Aaron Afan Izang*![]() | Oluwabukola F. Ajayi

| Oluwabukola F. Ajayi![]() | Omolayo Junaid

| Omolayo Junaid![]() | Bonaventure Nwigwe | Princewill Onyekachi Onyeka

| Bonaventure Nwigwe | Princewill Onyekachi Onyeka

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Peer-to-peer (P2P) student lending platforms have emerged as an alternative source of funding for students who are unable to obtain loans from traditional lenders. Traditional loan systems have become less accessible and affordable for all students, and information asymmetry is a significant challenge that can have serious consequences for lenders and borrowers. The rising cost of higher education in many countries has made it challenging for some students to access the funds they need to finance their education. This study aims to design and implement a P2P student lending system that addresses these challenges. The research conducted enables the production of a P2P loan framework using PHP, Mysql, and Javascript that incorporates essential features gleaned from literature and existing P2P applications. The study improves the payback rate by reducing information asymmetry in the P2P lending system using the following methods; detailed applicant profiles, robust credit scoring models, income verification, transparent loan terms, and peer reviews and ratings. The prototype software development model was used to develop the P2P framework. The system is evaluated against industry-relevant metrics, such as loan characteristics, credit risk, and loan performance. The software was developed using HTML, JavaScript, PHP, and CSS, with the Operating System being Microsoft Windows 11. The result of the research is a more accessible and transparent lending system that supports students who require funds to complete their education after a thorough verifiction process by the system. The system was evaluated based on the reviews and ratings gotten from the clients and users. The implementation of this system can significantly impact the education sector by increasing access to funding for students.

peer-to-peer lending, student loan, information asymmetry, credit risk, loan performance, P2P framework, software development, educational finance

Peer-to-peer (P2P) lending, also known as social lending or crowdfunding, is a type of financial transaction that occurs directly between individuals, without the need for traditional financial institutions such as banks or credit unions [1]. Peer-to-peer lending has grown in popularity over the past decade, and it has been used for various purposes such as business loans, personal loans, and student loans [2]. In particular, peer-to-peer student lending has emerged as a popular option for students who need to finance their education but are unable to obtain traditional student loans from banks or other financial institutions [3]. Nigeria has one of the largest numbers of schools, from primary to university level, both at public and private ownership with the most minimal sponsorship or loan opportunities.

The idea of peer-to-peer lending dates back to the early 2000s when a few companies, such as Zopa and Prosper, launched online platforms that allowed individuals to lend money directly to borrowers [4]. These platforms used sophisticated algorithms to match lenders with borrowers based on various criteria such as creditworthiness, loan amount, and interest rates. The idea behind peer-to-peer lending was to cut out the middleman, i.e., the banks, and provide borrowers with access to capital at lower interest rates than those offered by traditional lenders [5].

Peer-to-peer student lending gained popularity in the United States around 2006, when companies such as Fynanz and GreenNote launched online platforms that connected students with individual investors who were willing to lend them money [6]. These platforms allowed students to borrow money at competitive interest rates, and they offered investors the opportunity to earn higher returns than they could get from traditional savings accounts or CDs. Peer-to-peer student lending became widespread in the aftermath of the 2008 financial crisis when traditional lenders tightened their lending standards, making it harder for students to obtain loans [7]. Peer-to-peer student lending platforms offered an alternative source of funding for students who were unable to obtain loans from traditional lenders due to their credit history, income, or other factors.

Nigeria's educational financing faces challenges such as limited access to affordable loans, inadequate public funding, and a growing demand for education. Peer-to-peer (P2P) lending can address these issues by providing an alternative source of funding for students and institutions. P2P lending platforms connect borrowers directly with individual lenders, offering more accessible and flexible options. They reduce information asymmetry by providing transparent information about borrowers, allowing lenders to make informed decisions. P2P lending also allows for more flexible terms and conditions, allowing borrowers and lenders to negotiate terms that suit their preferences. It has a significant social impact by democratizing access to funding and integrating technology to streamline application and approval processes. Risk mitigation strategies like credit scoring models and social verification can help build a trustworthy and sustainable lending environment [8].

Here are some reasons why P2P lending is a good option for student [5]:

(1) Lower interest rates: P2P lending systems can offer lower interest rates to borrowers than traditional financial institutions because they have lower overhead costs.

(2) Access to funding: P2P lending provides a new source of funding for borrowers who may not qualify for traditional loans, such as small business owners, start-ups, or individuals with poor credit histories.

(3) Diversification of investment portfolio: P2P lending systems allow investors to diversify their investment portfolio by lending small amounts of money to many borrowers. This helps reduce risk and potentially increase returns.

(4) Transparency: P2P lending systems provide transparency in terms of fees, interest rates, and repayment terms, allowing borrowers and lenders to make informed decisions.

(5) Fast approval and funding: P2P lending systems can provide faster approval and funding for loans than traditional financial institutions, which can take several weeks or even months.

(6) Flexible repayment terms: P2P loans may offer more flexible repayment terms than traditional student loans. For example, borrowers may be able to choose a longer repayment period or have the option to make interest-only payments while they are in school.

(7) No origination fees: P2P lenders typically don't charge origination fees, which can save borrowers money on upfront costs.

(8) Diversification of funding sources: P2P lending can help students diversify their sources of funding and reduce their reliance on traditional student loans, which may have higher interest rates and more rigid repayment terms.

However, disadvantages of Peer-to-Peer systems could include:

(1) Risk of default: Borrowers may default on their loans, which can lead to loss of funds for lenders. P2P lending systems usually have some protections in place to minimize this risk, but it still exists.

(2) Lack of regulation: P2P lending systems are not as heavily regulated as traditional financial institutions, which can lead to potential scams or fraudulent activities.

(3) Limited loan amounts: P2P lending systems may not be able to provide large loan amounts, which can be a disadvantage for borrowers who need significant funding.

(4) Limited investor protections: P2P lending systems may not offer the same level of investor protections as traditional financial institutions, which can be a disadvantage for lenders.

(5) Lack of liquidity: P2P loans are usually illiquid investments, meaning they cannot be easily bought or sold on secondary markets.

Overall, P2P lending systems can be a beneficial alternative for both borrowers and lenders, but they also come with their own set of risks and limitations. However, it is important to note that P2P lending also comes with risks, including the potential for default and lack of regulation. Students should carefully consider their options and compare the terms and rates of P2P loans to traditional student loans before making a decision.

In this section, we take a close look at some of the top P2P lending systems available today that are closely related to the work we are creating, analyze their features, benefits, and potential drawbacks. By the end of this review, there should be a better understanding of how these systems work.

2.1 Lend layer

A cloud-based platform that enables peer-to-peer lending for educational institutions. It includes features such as loan origination, underwriting, servicing, and collections. It was founded in 2014 by a team of former students lead by Chris Sang, who were frustrated with the traditional student loan system and wanted to create a better alternative. LendLayer aims to make student loan refinancing more accessible and affordable, and to help borrowers manage their debt more effectively [9]. One of the unique features of LendLayer is its focus on community. The platform connects borrowers with alumni and other members of their school community who are interested in investing in their education. This creates a sense of camaraderie and support, and allows borrowers to get better rates and terms than they might find elsewhere.

To apply for a loan through LendLayer, borrowers must have at least $10,000 in student loan debt and be employed or have a job offer. The application process is straightforward and can be completed entirely online. LendLayer uses a proprietary algorithm to evaluate borrowers' creditworthiness and determine their interest rate and loan term. Borrowers can choose from fixed or variable interest rates and terms ranging from five to fifteen years. One of the benefits of LendLayer is its flexibility. Borrowers can choose to make interest-only payments for the first six months, which can help them manage their cash flow while they get settled into their post-graduation lives. There are also no prepayment penalties, so borrowers can pay off their loans early if they choose to do so (LendLayer Company Profile: Acquisition & Investors | PitchBook, n.d.).

However, there are some potential drawbacks to using LendLayer. One is that the platform is only available to graduates of certain schools, so not everyone will be eligible. Additionally, LendLayer does not offer any income-driven repayment plans, which may be a disadvantage for some borrowers who are struggling to make their monthly payments.

2.2 MPOWER Financing

MPOWER Financing is a school loan app that offers loans to international and DACA students in the United States. The app provides loans for graduate and undergraduate studies, with interest rates ranging from 7.99% to 13.99%. They provide educational loans to international students pursuing higher education in the United States and Canada. It aims to remove financial barriers to higher education by offering loans without requiring a co-signer or collateral. MPOWER uses a proprietary credit model that takes into account a student's academic and career potential, rather than just their credit history. The loans can be used for tuition, housing, books, and other education-related expenses. MPOWER has helped over 30,000 students from over 200 countries to finance their education and achieve their academic and career goals.

2.3 CommonBond

CommonBond is a school loan app that provides loans to undergraduate and graduate students in the United States. They are an online lender that provides student loan refinancing, as well as private student loans for graduate students. It was founded in 2011 by a group of MBA students who wanted to create a more transparent and affordable student lending industry. CommonBond offers competitive interest rates, flexible repayment terms, and a range of resources to help borrowers manage their debt. It also has a social mission to help address the student debt crisis, and partners with Pencils of Promise to fund education for children in developing countries. CommonBond has refinanced over $10 billion in student loans and has helped thousands of borrowers achieve financial freedom.

2.4 Prodigy Finance

Prodigy Finance is a school loan app that provides loans to international students pursuing graduate studies in the United States, United Kingdom, Europe, and Australia. The app offers flexible repayment options and competitive interest rates. They are a UK-based fintech company that provides loans to international postgraduate students studying at top universities around the world. It was founded in 2007 by three MBA graduates who struggled to secure funding for their own studies. Prodigy Finance offers loans to students from over 150 countries, without requiring a co-signer or collateral. The loans are based on the student's future earning potential, rather than their credit history or current income. Repayments are tied to a percentage of the student's income after graduation, which helps to make the loans more affordable. Prodigy Finance has helped over 20,000 students to finance their education and achieve their career goals.

2.5 Closely related work

Wu and Fu [10] proposed a recommendation model based on intelligent agent in P2P Lending for the borrowers. The model provides for the borrowers with individual risk assessment, the eligible lender search, the lending combination and the loan recommendation. Recommendations were made with reasoning on ontology-based knowledge. The model was developed in JADE and evaluated by the PROSPER’s sample data. Their result showed that, the model can meet borrower’s needs better and help borrower getting loan more efficiency

Sangster [11] aims to document the background to the need for commercial risk analysis within the domain of bank lending. It reports the development and structure of COMPASS, the Bank of Scotland's lending adviser expert system. The stages of its development are outlined; the knowledge elicitation process is described; knowledge articulation is examined from the perspective of the expert; the architecture of the system is explained; the consultation procedure is described; and the advantages by-products, and long-term benefits of COMPASS are summarized.

Lee and Wang’s [12] research aimed at presenting a logical approach for implementing dynamic business rules based on a context-aware integrated BPM-SOA framework. Their experimental implementation of business loan application process demonstrated the timely and improved potential loan default possibility while revealing the scalability of our proposed context-aware integrated BPM-SOA framework.

Houshmand and Kakhki [13] presented the development of a rule based expert system for evaluation of loan request. The purpose of system is to evaluate the loan request and do some sensitivity analyses on the evaluation result to find the critical criteria. To achieve their purpose, they utilized the Inference engine which works both forward (evaluation) and backward chaining (sensitivity analysis). Their result was a well-designed rule-based Loan Evaluation Expert System is designed for the Iranian bank of Industry and Mine. Darmon et al. [14] investigate the effects of implementing a bidding agent in online reverse auctions on a crowdlending platform. Findings indicate a substantial rise in the number of bids and bidders, alongside reduced collection time and improved portfolio diversification. Moreover, the bidding agent proves advantageous for both platform users, leading to savings in screening and bidding expenses. Notably, the synergy between rating-based and bidding agents plays a pivotal role in platform financial oversight.

Shoumo et al. [15] introduce a machine learning model aimed at precisely evaluating credit risk and forecasting loan defaulters for credit lending institutions. Leveraging tuned supervised learning algorithms such as Support Vector Machine and Recursive Feature Elimination with Cross-Validation, the model assesses metrics including F1 score, AUC score, prediction accuracy, precision, and recall. Its implementation enables financial institutions to detect potential loan defaulters proactively, thereby mitigating potential losses.

Skvarciany and Jurevičienė [16] employ a distinctive dataset to measure e-trust within the digital economy, encompassing EU nations and Iceland. Utilizing a multi-criteria approach for trust assessment, Ireland and Belgium emerge with the highest levels observed. Meanwhile, countries such as Iceland, the Netherlands, Cyprus, Germany, Luxembourg, Sweden, and Estonia exhibit average trust levels. Notably, France and Romania are excluded from the analysis due to data unavailability.

Budiharto et al. [17] peer-to-peer lending represents a burgeoning financial technology in Indonesia, providing alternative financing avenues for both individuals and businesses. Despite its growth, regulatory oversight remains limited. A theoretical legal research endeavor scrutinized the credit agreement mechanism and lender safeguards within peer-to-peer lending. Findings indicate that peer-to-peer lending practices align with Financial Services Authority Regulation No. 77/POJK.01/2016. However, it's noted that the OJK has yet to establish comprehensive private law protections for lenders, highlighting an area warranting attention.

Basha et al. [18] examine online peer-to-peer lending from 2008 to 2020, focusing on funding success and loan attributes. It highlights the shift from traditional methods to artificial intelligence and the debate on self-regulatory versus stricter regulations. Future research should explore platforms' performance in emerging markets, regulatory differences, behavioral characteristics, and the relationship between P2P lending and traditional finance channels.

Ren and Malik [19] online peer-to-peer lending (P2PL) systems provide convenience and promising returns, yet face challenges such as low financial liquidity and prolonged investment durations. This paper introduces a recommendation framework aimed at constructing an investment portfolio that maximizes returns while minimizing risk. The framework employs predictive models to anticipate future loan grades and quantities, surpassing existing methodologies. Experimental findings demonstrate that the proposed system substantially enhances the likelihood of attaining optimal returns with minimal risk, achieving an improvement of approximately 69% compared to current practices.

Babaei and Bamdad’s [20] paper introduces a data-centric framework for investment decision-making in peer-to-peer lending, employing artificial neural networks and logistic regression to forecast loan returns and default probabilities. Validation with real-world data underscores the impact of platform attributes on problematic platforms, suggesting implications for governmental involvement in platform oversight and management.

Xia et al. [21] examine factors influencing P2P lending platforms, pinpointing problematic ones and devising a risk early warning model. Employing web crawler software, it scrutinizes 1427 platforms from China's P2Peye and WDZJ. Results reveal that platform attributes, including basic features, capital security, operations management, and social network, significantly influence the identification of problematic platforms. The study's practical implications extend to investors and regulators, advocating for governmental involvement in platform oversight to foster the healthy development of the P2P lending sector. However, limitations exist, such as the potential oversight of external factors like government policies.

Wang et al. [22] delved into the rapidly evolving Chinese peer-to-peer lending sector, highlighting the importance of assessing default risk. It introduces a novel consumer credit scoring technique leveraging attention mechanism LSTM, utilizing online operational behavior data and Word2vec model. Compared to conventional feature extraction methods and standard LSTM models, this approach significantly enhances predictive accuracy.

In their research, Bastani et al. [23] presents a two-stage scoring method tailored for lenders operating in the peer-to-peer lending market. By integrating credit and profit scoring, it aims to distinguish non-default loans and forecast profitability. Employing wide and deep learning techniques, predictive models are developed for each stage. Extensive numerical analyses demonstrate the superiority of this approach over conventional credit and profit scoring methods, effectively tackling the issue of imbalance and enhancing the accuracy of profitability prediction.

This deals with the methodology undertaken to design an effective peer-to peer lending system. The chosen SDLC methodology is the prototype methodology. The Prototype model is a software development lifecycle model that involves creating a working model of the software application, which is then refined based on user feedback until the final product is developed. This model is best suited for the design and implementation of a peer-to-peer student lending system because it allows for rapid prototyping and iterative development.

In a peer-to-peer lending system, the user experience is crucial, and the Prototype model ensures that the user's needs are met. With this model, a working model of the student lending system can be created quickly, and user feedback can be gathered to refine the system. This iterative process helps to ensure that the final product meets the user's needs and expectations.

Another advantage of the Prototype model is that it allows for flexibility and adaptability. In the design and implementation of a peer-to-peer lending system, there may be changes in the market or regulatory environment that require the system to be updated. The Prototype model allows for these changes to be incorporated easily, as the system is continually refined based on user feedback. The Prototype model is cost-effective, as it reduces the risk of costly mistakes by identifying problems early on in the development process. This means that resources are used efficiently, and the final product is of high quality.

XAMPP package was used for the development of the entire system. This is because XAMPP is a cross platform package and has the ability to work on any operating system. MySQL a component of XAMMP was used for to develop the database that houses all the data and information entered into the system by the administrator and the other staff members with access to the system.

Windows operating system. It was chosen because it works well with the Windows Operating System and also has:

(i) Apache web server.

(ii) MySQL to create the database for the application using PHPMyAdmin.

(iii) HTML, CSS, and PHP were used to design the web pages for the application.

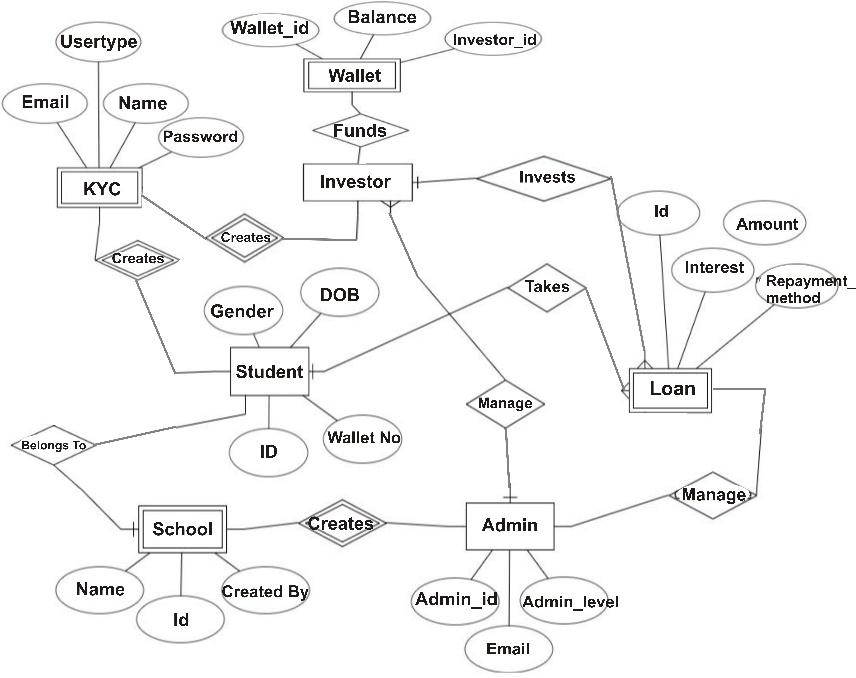

The diagram above explains a workflow of the peer-to-peer student lending system.

3.1 Use case

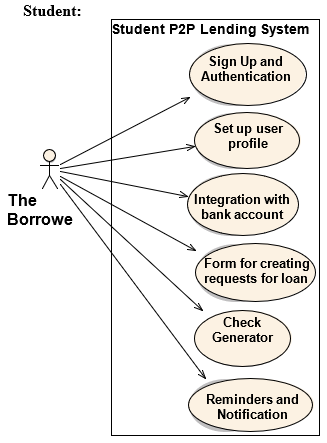

The actor in this use case is the student and he is able to perform actions which include:

(i) Login: The login page gives access to the students registered in the system. This action allows them to have full access to the pages allowed by the administrator on the system.

(ii) Add/edit data: The system allows the user to enter and alter data to the system such as their profile and some aspects of their KYC (Know Your Customer). The data that is entered is what will eventually be used in the application of loans.

(iii) Apply For a Loan: After the student completes the KYC process, he/she can go ahead to apply for a loan.

(iv) Belong to a school: Students are to add a school to their profiles to give an insight to investors. The scope for this system is private tertiary institutions.

There are three main actors in Figure 1, which are the student, investor and the administrator. Their functions are as follows.

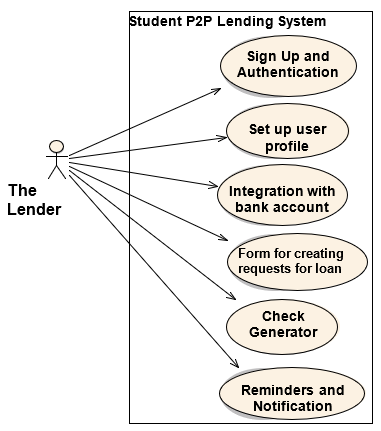

Figure 2 shows the use-case diagram for borrower. These are people that come to lend on the platform. They will be granted access by the administrator and be able to use the functions that the system provides, and they will be able to do the following:

(a) Login

(b) Fund loans

(c) Invest in loans

(d) Create a profile

(e) Belong to a school

(f) Start the KYC (Know your customer) process

(g) Logout

Figure 1. Entity relationship diagram of the system showing the system and their functions

Figure 2. Use case diagram for borrowers

3.2 Investor

Figure 3 shows the use-case diagram for lenders. These are people that come to give loans on the platform. They will be granted access by the administrator and be able to use the functions that the system provides, and they will be able to do the following:

(a) Login

(b) Apply for loans

(c) Create a profile

(d) Start the KYC (Know your customer) process

(e) Logout

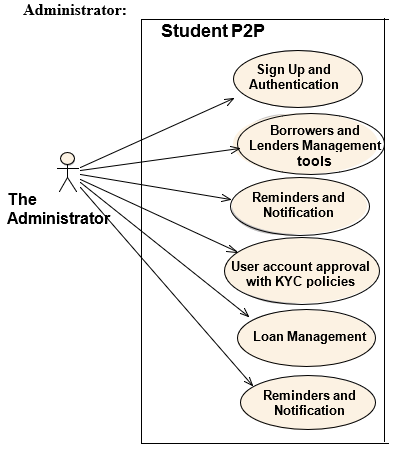

Figure 4 shows the use-case diagram for administrator. This actor monitors all predictions and events happening on the platform. He is registered by default and can create users who will enter and use data in the system. He is also able to do the following:

(a) Create new users

(b) Login

(c) Add and edit data

(d) Review feedback

(e) Logout

(f) Manage the system

Figure 3. Use case diagram for lenders

Figure 4. Use case diagram for administrator

The implementation phase is the process of developing and deploying the system. This phase involves coding, integration, testing, and deployment of the system. The system designed comprises of the front-end and the back-end. The front-end of the system includes the interface of the system, i.e., what the users can see. The front-end components include the various pages of the system i.e., Dashboard, Administrator’s module page, the datasets page, the registered students page. Furthermore, these pages (front-end) are linked to the back-end component which contains the database of the system. Using PHP scripting language, the database was connected to the front-end.

(1) Development of the System: The first step in implementing the P2P student lending system is to develop the system. This involves coding the software, designing the user interface, and integrating the system with other third-party systems. The development of the system is done using various programming languages, such as PHP, JavaScript, HTML, and CSS which we all used.

(2) Database Design and Implementation: The second step in implementing the P2P student lending system is to design and implement the database. The database is used to store all the data related to the system, such as user information, loan information, and transaction information. The database design is done using MySQL, a widely used open-source relational database management system.

(3) Integration of Payment Gateways The third step in implementing the P2P student lending system is to integrate payment gateways. Payment gateways are used to facilitate transactions between lenders and borrowers. The payment gateways allow lenders to deposit funds into their accounts and borrowers to withdraw funds from their accounts. The payment gateways used in the system is Paystack.

(4) User Testing: The fourth step in implementing the P2P student lending system is to test the system. User testing is done to ensure that the system is working as expected and meets the requirements of the users. The user testing is done by a group of selected users who test the system and provide feedback.

(5) Deployment: The final step in implementing the P2P student lending system is to deploy the system. Deployment involves installing the system on the production server and making it available to users.

Figure 5 shows the screenshot for the development environment where the implementation of the payment function is done while Figure 6 shows a screenshot of the linking of all the CSS files used in implementation of the P2P lending application.

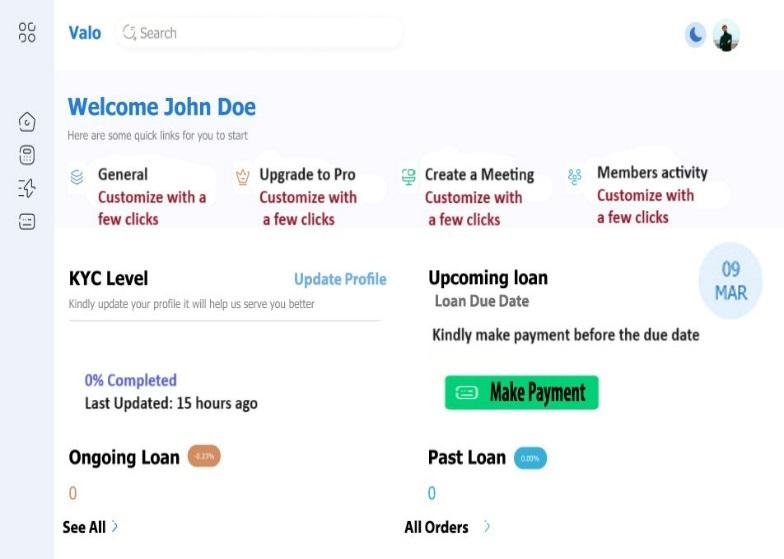

4.1 The dashboard

Figure 7 shows the dashboard. The dashboard is normally the primary web page a tourist navigating to a website from an internet browser will see, and it could also function as a landing page to draw visitors. The dashboard is used to facilitate navigation to other pages on the website.

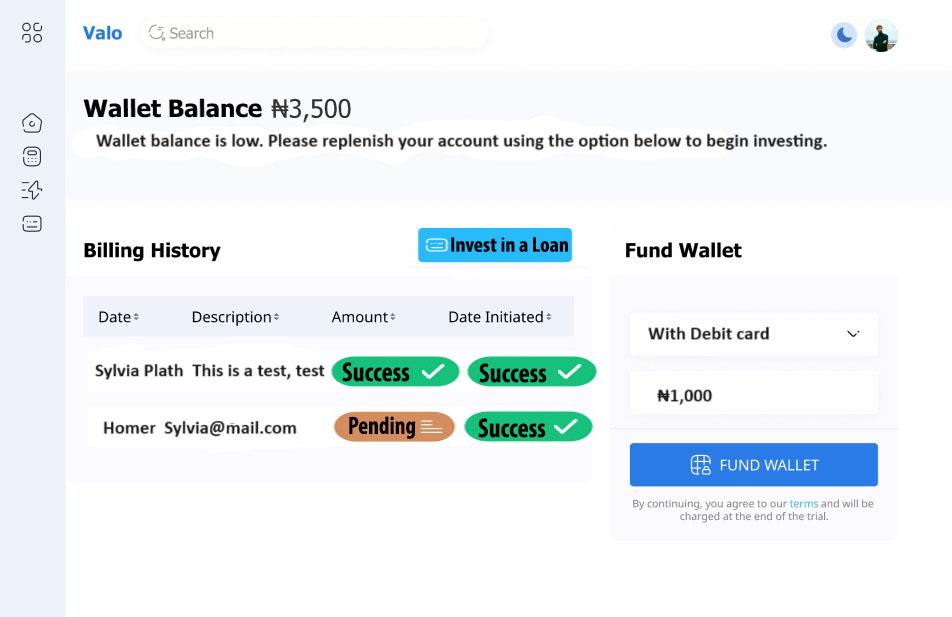

4.2 Wallet page

Figure 8 shows the Wallet history and billing history page. Here Investors and students can check their wallet balance and history. They can fund their wallet and check the status of the transaction.

4.3 KYC page (Know your customer)

Figure 9 shows the KYC Process page. The students and investors are those the system is designed for. They are the users of the application, and since this is a peer-to-peer system, the intended users are the students and investors who will be applying for and funding loans respectively.

The module provides the students and investors with an interface that enables the user to fill in information needed to perform loan activities (fund, invest and apply).

Figure 5. Screenshot of development environment

Figure 6. Screenshot of development environment Screenshot showing links to CSS files

Figure 7. The dashboard

Figure 8. The wallet history and billing history page

Figure 9. The page which shows the KYC Process

The implementation of the P2P student lending system offers a solution to the challenges faced by students who need financial assistance to pursue their education. This system enables students to access loans from individual lenders, reducing the dependence on traditional bank loans. The P2P lending system offers several advantages, including lower interest rates, streamlined loan approval processes, and simplified loan repayment plans.

The P2P student lending system provides an alternative source of funding for students who may not be eligible for traditional bank loans. It also enables lenders to earn a return on their investment while helping students achieve their academic goals.

The design and implementation of the P2P student lending system involve several critical stages, including system development, database design, payment gateway integration, user testing, and system testing. Testing is essential in software development as it ensures that the system is working as expected and meets the requirements of the users. The P2P student lending system presents opportunities for both borrowers and lenders. Borrowers can access loans at lower interest rates, while lenders can earn a return on their investment while helping students achieve their academic goals. The implementation of this system can significantly impact the education sector by increasing access to funding for students.

Based on the findings of our research paper, the following recommendations are in order, there should be:

(1) Collaboration with universities and colleges: The research has shown that students are interested in using the P2P student lending system. To ensure the success of the system, it is recommended that the lending platform collaborates with universities and colleges to promote the system and educate students on the benefits of using it.

(2) Provide incentives: To encourage students to use the system, it is recommended that the lending platform provides incentives such as reduced interest rates, referral bonuses, and cashback rewards.

(3) Implement robust security measures: To protect the system from fraud, it is recommended that the lending platform implements robust security measures such as two-factor authentication, encryption, and fraud detection algorithms.

(4) Monitor the system: To ensure the smooth running of the system, it is recommended that the lending platform monitors the system for any bugs or errors and fixes them promptly.

[1] Bholat, D., Atz, U. (2016) Peer-to-peer lending and financial innovation in the united kingdom. Bank of England Working Paper, 598. https://doi.org/10.2139/ssrn.2774297

[2] Basha, S.A., Elgammal, M.M., Abuzayed, B.M. (2021). Online peer-to-peer lending: A review of the literature. Electronic Commerce Research and Applications, 48: 101069. https://doi.org/10.1016/j.elerap.2021.101069

[3] Sicuranza, C., Rock, K., Xiao, S. (2017). The changing landscape of student loans. Guide house, 1-4.

[4] Cornelli, G., Frost, J., Gambacorta, L., Jagtiani, J. (2022). The impact of fintech lending on credit access for U.S. small businesses. BIS Quarterly Review, 1-43. https://www.bis.org/publ/work1041.pdf

[5] Balyuk, T. (2021). Financial Innovation and Borrowers: Evidence from Peer-to-Peer Lending, SSRN Electronic Journal.

[6] Kapadia, R. (2015) A Solution to the Student Loan Crisis: Human Capital Contracts. Brooklyn Journal of Corporate, Financial & Commercial Law, 9(2): 591-614.

[7] Kolari, J.W., Shin, G.H. (2014). Assessing the profitability and riskiness of small business lenders in the banking industry. SSRN. https://doi.org/10.2139/ssrn.1017093

[8] Triki, T., Faye, I. (2013) Financial inclusion in Africa. The Transformative Role of Technology, African Development Bank (AfDB) African Development Bank Group, page 106-115. https://www.afdb.org/fileadmin/uploads/afdb/Documents/Project-and-Operations/Financial_Inclusion_in_Africa.pdf.

[9] LendLayer Company Profile: Acquisition & Investors. https://pitchbook.com/profiles/company/66176-65#overview.

[10] Wu, J.H., Fu, R. (2010). An intelligent agent system for borrower's recommendation in P2P lending. In 2010 International Conference on Multimedia Communications, Hong Kong, China, pp. 179-182. https://doi.org/10.1109/MEDIACOM.2010.69

[11] Sangster, A. (1995). The bank of scotland's lending adviser expert system, COMPASS. In Proceedings the 11th Conference on Artificial Intelligence for Applications, Los Angeles, CA, USA, pp. 24-30. https://doi.org/10.1109/CAIA.1995.378793

[12] Lee, V., Wang, N. (2012). An intelligent system for business loan processing. In 2012 Third International Conference on Intelligent Systems Modelling and Simulation, Kota Kinabalu, Malaysia, pp. 390-396. https://doi.org/10.1109/ISMS.2012.128

[13] Houshmand, M., Kakhki, M.D. (2007). Presenting a rule based loan evaluation expert system. In Fourth International Conference on Information Technology (ITNG'07), Las Vegas, NV, USA, pp. 497-502. https://doi.org/10.1109/ITNG.2007.155’’

[14] Darmon, E., Oriol, N., Rufini, A. (2022). Bids for speed: An empirical study of investment strategy automation in a peer-to-business lending platform. Decision Support Systems, 156: 113732. https://doi.org/10.1016/j.dss.2022.113732

[15] Shoumo, S.Z.H., Dhruba, M.I.M., Hossain, S., Ghani, N. H., Arif, H., Islam, S. (2019). Application of machine learning in credit risk assessment: A prelude to smart banking. In TENCON 2019 IEEE Region 10 Conference (TENCON), Kochi, India, pp. 2023-2028. https://doi.org/10.1109/TENCON.2019.8929527

[16] Skvarciany, V., Jurevičienė, D. (2023). Assessment of trust level in digital economy. In New Perspectives and Paradigms in Applied Economics and Business: Select Proceedings of the 2022 6th International Conference on Applied Economics and Business, pp. 147-154. https://doi.org/10.1007/978-3-031-23844-4_11

[17] Budiharto, B., Lestari, S.N., Hartanto, G. (2019). The legal protection of lenders in peer to peer lending system. Law Reform, 15(2): 275-289. https://doi.org/10.14710/lr.v15i2.26186

[18] Basha, S.A., Elgammal, M.M., Abuzayed, B.M. (2021). Online peer-to-peer lending: A review of the literature. Electronic Commerce Research and Applications, 48: 101069. https://doi.org/10.1016/j.elerap.2021.101069

[19] Ren, K., Malik, A. (2019). Investment recommendation system for low-liquidity online peer to peer lending (P2PL) marketplaces. In Proceedings of the Twelfth ACM International Conference on Web Search and Data Mining, pp. 510-518. https://doi.org/10.1145/3289600.3290959

[20] Babaei, G., Bamdad, S. (2020). A multi-objective instance-based decision support system for investment recommendation in peer-to-peer lending. Expert Systems with Applications, 150: 113278. https://doi.org/10.1016/j.eswa.2020.113278

[21] Xia, H., Wang, P., Wan, T., Zhang, Z.J., Weng, J., Jasimuddin, S.M. (2022). Peer-to-peer lending platform risk analysis: An early warning model based on multi-dimensional information. The journal of risk finance, 23(3): 303-323. https://doi.org/10.1108/JRF-06-2021-0102

[22] Wang, C., Han, D., Liu, Q., Luo, S. (2019). A deep learning approach for credit scoring of peer-to-peer lending using attention mechanism LSTM. IEEE Access, 7: 2161-2168. https://doi.org/10.1109/ACCESS.2018.2887138.

[23] Bastani, K., Asgari, E., Namavari, H. (2019). Wide and deep learning for peer-to-peer lending. Expert Systems with Applications, 134: 209-224. https://doi.org/10.1016/j.eswa.2019.05.042