Remzi Smajli![]() | Nakije Kida*

| Nakije Kida*![]() | Julinda Morina

| Julinda Morina![]() | Vesa Morina

| Vesa Morina![]() | Florije Miftari

| Florije Miftari![]() | Medain Hashani

| Medain Hashani![]() | Albana Pasjaqa

| Albana Pasjaqa![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study aims to analyze the impact of key economic factors on the motivation of foreign investors in Kosovo, focusing on indicators such as exchange rate (ER), inflation (INF), interest rates (IR), access to credit (AC), competition (CO), banking services and e-banking (E-BBS), economic growth (EGr), and taxes (Tax). Primary data were collected through a structured questionnaire randomly distributed to a sample of 148 foreign investors. The reliability and validity of the data were assessed through statistical tests such as Cronbach’s Alpha, KMO and Bartlett’s Test, as well as Principal Component Analysis (PCA) and Collinearity Statistics. For data analysis, multiple linear regression and Kendall’s Tau-b analysis were applied using the SPSS 25 statistical software package. The findings highlight that Economic Growth, strongest positive impact (B=6.497, p<0.001), indicating that GDP growth enhances investor confidence. ER, significant positive effect (B=2.584, p =0.009), highlighting the importance of currency stability. INF Rate, notable positive influence (B=2.734, p=0.019), suggesting that predictable INF is acceptable to investors. AC, strong negative effect (B=-5.575, p<0.001), emphasizing that limited credit access deters investment. IR, marginal negative impact (B=-3.144, p=0.055), implying that higher IR may reduce investment motivation. The model explains 30.8% of the variability in investor motivation, implying that other factors also deserve further analysis. Kendall’s tau-b analysis confirms a strong correlation between ER and AC with investor motivation, while IR and banking services show a weak correlation. In line with Dunning’s theory, location advantages–such as the ER and economic growth–play a vital role in attracting investments, while internalization advantages – such as AC–also contribute significantly. This research challenges traditional views by revealing a positive relationship between INF and foreign direct investment (FDI), offering new perspectives for policymakers. It recommends focusing on ER stability, improving AC, and undertaking structural reforms as mechanisms for boosting foreign investment in Kosovo. The original contribution of this study lies in identifying a positive link between INF and FDI, as well as highlighting less-studied factors such as ER and credit access as key elements. Additionally, it emphasizes the impact of competition and banking services, the challenges to economic growth, and the role of structural reforms and fiscal incentives in attracting new investors.

FDI, external economic environment, PCA test, modedel OLS, Kendall's Tau-b, Kosovo

Foreign direct investment (FDI) represents a fundamental pillar of the globalization process, having experienced significant growth in recent decades due to technological advancements and the liberalization of capital markets worldwide. FDI is widely regarded as a key mechanism of international capital movement, contributing to economic development, fostering integration into regional and global markets, and enhancing the competitive advantages of host countries.

This study employs Dunning's Eclectic Paradigm (the OLI framework) to analyze FDI decision-making, focusing on three core advantages that multinational enterprises (MNEs) must possess to invest abroad: Ownership (O), Location (L), and Internalization (I) advantages. Specifically, the study examines location-specific factors such as inflation stability, tax policies, and banking infrastructure, which align with the “L” component of the OLI model and highlight Kosovo’s potential to attract foreign investors.

Hymer [1], a pioneer in the theory of multinational enterprises, argued that firms engage in foreign investment primarily to reduce local competition and exploit firm-specific advantages abroad. While Hymer [1] emphasized competitive motivations; Dunning [2, 3] expanded the theoretical framework by introducing a more structured model that combines ownership, location, and internalization advantages to explain the strategic decisions of MNEs in international markets. According to the OLI paradigm, the presence of all three advantages is essential for successful FDI.

However, the theoretical foundations of FDI extend even further. Buckley [4] pointed out that the modern theory of multinational firms originates from Hymer's doctoral dissertation, completed in 1960 and published in 1979. Nevertheless, earlier contributions from scholars such as Coase [5], Kaldor [6], and Robinson [7] laid important groundwork for this field. Hymer’s work was also significantly influenced by Dunning and Rugman [8], while more recent perspectives including those of Buckley [4] have expanded the scope to a broader theory of the firm, positioning MNEs as a specific form within that larger framework.

In the modern context, Buckley [9] emphasizes that FDI remains a core strategy for multinational corporations to ensure global competitiveness. However, recent developments have introduced new challenges. According to UNCTAD [10], global FDI fell by 2% in 2023, reaching $1.3 trillion, largely due to economic slowdowns and rising geopolitical tensions. When excluding temporary fluctuations in certain European economies, the decline exceeds 10%. Investments in Sustainable Development Goal (SDG)-related sectors, particularly agriculture, food, and water, dropped by more than 10%. The report suggests that improved business facilitation and digital government solutions could enhance transparency and efficiency in the investment environment.

At the national level, Kosovo exhibits similar trends. In 2023, Kosovo's current account deficit narrowed to 7.7% of GDP, down from 10.3% in 2022, driven by a reduced goods trade deficit and an improved balance in services. However, net FDI inflows slightly decreased to 6.5% of GDP, while portfolio investments recorded net outflows [11]. Although Kosovo has experienced an average GDP growth rate of 4% over the past two decades, FDI inflows remain modest. This underscores the need for stronger investment promotion efforts and institutional reforms to better position Kosovo within the global FDI landscape [11].

Kosovo has undergone a complex economic transition, facing significant challenges throughout this process. However, international support and domestic policies have played a crucial role in improving the investment climate, particularly for FDI. Although progress has been made, Kosovo must continue to address regional competition, bureaucratic obstacles, and structural weaknesses to ensure sustainable economic growth through foreign investment.

According to the Central Bank of Kosovo [12], from 2007 to September 30, 2024, total FDI inflows in Kosovo amounted to €6,897.2 million, of which equity capital accounted for €5,925.4 million and debt instruments €913.3 million. Germany and Switzerland are the main contributors to FDI in Kosovo, with each investing over €1 billion, mainly in the real estate, financial services, and energy sectors. Other sectors such as Information and Communication Technology (ICT), infrastructure, and renewable energy also show potential for future investments. Meanwhile, FDI outflows from Kosovo have also impacted the economy, reaching €1,105.4 million, with Albania as the main recipient, followed by Germany and EU countries. Additionally, portfolio investments during this period reached €3,218.6 million, of which €2,427.6 million were in equity and investment fund shares, while €791 million were in debt instruments. In 2023 alone, Kosovo's net FDI inflows reached €816 million, marking an increase compared to the previous year [12].

Kosovo maintains a positive balance of FDI, with more inflows than outflows, creating opportunities for economic growth and the strengthening of key sectors. However, the current level of investment remains insufficient to close the capital gap, which is a central issue of this study. Therefore, attracting more foreign investment is essential for long-term development and for diversifying funding sources.

To this end, Kosovo has established a strong legal and institutional framework to attract foreign investors. The foundation of this framework lies in continuous legal reforms, including Law No. 04/L-220 on Foreign Investment, which guarantees national treatment for foreign investors in nearly all sectors [13]. In addition, Law No. 05/L-079 on Strategic Investments supports FDI by streamlining administrative procedures and providing incentives for foreign companies [14, 15]. The most recent law, Law No. 08/L-209 on Sustainable Investments, adopted in 2024, further strengthens the legal basis for attracting and protecting foreign capita [16].

These legal measures are supported by institutions such as the Kosovo Investment and Enterprise Support Agency (KIESA), whose mandate includes promoting investment, developing exports, supporting SMEs, and advancing Economic Zones [17]. In addition, the Inter-ministerial Commission for Strategic Investments and the European Investors Council in Kosovo, established in 2014, play an active role in enhancing the investment climate [18-20].

Furthermore, Kosovo has signed several key international agreements that improve its investment climate. The Stabilization and Association Agreement (SAA) with the European Union supports regulatory harmonization and economic cooperation [21, 22], while membership in CEFTA strengthens regional trade integration [23]. Additionally, double taxation avoidance agreements with several countries (Albania, Austria, Belgium, Croatia, Finland, Germany, Hungary, Ireland, Latvia, Lithuania, Luxembourg, Malta, Netherlands, North Macedonia, Saudi Arabia, Slovenia, Switzerland, Turkey, United Arab Emirates (UAE), United Kingdom (UK) create more favorable conditions for cross-border investments [24]. According to the U.S. Department of State [25], double taxation avoidance agreements with several countries create more favorable conditions for cross-border investments in Kosovo.

These efforts, together with public consultation platforms and the development of digital government solutions, make Kosovo an increasingly attractive destination for foreign investors [26].

This study applies Dunning’s Eclectic Paradigm, focusing on location-specific factors like inflation stability, taxation policies, and banking infrastructure that influence investment decisions in Kosovo. The research highlights Kosovo's potential to attract FDI and suggests future studies refine the paradigm to better reflect the evolving investment climate. Using structured questionnaires, the study gathers insights from randomly selected foreign investors across Kosovo ARBK [27].

The analysis examines the impact of variables such as exchange rates (ER), INF, interest rates (IR), access to credit (AC), and banking services on FDI. The research aims to answer two key questions:

a) Does economic stability positively affect foreign investors’ motivation in Kosovo?

b) Is there a significant correlation between economic stability and foreign investors' motivation?

These questions are addressed through two hypotheses tested using Multiple Linear Regression (MLR) to evaluate the impact of economic factors on FDI. Additionally, Kendall's Tau-b correlation coefficient analyzes the complex relationships between these factors and FDI growth in Kosovo. The study incorporates factors such as ERs, INF, IR, credit access, competition, banking services, economic growth, and taxation.

Analyzing Key Economic Factors Shaping FDI in Kosovo:

Together, these studies underline the relevance of these economic indicators in shaping Kosovo's investment climate. They provide a theoretical and empirical foundation for understanding how external capital interacts with local economic structures.

The findings of this study aim to inform policymakers, businesses, and civil society on strategies to strengthen Kosovo's economic competitiveness and attract sustainable foreign investment. The structure of the study is as follows: Section two presents the literature review, Section three outlines the methodology, Section four discusses the results, and Section five concludes with policy recommendations.

FDI is a form of investment where a foreign company or individual invests directly in a business or asset located in another country, taking control or at least a significant stake in the management of the business and this investment may include purchasing shares in a foreign company, establishing subsidiaries, or purchasing real estate and other activities that require direct involvement and commitment in the management of the business [43].

In this paper, the main theories related to the influence of macroeconomic factors on FDI include several concepts and authors who have contributed to the development of these theories. Dunning's theory [2], known as the Eclectic Paradigm or OLI, mentions three key advantages that a firm must have to invest abroad: Ownership Advantage (O), Location Advantage (L), and Internalization Advantage (I). Dunning emphasizes the importance of location factors such as INF, tax policies, and banking infrastructure that play an important role in attracting FDI, thus supporting investors' demands for a stable economic and institutional environment.

Hymer's theory [1] focuses on the competitive advantages of international firms, arguing that they invest in foreign markets to avoid local competition and to exploit advantages that cannot be realized in domestic markets. He emphasizes that foreign investment is driven by the desire to create dominant positions in international markets.

This study draws on Dunning's Eclectic Paradigm (OLI framework) to examine FDI decisions, emphasizing location-specific factors such as inflation stability, taxation policies, and banking infrastructure. These factors align with the paradigm's location advantages, showcasing Kosovo's potential to attract foreign investors.

Dunning and Hymer are two important figures in the development of the multinational enterprise (MNE) theory and have contributed to the understanding of the factors that drive the growth and international expansion of these firms.

Hymer was one of the pioneers in the theory of multinational firms. He argued that firms operating in international markets possess unique advantages, such as the ability to avoid local competition and create a dominant position. He mentioned that MNEs are motivated to invest abroad in order to spread their competitive advantages and escape from the limitations and competition of local markets [1].

Hymer's theoretical framework (Table 1) emphasizes the significance of market imperfections, firm-specific advantages, and barriers to internationalization. The variables in the study align closely with these theoretical aspects, providing a clear context for understanding the motivations of foreign investors.

Table 1. Hymer's theoretical framework and its connection to the variables in your study on the motivation of foreign investors in Kosovo

|

Theoretical Aspect by Hymer |

Description |

Connection to Study Variables |

|

Market Imperfections |

Hymer argues that firms invest abroad to avoid competition and exploit firm-specific advantages. |

CO: Your study analyzes how competition in the local market impacts the motivation of foreign investors. |

|

Firm-Specific Advantages |

Firms with specific advantages (e.g., technology, managerial skills) use these to succeed in foreign markets. |

Economic Growth (EGr): Kosovo's growing economy may serve as a pull factor for foreign investors. |

|

Barriers to Market Internationalization |

Firms invest directly to avoid transaction costs and uncertainties in international markets. |

IR: High interest rates can act as barriers for investors, influencing their decisions. |

|

Access to Local Resources |

Investors seek direct access to markets and local resources to maximize profits. |

AC: The ability to secure credit in Kosovo is a critical factor for investors' decisions. |

|

Avoidance of Domestic Competition |

Investors enter foreign markets to avoid competition in their domestic market. |

Taxes (Tax): Tax policies in Kosovo may make the market more attractive to investors seeking to avoid domestic constraints. |

|

Impact of Macroeconomic Uncertainty |

Economic and political stability in a country influences FDI flows. |

INF: Price stability in Kosovo impacts investor confidence and their motivation to invest. |

Dunning [2, 3, 44, 45] introduced the Eclectic Paradigm (OLI Theory), combining prior theories to explain why MNEs invest abroad:

- Ownership Advantage (O): Competitive assets like technology, brand, or human capital.

- Location Advantage (L): Host-country benefits like low labor costs, market access, or favorable policies.

Table 2 presents Dunning's theoretical framework (OLI paradigm) and its connection to the study variables, illustrating how ownership, location, and internalization advantages influence the motivation of foreign investors in Kosovo.

Table 2. Dunning's theoretical framework (OLI paradigm) and its connection to the variables in the study

|

Dunning's Theoretical Framework (OLI Paradigm) Dunning's (1977, 1980, 2000, 2015) |

Description |

Connection to Study Variables |

|

Ownership Advantages (O) |

Firm-specific assets such as technology, managerial skills, brand reputation, and innovation. |

Economic Growth (EGr): Investors are motivated by Kosovo's growing market potential to utilize their ownership advantages. |

|

Location Advantages (L) |

Advantages related to the host country, such as market size, infrastructure, tax incentives, and labor cost. |

Taxes (Tax): Favorable tax policies attract investors to Kosovo. CO: Investors assess competitive conditions in Kosovo. |

|

Internalization Advantages (I) |

Firms prefer to internalize operations to reduce transaction costs, protect proprietary knowledge, and improve efficiency. |

IR: High interest rates may discourage externalization, encouraging firms to operate internally. AC: The availability of credit is a key factor influencing internalization decisions. |

|

Market Opportunities |

Potential for market growth and access to regional and global markets. |

INF: Price stability ensures better market opportunities for foreign. investors. E-Banking and Banking Services (E-BBS): Reliable banking systems improve market efficiency. |

- Internalization Advantage (I): Direct control over operations to avoid risks like IP theft or inefficiencies in outsourcing.

The OLI framework highlights that MNEs need all three advantages to succeed internationally. While Hymer emphasized competitive advantages, Dunning created a structured model to explain FDI motivations and strategic decisions. Study Alignment with OLI Framework Dunning [2, 3, 44-46]:

- Ownership (O): Highlights the firm-specific advantages that foreign investors bring to Kosovo, such as expertise and technology.

- Location (L): Emphasizes Kosovo’s attractiveness as an investment destination, influenced by factors like tax policies and competitive conditions.

- Internalization (I): Explains how foreign investors aim to maximize efficiency by internalizing operations, which is affected by access to credit and interest rates.

The table effectively aligns Dunning’s OLI framework with the specific variables in study to explain the motivation of foreign investors in Kosovo.

The integration of the following studies within Dunning's OLI paradigm underscores the multifaceted nature of FDI decisions, emphasizing the significance of a favorable environment in attracting FDI. This theoretical lens enhances the relevance of Dunning’s framework, particularly for emerging economies like Kosovo, by highlighting critical determinants such as ownership advantages, location-specific factors, and internalization incentives.

Institutional theories, including those proposed by Globerman and Shapiro [47] and North [48], stress the necessity of political and economic stability for attracting FDI. A robust institutional environment mitigates risk and fosters investor confidence. These insights align with findings by Blomström et al. [49, 50], and Borensztein et al. [51], who assert that FDI promotes economic development through the transfer of technology, knowledge spillovers, and the enhancement of human capital.

Macroeconomic theories concerning exchange and interest rates further contribute to our understanding of FDI inflows. Aizenman and Noy [52] argue that ER volatility discourages FDI due to increased uncertainty. Conversely, Edwards [53] and Hermes and Lensink [54] note that a developed financial system and lower IR can facilitate FDI by easing access to capital and supporting technology diffusion.

Building on the foundational work of Coase [5], who introduced transaction cost theory to explain firm behavior, Buckley and Hashai [55] refined these ideas through a general equilibrium model that integrates ownership, location, and internalization advantages—the pillars of Dunning’s paradigm. These contributions laid the groundwork for Hymer’s and Dunning’s theories on multinational enterprises (MNEs), which explore why firms internationalize and how they navigate cross-border operations.

Cantwell and Narula [56] highlight the complementary perspectives of Hymer, who focused on firm-specific competitive advantages, and Dunning, who emphasized cost efficiencies and development opportunities. Narula [57] later warned that the eclectic paradigm risks becoming tautological without a unifying framework, proposing a streamlined version (“EP-lite”) to preserve theoretical clarity.

Despite its widespread application, the eclectic paradigm has been critiqued for a lack of cumulative theoretical development. Wagner [58], through a comprehensive review of 66 studies from 1980 to 2017, illustrated its evolution into a complex interdisciplinary model, while also identifying the need for methodological consistency in future research. Other empirical applications, such as Brouthers et al. [59], demonstrate that even small and medium service firms, like U.S. software companies, follow patterns predicted by Dunning’s theory.

Emerging Market Multinational Enterprises (EMNEs) present additional challenges to traditional FDI theories. Nayyar [60] emphasized the role of state [61] critiques attempts to radically redefine FDI frameworks, advocating for better theoretical alignment rather than wholesale replacements. Similarly, Gaur and Kumar [62] call for new models to explain the distinct paths of EMNEs compared to developed market firms.

Other contributions provide sector-specific and context-specific insights. For instance, Teixeira and Heyuan [63] demonstrated how university-industry linkages in China enhance FDI, while Pitelis and Teece [64] introduced orchestration theory to explain how dynamic capabilities influence MNE behavior.

Recent empirical studies further reinforce these theoretical claims. Bénassy-Quéré et al. [65] found that corruption, weak institutions, and labor protections inhibit FDI, while stronger legal and financial systems foster investment. Erlina and Sitorus [66] confirmed the negative impact of corruption, whereas GDP remains a consistent positive determinant. Meanwhile, Khan et al. [67] highlighted how political instability deters FDI in Pakistan, but trade openness and GDP growth can offset these effects.

ER continue to play a critical role in FDI dynamics. Madaki et al. [68] have shown that foreign ER fluctuations significantly affect economic growth, while other factors like IR and INF have weaker effects. Desai et al. [69] added that high corporate tax rates reduce profitability and capital investment in foreign affiliates, although indirect taxes have less influence.

These diverse theoretical and empirical contributions collectively demonstrate that FDI is shaped by a complex interplay of macroeconomic variables, institutional quality, and firm-specific strategies. In the context of Kosovo, applying the eclectic paradigm helps clarify how factors such as political stability, favorable tax regimes, ER predictability, and AC influence foreign investment decisions. While Dunning’s paradigm remains central, evolving global conditions and the rise of EMNEs suggest a need for continual refinement and contextual adaptation of these theoretical models.

This study presents an empirical quantitative analysis based on primary data, aimed at examining the views of foreign investors on how economic factors influence their decisions to invest in Kosovo. It spans the period from 2018 to 2023, focusing on the experiences of foreign investors who began their operations in Kosovo in 2018 and are still active. This period allows for the evaluation of shifts in investor opinions over time.

Data for this study were collected using a structured Likert scale survey, targeting foreign companies selected at random from all sectors of Kosovo's economy. Between 2018 and 2023, 460 companies were registered, of which 233 remained active, while the rest were closed. Using the YAMANE automatic formula a sample size of 148 companies was determined (https://statsmartly.com/Pop/Yamane.php/#).

Data collection occurred in two phases: the first phase involved gathering 52 surveys from October to December 2024 via email and direct contact. In January 2025, the second phase saw the collection of 96 surveys from investors who preferred face-to-face interaction. The questionnaire was pre-tested to ensure clarity, comprehensibility, and reliability, as well as to identify and correct any issues or ambiguities before it was fully deployed in the study. In addition to the survey data, supplementary information was obtained from annual reports of the Central Bank of Kosovo [70], the Kosovo Agency of Statistics [71], the Kosovo Business Registration Agency [72], the Kosovo Tax Administration [73], official publications from the Ministry of Industry, Entrepreneurship and Trade of Kosovo [74], and both local and international research.

Econometric methods were employed to analyze the data, including descriptive statistical analysis to assess foreign investors' confidence in relation to economic factors (ER, INF, IR, AC, CO, banking services, economic growth, and taxation). Correlation analysis was used to examine the relationships between FDI and economic indicators, as well as the interconnection between independent variables. Regression analysis was applied to evaluate the statistical significance of the impact of these independent variables on foreign investors' motivation.

Here is the connection between the study variables and the theories of Hymer and Dunning, including the model used, tests applied, and the key authors referenced in the analysis of multinational enterprise theory:

The results were interpreted by comparing them with previous studies on foreign investment and economic stability, focusing on factors such as ER volatility, tax incentives, interest rate stability, economic growth, INF, competitiveness between foreign and domestic firms, and AC. This comparison helped assess the motivation of current foreign investors and their potential impact on attracting future investors to Kosovo. Data for the study was sourced from the Statistics Agency of Kosovo, (ASK) and the Tax Administration of Kosovo (ATK). The sample size was determined using [75] formula and [76] method to ensure representativeness. The survey included companies from all sectors, with a focus on large and medium-sized firms, and was stratified by region (with higher concentration in Pristina and Ferizaj). Companies were selected randomly within these sectors and regions.

The data collected through the structured questionnaire were processed and subsequently standardized using the Z-score method prior to performing the MLR analysis. Although all items were originally measured on a uniform 7-point Likert scale (ranging from 1 to 7), standardization was conducted to ensure comparability across variables and to minimize the potential influence of different value magnitudes on the regression results.

Table 3 provides a comprehensive overview of the study's theoretical and methodological framework. The research adopts a quantitative design using structured questionnaires distributed randomly to foreign companies in Kosovo, with a sample size of 148 out of 233 identified firms. Two main hypotheses and related research questions guide the investigation of economic variables influencing FDI motivation. Data were analyzed using statistical tests such as Kendall's Tau-b, Cronbach's Alpha, ANOVA, KMO, and PCA through SPSS software. The framework is grounded in Hymer's and Dunning's theories, integrating key contributions from recent scholarly literature to support the validity and relevance of the study's approach.

Table 3. Overview of the research framework and methodological approach

|

Component |

Description |

|

Research Design |

Quantitative research using primary data collected through a structured questionnaire targeting foreign companies in Kosovo. |

|

Structured Questionnaire |

The questionnaire is designed to collect primary quantitative data, which is gathered randomly from foreign companies in Kosovo. |

|

Sample and Population |

The sample consists of 233 foreign companies, while the total population (sampling frame) includes 148 foreign companies. |

|

Hypotheses |

H1: "ER, INF, IR, AC, CO, e-banking and banking services (E-BBS), economic growth (EGr), and taxes (Tax) have a positive and statistically significant impact on the return of the motivation of foreign investors in Kosovo." |

|

|

H2: "There is a positive and statistically significant correlation among ER, INF, IR, AC, CO, e-banking and banking services (E-BBS), economic growth (EGr), and taxes (Tax) with the motivation of foreign investors in Kosovo." |

|

Research Questions |

i) Does economic stability have a positive and statistically significant impact on the return of the motivation of foreign investors in Kosovo? |

|

|

ii) Is there a positive and statistically significant correlation between economic stability and the motivation of foreign investors in Kosovo? |

|

Data Collection |

Primary data was collected from 148 foreign companies (sample) operating in Kosovo through a structured questionnaire. |

|

Tests Applied |

Kendall's Tau b: Measures the strength and direction of relationships between variables. |

|

|

Cronbach’s Alpha: Evaluates internal consistency and reliability of the data collected. |

|

|

ANOVA with Friedman's Test: Detects differences between related samples. |

|

|

KMO and Bartlett's Test: Assesses data suitability for factor analysis. |

|

|

Principal Component Analysis (PCA): Reduces data dimensionality while retaining key information for analysis. |

|

Statistical Software |

SPSS, 25 software will be used for data analysis. |

|

Refs. |

[1-4, 8, 9, 32, 33, 36, 37, 39-41, 43-45, 47, 49, 50, 53-58, 60, 79] |

The analysis employed standardized variables (denoted by the prefix "Z”), which represent transformed versions of the original variables with a mean of 0 and a standard deviation of 1. This standardization approach contributed to the robustness of the statistical analysis and allowed for a clearer interpretation of the relative weight of each predictor variable within the regression model.

Standardization of variables is considered an important step in regression and multivariate analysis to ensure comparability of coefficients and eliminate scale-related bias [77].

Standardizing variables before conducting linear regression enhances the interpretability of coefficients and simplifies calculations, as it involves transforming each variable by subtracting its sample mean and dividing by its standard deviation, resulting in variables with a mean of zero and a standard deviation of one [78].

The confidence level in the sample size calculation was determined using Yamane's formula, based on a population of 233 companies and a 5% margin of error [75]:

$n=\frac{\mathrm{N}}{1+N e^2}$ (1)

where, n = sample size needed; N = population size (total number of individuals or units); e = margin of error (acceptable error level, e.g., 0.05 for 5%).

$\begin{gathered}n=\frac{233}{1+233 \times(0.05)^2}=\frac{233}{1+233 \times 0.0025}=\frac{233}{1+0.5825}=\frac{233}{1.5825} \approx 147.2\end{gathered}$ (2)

So, the sample size ≈147, which rounds to 148.

The Yamane formula [75] assumes a normal distribution for interpreting perceptions of required and applied skills in practice, making it an appropriate method for sample size determination. In this study, the total population of active foreign companies in Kosovo is N=233, and the calculated sample size is n=148. A 95% confidence level was applied, with an assumed population proportion p=0.5.

The calculation follows the procedure described in Yamane [75].

Figure 1. Sample selection flowchart

Also expressed in Figure 1, the sample selection flowchart clearly outlines the three-step process, identifying the target population of foreign investors, the total population size (N = 233), and the final sample size (n = 148), ensuring a representative and reliable dataset for analysis.

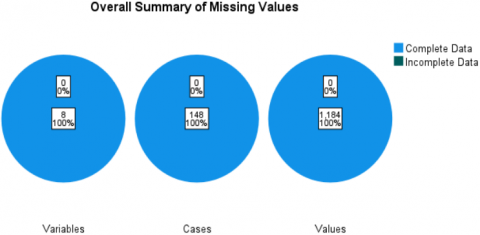

Figure 2. Overall summary of missing values

In this case, a sample of 148 companies is sufficient to draw reliable conclusions for the population of 233 companies in Kosovo. Figure 2 shows that there were no missing responses in any of the 148 surveys.

The data used in this study are cross-sectional in nature, collected through a structured questionnaire over a four-month period. Initially, 52 questionnaires were tested and the results were published. Subsequently, 96 more surveys were collected in January 2025, bringing the total to 148 surveys from foreign companies in Kosovo. The sample consists of 233 active companies for the period 2018-2023 (the period 2018-2023 was specified for convenience in locating them, as access to data is very difficult due to confidentiality concerns from the tax office). A Likert scale was used to measure their opinions regarding the impact of economic factors on the increase or decrease in motivation among foreign investors operating in Kosovo. The data were collected only once from each company. There are no repeated measurements for the same company across different time periods. The four-month data collection period does not classify the data as time series but as cross-sectional (also highlighted are the tests that should be used), as the goal was to include as many companies as possible within a single period, rather than to observe changes over time.

The realization of the study was made possible through a structured questionnaire consisting of 16 questions independent variable and 8 questions and dependent variables on a Likert scale [80]: (1 (Very Negative), 2 (Negative), 3 (Somewhat Negative), 4 (Neutral), 5 (Somewhat Positive), 6 (Positive), 7 (Very Positive).

Before testing, the Likert scale responses were standardized in order to generate the output from SPSS. For the dependent variable of the study and the independent variables, PCA was used to reduce the variables that do not have significance in assessing the motivation of investors. Similarly, PCA was applied to the independent variables to retain only those variables that contribute meaningfully to the model, ensuring that any errors during calculation were minimized.

In this research, a) the “Dependent variable” associated with the hypothesis is the "Motive of Foreign Investors", denoted by the symbol (MFI) which consists of 16 variables which, through the PCA test, have been reduced to 6 components that most motivate foreign investors: (Motivation for Starting a Business in Kosovo: Easy access to local markets; Size of the available market; Availability of workforce; Availability of natural resources; Low CO in the market; Low cost of doing business; Easy access to market information; Healthy economic policies; Poor business environment in Kosovo; Government support for export promotion; Simple government regulations for foreign businesses; Simple regulations for imports; Influence from friends and family members; encouragement from local businesses in Kosovo; The culture of the Albanian people; FDI from other markets).

The formula is a way to calculate the MFI_index that measures the motivation of foreign investors in Kosovo, by combining ratings and weights for 16 economic variables.

Then, the MFI Index would be:

$M F I_{\text {index }}=\frac{1}{n} \sum_{i=0}^n \text { Rating of } \text { Factor }_i$ (3)

where, n is the number of factors (in this case, 16); Rating of Factori is the rating for each individual factor, scored from 1 to 7.

$\begin{aligned} & M F I_{{index }} =\frac{1}{16} \sum_{i=0}^n\left(\frac{\left(\begin{array}{c}\text { Weight1 } * \text { Rating1 }+\ldots \\ + \text { Weight16 } \\ * \text { Rating16 }\end{array}\right)}{(\text { Weight1 }+\ldots+\text { Weight16 })}\right)\end{aligned}$ (4)

where,

- Ratingi: The score given to the i-th variable (e.g., political stability, infrastructure, tax policy, etc.).

- Weighti: The importance (weight) assigned to the i-th variable (how significant each variable is to foreign investors).

- 16: Indicates that there are 16 economic variables being considered PCA (PCA- is used to reduce variables (dimensionality). From 16 variables, PCA extracts several principal components (1, 2, 3, 4, 5, 6 or more) that represent the majority of the information. PCA eliminates multicollinearity: if some variables are strongly correlated with each other, PCA combines them without repetition. It creates an objective index: instead of assigning subjective weights to the variables, PCA automatically generates weights based on the variance of the data. This test was applied separately to the dependent variable, which is represented by 16 variables, and it was also repeated for the independent variables, which include 8 variables, in order to reduce them to 3 or 4 components that best represent the economic environment in Kosovo).

- The inner part (in parentheses): This is a weighted average of the ratings for all 16 variables, where each rating is multiplied by its respective importance (weight).

- The summation ∑ from i=1 to n: Represents the total number of respondents or cases (for example, how many investors filled out the questionnaire).

- The 1/16 factor: This seems to be an additional normalization, but depending on the structure of the formula, it might not be necessary here if you’re already averaging across respondents.

Economic factors are measured on a Likert scale the factors: ER, INF, IR, AC, CO, E-Banking and Banking Services (E-BBS), Economic Growth (EGr), and Taxes (TAX).

The Hypotheses Study:

H1: ER, INF, IR, AC, CO, e-banking and banking services (E-BBS), economic growth (EGr), and taxes (Tax) have a positive and statistically significant impact on the return of the motivation of foreign investors in Kosovo.

H2: There is a positive and statistically significant correlation among ER, INF, IR, AC, CO, e-banking and banking services (E-BBS), economic growth (EGr), and taxes (Tax) with the motivation of foreign investors in Kosovo. To ensure reliable results, tests were performed prior to inferential statistics and hypothesis testing. Descriptive statistical tools were used to calculate the mean and standard deviation, summarizing key data trends.

Descriptive analysis of questionnaire variables begins with the weighted arithmetic mean.

The arithmetic mean is calculated as follows, Eqs. (3) and (5) [81]:

$x_i=\frac{\text { Upper class limit }+ \text { Lower class limit }}{2}$ (5)

and,

Mean $=\overline{\mathrm{x}}=\frac{\sum \mathrm{f} i x i}{\mathrm{f} i}$ (6)

After using variance as an absolute indicator of deviation, the analysis also applies the Sample Standard Deviation formula to measure the dispersion of variables. This method is calculated using a standard formula widely recognized in statistical literature [81].

Eq. (7) shows quantities that are multiplied by their respective weights, summed, and then divided by the total weight, followed by the calculation of the standard deviation.

$\sigma=\sqrt{\frac{\left.\sum(\mathrm{xi} \,\overline{\mathrm{x}})^2\right)}{n-1}}$ (7)

σ =Standard Deviation; xi = terms given in the data; x̄ = mean; n = total number of term.

Test Reliability refers to the extent to which a test is free from measurement error. The greater the measurement error, the less reliable the test becomes [75]. In our study, Cronbach's Alpha is used to assess the reliability of the survey, particularly for the group of 20 questions (variables) in sections 2 and 3 of the questionnaire (see Table 3). Cronbach’s Alpha is a statistical measure that evaluates the internal consistency of multiple Likert-type questions within a survey. Developed by Cronbach [76], this reliability test gauges how well the items in a scale are related to one another and if they measure the same underlying construct. According to UEDUFI [82], Cronbach's Alpha indicates the degree to which scale items correlate with each other as a group. The formula for Cronbach’s Alpha is presented by Bonett and Wright [83]:

$a=\left(\frac{K}{K-1}\right)+\frac{S y^2-S u m S i^2}{S y^2}$ (8)

where, α=Cronbach's Alpha; K=the number of items in the scale; Si=the sum of the item scores for the each item; S=the sum of the total scores for all items.

Friedman's Test [84], is a non-parametric alternative to repeated measures ANOVA, used when data is ordinal or not normally distributed. It tests if there are differences in ranks across related groups or conditions. The test statistic is calculated based on ranks, and the formula is:

$\chi^2=\frac{12}{n k(k+1)}=\sum_{j=1}^k R^2-3 n(k+1)$ (9)

Developed by Friedman [85], it's useful when assumptions of normality are violated, particularly for repeated measures or ranked data.

- The Kaiser-Meyer-Olkin (KMO) Test and Bartlett's Test of Sphericity are statistical tests used to assess the suitability of data for factor analysis.

KMO Test, Kaiser [86]: Measures the sampling adequacy for factor analysis. A high KMO value (close to 1) indicates that factor analysis is appropriate, while a low value (below 0.5) suggests it is not.

KMO Formul:

$K M O=\frac{\sum_{i \sum_j} R_{i j}^2}{\sum_{i \sum_j} R_{i j}^2+\sum_{i \sum_j} S_{i j}^2}$ (10)

where, Rij is the correlation coefficient and Sij is the partial correlation.

- Bartlett's Test [87]: Tests whether the correlation matrix is an identity matrix (i.e., no correlations between variables). A significant result (p<0.05) indicates that factor analysis is appropriate.

Bartlett Formula:

$X^2=\left(\mathrm{N}-1-\frac{2 p+5}{6}\right) \cdot \ln |\mathrm{R}|-\frac{1}{2} \cdot(2 \mathrm{p}+5)$ (11)

where, N is the sample size, p is the number of variables, and R is the correlation matrix.

Both tests help determine whether the data is suitable for factor analysis.

PCA [88] is a statistical technique used to reduce the dimensionality of data while preserving its essential variance. It transforms correlated variables into uncorrelated principal components that capture the maximum variance in the dataset. PCA is widely used for dimensionality reduction, feature extraction, and data visualization, making complex datasets easier to analyze and interpret [89]. It helps in improving processing efficiency and identifying patterns within data. The method is based on the calculation of eigenvectors and eigenvalues from the covariance or correlation matrix:

The principal components are derived using the formula [89, 90]:

$X=V L^{1 / 2}$ (12)

where, X, principal components (transformed data); V: Eigenvectors (matrix of loadings); L, matrix of eigenvectors (directions of components).

$V \sqrt{L}$, represents the transformation used to derive principal components ($L^{1 / 2}$ square root of the diagonal matrix of eigenvalues (variance explained by each component). The formula $X = V L^{1 / 2}$ means that to obtain the principal components, you multiply the eigenvectors by the square root of the eigenvalues.

Kendall's Tau_b [91], is an alternative method for measuring bivariate correlation, especially suitable for ordinal or categorical data. It is a variant of the rank correlation coefficient that accounts for ties (when two or more observations have the same rank). Kendall's Tau-b is particularly effective when the data exhibits non-linear relationships or when dealing with ordinal variables, such as investor preferences or market conditions.

In the context of this study, Second Hypothesis (H2) seeks to determine whether there are significant and strong relationships between the dependent variable, MFI, and the independent variables (ER, INF, IR, AC, CO, E-BBS, EGr, and Tax). To assess these relationships, Kendall's Tau B is employed as a nonparametric correlation coefficient. This method measures both the strength and direction of the relationship between two ordinal or interval variables [92]. Kendall's Tau_b [91] is particularly useful when the data does not adhere to a normal distribution or when the sample size is small, as is the case with the 148 investor cases in this study. This makes Kendall's Tau B more appropriate than parametric tests. The Tau B coefficient is computed using the following formula [91]:

Kendall's Tau_b $=\frac{(D-D)}{\sqrt{\left(C+D+T_X\right) *\left(C+D+T_Y\right)}}$ (13)

where, C is the number of concordant pairs (where one variable increases when the other increases), D is the number of discordant pairs (where one variable increases and the other decreases), and TX and TY are the numbers of equalities in each variable. In addition, τb takes values from -1 (perfect negative relationship) to +1 (perfect positive relationship), with 0 indicating no relationship. A statistically significant value indicates that the variables have a statistically valid relationship.

For H1, this method can answer the following questions:

The first hypothesis (H1) aims to determine whether the independent variables—ER, INF, IR, AC, CO, E-Banking and Banking Services (E-BBS), Economic Growth (EGr), and Taxes (Tax)—have a positive and statistically significant impact on the dependent variable, Motivation of Foreign Investors (MFI). According to Gujarati and Porter [93], the concept of regression was first introduced by Francis Galton in 1892 as part of his studies on heredity. It is a method used to examine the relationship between a response variable (Y) and a covariate (X), where Y represents the dependent variable and X represents the independent variable. In essence, regression seeks to understand how changes in the independent variable affect the dependent variable and reveals the average quantitative relationship between two or more phenomena. Linear regression (LR) is a foundational predictive analysis tool that helps explore functional relationships between variables. One variable is treated as explanatory, while the other is treated as dependent. The analysis begins with Simple Linear Regression (SLR), expressed in Eq. (13), and MLR in Eq. (14). As discussed by Gujarati and Porter [93] and other scholars, these regression models provide a structured framework for understanding the relationships between variables and for making predictions based on these relationships.

Y = a + bx (14)

where, a and b are given by the following formulas:

$a({ intercept })=\frac{\sum y \sum x^2-\sum x \sum x y}{\left(\sum x^2\right)-\left(\sum x\right)^2}$ (15)

and,

$b( slope)=\frac{n \sum x y-\left(\sum x\right)\left(\sum y\right)}{n \sum x^2-\left(\sum x\right)^2}$ (16)

In this equation, x and y represent the two variables along the regression line; b is the slope of the line, a is the y-intercept, x corresponds to the values from the first dataset, and y corresponds to the values from the second dataset.

The Equation of the Theoretical Model of MLR:

$Y=\beta_0+\beta_1 \mathrm{X}_1+\beta_2 \mathrm{X}_2+\beta_3 \mathrm{X}_3+\ldots+\beta \mathrm{pXp}+\varepsilon$ (17)

Y: Represents the response variable;

β0: Denotes the y-intercept;

β1: Represents the average change in Y resulting from a one-unit increase in Xj, while keeping all other predictors constant;

X1: Indicates the first predictor variable;

ε: Represents the error term.

The coefficients β0, β1, β2, …, βp are estimated using the Least Squares Method, which aims to minimize the Residual Sum of Squares (RSS).

The Residual Sum of Squares (RSS) is determined by summing the squared differences between the actual response values (yi) and the predicted values (ŷi) from the MLR model.

RSS $=\Sigma\left(\mathrm{y}_{\mathrm{i}}-\hat{\mathrm{y}}_{\mathrm{i}}\right)^2$ (18)

where, Σ represents the summation; yi is the observed value for each data point, and ŷi is the corresponding predicted value.

The F distribution with degrees of freedom is used for regression.

dfR = k (19)

where, dfR = degrees of freedom for regression, k = number of independent variables (predictors) in the model.

The F-distribution is used to test the overall significance of the regression model. The degrees of freedom for regression (dfR) equal the number of predictors (k), while the degrees of freedom for error (dfE) are calculated as the total number of observations minus the number of predictors and the intercept, i.e., dfE = n − k − 1.

A right-tailed ANOVA test is then applied to determine whether the variation explained by the regression model is greater than the variation caused by error. The main components of the ANOVA table include the test statistic and the p-value, which indicate the statistical significance of the model. In contrast, the t-test focuses on evaluating whether a specific variable (β1) significantly influences the prediction of the dependent variable (y), rather than assessing the overall regression model.

$\mathrm{t}_{\mathrm{n}-\mathrm{k}}=\frac{\mathrm{b} 1}{\text { Std error of b1 }}$ (20)

and, Std error of b1:

$\left(\mathrm{Sb}_1\right)=\frac{\sqrt{\mathrm{MSE}}}{\sqrt{(X-X)^2}}$ (21)

This model helps assess the influence of independent variables on the dependent variable, offering a clearer insight into how these relationships might impact the study's outcomes.

The analysis was processed with SPSS 25 to extract results.

To assess the influence of independent variables on the dependent variable (MFI) and examine the relationships between variables, a series of estimation steps were followed. Initially, a descriptive statistical analysis was performed to summarize the main features of the data. Next, demographic analysis was carried out, with the study data being visualized through graphs to emphasize key demographic characteristics. Subsequently, diagnostic tests were conducted to verify the reliability and suitability of the data, ensuring that valid statistical conclusions could be drawn. Following this, Kendall's Tau-b analysis was employed to measure the relationships between variables. Finally, MLR analysis was applied to estimate the structural equation model and assess the impact of the independent variables on the dependent variable (MFI).

4.1 Descriptive statistics

Key statistical measures (Table 4), including the number of observations, mean, standard deviation, Skewness and Kurtosis, were calculated for each variable: To identify the most suitable variables for analyzing the motivation of foreign investors in Kosovo, several aspects of descriptive statistics are considered. Stability and Reliability: Variables with lower variability, such as interest rate (SD: 0.891), AC/loans (SD: 1.073), and taxes (SD: 1.058), are more stable and reliable for analysis. Response Distribution: AC/loans and interest rate have lower skewness and are closer to a normal distribution, indicating a more consistent perception among investors. Investor Perception: Variables with higher averages, such as AC/loans (6.07) and investor motivation (25.84), show a positive perception and significant impact.

Table 4. Descriptive statistics

|

|

N |

Mean |

Std. Deviation (SD) |

Skewness |

Kurtosis |

||

|

Statistic |

Statistic |

Statistic |

Statistic |

Std. Error |

Statistic |

Std. Error |

|

|

Motive for foreign investors |

148 |

25.84 |

13.067 |

-.603 |

.199 |

-.880 |

.396 |

|

ER |

148 |

4.43 |

1.910 |

-.684 |

.199 |

-1.222 |

.396 |

|

INF |

148 |

3.97 |

1.154 |

.107 |

.199 |

-1.411 |

.396 |

|

IR |

148 |

5.45 |

.891 |

-.792 |

.199 |

.721 |

.396 |

|

AC |

148 |

6.07 |

1.073 |

-.939 |

.199 |

-.398 |

.396 |

|

CO |

148 |

4.63 |

1.907 |

-.570 |

.199 |

-1.088 |

.396 |

|

E-banking and banking services EBBS |

148 |

4.10 |

1.465 |

-.165 |

.199 |

-1.247 |

.396 |

|

Economic growth EGr |

148 |

5.00 |

1.119 |

-.739 |

.199 |

-.005 |

.396 |

|

Taxes Tax |

148 |

5.87 |

1.058 |

-.648 |

.199 |

-.633 |

.396 |

|

Valid N (listwise) |

148 |

|

|

|

|

|

|

Negative Kurtosis: Variables such as ER, INF, and E-BBS exhibit a flatter distribution, requiring further analysis. Interest rate, access to credit/loans, and taxes are the most reliable variables, while investor motivation remains a key factor.

4.2 Demographic statistics

FDI and other variables are presented in graphical and tabular form below.

Based on data from the Central Bank of Kosovo (CBK) for the period from January to September 2024 (Figure 3), FDI reached €657.3 million, marking an increase of €38.5 million or approximately 6.2% compared to the same period in 2023. However, compared to previous years, there is a decline in the annual growth trend.

Figure 3. FDI by year (millions of euros) and annual increase/decrease in %

According to data from January to September 2024 (Figure 4), FDI continue to be predominantly dominated by real estate activities, accounting for 71.4%, followed by financial and insurance activities at 14.9%. The remaining 13.7% consists of other sectors, including construction at 1.6%, manufacturing at 1.5%, mining and quarries at 1.4%, wholesale and retail trade, motor vehicle repair, and motorcycle repair at 1.3%, among others. Motivation of foreign investors in Kosovo.

Figure 4. FDIs by year and economic activities in %

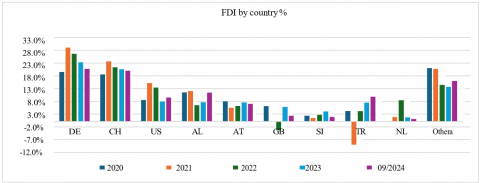

According to analysis by country of origin, the leading investors in Kosovo are from the EU 27 (Figure 5). FDI in Kosovo by country (net) for the period from January to September 2024 are as follows: Germany 20.8%, Switzerland 20.0%, the USA 9.5%, Albania 11.4%, Austria 7.0%, the United Kingdom 2.3%, among others, representing their share in total FDI.

Figure 6. Motive of investors and the performance of economic factor's

The opinion of foreign investors on economic factors is presented in the created Figure 6.

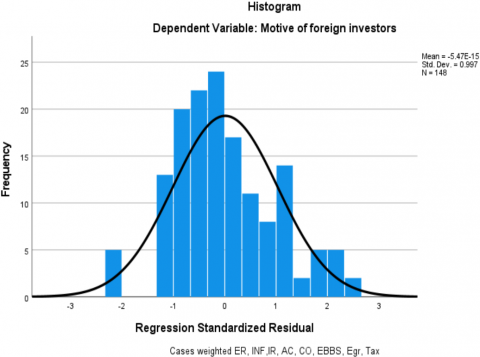

The results presented in Figure 6, based on the statistical analysis of the motives of foreign investors, suggest that although various economic factors such as ER, INF, IR, AC, CO, e-banking and banking services, economic growth, and taxes are related to these motives, their impact is moderate in this sample. The low mean and standard deviation indicate that the data distribution is compact, with low variability among the data values.

This may imply that the analyzed factors do not have a high impact on the motives of foreign investors. To better understand the potential impacts, it may be necessary to apply more advanced statistical methods or consider additional factors that were not included in this analysis.

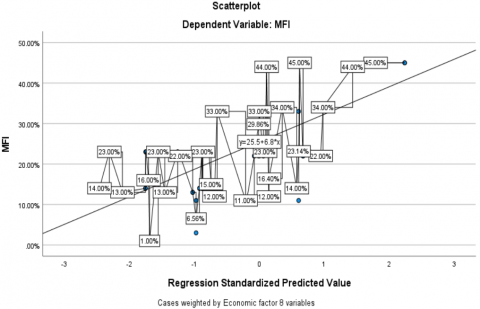

Figure 7. The impact of 8 independent variables on the dependent variable MFI

Figure 7 presents the results of the linear regression analysis, indicating that economic factors influence the motivation of foreign investors to invest in Kosovo. The regression equation Y=25.5+6.8X reveals a positive relationship between the economic variables and investor motivation. The R² value of 45% suggests that 45% of the variation in investor motivation can be explained by these economic factors. The scatter plot displays the distribution of motivation based on the predicted values. To boost investments, it is recommended to improve economic conditions, particularly by enhancing AC and stabilizing ER.

4.3 Statistical tests

To create the motivation index (Dependent variable), data from the components PCA have been used, and the formulas and calculations for each of the 6 components we extracted were processed. The loadings for each variable in the components have been used and multiplied by the weights provided.

4.3.1 Testing dependent variables

Calculations, Cronbach's Alpha, KMO test and PCA for each component Dependent variable MFI (See: This part was not included in the article due to the volume of words that were added too much):

a) A Cronbach's Alpha (Table 5)

Value of 0.849 indicates that the 16 items in the foreign investor motivation index demonstrate high internal consistency and reliably measure the same underlying construct.

Table 5. Reliability statistics-MFI

|

Cronbach's Alpha |

N of Items |

|

.849 |

16 |

b) KMO and Bartlett's Test (Table 6)

With a KMO Table 6 value of 0.745: The sample is suitable for factor analysis, because the value falls into the "good" category. However, Bartlett's Test of Sphericity is statistically significant (p<.001), which means that the correlations between items are sufficient to proceed with factor analysis.

Table 6. KMO and Bartlett's test-MFI

|

Kaiser-Meyer-Olkin Measure of Sampling Adequacy |

.745 |

|

|

Bartlett's Test of Sphericity |

Approx. Chi-Square |

792.107 |

|

df |

120 |

|

|

Sig. |

.000 |

|

c) Tests PCA-MFI

Table 7. Component matrixa

|

Variable |

Component |

|||||

|

1 |

2 |

3 |

4 |

5 |

6 |

|

|

Investors' Motive |

-.761 |

.316 |

-.174 |

-.143 |

-.075 |

.178 |

|

Easy Access to Local Markets |

.149 |

.679 |

.287 |

.034 |

-.193 |

.274 |

|

Demonstrated Size of Investment |

-.557 |

.119 |

-.088 |

.410 |

.447 |

-.133 |

|

Availability of Labor |

.146 |

-.337 |

.514 |

-.167 |

-.584 |

.074 |

|

Availability of Natural Resources |

-.668 |

-.337 |

.181 |

.057 |

.243 |

.151 |

|

Low Market Competition |

.566 |

.523 |

.065 |

.070 |

.257 |

-.148 |

|

Low Cost of Doing Business |

.465 |

.002 |

-.545 |

-.560 |

.104 |

-.016 |

|

Ease of Access to Market Information |

-.064 |

.266 |

-.283 |

.579 |

-.601 |

-.069 |

|

Sound Economic Policies |

-.374 |

.618 |

-.100 |

.386 |

.079 |

.074 |

|

Weak Business Environment in Kosovo |

.424 |

.544 |

.352 |

-.232 |

.247 |

.081 |

|

Government Cares for Export Promotion Initiatives |

.299 |

.061 |

-.050 |

.095 |

-.093 |

.795 |

|

Simple Government Regulations for Foreign Businesses |

.289 |

-.552 |

-.233 |

.383 |

-.149 |

-.134 |

|

Simple Import Regulations |

.199 |

-.019 |

.702 |

.352 |

.084 |

-.001 |

|

Influence from Friends and Family Members |

-.166 |

.337 |

.451 |

-.199 |

-.242 |

-.534 |

|

Encouragement from Kosovar Businesses |

.741 |

.054 |

.101 |

.329 |

.259 |

-.033 |

|

Culture of the Albanian People |

.041 |

-.712 |

.393 |

.114 |

.255 |

.132 |

|

FDI from Other Markets |

.709 |

-.084 |

-.338 |

.265 |

-.038 |

-.110 |

|

Extraction Method: PCA. |

||||||

|

a. 6 components extracted. |

||||||

Table 7 identifies which variables contribute most to each of the 6 main components, with the aim of building a common index that measures the motivation of foreign investors in Kosovo.

Summary of Key Components

-Component 1 – Local Support and Positive Climate:

Positive: Support from Kosovar businesses, FDI from other markets, low CO.

Negative: Personal motive for investment, natural resources. Reflects the influence of the supportive local climate on motivation.

- Component 2 – Institutional Access and Local Market:

Positive: Access to local markets, economic policy, business environment.

Negative: Albanian culture, regulations for foreign businesses. Indicates the importance of institutional structures and perception of the environment.

- Component 3 – Regulatory Framework and Social Impact:

Positive: Import regulations, labor force, family impact. Reflects regulatory ease and social impacts on decision-making.

- Component 4 – Access to Information and Market Size:

Positively: Market information, market size, government regulations

Assess easy access to information and the size of opportunities.

- Component 5 – Cost and Benefit:

Positively: Size of investment, low competition.

Negatively: Labor force, market information. Measures the balance between cost and benefit in investment.

- Component 6 – Institutional Support:

Positively: Government care for exports.

Negatively: Influence from family/friends. Related to the role and trust in the government in attracting investment.

These components were then used to calculate the overall investor motivation index, based on their scores and the weight of each factor. This approach has also been applied previously [94] demonstrating the importance of PCA testing in reducing insignificant variables

The result of the main components (component scores) calculated based on the average ratings and the matrix of components:

The Component Transformation Matrix (Table 8), for MFI shows the correlations between the original factors and the newly extracted factors after applying Varimax rotation. High positive loadings (e.g., 0.860 for Component 1) indicate a strong relationship between the original variable and the new component. Negative values (e.g., -0.177 for Component 2 on Component 1) suggest an inverse correlation. The matrix helps to identify which components are strongly associated with each extracted factor, providing clearer interpretation of the data. The use of PCA and Varimax rotation makes it easier to understand the underlying dimensions of the data by maximizing variance explained per component.

Table 8. Component transformation matrix-MFI

|

Component |

1 |

2 |

3 |

4 |

5 |

6 |

|

1 |

.860 |

.148 |

.330 |

-.306 |

.150 |

-.119 |

|

2 |

-.177 |

.724 |

.478 |

.085 |

-.333 |

.312 |

|

3 |

.143 |

-.540 |

.514 |

.536 |

-.032 |

.367 |

|

4 |

.023 |

.369 |

-.097 |

.519 |

.764 |

-.021 |

|

5 |

-.399 |

-.155 |

.421 |

-.563 |

.529 |

.206 |

|

6 |

.222 |

.035 |

-.459 |

-.158 |

.048 |

.843 |

|

Extraction Method: PCA. Rotation Method: Varimax with Kaiser Normalization. |

||||||

Component 1: Low market competition; Easy access to local markets; Component 2: Healthy economic policies; Weak business environment in Kosovo; Component 3: Availability of labor force; Simple import regulations; Component 4:Ease of access to market information; Simple government regulations for foreign businesses; Component 5: Market size available; Availability of natural resources; Component 6: Government care for export promotion initiatives.

This index represents a summary of the influence of each component on motivation, considering the loadings of the respective variables and the weights we assigned.

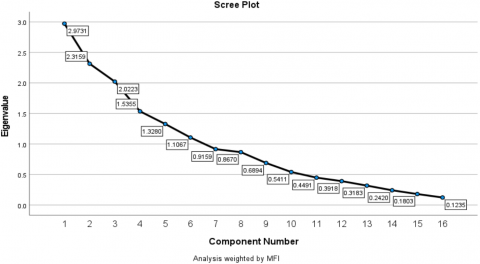

A scree plot is used to visualize the results of a PCA and helps in determining the number of components that should be retained in the model (Figure 8). This plot shows the eigenvalues (the amount of variance explained) for each component and typically uses a "Kaiser criterion" to decide the optimal number of components. In a scree plot, components with an eigenvalue greater than 1 are considered significant and should be retained, while those with an eigenvalue less than 1 can be excluded.

Figure 8. Screen plot-the reduced variables with the most impact on investor motivation

MFI Index based on these 16 factors, we can use a simple weighted sum formula or an average-based approach, depending on how you want to weigh the factors. No, there is no need for standardization to create an index with the average of Likert scales (when the variables are on the same Likert scale). Using the mean of Likert data, where each value has the same importance across all questions, is sufficient to obtain an overall summary without the need for standardization of variables. In addition to using PCA for the independent variables, it should be noted that PCA was used (also for the dependent variable since it is represented by 16 variables to identify the main factors that measured the motivation of foreign investors in Kosovo), then an index was created based on these components, with the weights resulting from PCA. Furthermore, further validation is always necessary, internal consistency (Cronbach's Alpha) to verify that the components are reliable, which has been done.

Formula for the Index: If we assume equal weights for each factor (which is common when there are no specific reasons to assign different weights), the formula for the MFI Index would be:

This will give you an average score for all the factors, which can be interpreted as the overall MFI Index.

Table 9. Using weights from PCA

|

No. |

Variable |

Rating |

Weight from PCA |

Rating×Weight |

|

1 |

Easy access to local markets |

5 |

0.149 |

0.745 |

|

2 |

Size of the available market (Demonstrated Size) |

6 |

-0.557 |

-3.342 |

|

3 |

Availability of workforce (Labor) |

4 |

0.146 |

0.584 |

|

4 |

Availability of natural resources |

6 |

-0.668 |

-4.008 |

|

5 |

Low competition in the market |

5 |

0.566 |

2.830 |

|

6 |

Low cost of doing business |

7 |

0.465 |

3.255 |

|

7 |

Easy access to market information |

6 |

-0.064 |

-0.384 |

|

8 |

Healthy economic policies |

4 |

-0.374 |

-1.496 |

|

9 |

Poor business environment in Kosovo |

3 |

0.424 |

1.272 |

|

10 |

Government support for export promotion |

6 |

0.299 |

1.794 |

|

11 |

Simple gov. regulations for foreign businesses |

5 |

0.289 |

1.445 |

|

12 |

Simple regulations for imports |

4 |

0.199 |

0.796 |

|

13 |

Influence from friends and family members |

7 |

-0.166 |

-1.162 |

|

14 |

Encouragement from local businesses in Kosovo |

6 |

0.741 |

4.446 |

|

15 |

Culture of the Albanian people |

5 |

0.041 |

0.205 |

|

16 |

FDI from other markets |

6 |

0.709 |

4.254 |

|

|

Total |

|

|

10.564 |

Table 9 presents the key factors influencing the motivation of foreign investors in Kosovo, where each factor is assigned a rating by respondents and a weight obtained from Principal Component Analysis (PCA). By multiplying each rating by its corresponding PCA weight and summing these weighted scores, a total value of 10.564 is obtained.

- Formula for Motivation of Foreign Investors (FDI) Index

Applying this to your factors:

$\begin{aligned} M F I_{ {index }}=\frac{1}{16} \sum_{i=0}^n & \text { (Easy access to local markets + ... } + \text { Rating of FDI from other markets }+\ldots+\text { ) }\end{aligned}$ (22)

The Motivation of Foreign Investors Index (MFI_index) formula then divides this total by the number of factors (n=16) to calculate the average motivation score:

$\begin{aligned} & M F I_{ {index }} \\ & =\frac{1}{n} \sum_{i=0}^n\left(\frac{\binom{\text { Weight PCA1 } * \text { Rating } 1+\ldots}{+ \text { WeightPCA16 } * \text { Rating } 16}}{(\text { Weight } 1+\ldots+\text { Weight } 16)}\right)=\frac{10.564}{16}=5.11\end{aligned}$ (23)

Final result: MFI Index=5.11 (This result indicates a relatively high level of investor motivation in relation to local support, positive business climate, and economic factors).

In summary, using PCA-derived weights assigns statistical significance to each factor rather than relying solely on subjective ratings, resulting in a more reliable and objective measure of investor motivation.

This value was transferred to SPSS 25 to the dependent variable MFI.

4.3.2 Testing independent variables

Statistical tests are essential for assessing data reliability, validity, Cronbach's Alpha evaluates internal consistency and reliability. ANOVA with Friedman’s Test is used to detect differences between related samples, and KMO and Bartlett's Test assess data suitability for factor analysis. Lastly, PCA reduces data dimensionality while retaining key information for analysis.

a) The Cronbach's alpha coefficient (CORR) test

Table 10, Reliability assessed by looking at the mean, standard deviation, and sample size. Mean: Both variables (MFI and Economic Factors) show positive evaluations, with means around 4.5 and 5, suggesting favorable opinions from respondents. Standard Deviation: The small standard deviations (0.25923 and 0.28588) indicate consistent responses, with little variation and a high level of agreement. Sample Size: A sample size of 148 is sufficient for reliable analysis and allows for generalization of the results.

Table 10. Item statistic

|

|

Item Statistic Mean |

Std. Deviation |

N |

|

Investors' Motive Foreign (MFI) (The missing variable index (MFI) is specified in the additional annex.) |

4.5107 |

.25923 |

148.00 |

|

Economic Factors |

5.0312 |

.28588 |

148.00 |

Instrument Reliability Analysis (Reliability Statistics) Table 11: To assess the reliability of the questionnaire used in this study, Cronbach's Alpha coefficient was applied, which measures the internal consistency of a group of items that are supposed to measure the same theoretical construct.

Table 11. Reliability instrumental statistics (Cronbach’s alpha test)

|

Cronbach's Alpha |

Cronbach's Alpha Based on Standardized Items |

N of Items |

|

.769 |

.787 |

9 |

The Cronbach's Alpha value=.769 indicates a good level of reliability, as in the literature values above .70 are considered acceptable for research analysis [75]. The Alpha value based on standardized items (.787) is slightly higher, which indicates that standardization of items may have slightly increased uniformity among them. The number of items included in the analysis is 9, which is an adequate number for a simple factorial structure.

Based on these values, the instrument used to measure factors affecting foreign investment in Kosovo shows a good degree of internal consistency and is suitable for use in further statistical analyses.

b) ANOVA with Friedman's Test

Table 12. ANOVA with Friedman's test

|

|

Sum of Squares |

df |

Mean Square |

Friedman's Chi-Square |

Sig |

|

|

Between People |

12.434 |

147 |

.085 |

|

|

|

|

Within People |

Between Items |

20.054a |

1 |

20.054 |

100.568 |

.000 |

|

Residual |

9.458 |

147 |

.064 |

|

|

|

|

Total |

29.513 |

148 |

.199 |

|

|

|

|

Total |

41.947 |

295 |

.142 |

|

|

|

Grand Mean=4.7710

a. Kendall's coefficient of concordance W= .478.

Table 12 presents the results of Friedman's ANOVA test.

Key points: Friedman's Chi-Square=100.568, p=0.000: There is a statistically significant difference between the items. Kendall's W=0.478: Indicates a moderate level of agreement among participants on how they rank the items.

Grand Mean=4.7710: The overall average score across all items. The results show that the items differ significantly, with moderate agreement in rankings among respondents.

c) Factor Analysis-KMO and Bartlett's Test

The Kaiser-Meyer-Olkin (KMO) Measure of Sampling Adequacy is a test developed by Kaiser [95] in 1970. This test is used to assess the suitability of data for factor analysis. Kaiser [95] was a psychologist and statistician who contributed to the development of statistical techniques, and one of his most well-known contributions is the development of this index to evaluate the adequacy of a sample for factor analysis.

Factor Analysis Results Interpretation:

i) Kaiser-Meyer-Olkin (KMO) Measure of Sampling Adequacy

The KMO (Table 13) value is 0.707, which indicates a moderate level of sampling adequacy. A KMO value between 0.5 and 0.7 is considered acceptable, suggesting that the data is suitable for factor analysis, but there may still be some room for improvement.

Table 13. KMO and Bartlett's test

|

Kaiser-Meyer-Olkin Measure of Sampling Adequacy. |

.707 |

|

|

Bartlett's Test of Sphericity |

Approx. Chi-Square |

732.42 |

|

df |

36 |

|

|

Sig. |

.000 |

|

ii) Bartlett's Test of Sphericity

The Chi-Square (Table 13), value is 732.42 with 36 degrees of freedom (df), and the Sig. value is 0.000. This result is statistically significant (p<0.05), meaning that the correlation matrix is not an identity matrix, and there are sufficient correlations among variables to perform factor analysis.

c) PCA tests

Table 14 indicates how much of the variance in each variable is explained by the extracted factors. Variables with high communalities, such as the ER (0.849) and CO (0.801), are strongly related to the factors.

In contrast, the tax variable has a lower communality (0.551), indicating a weaker relationship with the factors. This suggests that the extracted factors adequately describe the data for most of the variables.

Table 14. Communalities

|

|

Initial |

Extraction |

|

Foreign investor motivation-MFI |

1.000 |

.710 |

|

ER |

1.000 |

.849 |

|

Inflation rate-INF |

1.000 |

.645 |

|

Interest rate-IR |

1.000 |

.754 |

|

AC |

1.000 |

.648 |

|

CO |

1.000 |

.801 |

|

E-banking and banking system services-EBBSS |

1.000 |

.793 |

|

Economic growth-Egr |

1.000 |

.740 |

|

Taxes-Tax |

1.000 |

.551 |

|

Extraction Method: PCA. |

||

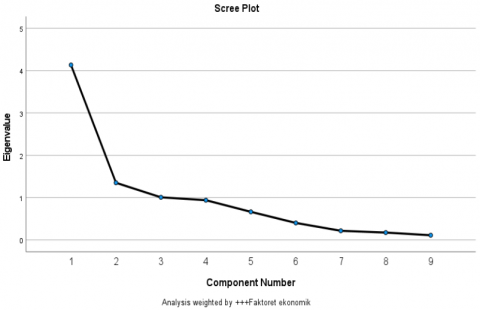

Table 15 presents the variance explained by each component in PCA, used by Kida et al. [96], originally introduced by Hotelling [97]. The first three components explain 73.09% of the total variance, suggesting that they are the most important factors in understanding the data. The remaining components (4-9) explain a smaller portion of the variance, indicating they have less influence on the overall data structure. The rotation process redistributed the variance explained by each component, but the overall variance explained by the three key components remained the same. Overall, the PCA suggests that the first three components are the most critical factors in understanding the underlying structure of the data, and the other components do not significantly contribute.

Table 15. Total variance explained

|

Component |

Initial Eigenvalues |

Rotation Sums of Squared Loadings |

||||

|

Total |

% of Variance |

Cumulative % |

Total |

% of Variance |

Cumulative % |

|

|

1 |

4.224 |

46.939 |

46.939 |

2.631 |

29.229 |

29.229 |

|

2 |

1.198 |

13.311 |

60.250 |

2.229 |

24.767 |

53.997 |

|

3 |

1.156 |

12.839 |

73.089 |

1.718 |

19.092 |

73.089 |

|

4 |

.840 |