Sarthak Mishra*![]() | Namita Rath

| Namita Rath![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The ever increasing serious consequences of global warming and climate change have made the environmental performance, a top concern for all organisations. Since anthropogenic activities are the main cause behind the environmental degradation, it is in the domain of human beings for taking rectificatory steps to save the situation. In this context, Green Human Resource Management (GHRM) practices hold hope for improving environmental performance through reduction of Green House Gas (GHG) emission and efficient use of natural resources and energy. The aim of this paper is to examine the impact of GHRM practices of Green Recruitment and Training (GRT) and Green Performance and Reward (GPR) on environmental performance in the Indian Banking sector. An empirical analysis has been done in State Bank of India (SBI) and HDFC Bank, the largest and leading Indian banks in public and private sector respectively. Hypothesis has been developed using Ability, Motivation and Opportunity(AMO) theory, Natural Resource Based View (NRBV) theory and Social Exchange theory (SET). With Structural Equation Modelling (SEM) technique,the data analysis is done using the statistical tool SMART PLS4. The results reveal that GRT and GPR can have significant impact on environmental performance via the mediation of Organisational Citizenship Behaviour for Environment (OCBE). The Importance and Performance Matrix Analysis (IPMA) also shows that OCBE as a mediator is the best performing construct in influencing the environmental performance in both the organisations. The study has practical implication for practicing bankers and policy makers to effectively mould GHRM practices towards better environmental performance.

Green Human Resource Management (GHRM), organizational citizenship behavior for environment, environmental performance, Green House Gas (GHG), importance-performance matrix analysis, PLS predict

In recent times climate change and its increasing adverse impact has become the most serious global issue posing the greatest challenge ever faced by the mankind. The Intergovernmental Panel on Climate Change (IPCC)-the United Nations body for making periodical scientific assessment about climate change has recently reported [1] that actions so far and current plans are inadequate to address climate change issues. Global warming has already reached 1.1above the pre-industrial level (1850-1900) resulting in more frequent and intense extreme weather events. In order to limit global warming to 1.5℃ above the pre-industrial level, all sectors need to reduce Green House Gas (GHG) emissions rapidly and on sustained basis by almost half by 2030. Global warming beyond 1.5℃ will bring further disasters to the entire world. With reference to the Indian context, it has been highlighted [2] that the instances of natural disasters have increased considerably during the last two decades as compared to previous hundred years. There is increase in average temperature and decline in monsoon precipitation since middle of the twentieth century and definite scientific evidence shows that human activities have caused such changes in regional climate.

In order to arrest the deteriorating trends, organizations irrespective of sectors are facing increasing expectations from all stakeholders and regulators towards reduction of overall environmental impact of their business operations and accordingly are redesigning their human resource management policies to incorporate the environmental dimension as a parameter for sustainable performance. Indian Banking sector with their huge branch network, large customer base and sizeable man power not only have a major share in use of resources and energy but more to that through their lending operations, banks also contribute a lot to pollution indirectly. Climate changes also entail various physical and transition risks for banks. While it is important to protect the health of this sector as the long term financial and economic growth of the nation depends on it, responsibility falls on banks to ensure better environmental management in terms of reduced GHG emission and energy consumption, lower carbon foot print, reduction/recycling of waste and efficient use of natural resources. These measures will also help banks in reducing their cost of operations and increasing competitive strength.

In this context, Green Human Resource Management (GHRM) practices involving eco-friendly HR practices and Organisational Citizenship Behaviour for Environment (OCBE) implying individual discretionary behaviour have assumed very important roles and are attracting lot of attention from organisations as well as researchers world over. Organisational Citizenship Behaviour (OCB) though not formally recognised by the organisation, yet it helps in its effective and efficient functioning and is classified into six main categories [3]: helping, sportsmanship, organisational loyalty, organisational compliance, individual initiatives and self development. Since environmental issues are complex in nature and involve informal, human and preventive aspects, decentralised and voluntary efforts resulting from OCBs are needed. Therefore, these OCBs can be utilised for environmental considerations and accordingly environmental OCB or OCBE can help in improving effectiveness of environment management in organisations [4]. Inspired by the above findings, several studies have since been carried out across various sectors linking the OCBE to GHRM to enhance environmental performance. However, no empirical study linking GHRM to OCBE and environmental performance in Indian Banking sector was found in the body of literature. Hence, the present study is a humble attempt to bridge the gap.

The study has chosen State Bank of India (SBI) and HDFC Bank as these banks are the largest and leading Indian Banks in public sector and private sector respectively with large nos. of branches, huge nos. of employees and mammoth customer base. As on March, 2023, SBI [5] has 22405 branches, 235858 employees and 48 crore+ customers and HDFC Bank [6] has 7821 branches, 173222 employees and 8.28 crore + customers. In view of larger presence of these banks, their environmental performance will have a wider impact on the Indian Banking sector.

The paper contains seven sections including the introduction. The next section gives brief overview of trend of GHG emission and energy consumption of banks under study for the last five Financial Years (FYs). Section3 covers the theoretical framework followed by existing literatures relating to the role of GHRM and OCBE in improving environmental performance together with the hypothesis development. Literatures concerning GHRM in Indian cultural and regulatory context, corporate governance, sustainable development and global trends in GHRM have also been discussed.In Section 4, we discuss the research methodology adopted for the study, followed by data analysis and interpretation in Section 5. In Section 6, we summarise the results and the interpretation thereof. Conclusion of the study is highlighted in the last section including theoretical and practical implications as well as limitations and future research direction.

It is pertinent to mention the status of reporting of GHG emission and energy consumption in these banks. Reserve Bank of India (RBI) being the banking regulator, has advised Indian Banks [7] to follow the disclosure framework recommended by the Task Force on Climate-related Financial Disclosures (TCFD). TCFD disclosure framework for GHG emissions has categorised it under three categories: Scope 1 (all direct GHG emissions like emissions from own vehicles and own Diesel Generator (DG) sets), Scope 2 (indirect GHG emissions like electricity consumption, diesel consumption by hired DG sets), Scope 3 (other indirect emissions not covered under Scope 2 like business travel by the employees, Taxi hire, Paper consumption, and E waste etc).

It is observed that this disclosure framework is yet to stabilise in Indian Banks and not being reported by many banks with proper scope-wise classification. We mention GHG emission and energy consumption figures of SBI [8] and HDFC Bank [9, 10] for the last five FYs (2018-19 to 2022-23) in Tables 1 and 2 respectively.

Table 1. GHG emission and energy consumption of SBI

|

Financial Year (FY) |

GHG Emission (In Tonnes of CO2e) |

Emission Intensity Per FTE |

Energy Consumption in Giga Joule (GJ) |

|||

|

Scope 1 |

Scope 2 |

Scope 3 |

Total |

|||

|

2018-19 |

418 |

1163367 |

181822 |

1345607 |

5.24 |

5897365 |

|

2019-20 |

390 |

1066386 |

192459 |

1259235 |

5.05 |

5500309 |

|

2020-21 |

553 |

1169146 |

135811 |

1305510 |

5.31 |

5861801 |

|

2021-22 |

547 |

1144641 |

140044 |

1285232 |

5.26 |

6020453 |

|

2022-23 |

217272 |

742732 |

46299 |

1006303 |

4.27 |

4339160 |

Source: SBI Sustainability Reports (from FY 2018-19 to FY 2022-23)

FTE: Full Time Employee

Table 2. GHG emission and energy consumption of HDFC bank

|

Financial Year (FY) |

GHG Emission ( In Tonnes of CO2e) |

Emissions Intensity Per FTE |

Energy Consumption in Giga Joule ( GJ) |

|||

|

Scope 1 |

Scope 2 |

Scope 3 |

Total |

|||

|

2018-19 |

7000 |

449700 |

15700 |

472400 |

4.82 |

2120500 |

|

2019-20 |

7649 |

390176 |

16419 |

414244 |

3.54 |

1961940 |

|

2020-21 |

5826 |

300141 |

9173 |

315140 |

2.62 |

1398980 |

|

2021-22 |

20877 |

287667 |

42697 |

351241 |

2.48 |

1596499 |

|

2022-23 |

29829 |

306840 |

48596 |

385265 |

2.22 |

1975098 |

Source: HDFC Bank Sustainability/ Integrated Annual Reports FY 2018-19 to FY 2022-23.

FTE: Full Time Employee

From the trends of GHG emission and energy consumption of SBI (Table 1), during the last five FYs, it may be noticed that unlike preceding FYs, the last FY of 2022-23 shows substantial reduction and scope-wise large variation in GHG emission which was mostly due to change in calculation methodology adopted by SBI during FY 22-23. In case of HDFC Bank (Table 2), during FY 22-23 there is increase in all types of GHG emission as well as energy consumption from the previous year. Despite increase in GHG emission during FY 21-22 and FY 22-23, Emission Intensity has come down as nos. of Full Time Employees (FTE) increased by 21486 during FY 21-22 and 31643 during FY 22-23.

Rapid reduction of GHG emission and energy consumption will help both the banks towards achieving their targeted goals to become carbon neutral by FY 2030 and FY 2032 respectively. In this regard, employees can play a major role with their voluntary support by adopting energy saving and carbon reduction measures. Strategic adoption of GHRM practices with higher level of OCBE can help improve environmental performance including reduction of GHG emission and energy consumption with change in approach which the present study aims to examine through an empirical analysis for which we discuss the related theoretical framework, literature review alongwith hypothesis formulation in the following section.

3.1 Theoretical framework

The present study relies on Ability, Motivation and Opportunity (AMO) theory, Natural Resource Based View (NRBV) theory and Social Exchange Theory (SET) to design a holistic framework for improving environmental performance in the banking sector with the supporting role of OCBE.

3.1.1 Ability, Motivation and Opportunity (AMO) theory

The AMO theory [11] is more often used to explore the impact of GHRM practices in accomplishing positive environmental outcome of the employees. Green Recruitment practices incorporate environmental perspective in the recruitment process with the aim of selecting candidates who show concern about environmental issues and are committed to the cause of effective environmental performance. Green Training is designed to enhance environmental skills and for building employee green expertise [12] about importance of environmental protection, to learn basics of energy conservation and waste reduction at the workplace [13]. Employees with high environmental value or skills will be more concerned to environmental issues and would display better eco-friendly behavior and green performance in the workplace [14]. Green Recruitment followed by Green Training (GRT) is essential organizational process to facilitate environmental welfare of the organization [15, 16]. Thus, GRT can build up the abilities (A) of human resources towards better environmental outcome. Green performance management incorporates various environmental responsibilities and provides an employee with clear information about the environmental role clarity. It also includes giving regular feedback to them about environmental performance which motivates them in improving their knowledge, skills, and ability in environmental management [17]. These activities can be summarized into four aspects: fixing green targets for all employees, devising green performance indicators, evaluating employees’ green outcomes, and using dis-benefits [14]. Green Reward for better environmental performance enhances employees’ commitment for environmental responsibility [18]. Thus, Green Performance and Rewards (GPR) can promote motivation (M) of the trained employees towards achieving targeted environmental goals. In this way GRT will help in green competence building and GPR act as green motivation enhancing practices [19], which will orient employee behaviors towards achieving organization’s environmental goals [20]. These organizational support measures provide opportunity (O) through knowledge sharing, empowerment and involvement among employees. This will lead to greater employee participation in the development process of the organization [12] and thus, Green HRM practices based on the AMO concept, impact OCBE significantly and OCBE has a significant relationship with environmental performance [21].

3.1.2 Natural Resource Based View (NRBV) theory

NRBV theory has been formulated [22] by incorporating environmental dimension to the original concept of Resource Based View Theory [23]. The environmental impact of the organizational resources and its operational activities, have been taken into account in the formulation to achieve sustainable green competitive advantage for business [24]. It emphasizes on environmental strategies like pollution prevention, product stewardship and sustainable development of the organization, which can be ensured with the valuable, rare, inimitable and non-substitutable resources, the main attributes of the RBV theory. Thus, for designing and development of these strategies, it requires active incorporation of environmental perspectives into the routine HR policies, i.e. adopting GHRM practices of GRT as well as GPR in the organization. Specifically, employees empowered through Green training, can ensure better pollution prevention and the practices of Green performance and reward can motivate them further to develop product stewardship. As per a theoretical study [25], GHRM practices positively influence environmental performance, thereby accomplishing sustainable green competitive advantage through the natural resource-based view perspective. Recent findings through empirical studies also reveal positive influence of GHRM on environmental performance in manufacturing industries of Malaysia [26] and hospitality sector in Indonesia [27].

3.1.3 Social Exchange Theory (SET)

Social exchange [28] is synonymous with voluntary behaviour, which the employees reciprocate in response to the benefits received from the organisation. Whenever employees feel that the organisation has paid enough attention to satisfy their needs, their social exchanges with the organisation turn more valuable [29]. Correlation between social exchange and organisational citizenship behaviour (OCB) is very high and there is highest correlation between perceived supervisory support and OCB [30]. Another study [31] reveals that relationship between OCB and Social Exchange constructs go beyond their prescribed role and responsibility and leads to engagement of employees in extra-role behaviour for the betterment of the organisation. Thus, Social Exchange theory [32] can be extended to explain the effects of GHRM on OCBE to achieve environmental performance, like efficient use of resources and prevention of environmental pollution. Based on this theory, research findings [33] among employees of hotel industry in Vietnam, show that Green training and Green organizational culture enhance reciprocated employee behaviour towards the organisation by way of higher employee commitment for environment. These factors influence OCBE positively in accomplishing environmental outcome voluntarily.Organisational support on the environment-oriented priorities, boost employees' willingness in the eco-activities at work. Thus, in the context of banking sector, Social exchange theory can also act as a base for OCBE to enhance the environmental performance.

In the following sub-sections, we discuss the findings of existing research studies in the context of GHRM practices, OCBE and environmental performance and accordingly formulate the hypothesis for our present study.GHRM in the Indian cultural and regulatory context, corporate governance, sustainable development and global trends in GHRM have also been discussed in subsequent sub-sections.

3.2 Green HRM and OCBE

Boiral and Paille [34] have classified OCBE into three categories: eco-initiatives (personal environmental initiatives), eco-helping (mutual pro-environmental assistance) and eco-civic engagement (contributions to corporate environmental activities). An integrative study in manufacturing sector of Pakistan [35], has assessed the effects of GHRM practices on OCBE via Green Employee Empowerment (GEE) by incorporating the moderating effects of individual green values (IGV). The study revealed that IGV act as a significant moderating component in influencing positive relationship between GEE and OCBE, towards sustainable environmental performance. GHRM practices on the basis of AMO theory can instil green culture [36] leading to OCBE at the organisation level. Implementation of GHRM practices in an organisation have a significant effect on facilitating the OCBE, thereby contributing to environmental performance. In the context of banking sector of Bahrain, an empirical study [37] shows significant impact of green training and green reward practices on OCBE.

In view of the above findings, we have proposed the following hypothesis:

H1: Green Recruitment and Training (GRT) has a direct significant impact on OCBE.

H2: Green Performance and Reward (GPR) has a direct significant impact on OCBE.

3.3 GHRM, OCBE and environmental performance

The main influencing agents to develop OCBE are supervisory support for environmental efforts and organizational commitment [38]. In other words, environmental practices at the organizational level influence OCBE which in turn has significant effect on environmental performance. A positive and significant relationship between OCBE, environmental management practices and environmental performance was revealed through an empirical analysis in the manufacturing companies of Canada [39]. In manufacturing industry of Malaysia, an empirical research [26] reveals the mediating role of Environmental Performance in influencing the GHRM for successful Business performance. Explicitly GHRM practices as well as the Green empowerment and participation, Green organizational culture have been shown to influence environmental performance, which in turn will enhance the business performance. A study in hotel industry of Thailand [40], shows that GHRM has positive impact on employees’ organizational commitment (EOC), their eco-friendly behavior (EEB) and hotels’ environmental performance (HEP). Based on the Social Identity Theory, the mediating role of EOC and EEB has been shown to be relevant to establish the significant relationship between GHRM and environmental performance. In respect of Chinese manufacturing firms, a study [41] has highlighted the significant relationship between GHRM practices and environmental performance with full mediation effect of the Enablers of Green organizational Culture (EGC). The impact of GHRM strategy on task related and voluntary green behavior of the employees in the banking sector of UAE [42] reveals the role of environmental values as a moderator to influence the employees’ outcome.

In view of the above findings, since no empirical study was found in the context of linking GHRM practices with environmental performance with the support of OCBE in the Indian banking sector, a research gap has been observed. Accordingly, we propose the following further hypothesis for our present study:

H3: GRT has a direct significant impact on EP.

H4: GPR has a direct significant impact on EP.

H5: OCBE has a direct significant impact on EP.

H6: OCBE mediates the relationship between GRT and EP.

H7: OCBE mediates the relationship between GPR and EP.

3.4 GHRM practices in Indian cultural and regulatory context

Religion and nature are closely connected and India has a rich traditional culture based on values enshrined in ancient scriptures of Vedas, Puranas, Upanishads and great epics of Ramayan and Mahabharat. GHRM practices may incorporate such values towards pro-environment behaviour, sustainable life style to tackle environmental challenges. In this context, we discuss following relevant literature. In a study [43] based on world value survey data collected during 1989 to 2014 from 212995 respondents in 91 countries, the results revealed that religion induces pro-environment behaviour and therefore, suggested to integrate religion into policies and programmes of environment for better outcome. In a study how ancient Hindu scriptures can mitigate global warming [44], it was suggested to rediscover eco-friendly way of livng basing on spiritual values to mitigate climate change. Ancient Indian philosophy can provide the road map. Another study on traditional techniques of environmental protection [45], opines to learn from the spiritual heritage of India as it offers unique moral values and customs which can serve as a guide to nurture the relationship between man and nature towards a sustainable future.

As regards the regulatory aspects in India, environment related practices come under the Environmental, Social and Governance (ESG) norms the concept of which was originated at United Nations (UN) in 2004 and it is governed under various laws of India like Companies Act, 2013, Security Exchange Board of India (SEBI) rules and several environment and labour related laws. As far as banks in India are concerned, the topic of environmental management came into prominence when the Reserve Bank of India (RBI)-the banking regulator issued instructions to banks in the year 2007 [46] to give urgency to sustanable development and to put in place board approved plan of action for the same. Recently, RBI has issued instruction [47] on disclosure framework for climate related financial risks and Indian banks have been advised to ensure disclosure on four thematic pillars of Governance, Strategy, Risk Management, Metrics and Targets.

3.5 Corporate governance, sustainable development and global trends in GHRM

In a very recent study [48], the results reveal positive relationship between financial performance (FP), corporate governance (CG) and sustainable development goal prioritisation (SDGP). The study further finds that FP partially mediates the relationship between CG and SDGP and highlighted important helping role of CG towards achieving 2030 SDG agenda in Latin America. Another study [49] presented results from their survey revealing the changes which occurred in corporate governance due to the global application of sustainable development. Environment pillar has become the most popular aspect in sustainable development and because of its most sensitive character in society, companies have directed their efforts towards it. A study on Indian banking sector [50] which claimed to be the first one in examining the extent of sustainability reporting by Indian commercial banks reveals that Indian banks are very slow to adopt sustainability reporting practices. The environmental indicators are also not being addressed by most of the banks in India.

As regards the trends and findings of global GHRM research, a bibliometric analysis of GHRM [51] based on scopus platform has revealed shortage of studies in service sector being only 37% as compared to 63% in manufacturing sector with suggestion to address this gap as service sector’s contribution to economy, GDP and job creation is more. The study also noted that topics like employees’ green behaviour, green training, environmental orientation, green employee empowerment and top management commitment are in developing phase and receiving more attention. Geographical scope analysis of a very recent systematic literature review study [52] covering scientific articles from 2006 to 2022 demonstrates world-wide interest in GHRM but developing countries have shown more interest than the developed ones. The study notes that strong internal belief of employees that GHRM can usher in eco-friendly organisation culture leading to cost and pollution reduction and positive organisational image is the most critical element in its implementation.

The study adopts a quantitative approach with primary data collection method through self administered structured questionnaire consisting of twentyfive questions. The questionnaire was designed by using a five point Likert scale (with 1: Strongly disagree, 2: Somewhat disagree, 3: Neutral 4: Somewhat agree, 5: Strongly agree). The items were segmented in the following manner: GRT (8 items), GPR (7 items), OCBE (5 items) and EP (5 items).For measuring GRT and GPR, questions have been designed as per Tang et al. [14] whereas questions on OCBE and EP have been framed as per Anwar et al. [21] after examining and confirming their relevance in the context of Indian banking sector. Accordingly, the study uses two exogenous constructs namely GRT and GPR, two endogenous constructs: EP and OCBE. Here OCBE acts as a mediator variable. In the lens of AMO theory, GRT represent the Green Ability, whereas GPR will expedite the Green Motivation.

As mentioned before, the study has considered State Bank of India (SBI), the largest public sector bank and HDFC bank, the largest private sector bank in India, for empirical analysis. The criteria for selecting the above two banks for our study are that among all Indian Banks, only these two banks have disclosed year-wise GHG emission and energy consumption figures which helps in trend analysis and correlation of secondary data with primary data analysis. Besides their mammoth customer base, large branch network and huge man power as detailed under introduction section which has ramifications from environment angle, as on March,2023, their combined market share is 32.78% in deposits and 29.31% in advances at whole country level and in Odisha State, where the empirical study is undertaken, their combined market share is 41.30% in deposits and 32.07% in advances. These two banks were, therefore, considered to represent the Indian banking sector adequately for our study. Further, three Indian banks ( SBI, HDFC Bank and ICICI Bank) figure in the banking regulator-RBI’s 2023 list of Domestic Systematically Impotant Banks (D-SIBs) [53], in which SBI and HDFC Bank are placed in higher buckets depending on their systemic important scores (SISs) and these two banks have set targets to become carbon-neutral by the year 2030 and 2032 respectively.

As regards the data cleaning and preparatory stages, during a preliminary survey, we observed the response of the junior level officers in both the banks were inadequate and incomplete, which may be attributed to their lack of exposure and awareness in the related area and therefore, their responses may not reflect the correct scenario. Hence, we have chosen senior level officers in both the banks as our target respondents with the expectation that significant insights can be drawn from them as they have the experience of working across different departments and assignments with reasonably long period of time and are expected to be acquainted with bank’s HR policy and practices.

Accordingly, in SBI, our target population cover 502 senior level officers (Asst. General Managers and Chief Managers) working in various offices/branches of Odisha State. In HDFC Bank, the target population cover 250 senior officers (Deputy Vice President, Senior Manager and Deputy Manager) working in various offices and branches of Odisha. For data collection, we have adopted purposive sampling method and followed the Yamane formula [54] with level of precision=0.05. for sampling calculation. Total 350 and 220 questionnaires were distributed among SBI and HDFC bank executives respectively. 223 valid responses from SBI and 180 valid responses from HDFC Bank were chosen for the analysis which meets the threshold sampling criteria. Majority of the respondents are within the age group of 40- 50 years with good amount of work experience of more than 10 years and have handled various assignments including human resource departments in different branches and offices in the State of Odisha.

In the following section, we have done the data analysis by using the Structural Equation Modelling (SEM), with the statistical tool Smart PLS4. We have used bootstrapping procedure for hypothesis testing, PLS predict for evaluating accuracy of the model and IPMA to know the importance and performance score of the constructs.

A detailed SEM analysis of the data collected from the respondents has been done through measurement model and structural model assessment. For data analysis, we have used the most suitable Partial Least Square-Structural Equation Modelling (PLS-SEM) technique which is basically variance-based (VB) SEM method. The rationale behind choosing this method are as follows: It can simultaneously establish (i) the relation between each construct and it’s indicators through measurement model (ii) relation between the constructs through structural model. It can evaluate the direct effect of independent variables on dependent variables as well as the indirect effect through mediation. In more recent developments, PLS-predict has been used to test how far the proposed model can predict the desired outcome.

As regards the stastical technique, we have used SMART-PLS 4 soft ware, the recent version of PLS-SEM.The research objective has been targeted through bootstrapping procedure so as to test the proposed hypothesis. As mentioned before, the PLS-Predict and IPMA have been included in the study which add value to the proposed model by focussing on its predictive power as well as the significance of the respective constructs.

5.1 Measurement model assessment

As a prerequisite for accurate estimation in SEM, initially the factor loading of each item are checked and for better estimation, the items with low loading (<0.5) are deleted. Then the reliability of the measured parameter has been checked by calculating Composite Reliability (CR) and Cronbach alpha. The Average Variance Extracted (AVE) value has been tested for convergent validity [55]. In the next step, the discriminant validity was assessed for consistency using more reliable HTMT ratio method. The inner VIF (Variance Inflation Factor) values are checked for collinearity of the constructs.

The tables for measurement model assessment tests for both SBI and HDFC banks are given below.

Table 3. Cronbach alpha, AVE, composite reliability

|

Construct |

Cronbach’s Alpha |

Composite Reliability (rho a) |

Composite Reliability(rho c) |

Average Variance Extracted(AVE) |

|

State Bank of India |

||||

|

EP |

0.825 |

0.838 |

0.883 |

0.655 |

|

GPR |

0.824 |

0.848 |

0.877 |

0.592 |

|

GRT |

0.749 |

0.774 |

0.835 |

0.512 |

|

OCBE |

0.797 |

0.798 |

0.866 |

0.619 |

|

HDFC Bank |

||||

|

EP |

0.748 |

0.766 |

0.854 |

0.662 |

|

GPR |

0.818 |

0.852 |

0.874 |

0.586 |

|

GRT |

0.744 |

0.759 |

0.842 |

0.577 |

|

OCBE |

0.801 |

0.809 |

0.869 |

0.624 |

The results in above Table 3 show that AVE ≥ 0.5, CR and Cronbach alpha coefficients ≥ 0.7 for each case. Thus, the reliability criteria of the measurement model is fulfilled. The discriminant validity is assessed through HTMT ratio, shown in Table 4 below.

Table 4. HTMT ratio

|

State Bank of India |

||||

|

Construct |

EP |

GPR |

GRT |

OCBE |

|

EP |

|

|

|

|

|

GPR |

0.428 |

|

|

|

|

GRT |

0.443 |

0.727 |

|

|

|

OCBE |

0.674 |

0.583 |

0.772 |

|

|

HDFC Bank |

||||

|

EP |

|

|

|

|

|

GPR |

0.402 |

|

|

|

|

GRT |

0.395 |

0.610 |

|

|

|

OCBE |

0.624 |

0.594 |

0.789 |

|

Table 5. Inner VIF value

|

Construct Relation |

State Bank of India |

HDFC Bank |

|

GPR → EP |

1.568 |

1.454 |

|

GPR → OCBE |

1.476 |

1.317 |

|

GRT → EP |

1.885 |

1.750 |

|

GRT → OCBE |

1.476 |

1.317 |

|

OCBE → EP |

1.723 |

1.808 |

The HTMT values in the Table 4, are shown to be <0.85 thus, satisfying the stricter criterion of discriminant validity. The inner VIF values are given in Table 5 below.

The values are shown to be less than 3.3 implying that there is no collinearity issue.

On the basis of the results of the above tables, the measurement model meets all the criteria successfully. The structural model assessment has been done on the basis of bootstrapping results to check the hypothesized relationships.

5.2 Structural model assessment

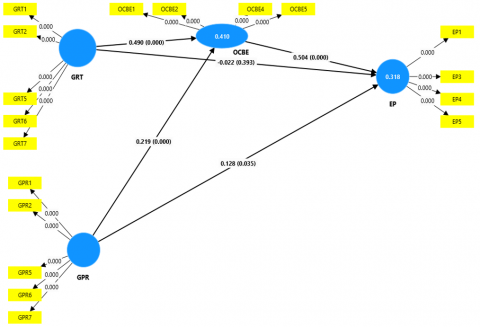

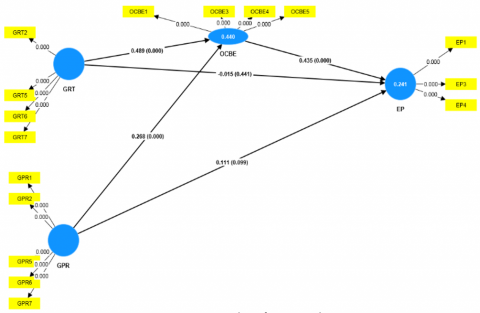

In structural model assessment [56], we test the hypothesized relationships of the exogenous constructs GRT and GPR influencing the endogenous construct EP through the mediator variable OCBE. Explanatory power of the model is ascertained from R2 value, the coefficient of determination [57]. With respect to the effect of GRT and GPR on OCBE, R2 is 0.410 and 0.440 for SBI and HDFC Bank respectively. This shows that GRT and GPR explained variance of 41% in SBI and 44% in HDFC Bank with OCBE. With regard to the effect on EP, R2 is 0.318 and 0.241 for SBI and HDFC Bank respectively. It shows the exogenous constructs explained variance of 31.8% and 24.1% for SBI and HDFC Bank respectively. ( R2 values are reflected in the PLS-SEM images as shown in Figure 1 and Figure 2 for SBI and HDFC Bank respectively).

Through bootstrapping method [58] and one-tailed test, the β values, t-values and p-values are measured to visualise the acceptance/rejection of the proposed hypothesis. The hypothesis testing results showing direct and indirect effects are given in Tables 6 and 7 respectively.

Table 6. Direct effect

|

State Bank of India |

||||||||

|

Hypothesis |

Beta Coefficient |

Sample Mean |

Standard Deviation |

T statistics |

Confidence Interval 5%-95% |

P-values |

Remark |

|

|

H1: GRT →OCBE |

0.490 |

0.491 |

0.074 |

6.603 |

0.364 |

0.606 |

0.000 |

Accepted |

|

H2: GPR → OCBE |

0.219 |

0.224 |

0.059 |

3.711 |

0.128 |

0.325 |

0.000 |

Accepted |

|

H3: GRT → EP |

-0.022 |

-0.021 |

0.083 |

0.271 |

-0.158 |

0.114 |

0.393 |

Not Accepted |

|

H4: GPR → EP |

0.128 |

0.128 |

0.071 |

1.813 |

0.011 |

0.243 |

0.035 |

Accepted |

|

H5: OCBE→EP |

0.504 |

0.507 |

0.085 |

5.959 |

0.359 |

0.635 |

0.000 |

Accepted |

|

HDFC Bank |

||||||||

|

Hypothesis |

Beta Coefficient |

Sample Mean |

Standard Deviation |

Tstatistics |

Confidence Interval 5%-95% |

P-values |

Remark |

|

|

H1: GRT→OCBE |

0.489 |

0.490 |

0.067 |

7.312 |

0.374 |

0.592 |

0.000 |

Accepted |

|

H2: GPR→OCBE |

0.268 |

0.274 |

0.057 |

4.686 |

0.178 |

0.368 |

0.000 |

Accepted |

|

H3: GRT→EP |

-0.015 |

-0.014 |

0.098 |

0.149 |

-0.173 |

0.151 |

0.441 |

Not Accepted |

|

H4: GPR→EP |

0.111 |

0.113 |

0.086 |

1.288 |

-0.026 |

0.260 |

0.099 |

Not Accepted |

|

H5: OCBE → EP |

0.435 |

0.437 |

0.109 |

3.976 |

0.247 |

0.607 |

0.000 |

Accepted |

Table 7. Indirect effect

|

State Bank of India |

||||||||

|

Hypothesis |

Beta Coefficient |

Sample Mean |

Standard Deviation |

T-statistics |

Confidence Interval 5%-95% |

P-values |

Remark |

|

|

H6: GRT → OCBE→EP |

0.247 |

0.249 |

0.058 |

4.258 |

0.155 |

0.349 |

0.000 |

Accepted |

|

H7: GPR →OCBE → EP |

0.110 |

0.113 |

0.033 |

3.366 |

0.062 |

0.169 |

0.000 |

Accepted |

|

HDFC Bank |

||||||||

|

Hypothesis |

Beta Coefficient |

Sample Mean |

Standard Deviation |

T-statistics |

Confidence Interval 5%-95% |

P-values |

Remark |

|

|

H6: GRT→OCBE→EP |

0.213 |

0.215 |

0.062 |

3.423 |

0.114 |

0.319 |

0.000 |

Accepted |

|

H7: GPR→OCBE→EP |

0.116 |

0.119 |

0.038 |

3.092 |

0.061 |

0.183 |

0.001 |

Accepted |

In SBI, the direct effect results show that with respect to H1: impact of GRT on OCBE; β = 0.490, t-value = 6.603 and p-value = 0), H2: impact of GPR on OCBE; β= 0.219, t-value = 3.711, and p-value= 0, H3:impact of GTR on EP; β = -0.022, t-value = 0.271, and p-value= 0.393, H4:impact of GPR on EP; β= 0.128, t-value = 1.813, and p-value = 0.035 and H5: impact of OCBE on EP; β = 0.504, t-value = 5.959, and p-value = 0. It is further seen that for H1, H2, H4 and H5 the confidence intervals don’t contain 0 in between the 5% and 95% levels, thus accepting these Hypothesis with p-value<0.05. However, H3 is rejected with p> 0.05.Similarly, in case of HDFC Bank, the respective values are given as (1) β= 0.489, t-value = 7.312 and p-value= 0 (2) β=0.268, t-value = 4.686, and p-value= 0 (3) β= -0.015, t-value = 0.149 and p-value= 0.441 (4) β= 0.111, t-value = 1.288 and p-value= 0.099 (5) β= 0.435, t-value = 3.976, and p-value= 0, implying acceptance of the hypothesis H1, H2 and H5 with rejection of H3 and H4.

Here the indirect effect of GRT and GPR via OCBE as a mediator variable was found to be significant with p-value<0.05. Explicitly in SBI, for H6: β= 0.247, t-value =4.258 and p-value=0, for H7: β= 0.110, t-value = 3.366 and p-value=0. Similarly in HDFC bank, for H6: β= 0.213, t-value = 3.423 and p-value=0, for H7: β= 0.116, t-value = 3.092 and p-value=0.001. The data results as above confirm the hypothesis H6 and H7 for both the banks.

For better clarity we give here the PLS-SEM diagram for both the banks. The diagram shows the values of beta (path) coefficient, p-value and R2 value for the constructs.

Now we analyse the PLS predict results to determine the predictive power of our model.

5.3 PLS predict

The predictive power [59] of the model has been assessed through the PLS predict tool, given in Table 8.

Table 8. PLS predict results

|

Construct |

Q²predict |

RMSE |

MAE |

|

State Bank of India |

|||

|

EP |

0.144 |

0.939 |

0.744 |

|

OCBE |

0.383 |

0.797 |

0.599 |

|

HDFC Bank |

|||

|

EP |

0.101 |

0.968 |

0.773 |

|

OCBE |

0.417 |

0.780 |

0.570 |

RMSE: Root Mean Square Error MAE: Mean Absolute Error

Positive Q2 values for endogenous construct (OCBE and EP) prediction establish predictive relevance of the model in both SBI and HDFC Bank. As per Hair et al. [60], Q2 > 0.35 signifies strong degree of predictive relevance for the model. In the present case Q2 is 0.383 in case of SBI and 0.417 in case of HDFC Bank with respect to OCBE construct indicating strong degree of prediction. In regard to EP, moderate degree of predictive relevance is established, for SBI and HDFC Bank as Q2 stands at 0.144 and 0.101 respectively.

5.4 Importance and performance matrix analysis (IPMA)

IPMA procedure is carried out to assess the importance and performance scores of the constructs GRT, GPR and the mediator variable OCBE in influencing the endogenous construct EP, in both the banks.

Table 9. IPMA results

|

State Bank of India |

||||

|

Construct |

Importance |

Mean Importance |

Performance |

Mean Performance |

|

GRT |

0.224 |

0.322 |

74.025 |

69.79 |

|

GPR |

0.238 |

58.307 |

||

|

OCBE |

0.504 |

77.061 |

||

|

HDFCBank |

||||

|

Construct |

Importance |

Mean Importance |

Performance |

Mean Performance |

|

GRT |

0.198 |

0.286 |

73.843 |

69.53 |

|

GPR |

0.227 |

57.477 |

||

|

OCBE |

0.435 |

77.270 |

||

The IPMA analysis in the above Table 9 shows that OCBE as a mediator variable has maximum pronounced effect in terms of importance and performance on the target endogenous construct environmental performance for both SBI and HDFC Bank. This means OCBE signifies the course of action “Keep up the good work” [59]. GRT is the second best in terms of performance in both the banks in influencing the environmental performance. However, GPR despite having more importance is shown to have less performance as compared to GRT. Therefore, the GPR construct lies in the “concentrate here” region of the IPMA graph indicating the need for more focused attention to GPR from both SBI and HDFC Bank so as to improve its overall performance in influencing OCBE as well as environmental performance.

The aim of this study was to ascertain the trend of environmental performance in terms of GHG emission and energy consumption in two leading Indian Banks namely SBI and HDFC Bank through secondary data analysis and to find out how GHRM practices can help improve the position through an empirical study.

The secondary data analysis clearly indicates that there is no noticeable reduction trend in these environmental performance parameters during the last five FYs. As regards the empirical study, it was undertaken to investigate the impact of GHRM Practices (GRT, GPR) on Environmental performance by using OCBE as a mediator variable. The bootstrapping results for both SBI and HDFC Bank, revealed significant direct impact of GRT and GPR on OCBE and indirect impact of GRT and GPR practices on Environmental Performance (EP), with the inclusion of the mediator OCBE. However, in SBI, GPR has also direct impact on EP, indicating that motivating employees with reward and acknowledgement will encourage them for better environmental performance.As regards comparison with findings of similar studies, past studies in diverse sectors and in different economic contexts (detailed in literature review section) like manufacturing [26, 39], banking [37], education [21] and hospitality [27] revealed significant effect of GHRM practices on environmental performance either directly or through the mediating support of OCBE. Further, a similar recent study in Commercial Bank of Bangladesh [61] reveals significant positive impact of green training and development, green performance appraisal and green employee empowerment on OCBE. The unique revealation of our study is that GHRM practices have no direct significant impact on environmental performane (except GPR in case of SBI) but indiectly through OCBE it impacts EP significantly. This has strong implication for Indian Banking sector in as much as banks need to give utmost thrust to OCBE.

The PLSPredict result with positive Q2 shows predictive relevance of the proposed model. With regard to the constructs of OCBE and EP, the model shows strong and moderate degree of predictive relevance respectively in both the banks. The IPMA result shows highest importance and performance score for OCBE, signifying that OCBE is the key to accomplish better environmental performance in the banks. The HR practices in Indian Banks, therefore, need to focus on facilitating OCBE, that would urge the employees to go beyond their prescribed job roles and responsibilities and voluntarily take up environmental welfare at the workplace.

The present study has tried to explore the environmental potential of the Indian banking industry and has revealed through its results about the priority areas of GHRM practices which need special focus and attention by HR managers so as to fulfil the environmental obligations and goals of the organisation. The employer and employee symbiotic association along with a systematic GHRM policy planning, is absolutely necessary to accomplish the “Going Green” goal of the organisation. Considering the trends, the banks have to intensify their measures to improve environmental performance during the coming years and as evidenced from empirical findings, strategic adoption of GHRM practices very well stands as one of the options which may need appropriate attention and intensification.

7.1 Theoretical implications

We have explained under theoretical framework how GHRM practices can facilitate better environmental performance basing on the AMO concept. GHRM practices need to be appropriately strngthened so as to have higher OCBE to fulfill the AMO concept. Empirical results of our study show that GHRM practices do not impact environmental performance directly but only when it is mediated by OCBE, the environmental performance is impacted. The empirical results, therefore, support the AMO theory. This is also in line with findings of a study [21] which based on AMO framework revealed significant impact of GHRM practices on environmental performance in higher education sector of Malaysia through the mediating support of OCBE.In the lense of AMO theory, banks need to assess the basic environmental knowledge and aptitude of candidates during recruitment and to train them appropriately. Pro-environment behaviour,adopted at work place could build up their green ability for better EP. As IPMA analysis reveals lower performance score for GPR in both the banks, it needs additional attention from Indian banks as motivation enhancing practices to improve environmental performance. In this context, banks need to fix green targets among employees, evaluate their performance and to give suitable recognition for exemplary achievements.In addition, more opportunities need to be ensured at work place by seeking greater participation of employees in environmental activities as well as empowering them through involvement in decision making and problem solving.

NRBV theory [24] advocated strategic capabilities of product stewardship, pollution prevention and sustainable development towards sustained green competitive advantage as well as better environmental outcome. Under the theoretical framework, we have discussed how GHRM practices can have such capabilities. Empirical results of our study reveal GHRM practices have significant impact on environmental performance through mediation of OCBE which may imply that OCBE brings such strategic capabilities and required attributes for GHRM. Thus, our empirical study results stand supported by the NRBV theory. In tune with NRBV framework, GHRM practices need to be implemented strategically so as to make it a valuable, rare, inimitable and non-substitutable resource. Focusing on less paper use with increased digitisation, better recycling, waste management and efficient resource and energy use will not only reduce carbon emission but will improve operational efficiency with reduced cost thereby making GHRM a valuable resource. Green human capital (green talent and green training), Green physical capital (green work place with energy saving devices) and Green organisational capital (suitable environment policy and organisation structure for effective environment management system) are very essential so as to make GHRM rare and unique resource. Strategic adoption of GHRM by Indian Banks will help usher in green work culture, green organisation value and belief which are socially complex resources and therefore, become inimitable. Through appropriate green learning and development exercise, Indian Banks can make their green human resources non-substitutable.

We have discussed under theoretical framework how previous studies have linked OCB with Social Exchange theory based on the concept of reciprocity [28-33]. As the empirical results of this study establish significant impact of GHRM practices on OCBE, it confirms to the reciprocity principle under the Social Exchange Theory (SET) in line with previous findings [30, 32]. Banks need to ensure that employees perceive the supervisory support and benefits of GHRM practices so that the principle of reciprocity can be satisfied and reflected in higher OCBE and better environmental performance.

7.2 Practical implications

As far as the practical implication of the study result is concerned,its coverage and findings contribute to academic discouse in several areas as discussed below and opens up vast scope for future research in all these fields. Importance of GHG emission and energy consumption disclosure for Indian banking sector was covered which can also be more important for manufacturing sectors. Unless these vital environmental parameters are kept under radar and monitored for improvement, the goal of carbon neutrality and tackling global warming will elude us constantly. Relying on AMO, NRBV and SET theories, the study has presented valuable practical suggestions on how to strengthen and effectively implement GHRM to augment OCBE at workplace towards better environmental performance(EP) in Indian Banking sector. This provides lot of opportunities for research in each of the GHRM practice in various sectors as well as in the areas such as green human capital, green physical captal, green organization capital, green work culture, green organisation value and belief etc. and how each is related and can impact OCBE and EP. With coverage of GHRM in Indian cultural and regulatory context, the study has not only added academic discourse in these areas but brings out the scope how values enshrined in ancient Indian scriptures/epics and regulatory steps can ensure effectiveness of GHRM practices. The study adds further academic discourse and scope for research by covering the global trend of GHRM as well as corporate governance and sustainable development issues where limited research has been done linking with GHRM.

Moreover, it is expected to aid the human resource practitioners and policymakers of banks to prioritise Green HRM practices and link them to the real time job setting to facilitate pro-environmental behaviour of bank employees. It can also orient human resource management activities in the direction of improving environmental performance outcomes through emission reduction, planned energy consumption with the long term vision of achieving carbon neutrality. The IPMA analysis of the empirical study, determines the priority factors in enhancing OCBE in banks, which has not been found in previous literatures concerning GHRM in the banking sector. Findings may receive attention of bank managements of entire banking fraternity to introduce adequate mechanisms and system for proper disclosure of GHG emission as well as energy consumption so as to ensure effective monitoring for improving environmental performance.

7.3 Limitations and future research direction

The study is confined to two Indian premier banking organisations of SBI and HDFC bank and the empirical findings were limited to the State of Odisha. The above limitations may affect on assessing OCBE of the employees working under different organisational culture as well as varied supervisory support. Including more nos. of banks with larger geographical area in the study may give a broader perspective on employees’ perceptions because of varied implementation pattern of GHRM practices. The study can be scaled up to cover other public and private sector banks as well as Cooperative and Regional Rural Banks with increased geographical coverage and inclusion of junior grade employees so to understand how the employee opinion and concerns vary with change in organisation, geography and demography. The study has examined OCBE as mediating variable between GHRM and environmental performance. Future researchers may examine other mediating variables like Supervisory Support, Individual Self-efficacy [40], Organisational Culture, Employee Attitude [21]. Since the study is cross-sectional, future research may adopt a longitudinal approach for deeper understanding.

[1] IPCC Synthesis Report. (2023) https://www.ipcc.ch/2023/03/20/press-release-ar6-synthesis-report.

[2] Ministry of Earth Sciences, Government of India. (2020). Assessment of Climate over the Indian Region: A report of Ministry of Earth Sciences (MoES), Govt. of India. https://reliefweb.int/report/india/assessment-climate-change-over-indian-report-ministry-earth-sciences-moes.

[3] Organ, D.W., Podsakoff, P.M., MacKenzie, S.B. (2005). Organizational Citizenship Behavior: Its Nature, Antecedents, and Consequences. Sage Publications. https://doi.org/10.4135/9781452231082

[4] Boiral, O. (2009). Greening the corporation through organizational citizenship behaviors. Journal of Business Ethics, 87: 221-236. https://doi:10.1007/s10551-008-9881-2

[5] State Bank of India. (2022). Annual Report, FY 2022-23. https://www.sbi.co.in.

[6] HDFC Bank Integrated Annual Report FY 2022-23. (2022). https://www.hdfcbank.com.

[7] Reserve Bank of India (July,2022). Discussion Paper on Climate Risk and Sustainable Finance. https://www.rbi.org.in

[8] State Bank of India. (2022). Sustainability Report FY 2018-19, 2019-20, 2020-21, 2021-22 and 2022-23. https://www.sbi.co.in.

[9] HDFC Bank Sustainability Report FY 2018-19, 2019-20. (2022). https://www.hdfcbank.com.

[10] HDFC Bank Integrated Annual Reports FY 2020-21, 2021-22 and 2022-23. (2022). https://www.hdfcbank.com.

[11] Bailey, T. (1993). Discretionary effort and the organization of work: Employee participation and work reform since Hawthorne. New York: Institute on Education and the Economy, Teachers College, Columbia University.

[12] Renwick, D.W., Redman, T., Maguire, S. (2013). Green human resource management: A review and research agenda. International Journal of Management Reviews, 15(1): 1-14. https://doi.org/10.1111/j.1468-2370.2011.00328.x

[13] Jabbour, C.J.C. (2015). Environmental training and environmental management maturity of Brazilian companies with ISO14001: Empirical evidence. Journal of Cleaner Production, 96: 331-338. https://doi.org/10.1016/j.jclepro.2013.10.039

[14] Tang, G., Chen, Y., Jiang, Y., Paille, P. (2018). Green human resource management practices: Scale development and validity. Asia Pacific Journal of Human Resource, 56: 31-55. https://doi.org/10.1111/1744-7941.12147

[15] Bauer, T.N., Erdogan, B., Taylor, S. (2012). Creating and maintaining environmentally sustainable organizations: Recruitment and on boarding. Business Faculty Publications and Presentations, 28: 1-26.

[16] Milliman, J. (2013). Leading-edge green human resource practices: Vital components to advancing environmental sustainability. Environmental Quality Management, 23(2): 31-45. https://doi.org/10.1002/tqem.21358

[17] Jackson, S.E., Renwick, D.W., Jabbour, C.J., Muller-Camen, M. (2011). State-of-the-art and future directions for green human resource management: Introduction to the special issue. German Journal of Human Resource Management, 25(2): 99-116. https://doi.org/10.1177/239700221102500203

[18] Daily, B.F., Huang, S.C. (2001). Achieving sustainability through attention to human resource factors in environmental management. International Journal of Operations and Production Management, 21(12): 1539-1552. https://doi.org/10.1108/01443570110410892

[19] Teixeira, A.A., Jabbour, C.J.C., Jabbour, A.B.L. (2012). Relationship between green management and environmental training in companies located in Brazil: A theoretical framework and case studies. International Journal of Production Economics, 140(1): 318-329. https://doi.org/10.1016/j.ijpe.2012.01.009

[20] Harvey, G., Williams, K., Probert, J. (2013). Greening the airline pilot: HRM and the green performance of airlines in the UK. The International Journal of Human Resource Management, 24(1): 152-166. https://doi.org/10.1080/09585192.2012.669783

[21] Anwar, N., Mahmood,N.H.N., Yusliza, M.Y., Ramayah,T., Faezah, N.J., Khalid, W. (2020). Green human resource management for organisational citizenship behaviour towards the environment and environmental performance on a university campus. Journal of Cleaner Production, 256: 120401. https://doi.org/10.1016/j.jclepro.2020.120401

[22] Hart, S.L. (1995). A natural-resource-based view of the firm. Academy of Management Review, 20(4): 986-1014. https://doi.org/10.5465/amr.1995.9512280033

[23] Barney, J.B. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1): 99-120. http://doi.org/10.1177/014920639101700108

[24] Hart, S.L., Dowell, G. (2011). A natural-resource-based view of the firm: Fifteen years after. Journal of Management, 37(5): 1464-1479. http://doi.org/10.1177/0149206310390219

[25] Almada, L., Borges, R. (2018). Sustainable competitive advantage needs green human resource practices: A framework for environmental management. Revista de Administração Contemporânea, 22: 424-442. https://doi.org/10.1590/1982-7849rac2018170345

[26] Ghouri, A.M., Mani, V., Khan, M.R., Khan, N.R., Srivastava, A.P. (2020). Enhancing business performance through green human resource management practices: Empirical evidence from Malaysian manufacturing industry. International Journal of Productivity and Performance Management, 69(8): 1585-1607. https://doi.org/10.1108/IJPPM-11-2019-0520

[27] Hadi, H.K., Kautsar, A., Fazlurrahman, H., Rahman, M.F.W. (2023). Green HRM: The link between environmental and employee performance, Moderated by green work climate perception. International Journal of Sustainable Development and Planning, 18(5): 1573-1580. https://doi.org/10.18280/ijsdp.180528

[28] Blau, P.M. (1964). Power and Exchange in Social Life. Wiley & Sons, New York.

[29] Kramer, R.M. (1991). Intergroup relations and organizational dilemmas: The role of categorization processes. Research in Organizational Behaviour, 13: 191-227.

[30] Ahmadi, P., Forouzandeh, S., Kahreh, M.S. (2010). The relationship between OCB and social exchange constructs. European Journal of Economics, Finance and Administrative Sciences, 19: 107-120.

[31] Podsakoff, P.M., MacKenzie, S.B., Paine, J.B., Bachrach, D.G. (2000). Organizational citizenship behaviors: A critical review of the theoretical and empirical literature and suggestions for future research. Journal of Management, 26: 513-563. https://doi.org/10.1177/014920630002600307

[32] Emerson, R.M. (1976). Social exchange theory. Annual Review of Sociology, 2: 335-362.

[33] Pham, N.T., Phan, Q.P.T., Tučková, Z., Vo, N., Nguyen, L.H.L. (2018). Enhancing the organizational citizenship behavior for the environment: The roles of green training and organizational culture. Management & Marketing. Challenges for the Knowledge Society, 13(4): 1174-1189. https://doi/10.2478/mmcks-2018-0030

[34] Boiral, O., Paille, P. (2012). Organizational citizenship behaviour for the environment: Measurement and validation. Journal of Business Ethics, 109: 431-445. https://10.1007/s10551-011-1138-9

[35] Hameed, Z., Khan, I.U., Islam, T., Sheikh, Z., Naeem, R.M. (2019). Do green HRM practices influence employees’ environmental performance? International Journal of Manpower, 41(7): 1061-1079. https://doi/10.1108/IJM-08-2019-0407

[36] Muisyo, P.K., Qin, S., Ho, T.H. (2021). The role of green HRM in driving a firm's green competitive advantage: The mediating role of green organizational identity. SN Business and Economics, 1: 1-19. https://doi.org/10.1007/s43546-021-00154-6

[37] Ogalo, H., Fatima, S., Hasnain, A. (2020). Green HRM and OCBE in the banking sector: An empirical view. International Journal of Psychosocial Rehabilitation, 24(7): 2695-2705. https://doi/10.37200/V2417/14863

[38] Daily, B.F., Bishop J.W., Govindarajulu, N. (2009). A conceptual model for organisational citizenship behaviour directed toward the environment. Business Society, 48(2): 243-256. https://doi/10.1177/0007650308315439

[39] Boiral, O., Talbot, D., Paille, P. (2015). Leading by example: A model of organizational citizenship behaviour for the environment. Business Strategy and the Environment, 24: 532-550.

[40] Kim, Y.J., Kim, W.G., Choi, H.M., Phetvaroon, K. (2019). The effect of green human resource management on hotel employees’ eco-friendly behaviour and environmental performance. International Journal of Hospitality Management, 76: 83-93. https://doi.org/10.1016/j.ijhm.2018.04.007

[41] Roscoe, S., Subramanian, N., Jabbour, C.J.C., Chong, T. (2019). Green human resource management and the enablers of green organisational culture: Enhancing a firm’s environmental performance for sustainable development. Business Strategy and the Environment, 28: 737-749. https://doi.org/10.1002/bse.2277

[42] Abid, S., Matloob, S., Raza, A., Ali, S.A., Nayab, D.E. (2020). The impact of green human resource management on employee’s outcome: Does environmental values moderate? PalArch’s Journal of Archaeology of Egypt/Egyptology, 17(7): 13577-13591.

[43] Zemo, K.H., Nigus, H.Y. (2020). Does religion promote pro-environment behaviour? A cross-country investigation. Journal of Environmental Economics and Policy, 1-24. https://doi.org/10.1080/21606544.2020.1796820

[44] Agoramoorthy, G., Hsu, M.J. (2011). Ancient Hindu scriptures show the ways to mitigate global warming through responsible action. Anthropos, H.1: 211-216.

[45] Shyamala, B., Shwetha, S.S. (2018). Relevance of ancient Indian methods of environmental protection in the present day scenario. International Review of Business and Economics, 1(3): 162-165. https://doi.org/10.56902/IRBE.2018.1.3.37

[46] Reserve Bank of India. (2007). Corporate social responsibility, sustainable development and non-financial reporting-role of banks. Circular DBOD Dir.BC.58/13.27.00/2007-08 dated December, 30, 2007. https://rbi.org.in.

[47] Reserve Bank of India. (2024). Disclosure framework on climate-related financial risks. Circular DOR.SFG.REC/30.01.021/2023-24 dated February, 28, 2024. https://rbi.org.in.

[48] Correa-Mejia, D.A., Garcia-Benau, M.A., Correa-Garcia, J.A. (2024). The critical role of corporate governance in sustainable development goals prioritisation: A 5 Ps-based analysis for emerging economies. Heliyon, 10(2024): e25480. https://doi.org/10.1016/j.heliyon.2024.e25480

[49] Boeva, B., Zhivkova, S., Stoychev, I. (2017). Corporate governance and the sustainable development. European Journal of Economics and Business Studies, 7(1): 17-24

[50] Kumar, K., Prakash, A. (2019). Examination of sustainability reporting practices in Indian banking sector. Asian Journal of Sustainability and Social Responsibility, 4(2): 1-16.

[51] Khan, M.H., Muktar, S.N. (2020). A bibliometric analysis of green human resource management based on scopus platform. Cogent Business &Management, 7: 1831165. https://doi.org/10.1080/23311975.2020.1831165

[52] Mahdy, F., Alqahtani, M., Binzafrah, F. (2023). Imperatives, benefits and initiatives of green human resource management (GHRM): A systematic literature review. Sustanability, 15: 4866. https://doi.org/10.3390/su15064866

[53] Reserve Bank of India. (2023). RBI releases 2023 list of domestic systematically important banks (D-SIBs). https://www.rbi.org.in.

[54] Yamane, T. (1967). Statistics: An Introductory Analysis. 2nd edition, Harper and Row, Newyork.

[55] Bagozzi, R.P., Yi, Y. (1988). On the evaluation of structural equation models. Journal of the Academy of Marketing Science, 16(1): 74-94. http://doi.org/10.1007/BF02723327

[56] Hair, J., Risher, J., Sarstedt, M., Ringle, C. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1): 2-24. https://doi.org/10.1108/EBR-11-2018-0203

[57] Henseler, J., Ringle, C.M., Sinkovics, R.R. (2009). Use of partial least squares path modelling in international marketing. Advances in International Marketing, 20: 277-319. https://doi.org/10.1108/S1474-7979

[58] Ramayah, T., Cheah, J., Chuah, F., Ting, H., Memon, M.A. (2018). Partial Least Squares Structural Equation Modelling (PLS-SEM) Using Smart PLS 3.0: An Updated Guide and Practical Guide to Statistical Analysis, 2nd ed. Kuala Lumpur Pearson, Malaysia.

[59] Ringle, C.M., Sarstedt, M. (2016). Gain more insight from your PLS-SEM results: The importance-performance map analysis. Industrial Management & Data Systems, 116(9): 1865-1886. http://doi.org/10.1108/IMDS-10-2015-0449

[60] Hair, J.F., Ringle, C.M., Sarstedt, M. (2013). Partial least squares structural equation modelling: Rigorous applications, better results and higher acceptance. Long Range Planning, 46(1-2): 1-12. https://doi.org/10.1016/j.lrp.2013.01.001

[61] Sharmin, S., Rahman, M.H.A., Karim, D.N. (2022). Green human resource practices and organizational citizenship behaviour towards the environment in the banking sector of Bangladesh. Bangladesh Journal of Public Administration, 30(1): 29-48. https://doi.org/10.36609/bjpa.v3011.111