Ayoub Razouk*![]() | Hamza Melliani

| Hamza Melliani![]() | Jallal Mohamed El Adnani

| Jallal Mohamed El Adnani![]() | Moulay El Mehdi Falloul

| Moulay El Mehdi Falloul![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

As a burgeoning alternative to conventional finance, Islamic finance, characterized by its ethical and Shariah-compliant financial offerings, has garnered increasing global attention. This study sought to gauge public sentiment towards Islamic finance by leveraging sentiment analysis on a dataset of tweets amassed between 2007 and 2022. Data extraction from Twitter was performed using keywords pertinent to Islamic finance. The subsequent preprocessing of the tweets facilitated a text analysis, conducted with the aid of the pre-trained Twitter-roBERTa-base model. This model, trained on approximately 124 million tweets and fine-tuned on analogous data, was aptly suited for categorizing the Islamic finance-related tweets into positive, negative, or neutral sentiments. The findings primarily showed a neutral sentiment distribution: 57% neutral, 17.9% positive, and 24.8% negative. The term "Interest-free" surfaced as the most commonly associated with Islamic finance, followed by "Profit sharing," "Risk mitigation," and "Islamic banking." The study identified regions such as the United States, Gulf Cooperation Council (GCC) countries, Southeast Asia, the United Kingdom, and other European countries with large Muslim populations as prolific contributors to the Islamic finance discourse on Twitter. Moreover, the study underscored a cultural influence on public sentiment, with Muslim-majority nations predominantly expressing positive views towards Islamic finance, in contrast to the more negative sentiment prevalent in non-Muslim-majority nations. These findings provide valuable insights that could be harnessed to shape marketing and outreach initiatives, devise effective communication strategies, and guide policymakers in promoting awareness of Islamic finance through comprehensive education and awareness programs.

geolocation analysis, Islamic finance, sentiment analysis, social media perception, Twitter

In recent years, Islamic finance, with its ethical and Shariah-compliant financial offerings, has gained prominence as a credible alternative to traditional finance. This is particularly notable given the rise of the global Muslim population and the ensuing demand for such services. As Islamic finance penetrates the global financial landscape, its presence and influence are concurrently being observed on social media platforms, particularly on Twitter. With a user base exceeding 330 million worldwide [1], Twitter serves as a platform for individuals to articulate their perceptions and sentiments, thereby making it an ideal source for garnering insights into public sentiment towards Islamic finance.

It has been well established that big data analysis can provide organizations with significant insights into their operational landscape and customer needs [2]. Among all social media platforms, Twitter is often selected as the primary data source for sentiment analysis research. The reasons are manifold. Firstly, Twitter provides extensive, publicly available data, easily accessible to researchers. Secondly, the data collection process from Twitter is facilitated by the use of APIs and web scraping tools. Thirdly, the brevity of tweets ensures the quality of the data, making it manageable for analysis. Fourthly, the real-time update of Twitter data renders it suitable for examining current events and trends. Finally, its global popularity and wide user base make it an ideal platform for studying public opinion and sentiment [3-5]. Hence, platforms like Twitter have become invaluable for analyzing public perceptions and attitudes towards Islamic finance.

The global Islamic financial services industry (IFSI), valued at 3.06 trillion USD in 2021 [6], comprises significant segments like Islamic banking, which account for 68.7% of IFSI assets (2.10 trillion USD) with a growth rate of 6.5%, and the Islamic Capital Markets (ICM) segment, which constituted 30.5% of global IFSI assets (930.3 billion USD) in 2021, growing at a rate of 12.5% annually. Assets under Islamic fund management also saw a 6% increase. This growth trajectory is propelled by rising demand from Muslim consumers and growing awareness of the benefits of ethical, Shariah-compliant finance. However, despite this growth, perceptions of Islamic finance among non-Muslims and even some Muslims remain varied, with misconceptions and lack of understanding often culminating in negative perceptions. The increasing popularity of Islamic finance has simultaneously led to a surge in social media discussions on the topic, providing a fertile ground for data analysis.

Understanding the public's perception of Islamic finance is essential because it is a critical test of the sector's acceptance, growth, and sustainability. In this context, the public can be assimilated to a consumer who, faced with multiple financial products, has to make a reasoned choice. Public sentiment not only influences market dynamics but also shapes regulatory policies, educational initiatives, and the sector's competitive position in the wider financial landscape. Therefore, understanding and managing public perception is critical to the success of Islamic finance.

In this study, we conducted a sentiment analysis of tweets related to Islamic finance from 2007 to 2022. Our primary objective was to explore people's opinions and perceptions regarding this field and analyze the geographic distribution of these opinions. In particular, we seek to answer the following research questions: (1) What is the overall sentiment of Twitter users towards Islamic finance? Are tweets about Islamic finance predominantly positive, negative, or neutral? (2) What are the key themes and topics associated with Islamic finance on Twitter? What are the most frequently discussed aspects of Islamic finance on this platform?

We used SnScrape, a scraping tool for social networking services, to collect tweets related to Islamic finance from 2007 to 2022. We analyzed these tweets using Twitter-roBERTa-base model, this model is suited for classifying Islamic finance tweets because it has been trained on approximately 124 million tweets from and fine-tuned on similar data to categorize tweets into positive, negative, or neutral classes, and we conducted a detailed analysis of the resulting data. Also, we conducted an analysis of prevalent topics and themes by creating a word cloud, a data visualization technique that visually represents the most frequently occurring terms in our tweet’s dataset about Islamic finance. Additionally, we explore the geographical distribution of these tweets to provide insights into the global perception and popularity of Islamic finance.

The findings of our study provide valuable insights into people's perceptions of Islamic finance and its popularity worldwide. By analyzing the sentiments expressed in these tweets, we can identify the key features of Islamic finance that are most commonly discussed, and understand the drivers of these discussions. Additionally, we can identify regions where Islamic finance is the most popular, providing insights for policymakers and financial institutions in these regions. Overall, this study provides a comprehensive analysis of the sentiment surrounding Islamic finance on social media, providing valuable insights for policymakers, financial institutions, and researchers.

In the rest of our paper, we first provide a literature review on the perception of Islamic finance and sentiment analysis applications in finance. We then describe our methodology, including the data collection and sentiment analysis techniques. Next, we present the results and discuss their implications. Finally, we conclude with a summary of our findings and offer recommendations for future research.

Islamic finance, while having historical roots in the Muslim world during the Middle Ages, where it played a pivotal role in fostering trade and business activities with the development of credit, is a concept that is relatively new, with the term "Islamic financial system" emerging only in the mid-1980s [7]. Islamic finance is a financial system based on Islamic principles and Sharia law, aiming to support economic and financial activities while adhering to Islamic Law.

The key distinctions between Islamic finance and conventional finance is the absence of interest, or "riba." in Islamic finance [8], Risk Sharing, the risk is shared between the parties involved in a transaction, whereas in conventional finance it is the borrower who bears most of the risk [9], Asset-backed financing, Islamic finance requires that transactions to be backed by tangible assets, while conventional finance often relies on intangible assets [10], and the ethical considerations, Islamic finance prohibits investing in industries that are considered unethical, such as gambling, alcohol, and tobacco, while conventional finance does not have such restrictions [11].

With our understanding of the principles of Islamic finance and how it differs from conventional finance, let's now focus on the public perception of Islamic finance and the sentiment analysis and its financial applications in the next subsections.

2.1 Review of public perception towards Islamic finance

Public perception refers to the collective awareness, beliefs, attitudes, and opinions held by a group of individuals, often within a society or community, about a particular subject, issue, person, organization, product, or concept. It is the way people perceive and interpret information, events, or entities. It can be influenced by a variety of factors, including personal experience, cultural background, media coverage, and education [12].

In academic and practical contexts, understanding public perception is crucial, as it can influence various aspects of society, including decision-making, public policy, consumer behavior, and the reputation of organizations or individuals. Researchers, marketers, and policymakers often study and analyze public perception to gain insights into how to effectively communicate, engage, or address issues within a given community or society.

Since the Islamic finance has gained increasing popularity in recent decades, expanding its presence in many countries, including the post-Soviet space [13, 14]. Public and business perceptions of Islamic finance have been widely studied to understand the demand for this type of financial service. Several studies [15-19] have explored the perception of Islamic finance in the MENA region. These studies show that the general population has a positive perception of Islamic finance and its principles. In particular, respondents appreciated the focus on ethics, fairness, and justice in Islamic finance, which they believed was in line with the values and principles of their religion. For example, Al Balushi et al. [19] investigates the awareness, willingness, and perceptions of small and medium enterprises (SME) owner-managers in Muscat, Oman towards Islamic financing instruments. The study used a mixed-method approach with a questionnaire survey and face-to-face discussions with SME owner-managers. The findings show that SME owner managers have positive perceptions of Islamic financing, but their willingness to adopt it is motivated by factors other than finance. Khursheed et al. [17] examined the factors affecting customer perceptions of adopting Islamic banking and finance. The data were collected through a survey of university students and bank employees in three Gulf Cooperation Council countries (the UAE, Kuwait, and Saudi Arabia). The results, analyzed using regression modeling, indicate that all independent variables - understanding, awareness, religious inspiration, customer innovativeness, and perceived risk - significantly influence customers' perceptions of Islamic financing.

The public's perception of Islamic finance in Europe and America has been the focus of several studies [20-24]. The results indicate that, while the majority of respondents hold a positive view of Islamic finance and its principles, they lack a deep understanding of the system. For example, Aldarabseh [25] examined the popularity of Islamic finance in the USA from 2014 to 2019 using Google Trends. The results showed a decrease in search volumes for "Islamic finance" and "Islamic bank" which suggests a decline in popularity.

Studies conducted in Asia [26-30] have explored the perception of Muslim and non-Muslim customers towards Islamic banking products and services. These studies show that Islamic banking services are gaining popularity among non-Muslims.

In Africa, Saiti et al. [31] investigated the factors influencing the choice of Islamic banking among non-Muslim customers in Nigeria. The growth of Islamic banking has slowed down due to criticism and sentiments from some non-Muslim segments of society, despite non-Muslims making up a significant customer base. In the other hand [32] examined the level of perception of Muslim account holders in a conventional bank toward Islamic banking products and determined the relationship between their perception and decision to use Islamic banking services. In Ghana, Mbawuni and Nimako [33] conducted a study to examine the perceptions of both Muslim and non-Muslim consumers regarding the implementation of Islamic banking while Saini Yvonne et al [34] explores the level of consumer awareness and utilization of Islamic banking products in South Africa., the research analyzed the factors that influence the decision between Islamic and conventional banks. The results show that while Muslim customers are aware of Islamic banking options, their usage remains low. The key factors influencing their banking choices include efficiency, lower bank fees, accessibility of ATMs, and a wide-branch network, rather than religious adherence to Islamic principles.

In conclusion, the literature review highlights that the public perception of Islamic finance varies across regions and that there is a general lack of understanding of the principles and concepts of Islamic finance, indicating a need for better education and awareness programs.

2.2 Sentiment analysis and its applications in finance

Sentiment analysis is a technique that utilizes Natural Language Processing to identify, extract, and analyze sentiments expressed in text and categorize them into positive, negative, or neutral sentiments [35]. The Sentiment Analysis, which is an interdisciplinary field, encompasses the integration of Natural Language Processing, Computational Linguistics, and text analysis techniques for the purpose of examining individuals' perceptions [36]. This is achieved through the identification and examination of subjective data from various sources, such as the web and social media platforms [37]. The objective of Sentiment Analysis is to gain an understanding of the public's sentiments or attitudes towards specific individuals, products, or concepts by determining the contextual polarity of information. As the field continues to evolve, sentiment analysis is becoming increasingly sophisticated, incorporating machine learning and deep learning methods to enhance accuracy and address the complexities of language, context, and cultural nuances in sentiment interpretation [36].

For the past ten years, researchers have been engaged in the study of sentiment analysis, which has seen an increase in the number of papers published since 2002 [38]. The Sentiment analysis is classed into three categories: sentence-level analysis, document-level analysis, and feature-level analysis. The objective is to classify opinions from sentences, documents, or features as positive or negative sentiments [38]. Two main techniques for sentiment analysis have been identified: machine learning and lexicon-based methods. The machine learning approach uses algorithms to identify sentiment in data [39], whereas the lexicon-based approach involves counting the number of positive and negative words associated with the data [40, 41].

Social Media is one of the notable emerging technology trends that drive the digital transformation [42] and with the rise of social media, access to information on public opinion has become plentiful. Social media platforms have become ideal venues for individuals to express their emotions and thoughts on a wide range of topics, which, in turn, can greatly influence overall public opinion. In particular, Twitter, a microblogging service, has received considerable interest from researchers because of its ability to provide real-time updates and allow users to interact with each other's thoughts and opinions [43]. Different studies have used Twitter data to analyze the relationship between Twitter sentiment and stock market trends. For example, Oliveira et al. [44] analyzed all tweets related to US stocks and used the Stanford CoreNLP tool to process the text. The study found a strong correlation between Twitter sentiments and popular survey sentiment indicators. Pagolu et al. [45] analyzed 250,000 tweets about Microsoft and found that sentiment analysis had an accuracy of 70% for stock movement prediction. Batra and Daudpota [46] analyzed 300,000 tweets about Apple from StockTwits between 2010-2017 and used an SVM model for sentiment analysis. The preprocessing of tweets included tokenization and the removal of stop words and Twitter symbols.

In the banking and financial sector there is several studies applying sentiment analysis techniques to examine the level of perception towards banking products and services [47-54]. For example, Fernandez et al. [55] employed sentiment analysis techniques to create a sentiment index based on tweets in Spanish, with the aim of capturing the perception of risk in Mexico's financial system as reflected on Twitter. Lappeman et al. [56] performed a sentiment analysis on over 1.7 million social media posts in South Africa to understand the effect of online negative word-of-mouth (nWOM) firestorms in the retail banking sector. The sentiment analysis utilized both natural language processing (NLP) and human validation techniques to measure changes in social media sentiment during firestorms, which included each of South Africa's major retail banks over a twelve-month period. Ghobakhloo and Ghobakhloo [57] conducted a study aimed at improving customer retention and identifying customer needs through sentiment analysis. The goal was to design a recommender system that provides personalized services based on customer satisfaction, sentiment, and experience. The proposed method uses opinions and experiences gathered from tweets related to banking services to understand customer sentiment orientation. The study utilized correlation scores, cosine similarity, and reliability to quantify customer sentiment and employed suitable classification methods, opinion mining techniques, and proper validation approaches to provide personalized banking services.

The perception of Islamic finance and banking has been the subject of numerous academic and research studies. However, despite the abundance of literature in the field, there has been limited investigation into the perception of Islamic finance on social media platforms, such as Twitter. Sentiment analysis has been widely used in the banking sector to study customer opinions and perceptions, but there is a lack of research specifically focused on the perception of Islamic finance on Twitter. This study aims to fill this gap by being the first to investigate the perception of Islamic finance on Twitter using sentiment analysis techniques.

In this paper, we have based on the domain of sentiment analysis in order to analyze the tweets related Islamic finance during the period from 2007 to 2022. The collected tweets were classified them into classes such as positive, negative, or neutral. The main objective was to analyze the perceptions of Islamic finance from the collected tweets.

To do this, there are some steps to follow: data collection, data cleaning, and data analysis using an approach of classification.

3.1 Data collection

For data collection, we used Snscrape, a scraping tool for social networking services (SNS). It scrapes items such as users, user profiles, hashtags, searches, threads, and list of posts and returns the discovered items without using Twitter’s API. The keywords used for data collection in this study are based on four sources [58-61]. These sources provide a comprehensive list of technical terms and concepts used in Islamic finance and banking, which were used as keywords for collecting tweets on Twitter using Snscrape. Figure 1 shows the different steps used to construct the dataset.

Figure 1. Steps for constructing the dataset

As shown in Figure 1, after applying the Snscrape tool, we retrieved tweets related to our work. Each collected tweet had four features:

• Tweet ID: A unique value that every tweet published on Twitter has.

• Datetime: The date and time at which the tweet was published.

• Username: Tweet holder.

• Location: The location of the user.

• Text: Textual content of tweets.

3.2 Text preprocessing

Data published in social networks, especially on Twitter, can contain irrelevant information that negatively affects the process of classification (sentiment analysis). To prepare the collected tweets for the analysis and decrease the classification error, we applied a number of text preprocessing methods to clean the tweets.

• Removing the Hashtags.

• Removing web links.

• Removing special characters.

• Substitute the multiple spaces with single spaces.

• Removing all the single characters.

• Removing the twitter handlers.

• Removing numbers.

• Remove characters that have a length less than 2.

• Tokenization: Each tweet was split into individual words.

• Removing stop words: Deleting any word that does not emphasize any emotions, such as the preposition (are, is, am) and the articles (a, an, the).

• Stemming and lemmatization: Reduce inflectional forms and sometimes derivationally related forms of a word into a common base form. We used this preprocessing method because its use has shown very positive results in the classification of social network data [62].

3.3 Text analysis

After preprocessing the tweets related to Islamic finance, we performed text analysis using the pre-trained Twitter-roBERTa-base model. which is trained on tweets' text, has shown impressive results [63]. Given that our project is Twitter-centric, we opted for this model. Selecting a model that has been fine-tuned on similar data or has a proven ability to handle short, informal text is advantageous. Furthermore, it's crucial to choose a model with a strong track record in sentiment analysis tasks, as evidenced by the articles referenced [64, 65]. Additionally, the availability of pre-trained models and resources for fine-tuning is a key consideration. Certain models offer publicly accessible pre-trained checkpoints, and this is indeed the case with the Twitter-roBERTa-base model.

The model was specifically trained on approximately 124 million English tweets from January 2018 to December 2021. It has been fine-tuned for sentiment analysis using the TweetEval benchmark (Sentiment analysis tasks in TweetEval involve classifying tweets into sentiment categories like positive, negative, or neutral.) Barbieri et al. [66] making it an appropriate choice for classifying tweets related to Islamic finance into positive, negative, or neutral sentiment categories.

The findings of the analysis were examined in light of the research questions posed in the introduction.

4.1 Islamic finance-related tweets throughout the global population

One of the most typical analytics for text-based datasets is an illustrated word cloud that displays the most commonly used terms. It graphically displays the most popular terms and provides a simple method for summarizing the tweet content. Figure 2 shows the word cloud of tweets from the Islamic finance database.

Figure 2. Word cloud of tweets about Islamic finance

The larger the word inside the word cloud, the more frequently it is used. As shown in Figure. 2, 'Interest free ' is the most-used term in tweets, followed by 'Profit sharing,’ 'Risk mitigation,’ ‘Free loan’ and 'Islamic banking.’ They are the most used words related to Islamic finance on Twitter This is not surprising, as all three terms are the key features of Islamic banking. Profit sharing is a financing instrument unique to Islamic banking that involves sharing risks between the lender and customer [67-69]. Risk mitigation is an important part of risk management in Islamic finance literature [70]. Interest-free it is a central tenet of Islamic finance. One of the fundamental principles of Islamic finance is the prohibition of interest (riba), which is considered to be unjust and exploitative [71-74]. Since the 1960s, there has been much debate among modern Muslims regarding the ban on riba (interest) in Islam [75].

4.2 Geolocation of main populations involved in Islamic finance tweeting throughout the world

The location of the users involved in tweets on Islamic finance is a crucial piece of information obtained using the Snscape library. It should be noted that this analysis is only available to users who provide their locations. Consequently, it did not reflect the entire extracted dataset stated previously.

Figure 3 displays the geographical locations on a map where these tweets were posted as well as the frequency or density of tweets in different regions. This type of representation can provide insights into the spread and popularity of Islamic finance as a topic of discussion on social media as well as highlight areas where it is more or less prevalent.

The spread of tweets is evident in several key regions, including the Gulf Cooperation Council (GCC) countries, Southeast Asia, the United Kingdom, and other European countries with large Muslim populations, the United States, and Canada.

In the GCC region, countries such as Saudi Arabia, the United Arab Emirates, and Qatar are highly active in tweeting about Islamic finance, highlighting their strong involvement and interest in the field [76, 77]. Additionally, the high density of tweets in Southeast Asia, particularly in Malaysia and Indonesia, suggests that Islamic finance is rapidly gaining popularity in this region [78, 79].

The presence of tweets in the United Kingdom and other European countries with large Muslim populations highlights the relevance of Islamic finance in these communities [22, 24, 80]. Similarly, the United States and Canada also showed significant engagement in the topic, indicating a growing interest in the field in North America [81].

Islamic finance is a growing industry in West Africa, especially Nigeria. This can be attributed to the increasing demand for Shariah-compliant financial products and services in the region [82-84].

Overall, this map provides valuable insights into the spread and popularity of Islamic finance on social media platforms. It serves as a useful tool for monitoring trends and patterns of discussion and for identifying areas where further research and outreach efforts could be beneficial.

The United States, which accounts for the majority of tweets overall (19.83%), followed by Malaysia (19.56%), and India (9.62%), according to Figure. 4. This finding suggests that Islamic financing is not just practiced in Muslim-majority nations. Five of the top ten nations were non-Muslims (the United States, India, the United Kingdom, Canada, and Nigeria). Although a greater number of tweets about Islamic finance originated from non-Muslim nations, there is no evidence that the tweets were sent by Muslims [31]. This may be because these countries have more Twitter users than Muslim countries do. Furthermore, there are many Muslims in these five nations, notably in the United Kingdom [85].

Figure 3. Geographical distribution of tweets on Islamic finance

Figure 4. The top ten countries with the highest number of tweets

4.3 Sentiment analysis on Islamic finance: Examining its sentiment trends

Figure 5 presents a circular representation of the sentiment distribution in our tweet dataset. The chart was divided into proportional slices, each representing a sentiment category: positive, neutral, and negative. The result of 57% of tweets being neutral, 17.9% positive, and 24.8% negative suggests that there is a mixture of opinions and perspectives on Islamic finance among social media users. Many tweets related to Islamic finance may contain factual information, updates or professional discussions, which often do not evoke strong positive or negative emotions. Therefore, these tweets are more likely to be classified as neutral in sentiment analysis. It is also a topic of interest to people who want to learn more about it. In this case, the content shared on Twitter may be more informative and educational, resulting in a higher proportion of neutral tweets. However, neutral tweets may indicate a lack of strong opinions or limited engagement with the topic, while positive and negative tweets may indicate a more polarized view. A higher proportion of negative tweets may indicate concerns or criticisms of the topic, whereas positive tweets may reflect support and interest in Islamic finance. The following are some examples of negative tweets.

“Modern systems of (so-called) Islamic finance operating in such an environment usually simply hide the interest or call it by a different name.”

“It's one thing if we can't control ourself but to deal with riba.’ But it's totally another level of stupidity to ourself to said all this Islamic Finance is not riba’.”

“Without intrest gving or taking money, just to respect a particular religion wl be harmful for a dvloping economy like India #IslamicBanking”

Examples of positive tweets are as follows:

“In my tweet pleeing for Muslims being welcome in #EU, I welcome Islamic Banking too. #ethics #GPI “

“Follow the rules of Islamic economics and you will flourish”

“Fortunately, #IslamicBanking appears to present the perfect model for poverty eradication that the west is far from!”

Figure 5. Sentiment distribution

Figure 6 shows the trend of Islamic finance tweets per month for the period from 2007 to 2022, while Figure 7 shows the Sentiment Distribution per year. It’s clear that in the first three years there was few tweets about Islamic finance, the scarcity of tweets regarding Islamic finance in the initial three years can be attributed to the limited number of Twitter users during that period [86]. We also observe that tweets related to Islamic finance started after 2008 because, after the global financial crisis, Islamic finance emerged as a viable alternative system for conducting financial transactions. This system is based on mutual risk-sharing principles, which serve to reduce systemic risk and promote social equality by uplifting the less privileged segment of society [87].

From Figures 6 and 7, we can see that negative tweets started to be more than positive ones from 2016, and the internal challenges facing the Islamic finance industry could be a possible explanation for the increase in negative tweets from 2016. Abozaid [88] cited deficiencies in Shariah governance and product development methodology as internal challenges that could affect the credibility of Islamic finance and lead to loss of confidence in the industry. If these challenges remain unaddressed, Abozaid [88] suggests that people may lose confidence in Islamic finance if these challenges remain unaddressed.

Figure 6. Monthly sentiment trend

Figure 7. Sentiment distribution per Year

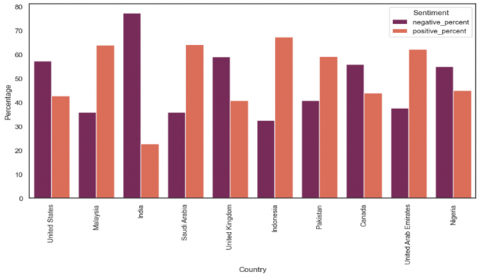

Figure 8. Sentiment analysis of top ten countries with the highest number of tweets

In addition, the Figure 8 displays the sentiment distribution of the top ten countries with the highest number of tweets related to Islamic finance. It highlights the balance of positive and negative sentiments in these countries.

This illustrates a significant divergence in public sentiment towards Islamic finance. Muslim-majority countries, such as Malaysia, Saudi Arabia, Indonesia, Pakistan, and the United Arab Emirates, exhibit a predominantly positive sentiment except for Nigeria, in contrast, non-Muslim-majority countries, including the United States, India, the United Kingdom, Canada, and lean more negatively. These findings highlight the impact of cultural and demographic factors on perceptions, underlining the need for targeted strategies to promote Islamic finance acceptance and understanding in diverse global contexts.

This study analyzes the perception of Islamic finance on Twitter between 2007 and 2022, based on sentiment analysis. We collected tweets using the SnScrape tool and performed data preprocessing to clean the data before analysis. We classified tweets into positive, negative, or neutral sentiments using the Twitter-roBERTa-base model, and found that interest-free, profit-sharing, and risk mitigation were the most frequently mentioned terms related to Islamic finance. We also found that Islamic finance is a popular topic of discussion in GCC countries, Southeast Asia, the United Kingdom, and other European countries with large Muslim populations, the United States, and Canada. In addition, our analysis reveals that Muslim-majority countries generally hold a more positive perception of Islamic finance compared to non-Muslim-majority countries, signifying a notable cultural and demographic influence on public sentiment.

This study has several implications for the Islamic finance industry as it provides insights into public perceptions and opinions about Islamic finance. The findings suggest that interest-free, profit-sharing, and risk mitigation are important factors in Islamic finance and that Islamic finance is gaining popularity in certain regions of the world. These insights can be used by industry professionals to better understand consumers’ needs and preferences as well as to develop marketing strategies and outreach initiatives.

Overall, this study demonstrates the value of social media analysis in understanding public perceptions and opinions about financial products and services and highlights the potential of sentiment analysis as a powerful tool for analyzing large-scale datasets.

Future research could use sentiment analysis of Islamic finance tweets to forecast Islamic index prices and investigate the impact of sentiment on Twitter on the growth of the Islamic finance industry. This could provide valuable insights for investors and industry professionals and contribute to a better understanding of the relationship between social media sentiment and financial markets in the Islamic finance industry.

[1] Statista, ‘Twitter - Statistics & Facts’, 2023. Accessed on Feb. 18, 2023, https://www.statista.com/statistics/303681/twitter-users-worldwide/.

[2] Zarina Abdul Jabar, Z., Wook, M., Zakaria, O., Ramli, S., Afiza Mat Razali, N. (2022). Establishment of big data analytics application model for malaysian public sector: an expert validation. Edpacs, 65(4): 1-20. https://doi.org/10.1080/07366981.2021.1958736

[3] Kharde, V., Sonawane, P. (2016). Sentiment analysis of twitter data: A survey of techniques. arXiv preprint arXiv:1601.06971. https://arxiv.org/abs/1601.06971

[4] Qi, Y., Shabrina, Z. (2023). Sentiment analysis using Twitter data: a comparative application of lexicon-and machine-learning-based approach. Social Network Analysis and Mining, 13(1): 31. https://doi.org/10.1007/s13278-023-01030-x

[5] Wang, Y., Guo, J., Yuan, C., Li, B. (2022). Sentiment analysis of twitter data. Applied Sciences, 12(22). https://doi.org/10.3390/app122211775

[6] Islamic Financial Services Board. (2022). Islamic financial services industry stability report.

[7] Iqbal, Z. (1997). Islamic financial systems. Finance and Development, 34: 42-45.

[8] Khan, W.M. (1989). Towards an interest-free Islamic economic system. Journal of King Abdulaziz University: Islamic Economics, 1. https://papers.ssrn.com/abstract=3141088

[9] Islahi, A.A. (2018). Risk-sharing in finance: The Islamic finance alternative. In Risk-Sharing in Finance: The Islamic Finance Alternative: Islahi, Abdul Azim. [Sl]: SSRN.

[10] Farooq, M.O. (2009). Global financial crisis and the link between the monetary and real sector: Moving beyond the asset-backed Islamic finance. In Proceeding of the 20th Annual Islamic Banking Seminar.

[11] El Qorchi, M. (2005). Islamic finance gears up. Finance and Development, 42(4): 46.

[12] de França Doria, M. (2010). Factors influencing public perception of drinking water quality. Water policy, 12(1): 1-19. https://doi.org/10.2166/wp.2009.051

[13] Kalimullina, M. (2020). Islamic finance in Russia: A market review and the legal environment. Global Finance Journal, 46: 100534. https://doi.org/10.1016/j.gfj.2020.100534

[14] Nagimova, A.Z. (2022). Islamic finance in the eyes of businesses and population of the CIS countries. Voprosy Economiki, (6): 69–90. https://doi.org/10.32609/0042-8736-2022-6-69-90

[15] Hossain, M., Leo, S. (2009). Customer perception on service quality in retail banking in Middle East: The case of Qatar. International Journal of Islamic and Middle Eastern Finance and Management, 2(4): 338-350. https://doi.org/10.1108/17538390911006386

[16] Khmous, D.F., Besim, M. (2020). Impact of Islamic banking share on financial inclusion: Evidence from MENA. International Journal of Islamic and Middle Eastern Finance and Management, 13(4): 655-673. https://doi.org/10.1108/IMEFM-07-2019-0279

[17] Khursheed, A., Fatima, M., Mustafa, F. (2021). Customers’ perceptions toward Islamic banking in the gulf region. Turkish Journal of Islamic Economics, 8(1): 111–135. https://doi.org/10.26414/A105

[18] Muhammad, A.M., Basha, M.B., AlHafidh, G. (2020). UAE Islamic banking promotional strategies: An empirical review. Journal of Islamic Marketing, 11(2): 405-422. https://doi.org/10.1108/JIMA-10-2018-0205

[19] Al Balushi, Y., Locke, S., Boulanouar, Z. (2019). Omani SME perceptions towards Islamic financing systems. Qualitative Research in Financial Markets, 11(4): 369-386. https://doi.org/10.1108/QRFM-06-2018-0078

[20] Belouafi, A., Chachi, A. (2014). Islamic finance in the United Kingdom: Factors behind its development and growth. Islamic Economic Studies, 130(1155): 1-42. https://doi.org/10.12816/0004130

[21] Ernawati, E., Asri, M. (2020). Knowledge and awareness of Islamic financial in Europe and America countries. Iqtishadia, 13(1): 23-37. https://doi.org/10.21043/iqtishadia.v13i1.7207

[22] Kaakeh, A., Hassan, M.K., van Hemmen Almazor, S.F. (2018). Attitude of Muslim minority in Spain towards Islamic finance. International Journal of Islamic and Middle Eastern Finance and Management, 11(2): 213-230. https://doi.org/10.1108/IMEFM-11-2017-0306

[23] Paton Schmidt, A. (2019). The impact of cognitive style, consumer demographics and cultural values on the acceptance of Islamic insurance products among American consumers. International Journal of Bank Marketing, 37(2): 492-506. https://doi.org/10.1108/IJBM-02-2018-0033

[24] Riaz, U., Burton, B., Monk, L. (2017). Perceptions on the accessibility of Islamic banking in the UK—Challenges, opportunities and divergence in opinion. In Accounting Forum, 41(4): 353-374. https://doi.org/10.1016/j.accfor.2017.10.002

[25] Aldarabseh, W.M. (2019). How popular is Islamic finance in the USA? Findings from google trends. International Journal of Finance & Banking Studies (2147-4486), 8(3): 58-65. https://doi.org/10.20525/ijfbs.v8i3.490

[26] Abdul Razak, D. (2011). Consumers' perception on Islamic home financing: Empirical evidences on Bai Bithaman Ajil (BBA) and diminishing partnership (DP) modes of financing in Malaysia. Journal of Islamic Marketing, 2(2): 165-176. https://doi.org/10.1108/17590831111139875

[27] Ehsan Wahla, A., Hasan, H., Bhatti, M.I. (2018). Measures of customers’ perception of car Ijarah financing. Journal of Islamic Accounting and Business Research, 9(1): 2-16. https://doi.org/10.1108/JIABR-10-2015-0051

[28] Riaz, U., Khan, M., Khan, N. (2017). An Islamic banking perspective on consumers’ perception in Pakistan. Qualitative Research in Financial Markets, 9(4): 337-358. https://doi.org/10.1108/QRFM-03-2017-0020

[29] Shaikh, I.M., Shaikh, F.M., Noordin, K. (2022). Predicting customers’ acceptance towards Islamic home financing using DTPB theory. Journal of Islamic Marketing, 13(11): 2331-2346. https://doi.org/10.1108/JIMA-12-2020-0372

[30] Wan Ahmad, W.M., Hisham Hanifa, M., Hyo, K.C. (2019). Are non-Muslims willing to patronize Islamic financial services?. Journal of Islamic Marketing, 10(3): 743-758. https://doi.org/10.1108/JIMA-01-2017-0007

[31] Saiti, B., Ardo, A.A., Yumusak, I.G. (2022). Why non-Muslims subscribe to Islamic banking?. Qualitative Research in Financial Markets, 14(2): 247-269. https://doi.org/10.1108/QRFM-01-2018-0005

[32] Jinjiri Ringim, K. (2014). Perception of Nigerian Muslim account holders in conventional banks toward Islamic banking products. International Journal of Islamic and Middle Eastern Finance and Management, 7(3): 288-305. https://doi.org/10.1108/IMEFM-04-2013-0045

[33] Mbawuni, J., Nimako, S.G. (2018). Muslim and non-Muslim consumers’ perception towards introduction of Islamic banking in Ghana. Journal of Islamic Accounting and Business Research, 9(3): 353-377. https://doi.org/10.1108/JIABR-04-2016-0050

[34] Saini Y., Bick Geoff, L.A. (2011). Consumer awareness and usage of Islamic banking products in South Africa. South African Journal of Economic and Management Sciences, 14(3): 298-313. https://doi.org/10.10520/EJC31353

[35] Agarwal, B., Mittal, N., Bansal, P., Garg, S. (2015). Sentiment analysis using common-sense and context information. Computational Intelligence and Neuroscience, 2015: 30-30. https://doi.org/10.1155/2015/715730

[36] Khalil, E.A.H., El Houby, E.M., Mohamed, H.K. (2020). Deep learning approach in sentiment analysis: A review. In 2020 15th International Conference on Computer Engineering and Systems (ICCES), Cairo, Egypt, pp. 1-10. https://doi.org/10.1109/ICCES51560.2020.9334625

[37] Awatramani, P., Daware, R., Chouhan, H., Vaswani, A., Khedkar, S. (2021). Sentiment analysis of mixed-case language using natural language processing. In 2021 Third International Conference on Inventive Research in Computing Applications (ICIRCA), pp. 651-658. https://doi.org/10.1109/ICIRCA51532.2021.9544554

[38] Pang, B., Lee, L., Vaithyanathan, S. (2002). Thumbs up? Sentiment classification using machine learning techniques. arXiv preprint cs/0205070. https://doi.org/10.48550/ARXIV.CS/0205070

[39] AlBadani, B., Shi, R., Dong, J. (2022). A novel machine learning approach for sentiment analysis on Twitter incorporating the universal language model fine-tuning and SVM. Applied System Innovation, 5(1): 13. https://doi.org/10.3390/asi5010013

[40] Khoo, C.S., Johnkhan, S.B. (2018). Lexicon-based sentiment analysis: Comparative evaluation of six sentiment lexicons. Journal of Information Science, 44(4): 491-511. https://doi.org/10.1177/0165551517703514

[41] Shah, P., Swaminarayan, P. (2021). Lexicon-based sentiment analysis on movie review in the Gujarati language. International Journal of Information Technology, Communications and Convergence, 4(1): 63-72. https://doi.org/10.1504/IJITCC.2021.10042767

[42] Tang, D. (2021). What is digital transformation?. Edpacs, 64(1): 9-13. https://doi.org/10.1080/07366981.2020.1847813

[43] Jansen, B.J., Zhang, M., Sobel, K., Chowdury, A. (2009). Twitter power: Tweets as electronic word of mouth. Journal of the American society for information science and technology, 60(11): 2169-2188. https://doi.org/10.1002/asi.21149

[44] Oliveira, N., Cortez, P., Areal, N. (2016). Stock market sentiment lexicon acquisition using microblogging data and statistical measures. Decision Support Systems, 85: 62-73. https://doi.org/10.1016/j.dss.2016.02.013

[45] Pagolu, V.S., Reddy, K. N., Panda, G., Majhi, B. (2016). Sentiment analysis of Twitter data for predicting stock market movements. In 2016 international conference on signal processing, communication, power and embedded system (SCOPES), pp. 1345-1350. https://doi.org/10.1109/SCOPES.2016.7955659

[46] Batra, R., Daudpota, S.M. (2018). Integrating StockTwits with sentiment analysis for better prediction of stock price movement. In 2018 international conference on computing, mathematics and engineering technologies (ICoMET), pp. 1-5. https://doi.org/10.1109/ICOMET.2018.8346382

[47] Agoraki, M.E.K., Aslanidis, N., Kouretas, G.P. (2022). US banks’ lending, financial stability, and text-based sentiment analysis. Journal of Economic Behavior & Organization, 197: 73-90. https://doi.org/10.1016/j.jebo.2022.02.025

[48] Alamsyah, A., Indraswari, A.A. (2017). Social network and sentiment analysis for social customer relationship management in Indonesia banking sector. Advanced Science Letters, 23(4): 3808-3812. https://doi.org/10.1166/asl.2017.9279

[49] Botchway, R.K., Jibril, A.B., Oplatková, Z.K., Chovancová, M. (2020). Deductions from a Sub-Saharan African Bank’s Tweets: A sentiment analysis approach. Cogent Economics & Finance, 8(1): 1776006. https://doi.org/10.1080/23322039.2020.1776006

[50] Chong, D., Li, L., Wu, H., Park, J., Shi, H., Yan, G. (2018). Social media sentiment and bank loan contracting. Journal of Industrial Integration and Management, 3(01): 1850007. https://doi.org/10.1142/S2424862218500070

[51] Elamir, E.A., Mousa, G.A. (2020). Sentiment analysis of banks' annual reports and bank features: LASSO approach. In 2020 International Conference on Decision Aid Sciences and Application (DASA), pp. 42-48. https://doi.org/10.1109/DASA51403.2020.9317075

[52] Hristova, G. (2022). Text analytics for customer satisfaction prediction: A case study in the banking domain. In AIP Conference Proceedings, 2505(1): 100001. https://doi.org/10.1063/5.0100865

[53] Masarifoglu, M., Tigrak, U., Hakyemez, S., Gul, G., Bozan, E., Buyuklu, A.H., Özgür, A. (2021). Sentiment analysis of customer comments in banking using bert-based approaches. In 2021 29th Signal Processing and Communications Applications Conference (SIU), pp. 1-4. https://doi.org/10.1109/SIU53274.2021.9477890

[54] Mittal, D., Agrawal, S.R. (2022). Determining banking service attributes from online reviews: Text mining and sentiment analysis. International Journal of Bank Marketing, 40(3): 558-577. https://doi.org/10.1108/IJBM-08-2021-0380

[55] Fernandez, R., Guizar, B.P., Rho, C. (2021). A sentiment-based risk indicator for the Mexican financial sector. Latin American Journal of Central Banking, 2(3): 100036. https://doi.org/10.1016/j.latcb.2021.100036

[56] Lappeman, J., Clark, R., Evans, J., Sierra-Rubia, L. (2021). The effect of nWOM firestorms on South African retail banking. International Journal of Bank Marketing, 39(3): 455-477. https://doi.org/10.1108/IJBM-07-2020-0403

[57] Ghobakhloo, M., Ghobakhloo, M. (2022). Design of a personalized recommender system using sentiment analysis in social media (case study: banking system). Social Network Analysis and Mining, 12(1): 84. https://doi.org/10.1007/s13278-022-00900-0

[58] Ayub, M. (2012). A comprehensive glossary of terms in Islamic commercial law–business, banking and finance. Journal of Islamic Business and Management, 2(2): 141–182. https://doi.org/10.12816/0004983

[59] Glossary of Islamic Finance. (2013). In Investing in Islamic Funds, John Wiley & Sons, Ltd, pp. 215–233. https://doi.org/10.1002/9781118670460.oth2

[60] Keltoum, B., Nabila, N., Djamel, M. (2018). Towards a reference ontology in islamic finance and banking. In 2018 International Conference on Information and Communication Technology for the Muslim World (ICT4M), pp. 74-79. https://doi.org/10.1109/ICT4M.2018.00023

[61] Khan, M.A. (2003). Islamic economics and finance a glossary.

[62] Madani, Y., Erritali, M., Bengourram, J. (2019). Sentiment analysis using semantic similarity and Hadoop MapReduce. Knowledge and Information Systems, 59: 413-436. https://doi.org/10.1007/s10115-018-1212-z

[63] Loureiro, D., Barbieri, F., Neves, L., Anke, L.E., Camacho-Collados, J. (2022). Timelms: Diachronic language models from twitter. arXiv preprint arXiv:2202.03829. https://arxiv.org/abs/2202.03829

[64] Bonifazi, G., Cauteruccio, F., Corradini, E., Marchetti, M., Sciarretta, L., Ursino, D., Virgili, L. (2022). A space-time framework for sentiment scope analysis in social media. Big Data and Cognitive Computing, 6(4): 130. https://doi.org/10.3390/bdcc6040130

[65] Liu, Y., Ott, M., Goyal, N., Du, J., Joshi, M., Chen, D., Stoyanov, V. (2019). Roberta: A robustly optimized bert pretraining approach. arXiv preprint arXiv:1907.11692. https://arxiv.org/abs/1907.11692

[66] Barbieri, F., Camacho-Collados, J., Neves, L., Espinosa-Anke, L. (2020). Tweeteval: Unified benchmark and comparative evaluation for tweet classification. arXiv preprint arXiv:2010.12421. https://arxiv.org/abs/2010.12421

[67] Farihana, S., Rahman, M.S. (2021). Can profit and loss sharing (PLS) financing instruments reduce the credit risk of Islamic banks?. Empirical Economics, 61(3): 1397-1414. https://doi.org/10.1007/s00181-020-01912-5

[68] Rammal, H.G., Zurbruegg, R. (2007). Awareness of Islamic banking products among Muslims: The case of Australia. Journal of Financial Services Marketing, 12: 65-74. https://doi.org/10.1057/palgrave.fsm.4760060

[69] Sutrisno, S., Widarjono, A. (2022). Is profit–loss-sharing financing matter for Islamic Bank’s Profitability? The Indonesian Case. Risks, 10(11): 207. https://doi.org/10.3390/risks10110207

[70] Al Rahahleh, N., Ishaq Bhatti, M., Najuna Misman, F. (2019). Developments in risk management in Islamic finance: A review. Journal of Risk and Financial Management, 12(1): 37. https://doi.org/10.3390/jrfm12010037

[71] Alam, N., Gupta, L., Shanmugam, B., Alam, N., Gupta, L., Shanmugam, B. (2017). Prohibition of Riba and Gharar in Islamic banking. Islamic Finance: A Practical Perspective, 35-53. https://doi.org/10.1007/978-3-319-66559-7_3

[72] Balkaran, L. (2013). The importance of multiculturalism on auditing. EDPACS, 47(6): 15-27. https://doi.org/10.1080/07366981.2013.795770

[73] Billah, M.M. (2014). The prohibition of Ribā and the use of Ḥiyāl by Islamic banks to overcome the prohibition. Arab Law Quarterly, 28(4): 392-408. https://doi.org/10.1163/15730255-12341288

[74] Mills, P.S., Presley, J.R. (1999). The Islamic critique of interest. in Islamic Finance, London: Palgrave Macmillan UK, pp. 7–14. https://doi.org/10.1057/9780230288478_2

[75] Saeed, A. (1995). The moral context of the prohibition of Ribā in Islam revisited. The American Journal of Islamic Social Sciences, 496-517. https://doi.org/10.35632/ajis.v12i4.2368

[76] Abid, I., Goaied, M., Ben Ammar, M. (2019). Conventional and Islamic banks’ performance in the Gulf cooperation council countries; efficiency and determinants. Journal of Quantitative Economics, 17: 623-665. https://doi.org/10.1007/s40953-018-0139-2

[77] Qanas, J., Sawyer, M. (2022). Financialisation in the Gulf States. Review of Political Economy, 1-18. https://doi.org/10.1080/09538259.2022.2099669

[78] Chowdhury, M.A.M., Haron, R. (2021). The efficiency of Islamic banks in the southeast Asia (SEA) region. Future Business Journal, 7: 1-16. https://doi.org/10.1186/s43093-021-00062-z

[79] Iqbal, M., Kusuma, H., Sunaryati, S. (2022). Vulnerability of Islamic banking in ASEAN. Islamic Economic Studies, 29(2): 159-168. https://doi.org/10.1108/IES-10-2021-0040

[80] Riaz, U., Burton, B., Monk, L. (2017). Perceptions on Islamic banking in the UK—Potentialities for empowerment, challenges and the role of scholars. Critical Perspectives on Accounting, 47: 39-60. https://doi.org/10.1016/j.cpa.2016.11.002

[81] Alharbi, A. (2016). Development of Islamic finance in Europe and North America: Opportunities and challenges. International Journal of Islamic Economics and Finance Studies, 2(3): 109-136.

[82] Clifford Obiyo, O. (2008). Islamic financing/banking in the Nigerian economy: Is it workable? A review of related issues and prospects. International Journal of Islamic and Middle Eastern Finance and Management, 1(3), 227-234. https://doi.org/10.1108/17538390810901159

[83] Faye, I., Triki, T., Kangoye, T. (2013). The Islamic finance promises: Evidence from Africa. Review of Development Finance, 3(3): 136-151. https://doi.org/10.1016/j.rdf.2013.08.003

[84] Yakubu, S.M., Naim, A.M., Yusuff, N. (2021). Dataset on the acceptance of islamic microfinance in Kano State, Nigeria. Data in Brief, 36: 107108. https://doi.org/10.1016/j.dib.2021.107108

[85] Saniotis, A. (2012). Muslims and ecology: Fostering Islamic environmental ethics. Contemporary Islam, 6(2): 155-171. https://doi.org/10.1007/s11562-011-0173-8

[86] Chen, G.M. (2011). Tweet this: A uses and gratifications perspective on how active Twitter use gratifies a need to connect with others. Computers in Human Behavior, 27(2): 755-762. https://doi.org/10.1016/j.chb.2010.10.023

[87] Hassan, M.K., Khan, A., Paltrinieri, A. (2021). Islamic finance: A literature review. Islamic Finance and Sustainable Development: A Sustainable Economic Framework for Muslim and Non-Muslim Countries, 77-106. https://doi.org/10.1007/978-3-030-76016-8_5

[88] Abozaid, A. (2016). The internal challenges facing Islamic finance industry. International Journal of Islamic and Middle Eastern Finance and Management, 9(2): 222-235. https://doi.org/10.1108/IMEFM-05-2015-0056