Ang Swat Lin Lindawati*![]() | Yoan Dwilliam Agata

| Yoan Dwilliam Agata![]() | Bambang Leo Handoko

| Bambang Leo Handoko![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Indonesia's engagement in the Sustainable Development Goals (SDGs) has prompted the implementation of mandatory SDG support measures for companies. However, challenges remain in the energy sector due to limited understanding and participation. This study investigates the effects of Green Innovation and Creating Shared Value as independent variables on the dependent variable Environmental Development Pillar, focusing on energy sector companies listed on the Indonesia Stock Exchange (IDX) from 2017 to 2021. Content analysis was employed to extract information from corporate sustainability reports regarding SDG-related disclosure, specifically Goals 6, 11, 12, 13, 14, and 15. A purposive sampling technique yielded a sample of 66 energy sector companies, with 10 meeting the selection criteria. Multiple linear regression analysis, conducted using SPSS version 29, revealed a significant influence of Green Innovation and Creating Shared Value on the Environmental Development Pillar. This study suggests that energy sector companies should prioritize environmentally conscious and socially responsible policies and that the Indonesian government should assess the Environmental Development Pillar guidelines, adapting them to various corporate sectors within the country.

green innovation, creating shared value, environmental development pillars, sustainable development goals

1.1 Research background

Environmental problems arise due to disruptions in natural ecosystems, which are often linked to irresponsible human activities. The impact of ecosystem damage results from deforestation, air pollution, and other polluting activities. These changes in ecosystems lead to the emergence of climate change effects, which significantly impact people's lives. The United Nations must address environmental degradation concerning threats, challenges, and climate change, such as 60% of tropical forest fires occurring in the Amazon rainforest and deforestation leading to the depletion of global oxygen [1]. Uncertain climate change conditions can affect economic growth, potentially leading to poverty for those who depend on agriculture and weather-dependent jobs [2]. One factor contributing to climate change is the use of non-renewable resources such as coal and oil. Energy sector companies in Indonesia play a role in obtaining coal and oil to meet people's energy needs. Indonesia is still heavily reliant on non-renewable energy, with daily consumption of engine fuel recorded at 800 thousand barrels of oil. The Ministry of Energy and Mineral Resources' strategy, which refers to the 2022 National Electricity General Plan for New Energy and Renewable Energy, requires an energy mix for power plants in 2025 with 55% coal. The demand for electricity is expected to continue increasing, reaching 2,500 Terra Watt Hour (TWh) by 2050 [3]. According to research by Rahman et al. [4], Indonesia has great potential for implementing an energy mix, but factors affecting the energy transition include excessive oil subsidies, an overlooked oil buffer strategy, and the political economy of coal usage.

Indonesia is committed to addressing global issues by actively participating in the Sustainable Development Goals (SDGs). The country has made it mandatory for companies to support the SDGs, as stated in the Financial Services Authority (OJK) Regulation No. 51/POJK.03/2017, which prescribes a company's obligation to produce a sustainability report. The National Development Planning Agency designed the implementation of SDGs in Indonesia, referred to as the Environmental Development Pillar metadata. This framework has been adapted from the United Nations Development Program's SDGs to suit Indonesia's unique situation and conditions.

The metadata aims to provide understanding for all stakeholders in the preparation, implementation, monitoring, and evaluation of SDG reporting. It also serves as a reference for measuring Indonesia's SDG achievements, enabling comparisons with other countries and among provinces, districts, and cities within Indonesia. The Environmental Development Pillar includes six main goals: Goal 6 Clean Water and Sanitation, Goal 11 Sustainable Cities and Communities, Goal 12 Responsible Consumption and Production, Goal 13 Climate Action, Goal 14 Life Below Water, and Goal 15 Life on Land.

Challenges in implementing the SDGs in the Indonesian energy sector arise from the low understanding and participation of companies in using the SDGs as guidelines to be followed. Research by Andrian et al. [5] reveal that the percentage of report disclosures related to the Sustainable Development Goals (SDGs) in non-financial sector companies from 2017 to 2019 does not reach 50% of all companies in Indonesia. The contribution of energy sector companies in disclosing sustainability reports in 2019 included the mining industry, which recorded only seven sustainability reports with a percentage of 28.00%; mining minerals, with three sustainability reports and a percentage of 44.44%; and oil and gas, with merely two sustainability reports at a percentage of 18.18%. Researchers identified factors that influence the disclosure of Sustainable Development Goals on the Environmental Development Pillar in Indonesia, using Green Innovation and Creating Shared Value variables, which employ the stakeholder theory approach and legitimacy theory.

The research that will be conducted discusses the relationship between Green Innovation and Creating Shared Value (CSV) based on an analysis conducted on the Sustainability Report (SR) of energy sector companies listed on the Indonesia Stock Exchange from 2017 to 2021. The research uses SR reports on sector companies’ energy listed on the Indonesia Stock Exchange from 2017 to 2021 because the preparation of the SR is guided by the Global Report Initiative (GRI) as reporting principles, standard disclosures, and implementation guidelines that must be followed for all corporate sectors. The GRI Guidelines contain disclosures on corporate governance approaches, performance, environmental, social, and economic impacts. Researchers use the research period from 2017 to 2021 as the effective period since the GRI Standard for company guidelines in issuing sustainability reports. This study aims to provide an implementation of the application of Green Innovation and Creating Shared Value related to the Pillars of Environmental Development in Indonesian energy sector companies. The sector plays an important role in achieving sustainable development success in creating affordable energy and minimizing environmental damage. Researchers are motivated by Indonesian energy sector companies because this sector contributes to environmental problems such as activities that damage the environment due to exploration in obtaining natural resources, reduced agricultural land and deforestation, pollution due to carbon dioxide exhaust gases, increasing temperatures due to depletion of the ozone layer, causing waste such as fly ash and bottom ash in coal, and decreased water quality.

Phenomena above that triggers us to make this research using green innovation variables, creating shared values and achievement of environmental development pillars.

1.2 Research questions

The following are research questions that we will answer using hypothesis testing in this study:

Does green innovation has significant effect on achievement of environment development pillars?

Does creating shared value has significant effect on achievement of environment development pillars?

The explanation discussed earlier shows that Indonesia has a strong commitment to being involved in the implementation of the Sustainable Development Goals (SDG) because Indonesia has guidelines for the Environmental Development Pillar in preserving and protecting the environment which is based on SDG important points. Policies that have been issued by the government such as regulation No. 51/POJK.03/2017 which stipulates the obligation of companies to make sustainability reports can be an opportunity for companies in Indonesia to contribute to making reports related to SDG. This policy also requires companies to be more creative in creating innovations and identification to overcome social and environmental problems because companies are obliged to fulfill legitimacy and involve all stakeholders.

This research focuses on energy sector companies that are listed on the Indonesia Stock Exchange from 2017 to 2021. Energy sector companies are companies that play an important role in meeting the energy needs of society, but their activities have a direct impact on the surrounding environment and society. Green Innovation (GI) can be a way for companies to innovate and develop products or processes that pay more attention to the environment. Research conducted by Awan et al. [6] related to the influence of stakeholder pressure to develop Green Products and Green Processes can help companies create green innovations in climate change mitigation, dealing with waste, preventing water pollution, reducing the risk of threats to human health, and preservation of biodiversity. The development of green innovation products in fulfilling legitimacy has directly contributed to the Environmental Development Pillar for environmentally friendly product investment in utilizing renewable energy [7].

Creating Shared Value can be a way for companies in the energy sector to identify ways to overcome social and environmental problems to have a positive impact on companies, society, and nature. Research from Kim [8] Legitimacy can be used by companies to identify CSV applications that contribute to achieving the Environmental Development Pillars in understanding economic, social, and environmental problems. CSV is a business strategy that is suitable for stakeholders in improving company performance by creating sustainable innovations so that social and environmental problems can be resolved by leading to the Environmental Development Pillar [9].

Energy sector companies can apply Green Innovation and Creating Shared Value to fulfill legitimacy and involve stakeholders to contribute to achieving the implementation of the Environmental Development Pillar in Indonesia. The framework described in Figure 1 shows the relationship between Green Innovation and Creating Shared Value towards the Environmental Development Pillar.

Figure 1. Research framework

The use of Green Innovation and Creating Shared Value variables will be discussed in the literature review which will be discussed below. The development of this hypothesis is formed through theories that are by the two variables. Green Innovation is useful for companies in developing ideas or innovations that pay attention to the environment and their impacts. The innovation development carried out by the company also needs to identify environmental and social problems by Creating Shared Value. The effect of these two variables influences the achievement of the Environmental Development Pillars in Indonesia.

3.1 Effect of green innovation on achievement of environmental development pillars

The development of the hypothesis on Green Innovation influences the Achievement of the Environmental Development Pillar which is built using legitimacy theory and stakeholder theory. The legitimacy faced by companies also encourages companies to try to develop environmentally friendly sustainable practices [7]. Legitimacy is used to provide assumptions to the community about fulfilling community expectations in social and environmental activities [10]. Stakeholder behavior will influence companies in developing environmentally friendly products [11].

Research by Shu et al. [12], which used a legitimacy theory approach, found that Green Innovation had a positive influence on the Environmental Development Pillars. The application of Green Innovation followed by the company's obligation to legitimacy for create products or processes that are more environmentally friendly can increase company awareness in adapting to the Environmental Development Pillar. Research by Galindo-Martín et al. [13] uses stakeholder theory states that Green Innovation has a positive influence on the Environmental Development Pillars. Green Innovation provides a boost in company performance because the resulting green processes, techniques, and products aim to prevent environmental damage and show stakeholders that the company contributes to protecting the environment in harmony with the achievements of the Environmental Development Pillars. The literature that has been discussed shows that Green Innovation and the Environmental Development Pillar have a reciprocal relationship in preserving the environment, especially in implementing green innovation processes and products in energy sector companies. The implementation of green innovation processes that have been carried out by companies such as clean production, pollution control, and environmental competence in a sustainable manner has a relationship with the Environmental Development Pillar [14]. Based on the description above, the first hypothesis in this study is:

H1: Green Innovation has positive effect on achievement of environmental development pillars.

3.2 Effect of creating shared value on achievement of environmental development pillars

The development of the Creating Shared Value hypothesis for the Achievement of the Pillars of Environmental Development is built on legitimacy theory and stakeholder theory. Company legitimacy must depend on the norms and standards that apply in society, if the norms and standards regarding legitimacy have not been established, the company must identify them to adapt to conditions in that environment [15]. Creating shared value for all stakeholders is a principle of stakeholder theory that will later affect entities within the company [16].

Creating Shared Value (CSV) arises from research conducted by Porter [17] regarding three strategies for implementing CSV, namely reconceiving products and markets which require companies to create sustainable product innovations, redefining productivity in the value chain which aims to design operational standards in the company productively or sustainably by involving the entire company's value chain, and creating an enabling local environment that creates added value or opportunities that involve all stakeholders in the company.

Saenz [18] found the identification of Creating Shared Value (CSV) which is by company activities in the energy sector related to social, environmental, and economic issues through their level of influence, namely Highest Materiality is a company activity that has a significant influence or impact on CSV both internally and externally to the company, Medium to High Materiality is a company activity that has a CSV effect on the external company but has little effect on the internal company. Low Materiality is a company activity that has less influence on CSV internally and externally.

Fraser [19] uses stakeholder theory states that Creating Shared Value (CSV) has a positive influence on the Environmental Development Pillar. The Creating Shared Value strategy can increase the achievement of the Environmental Development Pillar by collaborating with stakeholders to enhance the company's development and can lead to investment to address social and environmental issues. Research from Kim [8] which uses legitimacy theory finds that Creating Shared Value (CSV) has a positive influence on the Environmental Development Pillar. Legitimacy can be used by companies to identify CSV implementation that contributes to achieving the Environmental Development Pillar in understanding economic, social, and environmental issues while the Environmental Development Pillar will assist in Creating Shared Value in providing relevance of targets and goals in meeting the company's values and needs to adjust with the activities set out in the Environmental Development Pillars. Based on the description above, the first hypothesis in this study is:

H2: Creating Shared Value has positive effect on achievement of environmental development pillar.

4.1 Research method

The research method used is mixed method. We used combination of quantitative causal and qualitative content analysis. Quantitative causal is used in order to test the hypothesis using ordinary least square. Qualitative content analysis is aims to obtain information from the sustainability report by providing a code to make it easy to understand.

We use dummy variable for the quantitative method. The dummy variable consists of code "1" which means that the disclosure is following the criteria of the Environmental Development Pillar, Green Innovation, and Creating Shared Value, and the code of "0" which means that the disclosure does not comply with the criteria of the Environmental Development Pillar, Green Innovation, and Creating Shared Value. The results of this analysis will be recorded as a score based on the interpretation made [5].

Population of this study is company that has been listed in Indonesia Stock Exchange (IDX). We use purposive sampling to determine the sample of this study. Sample is determined through three sampling criteria requirements, namely:

Companies listed on the Indonesia Stock Exchange from 2017 to 2021,

Companies that issued sustainability reports for up to 5 consecutive years (2017 to 2021),

Companies that made sustainability reports based on Global Reporting Initiative guidelines.

Based on above criteria using purposive sampling, we found 10 energy sector companies listed on the Indonesia Stock Exchange from 2017 to 2021 that met the criteria for become research sample. Data obtained from 10 energy sector companies from 2017 to 2021 (5 years). So the total numbers of sample are 50 research objects from each company's sustainability report. Data processing was analyzed using software of Microsoft Excel and SPSS version 29 which presented data in descriptions, tables, and graphs. The number of 50 research object is considered as reliable, because it refers to the approach of (Roscoe 1975) which says that the appropriate number of samples is between 30 - 500 samples. We also conducted a robust test with dummy data of 50 samples to ensure that this number met the data quality test.

4.2 Measurement of variable

Measurements made on the Green Innovation variable combine two previous studies. The first researcher Xie [20] found Green Innovation practices that have a relationship between Green Product Innovation and Green Process Innovation. The second researcher Zhang [21] found six Green Innovation activities that are suitable for energy sector companies. The results of the merger produce Green Product Innovation measurements which consist of green innovation programs, green patents, or green innovation product inventions, and protecting natural biodiversity. In line with research by Lin et al. [22] companies carry out activities and have products that prevent environmental damage by implementing green innovation programs. The company developed a green patent [11]. The company also manages biodiversity and environmental ecology [23]. Green Process Innovation consists of saving water, increasing activities in the development of water resources, and overcoming the problems of waste generated. In line with research by Ma et al. [24], companies can utilize technology as a method used for monitoring and managing wastewater and facilities that reduce waste. The innovations implemented by companies in implementing green processes will overcome the problems of environmental pollution, consumption of natural resources, and cost savings [25].

Measurements made on the Creating Shared Value (CSV) variable used previous research in identifying CSV. Saenz [18] found the identification of CSV by company activities in the energy sector related to social, environmental, and economic issues through their level of influence, namely Highest Materiality is a company activity that has a significant influence or impact on CSV both internally and external company, Medium to High Materiality is a company activity that has CSV influence on the company's external but less influence on the company's internal. Low Materiality is a company activity that has less influence on CSV internally and externally.

5.1 Descriptive statistic

First, we present the descriptive statistic of this study. The descriptive statistic is presented in Table 1.

Table 1. Descriptive statistics

|

|

N |

Min |

Max |

Mean |

Std Dev |

|

EDP |

50 |

.03151 |

.42828 |

.2441528 |

.09534103 |

|

GI |

50 |

.50000 |

.83333 |

.7333333 |

.09523810 |

|

CSV |

50 |

.43403 |

.97222 |

.8300694 |

.11183599 |

|

Valid N |

50 |

|

|

|

|

The results of the descriptive statistical test in Table 1 descriptive statistics for the maximum value of the Environmental Development Pillar (EDP) of 0.4282 were obtained from the company PT. Bumi Resources Tbk. in 2019. Referring to the minimum value in the PPL variable of 0.0315 obtained from the company PT. Indika Energy Tbk. in 2017. The average value of the PPL variable is 0.2441 which means the results obtained are still low below 0.5. The results found can be assumed that of the 50 research samples, only 24.41% disclosed the Environmental Development Pillar. The results obtained indicate the low level of disclosure of the Environmental Development Pillar by energy sector companies listed on the Indonesia Stock Exchange (IDX) from 2017 to 2021. The low level of disclosure of Sustainable Development Goals disclosed by companies is due to a lack of overall understanding with a percentage below 50% of companies in the non-financial sector in Indonesia [5]. The standard deviation value of the PPL variable is 0.0953 which is smaller than the average value. These results show that the distribution of data in the study is homogeneous.

The average value of the GI variable is 0.7333, which means that the resulting average has exceeded 0.5 so it can be assumed that of the 50 research samples, 73.33% of companies disclose GI disclosures. These results show the good enthusiasm of energy sector companies in implementing the principles of Green Innovation in the company's value chain system. The standard deviation value obtained from the GI variable is 0.0952, so the result is smaller than the average value, indicating that the data in this study is homogeneous. The average value resulting from the CSV variable is 0.8300, which means that the resulting average has exceeded 0.5 so it can be assumed that of the 50 research samples, 83.00% of companies have implemented CSV. The data shows that many companies' involvement leads to CSV activities. The standard deviation value obtained from the CSV variable is 0.1118, so the result is smaller than the average value, indicating that the data in this study is homogeneous.

5.2 Hypothesis testing

Hypothesis testing in this study uses multiple linear regression analysis. The result is presented in Table 2.

Table 2. Linear regression

|

Model |

B |

Std Error |

Coefficient Beta |

t |

Sig |

|

|

-.369 |

.089 |

|

-4.159 |

.000 |

|

|

.246 |

.106 |

.246 |

2.334 |

.024 |

|

|

.521 |

.090 |

.612 |

5.799 |

.000 |

a. Dependent Variable: EDP

Table 2 shows that the Green Innovation (GI) Variable has a significance value of 0.024 which is less than 0.05 (0.024 <0.05) with a calculated t value (2.334) > t table (2.012). The results obtained show that Green Innovation (GI) influences the Environmental Development Pillar (EDP). The Creating Shared Value (CSV) variable has a significance of 0.001 with a value of less than 0.05 (0.001 <0.05) with a calculated t value (5.799) > t table (2.012). The results obtained show that Creating Shared Value (CSV) affects the Environmental Development Pillar (EDP).

5.3 Green product innovation

After hypothesis testing using multiple linear regression, then we analyze the green product innovation. The analysis is presented in Figure 2.

Figure 2. Green product innovation

Figure 2 shows the highest results in protecting biodiversity and nature and green innovation program for 5 consecutive years, but a significant decrease is seen in green patents. The energy sector company that made a complete disclosure of Green Product Innovation in 2017 was PT. Elnusa Tbk., in 2018 no company was found that did it in full, then in 2019 there were 3 companies, namely PT Indika Energy Tbk., PT. Bukit Asam Tbk., and PT. Medco Energi Internasional Tbk, in 2020 there are 2 companies namely PT. Bukit Asam Tbk. and PT. Perusahaan Gas Negara Tbk., lastly in 2021 there will be 2 companies, namely PT. Elnusa Tbk. and PT. Medco Energi Internasional Tbk. The activity most disclosed by companies in the energy sector with an average of 9.60 or almost all companies is the Protection of Biodiversity and Nature from 2017 to 2021. In line with the research of Hou et al. [23], the efforts made by companies in implementing green production also provide efforts to preserve and develop biodiversity and environmental ecology. Activities in other Green Product Innovations such as the Green Innovation Program are disclosed by most companies in the energy sector with an average of 8.80 from 2017 to 2021. Research by Lin et al. [22] companies contribute to providing products and activities that minimize environmental damage or the negative impact generated by the company by implementing green innovation practices as a program developed by the company. Another activity of Green Product Innovation is implementing Green Patents disclosed by companies in the energy sector with an average of 2.00 from all companies from 2017 to 2021. Implementation of Green Innovation by companies will provide good benefits for companies such as competitive advantages from products, development of company-owned patented products, and improvement of product quality [11].

Green Product Innovation activities that have been carried out by companies in the energy sector are related to the disclosure of the Environmental Development Pillars from 2017 to 2021 in Goals 11 Sustainable Cities and Communities indicator 11.4.1.(a) with an average of 3.20, Goals 12 Responsible Consumption and Production indicator 12.1.1 with an average of 6.40, indicator 12.4.2.(a) with an average of 9.00, indicator 12.7.1.(a) with an average of 5.20, indicator 12.7.1 .(b) with an average of 0.80, indicator 12.8.1.(a) an average of 4.40, and indicator 12.a.1 with an average of 3.80. Goals 13 Climate Action indicator 13.2.1 with an average of 8.20, indicator 13.2.2 with an average of 8.40, indicator 13.2.2.(a) with an average of 3.00, indicator 13.2.2.(b) with an average of 2.60, indicator 13.a.1.(a) with an average of 0.20. Goals 14 Life Below Water indicator 14.2.1 with an average of 5.80, and Goals 15 Life Below Land indicator 15.1.1 with an average of 5.40, indicator 15.3.1 with an average of 4.80, indicator 15.5. 1 with an average of 0.60, indicator 15.9.1.(a) with an average of 5.40, and indicators 15.a.1.(a) & 15.b.1.(a) with an average 6,20. Companies that implement Green Innovation to pay attention to the environment will be directly proportional to the company's awareness in adapting to the Pillars of Environmental Development [12]. Research by Li [7] states that the development of green innovation products has directly contributed to the Environmental Development Pillar as a form of environmentally friendly product investment in utilizing renewable energy. Line with research by Galindo-Martín [13] stated that Green Innovation provides a boost in company performance because the resulting green processes, techniques, and products aim to prevent environmental damage in line with the achievements of the Environmental Development Pillars.

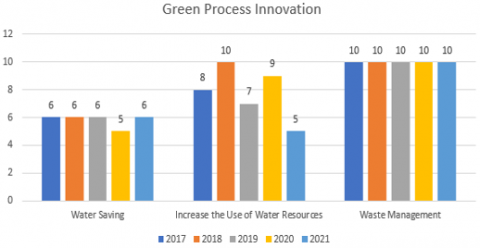

Figure 3. Green process innovation

Figure 3 shows the disclosure of complete waste management carried out by the company but water saving only received 6 disclosures during 2017 and 2019 then decreased to 5 disclosures in 2020, then increased the use of water resources experienced fluctuating disclosures for 5 years. 5 companies in the energy sector fully disclosed their Green Process Innovation in 2017, namely PT. AKR Corporindo Tbk., PT Petrosea Tbk., PT. Indo Tambangraya Megah Tbk., PT. Medco Energi Internasional Tbk., and PT. State Gas Company Tbk. 6 companies made full disclosures in 2018, namely PT Indika Energy Tbk., PT. Elnusa Tbk., PT Petrosea Tbk., PT. Indo Tambangraya Megah Tbk., PT. Medco Energi Internasional Tbk., and PT. State Gas Company Tbk. Disclosures found in 2019 there were 4 companies, namely PT. AKR Corporindo Tbk., PT Petrosea Tbk, PT. Indo Tambangraya Megah Tbk., and PT. State Gas Company Tbk. The disclosures made in 2020 included 4 companies, namely PT. AKR Corporindo Tbk., PT. Bumi Resource Tbk., PT Petrosea Tbk., and PT. Medco Energi Internasional Tbk. Disclosure found in 2021 there are 3 companies, namely PT. Bumi Resource Tbk., PT Petrosea Tbk., and PT. Indo Tambangraya Megah Tbk.

The activity carried out by the company in implementing Green Process Innovation is Overcoming Waste which is an activity that has been implemented by all companies in the energy sector with an average of 10.00 from 2017 to 2021. Research conducted by Ma et al. [24] implements green process innovation that aims to modify or change products using methods that further reduce the occurrence of environmental damage as well as improving technology in wastewater monitoring and management as well as the use of manufacturing that reduces waste at the source. Green Process Innovation that has been carried out by energy companies in activities to Increase Utilization of Water Resources has mostly been carried out by companies with an average of 7.80 from 2017 to 2021. The technology applied by companies in the green innovation process will be useful in reducing energy consumption and inefficient costs [25]. Green Process Innovation activities from Saving Water have mostly been expressed by energy sector companies with an average of 5.80 from 2017 to 2021. The use of technology such as recycling and monitoring water is a form of implementing Green Innovation in conserving water resources [24].

Green Process Innovation activities carried out by energy sector companies have a relationship with the disclosure of the Environmental Development Pillars from 2017 to 2021 in Goals 6 Clean Water and Sanitation indicator 6.1.1 with an average of 1.60, indicator 6.2.1 with an average of 7 .00, indicator 6.3.1.(a) with an average of 6.00, indicator 6.3.2.(a) with an average of 1.40, indicator 6.3.2.(b), indicator 6.4.2.( a) with an average of 7.80, indicator 6.4.2.(b) with an average of 5.20, indicator 6.5.1 with an average of 7.80, indicator 6.6.1 with an average of 1.40. Goals 12 Responsible Consumption and Production indicator 12.1.1 with an average of 6.40, indicator 12.4.2.(a) with an average of 9.00, indicator 12.5.1.(a) with an average of 3.00, Goals 14 Life Below Water indicator 14.2.1. with an average of 5.80. Research conducted by Khan et al. [14] regarding the implementation of green process innovation that has been carried out by companies such as clean production, pollution control, and environmental competence in a sustainable manner has a relationship with the Environmental Development Pillar. The application of green processes in company activities will result in efficient consumption of water resources and prevent environmental damage [26]. Saving water resources in implementing Green Innovation is aimed at mitigating climate change, overcoming risks to human health, and increasing awareness of environmental ecosystems [6].

Figure 4. CSV highest materiality

Creating Shared Value Highest Materiality has a big CSV influence on the company. Figure 4 shows companies that fully disclose CSV Highest Materiality activities in 2017, there are 4 companies, namely PT. Bumi Resources Tbk., PT. Elnusa Tbk., PT. Medco Energi Internasional Tbk., and PT. State Gas Company Tbk. 4 companies make full disclosure in 2018, namely PT. Bumi Resources Tbk., PT. Elnusa Tbk., PT. Bukit Asam Tbk., and PT. Indo Tambangraya Megah Tbk. 4 companies make full disclosure in 2019, namely PT. Bumi Resource Tbk., PT Indika Energy Tbk., PT. Elnusa Tbk., and PT. Indo Tambangraya Megah Tbk. 3 companies make full disclosure in 2020, namely PT Indika Energy Tbk., PT. Elnusa Tbk., and PT. Indo Tambangraya Megah Tbk. 4 companies make full disclosure in 2021, namely PT. AKR Corporindo Tbk., PT. Bumi Resource Tbk., PT Petrosea Tbk., PT. Indo Tambangraya Megah Tbk. Energy sector companies disclose CSV Highest Materiality activities which consist of 9 activities, namely the first is Waste and Hazardous Material Management with an average disclosure of 9.20 from 2017 to 2021.

The second activity of CSV Highest Materiality is Stakeholder Engagement which has been carried out by all energy sector companies with an average of 10.00 from 2017 to 2021. The third activity of CSV Highest Materiality is Water which has been disclosed by energy sector companies with an average of 8 .80 from 2017 to 2021. The fourth activity of CSV Highest Materiality is Environmental Compliance which has been disclosed by most companies in the energy sector with an average of 8.40 from 2017 to 2021. The fifth CSV Highest Materiality activity is Sustainable Benefits for Communities which has been disclosed by all energy sector companies with an average of 10.00 from 2017 to 2021. The sixth Highest Materiality CSV activity is the Rights and Engagement of Indigenous Peoples which has been disclosed by energy sector companies with an average of 6.00 from 2017 to 2021. CSV Highest Materiality activity to Human Rights has been disclosed by most energy sector companies with an average of 8.80 from 2017 to 2021. The eighth Highest Materiality CSV activity, namely Workforce Safety and Health, has been disclosed by energy sector companies with an average of 9.60 from 2017 to 2021. The ninth Highest Materiality CSV activity, namely Governance, and Accountability, has been disclosed by energy sector companies with an average of 8.20 from 2017 to 2021.

The activity of Creating Shared Value Highest Materiality carried out by companies in the energy sector correlates with the disclosure of the Pillars of Environmental Development from 2017 to 2021 in Goals 6 Clean Water and Sanitation indicator 6.1.1 with an average of 1.60, indicator 6.2.1 with an average 7.00, indicator 6.3.1.(a) with an average of 6.00, indicator 6.3.2.(a) with an average of 1.40, indicator 6.5.1 with an average of 7.80, indicator 6.6.1 with an average of 1.40, Goals 11 Sustainable Cities and Communities indicator 11.1.1.(a) with an average of 3.40, indicator 11.2.1.(a) with an average of 1.80, indicator 11.2.1.(b) with an average of 0.60, indicator 11.4.1.(a) with an average of 3.20, indicator 11.7.1.(a) with an average of 1.20, indicator 11. c.1.(a) with an average of 6.80. Goals 12 Responsible Consumption and Production indicator 12.1.1 with an average of 6.40, indicator 12.4.2.(a) with an average of 9.00, indicator 12.6.1.(a) with an average of 9.40, indicator 12.8.1.(a) with an average of 4.40, indicator 12.b.1.(a) with an average of 2.20, Goals 13 Climate Action indicator 13.2.1 with an average of 8.20, Goals 14 Life Below Water indicator 14.2.1. with an average of 5.80. The indicators in the CSV Medium to High Materiality for the seventh Human Rights and eighth Workforce Health and Safety did not find any conformity with the disclosure information on the Environmental Development Pillars.

Creating Shared Value Highest Materiality has an impact on companies both internally and externally in the energy sector [18]. Creating Shared Value strategy can increase the achievement of the Environmental Development Pillar in identifying community needs that must be carried out so that company development can lead to investment to address social and environmental problems [19]. Creating Shared Value is a profitable business strategy for improving company performance by creating sustainable innovations so that social and environmental problems can be resolved by leading to the Environmental Development Pillar [9].

The second identification of Creating Shared Value (CSV) is CSV Medium to High Materiality (1) having activities that affect the company's external but have less influence on the company's internal. Figure 5 shows the activities contained in the first CSV Medium to High Materiality (1) is Economic Performance which has been disclosed by all energy sector companies with an average of 10.00 from 2017 to 2021. The second CSV Medium to High Materiality (1) activity is Biodiversity and Land Use have been disclosed by most energy sector companies with an average of 9.60 from 2017 to 2021. The third CSV Medium to High Materiality (1) activity is Tax Strategy/Transparency which has been disclosed by energy sector companies with an average of 7.60 from 2017 to 2021.

The activity Creating Shared Value Medium to High Materiality (1) that has been carried out by companies in the energy sector is related to the disclosure of the Environmental Development Pillar from 2017 to 2021 on Goals 11 Sustainable Cities and Communities indicator 11.1.1.(a) with an average of 3.40, Goals 12 Responsible Consumption and Production indicator 12.1.1 with an average of 6.40, indicator 12.8.1.(a) with an average of 4.40, Goals 14 Life Below Water indicator 14.2.1 with an average 5.80, Goals 15 Life Below Land indicator 15.1.1 with an average of 5.40, indicator 15.3.1 with an average of 4.80, indicator 15.9.1.(a) with an average of 5.40, indicator 15.a.1.(a) and 15.b.1.(a) with an average of 6.20. The CSV Medium to High Materiality (1) activity, namely Tax Strategy/Transparency is not aligned with the disclosure of indicators on the Environmental Development Pillar. CSV can help the Environmental Development Pillars to contribute to understanding economic, social, and environmental problems [8].

Figure 5. CSV medium to high materiality (1)

Figure 6 shows the first CSV Medium to High Materiality (2) activity is Ethics which has been disclosed by most companies in the energy sector with an average of 9.20 from 2017 to 2021. The second CSV Medium to High Materiality (2) activity is Anticorruption and Compliance has been implemented by energy sector companies with an average of 9.60 from 2017 to 2021. The third CSV Medium to High Materiality (2) activity is Diversity which has been disclosed by energy sector companies with an average of 9.00 from 2017 to 2021. The fourth CSV Medium to High Materiality (2) activity is Inclusion and Equality which has been disclosed by energy sector companies with an average of 9.60 from 2017 to 2021. The fifth CSV Medium to High Materiality (2) activity is Workforce Engagement and Management has been implemented by energy sector companies with an average of 9.20 from 2017 to 2021. The sixth CSV Medium to High Materiality (2) activity is Air Quality has been disclosed by energy sector companies with an average of 4.80 from 2017 to 2021. The seventh CSV Medium to High Materiality (2) activity is Energy Management has been disclosed by energy sector companies with an average of 9.60 from 2017 to 2021. The eighth Medium to High Materiality (2) CSV activity, Climate Change, has been disclosed by energy sector companies with an average of 8.80 from 2017 to 2021.

The three CSV Medium to High Materiality (2) activities, namely Air Quality, Energy Management, and Climate Action, have a relationship that is in line with the disclosure of the Environmental Development Pillar in Goals 11 Sustainable Cities and Communities indicator 11.6.2.(b) with an average of 0,40, Goals 12 Responsible Consumption and Production indicator 12.6.1.(a) with an average of 9.40, indicator 12.a.1 with an average of 3.80, Goals 13 Climate Action indicator 13.2.1 with an average 8.20, indicator 13.2.2 with an average of 8.40, indicator 13.2.2.(a) with an average of 3.00, indicator 13.2.2.(b) with an average of 2.60, indicator 13.3.1.(a) with an average of 2.20, and Goals 15 Life Below Land indicator 15.9.1.(a) with an average of 5.40. The CSV Medium to High Materiality activities which consist of Ethics, Anticorruption and Compliance, Diversity, Inclusion, and Equality, and Workforce Engagement and Management are not related to the environmental development pillar disclosure indicators. CSV can be a way to identify sustainable business strategies through social issues and environmental issues that are in line with the Environmental Development Pillars [27].

Creating Shared Value Low Materiality is a CSV activity that has little influence on the company's internal and external. Figure 7 shows the CSV Low Materiality activity which has six CSV activities, namely the first Mine Closure has been disclosed by energy sector companies with an average gain of 4.00 from 2017 to 2021. The second CSV Low Materiality activity, namely Partnership, and Collaboration has been disclosed by some energy sector companies with an average of 9.80 from 2017 to 2021. The third CSV Low Materiality activity, namely Information and Asset Security, has been disclosed by energy sector companies with an average of 3.60 from 2017 to 2021. The fourth CSV Low Materiality activity is Supply Chain has been disclosed by energy sector companies with an average of 9.20 from 2017 to 2021. The fifth CSV Low Materiality activity, namely Emergency Preparedness, has been disclosed by energy sector companies with an average of 7.20 from 2017 to 2021. The sixth CSV Low Materiality activity, namely Public Policy, has been disclosed by the energy sector with an average of 6.00 from 2017 to 2021.

The activity of Creating Shared Value Low Materiality that has been carried out by companies in the energy sector correlates with the disclosure of the Pillars of Environmental Development from 2017 to 2021 on Goals 6 Clean Water and Sanitation indicator 6.2.1 with an average of 7.00, Goals 12 Responsible Consumption and Production, indicator 12.4.2.(a) with an average of 9.00, indicator 12.6.1 with an average of 10.00, indicator 12.6.1.(a) with an average of 9.40, Goals 13 Climate Action, indicator 13.1.2 with an average of 6.00, indicator 13.3.1.(a) with an average of 2.20, Goals 15 Life Below Land indicator 15.1.1 with an average of 5.40, indicator 15.3.1 with an average of 4.80, indicator 15.9.1.(a) an average of 5.40. CSV Low Materiality activity in Information and Asset Security and Supply Chain has no relation to the environmental development pillar disclosure indicators.

Figure 6. CSV medium to high materiality (2)

Figure 7. CSV low materiality

The results of the research that has been conducted show that the Environmental Development Pillars are related to Green Innovation (GI) and Creating Shared Value (CSV). Researchers found that green products and processes carried out by companies have a direct contribution to the application of green innovation through creating patents, preserving nature, management waste, saving and increasing water use which can be linked to the Environmental Development Pillar. The results of CSV identification through the level of materiality carried out for energy sector companies also directly contribute to the Environmental Development Pillar but several categories that are not relevant to environmental activities such as human rights, work safety, job training, tax strategy, ethics, anti-corruption, diversity, and equality due to the absence of categories that are by the guidelines for the Environmental Development Pillars. The results of this study can also be a recommendation for energy sector companies in implementing company policies that pay more attention to the environment and society. The Indonesian government can also carry out further evaluations regarding the Environmental Development Pillar guidelines so that it can adapt policies to various corporate sectors in Indonesia.

[1] Yoro, K.O., Daramola, M.O. (2020). CO2 emission sources, greenhouse gases, and the global warming effect. In Advances in Carbon Capture. Woodhead Publishing, pp. 3-28. https://doi.org/10.1016/B978-0-12-819657-1.00001-3

[2] Tol, R.S. (2018). The economic impacts of climate change. Review of Environmental Economics and Policy, 12(1): 4-25. https://doi.org/10.1093/REEP/REX027

[3] Reyseliani, N., Purwanto, W.W. (2021). Pathway towards 100% renewable energy in Indonesia power system by 2050. Renewable Energy, 176: 305-321. https://doi.org/10.1016/j.renene.2021.05.118

[4] Rahman, A., Dargusch, P., Wadley, D. (2021). The political economy of oil supply in Indonesia and the implications for renewable energy development. Renewable and Sustainable Energy Reviews, 144: 111027. https://doi.org/10.1016/j.rser.2021.111027

[5] Andrian, T., Sulaeman, P., Agata, Y.D. (2021). Sustainable development goal disclosures in Indonesia: Challenges and opportunities. Review of International Geographical Education Online, 11(3): 604-617.

[6] Awan, U., Sroufe, R., Kraslawski, A. (2019). Creativity enables sustainable development: Supplier engagement as a boundary condition for the positive effect on green innovation. Journal of Cleaner Production, 226: 172-185. https://doi.org/10.1016/j.jclepro.2019.03.308

[7] Li, D., Zheng, M., Cao, C., Chen, X., Ren, S., Huang, M. (2017). The impact of legitimacy pressure and corporate profitability on green innovation: Evidence from China top 100. Journal of Cleaner Production, 141: 41-49. https://doi.org/10.1016/j.jclepro.2016.08.123

[8] Kim, R.C. (2018). Can creating shared value (CSV) and the United Nations Sustainable Development Goals (UN SDGs) collaborate for a better world? Insights from East Asia. Sustainability, 10(11): 4128. https://doi.org/10.3390/su10114128

[9] Sukoharsono, E.G., Hariadi, B. (2020). The Meaningful practice creating shared value as a contribute to sustainable development goals: Case study at Pt Pupuk Kaltim. International Journal of Research in Business and Social Science, 9(7): 222-232. https://doi.org/10.20525/ijrbs.v9i7.934

[10] Deegan, C.M. (2019). Legitimacy theory: Despite its enduring popularity and contribution, time is right for a necessary makeover. Accounting, Auditing & Accountability Journal, 32(8): 2307-2329. https://doi.org/10.1108/AAAJ-08-2018-3638

[11] Dangelico, R.M. (2016). Green product innovation: Where we are and where we are going. Business Strategy and the Environment, 25(8): 560-576. https://doi.org/10.1002/bse.1886

[12] Shu, C., Zhou, K.Z., Xiao, Y., Gao, S. (2016). How green management influences product innovation in China: The role of institutional benefits. Journal of Business Ethics, 133: 471-485. https://doi.org/10.1007/s10551-014-2401-7

[13] Galindo-Martín, M.A., Castaño-Martínez, M.S., Méndez-Picazo, M.T. (2020). The relationship between green innovation, social entrepreneurship, and sustainable development. Sustainability, 12(11): 4467. https://doi.org/10.3390/su12114467

[14] Khan, P.A., Johl, S.K., Johl, S.K. (2021). Does adoption of ISO 56002-2019 and green innovation reporting enhance the firm sustainable development goal performance? An emerging paradigm. Business Strategy and the Environment, 30(7): 2922-2936. https://doi.org/10.1002/bse.2779

[15] Menghwar, P.S., Daood, A. (2021). Creating shared value: A systematic review, synthesis and integrative perspective. International Journal of Management Reviews, 23(4): 466-485. https://doi.org/10.1111/ijmr.12252

[16] Dmytriyev, S.D., Freeman, R.E., Hörisch, J. (2021). The relationship between stakeholder theory and corporate social responsibility: Differences, similarities, and implications for social issues in management. Journal of Management Studies, 58(6): 1441-1470. https://doi.org/10.1111/joms.12684

[17] Porter, M.E., Kramer, M.R. (2019). Creating Shared Value. In Managing Sustainable Business. Springer, Dordrecht. https://doi.org/10.1007/978-94-024-1144-7_16

[18] Saenz, C. (2019). Creating shared value using materiality analysis: Strategies from the mining industry. Corporate Social Responsibility and Environmental Management, 26(6): 1351-1360. https://doi.org/10.1002/csr.1751

[19] Fraser, J. (2019). Creating shared value as a business strategy for mining to advance the United Nations Sustainable Development Goals. The Extractive Industries and Society, 6(3): 788-791. https://doi.org/10.1016/j.exis.2019.05.011

[20] Xie, X., Huo, J., Zou, H. (2019). Green process innovation, green product innovation, and corporate financial performance: A content analysis method. Journal of Business Research, 101: 697-706. https://doi.org/10.1016/j.jbusres.2019.01.010

[21] Zhang, L., Zhao, S., Cui, L., Wu, L. (2020). Exploring green innovation practices: Content analysis of the fortune global 500 companies. SAGE Open, 10(1): 1-13. https://doi.org/10.1177/2158244020914640

[22] Lin, R.J., Tan, K.H., Geng, Y. (2013). Market demand, green product innovation, and firm performance: Evidence from Vietnam motorcycle industry. Journal of Cleaner Production, 40: 101-107. https://doi.org/10.1016/j.jclepro.2012.01.001

[23] Hou, C., Chen, H., Long, R. (2022). Coupling and coordination of China's economy, ecological environment and health from a green production perspective. International Journal of Environmental Science and Technology, 19(5): 4087-4106. https://doi.org/10.1007/s13762-021-03329-8

[24] Ma, Y., Hou, G., Xin, B. (2017). Green process innovation and innovation benefit: The mediating effect of firm image. Sustainability, 9(10): 1778. https://doi.org/10.3390/su9101778

[25] Hu, D., Wang, Y., Huang, J., Huang, H. (2017). How do different innovation forms mediate the relationship between environmental regulation and performance? Journal of Cleaner Production, 161: 466-476. https://doi.org/10.1016/j.jclepro.2017.05.152

[26] Shahzad, M., Qu, Y., Zafar, A.U., Appolloni, A. (2021). Does the interaction between the knowledge management process and sustainable development practices boost corporate green innovation? Business Strategy and the Environment, 30(8): 4206-4222. https://doi.org/10.1002/bse.2865

[27] Noh, J.E. (2020). Promotion of shared value for the SDGs (sustainable development goals): A case study of Australia. Journal of Sustainability Research, 2(3): e200025. https://doi.org/10.20900/jsr20200025