Ari Purwanti![]()

© 2025 The author. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The research idea is based on the fundamental need to analyze the influence of Blockchain adaptation (BA) and Environmental, Social, and Governance (ESG) index rankings on Green Accounting (GRA) through the Carbon Disclosure Project (CDP) as a mediator. The increasing number of start-up companies in Indonesia that have climate change initiatives and adapt blockchain to promote transparency, accountability, and sustainability in the financial sector requires an institution that assesses the disclosure of corporate climate change initiatives. This study is based on primary data collected from 190 respondents from start-up firms who answered questions from various start-up business software development companies located in the West Java and DKI Jakarta regions. Data analysis was carried out using the Partial Least Squares Structural Equation Modeling (PLS-SEM) method, which is operated through the Smart-PLS program. The results of the study show that Ba and ESG index rank have a dominant influence, while CDP climate change (CDPCC) as a moderator has a weak influence on GRA. This research implies that the presence of market responses is more dominant in the company's financial performance, so market players' awareness of the implementation of GRA, especially in start-up businesses, needs to receive regular attention from the IDX and requires more ESG data to be published as a means of education for investors. This study promotes greater corporate transparency and environmental accountability, particularly among start-ups, by demonstrating the importance of ESG practices and blockchain in GRA. The findings encourage regulatory bodies and investors to prioritize sustainability disclosures, fostering a more climate-conscious economy and enhancing public trust in corporate environmental commitments. GRA and the climate change CDP provide recommendations for improving these climate change initiatives and have an impact on reducing climate change.

blockchain technology, ESG, CDP climate change (CDPCC), Green Accounting (GRA), start-up business

Environmental issues and climate change have a wide impact on human life. Carbon dioxide and waste produced from various human activities since the beginning of the Industrial Revolution are closely related to the current conditions. In line with industrial development, problems related to environmental pollution, such as global warming, carbon emissions, and factory waste, have also increased. Global warming and environmental pollution are not only topics that must be discussed in Indonesia, but they must also be discussed internationally because of their enormous influence on the world.

In Indonesia, the practice of disclosing carbon emissions and implementing healthy business practices has generally not been implemented properly. Disclosure is therefore voluntary and rarely carried out by business actors. The Government of the Republic of Indonesia has consistently been active in carrying out social responsibility, as manifested in Law No. 17 of 2004, which recognizes the Kyoto Protocol as an instrument for establishing greenhouse gas (GHG) emission limit policies.

The increasing number of companies that have begun implementing climate change reduction activities in their operations requires company assessments [1]. Assessments are needed to prove whether the activities carried out have been completed. In addition, company assessments of Environmental, Social, and Governance (ESG) aspects, especially climate change, have become a hot topic in recent years. Therefore, investors who will invest their capital require or encourage companies to disclose information about their ESG performance [2, 3]. Sustainability and sustainable development are two processes that are interrelated. Sustainability is a goal to be achieved, while sustainable development is a way to achieve that goal [4]. Both sustainability and sustainable development are closely related to environmental issues and policies regarding environmental management [5]. There is a very urgent goal that needs to be achieved immediately by the whole world, namely SDG number 13, which is related to handling climate change [6]. Company assessments related to climate change reduction generally use ESG rating index platforms such as the Carbon Disclosure Project (CDP), Multianalytes, and others.

CDP is a global environmental disclosure platform whose ratings are used by investors. CDP ratings are utilized by companies, cities, and countries to measure and manage risks and opportunities related to climate change, water, and deforestation. Companies that participate in CDP ratings are required to disclose company data according to the methodology. After the company discloses data, CDP will assess the company's performance concerning climate change, water, and deforestation. The values assigned by CDP range from "A" to "D" and "F." Companies that achieve the "Leadership" category have successfully taken advantage of climate change opportunities, reduced the impact of climate change, and developed a climate change strategy. The "Disclosure" category is obtained when every CDP question is answered. Investors and experts prefer using the ESG rating index due to the quality and usefulness of the rating results. The CDP platform is the second most frequently used ESG rating platform by companies, following Sustainability’s ESG rating. ESG rating assessment is crucial for increasing stakeholder trust, particularly among investors, in the company's performance regarding climate change actions. Additionally, with the ESG index value, stakeholders related to the company can make more informed decisions regarding the company's climate risks that may impact finances. These stakeholders include banks, investors, governments, media, customers, and suppliers. Furthermore, to support the government in the Paris Agreement, the ESG index rating will evaluate the responsibility that the company has taken in reducing the negative impacts of climate change.

The abundance of start-ups in Indonesia presents both opportunities and risks. The life cycle of a start-up firm depends on large amounts of finance and high-quality human resources [7]. Software development is critical for assisting other businesses in a variety of sectors. Employees in start-up software development must have expertise and current knowledge to meet consumer wants and provide solutions to dynamic difficulties for each client. Indonesia's recent economic development appears to have been driven by the country's vibrant start-up culture and rapidly rising internet economy in recent years. In 2023, the country's start-up ecosystem was rated second in Southeast Asia. Indonesia has proven to be one of the region's start-up pioneers, having the largest market in Southeast Asia and ranking second only to Singapore in terms of unicorns. The expansion of start-ups and venture capital investment is inextricably connected. Over the last five years, the value of venture capital financing in Indonesia has nearly doubled. This was the country's largest number of venture capital agreements in 2022, spanning 340 investments. The growing number of larger investment transactions indicates the expansion of investments in Indonesian start-ups. More than 200 Indonesian businesses raised at least a million dollars in investment by the start of 2022. Furthermore, Indonesia's foreign direct investments (FDIs) have increased dramatically, rising from 3.92 billion US dollars in 2016 to 22 billion US dollars in 2022. Indonesia has a very dynamic and rapidly growing start-up ecosystem. As of January 2024, there were 2,647 start-ups registered in Indonesia, making it the sixth-largest country in the world in terms of the number of start-ups. Start-ups in Indonesia contribute significantly to the growth of the digital economy, accounting for around 4.6% of Indonesia's GDP. Start-up companies in the West Java and DKI Jakarta regions will be the units of analysis in this study. This assessment will serve as the basis for decision-making by stakeholders. Therefore, the results of this report can provide a major practical contribution to companies that will conduct ESG index evaluations using CDP. In addition, the results of the study are also useful for increasing understanding of the literature, especially in improving future research using the latest ESG performance measurements. Specifically, the results of the study will help energy companies understand the steps and strategies needed to respond to climate change action. More broadly, the results of the study provide a new perspective on using performance measurements through secondary data, including ESG disclosures that are part of sustainability performance.

Blockchain technology can be implemented in Green Accounting (GRA) to improve transparency, accountability, and efficiency in environmental reporting. Here are some ways blockchain can be used in GRA: 1) Emissions Measurement and Reporting: Blockchain can be used to record and verify carbon emissions data in real time. Every emissions transaction can be recorded in a secure, immutable block, ensuring data accuracy; 2) Verification and Audit: Using blockchain, auditors can automatically verify emissions data and environmental reporting, reducing audit time and costs; 3) Smart Contracts: Blockchain can be used to regulate and monitor a company’s environmental commitments, such as reducing emissions or using renewable energy; 4) Transparency and Accountability: Blockchain provides high transparency in the environmental reporting process, allowing all parties involved to see data in real time and ensuring that the company complies with environmental standards; 5) Reducing Greenwashing: With a trusted record of transactions, blockchain can help reduce greenwashing (false claims about sustainability) by providing tangible evidence of a company’s environmental performance. Blockchain implementation in GRA has great potential to improve reliability and efficiency in environmental reporting.

This research is critical in bridging the gap between start-ups' inventive spirit and the requirement for environmental accountability through a GRA method. In Indonesia's increasingly digital and competitive business ecosystem, start-ups have a significant opportunity to implement cutting-edge technologies such as blockchain to strengthen ESG practices transparently and in real time. However, many of them lack an accounting framework that can incorporate environmental responsibility into their business strategies. This is where our research's contribution comes in: by creating a blockchain-based ESG reporting and measurement mechanism, it encourages start-ups to focus not only on development and scalability but also on accepting responsibility for their environmental and social implications.

Let’s first examine the terms GRA and Climate Change Accounting. There are two branches of accounting that both focus on environmental impact, but with slightly different focuses.

Green Accounting:

1) Scope: Incorporates environmental impact into a company’s financial statements. It includes measuring and reporting carbon emissions, natural resource use, waste management, and environmental conservation initiatives.

2) Purpose: Encourages companies to be more environmentally responsible by showing the costs and benefits of environmentally friendly practices.

3) Key Activities: Sustainability reporting, recording costs and savings from green initiatives, and managing and reporting on the sustainable use of materials and energy.

Climate Change Accounting:

1) Scope: Specific to the impacts and risks a company faces related to climate change, and how the company adapts to and mitigates those impacts.

2) Purpose: Identify, measure, and manage risks related to climate change, and report on mitigation steps taken.

3) Main Activities: Climate risk reporting, greenhouse gas emissions management, assessment of the impact of climate change on a company’s operations and finances, and climate mitigation and adaptation strategies.

Key Differences:

1) Main Focus: GRA is broader in scope, covering all aspects of the environment, while climate change accounting specifically focuses on issues related to climate change.

2) Reporting: GRA typically produces an overall sustainability report, while climate change accounting produces more specific reports related to climate change risks and mitigation. Thus, GRA can be considered a broader umbrella that includes climate change accounting as one of its components.

Legitimacy theory states that every corporate activity must be consistent with social norms, values, and provisions, and must be appropriately accepted by all internal and external stakeholders [8, 9]. A previous study has shown that firms gain legitimacy by implementing initiatives that incorporate environmental and social considerations [10]. According to stakeholder theory, a firm acts to serve all stakeholders rather than just its own interests. Freeman defined stakeholders and highlighted how businesses behave in terms of social performance [11, 12].

CDP climate change (CDPCC) is a methodology used to measure the impact of climate change on corporate performance and to identify business risks and opportunities related to climate change. The methodology was developed by the UK-based non-profit organization CDP in 2000. Through this report, CDPCC facilitates interactions between companies, investors, policymakers, and the public in a more transparent and measurable way. The CDPCC methodology is currently one of the leading frameworks for measuring and reporting the impact of climate change on companies, and many large companies have used this methodology to report their performance on climate change. By using this methodology, companies can obtain accurate and relevant information about the impact of climate change on their operations, as has been done by startup companies in Indonesia.

Blockchain, well known for its role in cryptocurrencies, offers several potential possibilities that might have a huge influence on the energy sector. A distributed, decentralized ledger system called blockchain encourages transparency, safety, and effectiveness in data handling and transactions. Blockchain has the potential to revolutionize the stock exchange industry's distribution, accounting, and trading practices. Blockchain's potential to support a more decentralized and democratic stock market is what makes it promising for the stock exchange industry. This might lead to the creation of a peer-to-peer stock trading platform in which customers can buy, sell, or swap directly with one another, bypassing the established markets. A platform like this might not only improve the efficiency of stock trading, but it could also enable consumers to participate more actively in the trading market. Furthermore, the inherent transparency and immutability of blockchain make it a great tool for stock tracking. This can result in more precise and trustworthy data on energy consumption and generation, which is critical for managing stock resources and minimizing stock footprints. Security problems and high administrative expenses of centralized systems led to the development of blockchain, a distributed system. In a decentralized network, users log and manage transactions. Data is preserved in blocks on P2P-based distributed open-ledger blockchains, which are connected and kept in chain form via hash values. Blocks are divided into headers and block contents. Block headers provide information on the previous block's hash value, mining difficulty, block creation time, version, and Merkle root. They are connected to each other.

Mediation analysis is commonly conducted using regression analysis, and there are several statistical methods and models that can be used to test the mediation effect, such as Baron and Kenny's method, the Sobel test, bootstrapping, and causal mediation analysis [13]. It involves a series of regression analyses to examine the relationships between the predictor variable, mediator variable, and outcome variable. Moderation variables as mediators are typically introduced when there is an unexpectedly weak or inconsistent relationship between a predictor and a criterion variable [4]. Recommended mediation is tested across three regression models as follows:

This research, suitable for conditions of mediation, is tested by model 3; the mediator needs to significantly forecast the dependent variables. Overall, mediation statistics are a powerful tool for investigating the complex relationships between variables and providing insights into the underlying mechanisms driving those relationships.

2.1 Environmental, Social, and Corporate Governance (ESG) and CDP climate change

In recent years, the importance of incorporating Environmental, Social, and Corporate Governance (ESG) factors into corporate plans has grown, especially in the context of global climate change. Companies are increasingly recognizing the need to adopt sustainable practices and report their environmental impacts.

CDPCC is one of the most prominent platforms for environmental disclosure. It provides a comprehensive system for companies to measure, manage, and disclose their environmental impacts. The CDP scores companies based on their climate-related disclosures, which include information on their greenhouse gas emissions, climate risks and opportunities, and strategies for reducing their carbon footprint. High CDP scores indicate that a company is transparent about its environmental impact and is actively working to mitigate its contribution to climate change.

The influence of ESG on CDPCC reporting is profound. Companies that prioritize ESG are more likely to achieve high CDP scores. This is because the criteria for ESG and CDP overlap significantly, particularly in the environmental category. For example, a company that has a robust plan for reducing its carbon emissions and is transparent about its environmental impact will score well on both ESG and CDP metrics.

Furthermore, ESG reporting can enhance a company's reputation and build trust with stakeholders. Transparency about environmental impacts and efforts to address climate change can improve a company's public image and foster goodwill among consumers, employees, and regulators. This can be particularly valuable in industries that are heavily scrutinized for their environmental impact, such as energy, manufacturing, and agriculture.

H1: ESG has a positive and significant influence on CDPCC.

2.2 Environmental, Social, and Corporate Governance and Green Accounting

The integration of ESG considerations into GRA practices has gained significant traction as businesses strive to become more sustainable and responsible. ESG factors play a crucial role in shaping how companies report their environmental impacts, manage resources, and address social and governance issues, ultimately influencing their overall sustainability strategies. GRA provides the tools to quantify these risks and incorporate them into financial decision-making processes. This proactive approach helps companies mitigate potential liabilities and capitalize on opportunities related to sustainability.

The social aspect of ESG also plays a significant role in GRA. Companies are increasingly recognizing the importance of social responsibility, including fair labor practices, community engagement, and human rights. GRA enables businesses to assess and provide data on their social effects, such as workplace safety and health, inclusion and equity, and community development projects. By incorporating social metrics into their accounting systems, companies can better understand and manage their social performance, which is essential for building a positive reputation and maintaining a social license to operate.

Corporate governance, the third pillar of ESG, is equally important in GRA. Effective governance structures and practices are essential for ensuring that sustainability initiatives are implemented and monitored effectively. GRA encourages companies to adopt robust governance frameworks that support environmental and social goals. This includes establishing clear sustainability policies, setting performance targets, and implementing internal controls to monitor progress.

H2: ESG has a positive and significant influence on GRA.

2.3 Blockchain adaptation and CDP climate change

The adaptation of blockchain technology to CDPCC reporting represents a significant advancement in environmental accountability and transparency. Blockchain’s unique attributes—immutability, transparency, and decentralization—position it as a powerful tool to enhance the effectiveness of climate change initiatives and reporting mechanisms like those promoted by the CDP.

Companies might use blockchain to verify that their emissions data and other environmental indicators are securely preserved and unaltered. This decreases the danger of greenwashing, in which corporations mislead or exaggerate their environmental performance to appear more sustainable than they are. Enhanced transparency, blockchain also improves transparency in climate change reporting. All blockchain transactions are transparent to all network participants, allowing stakeholders to access real-time data on a company’s environmental performance. For instance, if a company commits to reducing its carbon emissions by a certain percentage, blockchain can provide a clear and verifiable record of the measures taken and progress achieved toward that aim. This openness can enhance the credibility of corporate sustainability claims and encourage companies to follow through on their environmental commitments.

Integrating blockchain with CDPCC reporting can streamline the entire data collection and reporting process. Companies can use blockchain to automate data capture from IoT devices and other sensors that monitor emissions, energy usage, and other environmental metrics. The data can then be securely stored and easily accessed for reporting purposes. This integration can also facilitate real-time monitoring and verification of environmental performance, enabling more timely and informed decision-making.

Ultimately, the adaptation of blockchain technology to CDPCC reporting can drive greater corporate accountability and action on climate change. Blockchain can assist firms in being held accountable for their environmental impact by offering a transparent, secure, and efficient way of storing and reporting environmental data.

H3: Blockchain adaptation (BA) has a positive and significant influence on CDPCC.

2.4 Blockchain adaptation and Green Accounting

The adaptation of blockchain technology to GRA represents a significant step forward in enhancing transparency, accuracy, and accountability in environmental reporting. Blockchain, with its immutable, transparent, and decentralized nature, offers unique advantages that can significantly enhance GRA practices. Immutable records are one of the main advantages of blockchain in GRA. In GRA, accurate and reliable data on environmental impacts, such as carbon emissions, resource usage, and waste management, are crucial.

Transparency is another key advantage of blockchain in GRA. Blockchain offers a decentralized ledger that is available to all network participants. This accessibility enables real-time tracking and verification of sustainability information, allowing stakeholders to better access and examine a company's environmental performance. This transparency can build trust with investors, regulators, and the public, demonstrating a genuine commitment to sustainability.

Blockchain also enhances accountability in GRA through smart contracts. Smart contracts can validate data against predefined criteria and trigger reporting mechanisms. They also decrease administrative burdens for businesses and lessen the chance of human error, resulting in more precise and trustworthy reports on environmental issues.

The integration of blockchain technology into GRA also makes environmental risk management more effective. Companies may better identify and manage risks connected with resource depletion, legislative changes, and climate change by maintaining a public and immutable record of environmental consequences. Blockchain's capacity to deliver real-time data and automate reporting procedures allows businesses to respond to developing environmental issues more effectively and quickly.

H4: BA has a positive and significant influence on GRA.

2.5 CDP climate change and Green Accounting

CDPCC reporting has a substantial and revolutionary impact on GRA standards. CDP offers a global platform for businesses to report their environmental impacts, with a special emphasis on greenhouse gas emissions and climate change initiatives. By integrating environmental costs and benefits into conventional accounting procedures, GRA is achieved. It incorporates the economic worth of environmental assets and liabilities to give a more thorough picture of a company's financial performance. CDPCC reporting enhances GRA by providing a standardized framework for measuring and disclosing environmental impacts. This helps companies accurately capture and report the financial implications of their environmental activities.

One of the primary influences of CDP on GRA is the emphasis on transparency. CDP's rigorous disclosure requirements encourage companies to publicly report their greenhouse gas emissions, climate risks, and mitigation strategies. This transparency is crucial for GRA, as it ensures that environmental data is accurate, consistent, and comparable across different companies and sectors. The detailed reporting requirements push companies to systematically assess their environmental impacts and develop strategies to mitigate climate-related risks. This integration of environmental considerations into core business strategies is a fundamental principle of GRA, as it ensures that environmental costs and benefits are factored into financial planning and performance evaluation.

Additionally, CDPCC reporting fosters a culture of continuous improvement in GRA. The feedback loop created by CDP reporting encourages companies to set ambitious environmental targets and continuously improve their environmental performance.

H5: CDPCC mediates the influence of ESG, along with BA, simultaneously on GRA.

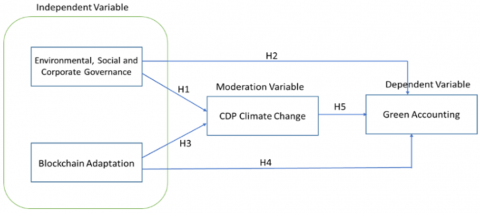

Figure 1. The structure of concepts

Figure 1 illustrates the structure of the concepts of this study, which is based on prior research and the formation of hypotheses as a form of research innovation [14-16].

From the structure of the concepts above, the definition and measurement of operational variables are as follows: BA and ESG as independent variables; CDPCC as a moderation variable; and GRA as a dependent variable.

The study's scope includes staff of start-up businesses in the domain of software development, with an estimated sample population in 2023 of 595 start-up companies located in the West Java and DKI Jakarta regions. From this population, 190 respondents participated in answering questions. The primary data were gathered from respondents to the questionnaire responses representing public firms. The research data were collected using online and offline questionnaires. Employees were contacted and invited to participate. After they granted their consent, the surveys were distributed directly. Data analysis was conducted using the Partial Least Squares Structural Equation Modeling (PLS-SEM) method operated through the Smart-PLS program. PLS could indicate the link between latent variables (prediction) and assist with the hypothesis [17].

The research instrument, as shown in Table 1, will be analyzed using relevant statistical tests, while the technique for measuring the answers to the questionnaire employs a Likert scale (scale 1 to 7).

Table 1. Research instrument

|

Variable |

Indicators |

Source |

|

ESG |

|

[18] |

|

|

|

[19] |

|

||

|

||

|

||

|

BA |

|

[20] |

|

|

|

[21] |

|

[22] |

|

|

[23] |

|

|

CDPCC |

|

[24] |

|

|

|

[25] |

|

[26] |

|

|

[27] |

|

|

||

|

||

|

GRA |

|

[28] |

|

|

|

[29] |

|

||

|

Sources: Author Estimate

3.1 Definition and measurement of operational variables

The equation model in this study illustrates the influence of variables using the regression formula presented below:

$\mathrm{GRA}=\beta_1 \mathrm{ESG}+\beta_2 \mathrm{BA}+\beta_3 \mathrm{CDPCC}^* \mathrm{ESG}+\beta_4 \mathrm{CDPCC}^* \mathrm{BA}+\beta_5 \mathrm{CDPCC}+\varepsilon$

Description:

ESG = Environmental, Social and Corporate Governance

BA = Blockchain Adaptation

CDPCC = Carbon Disclosure Project Climate Change

GRA = Green Accounting

* = Mediation Effect

ε = Galat Error

3.2 Description of data

In response to the profile, 61% of responders are men, and roughly 39% are women. In addition, 92 respondents, or 48%, are between the ages of 25 and 30, implying that most respondents are under 30. Furthermore, Table 2 shows that 38.4% of respondents have worked for more than four years.

Table 2. The respondent's profile

|

Characteristics |

Classification |

Total |

Percentage |

|

Gender |

Male |

116 |

61% |

|

Female |

74 |

39% |

|

|

Total |

190 |

100% |

|

|

Age |

25 - 30 years old |

92 |

48% |

|

31 - 35 years old |

60 |

32% |

|

|

36 - 40 years old |

38 |

20% |

|

|

Total |

190 |

100% |

|

|

Work Period |

≤ 2 years |

54 |

28.4% |

|

2 < wp ≤ 4 years |

63 |

33.2% |

|

|

> 4 years |

73 |

38.4% |

|

|

Total |

190 |

100% |

Sources: Author Estimate

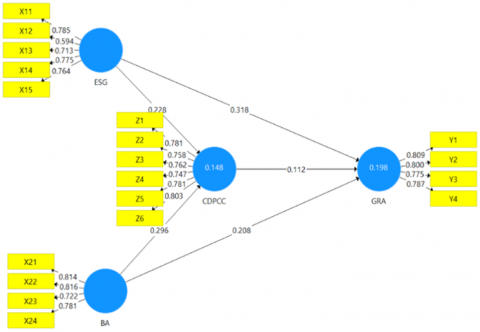

4.1 Confirmatory Factor Analysis (CFA) test of all exogenous variables

To see whether the construct of all exogenous variables has valid indicators, a validity test (CFA) is carried out, as shown in Figure 2.

Figure 2. Outer model

4.2 Validity and reliability

Data analysis includes a detailed examination of the measurement model's reliability and validity, as well as a full grasp of the interactions between constructs and their related items (refer to Table 3). The data analysis reveals the following insights. For reliability, considering the ESG construct, a Cronbach's Alpha score of 0.782 and a rho_A value of 0.800 indicate an exceptionally high level of internal consistency reliability. Similarly, BA has excellent internal reliability, with a Cronbach's Alpha of 0.798 and a rho_A of 0.821. CDPCC has outstanding reliability, with a Cronbach's Alpha of 0.865 and a rho_A of 0.871. GRA retains suitable internal consistency reliability, as evidenced by a Cronbach's Alpha score of 0.804 and a rho_A value of 0.809 [30].

Result for validity: The constructs have resilient CR values over 0.8 (as shown in Table 3), indicating strong convergent validity. Furthermore, AVE values for most constructs are close to 0.6, indicating that a considerable percentage of the variation is successfully captured by the latent variables. Thus, the measurement model has high reliability and convergent validity, as shown in Figure 3 [31].

Table 3. Confirmatory Factor Analysis

|

Construct |

Items |

Outer Loading |

Cronbach's Alpha |

rho_A |

CR |

AVE |

|

ESG Index Ranks |

X11 |

0.785 |

0.782 |

0.800 |

0.849 |

0.532 |

|

X12 |

0.594 |

|||||

|

X13 |

0.713 |

|||||

|

X14 |

0.775 |

|||||

|

X15 |

0.764 |

|||||

|

BA |

X21 |

0.814 |

0.798 |

0.821 |

0.864 |

0.615 |

|

X22 |

0.816 |

|||||

|

X23 |

0.722 |

|||||

|

X24 |

0.781 |

|||||

|

CDPCC |

Z1 |

0.781 |

0.865 |

0.871 |

0.899 |

0.597 |

|

Z2 |

0.758 |

|||||

|

Z3 |

0.762 |

|||||

|

Z4 |

0.747 |

|||||

|

Z5 |

0.781 |

|||||

|

Z6 |

0.803 |

|||||

|

GRA |

Y1 |

0.809 |

0.804 |

0.809 |

0.871 |

0.628 |

|

Y2 |

0.800 |

|||||

|

Y3 |

0.775 |

|||||

|

Y4 |

0.787 |

Sources: Primary data processed, 2024

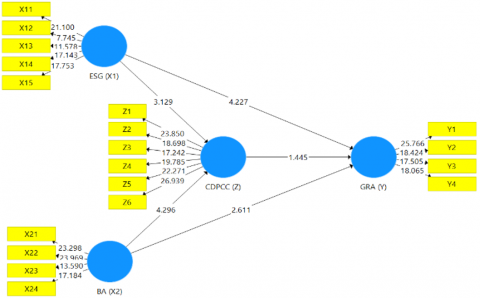

Figure 3. Inner model

Table 4. Path analysis

|

Hypothesis |

Construct |

Original Sample |

T-Statistic |

P-Values |

Result |

|

H1 |

BA(X2) -> CDPCC(Z) |

0.296 |

4.296 |

0 |

Accepted |

|

H2 |

BA(X2) -> GRA(Y) |

0.208 |

3.085 |

0.002 |

Accepted |

|

H3 |

ESG(X1) -> CDPCC(Z) |

0.228 |

3.129 |

0.002 |

Accepted |

|

H4 |

ESG(X1) -> GRA(Y) |

0.318 |

4.227 |

0 |

Accepted |

|

H5 |

CDPCC(Z) -> GRA(Y) |

0.112 |

1.445 |

0.148 |

Rejected |

4.3 Hypothesis result

The findings provide a thorough examination of the hypotheses that study the links between numerous constructs (refer to Table 4 and Table 5). The fourth and fifth hypotheses (H1 through H5) are accepted, suggesting significant relationships between different constructs. There is substantial evidence supporting the relationships between ESG and CDPCC, ESG and GRA, BA and CDPCC, and BA and GRA. However, Hypothesis 5 (H5: CDPCC -> GRA) was not accepted. This implies that there is no statistically significant or weak association between ESG and BA across the mediation variable CDPCC vs. GRA. As a result, the data analysis demonstrates significant influence between most constructs, allowing for a better understanding of how these factors interact. It does, however, indicate situations where such linkages are not statistically significant, which provides vital insights into the complicated interactions within the research environment.

Table 5. Confidence intervals

|

Construct |

Original Sample |

Sample Mean |

2.50% |

97.50% |

|

BA (X2) -> CDPCC (Z) |

0.296 |

0.304 |

0.162 |

0.431 |

|

BA (X2) -> GRA (Y) |

0.208 |

0.246 |

0.083 |

0.391 |

|

CDPCC (Z) -> GRA (Y) |

0.112 |

0.111 |

-0.052 |

0.258 |

|

ESG (X1) -> CDPCC (Z) |

0.228 |

0.235 |

0.086 |

0.372 |

|

ESG (X1) -> GRA (Y) |

0.318 |

0.352 |

0.207 |

0.491 |

Sources: Primary data processed, 2024

The moderate regression equation model in this study explains the influence between variables as follows:

GRA = 0.318ESG + 0.208BA + 0.228CDPCC*ESG + 0.296CDPCC*BA + 0.112 + ε

Description:

ESG = Environmental, Social and Corporate Governance

BA = Blockchain Adaptation

CDPCC = Carbon Disclosure Project Climate Change

GRA = Green Accounting

* = Mediation Effect

ε = Galat Error

H1: In conclusion, the implementation of ESG issues into corporate plans, as well as their effect on CDPCC reporting, demonstrates the rising relevance of sustainable and ethical business practices. Companies that pursue ESG principles are better able to manage climate risks, attract investment, and foster healthy stakeholder relationships. As the global climate crisis intensifies, the alignment between ESG and CDP will continue to drive corporate transparency and accountability in environmental stewardship.

H2: In conclusion, the influence of ESG considerations on GRA is profound and multifaceted. Companies that include ESG standards in their accounting methods can increase transparency, minimize environmental risks, and advance their social and management achievements. GRA provides a comprehensive framework for capturing the economic value of environmental and social assets and liabilities, enabling companies to make more informed and sustainable business decisions. The need for corporate transparency as well as sustainability continues to rise. The alignment between ESG and GRA will become increasingly important in driving positive environmental and social outcomes.

H3: In conclusion, the adaptation of blockchain technology to CDPCC reporting holds significant promise for enhancing environmental transparency, accountability, and efficiency. Blockchain's immutable records, enhanced transparency, decentralization, and smart contracts provide robust mechanisms to ensure accurate and reliable climate data reporting. By integrating blockchain with CDP, companies can streamline data collection, automate reporting processes, and build trust with stakeholders through transparent and verifiable records. This can drive greater corporate accountability, incentivize sustainable practices, and successfully contribute to worldwide climate change mitigation strategies. As blockchain technology evolves, its potential to transform climate reporting and drive meaningful environmental action will only grow.

H4: In conclusion, the adaptation of blockchain technology to GRA offers transformative benefits that enhance the transparency, accuracy, and accountability of environmental reporting. By leveraging blockchain's immutable records, transparency, decentralization, and smart contracts, companies can improve their GRA practices, build trust with stakeholders, and better manage environmental risks. As the trend for sustainable business operations develops, implementing blockchain in GRA will be essential for improving corporate sustainability efforts.

H5: In conclusion, the influence of CDPCC reporting on GRA is profound. CDP's emphasis on transparency, accountability, and the integration of environmental considerations has driven significant advancements in GRA practices. By providing a standardized framework for environmental disclosure, CDP enhances the reliability and comparability of environmental data, which is essential for effective GRA. However, CDPCC as a mediator variable to mediate Environmental, Social, Governance, and BA towards GRA shows that the relationship is still weak. This allows businesses to make more educated financial decisions, enhance their environmental performance, and contribute to global sustainability projects. As the significance of environmental accountability develops, the collaboration between CDPCC reporting and GRA will play a critical role in determining the future of business sustainability.

The findings of this study are intended to provide further knowledge regarding blockchain technology in connection to GRA, particularly as this technology is currently not well known in Indonesia. For corporations, it is expected that further research on blockchain will be conducted by expanding the scope of the potential implementation of blockchain, ESG, and CDP, as well as the novelty of references to remain relevant to existing conditions. Companies are required to better grasp the growth of innovations like blockchain and how it can be utilized in business management. In addition, the government is expected to create its own research center related to blockchain technology because blockchain has great potential to be applied in various fields.

Managerial recommendations and suggestions for practitioners and business stakeholders should include a few strategic steps that can be taken to strengthen each other and innovate together, namely: 1) Business Strategy Collaboration, 2) Cultural Transformation and HR Development in the form of cross-generational training or intrapreneurship programs, 3) Technology and Infrastructure Integration, 4) Government and Regulatory support, for example, fiscal incentives and inclusive regulations, 5) Strengthening the start-up ecosystem, for example, mentorship and community mapping, local needs, and increasing digital literacy.

[1] Gunawan, J., Susilo, H. (2021). Corporate social responsibility, corporate reputation, and share price: A study of consumer goods industries using Sustainable Accounting Standard Board (SASB) disclosures. Jurnal Magister Akuntansi Trisakti, 8(1): 65-84. https://doi.org/10.25105/jmat.v8i1.8770

[2] Holland, M., Stjepandić, J., Nigischer, C. (2018). Intellectual property protection of 3D print supply chain with blockchain technology. In 2018 IEEE International Conference on Engineering, Technology and Innovation (ICE/ITMC), Stuttgart, Germany, pp. 1-8. https://doi.org/10.1109/ICE.2018.8436315

[3] Mihalic, T. (2016). Sustainable-responsible tourism discourse–towards ‘responsustable’tourism. Journal of Cleaner Production, 111: 461-470. https://doi.org/10.1016/j.jclepro.2014.12.062

[4] Baron, R.M., Kenny, D.A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6): 1173. https://doi.org/10.1037/0022-3514.51.6.1173

[5] Zhixia, C., Hossen, M.M., Muzafary, S.S., Begum, M. (2018). Green banking for environmental sustainability-present status and future agenda: Experience from Bangladesh. Asian Economic and Financial Review, 8(5): 571-585. https://doi.org/10.18488/journal.aefr.2018.85.571.585

[6] Asadikia, A., Rajabifard, A., Kalantari, M. (2021). Systematic prioritisation of SDGs: Machine learning approach. World Development, 140: 105269. https://doi.org/10.1016/j.worlddev.2020.105269

[7] Zaky, M.A., Nuzar, I., Saputro, W.E., Praysuta, B.D.S., Wijaya, S.B., Riswan, M. (2018). Mapping & Database Startup Indonesia 2018. Badan Ekonomi Kreatif.

[8] DiMaggio, P.J., Powell, W.W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2): 147-160. https://doi.org/10.1016/S0742-3322(00)17011-1

[9] Deegan, C. (2009). Financial Accounting Theory. McGraw Hill. Australia: North Ryde.

[10] Guthrie, J., Parker, L.D. (1989). Corporate social reporting: A rebuttal of legitimacy theory. Accounting and Business Research, 19(76): 343-352. https://doi.org/10.1080/00014788.1989.9728863

[11] Freeman, R.E. (2010). Strategic Management: A Stakeholder Approach. Cambridge University Press.

[12] Leung, Z.B.G., Philomena, L. (2013). An empirical analysis of the determinants of greenhouse gas voluntary disclosure in Australia. Accounting and Finance Research, 2(1): 110-127. https://doi.org/10.5430/afr.v2n1p110

[13] MacKinnon, D. (2012). Introduction to Statistical Mediation Analysis. Routledge.

[14] Dayanti, P.R., Yulianti, P. (2023). How servant leadership and knowledge-sharing trigger innovative work behavior among millennials at start-up businesses? Jurnal Manajemen Teori dan Terapan, 16(1): 95-106. https://doi.org/10.20473/jmtt.v16i1.43224

[15] Manurung, M.I.S.R., Sudhartio, L. (2024). Analyzing the influence of strategic agility, innovation capability and organizational readiness on the performance of PT Pegadaian. Al Qalam: Jurnal Ilmiah Keagamaan dan Kemasyarakatan, 18(3): 1669-1686. https://doi.org/10.35931/aq.v18i3.3178

[16] Nuryanto, U.W., Quraysin, I., Pratiwi, I. (2024). Environmental management control system, blockchain adoption, cleaner production, and product efficiency on environmental reputation and performance: Empirical evidence from Indonesia. Sustainable Futures, 7: 100190. https://doi.org/10.1016/j.sftr.2024.100190

[17] Imam, G., Hengky, L. (2015). Partial Least Squares: Konsep, Teknik dan Aplikasi Menggunakan Program Smartpls 3.0. Universitas Diponegoro Semarang.

[18] Li, Y., Gong, M., Zhang, X.Y., Koh, L. (2018). The impact of environmental, social, and governance disclosure on firm value: The role of CEO power. The British Accounting Review, 50(1): 60-75. https://doi.org/10.1016/j.bar.2017.09.007

[19] Authority, E.B. (2021). EBA Report. https://www.eba.europa.eu/sites/default/files/document_library/About%20Us/Annual%20Reports/2021/1035237/EBA%202021%20Annual%20Report.pdf.

[20] Clohessy, T., Acton, T., Rogers, N. (2018). Blockchain adoption: Technological, organisational and environmental considerations. In Business Transformation through Blockchain, Cham: Springer International Publishing, pp. 47-76. https://doi.org/10.1007/978-3-319-98911-2_2

[21] Lu, L., Liang, C., Gu, D., Ma, Y., Xie, Y., Zhao, S. (2021). What advantages of blockchain affect its adoption in the elderly care industry? A study based on the technology–organisation–environment framework. Technology in Society, 67: 101786. https://doi.org/10.1016/j.techsoc.2021.101786

[22] Parmentola, A., Petrillo, A., Tutore, I., De Felice, F. (2022). Is blockchain able to enhance environmental sustainability? A systematic review and research agenda from the perspective of Sustainable Development Goals (SDGs). Business Strategy and the Environment, 31(1): 194-217. https://doi.org/10.1002/bse.2882

[23] Pascual Pedreño, E., Gelashvili, V., Pascual Nebreda, L. (2021). Blockchain and its application to accounting. Intangible Capital, 17(1): 1-16. https://doi.org/10.3926/ic.1522

[24] CDP.net. (2024). CDP Full Corporate Questionnaire. CDP.net.

[25] Baba, A.I., Neupane, S., Wu, F., Yaroh, F.F. (2021). Blockchain in accounting: Challenges and future prospects. International Journal of Blockchains and Cryptocurrencies, 2(1): 44-67. https://doi.org/10.1504/IJBC.2021.117810

[26] Bajwa, N., Prewett, K., Shavers, C.L. (2020). Is your supply chain ready to embrace blockchain. Journal of Corporate Accounting & Finance, 31(2): 54-64. https://doi.org/10.1002/jcaf.22423

[27] Sharma, M.Y., Sharma, M.B., Jain, D. (2019). Blockchain–creating positive vibes in the card payment industry. Annual Research Journal of SCMS, Pune, 7: 1-10.

[28] Lestari, J., Solikhah, B. (2019). The effect of CSR, tunneling incentive, fiscal loss compensation, debt policy, profitability, firm size to tax avoidance. Accounting Analysis Journal, 8(1): 31-37. https://doi.org/10.15294/aaj.v8i1.23103

[29] Hijau, L.A.A. (2018). Isu, Teori dan Aplikasi. Jakarta: Salemba Empat.

[30] Hair, J.F., Risher, J.J., Sarstedt, M., Ringle, C.M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1): 2-24. https://doi.org/10.1108/EBR-11-2018-0203

[31] Hair Jr, J., Hair Jr, J.F., Sarstedt, M., Ringle, C.M., Gudergan, S.P. (2023). Advanced Issues in Partial Least Squares Structural Equation Modeling. Sage Publications.