Nguyen Thi Bich Diep*![]() | Nguyen Mau Nhat Nam

| Nguyen Mau Nhat Nam![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Green banking in Vietnam is aligned with global sustainability goals and is increasingly embedded in national strategies. Commercial Joint Stock Bank (BAB) stands out as a pioneering institution by prioritizing green credit allocation to high-tech agriculture, environmental infrastructure, and social welfare. This study evaluates progress and challenges in promoting green banking in BAB, particularly its Hung Yen branch. The secondary data, which are collected from formal sources, are analyzed by the narrative and descriptive statistical method. The main findings show that BAB’s green credit portfolio grew significantly from 2021 to 2023, especially in agriculture, indicating a strong institutional commitment to sustainability. The bank also developed innovative green deposit products and digital banking services to reduce its ecological footprint. Despite this progress, key challenges persist, including limited access to long-term funding, insufficient staff expertise, and underdeveloped ESG data systems. The policy recommendations are: to strengthen regulatory support, enhance internal capacity, and diversify green financial products to scale sustainable finance in Vietnam.

green banking, practice, BAC A BANK, Vietnam

Green banking has emerged as a derivative of a broader green finance paradigm. Höhne et al. [1] conceptualized green finance as a financial investment in environmentally conducive projects that foster sustainable development. Ledgerwood [2] conceived that credit institutions have increasingly prioritized poverty alleviation and sustainability imperatives through the integration of green finance principles. Furthermore, Lindenburg [3] contended that green finance encompasses both public and private financial mechanisms concentrated on environmentally-oriented public goods and services, including governance frameworks, biodiversity conservation, and landscape preservation, to mitigate environmental degradation and climate change impacts.

The concept of green banking has attracted significant scholarly attention in recent years. International organizations [4, 5] emphasize integration of ecological criteria into banking operations and development of financial instruments that facilitate environmentally responsible investment, whereas academic discourse highlights the incorporation of environmental and social considerations into banking functions and services, with the concurrent objectives of sustainable development promotion, climate change mitigation, and economic viability [6]. The green banking paradigm encompasses a diverse spectrum of activities, including renewable energy project financing, energy efficiency promotion in infrastructure and operations, sustainable business practice incentivization, and environmental risk assessment incorporation in lending protocols [7-9]. Additionally, green banking practices advance social responsibility through the facilitation of projects that enhance societal welfare, such as educational initiatives, healthcare systems, and affordable housing developments [10-12].

SOGESID Spa [13] characterized green banks as institutions that simultaneously fulfill traditional banking functions while implementing initiatives directed toward community development and environmental conservation. These institutions transcend the binary objectives of corporate social responsibility and profitability, instead achieving a harmonious integration of economic, social, and environmental objectives to ensure sustainable development. According to Höhne et al. [1], green banking institutions must adhere to a comprehensive framework comprising social responsibility standards (23 criteria) and environmental responsibility standards (47 criteria). The operational framework of green banking can be conceptualized through the five-level taxonomic model proposed by Kaeufer [14].

Vietnam has consistently demonstrated proactive engagement with international commitments and agreements concerning climate change mitigation and green development initiatives. The implementation of green banking practices and sustainable development frameworks represented an unavoidable trend in global banking strategic imperatives and has attained the status of mandatory evaluation criteria among numerous international credit rating organizations. Consequently, the State Bank of Vietnam has promulgated multiple policy instruments and strategic directives to facilitate environmental risk management integration and green transformation processes among credit institutions, as evidenced by the Project on Developing Green Banking in Vietnam and the orientation towards green banking advancement delineated in the Strategy for Development of the Banking Industry to 2025, with a vision extending to 2030.

Notwithstanding these initiatives, empirical research indicates that within the Vietnamese banking sector, 91% of institutions demonstrate insufficient comprehension of green credit principles and lack coherent strategic frameworks addressing this domain, while 35% exhibit complete unfamiliarity with green finance and green credit concepts [15]. Furthermore, the regulatory and policy instruments promulgated by governmental authorities and the State Bank of Vietnam currently provide inadequate guidance for the systematic implementation of sustainable banking practices within the national financial infrastructure.

Bac A Commercial Joint Stock Bank (BAB), established under Decision No. 183/QD-NH5 dated September 01, 1994, issued by the Governor of the State Bank of Vietnam, represents one of the inaugural private banking institutions in the nation. The bank's institutional vision encompasses the cultivation of a customer demographic oriented toward sustainable development, with investment priorities focused on high-technology agricultural applications, rural development initiatives, and social security enhancement. Recognized as a preeminent institution in green banking implementation, BAB strategically prioritizes credit allocation and investment activities related to technological innovation in agriculture, rural development, nutrition, healthcare, pharmaceutical sectors, education, and social welfare domains. These strategic orientations generate sustainable value propositions for the bank's developmental trajectory while contributing to national innovation capacity and economic prosperity. Consequently, BAB has received recognition as "Outstanding Bank for Green Credit" within the evaluative framework of prestigious financial sector awards organized by the Vietnam Banks Association in 2023 and 2024.

Despite the growing body of literature and policy interest in green banking as a strategic response to climate change and sustainable development, the gaps still exist. While theories of green banking continue to evolve, the field remains criticized because of its conceptual ambiguity and limited empirical integration. Most studies in the world, as well as in Vietnam, most studies concentrate on institutional and supply-side dynamics, with limited attention given to customers’ awareness, behavioral preferences, and demand for green banking products. In addition, there is a lack of studies that analyze the effectiveness and efficiency of policies for banking practices.

In attempting to fill out the gaps mentioned, this research aims: (i) to conduct a comprehensive assessment of preliminary outcomes and implementation challenges encountered by a commercial bank in its pursuit of green banking practices, and (ii) to formulate strategic recommendations for the enhancement and expansion of sustainable banking operations at BAB in subsequent operational periods.

Vietnam has proactively taken actions following international commitments and agreements, aiming to respond to climate change and head towards green development. The State Bank of Vietnam has issued many policies and guidelines to encourage credit institutions in green transformation and environmental risk management in credit extension activities.

Several commercial banks have deployed green credit, such as BIDV, Agribank, Techcombank, ACB, ... Among several banks, BAB stands out as a pioneering institution that has prioritized green credit in recent years. As a result, this study employs secondary data and information collected from the published academic literature and reports from BAB's headquarters and its Hung Yen branch.

Narrative and descriptive statistical methods mainly analyze the data and information. Besides, a comparative analysis has been carried out to find the differences between BAB and other commercial banks in green banking practices. How BAB practices as a green bank is evaluated via ESG criteria, which were issued in a “Guide Book” by USAID and the Ministry of Planning and Investment (MPI) in 2023.

The preceding decennial period has witnessed substantial evolution in Vietnam's regulations governing green banking practices. These transformations have transpired within a global context characterized by intensified emphasis on environmental sustainability imperatives and responsible financial frameworks. In response to these international developments, Vietnam has initiated systematic efforts to align its financial sector operations, with particular emphasis on banking activities, with established green principles and sustainable finance paradigms. The regulatory infrastructure supporting green banking implementation in Vietnam has been codified through a multitude of policy instruments and legislative frameworks, as systematically delineated in Table 1.

Table 1. Legal framework for green banking practices in Vietnam

|

Policy Documents |

|

1. Central Government |

|

Decision No. 432/2012/QD-TTg approving the Sustainable Development Strategy in Vietnam for the period 2011-2020 |

|

Decision No. 1393/2012/QD-TTg approving the National Strategy on Green Growth for the 2011-2020 period and vision to 2030 |

|

Decision No. 403/2014/QD-TTg approving the National Action Plan on Green Growth for the 2014-2020 period |

|

Decision No. 2053/2016/QD-TTg approving the Plan to implement the Paris Agreement on climate change |

|

Resolution No. 136/NQ-CP dated September 25, 2020, of the Government on sustainable development |

|

Decision No. 1658/QD-TTg dated October 1, 2021, approving the National Strategy on Green Growth for the 2021-2030 period, with a vision to 2050 |

|

Decision No. 882/QD-TTg dated July 22, 2022, approving the National Action Plan on Green Growth for the 2021 - 2030 period |

|

Decision No. 687/QD-TTg dated June 7, 2022, of the Prime Minister approving the Circular Economy Development Project in Vietnam |

|

Decision No. 813/QD-NHNN dated April 24, 2017, on the loan program to encourage the development of high-tech agriculture, clean agriculture, and loans for coffee replanting in the Central Highlands |

|

Decree No. 75/2015/ND-CP dated September 9, 2015, of the Government implementing loan programs for production forest planting |

|

2. The State Bank of Vietnam |

|

Directive No. 03/CT-NHNN dated 24 March 2015 by the State Bank of Vietnam on promoting green credit growth and environmental-social risks management in credit-granting activities |

|

Decision No. 1552/QD-NHNN dated 6 August 2015 by the State Bank of Vietnam issued the Action plan of the banking sector for implementation of the National strategy for green growth by 2020 |

|

Circular No. 39/2016/TT-NHNN dated 30 December 2016 by the State Bank of Vietnam prescribing lending transactions of credit institutions and foreign bank branches with customers |

|

Decision No. 1604/QD-NHNN dated 7 August 2018 by the State Bank of Vietnam approving the scheme for green banking growth in Vietnam |

|

Decision No. 1658/QD-TTg dated 01 October 2021 by the Prime Minister approving the National strategy on green growth for the period of 2021 – 2030 with a vision to 2050 |

|

Law No. 72/2020/QH14 dated 17 November 2020 by the National Assembly on Environmental Protection |

|

Circular No. 17/2022/TT-NHNN dated 23 December 2022 by the State Bank of Vietnam provides guidelines on environmental risk management in credit extension by credit institutions and foreign bank branches |

|

Decision No. 1408/QD-NHNN dated 26 July 2023 by the State Bank of Vietnam promulgating the Action plan of the banking sector for implementation of the National strategy for green growth for the period of 2021 – 2030 and the Scheme for tasks and solutions for implementing the results of the United Nations Climate Change Conference COP26 |

Source: http://www.vbqppl.gov.vn

As evidenced in Table 1, commencing in 2012, the Vietnamese Government has implemented a comprehensive suite of policy instruments oriented toward achieving sustainable development and green growth objectives. The most important policy documents are Decision No. 1658/QD-TTg approving the National Strategy on Green Growth for the 2021-2030 period, with a vision to 2050, followed by Decision No. 882/QD-TTg dated July 22, 2022, approving the National Action Plan on Green Growth for the 2021-2030 period. In these documents, the Vietnamese government promulgated detailed regulations on the list of green projects, criteria, and conditions for identifying green projects and the confirmation of green projects to promote the formation and operation of the green credit and green bond market in Vietnam. Additionally, Vietnam has implemented loan programs for the development of high-tech agriculture, clean agriculture, and loans for coffee replanting in the Central Highlands according to Decision No. 813/QD-NHNN dated April 24, 2017, for forest planting according to Decree No. 75/2015/ND-CP, and for agricultural and rural development according to Decree No.116/2018/ND-CP.

In response to these governmental initiatives, the State Bank of Vietnam subsequently promulgated various regulatory directives to facilitate banking sector engagement in environmentally sustainable domains. Notwithstanding these regulatory efforts, there remained a demonstrable requirement for a more comprehensive and cohesive legal framework to effectively facilitate and govern green credit activities [16]. The recent temporal period has witnessed substantive development and refinement of the legal architecture surrounding green credit provision. The State Bank of Vietnam has issued numerous decisions, directives, and circulars, precipitating increased adoption of green practices among Vietnamese banking institutions, as follows:

- The project on developing green banking in Vietnam (Decision 1604/QD-NHNN dated August 7, 2018) has been supplemented and integrated into the orientation of developing green credit and green banking in the content of the Banking industry development strategy to 2025, with a vision to 2030 (Decision No. 986/QD-TTg dated August 8, 2018), aiming to increase awareness and social responsibility of the banking system in protecting the environment;

- The Action Plan of the Banking Industry to Implement the National Strategy on Green Growth to 2030, Action Plan of the Banking Industry to Implement the 2030 Agenda for Sustainable Development (Decision No. 1408/QD-NHNN dated July 26, 2023, and Decision No. 1731/QD-NHNN dated August 31, 2018);

- The Directive No. 03/CT-NHNN dated March 24, 2015, on promoting green credit growth and managing environmental and social risks in credit-granting activities;

- The Circular No. 17/2022/TT-NHNN dated December 23, 2022, guiding credit institutions to implement environmental risk management in credit granting activities of credit institutions and foreign bank branches, demonstrating the responsibility of the banking sector in implementing environmental protection work;

In addition, the State Bank has deployed many solutions to develop modern banking services based on Fintech and Blockchain technologies in the banking sector. The programs which support the poor in housing to prevent climate change have been implemented, such as: Loan program to build storm and flood-proof houses in the Central region, building houses in flooded areas of the Mekong Delta, credit programs to contribute to reducing greenhouse gas effects and environmental pollution such as clean water and rural environmental sanitation programs.

Concurrently, the Environmental-Social-Governance (ESG) paradigm has emerged as a structured evaluative framework for assessing sustainability performance metrics of financial institutions and their financing activities [17]. The term ESG first appeared in 2003 in the United Nations report “Who Cares Wins” [18]. In empirical studies, there are still many conflicting views on the impact of ESG standards on the performance of commercial banks. Some empirical studies have found a positive impact of ESG on the performance of commercial banks [19, 20]. Meanwhile, some other studies suggest that ESG can reduce the profitability of commercial banks [21-23]. From another perspective, some empirical studies have demonstrated that the positive effect of ESG on the performance of commercial banks only exists when these commercial banks achieve a certain level of ESG investment [23-25].

The green banking regulatory directives promulgated by the State Bank of Vietnam demonstrate substantial alignment with internationally recognized ESG standards, reflecting the integration of global sustainability frameworks into national banking regulations. Besides, the commercial banks in Vietnam must comply with the government’s ESG standards for private enterprises according to Decision No. 167/QD-TTg of the Prime Minister: Approving the "Program to support private sector enterprises to conduct sustainable business in the period 2022-2025".

The environmental standard (E) encompasses multiple dimensions: Environmental protection; Combating climate change; Directing credit flows towards financing environmentally friendly projects; promoting green manufacturing, services, and consumption; Efficient use of energy; Promoting clean energy and renewable energy. The green credit programs specifically designed to mitigate greenhouse gas emissions and environmental pollution are similarly incentivized within the regulatory framework.

The social dimension (S) of the ESG framework emphasizes protecting human health and financial inclusion, thereby removing barriers to access, ensuring small and medium enterprises, the poor and vulnerable can access to basic banking services. The social element mentioned in the government’s policy documents is not much.

The governance dimension (G) of the ESG framework include: Perfecting banking and credit institutions, enhancing awareness, capacity and environmental and social responsibility of the banking system; Managing environmental and social risks; strengthening anti-money laundering and anti-terrorist financing; Fully meeting standards on governance and safety of banking operations to approach international practices.

At the state management level, the Vietnamese government’s and the State Bank’s policies mentioned above, much more concentrated on the Environmental standards (E) in ESG, meanwhile, the content on the Social standards (S) and the Governance element (G) is still limited and unclear.

Up to March 31, 2025, 58 credit institutions in Vietnam had generated green credit balances with outstanding loans reaching over VND 704,244 billion, an increase of 3.57% compared to the end of 2024. These loans account for 4.3% of the total outstanding loans in the whole economy [26].

Even though an analysis of ten selected commercial banks done by Fair Finance Vietnam [27] showed that the average score for all three factors of ESG is 1.1 out of 10 points. Specifically, in the published strategies of selected commercial banks, environmental commitments were shown the least. Although social (S) and governance (G) factors were better reflected than environmental ones (E), they were still below average. Compared to other countries in the ASEAN region, the policy commitments on E and S factors of Vietnamese commercial banks are not too different from those of banks in Indonesia and Thailand. Thai banks are currently outstanding in G, scoring 3.5/10. However, the ESG commitments of all three countries, Indonesia, Thailand, and Vietnam, are still lower than the maximum score of 10 [27].

Apart from evaluating banks’ compliance with ESG standards carried out by Fair Finance Vietnam, the award "Outstanding Bank for Green Credit" was established in 2019 (by the International Data Group - IDG and the Vietnam Banking Association) to honor commercial banks with policies and products aimed at environmentally friendly and sustainable businesses and projects in Vietnam. In 2023 and 2024, BAC A BANK was honored in the "Outstanding Bank for Green Credit" award because of its policies and products aimed at environmentally friendly businesses and projects and sustainable development.

BAB has established its position as a pioneering institution within Vietnam's green banking ecosystem. The bank maintains rigorous adherence to governmental policy directives concerning sustainable development initiatives. BAB's strategic credit allocation prioritizes sustainable development projects within three principal sectors: agricultural and rural development, environmentally responsible processing industries - E, social welfare infrastructure - S [28], and a transparent, effective corporate governance system that complies with the law and business ethics - G.

4.1 Compliance of E-standards

BAB has developed and implemented innovative green deposit instruments that channel customer funds specifically toward environmentally sustainable investment opportunities, while providing enhanced transparency through systematic reporting protocols regarding funded initiatives [29]. Furthermore, BAB has expanded its digital banking infrastructure to facilitate reduced paper consumption and minimize customer transportation requirements, encompassing a comprehensive mobile banking platform with augmented functionality for environmental impact assessment of individual banking activities [30].

The bank's lending priorities demonstrate direct alignment with Vietnam's revised Nationally Determined Contribution (NDC) under the Paris Agreement framework, with particular emphasis on renewable energy transition and sustainable agricultural practices [31]. BAB maintains active participation in the State Bank of Vietnam's green credit initiative, which seeks to incrementally increase the proportion of environmentally sustainable loans within the banking sector to support Vietnam's commitment to carbon neutrality by 2050 [32]. The bank has established collaborative relationships with governmental agencies regarding pilot programs that support green financing mechanisms as delineated in Vietnam's National Climate Change Strategy [33]. Moreover, BAB's sustainable agriculture financing frameworks demonstrate congruence with Vietnam's National Adaptation Plan, which prioritizes climate resilience enhancement within the agricultural sector [34].

BAB consistently maintains an elevated agricultural lending ratio within its portfolio. The institution actively implements and systematically introduces diverse financial products that promote Vietnam's inherent agricultural strengths, particularly in high-technology applications within the agriculture, forestry, and fishery sectors. The prioritized investment projects in BAB's portfolio include dairy cattle husbandry combined with milk processing operations, and the cultivation and processing of medicinal herbs and natural flavoring compounds. These strategic investments generate dual benefits: sustainable economic returns for investors and enhanced health outcomes for consumers. As of 2024, the green credit portfolio constitutes approximately 21% of the institution's total outstanding loan balance [30].

As of December 31, 2023, BAB's operational network encompasses 175 transaction points distributed across 42 provinces and cities nationwide, including Hung Yen province. Situated centrally within the Red River Delta region, Hung Yen province hosts 17 industrial parks accommodating 437 projects with an aggregate investment valuation of 9 billion USD. In 2022, these industrial parks generated revenue of 5.5 billion USD, with export value approximating 3.1 billion USD and domestic budget contribution reaching 2,700 billion VND [35]. Industrial production represents a significant contributor to Hung Yen province's socio-economic development trajectory. Notwithstanding these positive economic impacts, industrial development in Hung Yen province confronts substantial environmental challenges requiring immediate remediation. Obsolete technological infrastructure and equipment deployed in industrial production processes, particularly in electricity generation, steel manufacturing, cement production, and chemical industries, constitute significant emission sources, resulting in severe environmental degradation and pollution. This situation necessitates an urgent transformation in industrial production methodologies within Hung Yen province. The emerging paradigm shift emphasizes green and circular production frameworks. To address capital requirements for developing environmentally responsible agricultural and industrial production systems, BAB's Hung Yen branch has implemented targeted lending programs for priority projects, with particular emphasis on organic and Vietgap (Vietnamese Good Agricultural Practices), solid waste treatment facilities, and wastewater management infrastructure (Table 2).

Table 2. Hung Yen BAB’s green loan balance in the period 2021-2023

|

Production Activities |

Unit |

2021 |

2022 |

2023 |

Average Growth Rate (%) |

|

Agricultural production |

Mil. VND |

270,550 |

492,860 |

495,580 |

135.34 |

|

- Organic products |

Mil. VND |

200,000 |

295,530 |

300,000 |

122.47 |

|

- VietGAP |

Mil. VND |

70,550 |

197,330 |

195,580 |

166.50 |

|

Industrial production |

Mil. VND |

18,387 |

18,348 |

19,676 |

103.45 |

|

- Solid waste treatment |

Mil. VND |

16,597 |

16,827 |

18,350 |

105.15 |

|

- Sewage management |

Mil. VND |

1,790 |

1,521 |

1,326 |

86.07 |

|

Total green loan balance |

Mil. VND |

288,937 |

411,208 |

515,256 |

133.54 |

|

Proportion in total balance |

% |

22.5 |

23.5 |

25.3 |

- |

Source: Hung Yen BAC A BANk office

Note: Average growth rate = (Value 2023/Value 2021)^(1/2)*100

One USD equals to 26,147,000 VND on April 24, 2025. Retrieved from https://www.vietcombank.com.vn/vi-VN/KHCN/Cong-cu-Tien-ich/Ty-gia

Hung Yen BAB's green loan portfolio composition is quantitatively presented in Table 2. Among the 12 green credit priority sectors stipulated by the State Bank of Vietnam (encompassing green agriculture, sustainable forestry, green industry, renewable energy, resource reuse, waste treatment, environmental protection, water management in urban and rural contexts, afforestation initiatives, sustainable transportation, environmental protection services, and miscellaneous categories), BAB has concentrated its implementation efforts in three principal sectors: green agriculture, solid waste treatment, and sewage management in urban areas and industrial zones. Hung Yen BAB's green credit portfolio exhibited substantial growth during the 2021-2023 period, with an average annual expansion rate of 33.54%, wherein the agricultural sector demonstrated both higher proportional representation within the outstanding loan portfolio and superior growth metrics compared to the industrial sector (35.34% and 3.45%, respectively). This sectoral disparity is attributable to Hung Yen BAB's strategic extension of credit facilities not exclusively to agricultural producers within the province, but comprehensively throughout the Red River Delta region, aligning with BAB's institutional development strategy. Despite operating within an industrialized province, the proportion of green loans allocated to industrial sectors remains modest and exhibits a declining trajectory, decreasing from 6.36% in 2021 to 3.83% in 2023. This pattern indicates BAB's strategic prioritization of the agricultural sector and suggests the underdevelopment of green industrial initiatives within Hung Yen province.

Kaeufer [14] suggested that green banking extends beyond financing environmentally sustainable production initiatives. It also involves operational practices such as minimizing paper consumption by both banking institutions and their clients, promoting the use of online banking platforms, and reducing the number of physical branches and offices. These efforts contribute to making internal processes, infrastructure, and information technology systems more environmentally efficient by minimizing their negative ecological impacts [36]. In this context, Hung Yen BAB has made notable progress in promoting a cashless economy, particularly through the expansion of electronic banking services. Internal data reveal that the bank has experienced an average annual growth rate of 34.3% in cashless transactions, with e-banking adoption increasing at a rate of 35.1% per year. Comparatively, paper usage annually at Hung Yen BAB decreased by 24%, and the number of customers coming to do direct transactions at the bank fell by 30%. However, BAB has not issued any apps with tracking carbon features. Thus, it is not possible to estimate carbon based on the type of goods and services that customers consume.

In addition, the interest rates offered on green project loans remain comparable to conventional lending rates, ranging from approximately 4.0% to 5.5% annually. These rates may not be sufficiently attractive to encourage greater investment in green initiatives. In addition to refraining from financing projects that contravene the Law on Environmental Protection in Vietnam, BAB, both at the national level and its Hung Yen branch, have demonstrated a strong commitment to addressing social responsibility. This includes efforts to safeguard workers’ rights, support local community development, and contribute to educational initiatives.

4.2 Implementation of S-standards

Human resource development is an important task in BAB's and its branches’ sustainable development strategies. BAB's S-standards are realized in policies that protect staff’s benefits and social responsibility to local communities.

BAB always focuses on training its staff to improve their professional qualifications and working skills as well as to keep up with the development of new technologies in banking operations. In 2023, BAB conducted 67 training courses with 141 classes for 29,372 turns of people in the whole system. On average, each staff member has been trained about 8 times a year.

Concerning employee compensation, Hung Yen BAB consistently ensures the timely and accurate disbursement of monthly salaries, performance-based bonuses, and other welfare-related payments. The bank’s Human Resources and Welfare Department conducts annual surveys to assess employee satisfaction, using the results as a foundation for reviewing and adjusting compensation and benefits for the subsequent year. Additionally, Hung Yen BAB provides annual health examinations and maintains a comprehensive health insurance program for all employees. These welfare initiatives have been well-received and are positively regarded by staff members.

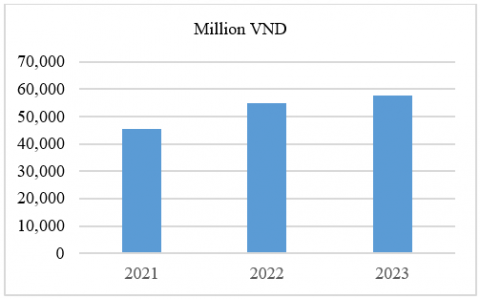

In 2023, BAB allocated over 15 billion VND toward social security initiatives, encompassing a broad range of activities such as educational and healthcare support, poverty alleviation, disaster relief, and gratitude programs for individuals with past contributions to the nation. Furthermore, BAB’s headquarters and branches nationwide, including Hung Yen BAB, collaborated with government agencies and community organizations to mobilize an additional 13.56 billion VND in donations and contributions aimed at supporting underprivileged populations. Not only funding, Hung Yen BAB also gives priority to small and start-up enterprises to get loans with preferential interest rates. Figure 1 shows that the amount of capital that Hung Yen BAB lends to small businesses increased significantly from 2021 to 2023.

Figure 1. Hung Yen BAB’s loans to small enterprises

In addition to the aforementioned initiatives, Hung Yen BAB actively participates in and sponsors charitable programs in response to appeals from governmental agencies, local departments, and non-profit organizations within Hung Yen Province. In 2023 alone, the branch contributed a total of 50 million VND to support various social security activities at the local level.

4.3 Practicing G-standards

G-standards refer to compliance with legal regulations and building a set of principles towards sustainable development within a bank. The management structure of BAB includes: General Meeting of Shareholders, Board of Directors, Board of Supervisors, Board of General Directors, and ensures obedience with current legal regulations. Hung Yen BAB has gradually implemented transparency and accountability among departments within the branch and with ít partners.

Despite the benefits associated with green banking, BAB faces several challenges in implementing these practices effectively. First, the proportion of green loans remains relatively low, accounting for only about 30% of the bank’s total outstanding credit. Most funding for green projects is sourced from customer deposits, as government-backed financial support remains limited. Consequently, branches such as Hung Yen BAB must carefully manage and balance their capital sources to support green credit initiatives. Second, green projects typically require substantial financial investment and long-term funding. However, Hung Yen BAB predominantly relies on short-term deposits from individuals, and recent regulatory changes by the State Bank of Vietnam have further restricted the allowable proportion of short-term capital that can be allocated to medium- and long-term loans. Third, the capacity of bank staff to evaluate and approve loans based on environmental and social criteria remains limited. Effective green lending demands a robust internal framework for managing environmental and social risks, which is still under development. Finally, the bank’s data systems concerning environmental and social metrics are currently fragmented and inconsistent, making it difficult to aggregate and analyze information to assess sustainability performance comprehensively.

Green banking, with a particular emphasis on green credit, represents a central pillar of the sustainable development strategy within the banking sector. BAB has emerged as one of the pioneering institutions in promoting green credit. Green banking practices at BAB reveal significant achievements and persistent challenges. BAB has emerged as a pioneering institution, demonstrating substantial progress across E-S-G dimensions. The bank's green credit portfolio exhibited remarkable growth with an average annual expansion rate of 33.54% during 2021-2023, channeling approximately 21% of its total outstanding loans toward sustainable projects by 2024. Notable achievements include comprehensive ESG integration across high-technology agriculture, renewable energy, waste management infrastructure, innovative green deposit products, and digital banking services that reduce ecological footprints. The institution's commitment extends beyond environmental compliance to encompass robust social responsibility through extensive staff training programs (29,372 participants in 2023), substantial social security investments (over 15 billion VND), and preferential lending to start-ups and small enterprises. As a result, BAB has been given the "Outstanding Bank for Green Credit" award by the International Data Group and the Vietnam Banks Association in 2023 and 2024.

Despite the progress, several structural constraints impede optimal green banking implementation. The most critical challenge involves capital structure limitations, as green projects require long-term financing while BAB relies predominantly on short-term customer deposits. Recent regulatory changes by the State Bank of Vietnam have further restricted medium and long-term lending capacity, creating additional liquidity management complexities. Limited government-backed financial support forces reliance on customer deposits for green project financing, constraining portfolio scaling capabilities. Staff capacity represents another significant barrier, as effective green lending demands sophisticated environmental and social risk assessment expertise currently lacking among personnel. Additionally, fragmented data systems for environmental and social metrics hamper comprehensive sustainability performance assessment and transparent stakeholder reporting, while modest interest rate differentiation between green and conventional loans (4.0-5.5% annually) provides insufficient borrower incentives for sustainable project prioritization.

To enhance green banking effectiveness, policy recommendations are drawn from the research, including: (1) The Vietnamese government should expedite comprehensive legal framework development for sustainable finance, establish clear green project taxonomies, standardize environmental impact criteria, and implement preferential capital requirements. (2) The State Bank of Vietnam should create specialized refinancing facilities providing commercial banks with long-term, low-cost funding for sustainable projects. (3) For BAB specifically, developing comprehensive green banking strategies with defined targets and diversified product portfolios beyond traditional lending is crucial. Investment in human capital through specialized ESG training programs, strategic partnerships with international development finance institutions, and the establishment of unified environmental and social data management systems will strengthen implementation capacity. It is important to offer carbon tracking features to BAB’s apps to help customers track how their consumption contributes to or reduces carbon emissions, and to provide them with information about environmental programs.

[1] Höhne, N., Khosla, S., Fekete, H., Gilbert, A. (2012). Mapping of Green Finance Delivered by IDFC Members in 2011. Project No. CLIDE12246. https://www.idfc.org/wp-content/uploads/2019/03/idfc_green_finance_mapping_report_2012_06-14-12.pdf.

[2] Ledgerwood, J. (2013). The new microfinance handbook: A financial market system perspective. World Bank Publications.

[3] Lindenburg, N. (2014). Definition of green finance. https://ssrn.com/abstract=2446496.

[4] UNEP-FI. (2019). Principles for responsible banking. United Nations Environment Programme – Finance Initiative. https://www.unepfi.org/banking/bankingprinciples/.

[5] INDEF. (2021). Sustainable banking and ESG in Southeast Asia. Institute for Development of Economics and Finance.

[6] Rehman, M.A., Ullah, M.A., Rahman, M.M. (2021). Adoption of green banking practices and environmental performance in Pakistan: A demonstration of structural equation modelling. Environment, Development and Sustainability, 23: 13200-13220. https://doi.org/10.1007/s10668-020-01206-x

[7] Xu, X., Li, J. (2020). Asymmetric impacts of the policy and development of green credit on the debt financing cost and maturity of different types of enterprises in China. Journal of Cleaner Production, 264: 121574. https://doi.org/10.1016/j.jclepro.2020.121574

[8] Khatun, M.N., Sarker, M.N.I, Mitra, S. (2021). Green banking and sustainable development in Bangladesh. Sustainability and Climate Change, 14(5): 262-271. https://doi.org/10.1089/scc.2020.0065

[9] Zhang, S., Wu, Z., He, Y., Hao, Y. (2022). How does the green credit policy affect the technological innovation of enterprises? Evidence from China. Energy Economics, 113: 106236. https://doi.org/10.1371/journal.pone.0302789

[10] Gupta, J. (2015). Role of green banking in environmental sustainability –A study of selected commercial banks in Himachal Pradesh. International Journal of Multidisciplinary Research and Development, 2(8): 349-353.

[11] Sahoo, P., Nayak, B. (2007). Green banking in India. The Indian Economic Journal, 55(3). https://doi.org/10.1177/0019466220070306

[12] Dikau, S., Volz, U. (2018). Central banking, climate change and green finance. ADBI Working Paper, No. 867, Asian Development Bank Institute (ADBI), Tokyo.

[13] SOGESID Spa. (2012). The evolution of the Sustainable Development concept. http://www.sogesid.it/english_site/Sustainable_Development.html.

[14] Kaeufer, K. (2010). Banking as a Vehicle for Socio-Economic Development and Change: Case Studies of Socially Responsible and Green Banks. Presencing Institute, Cambridge, MA.

[15] Tu, V.T., Quang, L.H. (2017). Awareness and practices of green banking in Vietnamese financial institutions. Journal of Economic Development, 24(3): 56-70.

[16] Tam, N., Quynh, P. (2024). Legal frameworks for sustainable finance in Vietnam: Progress and prospects. Journal of Vietnamese Law, 19(1): 12-29.

[17] Gillan, S.L., Koch, A., Starks, L.T. (2021). Firms and social responsibility: A review of ESG and CSR research in corporate finance. Journal of Corporate Finance, 66: 101889. https://doi.org/10.1016/j.jcorpfin.2021.101889

[18] Bătae, O.M., Dragomir, V.D., Feleagă, L. (2021). The relationship between environmental, social, and financial performance in the banking sector: An European study. Journal of Cleaner Production, 290: 125791. https://doi.org/10.1016/j.jclepro.2021.125791

[19] Bischof, R., Bourdier, N., Gassmann, P., Wackerbeck, P., Marek, S. (2021). European bank transformation: Why banks can no longer ignore ESG. https://www.strategyand.pwc.com/de/en/industries/financial-services/transforming-eu-banks/esg.html.

[20] Danisman, G.O. (2022). ESG scores and bank performance during COVID-19. In Handbook of Research on Global Aspects of Sustainable Finance in Times of Crises. IGI Global, Pennsylvania, pp. 241-260. https://doi.org/10.4018/978-1-7998-8501-6.ch012

[21] Galant, A., Cadez, S. (2017). Corporate social responsibility and financial performance relationship: A review of measurement approaches. Economic Research-Ekonomska Istrăzivanja, 30(1): 676-693. https://doi.org/10.1080/1331677X.2017.1313122

[22] Tommaso, C.D., Thornton, J. (2020). Do ESG scores effect bank risk taking and value? Evidence from European banks. Journal Corporate Social Responsibility and Environmental Management, 27: 2286-2298. https://doi.org/10.1002/csr.1964

[23] Yuen, M.K., Ngo, T., Le, T.D.Q., Ho, T.H. (2022). The environment, social and governance (ESG) activities and profitability under COVID-19: Evidence from the global banking sector. Journal of Economics and Development, 24(4): 345-364. https://doi.org/10.1108/jed-08-2022-0136

[24] Azmi, W., Hassan, M.K., Houston, R., Karim, M.S. (2021). ESG activities and banking performance: International evidence from emerging economies. Journal of International Financial Markets, Institutions and Money, 70: 101277. https://doi.org/10.1016/j.intfin.2020.101277

[25] Nollet, J., Filis, G., Mitrokostas, E. (2016). Corporate social responsibility and financial performance: A non-linear and disaggregated approach. Economic Modelling, 52: 400-407. https://doi.org/10.1016/j.econmod.2015.09.019

[26] Huong, D. (2025). Green credit balance accounts for 4.3% of the total outstanding debt of the entire economy. https://tapchitaichinh.vn/du-no-tin-dung-xanh-chiem-4-3-tong-du-no-toan-nen-kinh-te.html.

[27] Fair Finance Vietnam. (2020). Environmental – social – governance commitments in the banking sector: Overview and case analysis in ten Vietnamese commercial banks. Hanoi, Vietnam. https://vietnam.fairfinanceasia.org/.

[28] Nguyen, T., Tran, M. (2023). Evaluation of green lending practices in Vietnam: A case study of BAC A BANK. Vietnam Banking Review, 35(2): 45-58.

[29] Vietnam Investment Review. (2023). Greener credit headlining BAC A BANK’s modernization. VIR Online. https://vir.com.vn/greener-credit-headlining-bac-a-banks-modernisation-102762.html.

[30] BAC A Bank. (2024). Annual report on green credit and sustainable development initiatives. BAC A Commercial Joint Stock Bank.

[31] Ministry of Natural Resources and Environment of Vietnam. (2023). Revised nationally determined contributions (NDC) report. Government of Vietnam.

[32] SBV. (2024). Green credit initiatives and strategic directions for sustainable finance in Vietnam. State Bank of Vietnam.

[33] Tran, H., Nguyen, L. (2024). Promoting green finance in Vietnam: The role of public-private partnerships. Asian Economic Policy Review, 20(1): 34-47.

[34] Ministry of Agriculture and Rural Development. (2023). National adaptation plan for climate-resilient agriculture. Government of Vietnam.

[35] Hung Yen Provincial People Committee. (2022). Report on the strategy of environmental assessment of Hung Yen Province. A plan for the period 2021-2030 and a vision to 2050.

[36] IDRBT. (2013). Green banking initiatives of Indian banking sector. Institute for Development and Research in Banking Technology.