Nor Asyira Fakriah Mohamad Noor Azaidi![]() | Hanani Farhah Harun*

| Hanani Farhah Harun*![]() | Mohd Lazim Abdullah

| Mohd Lazim Abdullah![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study systematically reviews advancements in mathematical models for portfolio optimization, focusing on the integration of non-Gaussian distributions and artificial intelligence (AI) techniques to address evolving market complexities. Employing a systematic literature review (SLR) guided by the Search, Appraisal, Synthesis, and Analysis (SALSA) framework, data were extracted from 61 high- and moderate-quality studies published between 2009 and 2024, identified through comprehensive searches in the Scopus database. The study evaluates trends, challenges, and gaps in the application of mathematical models, emphasizing support vector regression (SVR), mean-variance optimization (MVO), neural networks, and Copulas. Quantitative analysis revealed a growing adoption of non-Gaussian models, particularly SVR, which accounted for 30% of the reviewed studies due to its robust handling of non-linear and non-Gaussian data. These models demonstrated superior performance in optimizing risk-adjusted returns, especially when combined with complementary algorithms such as LASSO. Qualitative synthesis highlighted the integration of AI techniques in sustainability-focused investments, with emerging trends in green finance and environmental, social, and governance (ESG) optimization. However, challenges such as computational inefficiencies, limited empirical validation in emerging markets, and inconsistent ESG metrics were identified as key barriers. The findings emphasize the transformative potential of integrating non-Gaussian models and AI in portfolio optimization, providing insights into their application across diverse financial contexts.

non-Gaussian, AI, SVR, SLR, preferred reporting items for systematic reviews and meta-analyses (PRISMA), SALSA, green finance, ESG

Portfolio optimization stands as a cornerstone of financial strategy, enabling investors to achieve a calculated balance between returns and risks. These approaches incorporate essential factors such as expected returns, risk levels, and correlations between assets [1, 2]. Historically, portfolio optimization has been anchored in Markowitz's Modern Portfolio Theory (MPT) (1952), which established a quantitative framework for maximizing returns at a given level of risk. MPT employs variance as a measure of risk and mean returns as a reward indicator to formulate efficient investment strategies [3-5].

Central to this approach is the principle of diversification, which mitigates the likelihood of significant losses by distributing investments across assets with low or negative correlations [6-9]. These models assume normally distributed asset returns, simplifying the analytical processes involved in risk and return management [2, 7]. However, real-world markets deviate significantly from Gaussian assumptions. Market returns frequently exhibit fat tails, skewness, and asymmetric distributions, leading to underestimation of extreme risks in traditional models [2, 7]. The assumption of normality fails to account for market anomalies such as financial crises, sudden price shocks, and contagion effects, where asset correlations become unstable and tail dependencies intensify. This shortcoming results in models that are ill-equipped to manage tail risks and systemic shocks, limiting their applicability in volatile market conditions. For instance, empirical evidence suggests that extreme events—such as the 2008 global financial crisis and the COVID-19 market collapse—produce return distributions that significantly deviate from the Gaussian framework, demonstrating heightened kurtosis and non-linear dependencies among assets.

A notable example of Gaussian model failure occurred during the 2008 global financial crisis. Traditional Value-at-Risk (VaR) models, which assume normally distributed returns, significantly underestimated the probability of extreme losses, leading to severe miscalculations in risk exposure [10, 11]. Financial institutions relying on these models faced catastrophic failures as their risk management frameworks could not capture the compounding effects of tail risk and systemic contagion [12]. Lehman Brothers and other major banks, for instance, experienced liquidity crises due to these miscalculations, ultimately leading to their collapse.

Similarly, during the COVID-19 pandemic, equity markets experienced abrupt crashes, with indices like the S&P 500 and Dow Jones witnessing rapid declines of over 30% within weeks [13]. Gaussian-based portfolio models failed to anticipate such extreme price movements, resulting in liquidity shortfalls and portfolio misallocations [14]. In contrast, non-Gaussian approaches, incorporating fat-tailed distributions and Copula models, provided more accurate risk estimates and improved downside protection [15]. These models demonstrated superior performance in capturing extreme tail events, reinforcing the necessity of adopting non-Gaussian frameworks in modern portfolio optimization.

Consequently, investors relying solely on MPT-based models may underestimate downside risks and misallocate capital, leading to suboptimal portfolio performance during market stress periods. This inadequacy has driven the evolution of more sophisticated mathematical frameworks that integrate advanced techniques like stochastic modeling, higher-order statistics, and machine learning algorithms to address the non-Gaussian characteristics inherent in real-world financial markets.

Recent trends in portfolio optimization have broadened the scope of mathematical models, integrating advanced statistical techniques, environmental, social, and governance (ESG) factors, and AI. Non-Gaussian models have emerged as transformative tools, addressing the shortcomings of traditional Gaussian-based methods by capturing complex market phenomena like extreme co-movements and dynamic correlations [16, 17]. Moreover, ESG integration underlines a shift toward sustainability-driven investing, emphasizing financial models that align with broader societal goals.

The introduction of AI and machine learning techniques has further revolutionized portfolio optimization. Methods such as support vector regression (SVR), neural networks, and metaheuristic algorithms like genetic algorithms (GA) offer improved adaptability, scalability, and precision in navigating market complexities. For instance, SVR demonstrates superior performance in managing risk-adjusted returns and addressing non-linear dependencies in financial data [18]. These advancements allow for the modeling of non-linear relationships, heavy-tailed distributions, and dynamic correlations between assets, which are often overlooked by classical models.

Given the increasing complexity and volatility characterizing contemporary financial markets, non-Gaussian models have become essential for effective portfolio management. These advanced approaches transcend the limitations of traditional Gaussian-based models by incorporating sophisticated mathematical techniques—such as higher-order co-moments and dynamic correlation structures—to provide a more accurate representation of market dynamics. These models account for real-world market anomalies, such as skewness, fat tails, and extreme dependencies, by leveraging advanced statistical techniques like Copulas, generalized hyperbolic distributions, and higher-order moments. In parallel, AI has emerged as a transformative tool in financial modeling, offering powerful machine learning algorithms such as SVR, deep learning, and ensemble methods to enhance predictive accuracy and risk assessment. The integration of AI-driven approaches with non-Gaussian models in Figure 1 presents a compelling solution for modern portfolio management, enabling investors to construct more resilient, adaptive, and data-driven investment strategies in increasingly volatile and complex financial markets. By integrating these cutting-edge methodologies, non-Gaussian models offer investors comprehensive frameworks for effectively managing risks while optimizing returns in increasingly uncertain environments. So, are non-Gaussian models the future of portfolio optimization?

Figure 1. Balancing advanced techniques for portfolio optimisation

This paper aims to systematically review and synthesize the existing literature on recent advancements in mathematical models for portfolio optimization, focusing on non-Gaussian distributions and AI integration. Through this examination, we will highlight their potential to transform portfolio management practices within volatile and sustainable markets. Utilizing a systematic literature review (SLR) approach, this study will explore key mathematical advancements in the field while identifying emerging trends and research gaps that warrant further investigation.

The remainder of this paper is organized as follows: Section 2 outlines the research methodology used to identify relevant studies within the scope of this review. Section 3 presents findings on current mathematical models for portfolio optimization, with a focus on approaches accommodating non-Gaussian distributions. Section 4 discusses the performance and adaptability of these models across financial markets, highlighting their sensitivity to market conditions and capacity to handle outliers. Finally, Section 5 concludes the paper by summarizing key insights and suggesting directions for future research.

2.1 Advancements in portfolio optimization: From Gaussian to non-Gaussian models

Historically, Gaussian-based models like Mean-Variance Optimization (MVO) have dominated portfolio optimization. These models assume that asset returns follow a normal distribution, allowing risk to be quantified using variance and return to be measured as the mean, variance, and covariance [2, 19]. This assumption simplifies the mathematical formulation of optimal portfolios, making MVO a widely adopted approach in modern finance. The appeal of Gaussian-based models lies in their intuitive risk-return tradeoff, computational efficiency, and applicability in a broad range of investment strategies [9, 20, 21]. However, the assumption of normality often misrepresents the realities of financial markets, where asset returns often exhibit by heavy tails, skewness, and volatility clustering, and extreme dependencies. Gaussian models struggle with "fat tails," where extreme returns are more frequent than normal distributions predict, and assume stable, symmetrical distributions, limiting their efficacy in managing skewed or non-linear relationships [22]. Such limitations are particularly evident during periods of high volatility or market disruptions, where traditional Gaussian-based methods can significantly underestimate risks [23]. The 2008 global financial crisis exposed these shortcomings, as Gaussian-based VaR models failed to anticipate extreme losses, leading to systemic failures [18]. These crises highlight the necessity for more sophisticated risk management frameworks that move beyond normality assumptions.

To address these shortcomings, non-Gaussian models have emerged as a transformative tool in portfolio optimization. Empirical evidence highlights the efficacy of these models in capturing complex market phenomena such as heavy tails, skewness, and extreme co-movements between assets [24]. Unlike their Gaussian counterparts, these models integrate higher-order statistical moments (skewness and kurtosis), Copula theory, and stochastic processes to more accurately capture real-world market behaviors. Multivariate generalized hyperbolic distributions, for example, effectively model tail dependencies and asymmetric risk structures, making them particularly suitable for managing portfolio risk under extreme market conditions [24]. These models incorporate higher-order statistical properties like skewness and kurtosis, providing a more realistic representation of financial market dynamics. For instance, multivariate generalized hyperbolic distributions effectively model tail dependencies and asymmetries, making them indispensable for managing portfolios in extreme market conditions.

Furthermore, empirical evidence demonstrates that the Omega portfolio model, which accounts for non-normal distributions of returns, outperforms MVO in terms of risk-adjusted returns and drawdown minimization, particularly during market crises such as the global financial downturn and COVID-19 pandemic [6, 25]. Similarly, local Gaussian correlation models, which adapt correlation structures dynamically, offer enhanced downside protection in volatile markets [16].

Non-Gaussian approaches are particularly adept at addressing intricate challenges such as market shocks, liquidity constraints, and behavioral biases, providing a robust framework for risk management [26]. Their effectiveness is most evident during market distress, where traditional Gaussian-based models often fail to capture the full extent of financial instability. Despite their advantages, non-Gaussian models present implementation challenges due to their reliance on computationally intensive algorithms and the need for advanced tools to manage high-dimensional data and asymmetric return distributions. Techniques such as global optimization are often employed in these models, to handle the complexities of asymmetric return distributions and high-dimensional data structures [27, 28].

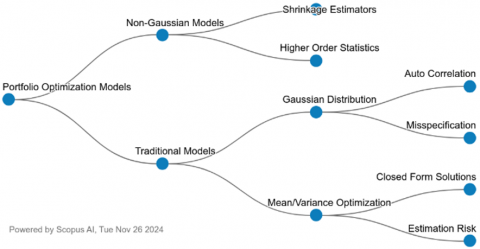

Figure 2. Conceptual summary of portfolio optimization models

One notable advancement in this domain is the Non-Gaussian Component (NGC) portfolio, which utilizes higher-order co-moments of asset returns to enhance the estimation process and optimize asset allocation. Empirical studies reveal that the NGC portfolio consistently outperforms benchmark models, proving its efficacy in constructing robust and efficient portfolios [29]. These findings highlight the growing relevance of non-Gaussian models in modern financial markets, particularly for applications requiring advanced modeling of risk and return dynamics. As illustrated in Figure 2, portfolio optimization has evolved from traditional MVO frameworks to more sophisticated non-Gaussian models that better reflect market realities.

2.2 Risk minimization and return maximization in portfolio optimization

Risk minimization and return maximization are foundational objectives in portfolio optimization, each tailored to distinct investor preferences and risk tolerance levels. Traditional risk minimization models, such as Markowitz's MVO, emphasize variance reduction to enhance portfolio stability. However, these models are limited in their ability to capture the complexities of modern financial markets, particularly during periods of heightened volatility or market anomalies. Contemporary approaches, including those by Harun et al. [17] and Lucey et al. [30], have incorporated advanced tail-risk measures like Conditional Value at Risk (CVaR) and CoVaR to address extreme market events and the irregularities associated with non-Gaussian distributions. These models have proven particularly effective in volatile environments, demonstrating superior capital preservation and downside risk mitigation.

In contrast, return maximization models prioritize higher returns, often at the expense of increased volatility. Momentum investing, for example, exploits return persistence patterns, while alternative assets, such as green cryptocurrencies and ESG-themed funds, offer higher return potential but increased exposure to tail risk, as explored by Chaudhury and Islam et al. [3] and Lim et al. [8]. While these approaches offer potential for significant gains, they frequently rely on Gaussian assumptions, which may fail to adequately capture real-world complexities like fat tails and asymmetric risk profiles. Sustainability-focused frameworks, such as those developed by Abate et al. [31] and Zheng et al. [32], enhance return maximization by incorporating ESG-weighted returns. Recent models [31, 33, 34] exemplify a multi-objective approach, balancing financial returns, ESG scores, and risk metrics. These models cater to socially conscious investors, integrating environmental, social, and governance considerations into portfolio decision-making processes.

Addressing non-Gaussian distributions remains a critical challenge in portfolio optimization. Pioneering contributions by Harun et al. [17], Lucey et al. [30], and Pham et al. [35] explicitly tackle market irregularities, including fat tails, skewness, and quantile-based risks. By incorporating these non-Gaussian characteristics, modern models enhance their robustness and applicability, making them suitable for dynamic and irregular financial environments.

2.3 ESG optimization and sustainability in portfolio management

The integration of ESG criteria represents a paradigm shift in portfolio optimization. By aligning investment strategies with sustainability goals, ESG-focused models offer advanced tools for managing financial risks while addressing broader societal concerns. For instance, multi-index frameworks and wavelet-based Conditional Value-at-Risk (CVaR) have proven effective in balancing risk and return in volatile markets while prioritizing ESG compliance [36, 37]. Similarly, fuzzy multi-objective chance-constrained optimization provides a robust decision-making framework that incorporates uncertainty into ESG-focused investment strategies [38]. While these innovative models improve understanding of risk-return dynamics in sustainable portfolios, their practical application remains a challenge due to the need for empirical validation across diverse market conditions.

The rise of green finance and sustainable investing marks a profound shift in the global financial landscape, blending financial objectives with environmental and societal goals. Green finance initiatives, such as green bonds and renewable energy investments, often exhibit non-Gaussian characteristics like high volatility and skewness. These green assets have demonstrated potential for risk mitigation, diversification, and long-term financial success, even as their performance varies across different market conditions [39, 40].

Beyond their ecological impact, green finance initiatives often demonstrate the ability to enhance financial outcomes, offering strategies to manage risks during the ecological transition while potentially delivering attractive returns [41-44]. Advanced models that incorporate ESG-specific metrics, such as climate risk indices, help investors construct portfolios that are both profitable and socially responsible [18, 40, 41]. For instance, sustainability-focused optimization models have been instrumental in balancing financial returns with ecological impact, offering viable strategies to navigate the transition toward greener economies [41, 43]. Wu et al. [18] demonstrated the effectiveness of fused LASSO optimization in constructing socially responsible portfolios that integrate ESG scores. These models not only improve return predictions but also mitigate risks associated with regulatory and market uncertainties [18, 40]. Additionally, models like Zhao’s [40] adaptation of the Markowitz framework with root algorithms demonstrate the feasibility of managing green portfolios under non-Gaussian distributions. These models are particularly well-suited for handling extreme returns and market volatility, common in green assets such as renewable energy and green cryptocurrencies. The integration of ESG principles into investment strategies further reinforces the importance of aligning portfolio management practices with broader sustainability objectives.

Modern portfolio optimization models, including those based on ESG criteria, emphasize a balanced approach to risk minimization and return maximization. Frameworks such as neutrosophic goal programming address the uncertainty and ambiguity inherent in ESG metrics, making them particularly effective for managing green assets in complex market environments [38]. Risk-adjusted return measures, such as the Sharpe Ratio, have also been adapted to account for ESG impact, further enhancing the relevance of these models in sustainable investing [6].

Metaheuristic algorithms like Genetic Algorithms and Simulated Annealing have been employed to improve the flexibility and scalability of ESG-integrated optimization frameworks. These algorithms effectively incorporate ESG metrics and carbon compliance measures, enabling investors to prioritize green energy projects and exclude non-compliant assets, such as fossil fuels, ensuring a socially responsible investment strategy [18, 41].

2.4 The role of artificial intelligence in portfolio optimization

AI has revolutionized portfolio optimization by enabling the modeling of non-linear relationships and dynamic market conditions. Techniques like SVR, neural networks, and metaheuristics such as GA have significantly enhanced the precision and adaptability of portfolio models [45, 46]. For instance, SVR outperforms traditional approaches by leveraging non-linear regression to predict returns and optimize asset allocation. Studies demonstrate that SVR, when combined with algorithms like LASSO and neural networks, achieves superior risk-adjusted returns, particularly in ESG-focused portfolios [18, 47].

AI-driven frameworks also excel in managing market anomalies and adapting to evolving conditions. Hybrid models integrating machine learning with traditional optimization techniques have shown significant improvements in performance across various asset classes, including real estate investment trusts (REITs) and commodities [48]. By focusing on support vectors, SVR-based approaches mitigate the impact of outliers, ensuring robust predictions even in noisy datasets [18].

2.5 Applications of SVR in portfolio optimization

SVR has emerged as a critical tool for portfolio optimization, offering notable advantages in predicting returns, managing risks, and enhancing portfolio resilience. Empirical evidence supports its effectiveness across diverse markets, including U.S. equities, REITs, and commodities such as gold and cocoa [49, 50]. SVR models improve risk-return trade-offs, particularly in ESG-focused portfolios, and have consistently outperformed traditional methods in achieving higher Sharpe ratios [18].

The adaptability of SVR to fluctuating market conditions makes it a cornerstone of modern portfolio management. By addressing challenges such as volatility, shifting investor sentiment, and data irregularities, SVR-based models provide reliable predictions and robust performance across various financial contexts [45, 47].

2.6 Synthesis of the literature review

This review highlights the evolution of portfolio optimization, transitioning from traditional Gaussian models to advanced non-Gaussian frameworks that capture the complexities of modern financial markets. The limitations of Gaussian models, such as their inability to account for heavy tails, skewness, and dynamic market dependencies, have been increasingly addressed by non-Gaussian models. These models, including multivariate generalized hyperbolic distributions and non-Gaussian component frameworks, provide robust solutions for managing tail risks, asymmetry, and extreme co-movements, particularly during periods of market turbulence. Similarly, ESG integration has emerged as a critical advancement, aligning portfolio optimization practices with sustainability goals and societal values. Despite their promise, these approaches often face challenges in empirical validation, scalability, and computational complexity.

AI-driven methodologies, particularly SVR and hybrid models integrating machine learning techniques, have revolutionized portfolio optimization by enhancing adaptability, precision, and the handling of non-linear market behaviors. These innovations address significant gaps in traditional models, including the need for more accurate risk prediction, better resilience to market anomalies, and improved optimization of ESG-focused portfolios. However, the practical application of these models is constrained by challenges such as algorithmic complexity, data availability, and their ability to generalize across diverse financial contexts.

Despite substantial progress, several gaps remain in the existing literature. First, while non-Gaussian models excel in capturing market irregularities, their integration with ESG-focused and AI-driven frameworks is still underexplored. Second, there is a lack of comprehensive studies that synthesize the effectiveness of these models across different asset classes and market conditions. Lastly, the scalability of these advanced frameworks in real-world portfolio management remains a critical area for further exploration.

This paper addresses these gaps by systematically reviewing and synthesizing the literature on recent advancements in mathematical models for portfolio optimization. It focuses on non-Gaussian distributions and the integration of AI techniques, offering insights into their transformative potential within volatile and sustainable markets. By utilizing a SLR approach, this study highlights key mathematical advancements while identifying emerging trends and research directions. The findings aim to bridge theoretical innovations with practical applications, providing a comprehensive understanding of how these models can reshape portfolio management in increasingly complex financial environments.

This study adopts a SLR approach to comprehensively explore recent advancements in mathematical models for portfolio optimization, with a specific focus on non-Gaussian distributions and AI integration. The SLR methodology ensures a structured, transparent, and replicable process for identifying, selecting, and synthesizing relevant studies. This section outlines the systematic process employed to achieve the objectives of this study, including the identification of research gaps and emerging trends.

3.1 SLR

3.1.1 Search, Appraisal, Synthesis, and Analysis (SALSA) framework

The SLR methodology employed in this study follows the SALSA framework, as proposed by Grant and Booth [51]. This framework provides a robust structured methodology for defining search protocols, evaluating study quality, synthesizing results, and analyzing research trends, ensuring methodological rigor and reproducibility. The SALSA framework emphasizes systematic processes to mitigate publication bias and enhance the credibility of findings [4]. The SALSA framework guides the review process through the following stages:

Numerous studies [52-54] have demonstrated the effectiveness of the SALSA framework in ensuring thoroughness and systematization in literature reviews. This study modified the standard SALSA framework by incorporating preferred reporting items for systematic reviews and meta-analyses (PRISMA) methodology to enhance transparency in study selection and minimize bias in research inclusion. The adaptation of the framework is summarized in Table 1.

Table 1. SALSA framework of the systematic analysis

|

Step |

Outcomes |

Methods |

|

Protocol |

Defined study scope |

This review will highlight advancements in handling non-Gaussian behaviour in financial models and identify potential areas for further research. |

|

Search |

Search strategy |

Searching strings; primarily focused on "portfolio optimization" and "non-Gaussian distribution." Additionally, other terms, including "mathematical model," "Copula," "SVR," "MVO," "sustainable invest," "machine learning," and "green invest". |

|

Search studies |

Search databases; Scopus database |

|

|

Appraisal |

Selecting studies |

Defining inclusion and exclusion criteria Inclusion criteria:

Exclusion criteria:

|

|

Quality assessment of studies |

Quality criteria |

|

|

Synthesis |

Extract data |

Extraction: selected papers to derive insights and conclusions. |

|

Categorize the data |

Organize the data based on its iterative definition and prepare it for further analysis. Synthesize the information into thematic areas: mathematical models, AI integration, optimization focus, and model effectiveness. Include both qualitative and quantitative analyses. |

|

|

Analysis |

Data analysis |

Quantitative categories, description, and narrative analysis of the organized data. |

|

Result and discussion |

Based on the analysis, show the trends, identify gap and result. |

|

|

Conclusion |

Deriving conclusion and recommendation. |

|

|

Report |

Report writing |

PRISMA methodology. |

|

Journal article production |

Summarizing the report result for the larger public. |

Data Sources and Search Strategy:

A comprehensive search was conducted using the Scopus database, widely recognized for its extensive coverage of multidisciplinary academic literature. The search phase involved designing and executing a precise query string to retrieve relevant documents. The strategy targeted articles focusing on portfolio optimization, mathematical models, and related concepts.

The search query included primary keywords, such as "Portfolio optimization", "Non-Gaussian distribution", "Machine learning". Additional terms were incorporated to expand the review, including "Mathematical model", "Copula", "SVR", "MVO", "Sustainable investing", and "Green investment". Boolean operators "AND" and "OR" were used to refine the search, ensuring maximum coverage while minimizing irrelevant results. To enhance transparency and reproducibility, Table 2 presents a detailed breakdown of the search strings and the number of retrieved articles.

Table 2. The searching terms used and the total number of publications from Scopus database

|

Searching String |

No. of Articles |

Date of Acquisition |

|

(“Portfolio optimization" OR "Portfolio optimisation”) AND "Mathematic* model" |

233 |

08/10/2024 |

|

"Portfolio optimi*" AND ("non-Gaussian distribution" OR "fat-tailed distribution" OR "heavy-tailed distribution") |

18 |

08/10/2024 |

|

"Non-Gaussian asset returns" AND ("optimi* models" OR "risk-adjusted returns" OR "portfolio construction") |

1 |

08/10/2024 |

|

"Copula" AND "Portfolio optimi*" AND (“non-Gaussian distribution" OR "fat-tailed distribution" OR "heavy-tailed distribution”) |

5 |

08/10/2024 |

|

"Green" AND (“risk management" OR "Portfolio optimi*”) AND (“non-Gaussian distribution" OR "fat-tailed distribution" OR "heavy-tailed distribution”) |

1 |

08/10/2024 |

|

"Portfolio optimi*" AND ("non-Gaussian distribution" OR "fat-tailed distribution" OR "heavy-tailed distribution") AND ("stochastic models" OR "mathematical model")" |

5 |

08/10/2024 |

|

(“SVR" OR "Support Vector Regression”) AND (“Portfolio optimi*" OR "risk management”) |

115 |

08/10/2024 |

|

(“MVO" OR "Median Variance Optimization “) AND (“Portfolio optimi*" OR "risk management”) |

22 |

08/10/2024 |

|

"Portfolio optimi*" AND (“Sustainable invest*" OR "green invest*”) |

23 |

09/10/2024 |

|

"Portfolio optimi*" AND (“machine learning" OR "artificial intelligence”) AND "Mathematic* model" |

10 |

09/10/2024 |

|

"Portfolio optimi*" AND (“machine learning" OR "artificial intelligence”) AND (“Sustainable invest*" OR "green invest*”) |

1 |

09/10/2024 |

To complement the electronic search, manual hand-searching was performed in leading financial journals and references cited in selected studies. Articles published between 2009 and 2024 were included to capture recent advancements in portfolio optimization models.

The search process adhered to established guidelines to ensure alignment with the study’s objectives. References deemed irrelevant during initial screening were excluded, focusing only on studies that addressed the core research questions.

3.1.2 SALSA framework and its application in this study

To tailor the SALSA framework to the objectives of this study, modifications were made in the search and appraisal stages to accommodate:

Table 3. How each stage of the SALSA framework was applied

|

Stage |

Application in This Study |

Modifications |

|

Search |

Systematic retrieval of relevant studies using Scopus. A well-defined search query with primary and secondary keywords was used. |

Expanded search scope with Boolean operators, synonyms, and truncations to capture diverse modeling approaches and AI techniques. |

|

Appraisal |

Studies were screened using inclusion and exclusion criteria, followed by a quality assessment to ensure relevance. |

Adopted a two-phase screening:

|

|

Synthesis |

Data were categorized into thematic areas, including mathematical models, AI integration, risk measures, and ESG considerations. |

Employed thematic coding for qualitative synthesis and frequency analysis for model adoption trends. |

|

Analysis |

Evaluated trends, model effectiveness, gaps, and future research directions. |

Incorporated comparative model evaluation to assess strengths and weaknesses of non-Gaussian vs. Gaussian approaches. |

3.2 Screening and quality assessment

The screening process adhered to the PRISMA protocol, ensuring transparency and reproducibility. To ensure the inclusion of high-quality and relevant studies, a two-stage screening process and a rigorous quality assessment were conducted. These steps ensured the methodological rigor and reliability of the findings.

3.2.1 Screening process

The screening process followed a systematic approach:

Titles and abstracts of the unique studies were evaluated against the predefined inclusion and exclusion criteria. This step eliminated irrelevant articles while retaining studies aligned with the research objectives.

The remaining articles identified during the initial screening underwent a comprehensive full-text review. This phase assessed the depth of the study, the methodology employed, and the alignment of findings with the study's objectives.

3.2.2 Inclusion and exclusion criteria

A rigorous appraisal phase followed the search, evaluating articles based on predefined inclusion and exclusion criteria (Table 4). These criteria were developed to ensure that only high-quality and relevant studies were included in the review.

Table 4. SLR study selection of literature using inclusion and exclusion criteria

|

Criteria |

Decision |

|

When the predefined keywords exist as a whole or at least in title, keywords, or abstract section of the paper |

Inclusion |

|

Studies published in peer-reviewed journals |

Inclusion |

|

Studies published within the last 15 years |

Inclusion |

|

Articles exploring mathematical models for risk management in financial only |

Inclusion |

|

Conference abstracts, review articles, or gray literature |

Exclusion |

|

Studies focusing only on Gaussian distribution models |

Exclusion |

|

Non-English articles |

Exclusion |

|

Inaccessible publications |

Exclusion |

Inclusion Criteria:

Exclusion Criteria:

The inclusion period reflects the rapid advancements in computational power and data availability over the last 15 years, particularly during the rise of deep learning and neural network innovations. Table 4 provides a summary of study selection criteria.

3.3.1 Quality assessment tools and checklist

A tailored approach was used for the quality assessment of the included studies, employing tools specific to the type of research:

For empirical research, the Cochrane Risk of Bias Tool was applied. This tool evaluates the methodological quality of studies by identifying potential biases that could affect the validity of results. The following domains were assessed:

For theoretical and conceptual studies, a customized checklist was developed. The checklist evaluated the following aspects:

3.3.2 Scoring and categorization

Each study was assigned a score based on its performance across the quality assessment criteria. Studies were categorized as:

Only studies categorized as high or moderate quality were included in the final synthesis, ensuring the reliability and relevance of findings.

3.3.3 Additional quality assurance measures

3.4 Data synthesis

The data synthesis process aimed to systematically organize and analyze the findings from the selected studies to address the research objectives of this paper. This process involved categorizing and summarizing data to uncover patterns, emerging trends, and gaps in the literature on non-Gaussian models and AI-driven portfolio optimization.

3.4.1 Quantitative and qualitative analysis

To address the research objectives comprehensively, the data synthesis employed both quantitative and qualitative methods:

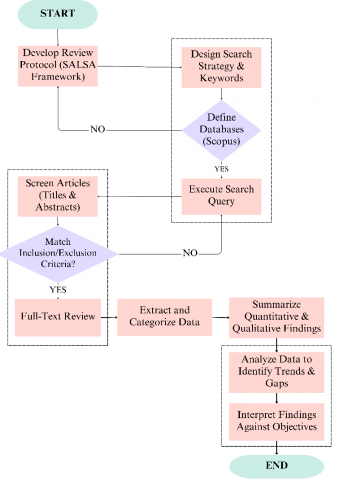

The extracted data from the final selected papers were organized into an Excel spreadsheet and analyzed to derive meaningful insights. Both qualitative and quantitative approaches were employed to address the research questions. Meta-analyses identified trends and evaluated the impact of specific mathematical models, while qualitative comparative analyses assessed their strengths and limitations. The whole methodology is summarized in Figure 3.

Figure 3. SALSA framework

The results and discussion section presents the findings from the SLR, aligning them with the objectives of the study. This section synthesizes quantitative and qualitative insights, highlights emerging trends, and identifies research gaps in the application of mathematical models for portfolio optimization, with a focus on non-Gaussian distributions and AI integration.

4.1 Screening and study selection

The general screening process and the selection flow of relevant literature are illustrated in Figure 4. These studies were categorized using the PRISMA protocol, guided by the SALSA framework. From an initial pool of 443 studies retrieved through Scopus, the screening process reduced the dataset to 61 high- and moderate-quality studies that aligned with the research objectives. The initial phase involved eliminating studies based on exclusion criteria, including conference abstracts, non-peer-reviewed articles, and works unrelated to portfolio optimization or mathematical modeling. Following title and abstract reviews, a total of 177 studies remained for full-text evaluation. The PRISMA flow diagram summarizing the study selection process present in Figure 4.

Figure 4. General screening process and the selection flow using PRISMA protocol guided by SALSA method

During the comprehensive full-text screening, studies were critically appraised for methodological rigor, relevance to non-Gaussian models, and incorporation of AI techniques. Duplicate studies and those lacking empirical focus or robust analysis methods were excluded. The final selection reflects a highly curated dataset, ensuring that only studies addressing the core aspects of non-Gaussian distribution models and AI integration in portfolio optimization were included.

4.2 Quantitative analysis of non-Gaussian models

The application of mathematical models in portfolio optimization has evolved significantly over the years, with a growing emphasis on non-Gaussian distributions to address complex financial market dynamics. The increasing number of published studies highlights the importance of these advancements.

4.2.1 Annual trends in non-gaussian models

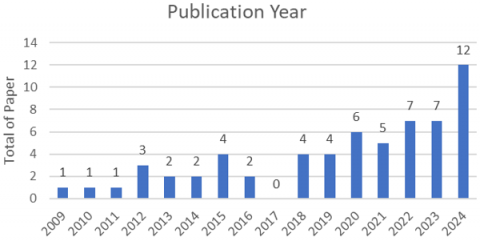

Figure 5 illustrates the increasing number of publications between 2009 and 2024, reflecting heightened interest in non-Gaussian models.

Notably, 2024 experienced a surge in research, indicating a shift towards advanced modeling techniques that account for fat tails, skewness, and asymmetric market behaviors.

Figure 5. Annual trends in portfolio optimization research (2009–2024)

This trend underlines the increasing recognition of non-Gaussian models as superior alternatives to traditional Gaussian-based portfolio optimization methods, particularly in the face of market anomalies and financial crises.

4.2.2 Most common mathematical models and algorithms for portfolio optimization

The review identified seven prominent mathematical models frequently applied in portfolio optimization: SVR, MVO, neural networks, Copulas, VaR and CVaR, GA, and GARCH. Table 5 summarizes the usage frequency of these models.

Table 5. Usage frequency of paper publication year for the most used model types

|

Year |

Model Types |

||||||

|

SVR |

MVO |

NN |

Copula |

VaR / CVaR |

GA |

GARCH |

|

|

2009 |

1 |

||||||

|

2010 |

1 |

||||||

|

2011 |

1 |

1 |

|||||

|

2012 |

1 |

1 |

|||||

|

2013 |

1 |

1 |

1 |

||||

|

2014 |

1 |

||||||

|

2015 |

1 |

2 |

1 |

||||

|

2016 |

1 |

1 |

1 |

1 |

|||

|

2017 |

|||||||

|

2018 |

3 |

1 |

|||||

|

2019 |

2 |

1 |

1 |

||||

|

2020 |

3 |

2 |

2 |

1 |

|||

|

2021 |

3 |

1 |

1 |

1 |

|||

|

2022 |

2 |

1 |

1 |

2 |

|||

|

2023 |

2 |

1 |

1 |

||||

|

2024 |

1 |

1 |

1 |

2 |

2 |

||

|

Total |

18 |

13 |

4 |

3 |

6 |

6 |

7 |

Among them, SVR emerged as the most widely used model, appearing in 30% of the reviewed papers. This dominance is attributed to its ability to handle non-linear relationships and non-Gaussian data distributions, making it particularly suitable for volatile and high-risk financial environments. In contrast, traditional models like MVO remain popular for their simplicity, despite their limitations in real-world market scenarios.

SVR outperformed other models in optimizing risk-adjusted returns and managing market volatility. Enhanced by complementary algorithms like LASSO and neural networks, SVR consistently improved allocation strategies and Sharpe ratios, making it particularly effective in ESG-focused portfolios [54].

Table 6 highlights SVR’s dominance, with list of highly cited studies supporting its application. Around 30% of the papers that were identified used the SVR model, demonstrating the model's high level of accuracy for mathematical models for portfolio optimization, particularly those addressing non-Gaussian distributions. By contrast, traditional models such as MVO (21%) remain widely used due to their simplicity, but they often fail to capture real-world market complexities, particularly under conditions of extreme volatility.

Table 7 illustrates the growing integration of algorithms into mathematical models for portfolio optimization over the past six years. Notably, approximately half of the reviewed studies have employed machine learning algorithms to enhance existing mathematical models, thereby improving optimization performance. Among these, regression emerges as the most widely applied and effective algorithm for tackling portfolio optimization challenges. It is followed by metaheuristics, deep learning, neural networks, regularization techniques, and ensemble methods.

Table 6. Frequency of top 5 mathematical models in portfolio optimization research (2009–2024)

|

Models |

Mostly Cited Papers |

Count of Papers from 2009 to 2024 |

The Proportion of Papers to the Total Number of Papers |

Accumulated Proportion |

|

SVR |

[11, 18, 49, 55] |

18 |

0.3 |

0.295 |

|

MVO |

[27, 43, 56] |

13 |

0.21 |

0.508 |

|

NN |

[7, 52] |

4 |

0.07 |

0.574 |

|

Copula |

[19, 47] |

3 |

0.05 |

0.623 |

|

GARCH |

[16, 47, 55] |

7 |

0.11 |

0.738 |

Table 7. Usage ranking of the six most used algorithms in in portfolio optimization research (2009–2024)

|

Year |

Algorithms |

|||||

|

Regression |

Meta-Heuristics |

Neural Networks |

Deep Learning |

Ensemble |

Regularization |

|

|

2009 |

1 |

|||||

|

2010 |

||||||

|

2011 |

||||||

|

2012 |

||||||

|

2013 |

1 |

|||||

|

2014 |

1 |

|||||

|

2015 |

1 |

|||||

|

2016 |

||||||

|

2017 |

||||||

|

2018 |

3 |

|||||

|

2019 |

1 |

1 |

||||

|

2020 |

2 |

1 |

2 |

|||

|

2021 |

2 |

1 |

||||

|

2022 |

1 |

1 |

||||

|

2023 |

2 |

1 |

1 |

|||

|

2024 |

2 |

1 |

2 |

|||

|

Total |

15 |

5 |

2 |

3 |

1 |

2 |

Prominent non-Gaussian techniques identified in the review include multivariate generalized hyperbolic distributions and Copula models. These methods have demonstrated superior performance in modeling asset dependencies and capturing market extremes. For instance, Copula-based models effectively address asymmetric dependencies, making them indispensable for volatile financial conditions.

4.2.3 Optimization objectives in portfolio models

Portfolio optimization models prioritize various objectives, including return maximization, risk minimization, and ESG alignment. Table 8 outlines the different areas of focus in portfolio optimization over the past 15 years.

Table 8. Focus areas on portfolio optimization models (2009–2024)

|

Year |

Portfolio Optimization Focus |

|||

|

Return Maximization |

Variance/Risk Minimization |

Risk-Adjusted Returns Optimization |

ESG Optimization |

|

|

2009 |

1 |

|||

|

2010 |

1 |

|||

|

2011 |

1 |

|||

|

2012 |

1 |

2 |

||

|

2013 |

2 |

|||

|

2014 |

1 |

1 |

||

|

2015 |

1 |

2 |

1 |

|

|

2016 |

1 |

1 |

||

|

2017 |

||||

|

2018 |

2 |

1 |

||

|

2019 |

2 |

2 |

||

|

2020 |

2 |

3 |

||

|

2021 |

2 |

1 |

1 |

|

|

2022 |

2 |

3 |

||

|

2023 |

1 |

2 |

1 |

2 |

|

2024 |

3 |

7 |

1 |

|

|

Total |

8 |

20 |

24 |

3 |

Among these, risk-adjusted returns optimization emerges as the most prominent, highlighting its effectiveness in balancing risk and return under volatile market conditions. ESG optimization has gained traction recently, reflecting growing interest in sustainable investments. Models incorporating ESG-specific metrics, such as climate risk indices, provide investors with tools to achieve financial and societal goals. This trend highlights the increasing consideration of outliers and extreme market behaviours that deviate from the traditional Gaussian distribution.

4.2.4 Relevance and application to green investments and sustainability

The application of non-Gaussian models in green investments has emerged as a key research area, addressing the unique risks and opportunities of sustainable assets. ESG optimization models incorporating advanced metrics have demonstrated effectiveness in aligning financial returns with environmental and social goals. Table 9 further supports the findings presented in Table 8. The results outline the growing relevance of green investments in portfolio optimization research, highlighting their increasing prominence in addressing global sustainability challenges over the past three years. Specifically, ESG optimization, green finance, sustainable investment, and green investment have emerged as key areas of focus during this period. This trend emphasizes a growing interest in addressing global sustainability challenges and prioritizing environmentally focused projects, reflecting the rising importance of green investments in the financial landscape.

Table 9. Relevance of green investments in portfolio optimization studies (2009–2024)

|

Year of Publication |

Green Investment Relevance |

|

|

Addressed |

Not Addressed |

|

|

2009 |

- |

1 |

|

2010 |

- |

1 |

|

2011 |

- |

1 |

|

2012 |

- |

3 |

|

2013 |

1 |

1 |

|

2014 |

- |

2 |

|

2015 |

- |

4 |

|

2016 |

- |

2 |

|

2017 |

- |

- |

|

2018 |

- |

4 |

|

2019 |

1 |

3 |

|

2020 |

1 |

5 |

|

2021 |

- |

5 |

|

2022 |

2 |

5 |

|

2023 |

3 |

4 |

|

2024 |

8 |

4 |

|

Total |

16 |

45 |

4.3 Emerging trends and research gaps

This systematic review synthesized both qualitative and quantitative findings to uncover critical insights into the advancements in portfolio optimization models, particularly those addressing non-Gaussian distributions and AI integration. By evaluating the selected studies, the research identified emerging trends and significant research gaps, offering a roadmap for future developments in this field.

4.3.1 Emerging trends

a) Hybridization of Non-Gaussian and AI Models

The findings reveal a growing trend toward hybrid approaches that combine non-Gaussian models with AI techniques. These approaches enhance risk-adjusted returns, improve asset allocation strategies, and optimize portfolio performance. For instance, SVR models, when integrated with complementary algorithms such as LASSO and neural networks, consistently demonstrated superior performance in risk-adjusted returns optimization and asset allocation strategies [47]. These hybrid models effectively address complex market behaviors, including tail risks, skewness, non-linear dependencies between assets, and market anomalies that traditional Gaussian models fail to capture, making them indispensable for navigating modern financial markets.

For portfolio managers, the adoption of AI-enhanced non-Gaussian models allows for more adaptive risk management strategies, enabling real-time adjustments in asset allocation, volatility forecasting, and market trend identification. Investors benefit from more precise return predictions and enhanced downside protection, reducing exposure to market crashes. These models provide an edge over traditional optimization techniques, particularly during financial crises and black swan events, where Gaussian assumptions fail.

b) Sustainability-Driven Investments

The increasing emphasis on ESG integration is transforming portfolio optimization frameworks, with investors prioritizing sustainable investment strategies. Advanced models now incorporate sustainability metrics, such as climate risk indices, green investment scores, and carbon exposure constraints, enabling investors to align financial objectives with environmental and societal goals. Studies utilizing ESG-enhanced frameworks have shown improved Sharpe ratios and risk mitigation, with long-term financial stability, particularly in volatile markets [18]. The adoption of non-Gaussian methods further enhances the reliability of these models in managing the unique characteristics of green assets, such as high volatility and non-linear return distributions.

For investors, these models help align financial goals with sustainability objectives, allowing for responsible investing without sacrificing returns. Portfolio managers leveraging non-Gaussian frameworks can better capture the risk-return trade-offs of green assets, which often exhibit high volatility, asymmetric return distributions, and sector-specific market shocks.

Moreover, regulatory developments promoting green finance are accelerating the adoption of AI-driven ESG models. Governments and financial institutions are increasingly incorporating non-Gaussian risk modeling techniques into climate stress tests and ESG risk assessments, reinforcing their role in shaping future investment landscapes.

c) Scalability and Computational Advancements

With the expanding complexity of financial datasets, portfolio optimization models must handle high-dimensional data, multi-asset class portfolios, and dynamic correlations. AI-driven solutions, such as metaheuristic algorithms (e.g., Genetic Algorithms) and deep learning architectures, have been applied to enhance computational efficiency while maintaining accurate risk-return estimations. The adoption of non-Gaussian methods further enhances the reliability of these models in managing the unique characteristics of green assets, such as high volatility and non-linear return distributions.

For portfolio managers, these advancements streamline decision-making, allowing for real-time optimization of investment strategies in response to market fluctuations. By integrating machine learning techniques, investors gain faster, data-driven insights, reducing reliance on outdated static models that fail to adapt to market changes.

4.3.2 Research gaps

Despite the promising performance of non-Gaussian models and AI-driven approaches, their empirical validation across diverse market conditions remains a notable limitation. The majority of existing studies concentrate on developed markets, such as the U.S. and European financial sectors, while applications in emerging or less liquid markets are significantly underexplored. Expanding research into these regions is crucial to establish the generalizability and broader applicability of these models, ensuring they are effective across varied financial contexts.

The integration of ESG principles into portfolio optimization introduces additional challenges, primarily due to the lack of standardized metrics. Inconsistent definitions and varied methodologies for assessing ESG factors hinder the comparability of findings across studies. This inconsistency limits the practical adoption of ESG-focused models and their ability to serve as reliable decision-making tools. To address this issue, the development of universally accepted ESG evaluation frameworks is imperative. These frameworks could provide a consistent basis for future research and serve as benchmarks for aligning sustainability-focused investment practices.

While scalable models leveraging AI techniques hold considerable promise, the literature reveals a scarcity of studies tackling the computational challenges associated with high-dimensional data. The increasing complexity of financial datasets necessitates the development of efficient algorithms that strike a balance between computational efficiency and predictive accuracy. Addressing this gap is critical for advancing the scalability and robustness of portfolio optimization models in practical applications.

Moreover, the robustness of optimization models under varying market scenarios, such as economic crises or periods of extreme volatility, requires more comprehensive investigation. Current studies often overlook sensitivity analyses that evaluate how models perform under diverse conditions. Expanding the scope of sensitivity analyses is essential to assess the adaptability and reliability of these models, ensuring their practical utility in real-world scenarios. Such efforts would enhance the resilience of portfolio optimization frameworks in the face of market uncertainties and dynamic financial environments.

This systematic review critically evaluates whether non-Gaussian models represent the future of portfolio optimization by analyzing 61 studies published between 2009 and 2024. The findings provide strong evidence supporting the pivotal role of non-Gaussian models, particularly SVR, in addressing the limitations of traditional Gaussian-based approaches. Non-Gaussian models excel in capturing complex financial phenomena, such as skewness, kurtosis, and fat tails, enabling more accurate risk management and return forecasting in volatile and asymmetric markets. The increasing adoption of hybrid AI-enhanced approaches, which integrate SVR with machine learning techniques such as LASSO and deep neural networks, further enhances the scalability and predictive accuracy of these models. As financial markets become increasingly unpredictable, non-Gaussian methodologies appear well-positioned to serve as the foundation for future portfolio optimization strategies.

Another critical advancement identified in this review is the integration of ESG factors into portfolio optimization models. The application of multi-objective frameworks incorporating sustainability metrics, such as green investment scores and climate risk indices, enables investors to align financial objectives with broader societal and environmental considerations. These models have been shown to improve risk-adjusted returns while maintaining ethical investment standards, reinforcing the importance of ESG-focused decision-making in modern portfolio management.

Additionally, the review identifies emerging trends in AI-driven metaheuristic algorithms, which significantly enhance the scalability, efficiency and adaptability of optimization models. Hybrid models that merge traditional mathematical frameworks with advanced AI techniques, such as deep learning, ensemble methods, and evolutionary algorithms, demonstrate remarkable potential in handling non-Gaussian distributions and sustainability-focused portfolios. This facilitates the transition toward data-driven, real-time investment strategies.

Despite these advancements, several key research gaps remain that require further investigation. First, computational efficiency and scalability remain a significant challenge. While AI-driven non-Gaussian models improve accuracy, their high computational demands can limit their practical applications in real-time portfolio management. Future research should explore optimization techniques, such as model compression, parallel computing, and cloud-based AI frameworks, to enhance the accessibility and efficiency of these models for both institutional and retail investors.

Second, while AI-enhanced non-Gaussian models have shown strong predictive capabilities, their integration with advanced mathematical models, such as Bayesian networks, stochastic processes, and Copula-based risk modeling, remains limited. Future research should explore hybrid approaches that combine deep learning with probabilistic financial models, which could improve both interpretability and predictive power in highly volatile and nonlinear financial environments.

In conclusion, non-Gaussian models, particularly when integrated with AI and ESG considerations, represent a transformative step forward in portfolio optimization. These models address the challenges of traditional Gaussian-based approaches while enabling investors to adapt to dynamic market conditions and sustainability priorities. To solidify their position as the future of portfolio optimization, future research must focus on addressing computational inefficiencies and advancing hybrid AI-finance methodologies. By addressing these challenges, non-Gaussian models have the potential to revolutionize portfolio management, paving the way for more resilient, adaptive, and sustainable investment strategies in the era of data-driven finance.

This work is funded by the Ministry of Higher Education (MOHE) Malaysia under the Fundamental Research Grant Scheme (Ref: FRGS/1/2024/STG06/UMT/02/2).

[1] Valaei, M., Khodakarami, V. (2023). A new multi-dimensional framework for start-ups lifespan assessment using Bayesian networks. Journal of Risk and Financial Management, 16(2): 88. https://doi.org/10.3390/jrfm16020088

[2] Zhang, Y. (2024). Application of financial mathematical models combined with root algorithms in finance. Scalable Computing: Practice and Experience, 25(4): 2146-2158. https://doi.org/10.12694/scpe.v25i4.2447

[3] Chaudhury, R., Islam, S. (2022). Multi-objective mathematical model for asset portfolio selection using neutrosophic goal programming technique. Neutrosophic Sets and Systems, 50: 356-371

[4] de Freitas, R.A., Vogel, E.P., Korzenowski, A.L., Rocha, L.A.O. (2020). Stochastic model to aid decision making on investments in renewable energy generation: Portfolio diffusion and investor risk aversion. Renewable Energy, 162: 1161-1176. https://doi.org/10.1016/j.renene.2020.08.012

[5] Semmler, W., Lessmann, K., Tahri, I., Braga, J.P. (2024). Green transition, investment horizon, and dynamic portfolio decisions. Annals of Operations Research, 334(1): 265-286. https://doi.org/10.1007/s10479-022-05018-2

[6] Frausto Solis, J., Purata Aldaz, J.L., González del Angel, M., González Barbosa, J., Castilla Valdez, G. (2022). Saipo-taipo and genetic algorithms for investment portfolios. Axioms, 11(2): 42. https://doi.org/10.3390/axioms11020042

[7] Kolari, J.W., Liu, W., Pynnönen, S. (2024). Portfolio theory and practice. In Professional Investment Portfolio Management: Boosting Performance with Machine-Made Portfolios and Stock Market Evidence, Switzerland, pp. 3-23. https://doi.org/10.1007/978-3-031-48169-7_1

[8] Lim, S., Kim, M.J., Ahn, C.W. (2020). A genetic algorithm (GA) approach to the portfolio design based on market movements and asset valuations. IEEE Access, 8: 140234-140249. https://doi.org/10.1109/ACCESS.2020.3013097

[9] Zhang, Y.D., Mandal, J.K., So-In, C., Thakur, N.V. (Eds.). (2020). Smart trends in computing and communications. In Smart Innovation, Systems and Technologies, Springer: Singapore. https://doi.org/10.1007/978-981-15-0077-0

[10] Degiannakis, S., Floros, C., Livada, A. (2012). Evaluating value-at-risk models before and after the financial crisis of 2008: International evidence. Managerial Finance, 38(4): 436-452. https://doi.org/10.1108/03074351211207563

[11] Board, F.S. (2009). Risk management lessons from the global banking crisis of 2008. Basel, Switzerland: Senior Supervisors Group. https://www.fsb.org/uploads/r_0910a.pdf.

[12] Franzolini, B., Beskos, A., De Iorio, M., Poklewski Koziell, W., Grzeszkiewicz, K. (2024). Change point detection in dynamic Gaussian graphical models: The impact of COVID-19 pandemic on the US stock market. The Annals of Applied Statistics, 18(1): 555-584. http://doi.org/10.1214/23-AOAS1801

[13] Cardenas, V. (2024). Managing financial climate risk in banking services: A review of current practices and the challenges ahead. arXiv preprint arXiv:2405.17682. https://doi.org/10.48550/arXiv.2405.17682

[14] Ahn, K., Jang, H., Kim, J., Ryu, I. (2024). COVID-19 and REITs crash: Predictability and market conditions. Computational Economics, 63(3): 1159-1172. https://doi.org/10.1007/s10614-023-10431-1

[15] Cinciulescu, D. (2024). The impact of tail risk and black swan events on modern portfolio theory. A reassessment of risk assumptions in extreme market conditions. Young Economists Journal Revista Tinerilor Economisti, 21(43): 83

[16] Ghanbari, H., Mohammadi, E., Fooeik, A.M.L., Kumar, R.R., Stauvermann, P.J., Shabani, M. (2024). Cryptocurrency portfolio allocation under credibilistic CVaR criterion and practical constraints. Risks, 12(10): 163. https://doi.org/10.3390/risks12100163

[17] Harun, H.F., Bakar, M.A., Abdullah, M.H. (2024). Semiparametric option-implied information and median-variance approach: A game-changer in integrating sustainable practices in portfolio optimization. International Journal of Sustainable Development & Planning, 19(6): 2229-2241. https://doi.org/10.18280/ijsdp.190622

[18] Wu, Z., Yang, L., Fei, Y., Wang, X. (2023). Regularization methods for sparse ESG-valued multi-period portfolio optimization with return prediction using machine learning. Expert Systems with Applications, 232: 120850. https://doi.org/10.1016/j.eswa.2023.120850

[19] Katsikis, V.N., Mourtas, S.D., Stanimirović, P.S., Li, S., Cao, X. (2021). Time-varying mean-variance portfolio selection under transaction costs and cardinality constraint problem via beetle antennae search algorithm (BAS). Operations Research Forum, 2: 1-26. https://doi.org/10.1007/s43069-021-00060-5

[20] Bhatnagar, C.S., Bhatnagar, D., Kumari, V., Bhullar, P.S. (2023). Sin versus green investment: A retrospective study on investor choice during pre-and through COVID regime. Managerial Finance, 49(9): 1474-1501. https://doi.org/10.1108/MF-10-2022-0477

[21] Ta, V.D., Liu, C.M., Tadesse, D.A. (2020). Portfolio optimization-based stock prediction using long-short term memory network in quantitative trading. Applied Sciences, 10(2): 437. https://doi.org/10.3390/app10020437

[22] Barbosa Filho, A.C.B., da Silva Neiro, S.M. (2022). Fine-tuned robust optimization: Attaining robustness and targeting ideality. Computers & Industrial Engineering, 165: 107890. https://doi.org/10.1016/j.cie.2021.107890

[23] Danielsson, J., James, K.R., Valenzuela, M., Zer, I. (2016). Model risk of risk models. Journal of Financial Stability, 23: 79-91. https://doi.org/10.1016/j.jfs.2016.02.002

[24] Zhang, Y. (2024). Application of financial mathematical models combined with root algorithms in finance. Scalable Computing: Practice and Experience, 25(4): 2146-2158. https://doi.org/10.12694/scpe.v25i4.2447

[25] Min, L., Han, Y., Xiang, Y. (2023). A two-stage robust omega portfolio optimization with cardinality constraints. IAENG International Journal of Applied Mathematics, 53(1): 86

[26] Paolella, M.S., Polak, P., Walker, P.S. (2021). A non-elliptical orthogonal GARCH model for portfolio selection under transaction costs. Journal of Banking & Finance, 125: 106046. https://doi.org/10.1016/j.jbankfin.2021.106046

[27] Bianchi, M.L., Tassinari, G.L. (2020). Forward-looking portfolio selection with multivariate non-Gaussian models. Quantitative Finance, 20(10): 1645-1661. https://doi.org/10.1080/14697688.2020.1733057

[28] Saâdaoui, F., Rabbouch, H. (2024). Financial forecasting improvement with LSTM-ARFIMA hybrid models and non-Gaussian distributions. Technological Forecasting and Social Change, 206: 123539. https://doi.org/10.1016/j.techfore.2024.123539

[29] Lu, W., Huang, G. (2022). Estimating the higher-order co-moment with non-Gaussian components and its application in portfolio selection. Statistics, 56(3): 537-564. https://doi.org/10.1080/02331888.2022.2074006

[30] Lucey, B., Yahya, M., Khoja, L., Uddin, G.S., Ahmed, A. (2024). Interconnectedness and risk profile of hydrogen against major asset classes. Renewable and Sustainable Energy Reviews, 192: 114223. https://doi.org/10.1016/j.rser.2023.114223

[31] Abate, G., Basile, I., Ferrari, P. (2024). The integration of environmental, social and governance criteria in portfolio optimization: An empirical analysis. Corporate Social Responsibility and Environmental Management, 31(3): 2054-2065. https://doi.org/10.1002/csr.2682

[32] Zheng, Y., Shukla, K.N., Xu, J., Wang, D.X., O’Leary, M. (2023). MOPO-LSI: An open-source multi-objective portfolio optimization library for sustainable investments. Software Impacts, 16: 100499. https://doi.org/10.1016/j.simpa.2023.100499

[33] Xidonas, P., Essner, E. (2024). On ESG portfolio construction: A multi-objective optimization approach. Computational Economics, 63(1): 21-45. https://doi.org/10.1007/s10614-022-10327-6

[34] Zheng, J., Wang, Y., Li, S., Chen, H. (2021). The stock index prediction based on SVR model with bat optimization algorithm. Algorithms, 14(10): 299. https://doi.org/10.3390/a14100299

[35] Pham, S.D., Nguyen, T.T., Do, H.X. (2024). Impact of climate policy uncertainty on return spillover among green assets and portfolio implications. Energy Economics, 134: 107631. https://doi.org/10.1016/j.eneco.2024.107631

[36] Ameur, H.B., Ftiti, Z., Louhichi, W., Yousfi, M. (2024). Do green investments improve portfolio diversification? Evidence from mean conditional value-at-risk optimization. International Review of Financial Analysis, 94: 103255. https://doi.org/10.1016/j.irfa.2024.103255

[37] Varmaz, A., Fieberg, C., Poddig, T. (2024). Portfolio optimization for sustainable investments. Annals of Operations Research, 341(2): 1151-1176. https://doi.org/10.1007/s10479-024-06189-w

[38] Chiadamrong, N., Suthamanondh, P. (2022). Fuzzy multi-objective chance-constrained portfolio optimization under uncertainty considering investment return, investment risk, and sustainability. International Journal of Knowledge and Systems Science, 13(1): 1-39. https://doi.org/10.4018/IJKSS.302660

[39] D’Orazio, P., Popoyan, L. (2019). Fostering green investments and tackling climate-related financial risks: Which role for macroprudential policies? Ecological Economics, 160: 25-37. https://doi.org/10.1016/j.ecolecon.2019.01.029

[40] Zhao, L., Zhang, Y., Sadiq, M., Hieu, V.M., Ngo, T.Q. (2023). Testing green fiscal policies for green investment, innovation and green productivity amid the COVID-19 era. Economic Change and Restructuring, 56(5): 2943-2964. https://doi.org/10.1007/s10644-021-09367-z

[41] Argentiero, A., Bonaccolto, G., Pedrini, G. (2024). Green finance: Evidence from large portfolios and networks during financial crises and recessions. Corporate Social Responsibility and Environmental Management, 31(3): 2474-2495. http://doi.org/10.1002/csr.2687

[42] Guerard, J., Jin, H., Qiao, Y., Wang, Y., Zhang, H. (2023). ESG integration in portfolio management: Focus on climate change. SSRN. https://doi.org/10.2139/ssrn.4577403

[43] Luo, D., Shan, X., Yan, J., Yan, Q. (2023). Sustainable investment under ESG volatility and ambiguity. Economic Modelling, 128: 106471. https://doi.org/10.1016/j.econmod.2023.106471

[44] Fang, M., Tan, K.S., Wirjanto, T.S. (2019). Sustainable portfolio management under climate change. Journal of Sustainable Finance & Investment, 9(1): 45-67. https://doi.org/10.1080/20430795.2018.1522583

[45] Behera, J., Pasayat, A.K., Behera, H., Kumar, P. (2023). Prediction based mean-value-at-risk portfolio optimization using machine learning regression algorithms for multi-national stock markets. Engineering Applications of Artificial Intelligence, 120: 105843. https://doi.org/10.1016/j.engappai.2023.105843

[46] Valaei, M., Khodakarami, V. (2024). A framework for valuation and portfolio optimization of venture capital deals with contractual terms. Mathematical Problems in Engineering, 2024(1): 3427721. https://doi.org/10.1155/2024/3427721

[47] Habbab, F.Z., Kampouridis, M. (2024). An in-depth investigation of five machine learning algorithms for optimizing mixed-asset portfolios including REITs. Expert Systems with Applications, 235: 121102. https://doi.org/10.1016/j.eswa.2023.121102

[48] Ampountolas, A. (2024). Enhancing forecasting accuracy in commodity and financial markets: Insights from GARCH and SVR models. International Journal of Financial Studies, 12(3): 59. https://doi.org/10.3390/ijfs12030059

[49] Kara, M., Ulucan, A., Atici, K.B. (2019). A hybrid approach for generating investor views in Black-Litterman model. Expert Systems with Applications, 128: 256-270. https://doi.org/10.1016/j.eswa.2019.03.041

[50] Niu, Z., Wang, C., Zhang, H. (2023). Forecasting stock market volatility with various geopolitical risks categories: New evidence from machine learning models. International Review of Financial Analysis, 89: 102738. https://doi.org/10.1016/j.irfa.2023.102738

[51] Grant, M.J., Booth, A. (2009). A typology of reviews: An analysis of 14 review types and associated methodologies. Health Information & Libraries Journal, 26(2): 91-108. https://doi.org/10.1111/j.1471-1842.2009.00848.x

[52] Bathaei, A., Štreimikienė, D. (2023). A systematic review of agricultural sustainability indicators. Agriculture, 13(2): 241. https://doi.org/10.3390/agriculture13020241

[53] Holgado, A.G., Pablos, S.M., Peñalvo, F.J.G. (2020). Guidelines for performing systematic research projects reviews. International Journal of Interactive Multimedia and Artificial Intelligence, 6(2): 136-144. https://doi.org/10.9781/ijimai.2020.05.005

[54] Saunders-Smits, G.N., Cruz, M.L. (2020). Towards a typology in literature studies & reviews in engineering education research. In 48th Annual Conference on Engaging Engineering Education, SEFI 2020, Society for Engineering Education, pp. 441-450.

[55] Ali, F., Khurram, M.U., Sensoy, A., Vo, X.V. (2024). Green cryptocurrencies and portfolio diversification in the era of greener paths. Renewable and Sustainable Energy Reviews, 191: 114137. https://doi.org/10.1016/j.rser.2023.114137

[56] Aboussalah, A.M., Xu, Z., Lee, C.G. (2022). What is the value of the cross-sectional approach to deep reinforcement learning? Quantitative Finance, 22(6): 1091-1111. http://doi.org/10.2139/ssrn.3748130