Bahtiar Effendi*![]() | Rafles Ginting

| Rafles Ginting![]() | Ahalik

| Ahalik![]() | Irma Paramita Sofia

| Irma Paramita Sofia![]() | Yana Ermawati

| Yana Ermawati![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study aims to explore the influence of institutional ownership, managerial ownership, and audit committees on carbon emission disclosure, while considering environmental performance as a moderating variable. A quantitative approach was employed using Moderated Regression Analysis (MRA) over a five-year observation period. The findings reveal that institutional ownership and audit committees have a significant effect on carbon emission disclosure, whereas managerial ownership does not exhibit a significant influence. These results support the hypothesis that corporate governance structure plays a crucial role in enhancing corporate environmental transparency. Furthermore, the effectiveness of governance mechanisms is influenced by environmental performance, which is shown to moderate the relationship between the audit committee and carbon disclosure, but not the relationships involving institutional or managerial ownership. This study highlights the importance of simultaneously strengthening corporate governance practices and environmental performance to ensure that carbon emission disclosure becomes an integral part of corporate sustainability strategies in addressing global environmental challenges.

institutional ownership, managerial ownership, audit committee, carbon disclosure, environmental performance

Climate change is increasingly recognized as a pressing global issue, marked by a significant rise in global temperatures over recent decades. As reported by the National Oceanic and Atmospheric Administration (NOAA), the period from 2020 to 2024 has been recorded as the hottest years since temperature measurements began in the late 1800s (CGD, 2022). This phenomenon is primarily driven by Rising levels of greenhouse gases, especially carbon dioxide (CO₂), resulting from industrial activities, fossil fuel combustion, and widespread deforestation. According to the IPCC, the Earth's average surface temperature has risen by 0.74℃, with a possible variation of ± 0.18℃ and this is projected to continue, potentially exceeding 1.5℃ without significant intervention.

Industrial activities are among the main drivers of carbon dioxide emissions. In Indonesia, the industrial, power generation, and transportation sectors are the main sources of carbon emissions. According to the World Resources Institute (WRI), Indonesia ranked sixth among the world’s largest carbon emitters in 2020 [1]. The country's industrial growth reached 4.07% in 2022, which also contributed to the rise in carbon emissions [2]. Moreover, industrial expansion has led to permanent land-use changes, with more than 350,000 hectares converted annually, significantly increasing CO₂ emissions [3].

As a reaction to the effects of climate change, the international community has formulated various global agreements intended to lower greenhouse gas emissions [4]. Among these are the United Nations Framework Convention on Climate Change (UNFCCC) and the Kyoto Protocol. The Kyoto Protocol established binding commitments for industrialized countries to reduce their greenhouse gas emissions by 5.2% compared to 2000 levels. It also introduced three market-based mechanisms to facilitate emission reductions: Kyoto Protocol mechanisms such as Joint Implementation (JI), the Clean Development Mechanism (CDM), and International Emissions Trading (IET). Indonesia ratified the Kyoto Protocol in 2004 and reinforced its national commitment to emission control by issuing Presidential Regulations No. 61 and No. 71 of 2011 [5].

As a follow-up, the Indonesian government, through the Ministry of Environment and Forestry, launched the Corporate Performance Rating Program (PROPER), which evaluates and awards companies based on their environmental performance [6]. PROPER ratings, such as gold, green, blue, red, and black, are granted to encourage companies to adopt environmentally friendly business practices [7]. Companies that receive green or gold ratings are considered to have demonstrated high commitment to social and environmental responsibility, contributing to carbon emission control efforts [8].

The inclusion of carbon emission information in firms’ annual and sustainability reports is a form of transparency and accountability by companies in fulfilling their social and environmental responsibilities [9, 10]. However, in Indonesia, such disclosure remains voluntary, as outlined in PSAK No. 1 (revised 2024). As a result, not all companies with significant environmental impacts engage in this disclosure [11].

Although the relationship between corporate governance and carbon emission disclosure has been widely studied [12, 13], limited research has specifically investigated this issue in the context of Indonesia's mining sector, particularly by incorporating environmental performance (as proxied by PROPER) as a moderating variable. This study seeks to address this gap by providing empirical evidence from an emerging economy with unique institutional and regulatory settings, where carbon disclosure remains voluntary and environmental performance is formally evaluated through a government-issued rating system (PROPER). The originality of this research lies in its integrated approach to examining how corporate governance mechanisms, namely institutional ownership, managerial ownership, and audit committees influence carbon emission disclosure, while simultaneously exploring the moderating role of a nationally recognized environmental performance index.

This study investigates the extent to which corporate governance characteristics affect carbon emission disclosure, considering environmental performance as a moderating variable. Environmental performance is proxied by the PROPER rating assigned to the firm. A higher PROPER rating indicates superior environmental practices and is expected to reinforce the relationship between corporate governance and the level of carbon emission disclosure [14].

Good corporate governance encompasses several key elements, such as institutional ownership, managerial ownership, and the presence of an audit committee [15]. Institutional ownership, reflecting the involvement of financial institutions and institutional investors, serves as a monitoring mechanism for managerial actions, including those related to the disclosure of social and environmental responsibilities [16, 17]. Managerial ownership, the proportion of shares held by management, influences strategic decision making, including decisions related to environmental policies [18]. Meanwhile, the audit committee functions as an independent overseer, supporting the board of commissioners in ensuring that both financial and non-financial reporting is accurate and in line with transparency principles [19].

Previous studies have shown that companies with good corporate governance tend to be more responsible in environmental aspects. Strong institutional ownership can encourage management to disclose carbon emission information more comprehensively as a form of accountability to investors. Similarly, high managerial ownership can strengthen management’s involvement in environmental risk management. An active audit committee can enhance oversight of the reporting process, including the disclosure of carbon emissions in sustainability reports [20, 21].

Furthermore, Indonesia's involvement in the Paris Agreement, which was adopted on December 12, 2015, reinforces the global commitment to limit the rise in global temperatures to below 2℃, and ideally to below 1.5℃. Within this framework, Indonesia aims to reduce emissions by 26% independently and up to 41% with international support through the National Action Plan for Greenhouse Gas Emission Reduction (RAN-GRK). To achieve this target, active participation from companies in controlling greenhouse gas emissions is crucial [22].

As a tangible example of implementation, PT Bumi Resources Tbk received the PROPER green rating for three consecutive years, from 2021 to 2023, from the Ministry of Environment and Forestry. This award indicates that the company has implemented an environmental management system in accordance with international standards and has transparently disclosed its environmental performance to the public and stakeholders [6].

Given the urgency of climate change and the critical role of businesses in controlling carbon emissions, this study is highly relevant in advancing the literature on environmental accounting and corporate governance. In particular, the research focuses on examining how institutional ownership, managerial ownership, and audit committees influence carbon emission disclosure, with environmental performance measured through the government mandated PROPER rating serving as a moderating variable. While prior studies have explored the relationship between corporate governance and carbon disclosure, few have explicitly integrated internal governance mechanisms with external regulatory assessments such as PROPER, especially in the context of the Indonesian mining sector. Addressing this gap, the present study offers new insights into how corporate governance structures interact with government evaluations to shape firms’ carbon disclosure behavior. Therefore, this research is positioned to contribute not only to the academic discourse in emerging market contexts, but also to policy formulation aimed at enhancing environmental transparency and encouraging sustainable corporate governance practices in ecologically impactful industries. The findings are expected to provide empirical evidence that informs the development of more effective environmental reporting policies and strengthens companies’ commitment to environmental accountability.

2.1 Legitimacy theory

Legitimacy theory explains how companies strive to align with the values, norms, and social expectations prevailing in the environments where they operate. In this context, a company's existence is seen as part of the social contract between business entities and society [23]. This social contract grants companies the right to access resources such as labor and raw materials, with the condition that they conduct their operations in a lawful and socially acceptable manner [24].

This theoretical perspective emphasizes that firms are responsible for addressing environmental issues and supporting the communities in which they operate [25]. Therefore, companies voluntarily disclose social and environmental information, including carbon emissions data, in order to build a positive perception and maintain legitimacy in the eyes of the public [26, 27].

Proposed four main strategies that companies can adopt in response to threats to their legitimacy [23]:

These strategies are crucial in building a positive perception and maintaining the sustainability of the company’s legitimacy. One concrete form of these strategies is through voluntary environmental disclosure, including carbon emission disclosure [28].

The application of legitimacy theory aligns with the PROPER policy implemented by the government. Companies that actively report their environmental performance in sustainability reports, including carbon emissions, tend to receive higher PROPER ratings [29]. This rating not only reflects the company’s environmental performance but also strengthens its positive image in the eyes of the public [30].

If a company successfully gains appreciation from the public and environmental awards such as PROPER, internal stakeholders, such as institutional shareholders, management, and the audit committee, will be encouraged to continuously press the company to maintain its environmental performance and continue disclosing information related to carbon emissions [4]. Thus, the company’s legitimacy can be maintained, ensuring the sustainability of its operations in the long term.

2.2 Corporate governance

2.2.1 Institutional ownership

Institutional ownership refers to the ownership of company shares by institutions or financial entities such as insurance companies, banks, and investment firms [31]. From the stakeholder theory perspective, the presence of stakeholders is significantly related to the sustainability of the company. This relationship encourages management to be more transparent in its activities [32].

Institutional ownership plays a crucial role as a monitoring mechanism for management. Institutional shareholders have an interest in the long-term performance of the company, thus they are likely to push the company to be socially and environmentally responsible [27, 33]. In this context, pressure from institutional owners can encourage companies to disclose carbon emissions more transparently as part of their corporate social responsibility [34, 35].

In this study, institutional ownership is measured as the percentage of total shares owned by institutional investors relative to the total outstanding shares of the company [32]. A higher proportion reflects greater institutional oversight, which is expected to lead to more comprehensive disclosure of carbon emissions.

Therefore, the larger the proportion of institutional ownership, the stronger the pressure on management to voluntarily and accountably disclose environmental information, including carbon emissions.

2.2.2 Audit committee

The presence of an audit committee within a company's structure is a manifestation of the implementation of Good Corporate Governance (GCG) principles, particularly the principle of transparency [36]. The audit committee encourages the company to be open about all operational activities and to report them systematically through reports accessible to stakeholders [37].

As a supervisory body, the audit committee's role is to oversee the reporting process and ensure that the disclosed information, including environmental information such as carbon emissions [38], is presented accurately and with high quality. Through this supervisory role, the audit committee helps reduce agency costs and improve the quality of disclosures made by the company [39].

In this study, audit committee quality is operationalized using multiple indicators: the number of committee meetings held annually, the proportion of independent members on the committee, and the financial and environmental expertise of its members [38]. These dimensions reflect not only the formality but also the effectiveness of the audit committee in ensuring environmental transparency.

2.2.3 Environmental performance

Environmental performance reflects a company’s commitment to environmental preservation and the mitigation of adverse impacts resulting from its operational activities. This performance is described by Nawrocka and Parker [40] and Chelly et al. [41] describe this performance as encompassing efforts to create a green and sustainable environment, while Sra et al. [42] emphasize the importance of voluntary environmental disclosures to stakeholders.

In line with these expectations, companies are increasingly urged to assume social and environmental responsibility, particularly through the disclosure of environmental information in their annual reports [43].

In the Indonesian context, such responsibility is mandated under Law No. 40 of 2007, Article 74, concerning Social and Environmental Responsibility. In this study, environmental performance is measured using the PROPER rating issued by the Ministry of Environment and Forestry. The rating system consists of five categories gold, green, blue, red, and black each representing a different level of environmental compliance and initiative [6]. Companies with gold and green ratings are considered to have superior environmental performance, whereas red and black indicate poor compliance.

Furthermore, corporate environmental performance in Indonesia is assessed through the PROPER program, an initiative by the Ministry of Environment and Forestry, which serves as a comprehensive evaluation tool for environmental management practices [6, 44].

2.3 Previous research

Several previous studies have examined the relationship between corporate governance mechanisms and carbon emissions disclosure. The research by Kurnia et al. [22] indicates that institutional ownership and managerial ownership have a positive influence on carbon emissions disclosure. Companies with high institutional ownership tend to closely monitor management, encouraging the company to be more transparent in disclosing environmental information. Similarly, high managerial ownership can motivate managers to align their personal interests with stakeholder interests through better carbon emissions disclosure [45].

In addition, the role of the audit committee has also been studied as one of the governance mechanisms influencing environmental disclosure. The presence of an audit committee can enhance the quality of carbon emissions disclosure through more effective monitoring of the company’s activities [22].

However, other studies present varied results. Research by Lee [46] shows that managerial ownership does not always have a significant effect on carbon emissions disclosure due to the low proportion of shares held by management in some companies. On the other hand, Qi et al. [47] assert that the company’s environmental performance, measured through PROPER, is positively correlated with carbon emissions disclosure. This suggests that companies showing a high commitment to environmental management are more likely to be open in disclosing their carbon emissions [12].

Although several studies have examined the relationship between corporate governance mechanisms and carbon emissions disclosure, research integrating environmental performance, carbon disclosure, and governance mechanisms simultaneously remains limited. Therefore, this study aims to fill this gap by examining the effect of institutional ownership, managerial ownership, and the audit committee on carbon emissions disclosure, while considering the role of the company’s environmental performance.

2.4 Hypotheses

A hypothesis is a preliminary proposition derived from theoretical assumptions to address the research problem [48]. The theoretical framework supporting this study is illustrated in Figure 1.

Figure 1. Conceptual framework

2.4.1 Development of hypothesis

Institutional ownership refers to the ownership of company shares by institutions such as banks, insurance companies, and investment firms [22]. This type of ownership plays a role in overseeing management's performance and decisions, as well as encouraging companies to act transparently regarding social and environmental activities. Based on stakeholder theory, pressure from institutional shareholders encourages companies to disclose environmental information, including carbon emissions, in order to maintain public trust and enhance the company's image [48]. Furthermore, research by Ratmono et al. [49] found that the larger the institutional ownership, the higher the level of oversight, which encourages the open disclosure of carbon emissions. Based on this, the proposed hypothesis is:

H1: High institutional ownership positively influences carbon emission disclosure.

Managerial ownership refers to the situation where managers own shares in the company, which encourages them to improve the company's performance by disclosing environmental information, including carbon emissions [22]. As both owners and managers, executives have control over the company's policies and investment direction [49]. Therefore, managerial ownership can align the interests of management with those of stakeholders, while also strengthening commitment to corporate social responsibility [50]. The greater the proportion of shares owned by managers, the greater their influence in driving the disclosure of carbon emissions as part of the company's responsibility [51]. Based on this, the proposed hypothesis is:

H2: Managerial ownership positively influences carbon emission disclosure.

The establishment of an audit committee indicates adherence to GCG practices, particularly the principle of transparency, which encourages openness regarding all company activities, including environmental information disclosure [49]. The audit committee acts as a supervisor and controller of management, particularly in ensuring that carbon emission disclosures are optimally carried out [52].

The frequency of audit committee meetings reflects the quality of oversight. The more frequent the meetings, the greater the likelihood of decision-making that prioritizes stakeholder interests, including the push for carbon emission disclosure [53]. An active and quality audit committee understands the importance of environmental information for stakeholders and encourages the company to gain social legitimacy through carbon emission disclosure [54]. Based on this, the proposed hypothesis is:

H3: The audit committee positively influences carbon emission disclosure.

According to the Ministry of Environment and Forestry of the Republic of Indonesia, companies with the highest PROPER ratings demonstrate good environmental performance [55]. Achieving a high PROPER rating encourages companies to be more proactive in disclosing environmental information, including carbon emissions. On the other hand, high institutional ownership allows institutions to oversee and pressure management to act in accordance with sustainability principles [39].

Companies with high environmental performance, as reflected in their PROPER scores, exhibit a stronger relationship between institutional ownership and carbon emission disclosure [32]. This suggests that environmental performance can strengthen the influence of institutional ownership on the disclosure practices. Based on this explanation, the proposed hypothesis is:

H4: Institutional ownership affects carbon emission disclosure moderated by environmental performance.

PROPER serves as a benchmark for the public in assessing a company's compliance with its surrounding environment [56]. Companies that achieve the highest PROPER ratings tend to gain public legitimacy as they are perceived to comply with applicable norms and regulations [24].

Management ownership allows managers to participate in strategic decision-making [57], including encouraging the improvement of company performance through the disclosure of environmental performance [58]. High environmental performance, as reflected in the PROPER score, is expected to amplify the role of managerial ownership in encouraging transparent environmental disclosures, with a focus on carbon emissions, to fulfill stakeholder expectations [55]. Therefore, the proposed hypothesis is:

H5: Managerial ownership influences carbon emission disclosure moderated by environmental performance.

The implementation of GCG principles, particularly the principle of transparency, encourages companies to disclose information related to their operational activities, including environmental disclosures [22, 59]. The audit committee plays a role as a supervisor and controller, including in encouraging the disclosure of environmental information [49]. The frequency of audit committee meetings reflects the quality of supervision and the effectiveness of GCG implementation [22]. A company's environmental performance, reflected in the PROPER rating, can strengthen the audit committee's influence on carbon emission disclosure [58]. Audit committees in companies with high PROPER ratings will be more active in overseeing and encouraging the disclosure, enabling the company to gain public legitimacy [23]. Therefore, the proposed hypothesis is:

H6: The audit committee influences carbon emission disclosure moderated by environmental performance.

A hypothesis is a provisional answer provided to a problem based on theory [48]. Figure 1 illustrates the theoretical framework used in this study.

This research uses secondary data obtained from the financial reports of companies listed in Indonesia during the period from 2020 to 2024. The selected criteria focus on the mining sector companies that publish financial or sustainability reports on the official website of Indonesia Stock Exchange (IDX) at www.idx.co.id.

The research is based on a sample of 60 mining companies listed on the Indonesia Stock Exchange (IDX) during the period from 2020 to 2024, with data analyzed using multiple linear regression, moderated regression analysis (MRA), and partial hypothesis testing. The operational variables are categorized into independent, dependent, and moderating types.

The sample selection focuses on firms within the mining sector, which is known as one of the largest contributors to national carbon emissions in Indonesia. These companies were chosen based on their consistent publication of sustainability reports and their participation in the PROPER environmental performance evaluation by the Ministry of Environment and Forestry. This ensures data availability and reliability for analysis. While the sample size consists of 60 firms, these entities represent a substantial proportion of the mining sector’s total carbon footprint, making them reasonably representative of the industry's environmental disclosure practices. Moreover, the mining sector in Indonesia is relatively homogeneous in terms of regulatory exposure, operational characteristics, and environmental risk profiles, which supports the generalization of findings within this specific sectoral context. Nonetheless, caution is advised when extending these conclusions to other sectors with different industry dynamics and emission profiles.

Institutional ownership, as an independent variable, is used to evaluate how institutional shareholding contributes to strengthening supervision over the disclosure of carbon emissions; second, managerial ownership, which measures the evidence of shares owned by company managers to provide benefits, especially to stakeholders, by disclosing carbon emissions; third, the audit committee, which emphasizes the role of the company’s supervisory board in minimizing costs and improving the quality of disclosures made by the company, one of which is the disclosure of carbon emissions. The moderating variable in this study is environmental performance, measured by PROPER, which is divided into five categories and scored as follows: Gold (very good, score 5), Green (good, score 4), Blue (fair, score 3), Red (poor, score 2), Black (very poor, score 1) [6].

In the data analysis, the MRA method is used to test the relationship between the independent variables (institutional ownership, managerial ownership, and the audit committee) and the dependent variable (carbon emissions disclosure), while controlling for potential confounding variables, specifically environmental performance as a moderating factor.

This study seeks to deepen the understanding of how institutional ownership, managerial ownership, and the audit committee influence the disclosure of carbon emissions among mining companies listed on the Indonesia Stock Exchange during the observation period. In addition, it examines the moderating role of environmental performance in the relationship between these corporate governance mechanisms and carbon emission disclosure practices.

In the current context, carbon emission disclosure has emerged as a critical strategy for businesses seeking to respond to growing environmental and climate-related concerns. As public and regulatory expectations continue to rise, firms are increasingly encouraged to strengthen institutional and managerial oversight, including the role of audit committees, to ensure transparent and accountable carbon reporting practices. This study contributes to the existing body of knowledge by highlighting the positive influence of institutional ownership, managerial ownership, and audit committees on the extent of carbon emission disclosure.

Moreover, the application of MRA in this study allows for a more in-depth examination of dynamic changes throughout the observation period. By incorporating environmental performance as a moderating variable, the research offers a more holistic perspective on the role of institutional ownership, managerial ownership, and audit committees in enhancing carbon emission disclosure within the mining sector.

Ultimately, the results of this study are anticipated to offer practical insights for Indonesian companies seeking to adopt carbon emission disclosure practices. The findings may serve as a foundational reference for formulating more effective and sustainable strategies in reporting carbon emissions.

4.1 Equations and descriptive statistics

This study employs financial data derived from the annual reports of 60 companies listed on the Indonesia Stock Exchange (IDX) during the 2020–2024 period. The financial indicators used serve as the foundation for assessing the level of carbon emission disclosure. In addition to financial data, the analysis incorporates information from the companies' sustainability report disclosures. All firms included in the sample consistently published their sustainability reports on an annual basis throughout the observed period. To examine the relationships among the variables, this study applies the MRA method, with the regression model specified as follows:

$\begin{gathered}\mathrm{CED}=\alpha+\beta 1 \mathrm{KepIn}_{\mathrm{it}}+\beta 2 \mathrm{KepMen}_{\mathrm{it}}+\beta 3 \mathrm{KomAud}_{\mathrm{it}}+\beta 4 \mathrm{PROPER}_{\mathrm{it}}+e_1\end{gathered}$

where,

CED = Carbon emission disclosure

KepIns = Institutional ownership

KepMen = Managerial ownership

KomAud = Audit committee

PROPER = Environmental performance

i = Company

t = Year

MRA is an application specifically designed for multiple linear regression that involves a regression equation containing the multiplication of two or more independent variables [48].

The moderating variable (Z), which influences the relationship between the independent variable (X) and the dependent variable (Y), is identified based on the following criteria:

The MRA model used in this study is formulated as follows:

$Y=\beta 0+\beta 1 X 1+\beta 2 X 2+\beta 3 * Z+\beta 4 X 1^* Z+\beta 5 X 2^* Z+e$

where,

Y = Dependent variable

X1 = Independent variable 1

X2 = Independent variable 2

Z = Moderating variable

X1*Z = Interaction variable 1

X2*Z = Interaction variable 2

Therefore, in this study, the MRA equation can be obtained as follows:

$\begin{gathered}C E D=\beta 0+\beta 1 \text { KepIns }+\beta 2 \text { KepMen }+\beta 3 \text { KomAud }+\beta 4 \\ \text { PROPER }+\beta 5 \text { KepIns*PROPER }+\beta 6 \text { KepMen*PROPER }+ \\ \beta 7 \text { KomAud*PROPER }+\mathrm{e}\end{gathered}$

The inclusion of variables such as PROPER in the analysis is very important because this variable serves as the basis for calculation. It is crucial for assessing the level of carbon emissions disclosure, making it a valuable indicator when studying the relationship between carbon emissions disclosure and corporate governance mechanisms.

Moreover, this study also combines financial data with institutional ownership, managerial ownership, and audit committees. This indicates a more comprehensive outlook that transcends conventional financial indicators. Institutional ownership evaluates the extent to which share ownership held by other institutions encourages enhanced oversight of carbon emissions disclosure, while managerial ownership serves as evidence of shares owned by company managers to provide benefits to stakeholders through carbon emissions disclosure. The audit committee emphasizes the role of the company’s supervisory board in minimizing costs and improving the quality of disclosures made by the company, one of which is carbon emissions disclosure. These data are essential for understanding how corporate governance mechanisms and environmental performance can impact carbon emissions disclosure (Table 1).

Table 1. Descriptive statistics

|

N = 60 |

Mean |

Max |

Min |

Std. Dev. |

|

KepIns |

0.403 |

0.970 |

0.000 |

0.369 |

|

KepMen |

0.165 |

0.660 |

0.000 |

0.267 |

|

KomAud |

5.680 |

14.000 |

0.000 |

3.192 |

|

Proper |

1.670 |

4.000 |

0.000 |

1.714 |

|

CED |

0.063 |

0.170 |

0.000 |

0.059 |

Source: Data analysis results, 2025

This study focuses on mining sector companies, as they generally produce mineral resources with relatively stable demand that persists across different phases of the economic cycle.

Regarding multicollinearity, the variance inflation factor (VIF) was examined in the initial regression to ensure that multicollinearity was not at problematic levels. The highest VIF was 1.918. Therefore, multicollinearity is not at problematic levels for interpreting the regression results (Table 2).

Table 2. Results of multicollinearity test

|

Unstandardized Coefficients |

Collinearity Statistics |

||||

|

|

Model |

B |

Std. Error |

Tolerance |

VIF |

|

1 |

(Constant) |

0.027 |

0.014 |

|

|

|

KepIns |

0.009 |

0.023 |

0.522 |

1.915 |

|

|

KepMen |

0.038 |

0.025 |

0.793 |

1.262 |

|

|

KomAud |

0.000 |

0.002 |

0.853 |

1.172 |

|

|

Proper |

0.022 |

0.005 |

0.521 |

1.918 |

|

Source: Data analysis results, 2025

4.2 Regression analysis results

This study employs multiple regression analysis using the MRA model. The testing consists of three stages, namely:

$\begin{gathered}\mathrm{CED}=\alpha 1+\beta 1 \mathrm{KepIns}+\beta 2 \mathrm{KepMen}+\beta 3 \mathrm{KomAud}+e\end{gathered}$ (1)

$\begin{gathered}\mathrm{CED}=\alpha 1+\beta 1 \mathrm{KepIns}+\beta 2 \mathrm{KepMen}+\beta 3 \mathrm{KomAud}+\mathrm{PROPER}+e\end{gathered}$ (2)

$\begin{aligned} & \mathrm{CED}= \alpha 1+\beta 1 \mathrm{KepIns}+\beta 2 \mathrm{KepMen}+\beta 3 \mathrm{KomAud} +\mathrm{PROPER}+\beta 4 \mathrm{KepIns}{ }^* \mathrm{PROPER}+\beta 5 \mathrm{KepMen}{ }^* \mathrm{PROPER}+\beta 5 \mathrm{KomAud} \text { PROPER }+e\end{aligned}$ (3)

The results of the MRA testing based on the three stages are presented in Table 3.

Based on Table 3, the results of the MRA were obtained from three regression equations using a sample of 60 mining companies listed on the Indonesia Stock Exchange. The first equation presents the statistical test results to examine the influence of independent variables, namely institutional ownership, managerial ownership, and the audit committee on the dependent variable, which is carbon emission disclosure. The second equation presents the statistical test results to examine the influence of independent variables, namely institutional ownership, managerial ownership, and the audit committee on the dependent variable, which is carbon emission disclosure, with the addition of the moderating variable, environmental performance. The third equation assesses the effect of independent variables, namely institutional ownership, managerial ownership, and the audit committee, on the dependent variable, carbon emission disclosure, with the moderating variable of environmental performance, followed by the testing of interaction variables: institutional ownership with environmental performance, managerial ownership with environmental performance, and audit committee with environmental performance.

The first equation shows the significance values for institutional ownership at 0.000, managerial ownership at 0.593, and the audit committee at 0.314. The significance value for institutional ownership is smaller than 0.05 (0.000 < 0.05), meaning that institutional ownership has a significant impact on carbon emission disclosure, whereas the significance values for managerial ownership and the audit committee are greater than 0.05 (0.593 > 0.05) and (0.314 > 0.05), indicating that managerial ownership and the audit committee do not have a significant impact on carbon emission disclosure. The correlation in the first equation between each independent variable and the dependent variable is 0.209 or 20.9%. The coefficient of determination can be seen in the adjusted R² value of 0.167 or 16.7%, where carbon emission disclosure is influenced by institutional ownership, managerial ownership, and the audit committee, with the remaining 83.3% being influenced by other variables not explained in this study.

The second equation shows the significance values for the independent variables: institutional ownership at 0.700, managerial ownership at 0.38, audit committee at 0.905, and the moderating variable, environmental performance, at 0.000. Based on these values, the significance values for institutional ownership, managerial ownership, and the audit committee are all greater than 0.05, indicating that these variables do not significantly affect carbon emission disclosure. However, the significance value for the moderating variable, environmental performance, is smaller than 0.05, meaning that environmental performance significantly influences carbon emission disclosure. The correlation in the second equation, examining the relationship between the independent and moderating variables with the dependent variable, is 0.428 or 42.8%, showing an increase in correlation after introducing the moderating variable. The coefficient of determination, as shown in the adjusted R² value of 0.387 or 38.7%, indicates that carbon emission disclosure is influenced by institutional ownership, managerial ownership, the audit committee, and the moderating variable, environmental performance. The remaining 61.3% is influenced by other variables not explained in this study. The coefficient of determination has increased after introducing the moderating variable.

Table 3. Moderated regression analysis (MRA) test results

|

Description |

Equation |

||

|

1 |

2 |

3 |

|

|

Regression |

Y = 0.043 + 0.077 X1 + 0.014 X2 + -0.002 X3 |

Y = 0.027 + 0.009 X1 + -0.38 X2 + 0.000 X3 + 0.022 Z |

Y = 0.042 + 0.082 X1 + -0.022 X2 + -0.006 X3 + 0.008 Z + -0.022 X1*Z + -0.006 X2*Z + 0.004 X3*Z |

|

Coefficient Value |

$\begin{gathered}\beta 1=0.077, \beta 2=0.014, \beta 3=0.002\end{gathered}$ |

$\begin{gathered}\beta 1=0.009, \beta 2=0.38, \beta 3=0.000, \beta 4=0.022\end{gathered}$ |

$\begin{gathered}\beta 1=0.082, \beta 2=-0.022, \beta 3=-0.006, \beta 4=0.008, \beta 5=-0.022, \beta 6=-0.006, \beta 7=0.004\end{gathered}$ |

|

Sig. Value |

$\begin{gathered}\beta 1=0.000, \beta 2=0.593, \beta 3=0.314\end{gathered}$ |

$\begin{gathered}\beta 1=0.700, \beta 2=0.144, \beta 3= 0.905, \beta 4=0.000\end{gathered}$ |

$\begin{gathered}\beta 1=0.065, \beta 2=0.601, \beta 3=0.096, \beta 4=0.492, \beta 5=0.179, \beta 6=0.650, \beta 7=0.028\end{gathered}$ |

|

R2 |

0.209 |

0.428 |

0.493 |

|

Adj R2 |

0.167 |

0.387 |

0.424 |

|

F Statistic |

4.944 |

10.300 |

7.212 |

|

Sig. F |

0.004 |

0.000 |

0.000 |

|

N |

60 |

60 |

60 |

Source: Data analysis results, 2025

In the third equation, the significance values for the independent variables are as follows: institutional ownership at 0.065, managerial ownership at 0.601, audit committee at 0.096, and the moderating variable, environmental performance, at 0.492. This equation adds interaction variables between institutional ownership and environmental performance, managerial ownership and environmental performance, and the audit committee and environmental performance. The significance values for the interaction variables are as follows: the first interaction between institutional ownership and environmental performance at 0.179, the second interaction between managerial ownership and environmental performance at 0.650, and the third interaction between the audit committee and environmental performance at 0.028.

The significance values for the independent variables (institutional ownership, managerial ownership, audit committee) and the moderating variable (environmental performance) are all greater than 0.05, meaning these variables do not significantly affect the dependent variable, carbon emission disclosure. However, the significance values for the interaction variables indicate that the moderating variable, environmental performance, cannot moderate the effect of institutional ownership and managerial ownership on carbon emission disclosure, as the significance values for the first and second interactions are greater than 0.05. On the other hand, for the third interaction, the significance value is smaller than 0.05, meaning that environmental performance can moderate the effect of the audit committee on carbon emission disclosure. The correlation in the third equation increases to 0.493 or 49.3%. The coefficient of determination, as shown in the adjusted R² value of 0.424 or 42.4%, indicates that the dependent variable, carbon emission disclosure, is influenced by the independent variables (institutional ownership, managerial ownership, and the audit committee), the moderating variable (environmental performance), and the interaction variables (institutional ownership and environmental performance, managerial ownership and environmental performance, and the audit committee and environmental performance). The remaining 57.6% is influenced by other variables not explained in this study.

Based on the research findings and explanations above, the moderating variable, environmental performance, can moderate the audit committee variable, or H6 is accepted, meaning that the company’s inclusion in the PROPER program in the company can affect the relationship between the audit committee and carbon emission disclosure. The moderating variable, environmental performance, cannot moderate the institutional ownership variable, or H4 is not accepted, meaning that whether or not a PROPER rating is assigned to the company does not affect the relationship between institutional ownership and carbon emission disclosure. Furthermore, the moderating variable, environmental performance, cannot moderate the managerial ownership variable, or H5 is not accepted, meaning participation in the PROPER evaluation does not affect the relationship between managerial ownership and carbon emission disclosure. Below are the results of the partial tests to assess the ability of each independent variable, presented in Table 4.

Results from Table 4 show that the institutional ownership variable has a significance value of 0.056, which is less than 0.1, indicating that H1 is accepted, meaning institutional ownership has a positive and significant impact on carbon emission disclosure. The managerial ownership variable has a significance value of 0.548, which is greater than 0.1, indicating that H2 is rejected, meaning managerial ownership does not have an impact on carbon emission disclosure. The audit committee variable has a significance value of 0.059, which is less than 0.1, indicating that H3 is accepted, meaning the audit committee has an impact on carbon emission disclosure.

Table 4. Results of the t-test - Coefficientsa

|

Model |

Unstandardized Coefficients |

Standardized Coefficients |

t |

Sig. |

|

|

B |

Std. Error |

Beta |

|||

|

(Constant) |

0.046 |

0.015 |

|

3.015 |

0.004 |

|

KepIns |

0.085 |

0.043 |

0.526 |

1.955 |

0.056 |

|

KepMen |

-0.025 |

0.041 |

-0.112 |

-0.605 |

0.548 |

|

KomAud |

-0.006 |

0.003 |

-0.329 |

-1.928 |

0.059 |

|

Moderasi_X1 |

-0.018 |

0.015 |

-0.393 |

-1.207 |

0.233 |

|

Moderasi_X2 |

-0.005 |

0.014 |

-0.068 |

-0.338 |

0.737 |

|

Moderasi_X3 |

0.005 |

0.001 |

0.790 |

4.497 |

0.000 |

aDependent Variable: CED

Source: Data analysis results, 2025

For the moderating variables, moderator 1 is institutional ownership moderated by environmental performance, which has a significance value of 0.233, indicating that H4 is rejected, meaning the environmental performance moderator does not moderate the relationship between institutional ownership and carbon emission disclosure. Moderator 2, managerial ownership moderated by environmental performance, has a significance value of 0.737, indicating that H5 is rejected, meaning the environmental performance moderator does not moderate the relationship between managerial ownership and carbon emission disclosure.

Lastly, moderator 3, the audit committee moderated by environmental performance, has a significance value of 0.000, which is less than 0.1, indicating that H6 is accepted, meaning the environmental performance moderator can moderate the relationship between the audit committee and carbon emission disclosure.

Global awareness of the threat posed by greenhouse gas (GHG) emissions has been steadily increasing over time, leading to the formation of the Paris Agreement at the 21st Conference of the Parties (COP21) held in Paris in 2015.

The agreement aims to limit the increase in global temperatures to below 2℃ and encourages further efforts to keep it well below 1.5℃ above pre-industrial levels. As a form of commitment, Indonesia ratified the Paris Agreement through Law Number 16 of 2016, which is expected to encourage the business sector to contribute to emission reduction efforts. However, carbon emission disclosure in Indonesia remains voluntary, meaning that companies are not legally obligated to report their emissions to the public.

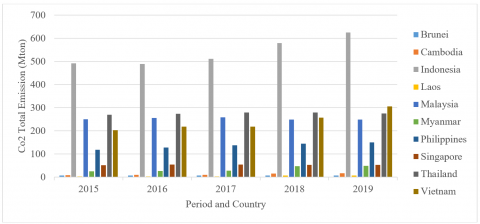

Figure 2 illustrates the trend of CO₂ emissions in Southeast Asian countries from 2015 to 2019. Indonesia consistently shows the highest level of carbon emissions compared to other ASEAN countries, with a steady increase over the five year period. This finding emphasizes Indonesia’s significant contribution to regional emissions and highlights the urgent need for stricter environmental governance and corporate accountability. Vietnam and Thailand also show an upward trend, albeit at a lower level than Indonesia. In contrast, countries like Brunei, Singapore, and Laos contribute relatively little to total regional CO₂ emissions.

Figure 2. Trend report CO2 Southeast Asia (2015-2019)

Source: Joint Research Centre of European Union (processed)

The inclusion of Figure 2 supports the argument that despite Indonesia’s regulatory commitment to the Paris Agreement, actual emissions continue to rise, underscoring the gap between policy and implementation at the corporate level. It reinforces the importance of enhancing not just environmental performance, but also transparent carbon disclosure practices in high emitting countries like Indonesia.

This disclosure can actually reflect the company's responsibility towards its environmental impact; however, since it has not yet had a significant effect on market value, investors tend to focus more on direct environmental management performance rather than technical carbon information. As a result, carbon information is less of a primary consideration in investment decision-making, especially since its disclosure is not yet mandated by regulations.

5.1 Institutional ownership and carbon emission disclosure

The findings of this study reveal that institutional ownership has a significant positive effect on corporate carbon emission disclosure, thereby supporting the acceptance of Hypothesis 1 (H1). This result implies that a higher proportion of institutional ownership is associated with greater levels of carbon emission disclosure by the company.

Companies with high institutional ownership are more likely to disclose information about carbon emissions due to pressure from institutional investors who expect transparency and environmental accountability. Institutional ownership plays a vital role in encouraging companies to act according to sustainability and good governance principles.

According to legitimacy theory, companies need to align their activities with prevailing social norms to maintain their existence in the public eye. In this context, institutional ownership acts as a driving mechanism for companies to disclose carbon emissions to gain legitimacy from society. Furthermore, this result also supports stakeholder theory, where institutional shareholders, as part of the stakeholders, have enough power and interest to influence corporate policies, including environmental transparency.

This finding is consistent with previous studies by Kurnia et al. [22] and Larondelle and Haase [60], which state that institutional ownership affects carbon emission disclosure. However, this result differs from research by Ratmono et al. [49], which concluded that institutional ownership does not influence carbon emission disclosure.

Overall, this finding underscores the active role of institutional owners in enhancing corporate transparency on environmental issues, especially in carbon emission disclosure, in line with increasing public and investor demands for corporate social responsibility and sustainability.

5.2 Managerial ownership and carbon emission disclosure

The results of this study indicate that managerial ownership does not have a statistically significant positive effect on corporate carbon emission disclosure, leading to the rejection of Hypothesis 2 (H2). This finding indicates that an increase in managerial ownership may be associated with a lower level of carbon emission disclosure by the company.

These results imply that the level of managerial ownership, whether high or low, does not affect the company's tendency to disclose carbon emissions. This implies that management, despite being part of the internal stakeholders, has not been able to encourage the company to actively disclose environmental issues.

This result aligns with previous studies which state that managerial ownership does not influence carbon emission disclosure [5, 49, 51]. This finding does not support stakeholder theory, as managerial ownership has not been fully effective in monitoring and guiding the company to report carbon emissions as part of the company’s social and environmental responsibility.

5.3 Audit committee and carbon emission disclosure

The results of this study show that the audit committee has a significant positive impact on carbon emission disclosure, meaning that H3 in this study is accepted.

These results imply that the frequency of audit committee meetings influences the company's decision to disclose carbon emissions. The more frequent the meetings, the greater the likelihood that environmental issues, including carbon emission disclosure, will be discussed and followed up by the company.

This finding is consistent with the results reported by Kurnia et al. [22], which states that the intensity of audit committee meetings can encourage greater carbon emission disclosure. The audit committee, as part of the internal governance mechanism, plays a role in ensuring transparency and accountability, including on environmental issues.

However, this finding does not fully align with legitimacy theory, as the influence of the audit committee reflects more of an internal oversight role rather than an external push from society [61]. Nevertheless, the high frequency of meetings indicates the company’s internal awareness of the importance of carbon emission reporting as a form of environmental concern and social responsibility.

5.4 Institutional ownership and carbon emission disclosure moderated by environmental performance

The findings reveal that environmental performance does not significantly moderate the relationship between institutional ownership and carbon emission disclosure. Consequently, Hypothesis 4 (H4) is not supported.

These results imply that the level of a company’s environmental performance, as measured by the PROPER rating, does not affect the ability of institutional ownership to encourage the company to disclose carbon emissions. This result contradicts the previous finding by Tang et al. [51], which stated that environmental performance strengthens the effect of institutional ownership on carbon emission disclosure.

Furthermore, this result does not align with legitimacy theory and stakeholder theory, which theoretically assume that stakeholders, including institutional owners, play an important role in demanding environmental accountability and transparency from companies [62]. However, in this context, institutional ownership has not demonstrated sufficient capacity to drive companies to improve environmental performance or actively disclose carbon emissions.

This finding may also reflect a low level of environmental awareness or commitment from companies, especially in environmentally sensitive sectors such as mining, where economic interests are often prioritized over environmental responsibilities. Moreover, it indicates a gap in the oversight from institutional investors, who have not effectively used environmental performance indicators as a basis for investment decision making and corporate governance assessment.

5.5 Managerial ownership and carbon emission disclosure moderated by environmental performance

The results of this study indicate that environmental performance does not play a significant moderating role in the relationship between managerial ownership and carbon emission disclosure. Therefore, hypothesis H5 is rejected.

These results imply that the level of a company’s environmental performance, as reflected in the PROPER rating, does not influence the role of managerial ownership in encouraging the company to disclose carbon emissions. In other words, even though the company has a certain environmental performance rating, this is not strong enough to drive management, as both an internal party and shareholder, to enhance environmental transparency through carbon emission disclosure [63].

This result is inconsistent with stakeholder theory, which assumes that internal stakeholders, such as company management, should have the concern and responsibility to ensure the company acts in accordance with societal expectations, including in the disclosure of environmental information [49]. In this context, managerial ownership has not shown an active role as a driving agent in carbon emission reporting, even though information on environmental performance is available.

Overall, this finding highlights a gap between environmental performance information and managerial response in disclosure practices, which may hinder the achievement of greater environmental transparency in the corporate sector.

5.6 Audit committee and carbon emission disclosure moderated by environmental performance

The results of this study indicate that environmental performance plays a significant moderating role in the relationship between the audit committee and carbon emission disclosure. Therefore, hypothesis H6 is accepted.

These results imply that an improvement in the company’s environmental performance, reflected in the PROPER rating, strengthens the influence of the audit committee on carbon emission disclosure. In other words, in companies with good environmental performance, the audit committee is more likely to actively carry out its role, including increasing the frequency of meetings to discuss environmental issues and ensuring the company reports carbon emissions transparently [51].

This finding aligns with legitimacy theory, which states that companies strive to gain support and trust from the public through actions that reflect concern for the environment [26, 64]. In this context, the audit committee plays an essential role in maintaining the company’s legitimacy through intensive oversight of sustainability reporting, particularly carbon emissions. The better the company’s PROPER rating, the more likely the audit committee is to increase oversight intensity and encourage carbon emission disclosure [65].

This study finds that institutional ownership has a significant and positive influence on carbon emission disclosure. This result suggests that institutional investors may exert pressure on companies to be more transparent regarding their environmental impact in order to enhance their public image and gain greater trust from stakeholders. By prioritizing carbon disclosure, firms can showcase their commitment to environmental responsibility, which in turn can enhance their reputation and positioning in the market reputation.

Conversely, the analysis reveals that managerial ownership does not exert a significant partial effect on carbon emission disclosure. One possible explanation is that, as internal stakeholders, managerial shareholders may not have a strong influence on decisions related to environmental transparency. Their role may be more aligned with operational control than with strategic environmental communication, thus limiting their influence over disclosure practices concerning carbon emissions.

The study also demonstrates that environmental performance significantly moderates the relationship between the audit committee and carbon emission disclosure. The presence of a PROPER rating appears to enhance the audit committee's engagement, prompting more frequent discussions and oversight of carbon-related reporting. The PROPER framework likely motivates audit committees to play a more active role in ensuring the firm’s environmental disclosures are accurate, timely, and comprehensive. As a result, companies become more transparent in reporting their carbon emissions, driven by both regulatory performance indicators and internal governance structures.

These findings lend support to legitimacy theory, which posits that organizations are driven to act in ways that gain societal acceptance. Carbon emission disclosure functions as a strategic tool for maintaining corporate legitimacy, particularly in response to increasing environmental scrutiny. In this context, the audit committee serves a vital governance function by overseeing environmental reporting practices, thereby contributing to the company’s public credibility and stakeholder trust.

In a broader theoretical sense, this study enriches the application of legitimacy theory by demonstrating how external regulatory mechanisms (PROPER) interact with internal governance structures to shape corporate disclosure behavior. This intersection highlights the evolving nature of corporate legitimacy, which is no longer determined solely by internal values or voluntary actions but also increasingly by formal environmental assessments mandated by the state. From a policy perspective, the findings imply that government agencies can play a strategic role in encouraging corporate transparency by strengthening environmental performance evaluations like PROPER and making them more integrated with financial and non-financial reporting standards. Regulators might consider moving toward semi-mandatory disclosure frameworks, particularly for high-impact industries such as mining, to ensure consistent and comparable environmental data. For practitioners, especially boards and senior management, the study underscores the importance of fostering institutional ownership structures and empowering audit committees not only as compliance bodies but also as strategic agents for sustainability governance. Enhancing environmental disclosure practices through governance-based mechanisms can serve as a competitive differentiator in markets increasingly sensitive to ESG (Environmental, Social, and Governance) performance.

Despite its contributions, this study has several limitations. The relatively small sample size and the inconsistency in social and environmental reporting across companies present challenges in ensuring data uniformity. Moreover, external influences such as economic shifts following the COVID-19 pandemic may have affected market dynamics and corporate behavior during the study period. Nevertheless, this research contributes to the theoretical advancement of legitimacy theory by incorporating a government mandated environmental assessment (PROPER) as a moderating variable an approach that is still rarely explored in the Indonesian mining context. This allows for a deeper understanding of how external regulatory frameworks interact with internal corporate governance mechanisms in shaping voluntary disclosure behavior.

Therefore, future research is encouraged to broaden the sample by including companies from other sectors and extending the observation period, which may provide stronger grounds for generalizing findings and developing a more unified framework for environmental governance and disclosure in emerging economies.

[1] Sari, D.I. (2022). 10 countries contributing the largest carbon emissions, Indonesia is fifth. https://travel.kompas.com/read/2022/04/03/220800827/10-negara-penyumbang-emisi-karbon-terbesar-indonesia-kelima?page=all.

[2] Indonesia Water Portal. (2021). Environment ministry: 59 percent of Indonesian rivers severely polluted. https://www.indonesiawaterportal.com/news/environme nt-ministry-59-percent-of-indonesian-rivers-severely- polluted.html.

[3] Amelia, A.R. (2025). 11 perusahaan migas dan tambang terkena sanksi pencemaran lingkungan. https://katadata.co.id/arnold/berita/5e9a55526efa2/11-perusahaan-migas-dan-tambang-terkena-sanksi-pencemaran-lingkungan, accessed on May 1, 2025.

[4] Depoers, F., Jeanjean, T., Jérôme, T. (2016). Voluntary disclosure of greenhouse gas emissions: Contrasting the carbon disclosure project and corporate reports. Journal of Business Ethics, 134: 445-461.

[5] He, Y., Tang, Q., Wang, K. (2016). Carbon performance versus financial performance. China Journal of Accounting Studies, 4(4): 357-378. https://doi.org/10.1080/21697213.2016.1251768

[6] Kementrian Lingkungan Hidup dan Kehutanan. (2022). Program penilaian peringkat kinerja perusahaan dalam pengelolaan lingkungan. https://www.menlhk.go.id/site/post/119, accessed on Apr. 23, 2022

[7] Global Sustainability Standard Board. (2016). GRI 305: Emissions 2016. https://www.globalreporting.org/standards/media/1012/gri-305-emissions-2016.pdf, accessed on May 5, 2025.

[8] Klingenberger, L., Shahi, S., Au, C.D., Frere, E., Zureck, A. (2022). Inclusive measurement of public perception of corporate low-carbon ambitions: Analysis of strategic positioning for sustainable development using natural language processing. International Journal of Sustainable Development and Planning, 17(1): 259-265. https://doi.org/10.18280/ijsdp.170126

[9] Elkington, J. (1998). Accounting for the triple bottom line. Measuring Business Excellence, 2(3): 18-22. https://doi.org/10.1108/eb025539

[10] Hahn, R., Reimsbach, D., Schiemann, F. (2015). Organizations, climate change, and transparency: Reviewing the literature on carbon disclosure. Organization and Environment, 28(1): 80-102. https://doi.org/10.1177/1086026615575542

[11] Muhammad, G.I., Aryani, Y.A. (2021). The impact of carbon disclosure on firm value with foreign ownership as a moderating variable. Jurnal Dinamika Akuntansi Dan Bisnis, 8(1): 1-14. https://doi.org/10.24815/JDAB.V8I1.17011

[12] Velte, P., Stawinoga, M., Lueg, R. (2020). Carbon performance and disclosure: A systematic review of governance-related determinants and financial consequences. Journal of Cleaner Production, 254: 120063. https://doi.org/10.1016/J.JCLEPRO.2020.120063

[13] Giannarakis, G., Konteos, G., Sariannidis, N., Chaitidis, G. (2017). The relation between voluntary carbon disclosure and environmental performance: The case of S&P 500. International Journal of Law and Management, 59(6): 784-803. https://doi.org/10.1108/IJLMA-05-2016-0049

[14] Ganda, F. (2018). The effect of carbon performance on corporate financial performance in a growing economy. Social Responsibility Journal, 14(4): 895-916. https://doi.org/10.1108/SRJ-12-2016-0212.

[15] Marshall, J.D., Toffel, M.W. (2005). Framing the elusive concept of sustainability: A sustainability hierarchy. Environmental Science and Technology, 39(3): 673-682. https://doi.org/10.1021/es040394k

[16] Haque, F., Ntim, C.G. (2020). Executive compensation, sustainable compensation policy, carbon performance and market value. British Journal of Management, 31(3): 525-546. https://doi.org/10.1111/1467-8551.12395

[17] Lewandowski, S. (2017). Corporate carbon and financial performance: The role of emission reductions. Business Strategy and the Environment, 26(8): 1196-1211. https://doi.org/10.1002/bse.1978

[18] Wang, L., Li, S., Gao, S. (2014). Do greenhouse gas emissions affect financial performance?- An empirical examination of Australian public firms. Business Strategy and the Environment, 23(8): 505-519. https://doi.org/10.1002/bse.1790

[19] Busch, T., Lewandowski, S. (2018). Corporate carbon and financial performance: A meta-analysis. Journal of Industrial Ecology, 22(4): 745-759. https://doi.org/10.1111/jiec.12591

[20] Ang, B.W., Su, B. (2016). Carbon emission intensity in electricity production: A global analysis. Energy Policy, 94: 56-63. https://doi.org/10.1016/J.ENPOL.2016.03.038

[21] Sekarwigati, M., Effendi, B. (2019). Pengaruh ukuran perusahaan, profitabilitas, dan likuiditas terhadap corporate social responsibility disclosure. STATERA: Jurnal Akuntansi dan Keuangan, 1(1): 16-33. https://doi.org/10.33510/statera.2019.1.1.16-33

[22] Kurnia, P., Darlis, E., Putra, A.A. (2020). Carbon emission disclosure, good corporate governance, financial performance, and firm value. Journal of Asian Finance, Economics and Business, 7(12): 223-231. https://doi.org/10.13106/JAFEB.2020.VOL7.NO12.223

[23] Brown, N., Deegan, C. (1998). The public disclosure of environmental performance information - A dual test of media agenda setting theory and legitimacy theory. Accounting and Business Research, 29(1): 21-41. https://doi.org/10.1080/00014788.1998.9729564

[24] Dowling, J., Pfeffer, J. (1975). Organizational legitimacy: Social values and organizational behavior. The Pacific Sociological Review, 18(1): 122-136. https://doi.org/10.2307/1388226

[25] Schaufele, B. (2021). Curvature and competitiveness: Carbon taxes in cattle markets. American Journal of Agricultural Economics, 104(4): 1268-1292. https://doi.org/10.1111/ajae.12272

[26] O’Donovan, G. (2002). Environmental disclosures in the annual report: Extending the applicability and predictive power of legitimacy theory. Accounting, Auditing & Accountability Journal, 15(3): 344-371. https://doi.org/10.1108/09513570210435870

[27] Effendi, B. (2021). The effect of environmental accounting on the increase in firm value. Conference Series, 3(1): 125-136.

[28] Chen, Y., Feng, J. (2019). Do corporate green investments improve environmental performance? Evidence from the perspective of efficiency. China Journal of Accounting Studies, 7(1): 62-92. https://doi.org/10.1080/21697213.2019.1625578

[29] Chiou, T.Y., Chan, H.K., Lettice, F., Chung, S.H. (2011). The influence of greening the suppliers and green innovation on environmental performance and competitive advantage in Taiwan. Transportation Research Part E: Logistics and Transportation Review, 47(6): 822-836. https://doi.org/10.1016/j.tre.2011.05.016

[30] Clarkson, P.M., Fang, X., Li, Y., Richardson, G. (2013). The relevance of environmental disclosures: Are such disclosures incrementally informative? Journal of Accounting and Public Policy, 32(5): 410-431. https://doi.org/10.1016/j.jaccpubpol.2013.06.008

[31] Li, J., Ji, S. (2020). Empirical analysis on the relationship between institutional pressure, environmental strategy and corporate environmental performance. International Journal of Sustainable Development and Planning, 15(2): 173-184. https://doi.org/10.18280/ijsdp.150207

[32] Houten, E.S., Wedari, L.K. (2023). Carbon disclosure, carbon performance, and market value: Evidence from Indonesia polluting industries. International Journal of Sustainable Development and Planning, 18(6): 1973-1981. https://doi.org/10.18280/ijsdp.180634

[33] Chang, K. (2015). The impacts of environmental performance and propensity disclosure on financial performance: Empirical evidence from unbalanced panel data of heavy-pollution industries in China. Journal of Industrial Engineering and Management, 8(1): 21-36. https://doi.org/10.3926/jiem.1240

[34] Rusmana, O., Purnaman, S.M.N. (2020). Pengaruh pengungkapan emisi karbon dan kinerja lingkungan terhadap nilai perusahaan. Jurnal Ekonomi, Bisnis Dan Akuntansi (JEBA), 22(1): 42-52.

[35] Effendi, B. (2024). Influence of green accounting, sales growth, and firm size on capital structure. Owner: Riset Dan Jurnal Akuntansi, 8(2): 1896-1903. https://doi.org/10.33395/owner.v8i2.2301

[36] Jiang, Y., Luo, L., Xu, J.F., Shao, X.R. (2021). The value relevance of corporate voluntary carbon disclosure: Evidence from the United States and BRIC countries. Journal of Contemporary Accounting and Economics, 17(3): 100279. https://doi.org/10.1016/j.jcae.2021.100279

[37] Sullivan, R., Gouldson, A. (2012). Does voluntary carbon reporting meet investors’ needs? Journal of Cleaner Production, 36: 60-67. https://doi.org/10.1016/J.JCLEPRO.2012.02.020

[38] Alsaifi, K., Elnahass, M., Salama, A. (2020). Market responses to firms’ voluntary carbon disclosure: Empirical evidence from the United Kingdom. Journal of Cleaner Production, 262: 121377. https://doi.org/10.1016/j.jclepro.2020.121377

[39] Giannarakis, G., Zafeiriou, E., Sariannidis, N. (2017). The impact of carbon performance on climate change disclosure. Business Strategy and the Environment, 26: 1078-1094. https://doi.org/10.1002/bse.1962

[40] Nawrocka, D., Parker, T. (2009). Finding the connection: Environmental management systems and environmental performance. Journal of Cleaner Production, 17(6): 601-607. https://doi.org/10.1016/j.jclepro.2008.10.003

[41] Chelly, A., Nouira, I., Hadj-Alouane, A.B., Frein, Y. (2021). A comparative study of progressive carbon taxation strategies: Impact on firms’ economic and environmental performances. International Journal of Production Research, 60(11): 3476-3500. https://doi.org/10.1080/00207543.2021.1924410

[42] Sra, J.K., Booth, A.L., Cox, R.A.K. (2022). Voluntary carbon information disclosures, corporate-level environmental sustainability efforts, and market value. Green Finance, 4(2): 179-206. https://doi.org/10.3934/gf.2022009

[43] Alfani, G.A., Diyanty, V. (2020). Determinants of carbon emission disclosure. Journal of Economics, Business, & Accountancy Ventura, 22(3): 333-346. https://doi.org/10.14414/jebav.v22i3.1207

[44] Hardiyansah, M., Agustini, A.T., Purnamawati, I. (2021). The effect of carbon emission disclosure on firm value: Environmental performance and industrial type. Journal of Asian Finance, Economics and Business, 8(1): 123- 133. https://doi.org/10.13106/jafeb.2021.vol8.no1.123

[45] Matsumura, E.M., Prakash, R., Vera-Muñoz, S.C. (2014). Firm-value effects of carbon emissions and carbon disclosures. Accounting Review, 89(2): 695-724. https://doi.org/10.2308/accr-50629

[46] Lee, S.Y. (2012). Corporate carbon strategies in responding to climate change. Business Strategy and the Environment, 21(1): 33-48. https://doi.org/10.1002/BSE.711

[47] Qi, G., Zeng, S., Li, X., Tam, C. (2012). Role of internalization process in defining the relationship between ISO 14001 certification and corporate environmental performance. Corporate Social Responsibility and Environmental Management, 19(3): 129-140. https://doi.org/10.1002/csr.258

[48] Harahap, S. (2011). Accounting Theory, 3rd ed. Universitas Diponegoro University.

[49] Ratmono, D., Darsono, D., Selviana, S. (2021). Effect of carbon performance, company characteristics and environmental performance on carbon emission disclosure: Evidence from Indonesia. International Journal of Energy Economics and Policy, 11(1): 101-109. https://doi.org/10.32479/ijeep.10456

[50] Chen, Z., Zhang, X., Chen, F. (2021). Do carbon emission trading schemes stimulate green innovation in enterprises? Evidence from China. Technological Forecasting and Social Change, 168: 120744. https://doi.org/10.1016/J.TECHFORE.2021.120744

[51] Tang, M., Cheng, S., Guo, W., Ma, W., Hu, F. (2022). Effects of carbon emission trading on companies’ market value: Evidence from listed companies in China. Atmosphere, 13(2): 240. https://doi.org/10.3390/atmos13020240

[52] Girerd-Potin, I., Jimenez-Garcès, S., Louvet, P. (2013). Which dimensions of social responsibility concern financial investors? Journal of Business Ethics, 121: 559-576. https://doi.org/10.1007/S10551-013-1731-1

[53] Choi, B., Luo, L., Shrestha, P. (2021). The value relevance of carbon emissions information from Australian-listed companies. Australian Journal of Management, 46(1): 3-23. https://doi.org/10.1177/0312896220918642

[54] Dong, F., Yu, B., Hadachin, T., Dai, Y., Wang, Y., Zhang, S., Long, R. (2018). Drivers of carbon emission intensity change in China. Resources, Conservation and Recycling, 129: 187-201. https://doi.org/10.1016/J.RESCONREC.2017.10.035

[55] Wedari, L.K., Alfian, H. (2024). Does green innovation impact on profitability of Indonesian consumer non-cyclicals companies? International Journal of Sustainable Development and Planning, 19(7): 2805-2812. https://doi.org/10.18280/ijsdp.190738

[56] Kumarasiri, J., Jubb, C. (2016). Carbon emission risks and management accounting: Australian evidence. Accounting Research Journal, 29(2): 137-153. https://doi.org/10.1108/arj-03-2015-0040

[57] Shen, Y., Su, Z.W., Huang, G., Khalid, F., Farooq, M.B., Akram, R. (2020). Firm market value relevance of carbon reduction targets, external carbon assurance and carbon communication. Carbon Management, 11(6): 549-563. https://doi.org/10.1080/17583004.2020.1833370

[58] Yadav, P.L., Han, S.H., Rho, J.J. (2016). Impact of environmental performance on firm value for sustainable investment: Evidence from large US firms. Business Strategy and the Environment, 25(6): 402-420. https://doi.org/10.1002/BSE.1883

[59] Darnall, N., Henriques, I., Sadorsky, P. (2008). Do environmental management systems improve business performance in an international setting? Journal of International Management, 14(4): 364-376. https://doi.org/10.1016/j.intman.2007.09.006

[60] Larondelle, N., Haase, D. (2012). Valuing post-mining landscapes using an ecosystem services approach - An example from Germany. Ecological Indicators, 18: 567- 574. https://doi.org/10.1016/j.ecolind.2012.01.008

[61] Burke, P., Jotzo, F., Best, R. (2020). Carbon Pricing Works: The Largest-Ever Study Puts It Beyond Doubt. The Conversation.

[62] Li, Y., Eddie, I., Liu, J. (2014). Carbon emissions and the cost of capital: Australian evidence. Review of Accounting and Finance, 13(4): 400-420. https://doi.org/10.1108/raf-08-2012-0074

[63] Zhang, R.L., Liu, X.H., Jiang, W.B. (2023). How does the industrial digitization affect carbon emission efficiency? Empirical measurement evidence from China’s industry. Sustainability, 15(11): 9043. https://doi.org/10.3390/su15119043

[64] Joseph, V.R., Mustaffa, N.K. (2021). Carbon emissions management in construction operations: A systematic review. Engineering, Construction and Architectural Management, 30(3): 1271-1299. https://doi.org/10.1108/ecam-04-2021-0318

[65] Choi, B.B., Lee, D., Psaros, J. (2013). An analysis of Australian company carbon emission disclosures. Pacific Accounting Review, 25(1): 58-79. https://doi.org/10.1108/01140581311318968