Mohammad Rifat Rahman*![]() | Md. Mufidur Rahman

| Md. Mufidur Rahman![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study investigates the factors influencing customers’ choice of financial institutions in Bangladesh, focusing specifically on the role of Digital Financial Services (DFS). The study explores the relationship between trust, risks, benefits, social influences and intention to choose financial institutions through DFS. The research adopts a quantitative methodology and employs Structural Equation Modeling (SEM) to analyze the data collected through a survey that use digital financial services in Bangladesh. The study examines by the modified UTAUT model to explore the direct and indirect relationships that influence the intention to choose financial institutions through using DFS. The results reveal that ‘Benefits’ and ‘Social Influences’ have a significant positive impact on the choice of financial institutions through DFS in Bangladesh, while ‘Trust’ and ‘Perceived Risks’ demonstrate an insignificant relationship with ‘Users' Intention’ to choose financial institutions through DFS. This study contributes to the literature on digital financial services (DFS) adoption by examining the factors influencing customers' choice of financial institutions in Bangladesh. Also, the research adds value by incorporating a modified theory of UTAUT model for finding the appropriate relationship among the variables. The findings highlight the importance of understanding the complex factors affecting customers' preferences for financial institutions and emphasize the need for financial institutions in Bangladesh to prioritize not only building trust and managing risks but also leveraging social influences and the benefits of using DFS to attract and retain customers. Finally, it also suggests important insights for financial institutions in Bangladesh to better attract and retain digitally-savvy customers.

digital financial services, risk, trust, benefits, social influences, user’s intention, modified UTAUT model, PLS-SEM analysis, financial institutions

The rapid growth of e-business, fueled by technological advancements and globalization, has compelled businesses to continually reassess their value chains and business models. The financial industry, particularly the Digital Financial Services (DFS) segment, is undergoing a significant transformation due to competitive, administrative, and technological forces [1]. Consequently, Financial Institutions (FIs) have embraced the internet to leverage its power and speed to adapt to the fast-paced changes in the business landscape.

Technological innovations have enabled Financial Institutions to offer an array of services to attract modern clients. The internet, mobile phones, emails, short message service (SMS), and card services are extensively utilized to address the evolving and challenging needs of customers. In a competitive landscape, clients have become more discerning, seeking tailored services that cater to their specific requirements [2]. Consequently, customer satisfaction has become a critical factor in decision-making when choosing a Financial Institution.

Contemporary financial services strategies and management approaches prioritize customer-centricity and adaptability to the ever-changing needs of clients [3]. The study [4] argues that retail Financial Institutions strive to offer similar services to remain competitive. There is a growing emphasis on customer satisfaction to attract new clients and, more importantly, to secure their loyalty and retain existing ones. Moreover, customer choice has become a complex and critical aspect in selecting FI nowadays [5].

Digital Financial Services represent a category of financial services where transactions occur electronically between financial institutions rather than through the exchange of cash, checks, or other negotiable instruments. Ownership and transfer of funds between FIs are recorded on computer systems connected via the internet, with customer identification secured through access codes such as passwords or personal identification numbers instead of signatures on physical documents [6].

Financial Institutions are increasingly recognizing that many clients prefer to conduct their financial services electronically. Implementing digital financial systems has proven to be an essential strategy for FIs to reduce operating costs. In this context, advanced FinTech enables Financial Institutions to minimize expenditure on physical infrastructure. It is widely acknowledged that DFS can help FIs reduce costs, increase revenue, and enhance customer experience [7].

Building upon extensive research on various issues of Digital Financial Services, the present study primarily aims to investigate the factors influencing customers' expectations of DFS from Financial Institutions, and the importance of digital services in selecting a Financial Institution. Building upon extensive research on various issues of Digital Financial Services, the present study aims to investigate the factors influencing customers' expectations of DFS from Financial Institutions, and the importance of digital services in selecting a Financial Institution. However, the research questions are 1) how trust, risks, benefits, and social influences affect users’ intentions to choose FIs through DFS, and 2) how perceived risks mediate users’ intentions to choose FIs through DFS.

Although many researchers have extensively examined several financial innovations, many recent inventions are still not widely studied. A few researches have been identified on technologies like mobile wallets, mobile money, and blockchain, whereas the majority of recent studies have concentrated on innovations like mobile banking and mobile payments. Adoption of DFS applications that significantly impact on the choice of financial institutions are mostly influenced by several variables including social impact, risk, and trust.

The majority of the prior research on DFS adoption has concentrated on technological aspects without taking social influences into account. For instance, while behavioral theories such as the Unified Theory of Acceptance and Use of Technology (UTAUT) or modified UTAUT framework are still hardly used whereas, technology adoption theories such as the Technology Acceptance Model (TAM) have been extensively used in research on digital innovations impact validation.

2.1 DFS conception

The rapid adoption of technology by the millennial generation has driven the financial sector to reevaluate and adapt its business practices. Digitization and digitalization are two crucial aspects of this digital transformation in financial organizations. Digitization refers to the process of converting manual or paper-based documents into digital format and adjusting business rules and procedures accordingly. On the other hand, digitalization represents a comprehensive shift in the mode of operation, leveraging technology to facilitate seamless electronic processing of financial transactions [8].

Operating with a customer-centric approach, digital financial services strive to maximize accessibility, utility, and cost benefits for clients. Financial institutions reap the rewards of reduced operational costs, fewer errors, enhanced services, and an overall superior user experience. Cutting-edge financial technologies, such as the Internet of Things (IoT), Blockchain, Augmented Reality (AR), Virtual Reality (VR), Open APIs, Big Data, Machine Learning, Smart Contracts, and Cloud Computing, can be employed individually or collectively to benefit the financial ecosystem and its users in numerous ways. These innovative business models for digital financial services are garnering significant global attention, particularly among customers [8].

2.2 DFS and open innovation

"Digital Financial Services (DFS)", also known as "fintech", encompass a wide array of innovative financial products and services enabled by Information and Communication Technologies (ICT) [8, 9]. DFS disrupts conventional financial models through strategies such as disintermediation, access expansion, hybridization, financialization, and customization [10]. As a result of evolving customer behaviors, shifting ecosystems, ICT advancements, and supportive policies, the financial services sector can now offer entirely new, cutting-edge solutions [11]. These solutions encompass a diverse range of mobile services, including bill payments, money transfers, loan requests, insurance purchases, asset management, investment opportunities, and crowdfunding [12].

New technologies such as blockchain, smart devices, cloud computing, AI, and machine learning have revolutionized the role of ICT in the financial industry, presenting novel opportunities, risks, and legal challenges [11, 12]. In Bangladesh, the DFS landscape fosters collaboration between clients, established businesses, and startups, with value creation strategies focused on competition and cooperation among industry actors. Open innovation projects have been pivotal in forging these mutually beneficial relationships and enhancing organizational innovation capabilities [13]. Favorable regulations, reliable telecommunications infrastructure, and numerous digital finance initiatives have supported the adoption of DFS applications in Bangladesh.

2.3 DFS resilience

Digital Financial Services (DFS) have proven to be remarkably resilient in today's rapidly changing financial landscape. Amidst socio-economic fluctuations, technological advancements, and regulatory shifts, DFS have shown a robust capacity to adapt and thrive [14]. Their inherent flexibility and digitized architecture enable them to withstand shocks and disturbances, thereby offering a more reliable and accessible financial solution. Moreover, DFS's resilience is evident in their ability to provide to diverse user needs, maintain service continuity during crises, and constantly innovate to improve user experience [15].

The conceptual literature on resilience has expanded to encompass a wide range of topics, including health services, disaster management, donation and many more [16]. Resilience can be defined as an individual's ability to cope with environmental shocks continuously. People can positively adapt in challenging situations by leveraging their resources and attributes, such as problem-solving abilities. During crises or emergencies, information and communication technology (ICT) plays a critical role in fostering resilient communities and individuals [17].

Digital finance innovations contribute to enhancing the resilience of rural and vulnerable populations, particularly those in developing countries, by facilitating access to financial resources. This access bolsters their economic robustness in times of crisis. In underserved regions, people can use mobile applications to access various financial services, including payments, savings, loans, and microcredit. Prominent examples of digital finance technologies offering financial services in Bangladesh include mobile services like BKash, Nagad, and Rocket etc. Recent studies suggest that DFS can provide financial services to 62.5% of unbanked individuals in Bangladesh [18]. By incorporating DFS into their resilience strategies, these populations can better withstand economic challenges and improve their overall well-being.

2.4 DFS in Bangladesh

The Fourth Industrial Revolution (4IR) is characterized by the pervasive use of technology, and Bangladesh is no exception to the global trend of the financial sector embracing 4IR. The traditional banking system in Bangladesh faces challenges posed by technological innovations in digital financial services. The government's efforts to establish "Digital Bangladesh" from 2009 to 2021 played a significant role in achieving this milestone. Key stakeholders in Bangladesh's DFS ecosystem include the central bank, commercial banks, mobile banking services, iFarmer, PayWell, Bimafy, SMEVai, GoRiseMe, and Amartaka. Collectively, they serve over 35 million users, with more than 170 million accounts. DFS providers provided mobile wallets and payment platforms that facilitated transactions worth over 66.1 billion USD in 2021, according to the ICT Division of the Government of Bangladesh [19].

According to the comparative summary statement 2020 of Bangladesh Bank (the central bank of Bangladesh), during the Covid-19 pandemic, electricity bill payments increased by almost doubled from Tk 441.12 crore to Tk 831.43 crore, and merchant payments more than tripled, from Tk 581 crore to Tk 1,879 crore between February to November of 2020 utilizing the digital financial services. Moreover, the government offered cash support to 50 lakh low-income families affected by the coronavirus outbreak through four significant MFS operators.

In light of the recent global economic downturn triggered by the pandemic and the ongoing recovery process, it is crucial to reevaluate Bangladesh Bank's accomplishments in leveraging digital financial innovations to serve underprivileged populations in recent years. Bangladesh deserves recognition as an "early adopter" in the field of digital financial advancements. Over the past few years, Bangladesh Bank and commercial banks in the country have implemented measures such as automating the Credit Information Bureau (CIB), establishing NPSB, BEFTN, and RTGS, adopting blockchain technology in transactions, enhancing online banking, mobile financial services, and agent banking, and applying E-KYC.

Figure 1. Percentage growth in mobile cellular subscriptions and Internet users in Bangladesh

The graph reveals a continuous increase in mobile cellular subscriptions in Bangladesh, reaching 19.1 million in 2006, 67.9 million in 2010, and 176.3 million in 2020. Figure 1 also illustrates the steady growth of internet users in Bangladesh over the years, from 1% in 2006 to 3.7% in 2010 to 24.8% in 2020. This trend shows the public's eagerness to benefit from the fourth industrial revolution, which in turn is driving the expansion of DFS in Bangladesh.

3.1 UTAUT model

The Unified Theory of Acceptance and Use of Technology (UTAUT) model provides the fundamental theoretical framework for our investigation [20]. Its comprehensive applicability and capability to explicate technology adoption and acceptance were instrumental in its selection. This model has undergone significant development in various studies, demonstrating its robustness in examining diverse technological contexts. However, the Technology Acceptance Model (TAM) was developed in the 1990s and subsequently refined in 2003, incorporating four primary constructs that took into account the social relevance of adoption and usage [21]. The model employs four constructs for moderating variables and evaluates these factors to understand their influence on behavioral intentions.

Our study's theoretical underpinning is the UTAUT model [20]. This model has been extensively developed and applied to various perspectives related to technology, making it a suitable choice for examining the adoption and acceptance of diverse technological contexts. The UTAUT model's evaluation of moderating variables contributes to a more comprehensive understanding of behavioral intentions [21].

Despite its strengths, the UTAUT model is fundamentally a broad model of technology adoption [22]. Numerous studies have utilized this model to explore a variety of factors that may influence behavior related to technology adoption [23]. By focusing on specific technology categories, the model becomes more efficient and descriptive than general construct models that attempt to encompass multiple technologies [24].

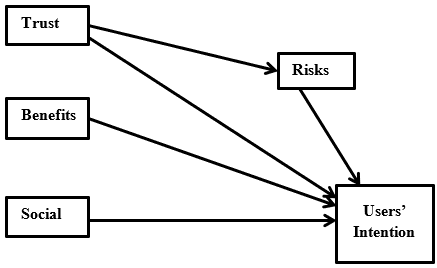

This study postulates that user acceptance of digital financial services significantly impacts the financial industry. Numerous researchers continue to expand the UTAUT model by incorporating additional concepts to elucidate various aspects of technology adoption. Based on previous research findings, the four primary UTAUT attributes are employed in this study, as they are believed to exert a substantial influence on users' intention to utilize Digital Financial Services (DFS). The proposed model, illustrated in Figure 2, offers a comprehensive overview of the factors affecting DFS adoption and usage.

Original UTAUT factors are performance expectancy, effort expectancy, social influence and facilitating condition, whereas users' intention is the dependent variable [25] However, to conduct the study on digital or mobile financial services, researchers adopt some additional variables as a modified UTAUT model, such as risks and trust [26-29]. The cyber security concern in financial institutions and also in money transactions particularly in developing countries face extensively and a concern which is recognized by researchers [30]. Due to insufficient public awareness of cyber security, internet users have limited comprehension and skills to defend themselves against online and mobile security risks [31, 32]. Moreover, the inadequate awareness of internet hacking fosters distrust among consumers of digital financial services in developing nations [33].

As a result, in this study, we included risks and trust to identify the factors that impact users' intention towards the use of Digital Financial Services (DFS). In addition, risks substantially impact the relationship between users' intentions and trust, as previously mentioned, so we employ risks as mediating factors in this model. The proposed model, illustrated in Figure 2, offers a comprehensive overview of the factors affecting DFS adoption and usage.

Figure 2. Modified UTAUT model

Formulating hypotheses in research is an essential process for comprehending the connections between multiple factors and their impact on a particular outcome. In the present study, the dependent variable is users' intention to select financial institutions, assumed to be influenced by several independent variables, including Benefits, Risks, Social Influences, and Trust. The modified UTAUT model serves as the basis for the hypotheses, which explore potential relationships among these variables. By examining these relationships, the study seeks to elucidate the intricate interplay between Benefits, Risks, Social Influences, and Trust, and how these factors collectively influence users' intention to select financial institutions through the adoption of DFS services.

Benefits: Recent advancements in information technology have provided customers with access to a wide array of novel financial services [34]. DFS applications have the potential to make mobile financial transactions more transparent, affordable, and convenient. Key advantages of DFS for customers include reduced time, effort, and cost associated with completing financial transactions [35, 36]. Benefits can be defined as "users' perception of the likelihood that utilizing DFS will result in favorable outcomes." The utility derived from using DFS applications can be reflected in the perceived benefits [35]. Users' intention to utilize these systems is influenced by their perceived usefulness and ease of use. Numerous studies have found that perceived benefits positively influence users' intentions to utilize DFS applications, such as mobile payments and crypto-currencies [37]. Based on these findings, the following hypothesis is proposed:

H1: Benefits of DFS applications have a positive and significant impact on users' behavioral intention.

Risks: Innovations in financial services are frequently accompanied by risks [35, 38, 39], One of the primary barriers to technology adoption is the perceived risk associated with the usage of DFS applications. In the context of DFS, risk is defined as "users' perception of uncertainty and potential adverse consequences arising from the use of DFS" [35]. Operational, financial, security, and privacy concerns are examples of risks associated with DFS applications [39, 40]. These risks deter customers from using digital financial applications, reducing their intention to do so. Furthermore, the intangible nature of DFS applications, coupled with perceived risks such as cyber-attacks and financial loss, discourages users from adopting these services [34]. Previous research findings have indicated a negative correlation between risk and the willingness to use DFS applications. Moreover, risks and trust directly and reciprocally influence customers' intentions to use DFS [38, 41]. Therefore, the following hypothesis is formulated:

H2: Risks associated with DFS applications have a negative and significant impact on users’ behavioral intention.

Social Influence: In the age of social media, customers' decisions to adopt new technologies are significantly influenced by the opinions of their peers [42, 43]. Endorsements from friends, family members, and colleagues can persuade users to embrace novel technologies. In social settings, users frequently engage with mobile services and are influenced by the actions of others [44, 45]. Social influence, also referred to as subjective norms or images, is the extent to which an individual believes that significant people in their life consider it important for them to adopt a new system [21]. Digital financial services, such as mobile banking and payment, have a substantial positive impact on social influence, although this effect is contingent upon factors like previous experience [43, 46]. Consequently, the following hypothesis is posited:

H3: Social influences exert a positive and significant effect on users' behavioral intention.

Trust: In the context of financial transactions, trust is considered crucial for technology acceptance [40, 47]. Establishing strong relationships with customers is a priority in the highly competitive financial services. According to the Oxford Dictionary, trust is the desire of one party to be reliant on the acts of another party with the anticipation that the other party will take a specific action that is significant to the recipients, regardless of the capability to monitor or control that other party. Users' trust in DFS applications indicates their belief in the system's competence, integrity, and benevolence. Conversely, as migrating from traditional financial systems can be costly, trust is deemed crucial for financial service providers [48, 49]. In ambiguous and risky situations, trust can lead to reduced risk perceptions and positive intentions toward adopting new technology [50]. Therefore, the following hypothesis is formulated:

H4: Trust in the DFS system has a positive and significant impact on users' behavioral intention.

H5: Trust in the DFS system has a negative and significant relationship with risks associated with using DFS.

Mediating Effects: It is postulated that users' trust in a system or service shapes their perceptions of risks related to using that system or service [51]. These perceived risks, in turn, influence users' intentions to engage with the system or service. As such, the mediating role of perceived risks elucidates the relationship between trust and users' intentions of choosing financial institutions through DFS, suggesting that trust can indirectly affect users' intentions via perceived risks.

H6: Perceived risks mediate the relationship between trust and users' behavioral intention.

5.1 Research instruments

This study suggests a model consisting of five variables to demonstrate the study framework. In this model, users' intention is the dependent variable, and risks are the mediating factors of trust and users' intention, where trust, risks, benefits, and social influences of DFS are the independent variables. The original UTAUT model was used to pick the survey questions for this study, with some mandatory sections making suitable modifications.

5.2 Designing a questionnaire

In order to get the required information employing a random sample technique, this study develops and distributes modified items of the specified variables through a self-structured questionnaire that chosen participants from the target population fulfilled. Students, employees in the private sector, public sector employees, people in business, and others were invited to participate in this study.

We ensured that participants understood the study's objectives and that all information they provided would be maintained in complete confidentiality. The survey also gathered data on the general profiles of the respondents, including their age, education level, gender, occupation, and location. The respondents from Chattogram and Dhaka divisions of Bangladesh were invited to participate in the study. The survey asked participants to score their level of agreement on a five-point Likert scale, from 1 (strongly disagree) to 5 (strongly agree).

5.3 Sample size-target population

The population sample size includes appropriate responses and is limited to participants from Chattogram and Dhaka divisions in Bangladesh. The minimum educational level for the responders was the Higher Secondary School Certificate (HSC). Participants who had used digital financial services for at least a few years were invited to participate in this study. We made personal visits and phone calls to various educational, government, and private institutions to inform them of the study's objectives and to ask that their students and employees take an active part in it. Some respondents were excluded from the study because they were unwilling to participate and reluctant to respond to inquiries during the pilot test.

The authors provided the respondents 15 days to comprehend and complete the survey once we had educated and trained them about its objectives. The students, people in business, and employees from the relevant institutions were allowed to participate in the survey, and we selected the measurement instruments from the literature to create an initial set of concepts. This study employed a pilot study to determine whether the review would be effective before the final survey began.

The pilot study's participants included students, academics, managers, and officials with in-depth knowledge and understanding of the users' trust, risks, advantages, and societal implications of digital financial services. We delivered 480 surveys to respondents in all, and 442 respondents returned filled-out, appropriate questionnaires. We employed Cronbach’s Alpha Reliability Statistics that is widely utilized metric for evaluating the internal consistency reliability of a set of items within a scale [52]. It measures the degree to which the items correspond to the underlying construct. Values span from 0 to 1, with higher values signifying better internal consistency. Generally, a Cronbach's Alpha value of 0.7 or higher is deemed acceptable, while values over 0.8 are considered excellent [53]. In this analysis, most of the variables exceeded the recommended threshold of 0.7 which means the reliability statistics are significant.

5.4 Data processing of the questionnaires

We distributed 480 surveys to students, people in business, government personnel, employees of private companies, and others in Chattogram and Dhaka. We obtained 442 properly completed questionnaires after analyzing the correctness of data. The three stages of the data-gathering process are shown in Figure 3.

In the first stage, the authors collected and analyzed previous studies to gather the concept of questions and assess the perfect nature of respondents related to the survey's specific variables of digital financial services available in Bangladesh. Through a pilot survey in the second stage, we could realize the dependability of the questionnaire items and make the necessary modifications. We conducted the survey and collected data from the respondents in the third and final stages.

Figure 3. Data collection procedure

Table 1. Respondents’ data on demographic profile

|

Variables |

Frequency |

Percentage |

|

Age (Years) |

||

|

18-24 |

186 |

42% |

|

25-32 |

154 |

35% |

|

33-40 |

53 |

12% |

|

40-50 |

37 |

08% |

|

More than 50 |

12 |

03% |

|

Total |

442 |

100% |

|

Gender |

||

|

Male |

257 |

58% |

|

Female |

185 |

42% |

|

Total |

442 |

100% |

|

Profession |

||

|

Students |

244 |

55% |

|

Job (Private Sector) |

120 |

27% |

|

Job (Public Sector/ Govt.) |

08 |

02% |

|

Business & Others |

70 |

16% |

|

Total |

442 |

100% |

|

Educational Qualifications |

||

|

H.S.C Equivalent |

151 |

34% |

|

Graduation Equivalent |

198 |

45% |

|

Post-Graduation Equivalent |

93 |

21% |

|

Total |

442 |

100% |

|

|

||

|

DFS Account |

Yes |

92% |

|

No |

08% |

|

|

Total |

442 |

100% |

|

Respondent’s Preferences |

DFS System |

94% |

|

Conventional System |

06% |

|

|

Total |

442 |

100% |

Source: Author’s findings

The research study analyzed the demographic information of 442 respondents (Table 1), ranging from 18 to 50+ years old, with a majority falling in the 18-24 age groups. The sample was relatively balanced in terms of gender, with 58% male and 42% female participants. The respondents held varying levels of education, with 34% holding HSC equivalent, 45% holding a bachelor's degree, and 21% holding a master's degree. The occupational profile was diverse, with students, private job holders, public sector job holders, business, and other professions represented. The majority of respondents (94%) preferred to use digital financial systems in the future, and most already had a digital financial services account (92%).

5.5 Model specification and estimation

To evaluate the effectiveness of the modified UTAUT framework in understanding the factors that influence customers' choice of financial institutions in Bangladesh, a Structural Equation Modeling (SEM) approach was employed. The SEM analysis allowed for a comprehensive examination of the relationships between observed and latent variables, and the Smart PLS 4.0 software was used to estimate the parameters of the SEM. Furthermore, it is an optimal choice due to its aptitude for managing complex models and addressing non-normal data. A path measurement model was developed to define the relationships between each UTAUT-based latent construct and its corresponding observed variables, with the statistical significance of the path coefficients tested through a bootstrapping procedure with 5000 samples.

To evaluate reliability and convergent validity of the measurement model Cronbach's Alpha, Composite Reliability (CR), and Average Variance Extracted (AVE) were utilized for this purpose, and subsequently to evaluate discriminant validity by employing the Heterotrait-Monotrait (HTMT) matrix and the Fornell-Larcker criterion. These tools validated the intelligibility of the constructs, ensuring they did not excessively overlap and preserving the uniqueness of constructs in the model. Overall, this approach will provide financial institutions with a more comprehensive understanding of the underlying mechanisms that drive customers' choices, ultimately helping them better cater to their needs and preferences.

A comprehensive multivariate statistical technique widely used to explore complex interactions between observed and latent variables across a wide range of fields is structural equation modeling (SEM) analysis [54]. In this regard, a number of important metrics, including Cronbach's Alpha, Composite Reliability (CR), Average Variance Extracted (AVE), Heterotrait-Monotrait (HTMT) matrix, Fornell-Larcker Criterion, Variance Inflation Factor (VIF), and Standardized Root Mean Square Residual (SRMR), play a crucial role in assessing the quality and robustness of the model under investigation [53]. These measurements help to evaluate the model thoroughly, assuring its correctness and capacity to be applied to the broader.

For assessing the internal consistency and reliability of a group of items inside a scale, Cronbach's Alpha (Table 2) is a commonly used metric [52]. It measures the degree to which the objects correspond to the underlying construct. Generally, higher values indicate more substantial internal consistency of the variables, which range from 0 to 1. Cronbach's Alpha levels between 0.7 and 0.8 are often regarded as satisfactory, whereas values over 0.8 are considered outstanding [53]. The majority of the variables in this research exceeded the recommended threshold of 0.7. This means the reliability statistics are considerably based on these findings, which supports the use of the SEM method for further analysis.

Table 2. Cronbach’s alpha reliability statistics

|

|

B0 |

IN |

R0 |

S0 |

T0 |

|

B01 |

0.804 |

|

|

|

|

|

B02 |

0.733 |

|

|

|

|

|

B03 |

0.594 |

|

|

|

|

|

B04 |

0.707 |

|

|

|

|

|

I01 |

|

0.826 |

|

|

|

|

I02 |

|

0.794 |

|

|

|

|

I03 |

|

0.679 |

|

|

|

|

I04 |

|

0.701 |

|

|

|

|

R01 |

|

|

0.788 |

|

|

|

R02 |

|

|

0.871 |

|

|

|

R03 |

|

|

0.649 |

|

|

|

R04 |

|

|

0.794 |

|

|

|

S01 |

|

|

|

0.741 |

|

|

S02 |

|

|

|

0.663 |

|

|

S03 |

|

|

|

0.767 |

|

|

S04 |

|

|

|

0.731 |

|

|

T01 |

|

|

|

|

0.844 |

|

T02 |

|

|

|

|

0.707 |

|

T03 |

|

|

|

|

0.504 |

|

T04 |

|

|

|

|

0.735 |

Table 3. Cronbach’s alpha, composite reliability, and AVE

|

|

Cronbach's Alpha |

Composite Reliability (CR) |

Average Variance Extracted (AVE) |

|

B0 |

0.719 |

0.856 |

0.639 |

|

IN |

0.736 |

0.895 |

0.695 |

|

R0 |

0.751 |

0.778 |

0.679 |

|

S0 |

0.697 |

0.766 |

0.571 |

|

T0 |

0.725 |

0.721 |

0.525 |

In Structural Equation Modeling (SEM), Composite Reliability (CR) is a measure used to evaluate the internal consistency of latent variables within a model. It assesses the extent to which a set of observed variables consistently represents the underlying latent construct. Composite Reliability (Table 3) is an alternative to Cronbach's Alpha and is often considered a more accurate measure of internal consistency, as it takes into account the factor loadings of individual indicators [55]. Generally, a CR value of 0.7 or higher is considered acceptable, indicating that the latent construct is reliably measured by the observed variables [54]. By examining the above Composite Reliability of latent variables, it can be determining the adequacy of the measurement models and ensure the validity and reliability of the constructs in this analysis.

Average Variance Extracted (AVE) is a measure used to assess the convergent validity of latent variables within a model. Convergent validity refers to the extent to which observed variables related to the same latent construct are highly correlated. AVE measures the amount of variance that a latent variable capture from its indicators, relative to the variance due to measurement error [56]. An AVE value of 0.50 or higher is considered acceptable, suggesting that the latent construct accounts for more than 50% of the variance in its observed variables [53]. By examining the above AVE values, it can assess the adequacy of their measurement models in terms of convergent validity due to all the variables exceeded the value of 0.50, and it ensure the constructs in the analysis are accurately represented by the observed variables.

Table 4. HTMT matrix

|

|

B0 |

IN |

R0 |

S0 |

T0 |

|

B0 |

|

|

|

|

|

|

IN |

0.587 |

|

|

|

|

|

R0 |

0.163 |

0.183 |

|

|

|

|

S0 |

0.341 |

0.539 |

0.242 |

|

|

|

T0 |

0.571 |

0.425 |

0.427 |

0.418 |

|

The Heterotrait-Monotrait (HTMT) matrix (Table 4) is a measure used to assess discriminant validity among latent variables within a model. Discriminant validity refers to the extent to which different latent constructs are distinct from one another, ensuring that they represent unique dimensions of the phenomenon under investigation. HTMT values typically range between 0 and 1, with lower values indicating better discriminant validity. A common threshold for acceptable discriminant validity is an HTMT value less than 0.85 or, more conservatively, less than 0.90 [57]. By examining the HTMT matrix from the above results, it can be assessed that the adequacy of their measurement models in terms of discriminant validity and ensure that the latent constructs are distinct and not overlapping.

Table 5. Fornell-Larcker criterion

|

|

B0 |

IN |

R0 |

S0 |

T0 |

|

B0 |

0.799 |

|

|

|

|

|

IN |

0.476 |

0.834 |

|

|

|

|

R0 |

-0.163 |

-0.241 |

0.824 |

|

|

|

S0 |

0.281 |

0.409 |

-0.126 |

0.756 |

|

|

T0 |

0.317 |

0.311 |

-0.373 |

0.224 |

0.724 |

Fornell-Larcker Criterion is a widely used approach for assessing discriminant validity among latent variables within a model. The Fornell-Larcker Criterion is based on the comparison of the square root of the Average Variance Extracted (AVE) for each latent construct with the correlations between the latent constructs [56]. According to the Fornell-Larcker Criterion, discriminant validity is established when the square root of the AVE for each latent construct is greater than its correlations with all other latent constructs in the model. This indicates that each construct shares more variance with its own indicators than it shares with other constructs in the model [54]. By applying the Fornell-Larcker Criterion, in the Table 5 we found the adequacy of measurement models in terms of discriminant validity and ensure the latent constructs are distinct and not overlapping.

Table 6. Coefficient of determination (R2) values

|

|

R-square |

R-square Adjusted |

|

IN |

0.574 |

0.551 |

|

R0 |

0.221 |

0.214 |

R-square (Table 6) is employed to determine a model's consistency or how well it fits the data. Based on the above constructed model, the study suggested that the direct effect method R-square is 0.57 among the variables using extended UTAUT approach. For the indirect approach of our study considering the mediating relationship among the variables Trust, Risks and Users’ Intention the R-square value is 0.22. From the above values of R-square it can be decided that the direct effects are moderate and the indirect effect is weak through it followed by the rules of thump that is, an R2 value of 0.25 is weak, 0.50 would be moderate, and 0.75 would be strong, respectively.

Table 7. Variance Inflation Factor (VIF) test

|

Variables Name |

VIF |

Variables Name |

VIF |

|

B01 |

1.242 |

R03 |

1.194 |

|

B02 |

1.288 |

R04 |

1.333 |

|

B03 |

1.099 |

S01 |

1.062 |

|

B04 |

1.127 |

S02 |

1.125 |

|

I01 |

1.315 |

S03 |

1.087 |

|

I02 |

1.392 |

S04 |

1.064 |

|

I03 |

1.211 |

T01 |

1.055 |

|

I04 |

1.147 |

T02 |

1.028 |

|

R01 |

1.205 |

T03 |

1.033 |

|

R02 |

1.392 |

T04 |

1.027 |

The Variance Inflation Factor (VIF) (Table 7) is a diagnostic tool used in Structural Equation Modeling (SEM) to assess multicollinearity among the predictor variables [58]. Multicollinearity occurs when predictor variables are highly correlated, which can lead to unstable parameter estimates and reduced model interpretability. VIF values greater than 10 are generally considered indicative of multicollinearity issues, while values below 5 are considered acceptable. From the above, it is established that the variables are not have an issue of multicollinerarity.

Table 8. Goodness of fit test

|

|

Saturated Model |

Estimated Model |

|

SRMR |

0.073 |

0.073 |

The Standardized Root Mean Square Residual (SRMR) is an important goodness-of-fit test (Table 8) in Structural Equation Modeling (SEM) that measures the discrepancy between observed and predicted covariance matrices. Lower SRMR values signify a better fit between the model and the observed data, with values less than 0.08 generally considered indicating a good fit [59]. In the study, the SRMR value was found to be 0.073, which falls within the acceptable threshold. This suggests that the model's fit to the observed data is relatively good, indicating that the model adequately represents the underlying relationships among the constructs.

6.1 Structural model analysis:

Structural Equation Modeling (SEM) serves as a robust and sophisticated multivariate statistical technique, extensively utilized to explore intricate relationships among observed and latent variables. If the measurement model evaluation is satisfactory, we can move on to the structural model evaluation, concentrating on the efficacy of its explanation and the statistical significance of the path coefficients [53]. This step-by-step approach allows for a comprehensive examination of the relationships among variables and contributes to the stability and reliability of the overall model. From the below, each observed and latent variables path coefficient values are described through the following structural line (Figure 4):

Figure 4. Path coefficient values

6.2 Structural model path significance values

Using 5000 samples, an advanced bootstrapping technique was used to examine the statistical significance level in path coefficients. Figure 5 shows the outcomes of the structural equation analysis. From the above, it is found that the variables Benefits and Social influences have a strong positive significance on the dependent variable users’ behavioral intention of using digital financial services in Bangladesh. On the other hand, the variables Trust factors and Risks factors of DFS are not statistically significant on the users’ behavioral intention of using DFS in Bangladesh.

For finding and analyzing the effects of earlier developed hypothesis on the perception of using DFS in Bangladesh helps to reveal the role of variables in relationships within the study. From the Table 9, the hypothesis H1 (β = 0.000; p < 0.05), H3 (β = 0.000; p < 0.05) and H5 (β = 0.000; p < 0.05) are found significant and supported the hypothesis earlier we developed. However, H2 (β = 0.056; p > 0.05), and H4 (β = 0.083; p > 0.05) are not statistically significant and do not support the hypothesis of using digital financial services for choosing financial institutions in Bangladesh.

The findings indicate that Benefits of using DFS and Social Influences positively impact users' intention to choose a financial institution. This aligns with previous research that highlights the importance of perceived benefits [60] and social influences [21] as critical determinants of technology adoption. However, Trust on DFS system and Perceived Risks were not found to significantly influence Users' intention to choose a financial institution in Bangladesh. This suggests that user attitudes towards trust and perceived risks might be influenced by other contextual factors, such as regulatory frameworks, cultural aspects, or the extent of familiarity with DFS.

Table 9. Structural model decision rule

|

|

Path Coefficient |

Sample Mean (M) |

Standard Deviation (STDEV) |

T Statistics (|O/STDEV|) |

P Values |

Decision Rule |

|

B0 -> IN |

0.308 |

0.313 |

0.047 |

6.552 |

0.00*** |

H1 Supported |

|

R0 -> IN |

-0.09 |

-0.091 |

0.047 |

1.908 |

0.056 |

H2 Not Supported |

|

S0 -> IN |

0.24 |

0.248 |

0.045 |

5.386 |

0.00*** |

H3 Supported |

|

T0 -> IN |

0.09 |

0.097 |

0.052 |

1.735 |

0.083 |

H4 Not Supported |

|

T0 -> R0 |

-0.273 |

-0.287 |

0.042 |

6.537 |

0.00*** |

H5 Supported |

Notes: **significant at 5% level; *** significant at 1% level.

Table 10. Mediating effects

|

|

Path Coefficient |

Sample Mean (M) |

Standard Deviation (STDEV) |

T Statistics (|O/STDEV|) |

P Values |

Decision Rule |

|

T0 -> R0 -> IN |

0.025 |

0.026 |

0.014 |

1.779 |

0.075 |

H6 Not Supported |

Notes: **significant at 5% level; *** significant at 1% level.

Figure 5. Path significance level

In Table 10, analyzing indirect effects helps uncover the mediating role of variables in relationships among constructs. The above analysis focuses on the indirect effect between trust and users' behavioral intention through the mediating variable risk. A positive insignificant relationship implies that the mediating role of risk in the relationship between trust and users' behavioral intention is not statistically significant, suggesting that the indirect effect through risk is not considerably influential.

6.3 Discussion of analysis

Digital Financial Services (DFS) have been rapidly embraced in Bangladesh and have changed the financial landscape by providing customers with a number of benefits. DFS offers a number of advantages in Bangladesh, including improved accessibility, convenience, cost-effectiveness, and quicker transactions [35]. These benefits are especially important for those living in rural areas because they frequently have less access to regular banking activities. Customers are, therefore, more likely to select financial institutions that provide digital financial services that are personalized to their requirements and preferences.

The importance of knowing and meeting customer demands in the competitive financial landscape is highlighted by the positive significant association between the benefits of using DFS and the preference of financial institutions in Bangladesh. Financial institutions that successfully integrate digital financial services to offer user-friendly, effective, and secure solutions will likely acquire a more extensive client base and gain a competitive edge in the market [36]. In order to meet the changing demands of their clients and promote a more inclusive financial ecosystem, financial service providers should emphasize the creation and use of cutting-edge DFS solutions.

Social influences in the research affect how DFS is adopted regarding interpersonal interactions, peer perceptions, and cultural norms [21]. When evaluating the usage of digital financial services and choosing financial institutions, people frequently depend on the opinions and recommendations of their social networks. The importance of social influences in prompting user adoption and determining the choices of financial institutions grows as DFS gains popularity and acceptance. Financial institutions in Bangladesh should consider social factors while developing their client engagement and marketing strategies. Financial institutions may use social influences to draw in and keep customers by promoting great customer experiences, encouraging referrals from friends and family, and using social media platforms [61].

As customers may be concerned about potential losses, fraud, privacy violations, and system malfunctions, perceived risks are frequently seen as a barrier to the adoption of digital financial services [35]. This finding suggests that financial institutions in Bangladesh may have been somewhat effective in addressing and alleviating customers' concerns about risks through the deployment of strong security measures, user-friendly interfaces, and rapid customer service [39]. Furthermore, while perceived risk concerns are frequently believed to have a negative impact on users' decisions about financial institutions, the lack of significance of this impact in the context of Bangladesh emphasizes the need to take into account the complex relationships between numerous factors that influence customer preferences. Financial institutions in Bangladesh should keep putting a priority on risk management and security procedures while also concentrating on utilizing the advantages of DFS, social impacts, and trust to draw in and keep customers.

Users' trust typically plays a crucial role in financial organizations that they perceive as dependable, safe, and transparent for the adoption of digital financial services [62, 63]. The lack of significance of trust factors in Bangladesh's financial institution selection suggests that other factors, such as the benefits of DFS and social influences, may have a greater impact on users' choices. According to this result, trust may not be the key factor influencing customers' choice of financial institutions in Bangladesh, yet it still remains a crucial one. The country's increasing acceptance of DFS as well as the existence of several reputable financial institutions may have a negative impact on the importance of trust as a deciding criterion [51]. To draw and keep consumers, financial institutions in Bangladesh should not just put their efforts into establishing trust; they should also emphasize providing concrete benefits of using DFS, capitalizing on social influences, and reducing perceived risks.

However, the mediating factor demonstrates that although trust and perceived risk are essential factors for consumers, their influence on financial institutions' behavioral intentions and decisions may not be as significant as initially assumed. This may be attributed to the growing acceptance of digital financial services and the increasing awareness of users regarding the potential risks and benefits associated with DFS. The positive insignificant relationship between trust, risks, and users' behavioral intention in the Bangladeshi context highlights the importance of understanding the complex interplay of factors affecting customers' preferences.

This research employed a modified model of the UTAUT theory to examine the intention to use DFS factors impact on financial institutions choice in Bangladesh perspective. The survey data obtained from 442 participators and SEM were used to examine the research model and its corresponding hypotheses. This research paper explored the relationships between various factors such as Benefits, Social Influences, Trust, and Perceived Risks, and their influence on users' intention to choose financial institutions. The study found that Benefits and Social Influences had a significant positive impact on the choice of financial institutions in the Bangladesh context.

Moreover, Trust factors and Perceived Risks showed an insignificant relationship with users' intention to choose financial institutions. Furthermore, the analysis of the mediating role of risk in the relationship between trust and users' behavioral intention revealed a positive insignificant relationship. This indicates that other factors, such as social influences and perceived benefits of using DFS, might be more influential in shaping users' choices of financial institutions in Bangladesh. Moreover, these findings emphasize the importance of understanding the complex interplay of factors affecting customers' preferences and highlight the need for financial institutions in Bangladesh to focus not only on building trust and managing risks but also on leveraging social influences and the benefits of using DFS to attract and retain customers.

However, the study is restricted geographically to Bangladesh; thus, the findings might not apply to other cultural or socio-economic contexts. Also, it considers a specific point in time, disregarding any changes in attitudes that might occur over a longer period due to shifts in technology or market trends. The cross-sectional design and the reliance on a modified UTAUT framework also restrict the depth of our insights. Future research could further explore the reasons behind these findings and investigate additional factors that might influence users' choice of financial institutions in Bangladesh. By doing so, it will contribute to the development of more effective strategies and interventions to promote the adoption of digital financial services and improve the overall financial ecosystem in the country.

This study emphasizes key practical recommendations for financial institutions aiming to enhance their Digital Financial Services (DFS). Firstly, leveraging social influence can be pivotal; creating DFS awareness campaigns and referral programs that incentivize current users to bring in new users could be an effective strategy. Secondly, promoting the benefits of DFS in a more targeted and personalized manner, keeping in mind the user profiles, could lead to greater adoption rates. Educational programs aimed at showcasing how DFS simplifies financial transactions, increases accessibility, and reduces transaction costs could also contribute to more positive perceptions.

Additionally, building trust remains important part of DFS using intention development. It can be accomplished by ensuring the security, user-friendliness, and reliability of DFS platforms. Transparency about security protocols, prompt customer service, and responsiveness to user feedback could reinforce trust. Risk mitigation is another key aspect, this can be achieved by strengthening cybersecurity measures, providing transparency in service terms and conditions, and offering rapid response and resolution to any DFS-related issues that customers might encounter.

To gain a competitive advantage, continual innovation and customization of DFS offerings are essential. Embracing new technologies like AI and data analytics can personalize customer experience, thereby setting institutions apart in the competitive DFS landscape. These strategies can effectively drive DFS adoption and secure a competitive position in the market.

This research paper is financed by the Research & Publication Cell, University of Chittagong, Chattogram-4331, Bangladesh, under the revenue budget of the year 2021-2022.

[1] Jeevan, M. (2000). Only Banks - No Bricks. Voice and Data.

[2] Degryse, H., Ongena, S. (2008). Competition and regulation in the banking sector: A review of the empirical evidence on the sources of bank rents. Handbook of Financial Intermediation and Banking, 2008: 483-554. https://doi.org/10.1016/B978-044451558-2.50023-4

[3] Al‐Eisa, A.S., Alhemoud, A.M. (2009). Using a multiple‐attribute approach for measuring customer satisfaction with retail banking services in Kuwait. International Journal of Bank Marketing, 27(4): 294-314. https://doi.org/10.1108/02652320910968368

[4] Walker, A.G., Smither, J.W., Waldman, D.A. (2008). A longitudinal examination of concomitant changes in team leadership and customer satisfaction. Personnel Psychology, 61(3): 547-577. https://doi.org/10.1111/j.1744-6570.2008.00122.x

[5] Alhemoud, A.M. (2010). Banking in Kuwait: A customer satisfaction case study. Competitiveness Review: An International Business Journal, 20(4): 333-342. https://doi.org/10.1108/10595421011065334

[6] AlNajem, M.N. (2018). Factors influencing customer choice in selection of banks in Kuwait. Quality Management Journal, 25(3): 142-153. https://doi.org/10.1080/10686967.2018.1474678

[7] Mondal, K., Saha, A.K. (2013). Client satisfaction of internet banking service in Bangladesh: An exploratory study. ASA University Review, 7(1): 131-141.

[8] Puschmann, T. (2017). Fintech. Business & Information Systems Engineering, 59: 69-76. https://doi.org/10.1007/s12599-017-0464-6

[9] Arner, D.W., Buckley, R.P., Zetzsche, D.A. (2018). Fintech for financial inclusion: A framework for digital financial transformation. UNSW Law Research Paper, 18-87.

[10] Chen, M.A., Wu, Q., Yang, B. (2019). How valuable is FinTech innovation?. The Review of Financial Studies, 32(5): 2062-2106. https://doi.org/10.1093/rfs/hhy130

[11] Tabetando, R., Matsumoto, T. (2020). Mobile money, risk sharing, and educational investment: Panel evidence from rural Uganda. Review of Development Economics, 24(1): 84-105. https://doi.org/10.1111/rode.12644

[12] DesJardine, M., Bansal, P., Yang, Y. (2019). Bouncing back: Building resilience through social and environmental practices in the context of the 2008 global financial crisis. Journal of Management, 45(4): 1434-1460. https://doi.org/10.1177/0149206317708854

[13] Mujeri, M.K., Azam, S. (2018). Role of digital financial services in promoting inclusive growth in Bangladesh: Challenges and opportunities. Institute for Inclusive Finance and Development, Working Paper, 55.

[14] Cooke, A.N. (2021). The Brick-and-Mortar Bank is Dead-COVID-19 Killed It: Analyzing the" New Normal" for Data Security in the Increasingly Digital Financial Services Industry. NC Bank. Inst., 25: 419.

[15] Shrier, D.L. (2022). Digital Financial Services. Global Fintech. https://doi.org/10.7551/mitpress/13673.003.0008

[16] Karusala, N., Holeman, I., Anderson, R. (2019). Engaging identity, assets, and constraints in designing for resilience. Proceedings of the ACM on Human-Computer Interaction, 3(CSCW): 1-23. https://doi.org/10.1145/3359315

[17] Bharadwaj, P., Jack, W., Suri, T. (2019). Fintech and household resilience to shocks: Evidence from digital loans in Kenya (No. w25604). National Bureau of Economic Research. https://doi.org/10.3386/w25604

[18] Aziz, A., Naima, U. (2021). Rethinking digital financial inclusion: Evidence from Bangladesh. Technology in Society, 64: 101509. https://doi.org/10.1016/j.techsoc.2020.101509

[19] Rashid, M.H. (2020). Prospects of digital financial services in Bangladesh in the context of fourth industrial revolution. Asian Journal of Social Science, 2(5): 88-95. https://doi.org/10.34104/ajssls.020.088095

[20] Sarfaraz, J. (2017). Unified theory of acceptance and use of technology (UTAUT) model-mobile banking. Journal of Internet Banking and Commerce, 22(3): 1-20.

[21] Venkatesh, V., Thong, J.Y., Xu, X. (2012). Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Quarterly, 157-178. https://doi.org/10.2307/41410412

[22] Obienu, A.C., Amadin, F.I. (2021). User acceptance of learning innovation: A structural equation modelling based on the GUAM framework. Education and Information Technologies, 26(2): 2091-2123. https://doi.org/10.1007/s10639-020-10341-x

[23] Alasmari, T., Zhang, K. (2019). Mobile learning technology acceptance in Saudi Arabian higher education: An extended framework and A mixed-method study. Education and Information Technologies, 24(3): 2127-2144. https://doi.org/10.1007/s10639-019-09865-8

[24] Rahi, S., Mansour, M.M.O., Alghizzawi, M., Alnaser, F.M. (2019). Integration of UTAUT model in internet banking adoption context: The mediating role of performance expectancy and effort expectancy. Journal of Research in Interactive Marketing, 13(3): 411-435. https://doi.org/10.1108/JRIM-02-2018-0032

[25] Attuquayefio, S., Addo, H. (2014). Using the UTAUT model to analyze students’ ICT adoption. International Journal of Education and Development Using ICT, 10(3): 75-86.

[26] Tohang, V., Lo, E., Anggraeni, A. (2021). Financial Technology 3.0 adoption in financial and non-financial institutions from Modified Utaut perspective. In Conference on International Issues in Business and Economics Research (CIIBER 2019), pp. 1-6. https://doi.org/10.2991/aebmr.k.210121.001

[27] Ivanova, A., Kim, J.Y. (2022). Acceptance and use of mobile banking in Central Asia: Evidence from modified UTAUT model. The Journal of Asian Finance, Economics and Business, 9(2): 217-227. https://doi.org/10.13106/jafeb.2022.vol9.no2.0217

[28] Oh, J.C., Yoon, S.J. (2014). Predicting the use of online information services based on a modified UTAUT model. Behaviour & Information Technology, 33(7): 716-729. https://doi.org/10.1080/0144929X.2013.872187

[29] Tang, K.L., Aik, N.C., Choong, W.L. (2021). A modified UTAUT in the context of m-payment usage intention in Malaysia. Journal of Applied Structural Equation Modeling, 5(1): 40-59. https://doi.org/10.47263/JASEM.5(1)05

[30] Alghazo, J.M., Kazmi, Z., Latif, G. (2017). Cyber security analysis of internet banking in emerging countries: User and bank perspectives. In 2017 4th IEEE International Conference on Engineering Technologies and Applied Sciences (ICETAS), Salmabad, Bahrain, pp. 1-6. https://doi.org/10.1109/ICETAS.2017.8277910

[31] Khan, N.F., Ikram, N., Saleem, S., Zafar, S. (2022). Cyber-security and risky behaviors in a developing country context: A Pakistani perspective. Security Journal, 36: 373-405. https://doi.org/10.1057/s41284-022-00343-4

[32] Nweke, L.O., Bokolo, A.J., Mba, G., Nwigwe, E. (2022). Investigating the effectiveness of a HyFlex cyber security training in a developing country: A case study. Education and Information Technologies, 27(7): 10107-10133. https://doi.org/10.1007/s10639-022-11038-z

[33] AlMindeel, R., Martins, J.T. (2021). Information security awareness in a developing country context: Insights from the government sector in Saudi Arabia. Information Technology & People, 34(2): 770-788. https://doi.org/10.1108/ITP-06-2019-0269

[34] Gomber, P., Kauffman, R.J., Parker, C., Weber, B.W. (2018). On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. Journal of management information systems, 35(1): 220-265. https://doi.org/10.1080/07421222.2018.1440766

[35] Ryu, H.S. (2018). What makes users willing or hesitant to use Fintech? The moderating effect of user type. Industrial Management & Data Systems, 118(3): 541-569. https://doi.org/10.1108/IMDS-07-2017-0325

[36] Kim, Y., Park, Y.J., Choi, J., Yeon, J. (2015). An empirical study on the adoption of “Fintech” service: Focused on mobile payment services. Advanced Science and Technology Letters, 114(26): 136-140. http://dx.doi.org/10.14257/astl.2015.114.26

[37] Ahamad, S., Nair, M., Varghese, B. (2013). A survey on crypto currencies. In 4th International Conference on Advances in Computer Science, AETACS, pp. 42-48.

[38] Kim, D.J., Ferrin, D.L., Rao, H.R. (2008). A trust-based consumer decision-making model in electronic commerce: The role of trust, perceived risk, and their antecedents. Decision Support Systems, 44(2): 544-564. https://doi.org/10.1016/j.dss.2007.07.001

[39] Rouibah, K., Lowry, P.B., Hwang, Y. (2016). The effects of perceived enjoyment and perceived risks on trust formation and intentions to use online payment systems: New perspectives from an Arab country. Electronic Commerce Research and Applications, 19: 33-43. https://doi.org/10.1016/j.elerap.2016.07.001

[40] Liébana-Cabanillas, F., Muñoz-Leiva, F., Sánchez-Fernández, J. (2018). A global approach to the analysis of user behavior in mobile payment systems in the new electronic environment. Service Business, 12: 25-64. https://doi.org/10.1007/s11628-017-0336-7

[41] Zhang, J., Mao, E. (2008). Understanding the acceptance of mobile SMS advertising among young Chinese consumers. Psychology & Marketing, 25(8): 787-805. https://doi.org/10.1002/mar.20239

[42] Ho, R.C., Amin, M., Ryu, K., Ali, F. (2021). Integrative model for the adoption of tour itineraries from smart travel apps. Journal of Hospitality and Tourism Technology, 12(2): 372-388. https://doi.org/10.1108/JHTT-09-2019-0112

[43] de Sena Abrahão, R., Moriguchi, S.N., Andrade, D.F. (2016). Intention of adoption of mobile payment: An analysis in the light of the Unified Theory of Acceptance and Use of Technology (UTAUT). RAI Revista de administracao e Inovacao, 13(3): 221-230. https://doi.org/10.1016/j.rai.2016.06.003

[44] Beldad, A.D., Hegner, S.M. (2018). Expanding the technology acceptance model with the inclusion of trust, social influence, and health valuation to determine the predictors of German users’ willingness to continue using a fitness app: A structural equation modeling approach. International Journal of Human–Computer Interaction, 34(9): 882-893. https://doi.org/10.1080/10447318.2017.1403220

[45] Koenig-Lewis, N., Marquet, M., Palmer, A., Zhao, A.L. (2015). Enjoyment and social influence: Predicting mobile payment adoption. The Service Industries Journal, 35(10): 537-554. https://doi.org/10.1080/02642069.2015.1043278

[46] Singh, N., Sinha, N. (2020). How perceived trust mediates merchant's intention to use a mobile wallet technology. Journal of Retailing and Consumer Services, 52: 101894. https://doi.org/10.1016/j.jretconser.2019.101894

[47] Shao, Z., Zhang, L., Li, X., Guo, Y. (2019). Antecedents of trust and continuance intention in mobile payment platforms: The moderating effect of gender. Electronic Commerce Research and Applications, 33: 100823. https://doi.org/10.1016/j.elerap.2018.100823

[48] Stewart, H., Jürjens, J. (2018). Data security and consumer trust in FinTech innovation in Germany. Information & Computer Security, 26(1): 109-128. https://doi.org/10.1108/ICS-06-2017-0039

[49] Pi, S.M., Liao, H.L., Chen, H.M. (2012). Factors that affect consumers' trust and continuous adoption of online financial services. International Journal of Business and Management, 7(9): 108-119. http://dx.doi.org/10.5539/ijbm.v7n9p108

[50] Li, Z., Sha, Y., Song, X., Yang, K., ZHao, K., Jiang, Z., Zhang, Q. (2020). Impact of risk perception on customer purchase behavior: A meta-analysis. Journal of Business & Industrial Marketing, 35(1): 76-96. https://doi.org/10.1108/JBIM-12-2018-0381

[51] Al Nawayseh, M.K. (2020). Fintech in COVID-19 and beyond: What factors are affecting customers’ choice of fintech applications? Journal of Open Innovation: Technology, Market, and Complexity, 6(4): 153. https://doi.org/10.3390/joitmc6040153

[52] Cronbach, L.J. (1951). Coefficient alpha and the internal structure of tests. Psychometrika, 16(3): 297-334. https://doi.org/10.1007/BF02310555

[53] Hair, J.F., Risher, J.J., Sarstedt, M., Ringle, C.M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1): 2-24. https://doi.org/10.1108/EBR-11-2018-0203

[54] Hair Jr, J.F., Matthews, L.M., Matthews, R.L., Sarstedt, M. (2017). PLS-SEM or CB-SEM: Updated guidelines on which method to use. International Journal of Multivariate Data Analysis, 1(2): 107-123. https://doi.org/10.1504/IJMDA.2017.087624

[55] Raykov, T. (1997). Estimation of composite reliability for congeneric measures. Applied Psychological Measurement, 21(2): 173-184. https://doi.org/10.1177/01466216970212006

[56] Fornell, C., Larcker, D.F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Journal of Marketing Research, 18(3): 382-388.

[57] Henseler, J., Ringle, C.M., Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43: 115-135. https://doi.org/10.1007/s11747-014-0403-8

[58] Härdle, W.K., Simar, L. (2015). Applied Multivariate Statistical Analysis. fourth edition. Springer Berlin, Heidelberg. https://doi.org/10.1007/978-3-662-45171-7

[59] Hu, L.T., Bentler, P.M. (1999). Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: A Multidisciplinary Journal, 6(1): 1-55. https://doi.org/10.1080/10705519909540118

[60] Chitungo, S.K., Munongo, S. (2013). Extending the technology acceptance model to mobile banking adoption in rural Zimbabwe. Journal of Business Administration and Education, 3(1): 51-79.

[61] Kingiri, A.N., Fu, X. (2020). Understanding the diffusion and adoption of digital finance innovation in emerging economies: M-Pesa money mobile transfer service in Kenya. Innovation and Development, 10(1): 67-87. https://doi.org/10.1080/2157930X.2019.1570695

[62] Liébana-Cabanillas, F., Marinkovic, V., De Luna, I.R., Kalinic, Z. (2018). Predicting the determinants of mobile payment acceptance: A hybrid SEM-neural network approach. Technological Forecasting and Social Change, 129: 117-130. https://doi.org/10.1016/j.techfore.2017.12.015

[63] Cao, X., Yu, L., Liu, Z., Gong, M., Adeel, L. (2018). Understanding mobile payment users’ continuance intention: A trust transfer perspective. Internet Research, 28(2): 456-476. https://doi.org/10.1108/IntR-11-2016-0359