine Learning.

A subjective view of the user on the possibility of using a system can improve performance. The benefits perceived by auditors when using machine learning will affect the interest in using machine learning for users. According to the study [28], perceived ease of use had positive correlation with the interest of customers to purchase and smartwatches for their healthcare services. Based on findings, it can be suggested that elderly customers are more likely to develop purchasing intentions for a smartwatch device if they find that device is useful and easy. Ummah and Sofyani [29] have also found perceived ease of use positively influenced the intentions of local government employees to use blockchain technology in accounting information system. Therefore,

H7: Perceived Ease of Use (PEU) has a significance effect on Intention to Use (ITU) machine learning.

This study uses a quantitative approach as a method to examine the impact of technology readiness in machine learning on the auditors’ intention to use. According to the study [30], quantitative research begins with a statement of the issue, generating hypotheses or research questions, reviewing related literature, and quantitative data analysis. The type of data that we used in this research is primary data obtained through distributing questionnaires to respondents through Google Form. We use non-probability sampling techniques with a purposive sampling which is based on specified criteria.

As for sampling in this study, it refers to the statement Roscoe dan Hair. According to the study [31], an appropriate sample size in research is 30 to 500. Whereas, Hair Jr et al. [32] explained that the total population size cannot be known with certainty and if there are more than 20 indicators on the sample size in SEM analysis (Structural Equation Model), then the sample size is between 100-200. Therefore, in this study we use an unknown population because the number of auditors working in an audit firm cannot be calculated exactly, where at any time there are auditors who join or resign.

Respondents in this study are auditors who currently work in Public Accounting Firms Indonesia around Jakarta and Tangerang areas. To measure the attitudes and opinions of auditor respondents, we use a Likert measurement scale. In this research we made questionnaire questions from the operationalization of variables using a Likert measurement scale of 1-4 where 1=“strongly disagree” and 4=“strongly agree”. On a Likert scale, respondents must indicate their level of agreement with the questions asked so as to avoid irrelevant answers. The likert scale is also used by researchers to make it easier to analyze data, where in this research we used SmartPLS 4 and Microsoft Excel for analysis.

The data source used in this research is primary data obtained from a questionnaire created and distributed through Google Form. Data collection in this study was conducted with a questionnaire containing respondents' personal data and indicators intended to test the variables used in the study. The list of questions used in the questionnaire was obtained from several previous studies that had been tested with some development by actual researchers.

Variable operationalization consist of research variables, dimensions and indicators to measure these variables. Variable operationalization can be used to identify observable criteria that make it easier to measure variables. The operational variables in this study are understanding Optimisim, Innovativeness, Perceived Usefulness, and Perceived Ease of Use as independent variables. Meanwhile, the dependent variable is Intention to Use. The operationalization is presented in Table 1 as follows:

Table 1. Variable operationalization

|

Variables |

Indicator |

|

|

Optimism |

OPT1 |

Technology's contribution to the quality of work |

|

OPT2 |

Ease of mobility |

|

|

OPT3 |

Job control with technology |

|

|

OPT4 |

Productivity |

|

|

Innovativeness |

INN1 |

Ability to provide information related to technology |

|

INN2 |

Good of technology usage |

|

|

INN3 |

Independence in utilization of technology |

|

|

INN4 |

Keeping up with technological developments |

|

|

Perceived Usefulness |

PU1 |

Work efficiency |

|

PU2 |

Job performance |

|

|

PU3 |

Productivity improvement |

|

|

PU4 |

Ease of work |

|

|

PU5 |

Assessment of benefits |

|

|

Perceived Ease of Use |

PEU1 |

Easy-to-learn technology |

|

PEU2 |

Easy to control the technology |

|

|

PEU3 |

Clear and easily understandable |

|

|

PEU4 |

Flexibility |

|

|

PEU5 |

Make the job easier |

|

|

Intention to Use |

ITU1 |

Interest in use |

|

ITU2 |

Interest in system development |

|

4.1 Result

The sample in this study was conducted using an online questionnaire through Google Form and distributed to auditors at the Public Accounting Firm in the DKI Jakarta and Tangerang areas. The questionnaire was distributed on September 14, 2023 to January 09, 2024. The final sample of the study is 100 auditors answered a survey questionnare. The questionnaire was specifically designed to accomplish the objectives of the study and test the study hypotheses. This questionnaire will measure the auditors’ intention to use machine learning.

Table 2. Characteristic of respondent

|

No |

Variable |

Frequency |

Percentage |

|

1 |

Age: 20-30 years old 31-40 years old 41-50 years old >50 years old |

91 6 1 2 |

91% 6% 1% 2% |

|

2 |

Gender: Female Male |

58 42 |

58% 42% |

|

3 |

Type of Public Accounting Firm: Big Four Non Big Four |

29 71 |

29% 71% |

|

4 |

Position: Partner Supervisor/Manager Senior Auditor Junior Auditor |

3 2 16 79 |

3% 2% 16% 79% |

|

5 |

Work Experience: 1-5 years 6-10 years 11-15 years >15 years |

92 5 0 3 |

92% 5% 0% 3% |

|

|

Total |

100 |

100% |

Table 2 shows the characteristic of respondent in this study. The distribution of respondents based on age showed that the majority were 20-30 years old (91%). Data based on gender, there is a higher percentage of female respondents (58%) than male respondents (42%). Respondents who work in non big four public accounting firms have a higher percentage (71%) compared to respondents who work in big four public accounting firms (29%). Meanwhile, for position and work experience, the highest percentage was obtained by respondents who worked as junior auditors (79%) and have been employed for 1-5 years (92%). We presented the path coefficient in Figure 2.

Figure 2. Measurement model

Based on the measurement model above, there are 5 variables consisting of 4 exogenous variables (OPT, INN, PU, PEU) and 1 endogenous variable (ITU) with a total of 20 statement items. The first stage of data processing is to test the outer model. The outer model test aims to explain the relationship between latent variables and their indicators. The results show that the outer loadings value of each relationship between the construct and its indicators gives a good result with a value of more than 0.70.

For the reliability test, this study used Cronbach alpha and Composite reliability values. If the Cronbach alpha and composite reliability values are more than 0.70, then the variables has good reliability results. Based on the test results in Table 3, the Cronbach’s alpha and Composite reliability values show that all variables have values greater than 0.70. It can be concluded that each variable used in this research is reliable.

Table 3. Result of construct reliability and validity

|

Variable |

Cronbach's Alpha |

Composite Reliability (Rho_c) |

Average Variance Extracted (AVE) |

|

INN |

0.841 |

0.894 |

0.68 |

|

ITU |

0.851 |

0.931 |

0.871 |

|

OPT |

0.81 |

0.875 |

0.637 |

|

PEU |

0.879 |

0.912 |

0.675 |

|

PU |

0.875 |

0.909 |

0.667 |

While for the convergent validity test, this study use Average Variance Extracted (AVE). If the rest results have an AVE value of more than 0.50 then the variables has good validity results. Based on the results in Table 3, it shows that each variable has an AVE value greater than 0.50. It can be concluded that the indicators for this research variable have met convergent validity.

In addition to the convergent validity test, there is also discriminant validity using the Fornell-Larcker criteria. In Table 4, the results of the discriminant validity test show that the root AVE value is higher than the correlation between constructs and other constructs. Thus, it can be concluded that the indicators of the research variables used have met good discriminant validity and all research data can be used validly.

Table 4. Result of discriminant validity (Fornell-Larcker criterion)

|

Discriminant Validity (Fornell-Larcker Criterion) |

|||||

|

Variable |

INN |

ITU |

OPT |

PEU |

PU |

|

INN |

0.824 |

|

|

|

|

|

ITU |

0.383 |

0.933 |

|

|

|

|

OPT |

0.522 |

0.76 |

0.798 |

|

|

|

PEU |

0.744 |

0.615 |

0.665 |

0.822 |

|

|

PU |

0.541 |

0.725 |

0.773 |

0.729 |

0.817 |

The multicollinearity test using the VIF method aims to check whether multicollinearity occurs in the research variables. The results of the multicollinearity test can be concluded as good if the VIF value is less than 10. The results of Table 5 show that the VIF value obtained in this study is below 10, which means that this research is free from symptoms of multicollinearity.

Table 5. Results of collinearity statistics (VIF) - Inner model

|

Collinearity Statistics (VIF)-Inner Model |

|||||

|

Variable |

INN |

ITU |

OPT |

PEU |

PU |

|

INN |

|

|

|

1.374 |

1.374 |

|

ITU |

|

|

|

|

|

|

OPT |

|

|

|

1.374 |

1.374 |

|

PEU |

|

2.113 |

|

|

|

|

PU |

|

2.113 |

|

|

|

In regression analysis it is used to determine and predict how large or important the contribution of the influence given by exogenous variables together to endogenous variables [33]. If the R-square result has a greater value, the better the explanatory power of the exogenous variable. Based on the test results in Table 6, the R-square value for the Intention to Use variable for auditors adopting machine learning succeeded in explaining 53.20%. This shows that 46.80% is explained by other variables outside this research. Furthermore, the Perceived Ease of Use variable succeeded in explaining 65.20% and 34.80% was explained by other variables outside this research. While, the Perceived Usefulness variable succeeded in explaining 67.10% and the remaining 32.90% was explained by other variables outside this research.

Table 6. R-square and R-square adjusted

|

Variable |

R-Square |

R-Square Adjusted |

|

ITU |

0.541 |

0.532 |

|

PEU |

0.659 |

0.652 |

|

PU |

0.681 |

0.671 |

There are seven hypotheses tested in this research using SmartPLS 4. Researchers used Bootstrapping analysis to assess the level of significance with t-statistics and p-value of the hypothesis results. If the significance value obtained is lower than 0.05 or 5% then the hypothesis can be accepted.

From the test results in Table 7, it can be seen that there are 5 hypotheses accepted and 2 hypotheses rejected. H2 and H7 are rejected because they have a p-value greater than the 5% significant level. While, the other five hypotheses have a significant level value of less than 5%, which means the hypothesis is accepted.

Table 7. Structural model testing

|

Variable |

Original Sample (O) |

T-Statistics |

P-Values |

Findings |

|

OPT→PU |

0.519 |

4.919 |

0.000 |

H1 Accepted |

|

INN→PU |

-0.034 |

0.351 |

0.726 |

H2 Rejected |

|

OPT→PEU |

0.381 |

5.277 |

0.000 |

H3 Accepted |

|

INN→PEU |

0.545 |

8.624 |

0.000 |

H4 Accepted |

|

PU→ITU |

0.591 |

6.773 |

0.000 |

H5 Accepted |

|

PEU→PU |

0.409 |

3.491 |

0.000 |

H6 Accepted |

|

PEU→ITU |

0.184 |

1.808 |

0.071 |

H7 Rejected |

In Table 7, it can be seen that Hypothesis H1 was accepted in this research because Optimism had a significant effect on Perceived Usefulness. These results show that H1 has a positive regression coefficient of 0.519, and a p-value of 0.000 with a t-value of 4.919. However, hypothesis H2 was rejected in this study because Innovativeness had no significant effect on Perceived Usefulness. The regression coefficient in this hypothesis has a negative result (-0.034) and a p-value of 0.726 with a t-value of 0.351, which means the significance value of H2 is greater than 0.05 so the hypothesis H2 is rejected.

Then the relationship between Optimism and Perceived Ease of Use in hypothesis H3 is accepted in this research. H3 has a positive relationship direction (0.381) and a p-value of 0.000 with a t-value of 5.277. Hypothesis H4 is also accepted, which is the relationship between Innovativeness and Perceived Ease of Use. The results of this hypothesis show a positive relationship direction (0.545) and a p-value of 0.000 with a t-value of 8.624.

Hypothesis H5 is accepted which is the relationship between Perceived Usefulness and Intention to Use. There is a positive relationship (0.591) and a p-value of 0.000 with a t-value of 6.773. Hypothesis H6 is also accepted, which is the relationship between Perceived Ease of Use and Perceived Usefulness. These results show a positive regression coefficient (0.409) and a p-value of 0.000 with a t-value of 3.491. Meanwhile, Hypothesis H7 is rejected because it has insignificant results, but it has a positive regression coefficient (0.184) and the p-value has a value greater than 0.05, that is 0.071 with a t-value of 1.808.

4.2 Discussion

(1) The Effect of Optimism on Perceived Usefulness and Perceived Ease of Use

Based on the data test results in H1 and H3, the final result is that optimism has a significant effect on perceived usefulness and perceived ease of use, so that both hypotheses are accepted. This finding is similar to researches [19, 24] showing that individual with high optimism are more likely to adopt new technologies. Therefore, from testing this hypothesis, it can be concluded that auditors have an optimistic attitude in using machine learning which can provide benefits and make it easier for them in the audit process. We assume that since several public accounting firms are currently integrating artificial intelligence in the audit process, so that auditors have a good perception of technology adoption.

(2) The Effect of Innovativeness on Perceived Usefulness and Perceived Ease of Use

The results of H2 show that innovativeness has no significant effect on perceived usefulness so the results of this hypothesis are rejected. The results contradict those of study [20], who found a significant effect of innovativeness on perceived usefulness. From these results, it can be concluded that auditors’ willingness to experiment and utilize the machine learning technology in the audit process is still lacking. A reasonable explanation for this results are auditors feel that the audit technology used at this time is enough to be useful.

Whereas the results of the H4 test are accepted because innovativeness has a significant effect on perceived ease of use. These findings are in line with the results of research conducted by the study [23] where it was found that innovativeness had a significant effect on perceived ease of use. So these results show that auditors have a level of interest in user knowledge in detecting anomalies using machine learning easily.

(3) The Effect of Perceived Ease of Use on Perceived Usefulness

In examining this effect of Perceived Ease of Use on Perceived Usefulness, the researcher proposes a hypothesis on H6 which gives the result that Perceived Ease of Use affects Perceived Usefulness, so the hypothesis is accepted. These findings are similar to the studies [21, 27] which have found the perceived ease of use positively influences its perceived usefulness. Perceived ease of use is also considered a determinant of perceived usefulness because it can affect the adoption of technology through perceived usefulness. From these results it can be concluded that auditors who have ease of use of machine learning tend to have confidence that the system will improve their performance.

(4) The Effect of Perceived Usefulness and Perceived Ease of Use on Intention to Use

The results of hypotheses H5 show that Perceived Usefulness has a significant influence on Intention to Use in adopting machine learning. This finding is aligned with the study [26]. Therefore, it can be concluded that auditors have perceived that using AI will make their work more efficient so they are more likely to have intention to use AI in audit process. Auditors have confidence that the use of machine learning technology can improve performance and work effectively and usefully.

While, the hypothesis test on H7 shows that Perceived Ease of Use has no significant effect on Intention to Use in adopting machine learning. This is contradicting the research [28]. We assumed that some auditors thought that adopting machine learning is difficult and they have to learn new machine learning application procedures. Therefore, the perception of ease of using machine learning by the auditors is still lacking.

This research has concluded that respondents, which in this case are auditors who work in public accounting firms, have a positive view of Technology Readiness to accept and adopt machine learning technology in detecting data anomalies. This results is proven that optimism have a significant influence on perceived usefulness and perceived ease of use. While innovativeness has only a significant effect on perceived ease of use. Auditors have the perception that the use of machine learning can help auditors to detect errors and fraud in financial statements. In addition, using machine learning will improve the performance of an auditor and work effectively. This makes users feel satisfied with the results of their work and will accept the adoption of machine learning in audit activities. The findings of this study indicate that Indonesian public accounting firms can adopt machine learning technology for the audit process to optimize the efficiency of the auditor's work. Practical application for audit firm to harness the full potential of AI in auditing, firms are advised to adopt a strategic and gradual approach. Prioritize investments in AI tools such as hardware and software that align with specific audit objectives and cater to the unique needs of the organization. Establish comprehensive training programs to enhance the digital skills of auditor and fostering a culture of continuous learning to keep pace with AI developments. In addition, develop a proactive cybersecurity framework to protect sensitive client information and maintain compliance with data protection regulations. Lastly, regularly assess and adapt AI strategies to remain agile in the face of developing technologies, positioning audit firms at the forefront of innovation in the constantly changing field of audit practices.

In conclusion, while this research provides insightful information with the challenges experienced by Indonesian auditors, it is critical to recognize the specific limitations within its scope. This study’s focus on the Indonesian context may limit the generalizability of findings to a broader global context, given the unique socio-economic, cultural and regulatory aspects of the country. Additionally, the evolving of rapid technological advancements, and potential industry specific variations highlight the need for continuous examination. The limitations of this study are focus only on public accounting firm that located in DKI Jakarta and Tangerang areas. Therefore, future research endeavors should consider expanding the geographical scope. Researchers can make similar studies but the samples are in different countries, their result can be compared and enrich the literature in the field of AI and Auditing.

This study provides a foundation for future researchers to expand the exploration of AI in auditing by conducting similar research in different countries. By replicating this study in diverse cultural, regulatory, and economic contexts, researchers can gain a deeper understanding of how AI is used and perceived in the global audit profession. Investigating the adoption of AI in audit practices in different countries can uncover unique challenges, opportunities, and best practices, thus enriching the knowledge base of academia and industry. In addition, comparative studies can encourage cross-country collaboration, facilitate knowledge exchange, and contribute to the development of international standards and guidelines for AI-based audit practices.

[1] Janssen, M., Van Der Voort, H., Wahyudi, A. (2017). Factors influencing big data decision-making quality. Journal of Business Research, 70: 338-345. https://doi.org/10.1016/j.jbusres.2016.08.007

[2] Smit, C., Roberts-Lombard, M., Mpinganjira, M. (2018). Technology readiness and mobile self-service technology adoption in the airline industry: An emerging market perspective. Acta Commercii, 18(1): 1-12. https://hdl.handle.net/10520/EJC-11e9e5d7f0

[3] Lin, C.H., Shih, H.Y., Sher, P.J. (2007). Integrating technology readiness into technology acceptance: The TRAM model. Psychology & Marketing, 24(7): 641-657. https://doi.org/10.1002/mar.20177

[4] Al-Ateeq, B., Sawan, N., Al-Hajaya, K., Altarawneh, M., Al-Makhadmeh, A. (2022). Big data analytics in auditing and the consequences for audit quality: A study using the technology acceptance model (TAM). Corporate Governance and Organizational Behavior Review, 6(1): 64-78. https://doi.org/10.22495/cgobrv6i1p5

[5] Hayek, A.F., Noordin, N.A., Hussainey, K. (2022). Machine learning and external auditor perception: An analysis for UAE external auditors using technology acceptance model. Journal of Accounting and Management Information Systems, 21(4): 475-500.

[6] Aly, H.G., Elguoshy, O.R., Metwaly, M.Z. (2023). Machine learning algorithms and Auditor’s assessments of the risks material misstatement: Evidence from the restatement of Listed London Companies. Information Sciences Letters, 12(4): 1285-1298.

[7] El Gawad, S.F.A. (2023). The effect of using machine learning algorithms alternatives on the prediction accuracy of going concern opinion. Scientific Journal of Studied and Research Financial and Administrative Studies, 15(3): 1-24. https://doi.org/10.21608/masf.2023.325469

[8] Khadka, R., Kohsuwan, P. (2018). Understanding consumers’ mobile banking adoption in Germany: An integrated technology readiness and acceptance model (TRAM) perspective. Catalyst, 18: 56-67.

[9] Hadisuwarno, A.E., Bisma, R. (2020). Analisis penerimaan pengguna aplikasi e-Kinerja dengan metode TRAM dan EUCS pada kepolisian. Teknologi: Jurnal Ilmiah Sistem Informasi, 10(2): 93-109. https://doi.org/10.26594/teknologi.v10i2.2062

[10] Parasuraman, A. (2000). Technology readiness index (TRI) a multiple-item scale to measure readiness to embrace new technologies. Journal of Service Research, 2(4): 307-320. https://doi.org/10.1177/109467050024001

[11] Simiyu, S.C., Kohsuwan, P. (2019). Understanding Consumers' mobile banking adoption through the integrated technology readiness and acceptance model (TRAM) perspective: A comparative investigation. Human Behavior, Development & Society, 20(4).

[12] Liu, Y., Wang, M., Huang, D., Huang, Q., Yang, H., Li, Z. (2019). The impact of mobility, risk, and cost on the users’ intention to adopt mobile payments. Information Systems and e-Business Management, 17: 319-342. https://doi.org/10.1007/s10257-019-00449-0

[13] Venkatesh, V., Davis, F.D. (1996). A model of the antecedents of perceived ease of use: Development and test. Decision Sciences, 27(3): 451-481. https://doi.org/10.1111/j.1540-5915.1996.tb00860.x

[14] Tony Sitinjak, M.M. (2019). Pengaruh persepsi kebermanfaatan dan persepsi kemudahan penggunaan terhadap minat penggunaan layanan pembayaran digital Go-Pay. Jurnal Manajemen, 8(2).

[15] Lai, P.C. (2017). Security as an extension to TAM model: Consumers’ intention to use a single platform E-Payment. Asia-Pacific Journal of Management Research and Innovation, 13(3-4): 110-119. https://doi.org/10.1177/2319510X18776405

[16] Davis, F.D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 319-340. https://doi.org/10.2307/249008

[17] Andayani, S., Ono, R.S. (2020). Analisis kesiapan penerimaan pengguna terhadap e-learning menggunakan model tram. JuSiTik: Jurnal Sistem dan Teknologi Informasi Komunikasi, 3(2): 32-39.

[18] Jati, N.J., Laksito, H. (2012). Analisis faktor-faktor yang mempengaruhi minat pemanfaatan dan penggunaan sistem e-ticket (Studi empiris pada biro perjalanan di Kota Semarang) (Doctoral dissertation, Fakultas Ekonomika dan Bisnis). Diponegoro Journal of Accounting, 1(1): 511-524.

[19] Kim, S., Chow, B.C., Park, S., Liu, H. (2023). The usage of digital health technology among older adults in Hong Kong and the role of technology readiness and eHealth literacy: Path analysis. Journal of Medical Internet Research, 25(1): e41915. https://doi.org/10.2196/41915

[20] Al-Adwan, A.S., Li, N., Al-Adwan, A., Abbasi, G.A., Albelbisi, N.A., Habibi, A. (2023). Extending the technology acceptance model (TAM) to Predict University Students’ intentions to use metaverse-based learning platforms. Education and Information Technologies, 28(11): 15381-15413. https://doi.org/10.1007/s10639-023-11816-3

[21] Anh, N.T.M., Hoa, L.T.K., Thao, L.P., Nhi, D.A., Long, N.T., Truc, N.T., Ngoc Xuan, V. (2024). The effect of technology readiness on adopting artificial intelligence in accounting and auditing in Vietnam. Journal of Risk and Financial Management, 17(1): 27. https://doi.org/10.3390/jrfm17010027

[22] Aisyah, M.N., Nugroho, M.A., Sagoro, E.M. (2014). Pengaruh technology readiness terhadap penerimaan teknologi komputer pada UMKM di Yogyakarta. Jurnal Economia, 10(2): 105-119. http://dx.doi.org/10.21831/economia.v10i2.7537

[23] Hassan, H.G., Nassar, M., Abdien, M.K. (2024). The influence of optimism and innovativeness on customers' perceptions of technological readiness in five-star hotels. Pharos International Journal of Tourism and Hospitality, 3(1): 70-80. https://doi.org/10.21608/pijth.2024.265141.1010

[24] Susanto, H., Pramono, A.J., Akbar, B., Suwarno, S. (2023). The adoption and readiness of digital technologies among auditors in public accounting firms: A structural equation modeling analysis. Research Horizon, 3(2): 71-85. https://doi.org/10.54518/rh.3.2.2023.71-85

[25] Arachchi, H.D.M., Samarasinghe, G.D. (2023). Impulse purchase intention in an ai-mediated retail environment: Extending the TAM with attitudes towards technology and innovativeness. Global Business Review, 09721509231197721. https://doi.org/10.1177/09721509231197721

[26] Sudaryanto, M.R., Hendrawan, M.A., Andrian, T. (2023). The effect of technology readiness, digital competence, perceived usefulness, and ease of use on accounting students artificial intelligence technology adoption. In E3S Web of Conferences. EDP Sciences, 388: 04055. https://doi.org/10.1051/e3sconf/202338804055

[27] An, S., Eck, T., Yim, H. (2023). Understanding consumers’ acceptance intention to use mobile food delivery applications through an extended technology acceptance model. Sustainability, 15(1): 832. https://doi.org/10.3390/su15010832

[28] Uzir, M.U.H., Bukari, Z., Al Halbusi, H., Lim, R., Wahab, S.N., Rasul, T., Thurasamy, R., Jerin, I., Chowdhury, M.R.K. Tarofderr, A.K., Yaakop, A.Y., Hamid, A.B.A., Haque, A., Rauf, A., Eneizan, B. (2023). Applied artificial intelligence: Acceptance-intention-purchase and satisfaction on smartwatch usage in a Ghanaian context. Heliyon, 9(8). https://doi.org/10.1016/j.heliyon.2023.e18666

[29] Ummah, R.S., Sofyani, H. (2024). Testing the intention of employees in local government to adopt blockchain technology in accounting information systems (AIS). Public Accounting and Sustainability, 1(1): 1-18.

[30] Williams, C. (2011). Research methods. Journal of Business & Economics Research (JBER), 5(3).

[31] Roscoe, J.T. (1969). Fundamental research statistics for the behavioral sciences. New York: Holt Rinehart & Winston, 1975. https://lccn.loc.gov/69017658.

[32] Hair Jr, J.F., Howard, M.C., Nitzl, C. (2020). Assessing measurement model quality in PLS-SEM using confirmatory composite analysis. Journal of Business Research, 109: 101-110. https://doi.org/10.1016/j.jbusres.2019.11.069

[33] Ghozali, I. (2016). Aplikasi analisis multivariate dengan program SPSS. Semarang: Badan Penerbit Universitas Diponegoro, vol. 8.