Sandeep Patalay* | Madhusudhan Rao Bandlamudi

© 2021 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Investing in stock market requires in-depth knowledge of finance and stock market dynamics. Stock Portfolio Selection and management involve complex financial analysis and decision making policies. An Individual investor seeking to invest in stock portfolio is need of a support system which can guide him to create a portfolio of stocks based on sound financial analysis. In this paper the authors designed a Financial Decision Support System (DSS) for creating and managing a portfolio of stock which is based on Artificial Intelligence (AI) and Machine learning (ML) and combining the traditional approach of mathematical models. We believe this a unique approach to perform stock portfolio, the results of this study are quite encouraging as the stock portfolios created by the DSS are based on strong financial health indices which in turn are giving Return on Investment (ROI) in the range of more than 11% in the short term and more than 61% in the long term, therefore beating the market index by a factor of 15%. This system has the potential to help millions of Individual Investors who can make their financial decisions on stocks and may eventually contribute to a more efficient financial system.

decision support system (DSS), machine learning, stock portfolio, artificial intelligence (AI), intrinsic stock value

The stocks markets have become an important investment activity around the world and the proliferation of internet and online trading systems have drawn millions of small individual investors in to the stock market [1]. For many small time individual investors it is beyond their budget and time to take the help of good financial advisors who can guide them in stock market investments. There is strong need for an Automated Decision Support System which can help individual investors to accurately predict stock prices and automatically create a good portfolio of stocks to diversify risk and earn premium returns.

While Machine learning and AI models have been applied in the financial domain for predicting stock prices [2], but there is a lack of quality literature and research in the application of AI/ML techniques for stock portfolio selection [3]. Decision Support Systems (DSS) to make financial decisions are based on many techniques like Mean Variance (MV) Markowitz method [4], Fuzzy logic based stock selection methods [5], Data Mining based Evolutionary systems [6], Fuzzy Clustering Rule-Based Expert System for Stock Price Movement Prediction [7], Fuzzy Inference systems based on Technical Indicators, Stock Selection based on knowledge discovery rules [8], all these techniques are depended on technical indicators or market statistics which are error prone for long term portfolio selection. Financial DSS based on Fundamental analysis techniques [9] have been proven to be more efficient and accurate [10] when portfolio selection pertains to long term time frame.

In this study, we propose a financial decision support system (DSS) which can automatically predict stock prices and perform stock financial health analysis with a reasonable degree of accuracy to automatically create a portfolio of top performing stocks for risk diversification and earning premium returns compared to average market return. The Financial DSS is based on AI and ML Systems Architecture which establishes the relationship between fundamental financial variables and the stock price and calculates the Intrinsic Value of the stock and also performs a comprehensive financial health and risk analysis based on Expert Knowledge rules for analyzing critical financial attributes of the stock. The Financial DSS in this study was tested using open source financial data of various stocks listed on the National Stock Exchange of India (NSE) [11].

The authors have done performed a review of existing literature in the domain of AI/ML and DSS used for the financial domain particularly the systems used for stock portfolio selection. The major goals of the literature survey are:

In the recent times, with the proliferation of Machine learning algorithms in the financial domain, many studies have focused on the usage of various machine learning algorithms including ANNs for stock price prediction, however there are many limitations in the current application of ANNs which have mostly focused on the technical parameters which result in inaccurate and unusable prediction by investors [12]. Many of the AI/ML models used in the domain of stock price prediction and portfolio selecton are purely based on the technical indicators which are basically time series variables and not based on the fundamental value of the stock. These types of models are suitable for Intraday trading [13] and cannot be used for value investing or long term investments [14]. The models that are based on time series data to predict long term stock behaviour and hence the selection of stocks are prone to wide variances [15, 16].

There are many studies available in the literature that discuss the comparison of various AI/ML techniques in terms of their inputs and output prediction accuracy, even though these studies have varying degree of prediction accuracies, one common theme is that the accuracy and reliability of the model increases when fundamental financial variables [17] are used for the establishing the relationship between input variables and stock price [18]. Literature available in the field of AI/ML applications for stock price prediction are based on the popular ML models such as Artificial Neural Networks (ANN), Support Vector Machines (SVM) and Decision Tree techniques such as Model Trees and Random Forests have technical indicators as inputs [19]. There are studies on comparison of various ML techniques used for stock price prediction and have indicated that linear regression models cannot capture the complex non-linearity in the stock prices and have also indicated that ANNs along with Decision trees have better performance when fundamental financial variables are chosen as the model inputs [20].

The relationship between the stock’s fundamental financial variables and the stock price is complex and a key indicator of the intrinsic or fundamental value of the stock [21]. There are instances in the literature where DSS have been built using various ML techniques where mostly the technical indicators in general and in few cases fundamental variables like Earnings per share (EPS) and profitability have been used to train the ML models but the accuracy of these DSS is questionable and only indicates the general trend of the stock price [22]. The reason for such inaccuracies can be attributed to the architecture of the ML models which work accurately on the training data, but perform poorly on the real world data. After performing the literature survey, the key inferences that can be made are:

Based on the above inferences, we believe that there are no comprehensive machine models currently to predict long-term movements of stock prices and select stocks to build top performing portfolios. We conclude that the Decision Support System based on AI and ML Systems Architecture is the best approach for stock price portfolio selection that offers premium results and better Risk and Reward analysis.

The System Architecture of the Financial DSS for Stock Portfolio Selection is based on Hybrid AI and ML model. The Architecture of the DSS consists of 4 main Subsystems:

The above subsystems are integrated to form a robust financial DSS that can be used by stock investors. The accuracy and reliability of the DSS is built in to the systems by incorporating multiple levels of checks in the form of AI/ML, independent mathematical stock intrinsic value model and comprehensive health check.

3.1 Architecture of financial DSS for automated stock portfolio selection

Figure 1 shows the Architecture of Financial Decision Support System for Automated Stock Portfolio Selection based on AI and ML Systems.

Figure 1. Architecture of financial DSS for automated stock portfolio selection

The Financial DSS can be mathematically represented as follows:

$S_{\text {Portfolio }}=\int_{0}^{T} \psi\left(S_{m l}, S_{\text {Intrinsic }}, S_{\text {Health }},\right.$ Fin $_{\text {Hist }},$ Fin $\left._{\text {Curr }}\right)$ (1)

where, $S_{m l}$ is the Stock Price prediction Model using Machine learning, $S_{\text {Intrinsic }}$ is the Stock Intrinsic Value Model, $S_{\text {Health }}$ is the Stock Health Model, Fin $_{\text {Hist }}$ is the historical financial data about stocks and Fin $_{\text {Curr }}$ is the current financial data about stocks.

3.2 Stock price prediction model based on machine learning

In the domain of Machine learning, the stock prediction is a regression problem as it requires numerical prediction. The ML model chosen for this study is based on the M5P model tree algorithm [23] which combines the power of classification and regression to predict stock prices. Model trees are just like ordinary decision trees, except that at each leaf they store a linear regression model that predicts the class value of instances that reach the leaf. This model is chosen because financial data is complex which needs to be classified and then numerical data can be predicted.

The Tree splitting criterion is used to determine which attribute is the best to split that portion T of the training data that reaches a particular node. It is based on treating the standard deviation of the class values in T as a measure of the error at that node, and calculating the expected reduction in error as a result of testing each attribute at that node. The attribute that maximizes the expected error reduction is chosen for splitting at the node. The expected error reduction, which we call SDR for standard deviation reduction, is calculated as below:

$S D R=s d(T)-\sum_{i} \frac{\left|T_{i}\right|}{|T|} * \operatorname{sd}\left(T_{i}\right)$ (2)

As noted earlier, a linear model (LM) is needed for each interior node of the tree; the model takes the form as show below:

$w_{0}+w_{1} * a_{1}+w_{1} * a_{1}+\cdots+w_{k} * a_{k}$ (3)

where, $a_{1}, a_{1}, \ldots, a_{k}$ are the financial attributes and $w_{1}, w_{1}, \ldots, w_{k}$ are the weights calculated using standard regression. The financial attributes considered for the Machine learning are as follows:

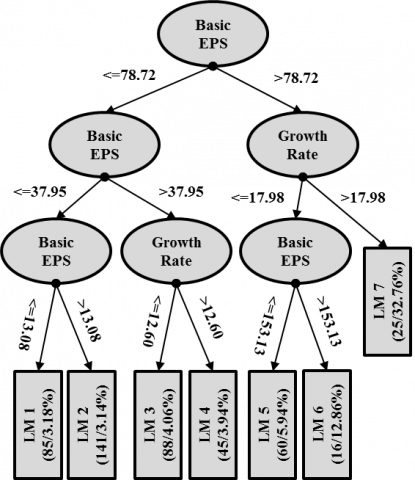

The Machine learning algorithm selects the attributes which have a direct effect on the share price, the model tree for this model is represented below Figure 2, the linear models at the end of each node of a tree is represented by LM1 to LM7.

Figure 2. M5P model tree for stock price prediction

3.3 Mathematical model for intrinsic value of a stock

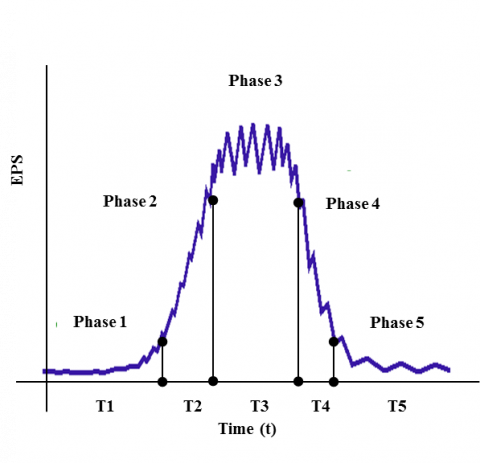

Intrinsic value refers to the value of a stock determined through fundamental analysis without reference to its market value. It is also frequently called the fundamental value of the stock. A mathematical model of calculating the intrinsic value based on the complete lifecycle of stock and the associated cash flows is depicted below in Figure 3.

Figure 3. Valuation life cycle of a stock

The model takes in to account 5 phases of the stock namely:

Based on the Figure 3, the intrinsic value of any stock can be calculated by the below equation.

$S_{\text {IntrValue }}=\sum_{i=T 1}^{T 5} \int_{i}^{i+1} f\left(E P S_{i}\right)$ (4)

where, $S_{\text {Intrvalue }}$ is the Intrinsic Value of the Stock and $E P S_{i}$ is the earnings per share at the start of the ith Phase.

3.4 Model for comprehensive financial health analysis of the stock

The model for Stock analysis and Portfolio selection consists of critical financial attributes as inputs and consists of the Expert Knowledge base rules for analyzing each of the financial attributes. The Model is described in the below Figure 4 consists of two distinct phases, firstly each of the attribute is passed through a Knowledge base rules and given a rating, the second phase consists of summing up all the ratings and forming an index value that is given as input to the inference engine of the DSS. The output of this subsystem is integrated with the overall DSS for choosing stocks not only based on price predictions but also based on sound financial health of the stock for long term reliability and safety of the investments.

The stocks chosen for financial DSS testing and validation are chosen specifically to give a broad based representation of all kinds of stocks in terms of market capitalization and industry segments. Therefore, the stocks chosen for evaluation are NIFTY50, NIFTY MIDCAP and NIFTY SMALLCAP.

Stocks $=\left\{S_{1}, S_{2}, S_{3}, \ldots S_{n}\right\}$ (5)

$S_{i} \in$ Nifty50 UMIDCAP U SMALLCAP (6)

$N I F T Y 50=\left\{S_{1}^{\text {Nifty }}, S_{2}^{\text {Nifty }}, S_{3}^{\text {Nifty }}, \ldots S_{n}^{\text {Nifty }}\right\}$ (7)

MIDCAP $=\left\{S_{1}^{\text {MidCap }}, S_{2}^{\text {MidCap }}, S_{3}^{\text {MidCap }}, \ldots S_{n}^{\text {MidCap }}\right\}$ (8)

SMALLCAP$=\left\{S_{1}^{\text {SmallCap }}, S_{2}^{\text {Smallcap }}, S_{3}^{\text {Smallcap }}, \ldots S_{n}^{\text {Smallcap }}\right\}$ (9)

where, Si represents the ith stock.

Figure 4. Model for stock financial health analysis

The health for each stock is given by the following equation:

$S_{h}^{i}=f\left(\alpha_{P e}^{i}, \alpha_{P e g}^{i}, \alpha_{D e}^{i}, \alpha_{E p s G r}^{i}, \alpha_{N e t P r o f i t G r}^{i}\right.$,$\left.\alpha_{\text {CurrRatio }}^{i}, \alpha_{\text {StockGr } r}^{i}, \alpha_{\text {RevGr }}^{i}, \alpha_{\text {IndPe }}^{i}, \alpha_{\text {Compadv }}^{i}\right)$ (10)

where, $S_{h}^{i}$ is the health index of the ith stock, $\alpha_{P e}^{i}$ is the Price to Earnings ratio of the $\mathrm{i}^{\text {th }}$ stock, $\alpha_{P e g}^{i}$ is the Price to Earnings to Growth (PEG) ratio of the $\mathrm{i}^{\text {th }}$ stock, $\alpha_{D e}^{i}$ is the Debt to Equity ratio of the $\mathrm{i}^{\text {th }}$ stock, $\alpha_{E p s G r}^{i}$ is the EPS growth rate of the ith stock, $\alpha_{\text {NetProfitGr }}^{i}$ is the Net profit growth ratio of the ith stock, $\alpha_{\text {Curratio }}^{i}$ is the Current Ratio of the ith stock, $\alpha_{\text {StockGr }}^{\mathrm{i}}$ is the Stock Price growth rate of the ith stock, $\alpha_{\text {RevGr }}^{i}$ is the Revenue growth rate of the ith stock, $\alpha_{\text {IndPe }}^{i}$ is the Industry PE ratio of the ith stock, $\alpha_{\text {Compadv }}^{i}$ is the Competitive Advantage rating of the $\mathrm{i}^{\text {th }}$ stock.

The health index equation can be computed as follows:

$S_{h}^{i}=\sum_{a t t r=1}^{n} \int f\left(\alpha_{a t t r}^{i}\right)$ (11)

where, $\alpha_{a t t r}^{i}$ is the attribute feature considered for the health index of the ith stock and $f\left(\alpha_{\text {attr }}^{i}\right)$ is the functional output of each attribute evaluation function.

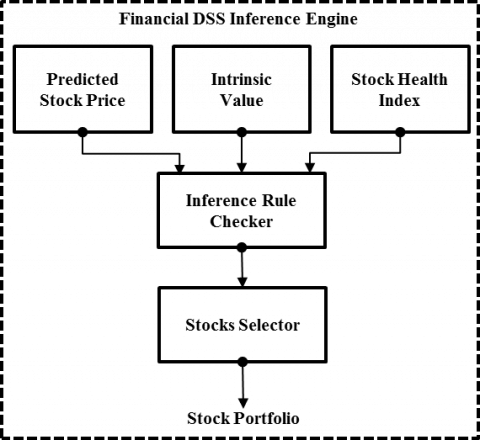

3.5 Inference engine

The inference engine is the brain of the DSS depicted in Figure 5 which combines various inputs and makes inferences and outputs the stock portfolio. The core logic involves mathematical rules to make decisions.

Figure 5. Inference engine of DSS

The stocks for the portfolio are selected based on the below logic.

$S_{\text {Select }}(i)=g\left(\alpha_{\text {PredPrice }}^{i}, \alpha_{\text {IntrValue }}^{i}, S_{h}^{i}\right)$ (12)

where, $S_{\text {Select }}=\left\{S_{1}, S_{2}, S_{3}, \ldots S_{n,}\right\}, \alpha_{\text {PredPrice }}^{i}$ is the predicted price of the $i^{\text {th }}$ stock calculated by ML model, $\alpha_{\text {IntrValue }}^{i}$ is the intrinsic value of the $\mathrm{i}^{\text {th }}$ stock calculated by the Mathematical model and $S_{h}^{i}$ is the health index of the ith stock.

Portfolio equations are as given as follows:

$S_{\text {Portfolio }}(i)=$$\left\{S_{\text {Portfolio }} \in S_{\text {Select }}: S_{\text {Select }}(i)=B U Y\right\}$ (14)

The selected portfolio of stocks will be a subset of the overall stocks considered for evaluation.

$g: S_{\text {Select }} \rightarrow S_{\text {Portfolio }}$ (15)

$S_{\text {Portfolio }} \subseteq S_{\text {Select }}$ (16)

The Portfolio Return of a combination of ‘n’ stocks is calculated using the below equations:

$S_{\text {Portfolio }}=\left\{S_{p}^{1}, S_{p}^{2}, \ldots S_{p}^{n}\right\}$ (17)

$R_{p}=\sum_{i=1}^{n} x_{i} r_{i}$ (18)

where, $S_{p}^{n}$ is the $\mathrm{n}^{\text {th }}$ stock in the portfolio, $R_{p}$ is the Portfolio Return, $x_{i}$ is the proportion of funds invested in each security, $r_{i}$ is the expected return of a particular Stock $S_{p}^{i}$ and 'n' is the number of Stocks in the Portfolio.

In this section, we discuss the data analysis, validation of models and results. As a first step the details of historical data collection for AI/ML model training is explained and then in the later part the real-time data required for intrinsic value calculations and the health analysis model are discussed long with the validation results.

4.1 Data collection

The Financial DSS has three core models for selection of stocks, as first step the data AI/ML model has to be trained using historical data. For the purposes of this research the authors have chosen the data of last 15 years for the top 50 stocks listed on the NSE. This data consists of fundamental variables of the particular stock; a snapshot of such data can be seen in Table 1. Since the data is voluminous in nature, an automated software program called web crawler was developed to fetch the data from open source websites for accuracy and reliability of the data compared to manual data collection techniques. The Data for DSS was collected using many open source financial data websites [24, 25]. All the data collection activities are automated and built on VBA programming language to collect process and analyze the data. For the purposes of this research, financial data of stocks listed in the NSE [11] was collected. The data was chosen to give a broad based representation of stocks listed on the NSE which cover a variety of market capitalization stocks and represent various industry segments.

After ML stock prediction models are trained, the second stop involves the collection of real-time stock information for intrinsic value calculation and performing comprehensive health analysis. A snapshot of the data for stock health analysis is depicted in Table 2.

A partial snapshot of the financial data collected for the inference engine of the DSS is as shown below in Table 2.

4.2 Data validation methodology and results

The three models namely the AI/ML stock price model, Intrinsic value model and the health analysis model along the Inference engine of the DSS shall be validated. The major steps in validating the integrated financial DSS used for stock portfolio selection are:

The first step in validating the DSS is the analysis of Machine learning stock prediction where the dataset was divided in to training and validation sets. The validation methodology for Machine learning model is based on the correlation coefficients and the relative absolute error. The below table shows the results of validation based on a high correlation coefficient and low relative error values validating the accuracy of the ML based stock prediction model. The results are shown in Table 3.

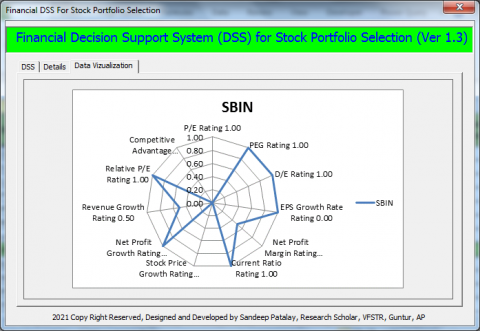

The validation methodology of the DSS is based on subjecting the DSS to past year data (i.e. 2019) and analyzing the portfolio results based on actual returns that have been achieved through the last year (i.e. 2020). A desktop based DSS SW was developed and validated with the historical and current data that was collected as part of this study. The UI of the DSS is shown in Figure 6, the DSS has screen to showcase the rationale behind selecting a particular stock and also gives detailed analysis in the form of a Radar chart.

The Financial DSS provides data visualization for easy analysis as shown in Figure 7.

Table 1. Snapshot of historical financial data of a stock for ML model training

|

Stock Code: TCS.NS |

31-Mar-2018 |

31-Mar-2017 |

31-Mar-2016 |

31-Mar-2015 |

31-Mar-2014 |

31-Mar-2013 |

|

Basic EPS (Rs.) |

131.2 |

120 |

117.1 |

98.31 |

94.15 |

65.22 |

|

Book Value/Share (Rs.) |

397.2 |

396.1 |

330 |

231.9 |

224.9 |

165.9 |

|

Dividend/Share(Rs.) |

50 |

47 |

43.5 |

79 |

32 |

22 |

|

Revenue from Operations/Share (Rs.) |

509.7 |

470.5 |

435.9 |

375.7 |

330.2 |

247.4 |

|

PBDIT/Share (Rs.) |

176 |

160.7 |

156.4 |

130.2 |

125.8 |

84.49 |

|

Net Profit/Share (Rs.) |

132.2 |

120.1 |

117.1 |

98.32 |

94.32 |

65.33 |

|

PBDIT Margin (%) |

34.52 |

34.15 |

35.88 |

34.65 |

38.11 |

34.14 |

|

Net Profit Margin (%) |

25.92 |

25.51 |

26.87 |

26.17 |

28.56 |

26.4 |

|

Total Debt/Equity (X) |

0 |

0 |

0 |

0 |

0 |

0 |

|

Current Ratio (X) |

4.85 |

6.4 |

4.72 |

2.46 |

2.84 |

2.43 |

|

Dividend Payout Ratio (NP) (%) |

36.78 |

38.73 |

34.63 |

80.35 |

33.92 |

33.67 |

|

Earnings Retention Ratio (%) |

63.22 |

61.27 |

65.37 |

19.65 |

66.08 |

66.33 |

Table 2. Snapshot of input financial data for DSS

|

Stock Name |

EPS |

P/E |

Revenue Growth Rate |

Net Profit Growth Rate |

Debt / Equity (D/E) |

Net Profit Margin (%) |

Current Ratio |

Current Share Value |

|

TECHM |

47.24 |

16.76 |

6.27 |

-11.33 |

0.12 |

10.84% |

3.16 |

768.15 |

|

TCS |

81.66 |

30.52 |

4.47 |

-3.12 |

0 |

19.87% |

3.3 |

2,488.40 |

|

HCLTECH |

35.14 |

23.1 |

14.47 |

18.58 |

0.1 |

16.32% |

1.69 |

812.75 |

|

INFY |

37.52 |

26.87 |

8.56 |

9.68 |

0 |

18.35% |

2.88 |

1,009.00 |

|

WIPRO |

15.5 |

20.23 |

2.85 |

4.79 |

0.14 |

15.88% |

2.78 |

311.50 |

|

DRREDDY |

200.87 |

25.83 |

16.16 |

-9.63 |

0.14 |

10.35% |

2.42 |

5,084.20 |

|

BAJAJ-AUTO |

155.59 |

18.52 |

-17.64 |

-3.96 |

0.01 |

17.23% |

1.55 |

2,897.50 |

|

ZEEL |

3.12 |

66.96 |

-9.01 |

-98.37 |

0.07 |

0.35% |

3.84 |

207.80 |

|

POWERGRID |

19.81 |

8.2 |

5.65 |

2.93 |

3.01 |

27.89% |

0.71 |

163.3 |

|

HDFCBANK |

49.69 |

21.71 |

13.6 |

15.74 |

1.9 |

39.84% |

15.35 |

1,062.55 |

|

KOTAKBANK |

29.46 |

43.05 |

7.56 |

18.38 |

2.05 |

26.72% |

12.25 |

1,263.25 |

|

BAJFINANCE |

76.77 |

42.71 |

33.72 |

15.54 |

|

28.96% |

1.28 |

3,294.75 |

|

COALINDIA |

18.19 |

6.38 |

-10.78 |

-22.73 |

0.2 |

16.42% |

7.7 |

117.65 |

|

AXISBANK |

4.47 |

95 |

10.93 |

17.48 |

0.22 |

8.78% |

1.91 |

426.85 |

|

ASIANPAINT |

23.49 |

84.56 |

-9.74 |

1.27 |

0.04 |

12.68% |

|

1,959.95 |

|

BRITANNIA |

72.72 |

52.23 |

9.89 |

47.1 |

0.35 |

13.81% |

1.45 |

3,736.85 |

|

LT |

41.24 |

21.86 |

-0.56 |

-13.66 |

2.13 |

6.00% |

1.18 |

895.45 |

|

BAJAJFINSV |

41.94 |

139.54 |

22.04 |

17.51 |

|

6.65% |

98.41 |

5,876.70 |

|

ITC |

11.63 |

14.76 |

-2.81 |

11.38 |

0 |

30.84% |

4.02 |

169.40 |

|

TITAN |

9.88 |

121.59 |

-12.69 |

-41.21 |

0.35 |

4.72% |

1.82 |

1,167.30 |

Table 3. Validation results of ML stock price model

|

Validation Parameter |

Value |

|

Correlation coefficient |

0.9934 |

|

Mean absolute error |

156.0648 |

|

Root mean squared error |

384.6342 |

|

Relative absolute error |

10.99% |

|

Root relative squared error |

12.42% |

Figure 6. Financial DSS user interface

Figure 7. Financial DSS data visualization

The Validating the Financial DSS, the data from 2019 was provided as input and its predictions were validated from the data collected for the year 2020. The results of the portfolio generation are compared with the actual returns achieved by the stocks in the last 1 year is shown below. Return on Investment (ROI) in the range of more than 11% in the short term and more than 61% in the long term, therefore beating the market index by a factor of 15%. The ROI is shown in Table 4.

Table 4. Performance of NIFTY selected stocks portfolio

|

Sno |

Stock Portfolio Type |

Short Term ROI (%) |

Long Term ROI (%) |

|

1 |

NIFTY 50 |

1.576 |

50.362 |

|

2 |

NIFTY NEXT 50 |

16.645 |

67.949 |

|

3 |

NIFTY MIDCAP |

11.168 |

51.908 |

|

4 |

NIFTY SMALLCAP |

15.297 |

75.534 |

|

Combined NIFTY Portfolio Absolute ROI |

11.1715 |

61.43825 |

|

The implications of this study for predicting the Stock Prices, Selection of Automatic Stock Portfolios and assisting individual investors with decision support are multi-fold:

The authors have designed and developed the financial DSS based on AI and ML Systems architecture. The Financial DSS was empirically tested on real-time data from collected from open source financial data websites. The results have proved that the DSS is performing well giving a portfolio return of Return on Investment (ROI) in the range of more than 11% in the short term and more than 61% in the long term, therefore beating the market index by a factor of 15%. The Financial DSS will benefit small time individual investors in providing accurate portfolio decision support for portfolio selection and earning premium returns.

[1] Tsai, C.F., Wang, S.P. (2009). Stock price forecasting by hybrid machine learning techniques. In Proceedings of the International Multiconference of Engineers and Computer Scientists, 1(755): 60.

[2] Sinha, A.K., Jacob, A.J. (2018). The performance of stock portfolios formed using fuzzy logic. Financial Statistical Journal, 1(2): 814. http://dx.doi.org/10.24294/fsj.v1i2.814

[3] DiPietro, D.M. (2019). Alpha cloning: Using quantitative techniques and SEC 13f data for equity portfolio optimization and generation. The Journal of Financial Data Science, 1(4): 159-171. https://doi.org/10.3905/jfds.2019.1.008

[4] Huang, K.Y., Jane, C.J., Chang, C. (2011). An enhanced approach to optimizing the stock portfolio selection based on Modified Markowitz MV Method. Journal of Convergence Information Technology, 6(2): 226-239.

[5] Fasanghari, M., Montazer, G.A. (2010). Design and implementation of fuzzy expert system for Tehran Stock Exchange portfolio recommendation. Expert Systems with Applications, 37(9): 6138-6147. https://doi.org/10.1016/j.eswa.2010.02.114

[6] Mehmanpazir, F., Asadi, S. (2017). Development of an evolutionary fuzzy expert system for estimating future behavior of stock price. Journal of Industrial Engineering International, 13(1): 29-46.

[7] Shakeri, B., Zarandi, M.F., Tarimoradi, M., Turksan, I. B. (2015). Fuzzy clustering rule-based expert system for stock price movement prediction. In 2015 Annual Conference of the North American Fuzzy Information Processing Society (NAFIPS) held jointly with 2015 5th World Conference on Soft Computing (WConSC), Redmond, WA, USA, pp. 1-6. https://doi.org/10.1109/NAFIPS-WConSC.2015.7284198

[8] Goumatianos, N., Christou, I., Lindgren, P. (2013). Stock selection system: building long/short portfolios using intraday patterns. Procedia Economics and Finance, 5: 298-307. https://doi.org/10.1016/S2212-5671(13)00036-1

[9] Shen, K.Y., Tzeng, G.H. (2015). Combined soft computing model for value stock selection based on fundamental analysis. Applied Soft Computing, 37: 142-155. https://doi.org/10.1016/j.asoc.2015.07.030

[10] Huang, Y., Capretz, L.F., Ho, D. (2019). Neural network models for stock selection based on fundamental analysis. In 2019 IEEE Canadian Conference of Electrical and Computer Engineering (CCECE), Edmonton, AB, Canada, pp. 1-4. https://doi.org/10.1109/CCECE.2019.8861550

[11] NSE, “Nifty50 List”. (2019). [Online]. Available: https://www.nseindia.com/live_market/dynaContent/live_watch/equities_stock_watch.htm. [Accessed: 06-Apr-2019].

[12] Pyo, S., Lee, J., Cha, M., Jang, H. (2017). Predictability of machine learning techniques to forecast the trends of market index prices: Hypothesis testing for the Korean stock markets. PloS one, 12(11): e0188107. https://doi.org/10.1371/journal.pone.0188107

[13] Moews, B., Ibikunle, G. (2020). Predictive intraday correlations in stable and volatile market environments: Evidence from deep learning. Physica A: Statistical Mechanics and Its Applications, 547: 124392. https://doi.org/10.1016/j.physa.2020.124392

[14] Diakoulakis, I.E., Koulouriotis, D.E., Emiris, D.M. (2002). A review of stock market prediction using computational methods. Computational Methods in Decision-Making, Economics and Finance, 379-403. https://doi.org/10.1007/978-1-4757-3613-7_20

[15] Mulwa, C. (2020). Prediction Stacking for long-term forecasting of the bombay stock exchange index by leveraging machine and deep learning models. Sumanth Bijadi Sridhar Rao National College of Ireland Supervisor . http://norma.ncirl.ie/4313/1/sumanthbijadisridharrao.pdf.

[16] Wu, D., Wang, X., Su, J., Tang, B., Wu, S. (2020). A labeling method for financial time series prediction based on trends. Entropy, 22(10): 1162. https://doi.org/10.3390/e22101162

[17] Baker, M., Wurgler, J. (2007). Investor sentiment in the stock market. Journal of economic perspectives, 21(2): 129-152. https://doi.org/10.1257/jep.21.2.129

[18] Obthong, M., Tantisantiwong, N., Jeamwatthanachai, W., Wills, G. (2020). A survey on machine learning for stock price prediction: algorithms and techniques. Soton, 1(1): 1–12. https://eprints.soton.ac.uk/437785/

[19] Ican, O., Celik, T.B. (2017). Stock market prediction performance of neural networks: A literature review. International Journal of Economics and Finance, 9(11): 100-108. https://doi.org/10.5539/ijef.v9n11p100

[20] Banik, S., Khodadad Khan, A.F.M., Anwer, M. (2014). Hybrid machine learning technique for forecasting dhaka stock market timing decisions. Computational Intelligence and Neuroscience. https://www.hindawi.com/journals/cin/2014/318524/abs.

[21] Oliver, M., Per, O., Soenke, S., Christian, S. (2020). Co-movement of price and intrinsic value - does accounting information matter? http://dx.doi.org/10.2139/ssrn.3748644

[22] Vaidya, A.M., Waghela, N.H., Yewale, S.S. (2015). Decision support system for the stock market using data analytics and artificial intelligence. International Journal of Computer Applications, 117(8): 21-28. https://doi.org/10.5120/20574-2977

[23] Witten, I.H., Frank, E. (2002). Data mining: practical machine learning tools and techniques with Java implementations. Acm Sigmod Record, 31(1): 76-77. https://doi.org/10.1145/507338.507355

[24] www.moneycontrol.com, “Stock Financial Data,” 2019. [Online]. Available: https://www.moneycontrol.com/, accessed on 06 Apr. 2019.

[25] www.valueresearchonline.com, “Stock Financial Data,” 2019. [Online]. Available: https://www.valueresearchonline.com, accessed on 06 Apr. 2019.