Dhahir Habib Bahedh*![]() | Suhail AL-Tamimi

| Suhail AL-Tamimi![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

In response to changes and challenges in the business environment, many global and local companies have sought to adopt sustainability due to stakeholder demands for sustainable practices in their operations. This study aims to explore the extent to which the general company for fertilizers industry meets economic, social, and environmental sustainability requirements, according to the latest edition of the GRI standards. To achieve this aim, a descriptive analytical methodology and a checklist were used; interviews were conducted with department and division heads to collect data and information relevant to the study. The checklist was designed in accordance with the GRI's economic, environmental, and social standards to determine the extent to which the study sample met these requirements. The results revealed that the level of meeting the economic sustainability requirements was 48%, environmental sustainability 33%, and social sustainability 61%. This study concludes that the fertilizer company prioritizes social sustainability over economic or environmental sustainability. This study contributes to bridging the research gap on this topic, as a review of previous local literature indicated the absence of a single study addressing this issue in the Iraqi manufacturing industries sector. Therefore, this study is the only one at the local level.

economic sustainability, environmental sustainability, social sustainability, GRI standards, Iraq

Rapid economic expansion and growth have had severe consequences, including environmental damage and pollution. This is confirmed by Yale University, Columbia University, and the Global Economic Forum in their 2018 report titled (Global Environmental Performance Indicators 2018), which argues that the globe is still a long way from meeting environmental goals [1]. This is causing the Earth's temperature to rise dramatically at the moment, putting the entire world community in danger both now and in the future; companies in several sectors, particularly the industrial sector, emit pollutants into the atmosphere, which is the main source of environmental pollution and global warming [2]. The Brundtland Report in 1987 solidified the international focus on protecting the Earth and the planet from degradation; still, the environment and its relationship to economic growth and social justice were not a priority on international and national agendas until the late 1980s [3-5]. As a result, sustainability developed in the Brundtland Report and quickly became the fundamental notion in debating humanity's relationship with the physical environment; this concept is now widely acknowledged and regarded as a basic metric for evaluating humanity's actions [6]. Sustainable development has made firms realise they affect more than just profits; as a result, modern company executives are beginning to support their organisations in ways other than financial performance; company strategy plans must include the social, economic, and environmental implications of their activities, as business sustainability is a worldwide issue [7]. Sustainability involves adherence to natural laws, economic and environmental equilibrium, social advancement, and the shift to renewable energy and a circular economy to mitigate climate change and fossil fuel emissions [8, 9]. The UN Plan for Planet Earth, which many nations have committed to achieving, promotes a sustainable planet for all current and future generations by being a goal of all development goals, which achieves permanent social and economic benefits for society and the planet [10-12]. Consequently, both domestic and international investors are exerting a growing amount of pressure on countries and corporations to evaluate the social and environmental consequences of their operations in addition to their economic impacts. This necessitates the implementation of specific sustainability standards or indicators, such as the Global Reporting Initiative (GRI) Standards, which enable companies to demonstrate their economic, social, and environmental sustainability performance for the purposes of transparency, accountability, and corporate environmental sustainability [13].

As a result, businesses, particularly industrial businesses, must consider all aspects of sustainability using their ethical commitment to safeguarding the environment and society from the pollution caused by their manufacturing and production activities. For this reason, Southern Fertilizers General Corporation was selected since it is a significant corporation in the manufacturing industry sector and a vital source of money for the state. In addition, it is a significant contributor to environmental pollution and ozone depletion due to the greenhouse gases that it emits. In order to address all of the issues it is confronted with, including the pressure from investors or government agencies that demand businesses to comply with environmental laws and regulations, all of its activities and practices must be sustainable inside the company.

The study problem was represented in the following question:

(What is the level of Southern Fertilizer Company’s compliance with the requirements of economic, environmental, and social sustainability according to GRI standards?)

The study's importance comes from knowing the Southern Fertilizers Company's commitment to sustainable development and its role in reducing the risks of environmental damage to society and the environment and global warming emissions, as well as its commitment to government laws and legislation and global sustainability guidelines, including GRI standards.

This research seeks to examine the extent to which the sample company fulfills sustainability standards, which is critically significant in the Iraqi setting. This study examined many prior investigations about the local environment and identified a research gap that has been neglected by all local studies, especially with the sample of this research. This study is the inaugural local investigation designed to address this research gap.

The study is organized as follows: Section 2 presents the theoretical basis; Section 3 presents a literature review; Section 4 presents the study methodology; Section 5 presents the results; Section 6 presents the conclusions; Section 7 presents the implications and limitations; and Section 8 presents the recommendations.

2.1 Economic sustainability

Hicks, an economist, came up with the idea of economic sustainability, which means a production system that meets current needs without putting future needs at risk. In the past, traditional economists thought that natural resources would never run out and that the market would do a good job of allocating resources; they also thought that economic growth would make it easier to use technology to replace natural resources that were used up during production; but now we know that natural resources are limited and that the growth of the economy has put pressure on the natural resource base [14]. Coronato [15] defines economic sustainability as the capacity of the economic system to produce sustainable growth in economic indications, namely the ability to generate capital and employment to support societal livelihoods. Furthermore, it aims to boost individuals' well-being by increasing their share of goods and services while reaching the highest economic efficiency level through efficient resource utilization [16].

2.2 Environmental sustainability

The primary goal of environmental sustainability is to preserve the environment, which means that companies will face challenges like climate change, environmental degradation, and their environmental footprint, so all of their operational actions must be sustainable [17]. The ecological balance of the Earth is significantly strained due to the increasing demand for natural resources and biological diversity, which is exacerbated by advancements in the industry and the proliferation of globalization inside the economy; furthermore, the utilization of these natural resources is not sustainable over the long term, as it produces complex environmental challenges [18]. Environmental sustainability involves corporate initiatives aimed at safeguarding the environment and natural resources; it includes minimizing environmental impacts, decreasing resource consumption and biodiversity decline, and averting significant environmental harm from pollution, diminished ozone layer, and greenhouse gas emissions [19]. Hence, the environmental challenge confronting partnerships is formulating suitable strategic plans by their experts to uphold essential environmental practices and functions associated with their operations, thereby reducing the potential environmental harm to society and the ecosystem [20, 21].

2.3 Social sustainability

Social sustainability pertains to the effects of a company's operations on the social systems within its sphere, encompassing aspects such as equitable labor practices, human rights, health, security, public services, education, and training, with the objective of fostering a society grounded in universal well-being standards [4]. It also covers the ideas of justice, accessibility, empowerment, cultural identity, and institutional stability. Thus, its fundamental essence shows that humans and society in general are important because sustainable development is linked to human beings and works to protect society from the environmental damage surrounding it [22]. Accordingly, social sustainability encompasses long-term efforts that impact society's well-being. These efforts include protecting human rights, engaging in charitable initiatives, and promoting employee well-being in areas such as employee health, training and skills development, work practices, workplace injuries and illness, and workplace discrimination; the primary goal of social sustainability is to maintain positive social values for both individuals and society [23, 24]. Another section of the literature also construed the social dimension as the organization's obligation to stakeholders, particularly employees, society, consumers, and suppliers [25, 26].

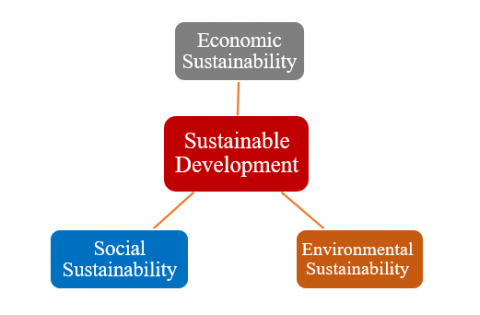

Therefore, as shown in Figure 1 below, achieving sustainable development requires integration between its essential dimensions. Sustainability cannot be achieved based on one dimension without the other dimensions.

Figure 1. Dimensions of sustainable development

Source: prepared by researchers

2.4 GRI

Companies worldwide now see sustainability as important, so they must produce sustainability reports that explain their efforts; they also have to follow standards that meet all the requirements, and the GRI standards are some of the best and most widely used worldwide for sustainability compliance [27]. The GRI standards are the dominant framework for preparing sustainability reports, illustrating the degree of firms' dedication to sustainable performance, specifically in understanding and communicating their implications about sustainability [28]. Integrating all dimensions of sustainability is crucial because companies that disclose all their sustainable activities gain a competitive advantage in this rapidly changing business environment. Therefore, companies need standards that can be relied upon to help them meet these challenges. GRI standards are the best choice because they enhance the credibility and reliability of sustainability information, giving stakeholders an impression of the legitimacy of the company’s existence in conducting its business in the environment in which it operates [29]. Sustainability reporting is now a prevalent practice among large corporations, particularly with the introduction of guidelines by the (GRI) to enhance the comparability and reliability of disclosures about social, environmental, and economic matters [30]. In addition, it serves as a mechanism that enables stakeholders to hold powerful actors accountable because it is a tool for measuring and evaluating the sustainable performance of companies; as a result, companies use it to demonstrate their commitment to sustainability [31].

Accordingly, this study will rely on the latest edition of the GRI standards issued in 2021, which will allow us to assess the Southern Fertilizer Company’s compliance with economic, environmental, and social sustainability.

This section reviews the most important previous studies at the local and international levels, which researchers contributed to, and which are related to this study. We note that the research gap for this study is determined by reviewing these studies, the aspects that were focused on, and the sectors in which they were researched.

3.1 GRI in the context of Iraq

Most studies focused on specific sectors; for example, Al Kaab and Wahhab [32] performed a study assessing the degree of sustainability dimension transparency across the banks in the sample listed on the Iraq Stock Exchange while also evaluating the influence of this disclosure level on market returns; the study found that the level of sustainability information given for the sample was way too low; it also found a strong link between the market returns of the bank's shares in the sample and the level of sustainability information given. The research conducted by Oleiwi et al. [33] sought to identify the factors influencing the preparation of sustainability accounting reports across economic, environmental, social, and governance aspects per GRI-G4 for all firms listed on the Iraq Stock Exchange; the findings of this study reveal that all sectors within the Iraq Stock Exchange experience disparities and deficiencies in the preparation of sustainable accounting reports, highlighting their limited contribution to sustainable development furthermore, various factors influence the decline and inconsistency in the quality of these reports, including sector type, disclosure regulations adhered to in the market, and the accounting system implemented. The research conducted by Ali et al. [34] sought to examine the influence of sustainability disclosure based on GRI indicators on the financial choices of investors in banks and industrial sectors listed on the Iraq Stock Exchange; the findings indicated no statistically significant effect of sustainability disclosure on the economic decisions of the investor sample studied. The study Al-Shammari [35] emphasises the importance of the (GRI) in improving sustainability reporting among firms listed on the Iraq Stock Exchange; it underscores that implementing GRI standards enhances the quality of financial and non-financial information, facilitating informed decision-making for users; the study indicates that applying GRI criteria aids economic entities in risk management and strategic planning, offering a holistic performance perspective; recommendations entail acquiring the requisite qualifications to implement GRI to guarantee valuable information for stakeholders efficiently. According to their investigation, AL-Janabi et al. [36] examined the commitment of UAE and Iraqi banks to sustainable development along economic, social, and environmental dimensions as measured by the GRI-G4; the study also looked at how this commitment affected the banks' financial performance the results showed that 57% of UAE banks were committed to sustainability, while 17% of Iraqi banks were; When it came to the impact of sustainability on financial performance, the study found that economic and social dimensions had a positive effect, while environmental dimensions had a negative effect. The study by Ali et al. [37] focused on evaluating Fadak Agricultural Company's sustainable performance according to its GRI standards; the study concluded that Fadak Agricultural Company has a weak interest in economic, environmental, and social sustainability. Aljajawy et al. [38] conducted a study on the level of application of sustainability reports according to GRI standards on the economic, environmental, and social sustainability of Iraqi companies and found that the level of application of sustainability reports for the study sample companies was very weak, at 19.76%. While Muhi's study [39] showed the extent of the commitment of Iraqi companies listed in the Iraqi market to disclosing environmental performance according to GRI standards, this study concluded that most of the companies in the study sample had weak disclosure of environmental performance.

3.2 GRI in a global context

At the international level, the study by Matuszak et al. [40] aimed to evaluate the level of disclosure of environmental sustainability requirements according to GRI standards for a sample of Polish energy companies; this study concluded that the Polish energy companies in the study sample disclosed environmental sustainability at a low level. The research conducted by Tres et al. [41] revealed the extent of disclosure in sustainability reports for firms across diverse sectors listed on the Brazilian Stock Exchange, adhering to GRI standards; the findings indicated that the overall level of sustainability disclosure among the sampled companies was markedly low; however, this deficiency varied among firms, with those in the public services sector demonstrating superior disclosure practices compared to their counterparts. Khan et al. [42] studied sustainability disclosure according to GRI standards of companies listed on the Pakistan Stock Exchange from 2016 to 2020; this study found that companies focused more on economic sustainability disclosure, followed by environmental sustainability, while social sustainability disclosure was scanty. The study of Fadillah and Norhamida [43] was conducted on companies operating in the energy and financial sectors in the Indonesian Stock Exchange to determine the level of disclosure of GRI standards in sustainability reports; this study concluded that the level of disclosure of GRI standards in energy sector companies was higher than that of financial sector companies. The study of Yehezkiel et al. [44] conducted a study on companies operating in the energy sector and the basic materials industry in the United Kingdom, Germany, France, Indonesia, Malaysia, and Thailand; this study aimed to determine the level of disclosure of sustainability reports; this study concluded that the sustainability disclosure level in developed countries, according to GRI standards, is higher than that of developing countries and all sectors. The study of Laskar [45] aimed to determine the extent to which the non-financial companies listed on the Bombay Stock Exchange, the study sample, adhered to sustainability disclosure according to GRI standards; this study concluded that 79% of companies disclosed the requirements specified by GRI in their sustainability reports.

3.3 Research gap in the manufacturing industry sector

To identify the differences in this study and identify the research gap through an analysis of previous studies, we review these differences as follows:

·In terms of the sector: Previous studies show more significant interest in companies operating in various industries and less interest in companies operating in the industrial sector [33, 35, 37-45]. Studies focused only on banks operating in the financial sector [32, 34, 36, 43]. The current study differs from previous studies in that it focuses on the Iraqi state-owned Southern Fertilizer Company, one of the most important companies operating in the manufacturing industries sector; it is considered a vital economic resource for the country and significantly impacts the environment and the surrounding community. Therefore, studying this company in a developing country like Iraq is crucial to understanding its commitment to sustainability and its alignment with the Iraqi government's sustainability orientations. In contrast, local (Iraqi) studies have neglected this important sector.

·Regarding the GRI standards: Most previous studies focused on applying previous GRI standards versions and guidelines. In contrast, the current study used the latest version of the GRI standards issued in 2021, which has undergone many important updates, including the deletion of previously issued standards and requirements and the addition of new ones in their place. This update represents a fundamental difference and quality in the information related to sustainability, which is why this current study relied on it.

Based on the previous literature reviewed in the local environment [32-39], and the international environment [40-45], it is clear to us that the manufacturing industries sector has not been studied in all of these environments, to the best of the researchers' knowledge, particularly in the local environment. This research gap deserves to be addressed at the local level, considering the importance of this industry to the Iraqi economy while also causing enormous harm to the environment and society. Thus, this study fills a research gap by assessing whether the Southern General Company for Fertiliser Industry, one of the largest manufacturing companies, meets (GRI) economic, environmental, and social sustainability standards. We employed a descriptive method to precisely and thoroughly explain the phenomenon under research to achieve the best results. Thus, this approach is suitable to answer this study's concerns about whether the study sample fulfills the current GRI sustainability standards, investigates them, and comprehends them.

4.1 Study questions

The study's major question is: To what extent can the Southern Fertilizer Company's requirements for sustainability be met in accordance with the (GRI) standards?

This question involves the following sub-questions:

Question 1: To what extent can Southern Fertilizer Company's economic sustainability requirements be met according to the (GRI) standards?

Question 2: To what extent can Southern Fertilizer Company's environmental sustainability requirements be met according to the (GRI) standards?

Question 3: To what extent can Southern Fertilizer Company's social sustainability requirements be met according to the (GRI) standards?

4.2 Sample

The study population represents companies operating in the Iraqi manufacturing industries sector, while the study sample is limited to the Southern State Fertilizer Company as a case study. The reason for selecting this company is as follows:

1) The Southern State Fertilizer Company is one of the oldest companies producing nitrogenous fertilizer (urea). It was established in 1975 to support agricultural development goals. It contributes to meeting the fertilizer needs of the Iraqi market, thereby supporting the local economy and developing industrial production in the fertilizer industry according to international standards.

2) Being a large company, it has a significant environmental impact on society and the planet due to the greenhouse gas emissions it emits from its operations.

3) It aims to commit to continuous improvement and quality, reduce pollution, and increase environmental awareness among all employees within the company, making it a daily work culture.

Accordingly, Table 1 shows the target category of individuals in the study sample for the Southern General Company for Fertilizer Industry.

Table 1. Target category

|

Participant |

Workplace |

No. |

|

Manager |

Internal Control Department Manager |

1 |

|

Manager |

Finance Department Manager |

1 |

|

Manager |

Legal Department Manager |

1 |

|

Manager |

Human Resources Department Manager |

1 |

|

Manager |

Commercial Department Manager |

1 |

|

Manager |

Quality Department Manager |

1 |

|

Manager |

Occupational Safety Department |

1 |

|

Manager |

Marketing Department Manager |

1 |

|

Manager |

Quality Control Department Manager |

1 |

|

Manager |

Maintenance Department Manager |

1 |

|

Manager |

Security Permits Department |

1 |

|

Manager |

Production Plants Department |

1 |

|

Manager |

Warehouse Department |

1 |

|

Manager |

R&D Department |

1 |

|

Manager |

Information Center Department |

1 |

|

Total |

15 |

|

Source: prepared by researchers

4.3 Checklist

The checklist is one of the scientific research tools used to collect data and information related to the sample under study. Therefore, the researchers used it to examine the extent to which economic, environmental, and social sustainability requirements were met according to the GRI standards of the Southern Fertilizer Company. The checklist requirements, as shown in Table 2, consist of 320 requirements. These requirements, which were included in the checklist, were based on the same GRI standards and the latest edition issued in 2021 by the Global Sustainability Standards Board. Therefore, these requirements were divided into (3) axes, with the number of requirements in the first axis, represented by economic criteria, amounting to (46) requirements; the number of requirements in the second axis, represented by environmental criteria, amounting to (108) requirements; and the number of requirements in the third axis, represented by social criteria, amounting to (79) requirements.

Table 2. Economic, environmental, and social sustainability requirements according to GRI standards

|

Economic Sustainability Standards |

N |

|

Economic performance |

10 |

|

Presence in the market |

7 |

|

Indirect economic impacts |

5 |

|

Purchasing practices |

3 |

|

Anti-Corruption |

11 |

|

Anti-competitive behavior |

2 |

|

Taxes |

8 |

|

Total requirements for economic sustainability |

46 |

|

Environmental Sustainability Standards |

|

|

Materials |

4 |

|

Energy |

21 |

|

Water and liquid waste |

17 |

|

Biodiversity |

8 |

|

Emissions |

36 |

|

Waste |

16 |

|

Environmental assessment of the resource |

6 |

|

Total requirements for environmental sustainability |

108 |

|

Social Sustainability Standards |

|

|

Employment |

8 |

|

Relations between management and workers |

2 |

|

Occupational Health and Safety |

27 |

|

Training and Education |

4 |

|

Diversity and equal opportunities |

3 |

|

Non-discrimination |

2 |

|

Freedom of association and collective bargaining |

2 |

|

Child labor |

3 |

|

Coerced work |

2 |

|

Security practices |

2 |

|

Rights of indigenous peoples |

2 |

|

Local communities |

2 |

|

Social evaluation of the resource |

6 |

|

Public policy |

2 |

|

Customer health and safety |

3 |

|

Marketing and posters |

6 |

|

Customer privacy |

3 |

|

Total requirements for social sustainability |

79 |

Notes: N= represents the requirements for each sustainability dimension standard (economic, environmental, and social).

Source: prepared by researchers

4.4 Data collection and measurement

As shown in Table 1, we conducted field visits and personal interviews with study sample members to obtain data and information related to the study. We limited our review of the 2024 annual report and all other official documents, such as the management report and official internal documents, to answer the study questions through a checklist. Fulfillment of these requirements was supported by or relied upon by official documents. Access to documents was permitted during the interviews to ensure the objectivity and impartiality of the information in fulfilling the checklist requirements.

The level of met economic, environmental, and social sustainability requirements is measured by applying the following steps:

1. Examine the content of the 2024 Annual Report and other official documents of the Southern Fertiliser Company for 2024.

2. According to the checklist, the number (1) is assigned to each requirement that has been met, and the number (0) is assigned to each requirement that has not been met. Therefore, this binary scale (0,1) represents the basis for all requirements of the economic, social, and environmental sustainability standards that are met and those that have not been met to determine the extent to which the company in the study sample has met those requirements.

3. The met requirements for each sustainability criterion are added separately and divided by the overall standards for the same category, as shown in the equation below:

$\mathrm{SDR}_{\mathrm{it}}=\frac{N R_{i t}}{T N R}$

where, SDRit=The level of meeting sustainability requirements during the year; NRit=The number of requirements that were met during the year; TNR=The total number of requirements.

An illustrative example of the percentage of economic sustainability requirements that have been met is 22 out of a total of 46, which are calculated based on the equation shown below:

$\mathrm{SDR}_{\mathrm{it}}=\frac{22}{46} * 100 \%=48 \%$

The percentage (48%) represents the percentage of economic sustainability requirements that were met by the fertilizer company, and so the rest is calculated according to the above method.

5.1 Economic sustainability requirements of the southern general fertilizer company according to GRI standards

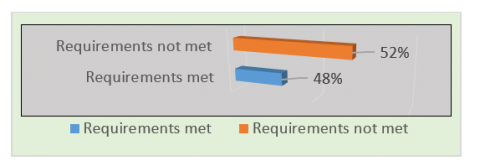

To answer the first research question, the sample company's economic sustainability requirements were analyzed using a checklist to establish the percentage of requirements fulfilled vs those not met. Figure 2 illustrates the results of the economic sustainability standards.

Figure 2. Percentage of economic sustainability requirements met and not met

Source: prepared by researchers

Figure 2 shows the percentages that were met and those that were not met for the economic sustainability standards. We note that the percentage of requirements that the company met in general for the southern fertilizer industry reached 48%, which is a very weak percentage, while the percentage of requirements that were not met reached 52%. The reason for this is the weak fulfillment of the requirements of the economic sustainability standards, as shown in Figure 3 below.

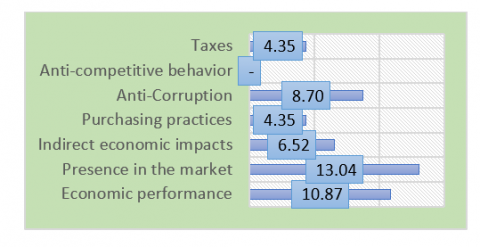

Figure 3. Percentage of economic sustainability requirements met

Source: prepared by researchers

From Figure 3 above, we can answer the first question and note that the lowest percentage of the requirements of the economic sustainability standards met was the anti-competitive behavior standard at (0%), and the reason for this is the lack of policies, laws, and instructions regarding the practice of such behavior. The highest percentage of the requirements of the economic sustainability standards met was the market presence standard at (13.043%), followed by the fulfillment of the requirements of the economic sustainability standards with the percentages shown in Figure 3 successively.

Based on the above, it is clear that the Southern Fertilizer Company has little interest in meeting the requirements of economic sustainability standards. This, in turn, negatively impacts its achievement of sustainable development itself. This gives various stakeholders the impression that the Southern Fertilizer Company has little interest in achieving or increasing economic and social welfare. In other words, it does not optimally utilize its available resources, which reduces its economic efficiency and consequently reduces the share of services and goods per individual in the company and society. Sustainable economic performance for sustainable development, on the other hand, focuses on providing real and effective guarantees for the purpose of achieving profitability for the company by achieving community welfare through the products and services it provides, which are characterized by high quality and competitive prices. As for the Southern Fertilizer Company, in this regard, it has a weak focus on sustainable economic performance for sustainable development.

The results of this study, in terms of weakness in meeting the requirements of economic sustainability according to GRI standards, amounting to 48%, are consistent with the studies by Oleiwi et al. [33] and Ali et al. [37] and differ from the studies by Khan et al. [42].

We recommend that the fertilizer company adhere to the requirements of economic sustainability and consider them when developing its strategic plans, making them a priority and making sustainability a prevailing business context to enhance its competitive position among competitors.

5.2 Environmental sustainability requirements for the southern fertilizer company according to GRI standards

To answer the second study question, the study sample company's environmental sustainability requirements were examined using the checklist, and Figure 4 shows the percentage of requirements met and those not met.

Figure 4. Percentage of environmental sustainability requirements met and not met

Source: prepared by researchers

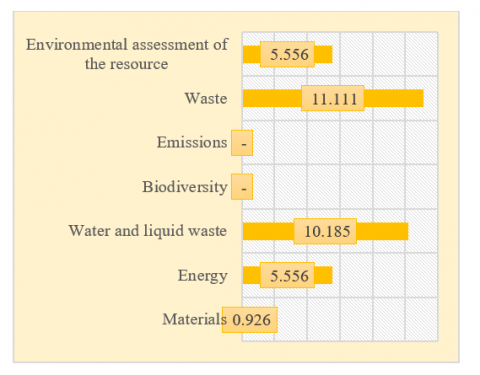

Figure 4 illustrates the percentages of compliance and non-compliance with environmental sustainability standards. We note that the company, in general, met 33% of the environmental sustainability standards, which is a very low percentage, while 67% of the requirements were not met. This is due, as Figure 5 below illustrates, to a lack of sufficient compliance with environmental sustainability standards.

Figure 5. Percentage of environmental sustainability

requirements met

Source: prepared by researchers

Through Figure 5 above, we can answer the second question and note that the lowest percentage of environmental sustainability standards met is the biodiversity standard at (0%), and the emissions standard at (0%). The reason for this is the lack of compliance with the laws that require the company to limit environmental damage from pollution and the lack of the required capabilities to reduce this with the lack of interest in environmental awareness. The highest percentage of environmental sustainability standards met is the waste standard at (11.111%), and after that comes the meeting of environmental sustainability standards with their percentages shown in Figure 5 successively.

Based on the above, it is clear that the Southern General Company for Fertilizer Industries has little interest in meeting environmental sustainability standards, which negatively impacts the achievement of sustainable development itself. This means that the Southern General Company for Fertilizer Industries has little interest in protecting the environment and natural resources from the damage caused by its activities. This has led to significant environmental deterioration due to the imbalance in the consumption of natural and non-natural resources, as well as its high consumption of non-renewable energy at the expense of renewable energy. Non-renewable energy consumption leads to significant and harmful emissions into the atmosphere and the ozone layer, such as the accumulation of methane, carbon dioxide, and other emissions. Therefore, sustainable environmental performance for sustainable development contributes to environmental preservation through optimal resource utilization, renewable energy consumption, and companies' reduction of harmful emissions. Regarding the Southern General Company for Fertilizer Industries, it has a weak focus on sustainable environmental performance for sustainable development.

The results of this study, in terms of the existence of a 33% weakness in meeting environmental sustainability requirements according to GRI standards, are consistent with the studies by Muhi [39] and Matuszak et al. [40] and Tres et al. [41] and differ from the studies by Laskar [45].

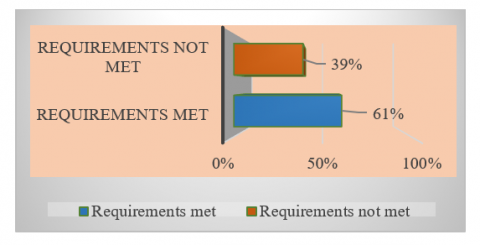

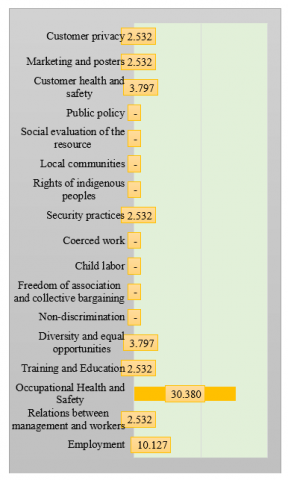

5.3 Social sustainability requirements for the Southern Fertilizer Company according to GRI standards

To answer the third study question, the study sample company's social sustainability requirements were examined using the checklist, and Figure 6 shows the percentage of requirements met and those not met.

Figure 6. Percentage of social sustainability requirements met and not met

Source: prepared by researchers

Figure 6 shows the percentages that were met and those that were not met for the social sustainability standards. We note that the percentage of requirements that the company met in general for the Southern Fertilizer Industry reached 61%, which is an average percentage. In comparison, the percentage of requirements that were not met reached 39%. The reason for this is to meet the requirements of the social sustainability standards, as shown in Figure 7 below.

Figure 7. Percentage of social sustainability requirements met

Source: prepared by researchers

From Figure 7 above, we can answer the third question and note that the lowest percentage of social sustainability standards met was the non-discrimination standard (0%), the freedom of association and collective bargaining standard (0%), the child labor standard (0%), the forced or compulsory labor standard (0%), the rights of Indigenous peoples standard (0%), the local communities standard (0%), the social assessment standard of suppliers (0%), and the public policies standard (0%). The reason for this is the lack of a clear policy, specific instructions, or standards that the company can apply to balance the requirements of social sustainability standards. Therefore, the fertilizer company must apply these standards to be more sustainable and pay attention to these aspects. The highest percentage of social sustainability standards met was the occupational health and safety standard (30.380%), followed by the fulfillment of social sustainability standards with the percentages shown in Figure 7 respectively.

Based on the above, it is clear that the Southern Fertilizer Company has a moderate level of interest in meeting the requirements of social sustainability standards, which is positively reflected in the achievement of sustainable development itself. This means that the Southern Fertilizer Company has a moderate level of interest in social aspects, such as its undertaking and contribution to charitable work for the surrounding environment, as well as reducing inequality to achieve social justice. It also focuses on employee care in various areas, such as employee health and safety from injuries and illnesses they are exposed to during their daily work at the workplace and employee training to develop their job skills and deliver the best possible performance. Sustainable social performance for social development focuses on these activities, which work to reduce the harmful social impacts on the company's operations in the community and resolve all issues and problems related to social issues. As for the Southern Fertilizer Company, it has a moderate level of interest in this aspect of sustainable social performance for sustainable development.

The results of this study are consistent with the percentage of sustainability requirements met according to GRI standards, which is 61%, with studies by Fadillah and Norhamida [43] and Laskar [45], and differ from studies Aljajawy et al. [38].

From the previous results, we note that the study sample company's highest compliance rate was with social sustainability standards, reaching 61%, compared to economic sustainability standards, which reached 48%, and environmental sustainability standards, which reached 33%. This is due to the company's commitment to laws, regulations, and procedures consistent with social sustainability standards. The company also places greater emphasis on and awareness of the social aspect than other aspects, given its profound and direct impact on employees, workers, and the surrounding environment.

This study aimed to explore the level of compliance with economic, social, and environmental sustainability requirements according to the latest GRI standards for the Southern Fertilizers Company. The purpose was to fill the research gap related to studying the dimensions of sustainability for one of the most important companies in the Iraqi manufacturing sector, which is the Southern Fertilizers Company. This is the only local study that addressed the dimensions of sustainability in this sector, as no previous local studies have addressed them. Furthermore, research addressing these dimensions within the manufacturing sector is rare regionally and internationally. The result of this study found that the level of compliance with economic sustainability requirements was 48% and environmental sustainability requirements were 33%, both of which are very weak. The level of compliance with social sustainability requirements was 61%, which is average, indicating that the Southern Fertilizers Company prioritizes social sustainability over economic and environmental sustainability. This is due to its commitment to the laws, instructions, and regulations that the company follows in its approach to the social aspect compared to the other aspects.

This study has implications for multiple stakeholders, including policymakers, practitioners, regulatory bodies, and sustainability oversight bodies, such as the National Energy Support and Emissions Reduction Initiative Taskforce, which represents the government in monitoring companies' sustainability performance to determine their alignment with the country's sustainability trends and their compliance with laws, regulations, and regulations related to environmental considerations and protection. Furthermore, the study can be used as a guide to assess the commitment of other companies to sustainability in this or other sectors, taking into account other sustainability-related impacts. An important implication of this study is the possibility of adopting these standards or issuing a local standard consistent with the GRI standards to evaluate companies' economic, environmental, and social sustainability. Performance, despite the findings of this study, has some limitations. The study is limited to the fertilizer company because it significantly impacts the environment and the surrounding community and is also a large company. Therefore, future research can consider the effects of other factors that may affect the performance of other companies, in addition to expanding the sample size to include other companies operating in the same sector or other sectors that have a significant environmental impact in Iraq.

Based on the results and conclusions, this study recommends the following:

1) It is essential for companies to pay greater attention to economic sustainability, as it is the foundation upon which they build their resources. They achieve this by optimizing the use of resources in their manufacturing operations. Furthermore, economic performance is of paramount importance to all stakeholders. Similarly, we have observed very little interest in environmental sustainability, which poses the greatest threat to the environment and society. Therefore, companies must pay greater attention to this aspect to preserve the surrounding environment and reduce emissions from their production processes as much as possible.

2) It is necessary to raise awareness of the importance of a culture of sustainability among employees and workers within the company and make it a constant working context.

3) This study recommends that local accounting regulatory bodies issue a comprehensive accounting standard on companies' economic, environmental, and social sustainability.

4) This study also recommends that government agencies enforce the implementation of environmental and social laws and encourage companies to implement them to protect the environment and society from environmental damage.

5) Further research should be conducted by researchers and academics in companies in this important sector to assess the level of sustainability implementation and shed light on it.

[1] Wu, J., Ding, Y., Zhang, F., Li, D. (2021). How to improve environmental performance of heavily polluting companies in China? A cross-level configurational approach. Journal of Cleaner Production, 311: 127450. https://doi.org/10.1016/j.jclepro.2021.127450

[2] Flayyih, H.H., Jawad, K.K., Al-Abedi, T.K. (2024). The role of environmental auditing in achieving sustainable development: Management systems as a mediator. International Journal of Sustainable Development and Planning, 19(4): 1253-1260. https://doi.org/10.18280/ijsdp.190403

[3] Tejedor-Flores, N., Galindo-Villardón, P., Vicente-Galindo, P. (2017). Sustainability multivariate analysis based on the global reporting initiative (GRI) framework, using as a case study: Brazil compared to Spain and Portugal. International Journal of Sustainable Development and Planning, 12(4): 667-677. https://doi.org/10.2495/SDP-V12-N4-667-677

[4] González, A.L., Martín, J.Á.C., Vaca-Tapia, A.C., Rivas, F. (2021). How sustainability is defined: An analysis of 100 theoretical approximations. Mathematics, 9(11): 1-20. https://doi.org/10.3390/math9111308

[5] Al.Tamimi, S. (2018). Accenting for renewable resources: Horizons and trends. Economic Sciences, 13(50): 105-116. https://www.iasj.net/iasj/download/0b51be586cdee34a

[6] Gray, R.H. (1994). Corporate reporting for sustainable development: Accounting for sustainability in 2000AD1. Environmental Values, 3(1): 17-45. https://doi.org/10.3197/096327194776679782

[7] Kumar, M., Raj, N., Singh, R.R. (2023). Ranking Indian companies on sustainability disclosures using the GRI-G4 framework and MCDM techniques. International Journal of Sustainable Development and Planning, 18(9): 2791-2799. https://doi.org/10.18280/ijsdp.180917.

[8] Duran, D.C., Gogan, L.M., Artene, A., Duran, V. (2015). The components of sustainable development - A possible approach. Procedia Economics and Finance, 26: 806-811. https://doi.org/10.1016/s2212 5671(15)00849-7

[9] Gakh, D. (2023). Societal patterns evolution model in development of economy, society, and environment. Journal of Research, Innovation and Technologies, 2(2): 142-161. https://doi.org/10.57017/jorit.v2.2(4).03

[10] Bexell, M., Jönsson, K. (2017). Responsibility and the United Nations’ sustainable development goals. Forum for Development Studies, 44(1): 13-29. https://doi.org/10.1080/08039410.2016.1252424

[11] Hasanov, R.I., Giyasova, Z., Azizova, R., Huseynova, S., Zemri, B.E. (2024). Long-term dynamics between human development and environmental sustainability: An empirical analysis of CO2 emissions in Azerbaijan. Challenges in Sustainability, 12(4): 273-280. https://doi.org/10.56578/cis120403

[12] Emina, K.A. (2021). Sustainable development and the future generations. Social Sciences, Humanities and Education Journal, 2(1): 57. https://doi.org/10.25273/she.v2i1.8611

[13] Kutay, N., Tektufekci, F. (2016). A new era for sustainable development: A comparison for sustainability indices. Journal of Accounting, Finance and Auditing Studies, 2(2): 70-95. https://doi.org/10.56578/jafas020204

[14] Basiago, A.D. (1998). Economic, social, and environmental sustainability in development theory and urban planning practice. The Environmentalist, 19: 145-161. https://doi.org/10.1023/A:1006697118620

[15] Coronato, M. (2020). The sustainability dimensions: A territorialized approach to sustainable development. Global Journal of Human-Social Science, 20(10): 23-31. https://doi.org/10.34257/gjhsshvol20is10pg2.

[16] Mohammed, M.J., Faris, A.H. (2023). The impact of the disclosure quality of sustainability information on financial performance. Journal of Business Economics for Applied Research, 5(2): 9-27. https://www.iraqoaj.net/iasj/article/282032

[17] Andersson, S., Svensson, G., Molina-Castillo, F.J., Otero-Neira, C., Lindgren, J., Karlsson, N.P.E., Laurell, H. (2022). Sustainable development—Direct and indirect effects between economic, social, and environmental dimensions in business practices. Corporate Social Responsibility and Environmental Management, 29(5): 1158-1172. https://doi.org/10.1002/csr.2261

[18] Atif, M., Bottura, M., Yasin, R. (2024). Public issues and public expectations: Disentangling responsibility discourse dimensions in CSR and sustainability books. European Management Journal, 42(6): 957-967. https://doi.org/10.1016/j.emj.2023.07.008

[19] Bahedh, D.H., Al-Tamimi, S.A. (2024). Measuring the environmental dimension of sustainable development according to the GRI standards: A proposed model. International Journal of Humanities and Educational Research, 6(5): 1-21. http://doi.org/10.47832/2757-5403.28.1

[20] Liu, X., Schraven, D., de Bruijne, M., de Jong, M., Hertogh, M. (2019). Navigating transitions for sustainable infrastructures-The case of a new high-speed railway station in Jingmen, China. Sustainability, 11(15): 4197. https://doi.org/10.3390/su11154197

[21] Al-Tamimi, S.A. (2022). Towards integrated management accounting system for measuring environmental performance. AgBioForum, 24(2): 149-161. https://agbioforum.org/menuscript/index.php/agb/article/view/139/83.

[22] Mensah, J. (2019). Sustainable development: Meaning, history, principles, pillars, and implications for human action: Literature review. Cogent Social Sciences, 5(1): 1653531. https://doi.org/10.1080/23311886.2019.1653531

[23] Dempsey, N., Bramley, G., Power, S., Brown, C. (2011). The social dimension of sustainable development: Defining urban social sustainability. Sustainable Development, 19(5): 289-300. https://doi.org/10.4324/9781351276481

[24] Chow, W.S., Chen, Y. (2012). Corporate sustainable development: Testing a new scale based on the mainland Chinese context. Journal of Business Ethics, 105(4): 519-533. https://doi.org/10.1007/s10551-011-0983-x

[25] Antolín-López, R., Delgado-Ceballos, J., Montiel, I. (2016). Deconstructing corporate sustainability: A comparison of different stakeholder metrics. Journal of Cleaner Production, 136: 5-17. https://doi.org/10.1016/j.jclepro.2016.01.11

[26] Linnenluecke, M.K., Russell, S.V, Griffi, A. (2009). Subcultures and sustainability practices: The impact on understanding corporate sustainability. Business Strategy and the Environment, 18(7): 432-452. https://doi.org/10.1002/bse.609

[27] Larrinaga, C., Bebbington, J. (2021). The pre-history of sustainability reporting: A constructivist reading. Accounting, Auditing and Accountability Journal, 34(9): 131-150. https://doi.org/10.1108/AAAJ-03-2017-2872

[28] Luo, L., Tang, Q. (2023). The real effects of ESG reporting and GRI standards on carbon mitigation: International evidence. Business Strategy and the Environment, 32(6): 2985-3000. https://doi.org/10.1002/bse.3281

[29] Bais, B., Nassimbeni, G., Orzes, G. (2024). Global reporting initiative: Literature review and research directions. Journal of Cleaner Production, 471: 143428. https://doi.org/10.1016/j.jclepro.2024.143428

[30] Machado, B.A.A., Dias, L.C.P., Fonseca, A. (2021). Transparency of materiality analysis in GRI-based sustainability reports. Corporate Social Responsibility and Environmental Management, 28(2): 570-580. https://doi.org/10.1002/csr.2066

[31] Hervieux, C., McKee, M., Driscoll, C. (2017). Room for improvement: Using GRI principles to explore potential for advancing PRME SIP reporting. International Journal of Management Education, 15(2): 219-237. https://doi.org/10.1016/j.ijme.2017.03.011

[32] Al Kaab, A.F.A.B., Wahhab, A.M.A. (2023). Evidence from Iraqi banks on the reporting of sustainability determinants and their impact on market returns. Technium Social Sciences Journal, 44: 79-102. https://doi.org/10.47577/tssj.v44i1.9053

[33] Oleiwi, Z.H., Mohsin, N.M.R., Yaqoob, I.I. (2020). Determinants of sustainability reporting under a global reporting initiative: Empirical evidence from Iraq. International Journal of Innovation, Creativity and Change, 10(10): 753-773. https://www.ijicc.net/images/vol10iss10/101019_Oleiwi_2020_E_R.pdf.

[34] Ali, M.N., Hameedi, K.S., Almagtome, A.H. (2019). Does sustainability reporting via accounting information system influence investment decisions in Iraq? International Journal of Innovation, Creativity and Change, 9(9): 294-312. https://www.ijicc.net/images/vol9iss9/9925_Ali_2019_E_R.pdf.

[35] Al-Shammari, S.A.N. (2022). The role of GRI standards in reporting the dimensions of sustainable development - An applied study in a number of local companies on the Iraq Stock Exchange. Journal of Economics and Administrative Sciences, 28(133): 200-215. https://doi.org/10.33095/jeas.v28i133.2364.

[36] AL-Janabi, A.M.A., Saei, M.J., Hesarzadeh, R. (2024). The impact of adherence to sustainable development, as defined by the global reporting initiative (GRI-G4), on the financial performance indicators of banks: A comparative study of the UAE and Iraq. Journal of Risk and Financial Management, 17(1): 17. https://doi.org/10.3390/jrfm17010017

[37] Ali, R.S., Falah, H.J., Ali, A.F. (2024). Sustainable performance evaluation according to the global reporting initiative (GRI) standards at Fadak Agricultural Company. Journal of Accounting and Financial Studies, 19(68): 247-261. https://doi.org/10.34093/qdn60455

[38] Aljajawy, T.M.A., Dolab, Y., Alkhfajy, E.J.A. (2023). The role of global reporting initiative (GRI) for achieving sustainability reporting. In Explore Business, Technology Opportunities and Challenges After the COVID-19 Pandemic( ICBT 2022), pp. 273-288. https://doi.org/10.1007/978-3-031-10212 7_24

[39] Muhi, S. (2024). Analysis of the Reflection of accounting disclosure on environmental performance on the quality of sustainability reports. Warith Scientific Journal, 6(18): 445-460. https://doi.org/10.57026/wsj.v6i18.240

[40] Matuszak, Ł., Różańska, E., Szczepankiewicz, E.I. (2025). Assessment of the compliance of environmental disclosures by energy companies using GRI standards with European sustainability reporting standards: A case Study. Sustainability, 17(8): 3380. https://doi.org/10.3390/su17083380

[41] Tres, P., Di Domenico, D., Tres, N. (2023). Level of disclosure in sustainability reports in accordance with the global reportinginitiative (GRI). Revista Ambiente Contábil, 15(2): 1-18. https://doi.org/10.21680/2176-9036.2023v15n2id33068

[42] Khan, I., Fujimoto, Y., Uddin, M.J., Afridi, M.A. (2023). Evaluating sustainability reporting on GRI standards in developing countries: A case of Pakistan. International Journal of Law and Management, 65(3): 189-208. https://doi.org/10.1108/IJLMA-01-2022-0016

[43] Fadillah, R.A., Norhamida, H. (2024). Comparison of disclosure levels of GRI standards on companies listed on the IDX (Case study energy and financial sector). Proceeding of the 7th International Seminar on Business, Economics, Social Science, and Technology (ISBEST4), pp. 1-5. https://doi.org/10.33830/isbest.v4i1.3351

[44] Yehezkiel, R.Y., Dwi Astuti, C., Noor, I.N. (2023). GRI standards-based sustainability reporting disclosure practices across countries. Media Riset Akuntansi, Auditing & Informasi, 23(2): 241-256. https://doi.org/10.25105/mraai.v23i2.17959

[45] Laskar, N. (2024). Assessing the drivers of corporate sustainability performance disclosures using the global reporting initiative (GRI) G4 framework. Journal of Risk and Financial Management, 17(11): 513. https://doi.org/10.3390/jrfm17110513