Nguyen Chien Thang![]() | Bui Viet Hung

| Bui Viet Hung![]() | Luong Thuy Duong*

| Luong Thuy Duong*![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study examines how corporate social responsibility (CSR) contributes to environmental sustainability in two rapidly industrializing provinces of Vietnam: Bac Ninh and Bac Giang. This paper adopts a multidimensional approach to CSR, focusing on employees, community engagement, ethical practices, and legal compliance. It then evaluates how this CSR implementation influences environmental planning and sustainable development outcomes. The results from a survey of over 500 related interviewees show that firms with strong legal adherence, ethical conduct, and proactive community involvement tend to achieve better environmental performance. The findings underscore the importance of integrating CSR into environmental management frameworks in developing industrial regions. This research offers practical insights for policymakers and urban planners seeking to align industrial growth with environmental sustainability in accordance with national legislation and global sustainable development goals.

corporate social responsibility, environmental policy, sustainable development, industrial zones, employees, legal

Corporate social responsibility (CSR) plays a crucial role in promoting environmental sustainability and remains a key concern worldwide. CSR has been widely recognized for its potential to enhance environmental performance and contribute to long-term sustainability. For instance, the study by Ajibike et al. [1] explores the effectiveness of environmental corporate social responsibility (ECSR) in shaping green buying intentions in the new energy vehicle market in China, finding that ECSR directly and indirectly, via green trust and green brand image, shapes green purchasing intentions positively. Similarly, Alexiadou [2] argued that CSR, particularly ESG, is gaining momentum as businesses shift from profit-only models to ones that are socially, environmentally and ethically conscious.

The relationship between CSR and innovation also features prominently. An [3] indicated that environmental regulations positively amplify the impact of CSR on green total factor productivity by encouraging R&D investment. Likewise, Aslan and Şendoğdu [4] demonstrated CSR is correlated with environmental strategy and green innovation, both of which improve environmental performance. In the same sphere, Becchetti et al. [5] indicated that CSR committees and ESG initiatives positively influence corporate sustainability by increasing environmental responsibility. The study by Bhatti et al. [6] shows that perceived CSR improves green organizational climate and employees’ workplace pro-environmental behavior (WPEB) and that a shared green vision enhances this relationship.

In terms of comprehensive CSR dimensions, Carroll [7] found all forms of CSR—toward environment, employee, community and consumer—positively impact environmentally sustainable development, which in turn enhances green innovation. Lastly, Castro-Casal et al. [8] confirmed that coercive pressure from policies acts as a positive mediator between CSR and environmental sustainability performance in Malaysia’s construction industry.

Bac Giang and Bac Ninh are two industrially developed provinces located near Vietnam’s capital and close to the seaports, making them ideal for trade and export activities. These two provinces have successfully invited many world-class groups to operate. Their rapid industrialization means that proper environmental protection and strict compliance with legal regulations—especially in environmental and labor law—are crucial to maximizing their geographical and development potential in the future. Therefore, investigating the role of CSR—particularly in relation to employees, legal compliance, ethics and community contributions—is essential for promoting sustainable development in these regions. This paper aims to examine how different aspects of CSR influence environmental sustainability with a focus on mediating role of CSR implementation. The goal is to provide empirical evidence on how CSR practices can drive both environmental outcomes and legal accountability in highly industrialized areas of a developing country like Vietnam. This is consistent with recent evidence from Vietnam’s banking sector, where environmental CSR initiatives are found to improve firms' financial performance, while social initiatives enhance stakeholder trust and investor confidence [9].

The four CSR dimensions examined in this study—community, employees, ethics, and legality—are grounded in classical CSR theory [10], particularly pyramid of corporate social responsibility and stakeholder theory [11]. Carroll’s framework outlines four fundamental roles that businesses should fulfill: legal, ethical, philanthropic, and economic responsibilities. This study focuses on the latter three (legal, ethical, and philanthropic) and adds employee-related CSR as a critical operational domain, aligning with the concerns of various stakeholder groups. In addition, stakeholder theory emphasizes that firms are accountable not only to shareholders as well as a wide array of other parties such as employees, community members, governmental bodies, and the broader society. Accordingly, the selected CSR dimensions reflect both external stakeholder engagement (community and legality) and internal responsibility (employees and ethics). These constructs are widely validated in prior CSR–performance and CSR–sustainability studies [12, 13], making them theoretically and empirically relevant for examining sustainability outcomes in industrial contexts.

2.1 CSR towards community

In relation to business outcomes, CSR has been found to contribute significantly to firm performance. CSR positively influences firm performance by shaping corporate reputation, which in turn affects consumers’ buying behavior [14]. Additionally, CSR initiatives are positively associated with firm efficiency and stronger effects observed in non-competitive industries. Local community-focused CSR initiatives significantly drive the overall effect [15]. Meanwhile, CSR contributes notably in enhancing both brand image and the firm's competitive position. Stakeholder influence significantly influences which CSR initiatives are adopted and helps build a positive organizational image. CSR performance in legal, ethical, environmental and philanthropic responsibility—excluding economic responsibility—has a significant influence on corporate reputation [16]. Moreover, clearly conveying and broadly disseminating CSR initiatives is recognized as a crucial strategy to enhance awareness and involvement among both employees and consumers. This type of communication enhances the performance of retail businesses while simultaneously contributing to their sustainability objectives [17]. Overall, the literature demonstrates that CSR initiatives targeting the community not only strengthen organizational performance and competitive advantage but also contribute meaningfully to social cohesion, public trust and long-term sustainability. Similarly, a recent study on Vietnamese enterprises finds that CSR programs implemented by state-owned enterprises significantly enhance the green performance of SMEs, regardless of external environmental uncertainty [18]. Hence, this research tests the following hypothesis and the search model is proposed as Figure 1.

Figure 1. Conceptual framework (developed by authors)

H1. CSR towards community has a positive relationship with CSR.

2.2 CSR towards employees

Employee satisfaction and organizational commitment are among the most frequently studied outcomes of CSR activities. Using a multilevel cognitive approach, Khuong et al. [19] revealed that organizational CSR climate and employees’ CSR-induced intrinsic attribution could serially mediate the relationship between firms’ CSR adoption and employees’ organizational commitment.

Evidence also suggests that CSR contributes to enhancing innovation and the generation of new knowledge. Kraus et al. [20] argued that higher levels of employee-focused CSR are linked to greater innovation achievements. This relationship becomes stronger when employee contributions to innovation are critical, and when the tendency for individuals to benefit without contributing (free-riding) is more prevalent. Additional tests indicate that employee-related CSR encourages innovation by promoting workforce stability and improving the efficiency of innovative activities. The psychological mechanisms linking CSR and employee behaviors are varied. For example, Li and Cao [21] found that substantive CSR has been shown to enhance employees’ emotional attachment to the organization, a relationship that is mediated by their sense of meaningfulness at work and further reinforced by their level of embeddedness, while symbolic CSR is not. This is reinforced by Lin et al. [22], who write that only when employees perceive CSR efforts as genuine (i.e., substantive) do they exhibit more discretionary service behaviors, and this is driven by the meaningfulness they derive from their work. CSR initiatives also foster organizational citizenship behaviors (OCBs). The study by Liu et al. [23] reports that the relationship between CSR and employees’ organizational citizenship behaviors (OCBs) is moderated by task significance, with stronger effects observed among employees who perceive their work as more meaningful. Similarly, Malinauskaite and Jouhara [24] confirmed a strong relationship between perceived CSR directed toward employees and their likelihood to engage in positive discretionary behaviors within the organization.

Other studies also underscore the importance of contextual factors and mediators. For example, the study by Mubushar et al. [25] reports a positive correlation between digitalization and employees’ CSR commitment. However, this relationship is found to be conditional upon the type of Human Resource Management (HRM) system in place and the extent to which employees’ need for autonomy is satisfied in the workplace.

Perceptions of CSR authenticity among employees also play a significant role in shaping outcomes. According to the study by Muliati et al. [26], when employees perceive their company’s CSR initiatives as authentic, it leads to both organizational benefits—such as increased employee loyalty, trust in management, and positive word-of-mouth—and personal benefits, including enhanced job satisfaction and emotional well-being. Moreover, CSR initiatives can contribute to a greater sense of meaning in employees' work. Building upon the preceding discussion, the following hypothesis is proposed.

H2. CSR towards employees has a positive relationship with CSR.

2.3 CSR towards ethics

CSR and ethical practices have been found to exhibit a strong and positive relationship with multiple dimensions of organizational performance. Specifically, CSR and ethics are positively associated with product innovativeness, brand equity, and customer trust. To capitalize on these benefits, organizations are encouraged to adopt transparent practices and demonstrate strong adherence to ethical and CSR strategies [13]. Likewise, Nejati and Shafaei [27] argued that CSR initiatives help build an ethical and reputable corporate image, which, in turn, enhances the credibility of the firm’s research and development (R&D) projects. Notably, this positive relationship between CSR efforts and R&D valuation tends to be more pronounced in highly competitive industries. These findings suggest that CSR initiatives not only reinforce brand value and foster innovation but also play a crucial role in enhancing the legitimacy of R&D efforts.

The importance of leadership and internal organizational dynamics is also emphasized. The study by Newman et al. [28] concludes that ethical leadership affects CSR positively. Social responsibility in turn affects corporate ethical values and behaviors positively.

The partial mediating role of CSR has also been identified in the study. Similarly, Ong et al. [29] emphasized the importance of alignment between employees’ perceptions of CSR and ethical leadership, as this consistency enhances their willingness to contribute to social good through relationship-building activities within the organization. These findings underscore the pivotal role of ethical leadership and the congruence between leaders and employees in fostering socially responsible behaviors.

On a broader level, the study by Schaefer et al. [30] suggests that ethics can act as a foundation for voluntary corporate self-regulation initiatives, with CSR playing a central role. This perspective positions CSR not only as an internal organizational instrument but also as an external mechanism for corporate governance. Based on these findings, the following hypothesis is proposed.

H3. CSR towards ethics has a positive relationship with CSR.

2.4 CSR towards legality

Several studies underscore the foundational role of national legal systems in shaping CSR practices. Extending this perspective, the study by Shahzad et al. [31] shows that legal frameworks influence corporate responsibility (CR) in both social and environmental dimensions. Corporations are more inclined to behave in environmentally responsible ways when robust and well-enforced regulations are in place. Furthermore, firms with a higher proportion of publicly held shares and lower debt levels tend to be more committed to social and environmental initiatives. A rights-based legal tradition is further illustrated in the study by Shahzad et al. [31], which argues that, as the UK constitution adopts a rights-based approach, corporate and business law safeguards individual and community rights on a case-by-case basis. It also enforces both criminal and civil liability on corporations and their leaders. Importantly, the law supports voluntary action but prohibits personal or proximate benefit, as well as actions carried out under legal compulsion. These findings collectively affirm the significant influence of national legal traditions and regulatory structures in shaping and reinforcing CSR engagement.

Another key area of scholarship focuses on the evolving relationship between soft law and hard law in driving CSR adoption. The study by Sharma-Nepal and Isce-Taylor [32] emphasizes that soft law being flexible has helped in many ways to make the CSR approach accessible to the consumer, shareholder and the stakeholders as well. However, the softness that this ideology of the soft law provides in some cases has posed itself to be a challenge in the path of developing CSR. Similarly, hard law and its strictness and binding factor is an effective way to make CSR a prominent factor to enhance various factors in business. Supporting this transition, Sheehy et al. [33] observed that there is a global policy shift moving CSR from a voluntary, organisation-based initiative to a practice mandated by law. This shift provides an opportunity to investigate the phenomenon of motivation in law. Based on an analysis of the programs of 12 firms in Indonesia, the authors find that CSR hard law appears to motivate CSR without displacing voluntary moral initiatives. Together, these contributions suggest that a hybrid legal architecture — combining the incentives of soft norms with the enforceability of hard laws — may offer a more effective foundation for CSR. From the previous studies, the following hypothesis is proposed.

H4. CSR towards legality has a positive relationship with CSR.

To test the main hypotheses, this study also proposes an additional hypothesis, which is that:

H5. CSR has a positive relationship with environmental sustainability.

H6. CSR implementing behaviors have a positive relationship with environmental sustainability.

H7. Interaction between CSR and CSR implementing behaviors has a positive relationship with environmental sustainability.

The survey was conducted with managers at different levels in companies, including both senior and junior leaders. It focused on two provinces in northern Vietnam: Bac Ninh and Bac Giang. These are highly industrialized areas with many industrial zones and a diverse range of businesses. The questionnaires were distributed to various types of companies, including both domestic and foreign enterprises, using printed survey forms. Approximately 600 questionnaires were distributed, but some were excluded due to missing or incomplete information. A simple stratified random sampling method was applied to select companies from different industries and ownership types (Vietnamese and foreign companies) in Bac Ninh and Bac Giang. This ensured ensure that the sample included a variety of business types and sizes. The data was collected from at the beginning of 2024. The survey was conducted using both printed questionnaires (distributed in person) and an online form (sent through emails and social networks) as mentioned above. This mixed method helped this current research reach more participants and improve the response rate.

Before the official survey, a small pilot test with several company managers and specialists was carried out. Feedback from the pilot was used to revise and clarify the wording of several survey items. Internal consistency of the constructs was assessed using Cronbach’s Alpha and other standard reliability measures. In addition, all responses were collected voluntarily, and participants were informed that their answers would be kept confidential. No personally identifiable or sensitive data was collected. Figure A1 provides a more detailed description of the research process.

Table 1. Demographic information

|

Characteristics |

Range |

Frequency |

Percentage |

|

Gender |

Male |

255 |

48.30 |

|

|

Female |

273 |

51.70 |

|

Age |

18-29 |

71 |

13.55 |

|

|

30-39 |

169 |

32.25 |

|

|

40-49 |

134 |

25.57 |

|

|

50-59 |

93 |

17.75 |

|

|

>60 |

57 |

10.88 |

|

Location |

Bac Ninh |

245 |

46.40 |

|

|

Bac Giang |

283 |

53.59 |

|

Total |

|

528 |

528 |

Source: Authors’ calculation based on original survey data collected in 2024.

A total of 528 people participated in the online and offline survey. Among them, 48.30% were male and 51.70% were female. In terms of age, most respondents were between 30 and 49 years old, which shows a strong presence of experienced working professionals. Regarding location, 46.40% of participants were from Bac Ninh and 53.59% were from Bac Giang. This group of participants represents a diverse and representative sample of company leadership in industrial regions (Table 1).

4.1 Validity and convergent

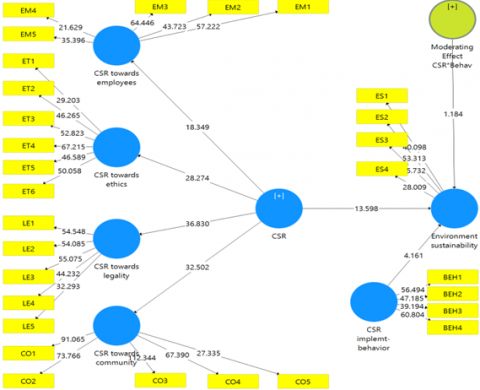

Table 2 and Figure 2 present construct reliability and validity results of the measurement model. Most constructs exhibit strong internal consistency, with Cronbach’s Alpha values exceeding the acceptable threshold of 0.70. All constructs demonstrate both strong reliability and convergent validity with Average Variance Extracted (AVE) values exceeding 0.50, the accepted number suggested by Subramaniam et al. [34]. For instance, CSR implementation behavior reports a CR of 0.922 and an AVE of 0.746, indicating robust construct validity. Similarly, CSR towards community, employees, ethics and legality each reflect high CR and satisfactory AVE levels. Environmental sustainability also demonstrates satisfactory reliability with AVE of 0.679 (CR = 0.894).

Figure 2. Measurement model from SmartPLS 3

Table 2. Construct reliability and validity

|

|

Cronbach’s Alpha |

rho_A |

CR |

AVE |

|

CSR |

0.928 |

0.930 |

0.936 |

0.412 |

|

CSR implemtation-behavior |

0.887 |

0.896 |

0.922 |

0.746 |

|

CSR towards community |

0.921 |

0.924 |

0.942 |

0.764 |

|

CSR towards employees |

0.888 |

0.892 |

0.918 |

0.691 |

|

CSR towards ethics |

0.911 |

0.912 |

0.931 |

0.694 |

|

CSR towards legality |

0.895 |

0.896 |

0.923 |

0.707 |

|

Environmental sustainability |

0.842 |

0.850 |

0.894 |

0.679 |

|

Moderating Effect: CSR*Behavior |

1.000 |

1.000 |

1.000 |

1.000 |

Source: Authors’ calculation based on PLS-SEM analysis using SmartPLS 3.

Note: CR and AVE stand for composite reliability and average variance extracted.

Table 3 presents the Fornell-Larcker criterion to assess discriminant validity among the study’s constructs. Discriminant validity ensures that each construct is distinct from the others. According to the Fornell-Larcker rule, the square root of the AVE for each construct, shown on the diagonal, should be higher than its correlations with other constructs [35]. The results show that BE (Implementation Behaviors), CO (CSR Orientation), EM (CSR towards Employees), ET (CSR towards Ethics), CSR (Corporate Social Responsibility) and ES (Environmental Sustainability) all have diagonal values higher than their correlations with other variables. This indicates that these constructs have good discriminant validity and are distinctly separated from each other.

The Heterotrait-Monotrait Ratio (HTMT) is shown in Table 4, which is used to test discriminant validity. For good discriminant validity, all HTMT values should be below 0.85 (or in some cases, 0.90). Most constructs in the table meet this criterion. For example, the HTMT value between BE (Implementation Behaviors) and other variables like CSR (0.499), EM (0.583) and LE (0.580) are all below 0.85, showing good discriminant validity. Similarly, EM (CSR towards Employees) has HTMT values below 0.85 with all other constructs, such as CSR (0.768), CO (0.408) and ET (0.293), indicating that EM is clearly distinct.

The factor loadings for each indicator within their respective constructs demonstrate strong internal consistency and reliability in Table 5. The indicator loadings of all questions are more than the threshold value of 0.708 suggested by Tran et al. [36] and as a result, no items are eliminated from the composite constructs. For example, for CSR towards employees, all items (EM1–EM5) have high loadings, ranging from 0.780 to 0.875, indicating that these statements reliably measure employee-related CSR activities.

Table 3. Fornell-Larcker criterion

|

CSR |

BE |

CO |

EM |

ET |

LE |

ES |

BE |

|

|

CSR |

0.642 |

|||||||

|

BE |

0.458 |

0.864 |

||||||

|

CO |

0.786 |

0.217 |

0.874 |

|||||

|

EM |

0.689 |

0.516 |

0.370 |

0.831 |

||||

|

ET |

0.765 |

0.167 |

0.570 |

0.266 |

0.833 |

|||

|

LE |

0.795 |

0.520 |

0.431 |

0.546 |

0.432 |

0.841 |

||

|

ES |

0.668 |

0.440 |

0.376 |

0.508 |

0.403 |

0.742 |

0.824 |

|

|

BE |

-0.073 |

-0.177 |

-0.121 |

-0.102 |

0.044 |

-0.055 |

-0.004 |

1.000 |

Source: Authors’ calculation.

Note: CSR, corporate social responsibility; BE, implementation behaviors; EM, CSR towards employees; ET, CSR towards ethics; LE, CSR towards legality; ES, Environmental sustainability.

Table 4. Heterotrait-Monotrait Ratio (HTMT)

|

CSR |

BE |

CO |

EM |

ET |

LE |

ES |

CSR*Beha |

|

|

CSR |

||||||||

|

BE |

0.499 |

|||||||

|

CO |

0.849 |

0.242 |

||||||

|

EM |

0.768 |

0.583 |

0.408 |

|||||

|

ET |

0.840 |

0.183 |

0.625 |

0.293 |

||||

|

LE |

0.857 |

0.580 |

0.474 |

0.614 |

0.478 |

|||

|

ES |

0.746 |

0.495 |

0.428 |

0.585 |

0.461 |

0.854 |

||

|

CSR*Beha |

0.139 |

0.190 |

0.138 |

0.108 |

0.094 |

0.088 |

0.052 |

Source: Authors’ calculation. HTMT values calculated using SmartPLS.

Note: CSR, corporate social responsibility; BE, implementation behaviors; EM, CSR towards employees; ET, CSR towards ethics; LE, CSR towards legality; ES, Environmental sustainability; Beha, Moderating Effect CSR*Behaviors.

Table 5. Convergent validity and reliability for outer loading model

|

Contruct and Indicators |

Item |

Factor Loadings |

CR |

AVE |

|

CSR towards employees |

|

|

0.918 |

0.691 |

|

We always provide fair compensation for all employees |

EM1 |

0.853 |

|

|

|

We have a strategy for training and developing future employees |

EM2 |

0.853 |

|

|

|

We value the collective voice of employees when making decisions |

EM3 |

0.875 |

|

|

|

We create equal opportunities for all workers to unleash their creativity |

EM4 |

0.793 |

|

|

|

We hold an annual workers' conference |

EM5 |

0.780 |

|

|

|

CSR towards ethics |

|

|

0.931 |

0.694 |

|

We treat all employees fairly and with respect, regardless of gender or ethnicity |

ET1 |

0.741 |

|

|

|

We do not use child labor (labor under the age of 16) |

ET2 |

0.844 |

|

|

|

We always protect the personal information and privacy of employees |

ET3 |

0.858 |

|

|

|

Employees have the right to refuse work that poses significant risks to their life or health |

ET4 |

0.886 |

|

|

|

We always comply with labor laws |

ET5 |

0.815 |

|

|

|

In employing labor, we do not engage in practices such as (retaining employee documents, making it difficult for employees to transfer jobs, requiring workers to deposit money, applying psychological violence, using force to threaten or coerce labor) |

ET6 |

0.846 |

|

|

|

CSR towards legality |

|

|

0.923 |

0.707 |

|

Our company complies with legal regulations in business (corporate law, competition law, consumer protection law, tax management laws, etc) |

LE1 |

0.859 |

|

|

|

Our company complies with recruitment regulations and policies on employee benefits |

LE2 |

0.877 |

|

|

|

In operations, our company adheres to standards and methodologies towards customers |

LE3 |

0.860 |

|

|

|

Our company complies with reporting regulations from relevant authorities |

LE4 |

0.851 |

|

|

|

Our company always adheres to laws and regulations on environmental protection |

LE5 |

0.750 |

|

|

|

CSR towards community |

|

|

0.942 |

0.764 |

|

We have scholarship funds and support funds for the poor |

CO1 |

0.910 |

|

|

|

We always participate in charitable programs and humanitarian blood donation |

CO2 |

0.890 |

|

|

|

We contribute to the development of local infrastructure and facilities |

CO3 |

0.926 |

|

|

|

We sponsor health and community medical projects |

CO4 |

0.886 |

|

|

|

We fulfill all local tax and legal obligations |

CO5 |

0.747 |

|

|

|

CSR implementation behaviors |

|

|

0.922 |

0.746 |

|

The business has an organizational structure (unit) to implement social responsibility |

BEH1 |

0.880 |

|

|

|

Establish criteria for evaluating the implementation of social responsibility |

BEH2 |

0.875 |

|

|

|

Measure the key results of CSR activities |

BEH3 |

0.834 |

|

|

|

Implement corrective and preventive actions |

BEH4 |

0.866 |

|

|

|

Environmental sustainability |

|

|

0.894 |

0.679 |

|

Reduce gas emissions. |

ES1 |

0.830 |

|

|

|

Reduce wastewater. |

ES2 |

0.858 |

|

|

|

Reduce solid waste. |

ES3 |

0.861 |

|

|

|

Reduce the consumption of hazardous ortoxic materials |

ES4 |

0.743 |

|

|

Source: Authors’ calculation. Based on original survey.

Note: CR and AVE stand for composite reliability and average variance extracted.

4.2 Structural model and path analysis

The empirical models estimated using SmartPLS 3 before bootstrapping as in Figure 3. Table 6 and Figure 4 report the effects among constructs based on a bootstrapping analysis with 5,000 resamples. This procedure tests the structural relationships among the model’s variables. The findings indicate that all direct effects from CSR to its components are statistically significant at p < 0.001. Specifically, CSR has significant positive relationships with CSR towards community (H1, β = 0.786, f² = 1.614), employees (H2, β = 0.689, f² = 0.904), ethics (H3, β = 0.765, f² = 1.411), legality (H4, β = 0.795, f² = 1.722) and environmental sustainability (H5, β = 0.589, f² = 0.521). These results confirm that CSR significantly influences all key areas, with medium to large effect sizes, particularly in legality and community-related activities.

In addition, CSR implementation behaviors also show a significant positive impact on environmental sustainability (H6, β = 0.184, p < 0.001), although the effect size is small (f² = 0.049). However, the moderating effect of CSR * Behaviors on environmental sustainability is not statistically significant (H7, β = 0.056, p = 0.231, f² = 0.009), indicating that the interaction does not boost the influence of CSR implementation behaviors on environmental sustainability.

Table 6. Bootstrapping

|

Statistical paths |

Hypothesis |

Original Sample |

Std. Dev |

P Values |

Results |

f2 |

|

CSR -> CO |

H1 |

0.786 |

0.024 |

0.000 |

Supported |

1.614 |

|

CSR -> EM |

H2 |

0.689 |

0.037 |

0.000 |

Supported |

0.904 |

|

CSR -> ET |

H3 |

0.765 |

0.027 |

0.000 |

Supported |

1.411 |

|

CSR -> LE |

H4 |

0.795 |

0.022 |

0.000 |

Supported |

1.722 |

|

CSR -> ES |

H5 |

0.589 |

0.044 |

0.000 |

Supported |

0.521 |

|

CSR implemt-behavior -> ES |

H6 |

0.184 |

0.044 |

0.000 |

Supported |

0.049 |

|

Moderating effect |

|

|

|

|

|

|

|

CSR*Behavior -> ES |

H7 |

0.056 |

0.047 |

0.231 |

Not supported |

0.009 |

|

R-squared |

0.474 |

|

|

|

|

|

|

Adjusted R-squared |

0.471 |

|

|

|

|

|

|

Q-squared |

|

|

|

|

|

|

Source: Bootstrapping analysis with 5,000 samples using SmartPLS.

Note: P < 0.001. CSR, corporate social responsibility; BE, implementation behaviors; EM, CSR towards employees; ET, CSR towards ethics; LE, CSR towards legality; ES, Environmental sustainability; Beha, Moderating Effect CSR*Behaviors.

Figure 3. PLS-SEM path model (SmartPLS 3 output)

Figure 4. Moderating effect of CSR implementation behaviors

Table 7. Correlation among variables

|

CSR |

BE |

CO |

EM |

ET |

LE |

ES |

|

|

CSR |

1 |

||||||

|

BE |

0.458 |

1 |

|||||

|

CO |

0.786 |

0.217 |

1 |

||||

|

EM |

0.689 |

0.516 |

0.370 |

1 |

|||

|

ET |

0.765 |

0.167 |

0.570 |

0.266 |

1 |

||

|

LE |

0.795 |

0.520 |

0.431 |

0.546 |

0.432 |

1 |

|

|

ES |

0.668 |

0.440 |

0.376 |

0.508 |

0.403 |

0.742 |

1 |

Source: Authors’ correlation analysis based on original data.

Note: CSR, corporate social responsibility; BE, implementation behaviors; EM, CSR towards employees; ET, CSR towards ethics; LE, CSR towards legality; ES, Environmental sustainability.

The model explains 47.4% of the variance in environmental sustainability (R² = 0.474), showing a moderate level of explanatory power.

Table 7 also expresses the correlation coefficients among key constructs in the study all less than 0.85. CSR has strong positive correlations with all outcome variables, particularly with legality (LE, r = 0.795), community (CO, r = 0.786) and ethics (ET, r = 0.765). CSR also correlates moderately with environmental sustainability (ES, r = 0.668) and employee-related CSR (EM, r = 0.689). CSR implementation behaviors (BE) show moderate correlations with EM (r = 0.516), LE (r = 0.520) and ES (r = 0.440), but weak correlations with CO and ET.

The relationship between CSR towards employees and overall CSR is significant (β = 0.689, p < 0.001), indicating strong support for the hypothesis. This means that businesses in Vietnam can enhance their overall CSR performance by prioritizing fair compensation, employee development, and inclusive workplace practices. Activities such as listening to employee voices and organizing annual worker conferences also contribute to this improvement. These actions show that employee-related CSR activities play an important role in building responsible and sustainable businesses. This finding is in line with Vuong and Bui [37] who state the dimensions of CSR influence internal and external activities at enterprises in Saigon, Vietnam positively. The results as well indicate that both internal and external CSR activities improve employee satisfaction.

The link between CSR towards legality and overall CSR is strong (β = 0.795, p < 0.001), thus supporting the hypothesis. This recognizes that when companies in the two provinces follow business laws, protect the environment, follow rules for hiring and employee benefits, report to the government and treat customers fairly, their CSR performance improves. Following the law helps businesses build trust and grow in a responsible way. This is aligned with Wang et al. [38] who assert that enterprises’ active fulfillment of social responsibility can reduce the legal risk they face. A well-established corporate governance structure can help enterprises mitigate legal risk.

The relationship between CSR towards community and overall CSR is highly significant, supporting the hypothesis. This shows that when companies give scholarships, support the poor, join charity events, help with local infrastructure, support healthcare and pay local taxes, they improve their CSR performance. These actions show care for the community and help build a positive image for the business. This research echoes the study by Xu and Wang [39] who emphasize that CSR directed toward the community plays a vital role in shaping corporate reputation, enhancing stakeholder engagement and fostering sustainable development across various sectors.

The link between CSR towards ethics and overall CSR is strong (β = 0.765, p < 0.001), so the hypothesis is supported. This means that when companies in Bac Ninh and Bac Giang treat employees fairly, avoid child labor, protect privacy, allow workers to refuse unsafe jobs, follow labor laws and avoid unethical practices, their CSR performance improves. Such ethical practices demonstrate corporate responsibility and foster greater trust among employees and the wider public. This finding is consistent with Zeshan et al. [40], who emphasize that ethical framing of CSR messages resonates positively with stakeholder perceptions in legal-cultural contexts.

The most important finding is that CSR has a significant positive effect on environmental sustainability (H5, β = 0.589, p = 0.000). This means that businesses practicing CSR are more likely to take actions like reducing gas emissions, cutting wastewater, minimizing solid waste and using fewer hazardous materials. For companies operating in the two provinces, this finding emphasizes the importance of CSR in improving environmental practices. Complementing this paper’s finding, the study by Zhang et al. [41] also confirms that state-owned enterprises will significantly increase their level of social responsibility after the implementation of the Paris Agreement. After implementing the Paris Agreement, enterprises in the growth phase will show a more significant increase in social responsibility. Enterprises with sound internal controls will increase their social responsibility more significantly after implementing the Paris Agreement.

On the other hand, the moderating effect of CSR*Behaviors on environmental sustainability is not statistically significant (H7). Although companies do many things to carry out CSR, like having a clear structure, setting goals, checking results and fixing problems, these actions do not make CSR more effective in improving environmental sustainability. The data indicates that the interaction between CSR and implementation behaviors does not significantly enhance environmental sustainability. So, doing CSR well is already good, but doing more of these actions doesn’t make a big difference for the environment in this study.

This study empirically confirms that CSR plays a pivotal role in supporting environmental sustainability, especially in the context of fast-growing industrial regions like Bac Ninh and Bac Giang in Vietnam. By analyzing CSR dimensions—community, employees, ethics, and legal compliance—this research demonstrates that legal adherence and proactive community engagement are key drivers of environmentally responsible behavior among enterprises.

More importantly, the findings highlight the practical relevance of CSR for regional environmental planning and sustainable industrial development. For policymakers and planners, integrating CSR into regional development strategies can help balance economic growth with environmental protection and social responsibility. From a governance perspective, the study suggests that stronger legal frameworks, localized CSR practices, and institutional support are essential to ensuring that corporate activities align with national sustainability goals. The findings are particularly relevant to developing countries undergoing rapid industrialization, where aligning corporate conduct with environmental planning is both urgent and necessary.

6.1 Limitations and future research

While this study provides valuable insights into the relationship between CSR and environmental sustainability in Vietnam’s industrial provinces, several limitations should be acknowledged. First, the research focuses only on two provinces—Bac Ninh and Bac Giang—which may limit the generalizability of the findings to other regions or industries. Second, the use of self-reported data may introduce potential biases due to social desirability or subjective interpretation. Third, the study employs a cross-sectional design, which restricts the ability to infer causality between CSR practices and environmental outcomes.

Future research could address these limitations by expanding the geographic scope to include more provinces or countries with similar development patterns. Longitudinal studies are also encouraged to track changes in CSR implementation over time and their effects on sustainability outcomes. Additionally, incorporating qualitative methods such as interviews or case studies could help deepen the understanding of internal CSR dynamics within firms.

This article was supported by Research on “Solutions to ensure corporate social responsibility implementation by Vietnamese enterprises in the context of Vietnam’s new generation free trade agreements (FTAs)” (Grant No.: KX.01.01/21-30).

Figure A1. Research process flowchart

[1] Ajibike, W.A., Adeleke, A.Q., Mohamad, F., Bamgbade, J.A., Moshood, T.D. (2023). The impacts of social responsibility on the environmental sustainability performance of the Malaysian construction industry. International Journal of Construction Management, 23(5): 780-789. https://doi.org/10.1080/15623599.2021.1929797

[2] Alexiadou, A.S. (2023). Business ethics and corporate social responsibility: Translating theory into action. Contributions to Management Science, Part F1957: 353-377. https://doi.org/10.1007/978-3-031-43785-4_15

[3] An, N.B. (2023). The role of hard law and soft law in developing CSR. Laws on Corporate Social Responsibility and the Developmental Trend in Vietnam, 1-12. https://doi.org/10.1007/978-981-19-9255-1_1

[4] Aslan, Ş., Şendoğdu, A. (2012). The mediating role of corporate social responsibility in ethical leader’s effect on corporate ethical values and behavior. Procedia - Social and Behavioral Sciences, 58: 693-702. https://doi.org/10.1016/J.SBSPRO.2012.09.1047

[5] Becchetti, L., Corrado, G., Pelligra, V., Rossetti, F. (2020). Satisfaction and preferences in a legality social dilemma: Does corporate social responsibility impact consumers’ behaviour? Journal of Policy Modeling, 42(2): 483-502. https://doi.org/10.1016/J.JPOLMOD.2019.07.003

[6] Bhatti, S.H., Iqbal, K., Santoro, G., Rizzato, F. (2022). The impact of corporate social responsibility directed toward employees on contextual performance in the banking sector: A serial model of perceived organizational support and affective organizational commitment. Corporate Social Responsibility and Environmental Management, 29(6): 1980-1994. https://doi.org/10.1002/csr.2295

[7] Carroll, A.B. (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, 34(4): 39-48. https://doi.org/10.1016/0007-6813(91)90005-G

[8] Castro-Casal, C., Vila-Vázquez, G., García-Chas, R. (2024). How and when employees’ attributions of their employers’ CSR activities affect their extra-role work behavior. Business Ethics, the Environment and Responsibility, 34(4): 1399-1411. https://doi.org/10.1111/beer.12719

[9] De Roeck, K., Farooq, O. (2018). Corporate social responsibility and ethical leadership: Investigating their interactive effect on employees’ socially responsible behaviors. Journal of Business Ethics, 151(4): 923-939. https://doi.org/10.1007/s10551-017-3656-6

[10] Fornell, C., Larcker, D.F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Journal of Marketing Research, 18(3): 382. https://doi.org/10.2307/3150980

[11] Freeman, R.E. (2010). Strategic Management: A Stakeholder Approach. Cambridge University press.

[12] Gainet, C. (2010). Exploring the impact of legal systems and financial structure on corporate responsibility. Journal of Business Ethics, 95: 195-222. https://doi.org/10.1007/s10551-011-0854-5

[13] Geng, L., Cui, X., Nazir, R., Binh An, N. (2022). How do CSR and perceived ethics enhance corporate reputation and product innovativeness? Economic Research-Ekonomska Istraživanja, 35(1): 5131-5149. https://doi.org/10.1080/1331677X.2021.2023604

[14] Hair, J.F., Howard, M.C., Nitzl, C. (2020). Assessing measurement model quality in PLS-SEM using confirmatory composite analysis. Journal of Business Research, 109: 101-110. https://doi.org/10.1016/J.JBUSRES.2019.11.069

[15] Hair Jr., J.F., da Silva Gabriel, M.L.D., Patel, V.K. (2014). Modelagem de equações estruturais baseada em covariância (CB-SEM) com o AMOS: Orientações sobre a sua aplicação como uma ferramenta de pesquisa de marketing. Revista Brasileira de Marketing, 13(2): 44-55. https://doi.org/10.5585/remark.v13i2.2718

[16] Ho, S.S.H., Oh, C.H., Shapiro, D. (2024). Can corporate social responsibility lead to social license? A sentiment and emotion analysis. Journal of Management Studies, 61(2): 445-476. https://doi.org/10.1111/JOMS.12863

[17] Ho, S.S.M., Li, A.Y., Tam, K., Tong, J.Y. (2016). Ethical image, corporate social responsibility, and R&D valuation. Pacific-Basin Finance Journal, 40: 335-348. https://doi.org/10.1016/J.PACFIN.2016.02.002

[18] Kanwal, S., Al Mamun, A., Wu, M., Bhatti, S.M., Ali, M.H. (2024). Corporate social responsibility: A driver for green organizational climate and workplace pro-environmental behavior. Heliyon, 10(19): e38987. https://doi.org/10.1016/J.HELIYON.2024.E38987

[19] Khuong, M.N., Truong an, N.K., Thanh Hang, T.T. (2021). Stakeholders and corporate social responsibility (CSR) programme as key sustainable development strategies to promote corporate reputation—Evidence from Vietnam. Cogent Business and Management, 8(1): 1917333. https://doi.org/10.1080/23311975.2021.1917333

[20] Kraus, S., Rehman, S.U., García, F.J.S. (2020). Corporate social responsibility and environmental performance: The mediating role of environmental strategy and green innovation. Technological Forecasting and Social Change, 160: 120262. https://doi.org/10.1016/J.TECHFORE.2020.120262

[21] Li, Z., Cao, J. (2025). Enhancing green total factor productivity through corporate social responsibility: The moderating effect of environmental regulations. Finance Research Letters, 71: 106466. https://doi.org/10.1016/J.FRL.2024.106466

[22] Lin, Y.T., Liu, N.C., Lin, J.W. (2022). Firms’ adoption of CSR initiatives and employees’ organizational commitment: Organizational CSR climate and employees’ CSR-induced attributions as mediators. Journal of Business Research, 140: 626-637. https://doi.org/10.1016/J.JBUSRES.2021.11.028

[23] Liu, B., Sun, P.Y., Zeng, Y. (2020). Employee-related corporate social responsibilities and corporate innovation: Evidence from China. International Review of Economics & Finance, 70: 357-372. https://doi.org/10.1016/J.IREF.2020.07.008

[24] Malinauskaite, J., Jouhara, H. (2024). Corporate social responsibility (CSR) and environmental, social and governance (ESG). In Introduction to sustainable business models. Sustainable Energy Technology, Business Models, and Policies. Elsevier, pp. 41-66. https://doi.org/10.1016/B978-0-443-18454-3.00010-2

[25] Mubushar, M., Rasool, S., Haider, M.I., Cerchione, R. (2021). The impact of corporate social responsibility activities on stakeholders’ value co-creation behaviour. Corporate Social Responsibility and Environmental Management, 28(6): 1906-1920. https://doi.org/10.1002/CSR.2168

[26] Muliati, M., Totanan, C., Jamaluddin, Pattawe, A., Iqbal, M., Mile, Y., Mayapada, A.G. (2024). Enhancing SME green performance: The role of environmental and social responsibility programs and environmental dynamism. International Journal of Sustainable Development and Planning, 19(2): 799-806. https://doi.org/10.18280/ijsdp.190238

[27] Nejati, M., Shafaei, A. (2023). Why do employees respond differently to corporate social responsibility? A study of substantive and symbolic corporate social responsibility. Corporate Social Responsibility and Environmental Management, 30(4): 2066-2080. https://doi.org/10.1002/CSR.2474

[28] Newman, C., Rand, J., Tarp, F., Trifkovic, N. (2020). Corporate social responsibility in a competitive business environment. The Journal of Development Studies, 56(8): 1455-1472. https://doi.org/10.1080/00220388.2019.1694144

[29] Ong, M., Mayer, D.M., Tost, L.P., Wellman, N. (2018). When corporate social responsibility motivates employee citizenship behavior: The sensitizing role of task significance. Organizational Behavior and Human Decision Processes, 144: 44-59. https://doi.org/10.1016/J.OBHDP.2017.09.006

[30] Schaefer, S.D., Cunningham, P., Diehl, S., Terlutter, R. (2024). Employees’ positive perceptions of corporate social responsibility create beneficial outcomes for firms and their employees: Organizational pride as a mediator. Corporate Social Responsibility and Environmental Management, 31(3): 2574-2587. https://doi.org/10.1002/CSR.2699

[31] Shahzad, M., Qu, Y., Javed, S.A., Zafar, A.U., Rehman, S.U. (2020a). Relation of environment sustainability to CSR and green innovation: A case of Pakistani manufacturing industry. Journal of Cleaner Production, 253: 119938. https://doi.org/10.1016/j.jclepro.2019.119938

[32] Sharma-Nepal, S., Isce-Taylor, L. (2020). The legal basis of CSR. In The Palgrave Handbook of Corporate Social Responsibility. Springer International Publishing, pp. 1-59. https://doi.org/10.1007/978-3-030-22438-7_77-1

[33] Sheehy, B., Khan, H.Z., Prananingtyas, P., Sophiana Sunarso Putri, P. (2023). Shifting from soft to hard law: Motivating compliance when enacting mandatory corporate social responsibility. European Business Organization Law Review, 24(4): 693-719. https://doi.org/10.1007/s40804-023-00284-4

[34] Subramaniam, R.K., Samuel, S.D., Seera, M., Alam, N. (2024). Utilising machine learning for corporate social responsibility (CSR) and environmental, social, and governance (ESG) evaluation: Transitioning from committees to climate. Sustainable Futures, 8: 100329. https://doi.org/10.1016/J.SFTR.2024.100329

[35] Tiep, L.T., Huan, N.Q., Hong, T.T.T. (2021). Effects of corporate social responsibility on SMEs’ performance in emerging market. Cogent Business & Management, 8(1): 1878978. https://doi.org/10.1080/23311975.2021.1878978

[36] Tran, N.M., Do, T.M.A., Bui, N.P. (2025). Do environmental or social initiatives benefit banks more? Evidence from Vietnam’s banking sector. International Journal of Sustainable Development and Planning, 20(3): 1265-1272. https://doi.org/10.18280/ijsdp.200331

[37] Vuong, T.K., Bui, H.M. (2023). The role of corporate social responsibility activities in employees’ perception of brand reputation and brand equity. Case Studies in Chemical and Environmental Engineering, 7: 100313. https://doi.org/10.1016/J.CSCEE.2023.100313

[38] Wang, H., Wang, L., Huang, D. (2025). Can corporate social responsibility and corporate governance structure reduce corporate legal risk? Finance Research Letters, 73: 106598. https://doi.org/10.1016/J.FRL.2024.106598

[39] Xu, H., Wang, Q. (2024). Energy regulatory compliance and corporate social responsibility. Finance Research Letters, 67: 105919. https://doi.org/10.1016/J.FRL.2024.105919

[40] Zeshan, M., Rasool, S., Cerchione, R., Centobelli, P., Morelli, M. (2024). The impact of digitalization on CSR commitment: The role of human resource management system and employee autonomy. Corporate Social Responsibility and Environmental Management, 32(2): 1618-1630. https://doi.org/10.1002/CSR.3021

[41] Zhang, J., Islam, M.S., Jambulingam, M., Lim, W.M., Kumar, S. (2024). Leveraging environmental corporate social responsibility to promote green purchases: The case of new energy vehicles in the era of sustainable development. Journal of Cleaner Production, 434: 139988. https://doi.org/10.1016/J.JCLEPRO.2023.139988