Jihad Satri*![]() | Hanaa Hachimi

| Hanaa Hachimi![]() | Chakib El Mokhi

| Chakib El Mokhi![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

In Morocco's port and foreign trade ecosystem, new electronic payment methods, such as online payments, have been introduced by public decision makers to speed up the payment process and thus the transit and clearance of goods. Despite their variety and availability, as well as their increased security, these new payment methods are not yet fully accepted by users in the port community, which makes the use of checks and cash still one of the most used payment methods. The proposed approach aims to encourage customers to use electronic payment methods in an ecosystem dominated by traditional payment methods by designing adaptive nudges from the three main domains: artificial intelligence, human-computer interaction, and user experience, in order to support this strategic decision towards electronic payment adoption. In fact, several studies have consistently shown that digital nudges are effective strategies for leveraging cognitive biases to positively influence user behavior and decision-making (Behavioral improvements ranging from 10% to 30% depending on the context and type of nudge). This article provides an illustration of the implementation of digital nudges through a well-defined process, drawing on evidence from other studies that have demonstrated the effectiveness of nudging. This approach is expected to influence user decisions in digital environments, particularly in the adoption of electronic payment methods, with the objective of achieving behavioral change of up to 30%. These insights offer a valuable foundation for researchers and practitioners focused on studying or designing information systems and interventions that support user decision-making in digital environments.

digital nudging, artificial intelligence, human-computer interaction, user experience, decision making, user

Throughout the main text, please follow these prescribed settings: 1) the font is mostly Times New Roman; 2) almost all the words are typed in 10 points; 3) each line throughout the paper is single-spaced; 4) in most cases, 10 pts spacing shall be left above and below any heading, title, caption, formula equation, figure and table.

As mentioned in the abstract section, it will be rather easy to follow these rules as long as you just replace the “content” here without modifying the “form”.

Morocco's port ecosystem has undergone a significant transformation with the introduction of a National Single Window, PortNet, aimed at simplifying foreign trade procedures. The project was initiated in 2008, in response to the growing competition in international trade and the consistent growth of Moroccan port traffic. The platform facilitates the digitization of documentation and streamlines formalities between the various stakeholders involved in foreign trade.

The foreign trade community includes a range of stakeholders, such as institutional bodies, ministries and public institutions (ANP, ADII, Ministry of Foreign Trade...), control agencies (ONSSA, MCDI...), banks, handling operators, shipping agents, importers and exporters, forwarders etc. (Figure 1).

Figure 1. Stakeholders

The PortNet Single Window simplifies and accelerates procedures and formalities for the entry or exit of goods. The flow of goods is improved; customs clearance is accelerated and transparency in the relationship between companies and administrations is increased. Among these main objectives:

The solution goes beyond just providing a 24/7 real-time payment platform through e-banking and m-banking channels. We also address the call by Weinmann et al. to mobilize behavioral sciences, specifically by applying a five-step process [1] for developing nudges in online decision environments, as shown in Figure 2. The goal is to influence and change the behavior of users who are still faithful to traditional payment methods like cash and checks. This innovative approach aims to meet three key criteria: desirability, sustainability, and feasibility. The solution is designed to address a specific need for instant payments, which would accelerate other administrative formalities. To better understand user expectations, a survey was conducted remotely, as outlined in the diagnosis chapter. In terms of sustainability, the project seeks to provide a strong return on investment for both customers and stakeholders in the port ecosystem by reducing processing times, uncovering hidden costs, and minimizing the ecological footprint. It also aims to rebuild trust with customers through nudging techniques, contributing to their overall well-being and enhancing the user experience. Finally, from a technical standpoint, the solution is highly feasible. The PortNet Single Window already has a solid technological infrastructure and a well-integrated collaboration system among stakeholders. However, expanding the solution to include other financial institutions offering 24/7 instant payment mechanisms is essential.

Figure 2. Nudging development process

The structure of this work is as follows. Section 2 gives a general review of digital nudging and electronic payment (EP) literature. In Section 3, the structure of our proposed method is described. Section 4 discusses the results obtained and suggested ideas for future research. Finally, the paper is concluded in Section 5.

2.1 Digital nudging

The concept of nudging as a mechanism of behavioral economics was popularized by a book by Thaler and Sunstein from 2008. Based on socio-psychological and cognitive theories, a nudge refers to a process or device that guides an individual's decision making, without constraint and in the individual's interest. As an incentive to do something, the purpose of a nudge is to transform an intention into an action, to provoke a change in order to solve a problem [2]. Adopted by governments for their citizens [3], then by companies or organizations to communicate with their clients or users [4, 5], nudge is a proposal that diverts each person from their "bad" practices, or from their attachment to the status quo, by leading them to make the right decision, without command, for their well-being or that of the community. This soft influence technique is considered, by its promoters, more efficient than the only recommendation or regulation, which it reinforces. In theory, the nudge, by its simplicity, can generate important beneficial changes, at a low cost.

Nudges are even more effective in a technological context since it is easier to create a controlled choice architecture that is not subject to the vagaries of the outside world. This is the development of what we call the user interface experience in the service of decision incitement through nudges: digital nudging. Digital nudging is defined by Weinmann et al. as: the use of user interface design elements to guide the behavior of individuals in digital choice architectures, by adjusting visual features and presenting choices in a deliberate way and by organizing navigation [6]. To put it simply, it is a matter of either modifying the content that constitutes the choice (in other words, the information displayed and that leads to the final choice) or the way in which the information is presented. Digital nudging is therefore a powerful weapon since an individual's decision making [7] is directly linked to the choice environment and therefore to the choice architecture. We can understand that the platform designer controls the implementation and a fortiori the degree of effectiveness of a nudge from A to Z. Moreover, nudges in a digital context are relatively easy, quick and very cheap to implement.

It is important to note that numerous studies have consistently demonstrated that digital nudges serve as highly effective strategies for harnessing cognitive biases to shape user behavior and decision-making in a positive direction [8-12]. Digital nudges exploit human tendencies, such as default bias or loss aversion, to encourage actions that align with desired outcomes. This has proven particularly valuable in domains like online payments [13-15], healthcare [16], and sustainable consumption [17], where nudges can lead to more informed, efficient, and beneficial decisions for users. As a result, the strategic application of digital nudges has become a powerful tool in both public policy and business, driving engagement and enhancing user experience across a wide range of digital platforms.

In concrete terms, to implement nudges in a digital context, the tools that make the user interface experience effective and successful are used, such as drop-down menus, radio buttons, check boxes, sliding bars, or pop-up windows. It depends on the objective that is decided upstream in the purpose of the nudge.

The personalization of "nudges" is an additional asset to support the transition to action [18]. Indeed, although we share systematic "inconsistencies" (our famous cognitive biases), we think and behave relatively differently depending on the context in which we find ourselves, and according to our personality or our motivations.

Our approach to promoting the adoption of the EP system in the PortNet platform involves the implementation of digital nudging through effective design of nudges and the use of artificial intelligence (AI) technologies [19-21] such as recommender systems [22, 23] and online communication channels such as email, SMS, graphical user interfaces (GUI), bots, or chatbots. These digital systems can interact with users in natural language, both written and spoken, and passively guide their choices towards the EP option. Our aim is to leverage these technologies to modify the user interfaces and encourage users to adopt EP.

Design is crucial for digital nudging, as human-computer interaction (HCI) research has extensively explored how to design technologies to be persuasive and promote behavior change. This has led to the emergence of common principles for good design [24, 25]. Digital nudging ultimately allows designers to select the right nudge, at the right time, for the right person, by learning to adapt to the user's state and context [26].

2.2 Electronic payment

EP methods have gained widespread adoption and have become an integral part of modern economies, transforming the way transactions are conducted across various sectors, including retail [27, 28], finance [29], transportation [30], and more. Even in the port ecosystem [31], EPs have become increasingly prevalent, providing numerous benefits to various stakeholders in terms of efficiency, security, cost savings, convenience, financial management, and sustainability. As technology continues to advance, EPs are expected to become even more prevalent in the port ecosystem, contributing to the overall growth and development of the industry.

In fact, according to Central Bank of Morocco reports, EPs in Morocco were gradually gaining traction, but cash transactions were still widespread in certain segments of the population. Mobile money services were becoming more prevalent, offering a convenient way for users to make payments, transfer money, and pay bills using their mobile phones. This expansion was driving financial inclusion in underserved areas. As well as, the rise of e-commerce was encouraging the use of EPs, as more consumers turned to online shopping. Digital payment options were increasingly preferred for purchasing goods and services from local and international merchants. In line with this trend, the Moroccan government was actively promoting the adoption of digital payments to modernize the financial sector and reduce reliance on cash transactions. Initiatives were in place to encourage businesses and consumers to adopt EP methods. Despite the growing popularity of EPs, concerns about security and the need for robust payment infrastructure persisted. In response, financial institutions and payment service providers are investing in secure technologies to address these concerns and ensure the safety of electronic transactions.

Given these points, the digital nudging strategy has numerous potential applications. It can be utilized to influence consumer behavior and to encourage the adoption of EP methods, such as credit/debit cards, mobile wallets, and other digital payment options. Field experiments can be designed and implemented to evaluate the effectiveness of various nudging techniques in influencing consumers to embrace EP [32]. Additionally, an experimental design could be developed with the aim of using adaptive nudges to influence consumer choices in multi-channel banking services [33]. This model considers factors such as social norms, perceived risk, gender-related and personality-related representations, and hypothesizes that individualized design features can nudge participants towards using the Internet channel for consumer credit. This contributes to the advancement of nudge theory by proposing adaptive, customer-specific nudges and exploring how multi-channel choices can be influenced. In the same fashion, credit card disclosure rules, such as those mandated by the CARD (Credit Card Accountability Responsibility and Disclosure) Act, can positively impact consumer debt repayment behavior [34]. The effects of the disclosures are primarily seen as an increased propensity to fully repay credit card debt each month. The study addresses potential criticisms of the CARD Act disclosures, including the fact that they only apply to paper statements and may have different effects on electronic bill payers. However, the study also acknowledges that the effectiveness of disclosure regulations may vary among different types of consumers, particularly those who are financially constrained. Similarly, the adoption of mobile payments in the United States remains low, partly due to concerns about security. However, carefully crafted informational interventions, such as nudges, can increase adoption of mobile payments [35]. Participants in the study who received nudges were more likely to use Apple Pay. Implementation intentions, in addition to nudges, may further help people translate intentions into action. While there is no one-size-fits-all solution, nudges and implementation intentions are potential tools to promote adoption of security-enhancing technologies like mobile payments.

3.1 Problematic

New EP methods, such as online payments, have been introduced to speed up the payment process and, consequently, logistics operations. This is expected to reduce costs and manage the waiting time for customs clearance. Despite the various solutions and initiatives of EP available to date, the adoption of online payment by economic operators/companies and its generalization among service providers is struggling to popularize. It can be seen that there is a clear and significant resistance to change when it comes to adopting new payment methods, particularly EPs, within certain organizations and industries, which is the case for the PortNet ecosystem. This resistance stems from various factors, including deeply ingrained management culture and established work habits that are often slow to evolve. Many organizations are accustomed to traditional payment systems, such as cash or checks, and may find it challenging to transition to newer, digital alternatives.

Fear and resistance to change, particularly in relation to new technologies, play a crucial role in this hesitation. Concerns about the complexity of implementing EP systems, lack of familiarity, and uncertainty about their long-term benefits often fuel this reluctance. Transaction security is another critical factor, as users may be skeptical about the safety and privacy of online transactions, especially in an era where cyber threats and data breaches are on the rise.

Furthermore, communication regarding the new payment methods is often inadequate or unclear, which can lead to confusion and mistrust. If users are not fully informed about the advantages, processes, and security measures associated with EPs, they are more likely to continue relying on familiar, traditional methods. Overcoming this resistance requires addressing these fears head-on, providing comprehensive education and support, and ensuring that the new payment methods are communicated effectively and transparently to all stakeholders involved.

However, the current methods are costly because additional verification steps are required. As a result, multiple challenges have been identified: delays in logistical procedures while waiting for payment, health risks during physical travel for payment, high mobilization of payment counters and manpower, etc. Thus, this situation directly impacts the customer experience and, consequently, the competitiveness of the national economy.

3.2 Survey

Prior to commencing the work, a survey was conducted remotely to understand and determine the payment method preferences of potential users within the port ecosystem. The survey questionnaire was initially prepared in French; a language suited to our target audience. In this endeavor, we opted for the convenience sampling method, which involves selecting individuals that are most readily available and accessible to the researcher. This method offers several advantages, such as ease of data collection, quick dissemination, and low cost. It is especially useful when time and resources are limited, and the focus is on obtaining responses from a specific group or well-defined population. Notably, PortNet possesses a database of PortNet users (comprising 64 945 clients) complete with their email addresses. This database served as the foundation for the development of an online questionnaire, tailored for distribution within this precisely targeted community. With respect to the intended population, as outlined in the published PortNet reports up to December 2022, we observe the following distribution of user profiles on the PortNet platform:

This comprehensive breakdown sheds light on the diverse range of participants engaging with the PortNet platform. Each of these profiles plays a crucial role in the port ecosystem, contributing to the smooth movement of goods, efficient logistics, and international trade. They collaborate to ensure that goods are transported, stored, and distributed effectively, while also adhering to various regulations and customs procedures.

Furthermore, the questionnaire combines multiple scales, which is especially interesting when the research aims to gather a comprehensive understanding of various constructs, attitudes, behaviors, or preferences. Combining different types of scales allows researchers to capture a broader range of information from participants, leading to a more nuanced and thorough analysis of the research topic. The scales employed in this study, ranging from 3 to 5, include the following:

The outcome of the questionnaire was impressive, with over 19 000 users participating in the survey from a diverse range of business sectors. Among the respondents, 78.7% identified themselves as importers (which makes sense given that the majority of the audience are importers), 14.9% as forwarders, 4.3% as freight forwarders, and 2.1% as exporters (Figure 3). Regarding the respondent’s sectors of activity (Figure 3), 38.3% are from the trade, commerce, and distribution sector, 12.8% from transport and logistics, 10.6% from textile, clothing, and footwear, and another 10.6% from the agri-food sector.

3.3 Diagnostic

The survey results revealed that 51.1% of the respondents preferred bank transfers, followed by 17% who preferred credit cards, 16.8% who preferred checks, and 15.1% who opted for other payment methods, including direct debit and cash. Furthermore, the survey results demonstrated the level of simplicity, speed, and availability of each payment method, as presented in Table 1. While a considerable number of respondents expressed their preference for using checks in certain scenarios, such as when the payment recipient does not accept other payment methods that the port user would have preferred, or when the payment amount is substantial and they do not have enough cash on hand, or simply because they find it more convenient and provides better expense management. It is evident that most port users acknowledge the benefits of EP. According to the survey results, 68.1% of the respondents had already used EP, and 63.8% of them reported that they had achieved cost and time savings through EP (Table 2).

Indeed, there is a clear indication of a desire to use EP more frequently than cash or checks, as demonstrated in Table 3. Specifically, 40.4% of respondents expressed a preference for making payments through e-banking, while 25.5% indicated a desire for an official instant payment platform enabling real-time transactions (Table 3).

Therefore, it is crucial to focus on individuals who are hesitant to adopt EP methods, and to devise strategies that can change their behavior and encourage greater usage of EP.

Figure 3. Respondent profiles and their business sectors

Table 1. Survey results (Simplicity, speed, and availability by payment type)

|

% |

Totally Agree |

Somewhat Agree |

Somewhat Disagree |

Totally Disagree |

|

Cash is easy to use? |

12.8 |

14.9 |

25.5 |

46.8 |

|

Cash allows you to pay very quickly? |

21.3 |

19.1 |

27.7 |

31.9 |

|

Cash is a means of payment that I always carry with me? |

2.1 |

25.5 |

34 |

38.4 |

|

Cash is suitable for paying any amount? |

0 |

2.1 |

19.1 |

78.8 |

|

With cash, it is possible to pay anywhere? |

17 |

25.5 |

25.5 |

32 |

|

Paying with cash allows you to control your spending? |

8.5 |

10.6 |

19.1 |

61.8 |

|

Cash is totally safe? |

12.8 |

14.9 |

23.4 |

48.9 |

|

The credit card is easy to use? |

66 |

21.3 |

8.5 |

4.2 |

|

The credit card allows to pay very quickly? |

68.1 |

17 |

10.6 |

4.3 |

|

The credit card is a means of payment that I always carry with me? |

66 |

12.8 |

8.4 |

12.8 |

|

The credit card is suitable for paying any amount? |

17 |

40.4 |

23.4 |

19.2 |

|

With the credit card, it is possible to pay anywhere? |

25.5 |

29.8 |

27.7 |

17 |

|

Paying with the credit card allows you to control your spending? |

46.8 |

29.8 |

12.8 |

10.6 |

|

The credit card is totally safe? |

36.2 |

36.2 |

19.1 |

8.5 |

|

When making an electronic payment (via credit card), have you ever been asked for additional information to authenticate yourself more securely, such as your date of birth or a verification code sent by SMS? |

59.6 |

17 |

4.3 |

19.1 |

|

The check is easy to use? |

27.7 |

42.5 |

17 |

12.8 |

|

The check allows to pay very quickly? |

19.1 |

29.9 |

25.5 |

25.5 |

|

The check is a means of payment that I always carry with me? |

29.8 |

25.5 |

25.5 |

19.2 |

|

The check is suitable for paying any amount? |

40.4 |

31.9 |

10.7 |

17 |

|

With the check, it is possible to pay anywhere? |

21.3 |

14.9 |

29.8 |

34 |

|

Paying with the check allows you to control your spending? |

42.6 |

34 |

10.6 |

12.8 |

|

The check card is totally safe? |

21.3 |

29.8 |

34 |

14.9 |

|

Do you support the elimination of the check as a means of payment? |

19.1 |

21.3 |

31.9 |

27.7 |

|

Bank transfer is easy to use? |

57.4 |

29.8 |

8.5 |

4.3 |

|

Bank transfer allows to pay very quickly? |

51.1 |

23.4 |

23.4 |

2.1 |

|

Bank transfer is a means of payment that I always carry with me? |

36.2 |

29.8 |

23.4 |

10.6 |

|

Bank transfer is suitable for paying any amount? |

48.9 |

36.2 |

8.5 |

6.4 |

|

With bank transfer, it is possible to pay anywhere? |

34 |

21.3 |

29.8 |

14.9 |

|

Paying with bank transfer allows you to control your spending? |

51.1 |

25.5 |

10.6 |

12.8 |

|

Bank transfer card is totally safe? |

66 |

25.4 |

4.3 |

4.3 |

Table 2. Survey results (EP – Part 1)

|

% |

Yes |

No |

No Opinion |

|

Are you familiar with the multi-channel payment solution offered by PortNet? |

61.7 |

38.3 |

|

|

Do you think PortNet's multi-channel payment solution is suitable for your B2B and B2G payments in connection with your import/export operations? |

54.3 |

8.7 |

37 |

|

Have you ever used EP methods in your company for port transit or import/export operations? |

68.1 |

31.9 |

|

|

If so, have you realized time and cost savings by using EP channels? |

63.8 |

4.3 |

31.9 |

Table 3. Survey results (EP – Part 2)

|

% |

No, Certainly Not |

No, Probably Not |

Yes, Probably |

Yes, Certainly |

|

|

For the payment of various port services, would you like to be able to use more EP rather than cash/check? |

12.8 |

2.1 |

25.5 |

59.6 |

|

|

% |

The Possibility to Pay via Online Banking (E-Banking) |

The Possibility of Instant Payment (in Real Time) via an Official Instant Payment Platform |

The Possibility to Pay with Your Cell Phone (Mobile Banking) |

The Possibility to pay Your Bills Online via a Specific Account: PayPal (if Authorized in Morocco) |

Others (Bank Transfer, Check, Cash) |

|

For the payment of port services, would you like to have each of the following means of payment? |

40.4 |

25.5 |

17 |

6.6 |

10.5 |

3.4 User journey

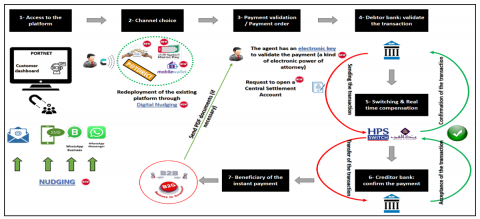

To complete all the necessary procedures in the current port system (Figure 4), the port user needs to go through several steps:

Figure 4. Functional architecture

Several challenges arise during these procedures, leading to delays in logistical processes and blockages caused by payment-related issues. These challenges include the involvement of multiple participants, lack of immediacy in transactions, unnecessary travel, and health risks. Waiting times become prolonged, and payment solutions are often inefficient, such as the time gap between the effective date and value date and insufficient transaction limits. Additionally, international payments pose difficulties due to heavy procedures and the involvement of numerous validators, among other issues.

Our goal is to enhance the existing platform (PortNet) and transform it into a comprehensive end-to-end solution that provides secure and instantaneous payment methods (available 24/7/365). The platform should be capable of completing all formalities within 24 hours while simultaneously improving the overall user/customer experience. Moreover, we aim to devise methods that encourage customers to adopt EP methods more frequently [36].

3.5 Designing adaptive nudges

The PortNet platform has undergone changes based on the principles of digital nudging. The platform's user interface has been redesigned to guide users through the available options, influencing their behavior towards adopting EP methods. User Experience (UX) design plays a crucial role in digital nudging for decision-making processes [37].

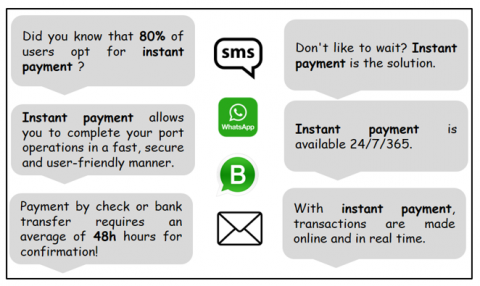

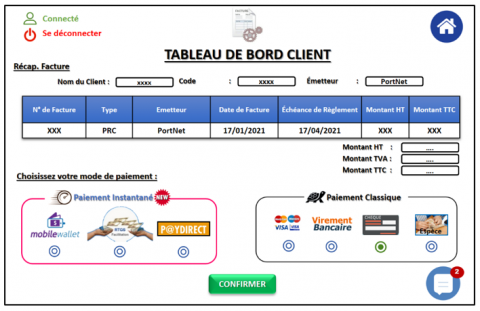

Upon authentication, the user lands on the Client dashboard screen (All web interfaces are in French, the language used on the PortNet platform) (Figure 5). New messages are available on the chatbot, which users can consult and interact with based on their navigation path on the platform. The chatbot serves as a guide to direct users towards different payment choices. Users also receive clear informative messages via SMS or WhatsApp to encourage them to make the best decisions (Figure 6). This aspect of the solution is vital as it will aid users in choosing EP methods. The concept is to merge nudging with AI using cognitive technologies [38]. In addition to the quick search area (Figure 5), the settings also feature a bill payment section that offers two payment blocks: classic payment and instant payment (Figure 7). The current version of the PortNet platform does not differentiate between these two types of payments. However, the updated version emphasizes instant payment over classic payment through graphical elements at the GUI level, such as the use of a turtle icon to indicate that choosing classic payment may slow down the process, and a speed icon to highlight the faster transaction speed of EP methods. These design elements serve to encourage users to choose EP over other payment options. The user's perception of payment methods is a crucial factor in their decision-making process. With this in mind, we have designed the platform's interface to convey the idea that classic payment methods take longer, while instant payments are much faster.

Figure 5. Client dashboard UI

Figure 6. Informative messages

Figure 7. Payment choice UI

Figure 8. Message box UI

To further simplify the process, we have also eliminated the intermediaries in a positive manner. For instance, users can pay directly with their bank card without having to go through an aggregator, which may charge additional fees.

When the user selects a classic payment method, such as paying by check, the Chatbot intervenes to influence the user's decision. It displays a message box, interrupting the process, to explain that this method requires an average of 48 hours for confirmation (Figure 8). The user is then given the choice to continue or change the payment method. If the user decides to proceed, the Chatbot asks for an explanation to add to our knowledge base (Figure 8). The same process applies to other classic payment methods. We aim to create an inadequate UX for classic payments by adding multiple messages and exchanges with the user. Additionally, we reinforce the informative component of the message by highlighting the disadvantages of this payment method. The frequency of the appearance of the message box can be set to a defined number, such as once every three payments.

The PortNet platform proposes three different modes of instant payment, which are grouped into one block for ease of use: Mobile Wallet, RTGS (real-time gross settlement), and PayDirect (Figure 7). For Mobile Wallet payments, the basket is segmented into three categories: banks, aggregators, and phone operators, allowing users to choose the Wallet that best suits their needs. An electronic validation key has also been added to overcome the problem of internal validation, which can be a bottleneck in some cases. With this solution, transactions are real-time and fully secured from end-to-end.

The second instant payment solution is RTGS. In this case, users have the option of creating a CCR (Central Settlement Account) or using an aggregator. This solution, as well as the P@YDirect solution, provide the same advantages as the Mobile Wallet payment option, including high levels of security and instantaneous transactions. Secret codes received via SMS are used to validate the transactions, and in some cases, an electronic validation key is required and communicated by the agent.

By offering these instant payment solutions, we aim to make the payment process more efficient and convenient for our users. Furthermore, by grouping the different modes of instant payment into one block and highlighting the advantages of using these methods over traditional payment methods, we hope to encourage users to adopt these new payment methods and ultimately improve their overall experience on the PortNet platform.

Figure 9. Technical architecture

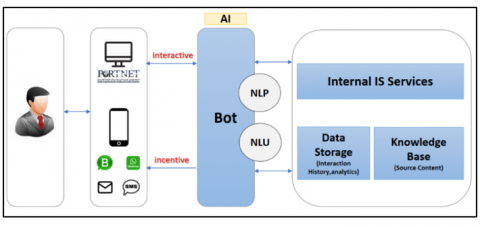

The proposed solution seamlessly integrates into the technical environment of the PortNet platform. On the front-end, we have the user interface (in our case, the interface of the PortNet platform) that facilitates the transmission of requests to the chatbot and returns the results to the user (Figure 9). The chatbot, in turn, responds to user requests using a preconfigured conversational decision tree, providing appropriate answers to a series of predetermined questions and enabling a real-time discussion between the chatbot and the user. This represents the interactive layer of the solution. Additionally, the chatbot includes an incentive messaging feature, where it sends messages to the user (via SMS/ WhatsApp/ Email) based on their navigation path on the platform, encouraging them to choose specific payment channels (Figure 6). Finally, the business layer of the chatbot generates the response body by leveraging the business services exposed by the information system (IS) through APIs.

The concept of "nudging" is increasingly relevant in the digital sphere, as more and more decisions are made on screens, such as mobile applications or websites. However, individuals in the digital environment are prone to make flawed decisions as they fail to process all relevant details to reach an optimal choice [39]. Nudging can be an effective tool to guide the decision making of users in the port community [40].

Table 4. Nudges implementation

|

Nudge |

Domain |

Type |

Effects |

|

Turtle icon |

HCI |

Change the digital environment |

Suggests that the payment option causes the process to lag. |

|

Speed icon |

HCI |

Change the digital environment |

Favors the choice of EP for its speed. |

|

Payment blocks |

HCI |

Change the digital environment |

Separation of choices to inform the user. |

|

Message box |

UX |

Provision of information |

To render UX lengthy and inadequate. |

|

Intermediaries payment |

UX |

Change the default option |

At the EP level, reducing payment middlemen means cutting out pointless processes that add to the expense and delay of the user experience. |

|

Chat bot |

AI |

Provision of information |

Evaluates and comprehends how users navigate the platform in order to provide recommendations. |

|

Informative messages |

AI |

Provision of information |

Give the user the information and facts they need to make the right decision. |

In this article, we have provided examples of digital nudges as shown in Table 4, categorized by type [41], to illustrate possible practical approaches following the process defined by Weinmann et al. [1]. This process is primarily based on (in accordance with our case study):

The main focus of this work is on the development and design of digital nudges aimed at promoting the adoption of EP among port users, informed by survey results from the port user. The initial step involved defining the context and objectives of promoting EP adoption, followed by outlining the approach for selecting relevant psychological effects to influence user behavior. Subsequently, we identified suitable nudges and implemented them on the PortNet platform. This demonstrates how designers can consider the effects of nudges when designing digital choice environments. The solution draws from three main domains in which nudges were used to encourage EP adoption:

These cues can take the form of visual design elements, such as placement of buttons or use of color, or they can be built into the functionality of the product, such as default settings or suggested options. The goal of digital nudging is to make it easier for users to make certain choices or complete certain actions, without limiting their freedom of choice.

While the proposed strategy appears to focus exclusively on the PortNet platform in this particular context, the scalability of these approaches across different industries or regions may face several challenges. One significant limitation is the diversity in user behavior and cultural attitudes towards technology adoption. What works well in the context of Morocco's port ecosystem may not be as effective in other settings where resistance to digital change, technology literacy, or transaction security concerns differ. Industries with more established digital infrastructures may require less emphasis on nudging, while sectors lagging in digital transformation might face greater hurdles in both the acceptance and application of these strategies. Furthermore, integration with non-Moroccan payment gateways (e.g., PayPal) requires regulatory alignment with local data laws, including compliance with cross-border data transfer rules, consumer protection standards, and security protocols. These considerations introduce technical and legal complexities that must be addressed before replicating the model elsewhere.

Another significant challenge in implementing digital nudges, particularly in sectors like digital payments, lies in the regulatory landscape. Different countries impose varying degrees of regulations on digital payments, data privacy, and security. These regulatory differences can significantly impact the scope and application of digital nudging strategies. In highly regulated environments, especially those with strict requirements on transparency and ethical behavior, the integration of AI-driven nudges may face serious constraints. This is particularly true when privacy laws require transparency in the use of user data, making it essential for organizations to clearly communicate how nudges are being applied, which could limit the subtlety that makes them effective.

Moreover, ethical concerns are paramount in this discussion. While nudges are designed to be unobtrusive and subtle, they must be applied with caution to avoid perceived manipulation or undue influence on users. This is especially important in industries where trust is critical, such as healthcare or finance. Aggressive nudging tactics in these sectors could potentially erode trust, leading to user resistance or even backlash. If users feel that they are being manipulated, especially without their full understanding or consent, the use of nudges could be seen as unethical, thus undermining the intended benefits of the intervention.

Addressing concerns about digital nudges requires a careful balance between guiding user behavior and preserving their autonomy. A thoughtful, context-specific approach is essential to ensure that nudges do not become manipulative, but instead empower users by enhancing their decision-making experience. This can be achieved by maintaining transparency, ensuring that users are aware of the nudges being employed and their purpose. By doing so, organizations foster trust, allowing users to feel in control of their choices while being subtly guided toward more beneficial outcomes. In the case presented in the article, this balance was achieved by designing nudges that provided clear information about the advantages of certain payment methods, such as highlighting the speed of electronic payments versus traditional methods. While the nudges steered users toward specific options, they were never forced into making a particular decision. Users retained full freedom of choice, with nudges acting as helpful suggestions rather than coercive prompts. This approach maintains user autonomy, making the interaction more user-friendly and respectful of individual preferences, while still encouraging a shift toward more efficient digital solutions. Ultimately, giving users the freedom to make informed decisions reinforces the positive impact of digital nudging without compromising ethical considerations.

The research will need to explore not only the technical and behavioral efficacy of digital nudging but also the ethical dimensions that govern its application. By integrating these ethical considerations, organizations can ensure that their digital nudges promote user empowerment rather than manipulation, while also adhering to regulatory guidelines.

In contexts where users may have limited access to digital infrastructure, nudges designed for highly connected environments might not be as effective. In rural areas or industries with lower digital literacy rates, traditional payment methods might persist, and the push towards EP adoption may be met with greater resistance. Here, more education and gradual transition strategies would be necessary, and nudges would need to be adapted accordingly.

On the other hand, the potential of this strategy, particularly the insights gained from the development and implementation of digital nudges in promoting EP adoption, holds significant promise for researchers and practitioners alike. These insights offer a useful starting point for those interested in researching or creating interventions and information systems that assist users in making decisions in digital environments.

By leveraging behavioral science, cognitive psychology, and UX principles, digital nudges provide a powerful framework for influencing user behavior in subtle but effective ways. For researchers, this strategy opens up avenues to explore how different psychological triggers can be integrated into information systems to guide users toward more efficient and beneficial decisions, such as the adoption of EP methods. It also serves as a practical example of how digital environments can be designed to reduce friction in decision-making, helping users navigate complex processes with minimal effort.

For practitioners, these findings provide actionable insights into how to craft user interfaces and digital experiences that not only meet business objectives but also create a more seamless and user-friendly experience. In sectors such as finance, e-commerce, healthcare, and government services, where digital transactions and decision-making are critical, the application of digital nudges can optimize user engagement and drive the adoption of more secure, efficient, and sustainable practices. The ability to tailor these nudges based on real-time data and user interactions, especially with the integration of AI, enhances the potential for creating personalized experiences that resonate with individual users.

Furthermore, this strategy is particularly valuable for organizations aiming to scale their digital services. By understanding how digital nudges can be used to promote specific user behaviors, practitioners can replicate successful interventions across different platforms, industries, or regions, adapting the approach as needed to suit varying user contexts. For example, the success of nudges in Morocco's port system could inform the design of similar strategies in industries such as retail, education, or transportation, where digital transformation is underway but still faces adoption barriers.

Further, it is important to track the user's behavior, as well as evaluating and measuring the effectiveness and efficiency of the implemented nudges. Measuring the effectiveness of nudges in a digital choice environment is generally done by comparing the behavior of users who were exposed to the nudge to those who were not. This can be done through A/B testing, where a randomly selected group of users is shown the nudge and the behavior of this group is compared to a control group that did not see the nudge. In fact, in our case, we need to make a comparative study of the statistics relating to the number of EP users before and after the implementation of digital nudges. The effectiveness of the nudge it can be measured by comparing metrics such as conversion rates, click-through rates, or time spent on a task. With respect to the efficiency of a nudge, it can be done by comparing the change in behavior to the cost of implementing the nudge. This can include the cost of designing and implementing the nudge, as well as any potential negative consequences of the nudge.

Moreover, it is important to consider the ethical considerations of the nudge, such as whether the nudge respects the user’s autonomy, and whether it's transparent, and non-manipulative [42].

Overall, measuring the effectiveness and efficiency of nudges in a digital choice environment requires a combination of quantitative and qualitative methods, including A/B testing, user surveys and interviews, and cost-benefit analysis.

In the final analysis, this concept can be harnessed to expedite the adoption of EPs in the Moroccan port ecosystem, primarily through the following comprehensive approach:

By strategically implementing digital nudging techniques, the Moroccan port ecosystem can accelerate the transition towards EPs, leading to increased efficiency, transparency, and financial inclusion in port operations [43]. It is essential for stakeholders to continuously assess the effectiveness of these nudging interventions and adapt their strategies based on real-time feedback and behavioral insights.

It is mandatory to have conclusions in your paper. This section should include the main conclusions of the research and a comprehensible explanation of their significance and relevance. The limitations of the work and future research directions may also be mentioned. Please do not make another abstract.

As technology becomes more pervasive in our daily lives, an increasing number of decisions will be made digitally. Digital nudging is a technique that leverages principles from behavioral science and information technology to gently steer users towards specific actions or choices through subtle cues or prompts. By studying and implementing digital nudging, we can gain a better understanding of human behavior and how minor nudges can influence it. In essence, digital nudging has the potential to transform our comprehension of decision-making and how we can shape those decisions.

In conclusion, this article demonstrates the potential of digital nudges in promoting the adoption of EP methods in a traditional payment ecosystem. By implementing adaptive nudges on the PortNet platform, we have shown how a well-defined process that integrates AI, HCI, and UX can alter user behavior towards EP methods. This example offers a model that can be adapted by other organizations aiming to increase the adoption of their digital services, while the insights gained provide a strong foundation for researchers and practitioners interested in studying or designing information systems and interventions that facilitate user decision-making in digital environments. Ultimately, this article highlights the importance of considering the effects of nudges when designing digital choice environments and the potential impact of this approach on user behavior.

Foremost, I would like to express my sincere gratitude to my supervisors Prof. Chakib el Mokhi and Prof. Hanaa Hachimi for their invaluable guidance and support throughout the writing process, for their patience, motivation, enthusiasm, and immerse knowledge. Their guidance helped me in all the time of research and writing of this paper.

[1] Weinmann, M., Schneider, C., Brocke, J.V. (2016). Digital nudging. Business & Information Systems Engineering, 58: 433-436. https://doi.org/10.1007/s12599-016-0453-1

[2] Thaler, R.H., Sunstein, C.R. (2009). Nudge: Improving Decisions about Health, Wealth, and Happiness. Penguin.

[3] Stroeker, N.E. (2016). An overview of behavioral economics in Dutch policy making. The next step: How to nudge policy makers. Apstract: Applied Studies in Agribusiness and Commerce, 10: 27-32. https://doi.org/10.22004/ag.econ.250216

[4] Bammert, S., König, U.M., Roeglinger, M., Wruck, T. (2020). Exploring potentials of digital nudging for business processes. Business Process Management Journal, 26(6): 1329-1347. https://doi.org/10.1108/BPMJ-07-2019-0281

[5] Tanaiutchawoot, N., Bursac, N., Rapp, S., Albers, A., Heimicke, J. (2019). NUDGES: An assisted strategy for improving heuristic decision in PGE-Product Generation Engineering. Procedia CIRP, 84: 820-825. https://doi.org/10.1016/j.procir.2019.04.294

[6] Eng, B.I.S. (2016). Markus Weinmann, Christoph Schneider & Jan vom Brocke.

[7] Qu, L., Xiao, R., Shi, W., Huang, K., Qin, B., Liang, B. (2022). Your behaviors reveal what you need: A practical scheme based on user behaviors for personalized security nudges. Computers & Security, 122: 102891. https://doi.org/10.1016/j.cose.2022.102891

[8] Haki, K., Rieder, A., Buchmann, L., W. Schneider, A. (2023). Digital nudging for technical debt management at Credit Suisse. European Journal of Information Systems, 32(1): 64-80. https://doi.org/10.1080/0960085X.2022.2088413

[9] Heinrich, T., Szasz, O. (2024). Evaluating design approaches for encouraging behavior change in editors: Exploring a digital nudging strategy in a non-personalized recommender system to promote adoption of augmented analytics. Proceedings of the Design Society, 4: 985-994. https://doi.org/10.1017/pds.2024.101

[10] Modin, D., Johansen, N.D., Vaduganathan, M., Bhatt, A.S., Lee, S.G., et al. (2023). Effect of electronic nudges on influenza vaccination rate in older adults with cardiovascular disease: Prespecified analysis of the NUDGE-FLU Trial. Circulation, 147(18): 1345-1354. https://doi.org/10.1161/CIRCULATIONAHA.123.064270

[11] Harder, T., Janneck, M. (2024). Digital nudging in online-learning environments: Enhancing self-regulation and decision through usability-centric design. In International Conference on Human-Computer Interaction, Switzerland, pp. 3-18. https://doi.org/10.1007/978-3-031-61672-3_1

[12] Purohit, A.K., Bergram, K., Barclay, L., Bezençon, V., Holzer, A. (2023). Starving the newsfeed for social media detox: Effects of strict and self-regulated Facebook newsfeed diets. In Proceedings of the 2023 CHI Conference on Human Factors in Computing Systems, New York, NY, United States, pp. 1-16. https://doi.org/10.1145/3544548.3581187

[13] Yogama, E.A., Gray, D.J., Rablen, M.D. (2024). Nudging for prompt tax penalty payment: Evidence from a field experiment in Indonesia. Journal of Economic Behavior & Organization, 224: 548-579. https://doi.org/10.1016/j.jebo.2024.06.003

[14] Bonan, J., d’Adda, G., Mahmud, M., Said, F. (2023). Nudging payment behavior: Evidence from a field experiment on pay-as-you-go off-grid electricity. The World Bank Economic Review, 37(4): 620-639. https://doi.org/10.1093/wber/lhad012

[15] Migchelbrink, K., Raymaekers, P. (2023). Nudging people to pay their parking fines on time. Evidence from a cluster-randomized field experiment. Journal of Behavioral and Experimental Economics, 105: 102033. https://doi.org/10.1016/j.socec.2023.102033

[16] de Vries, R., van den Hoven, M., de Ridder, D., Verweij, M., de Vet, E. (2022). Healthcare workers’ acceptability of influenza vaccination nudges: Evaluation of a real-world intervention. Preventive Medicine Reports, 29: 101910. https://doi.org/10.1016/j.pmedr.2022.101910

[17] Berger, M., Lange, T., Stahl, B. (2022). A digital push with real impact–Mapping effective digital nudging elements to contexts to promote environmentally sustainable behavior. Journal of Cleaner Production, 380: 134716. https://doi.org/10.1016/j.jclepro.2022.134716

[18] Hummel, D., Maedche, A. (2019). How effective is nudging? A quantitative review on the effect sizes and limits of empirical nudging studies. Journal of Behavioral and Experimental Economics, 80: 47-58. https://doi.org/10.1016/j.socec.2019.03.005

[19] Satri, J., El Mokhi, C., Hachimi, H. (2022). Artificial intelligence and machine learning for a better decision making in the public sector. In 2022 8th International Conference on Optimization and Applications (ICOA), Genoa, Italy, pp. 1-5. https://doi.org/10.1109/ICOA55659.2022.9934325

[20] Satri, J., El Mokhi, C., Hachimi, H. (2024). Predicting the outcome of regional development projects using machine learning. IAES International Journal of Artificial Intelligence, 13(1): 863-875. https://doi.org/10.11591/ijai.v13.i1.pp863-875

[21] Satri, J., Mokhi, C.E., Hachimi, H. (2022). Road accident forecast using machine learning. In the International Conference on Artificial Intelligence and Smart Environment, Springer International Publishing, pp. 701-708. https://doi.org/10.1007/978-3-031-26254-8_102

[22] Jesse, M., Jannach, D. (2021). Digital nudging with recommender systems: Survey and future directions. Computers in Human Behavior Reports, 3: 100052. https://doi.org/10.1016/j.chbr.2020.100052

[23] Sitar-Tăut, D.A., Mican, D., Buchmann, R.A. (2021). A knowledge-driven digital nudging approach to recommender systems built on a modified Onicescu method. Expert Systems with Applications, 181: 115170. https://doi.org/10.1016/j.eswa.2021.115170

[24] Sobolev, M. (2021). Digital nudging: Using technology to nudge for good. SSRN. https://doi.org/10.3138/9781487527525-023

[25] Mirbabaie, M., Ehnis, C., Stieglitz, S., Bunker, D., Rose, T. (2021). Digital nudging in social media disaster communication. Information Systems Frontiers, 23: 1097-1113. https://doi.org/10.1007/s10796-020-10062-z

[26] Schneider, C., Weinmann, M., Vom Brocke, J. (2018). Digital nudging: Guiding online user choices through interface design. Communications of the ACM, 61(7): 67-73. https://doi.org/10.1145/3213765

[27] Lok, C.K. (2015). Adoption of smart card-based e-payment system for retailing in Hong Kong using an extended technology acceptance model. E-services Adoption: Processes by Firms in Developing Nations, 23: 255-466. https://doi.org/10.1108/S1069-09642015000023B003

[28] Lai, P.M., Chuah, K.B. (2010). Developing an analytical framework for mobile payments adoption in retailing: A supply-side perspective. In 2010 International Conference on Management of e-Commerce and e-Government, Chengdu, China, pp. 356-361. https://doi.org/10.1109/ICMeCG.2010.79

[29] Claessens, S., Glaessner, T., Klingebiel, D. (2002). Electronic finance: Reshaping the financial landscape around the world. Journal of Financial Services Research, 22: 29-61. https://doi.org/10.1023/A:1016023528211

[30] Turban, E., Brahm, J. (2000). Smart card-based electronic card payment systems in the transportation industry. Journal of Organizational Computing and Electronic Commerce, 10(4): 281-293. https://doi.org/10.1207/S15327744JOCE1004_06

[31] Li, Y., Nie, Q. (2009). Study on the construction and development of Shanghai e-port System. In 2009 IEEE/INFORMS International Conference on Service Operations, Logistics and Informatics, Chicago, IL, pp. 295-299. https://doi.org/10.1109/SOLI.2009.5203948

[32] Aydogan, S., Van Hove, L. (2015). Nudging consumers towards card payments: A field experiment. In International Cash Conference 2014, Dresden, Germany, pp. 589-630.

[33] Hummel, D., Schacht, S., Maedche, A. (2017). Designing adaptive nudges for multi-channel choices of digital services: A laboratory experiment design. Association for Information Systems, Guimarães, Portugal, pp. 2677-2688.

[34] Jones, L.E., Loibl, C., Tennyson, S. (2015). Effects of informational nudges on consumer debt repayment behaviors. Journal of Economic Psychology, 51: 16-33. https://doi.org/10.1016/j.joep.2015.06.009

[35] Story, P., Smullen, D., Acquisti, A., Cranor, L.F., Sadeh, N., Schaub, F. (2020). From intent to action: Nudging users towards secure mobile payments. In Sixteenth Symposium on Usable Privacy and Security (SOUPS 2020), USA, pp. 379-415.

[36] Bukoye, O.T., Ejohwomu, O., Roehrich, J., Too, J. (2022). Using nudges to realize project performance management. International Journal of Project Management, 40(8): 886-905. https://doi.org/10.1016/j.ijproman.2022.10.003

[37] Mejtoft, T., Ristiniemi, C., Söderström, U., Mårell-Olsson, E. (2019). User experience design and digital nudging in a decision making process. In 32nd Bled e Conference: Humanizing Technology for a Sustainable Society, Bled, Slovenia, pp. 427-442.

[38] Mele, C., Spena, T.R., Kaartemo, V., Marzullo, M.L. (2021). Smart nudging: How cognitive technologies enable choice architectures for value co-creation. Journal of Business Research, 129: 949-960. https://doi.org/10.1016/j.jbusres.2020.09.004

[39] Mirsch, T., Lehrer, C., Jung, R. (2017). Digital nudging: Altering user behavior in digital environments. In 13th International Conference on Wirtschaftsinformatik, Switzerland, pp. 634-648.

[40] Hyytinen, A., Tuimala, J., Hammar, M. (2022). Enhancing the adoption of digital public services: Evidence from a large-scale field experiment. Government Information Quarterly, 39(3): 101687. https://doi.org/10.1016/j.giq.2022.101687

[41] Van Deun, H., van Acker, W., Fobé, E., Brans, M. (2018). Nudging in public policy and public management: A scoping review of the literature. In PSA 68th Annual International Conference, Cardiff, pp. 1-27.

[42] Renaud, K., Zimmermann, V. (2018). Ethical guidelines for nudging in information security & privacy. International Journal of Human-Computer Studies, 120: 22-35. https://doi.org/10.1016/j.ijhcs.2018.05.011

[43] Satri, J., Hachimi, H., El Mokhi, C. (2024). Nudging users towards embracing electronic payments. In the International Conference on Artificial Intelligence and Smart Environment, Springer Nature Switzerland, pp. 288-294. https://doi.org/10.1007/978-3-031-88304-0_39