Ahmad Albar Tanjung*![]() | Muliyani

| Muliyani![]() | Irsad Lubis

| Irsad Lubis![]() | M. Syafii

| M. Syafii![]() | Ikbar Pratama

| Ikbar Pratama![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Regional economic growth is one of the key indicators of national economic development. This investigation is conducted to assess the nexus among human capital, monetary policy, population, investment, and regional economic growth in Indonesia with the comparison of the West and East regions. To assess the dynamic nexus among regional economic growth, human capital, monetary policy, population size, and investment, Indonesia's 34 provinces were grouped into two regions: the western and eastern parts. The research period is 2016 to 2023 using panel data. The model applied is a dynamic panel model, and the estimation method used is the generalized method of moments (GMM). The results indicate that previous-period regional economic growth, human capital, investment, and population size influence economic growth across all provinces, as well as in the western and eastern sub-regions. However, the magnitude of change varies across sub-regions. In the eastern region (KTI), monetary policy and population size have no meaningful effects on economic growth. These findings suggest that, in the long run, Human resource development should be the focus of government through education, research, and development to enhance regional economic growth. Additionally, investment should take environmental sustainability into account to support sustainable development.

economic growth, human capital, monetary policy, population, investment, GMM model, regional

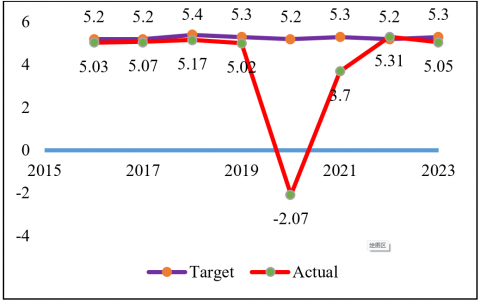

The goal of national development is to provide welfare for its people. National development must be supported by strong national economic development. The fundamental economic indicators used to measure the success of economic development are economic growth [1], price stability [2], and employment absorption. Economic growth is a crucial issue for a country's economic activities. Moreover, economic growth constitutes the eighth of 17 Sustainable Development Goals (SDGs). Action and collaboration of developing and developed countries in global partnerships are essential to achieve the SDGs Goal are to furnish a unified framework conducive to peace and prosperity for people. The development of Indonesia's economic growth from 2016 to 2023, as depicted in Figure 1, shows that the targeted economic growth has not been achieved. This is evident from the actual growth graph, which remains below the set economic growth targets. The most significant deviation from the target occurred in 2020 when the COVID-19 pandemic severely impacted all aspects of life in Indonesia, including the economic sector [3]. The target for 2020 was set at 5.2 percent, while the actual realization was only -2.07 percent. Indonesia's economic growth began to recover after the COVID-19 pandemic, this was marked by the start of positive economic growth from 2.07 percent in 2020 to 5.05 percent in 2023. This rebound was influenced by several factors, namely: monetary policy, namely interest rate cuts and liquidity easing; fiscal policy through economic stimulus, and social transfers [4], rising global commodity prices [5], such as coal and CPO, and increasing domestic and foreign investment, as well as improving the economies of Indonesia's trading partners.

Figure 1. Development of targets and actual of Indonesian Economic Growth 2016-2023

At the regional level, differences in actual economic growth among provinces are also noticeable. For instance, in 2023, one province in the western region of Indonesia exceeded the national economic growth target—Bali, with an economic growth rate of 5.71 percent. Meanwhile, in the eastern region of Indonesia, five provinces recorded economic growth above the national level in 2023. These provinces include East Kalimantan at 6.22 percent, North Sulawesi at 5.48 percent, North Sulawesi recorded a growth rate of 5.48 percent, Central Sulawesi at 11.91 percent, Southeast Sulawesi at 5.35 percent, and North Maluku at 20.49 percent. Apart from these provinces, economic growth remained below the national economic growth target.

Consistent with the neo-classical theory, long-term economic growth is influenced by capital accumulation and technology. Furthermore, the theory of endogenous growth stipulates that economic growth is concomitantly influenced by human capital and innovation [6]. Additionally, Keynesian Liquidity Theory and monetarist theory suggest that economic growth is influenced by monetary policy [7, 8], population [9], and investment [10]. Developing countries, including Indonesia, need to increase investment in education to enhance human capital and drive better economic growth [11]. In recent years, several empirical studies conducted in different countries worldwide have shown that Economic growth is meaningfully driven by improvements in human capital, with the relationship being both substantial and statistically validated. For instance, Gabriel and Darcilio [12] found in 32 developing countries, Sebki [13] found in forty developing countries, Fashina et al. [14] found in Nigeria, Han and Lee [15] found in Korea; Sultana et al. [16] found in 141 developing and developed countries; Opoku et al. [17] found in Africa.

Furthermore, researchers have examined the relationship between monetary policy and economic growth through empirical investigations. For example, Akalpler and Duhok [18] found that monetary policy positively influenced economic growth in Malaysia, Michael et al. [19] found a positive and significant effect in five African countries, Empirical findings by Agustina and Daryono [20] revealed that economic growth is positively and significantly influenced by monetary policy when proxied by money supply, and Gabriel and Darcilio [12] found a similar effect in Mozambique. Likewise Islam et al. [21] reported that Empirical studies conducted in both developing countries (e.g., Bangladesh) and developed nations (e.g., the UK) indicate that economic growth responds positively and significantly to monetary policy shocks.

Conversely, some empirical studies present contrasting findings. For instance, Matousek and Tzeremes [22] found that human capital negatively affects economic growth. Similarly, empirical research by Awan and Naseem [23] indicated that human capital exerts a negative influence on economic growth. Monetary policy, as proxied by the money supply, was found to have a negative effect on economic growth [24]. Furthermore, some studies indicate that population size negatively impacts economic growth [25]. While a negative relationship between investment and economic growth was also supported [26].

This research aims to assess the nexus among human capital, monetary policy, and regional economic growth in Indonesia. Although much previous research has analyzed the relationship between human capital, monetary policy, and economic growth, most have been conducted separately. This research integrates endogenous economic growth theory with Keynesian Liquidity Theory and Monetarist Theory. The novelty of this study is to integrate monetary policy, specifically money supply, as a variable that affects regional economic growth into the model. And want to prove whether there is a "catch-up effect" in the Eastern region of Indonesia. This aspect is the main differentiator between this research and previous studies.

Additionally, this study compares the western and eastern regions of Indonesia to provide a broader perspective on regional economic disparities. This comparison is conducted because there are differences in the sectors driving the economy of each region. The Western Region of Indonesia has a higher level of development compared to the Eastern Region of Indonesia. Sectors that develop in the western region are industry, trade, and service sectors. While Eastern Indonesia is still dominated by natural resource-based sectors, Eastern Indonesia also has limitations in infrastructure and economic connectivity. So that the results of this study become one of the references to assist the government in designing development policies that are more equitable and in accordance with the economic characteristics of each region.

Economic growth is a topic that remains a constant subject of discussion. Human capital, population, investment, monetary policy, and macroeconomic variables are key determinants of economic growth. During the age of digital transformation (Industry 4.0) and the transition toward a super-smart society (Society 5.0), the role of human capital has become increasingly important in the labor market [27], as skilled human capital can enhance productivity [28]. Currently, human capital plays an essential role in achieving sustainable economic growth [29]. Several empirical studies have been conducted by previous researchers. Sarwar et al. [30] analyzed the impact of human capital on economic growth using the Generalized Method of Moments (GMM) estimation method, and the results showed that human capital has a positive effect on economic growth. A study emphasizing BRICS countries (Brazil, Russia, India, China, and South Africa) utilizing panel data further substantiates this notion, demonstrating that human capital positively affects economic growth [31]. Otherwise, monetary policy is also an essential part of economic stability and creating a conducive environment for growth. Senbet [32] studied the relative impact of fiscal and monetary policies on U.S. economic growth using the Vector Autoregressive (VAR) model, with money supply and the Federal Reserve's benchmark interest rate as proxies for monetary policy. The results showed that monetary policy has a positive influence on economic growth.

Population size also affects economic growth. An increase in population leads to economic growth, as evidenced by research conducted by Brida et al. [33]. Cayssials et al. [34] confirmed this by conducting a causality analysis of population size and economic growth in 111 countries, finding that as the population increases, economic growth also rises. The Endogenous Growth Model also indicates that the relationship between population and economic growth is positive [35].

Investment is another key factor influencing economic growth. In a study on the impact of investment on economic growth in 63 Vietnamese provinces over the period 2000–2020, Nguyen and Nguyen [36] found that investment positively correlates with economic growth. Hayat [37] explored the effects of both domestic and foreign direct investment on economic growth in 104 countries with high, middle, and low incomes, concluding that investment positively influences economic growth.

3.1 Data and variables

Adopting a quantitative framework, the study examines the interplay of human capital, monetary policy, population dynamics, and investment in provincial economic development in Indonesia. Secondary data from 34 provinces over an eight-year period (2016–2023) are analyzed through a panel data approach, merging longitudinal and cross-provincial dimensions.

The 34 provinces are categorized into two regions: Western Indonesia [KBI] and Eastern Indonesia [KTI]. Western Indonesia spans 17 provinces, covering: Sumatra (Aceh, North Sumatra, West Sumatra, Riau, Jambi, South Sumatra, Bengkulu, Lampung, Bangka Belitung, Riau Islands), Java (Jakarta, West Java, Central Java, Yogyakarta, East Java, Banten), and Bali.

Eastern Indonesia spans 17 provinces across five major regions, covering: Nusa Tenggara (West Nusa Tenggara, East Nusa Tenggara), Kalimantan (West Kalimantan, Central Kalimantan, South Kalimantan, East Kalimantan, North Kalimantan), Sulawesi (North Sulawesi, Central Sulawesi, South Sulawesi, Southeast Sulawesi, Gorontalo, West Sulawesi), Maluku (Maluku, North Maluku), Papua (West Papua, and Papua).

The operational definitions of the variables used in this study can be found in Table 1.

Table 1. Variable definitions and specifications

|

Variables |

Description |

Sources |

|

PDRB |

Real Gross Regional Domestic Product (GRDP), Constant 2010 Price [in billions of Rp] |

https://www.bps.go.id |

|

JPP |

Population Size (in thousands of people) |

https://www.bps.go.id |

|

HDI |

Human Development Index (IPM) – Comparison of longevity, literate, educated, and affluent populations |

https://www.bps.go.id |

|

INV |

Foreign Direct Investment plus Domestic Direct Investment [in billions of Rp] |

https://www.bps.go.id |

|

JUB |

Money Supply (Narrow Definition) in the Region [in billions of Rp] |

https://www.bi.go.id |

3.2 Data analysis methodology

To analyze the role of human capital, monetary policy, and additional factors (investment and population) in Indonesia’s regional economic growth, this study adopts a dynamic panel model estimated via the GMM. The dynamic aspect of the model captures the persistence of economic growth by accounting for the influence of past growth rates on current performance [38], Furthermore, the GMM methodology addresses endogeneity concerns by utilizing lagged variables as instruments, a strategy well-documented in econometric literature [39, 40]. Another advantage of GMM is that it is able to provide more estimates than other methods, flexible in the use of instruments, able to overcome correlation bias between periods and able to accommodate individual heterogeneity.

The general form of the dynamic panel model is represented by the following Eq. (1):

$y_{i, t}=\delta y_{i, t-1}+\beta x_{i t}^{\prime}+u_{i t}$ (1)

The following Eq. (2) is used to investigate the nexus among human capital, monetary policy on regional economic growth:

$\begin{gathered}L P D R B_{i t}=\alpha_0+\alpha_1 L P D R B_{i, t-1}+\alpha_2 L J P P_{i, t}+ \alpha_3 L H D I_{i, t}+\alpha_4 L I N V_{i, t}+\alpha_5 L J U B_{i, t}+U_{i, y}\end{gathered}$ (2)

where, $L P D R B_{i t}$ is Logarithm Real Gross Regional Domestic Product, $L P D R B_{i, t-1}$ is the value of the logarithm real gross regional domestic product, $L J P P_{i, t}$ is the logarithm regional population, $L H D I_{i, t}$ is logarithm regional human development index, $LINV_{i, t}$ is logarithm total regional investment both of foreign direct and domestic investment. $L J U B_{i, t}$ is logarithm money supply (M1) which is a proxy for monetary policy.

The GMM method has two types: first-difference GMM and system GMM. First-difference GMM often produces biased and inaccurate results, and to address this issue, system GMM is used. Therefore, this study applies the system GMM method. The implementation of system GMM enhances the efficiency of estimators. To determine the best model, the estimated model must meet three criteria namely Instrument Validity – This is tested using the Sargan test, if the p-value is smaller than the significance level ($\alpha$=0.05) then the instrument is considered invalid, if the p-value is greater than $\alpha$ then it can be said that the instrument is valid; Consistency of Results – The test used is AR (2), where a p-value of AR (2) > 0.05 indicates that the results are consistent; and Unbiased Results – The estimated coefficient of the lagged dependent variable in FD-GMM or Sys-GMM should lie between the estimated coefficients of the Fixed Effects Model (FEM) and Pooled Least Squares (PLS).

4.1 Descriptive analysis

Table 2 reports the result of the descriptive statistical analysis for all the variables. All are variables used in this research in logarithm form.

A relatively low standard deviation for the human capital variable (LHDI) indicates less variation in human capital across provinces in Indonesia. Additionally, the coefficient of variation is an important aspect of descriptive analysis, as it represents the percentage of the standard deviation divided by the mean [8]. The variables LJPP, LINV, and LJUB have higher coefficients of variation, at 11.99%, 11.55%, and 13.7%, respectively, indicating a high level of data dispersion or greater heterogeneity. Meanwhile, the variables LPDRB and LHDI exhibit lower data variability, at 1.3% and 9.4%, respectively, meaning the data tends to be more homogeneous or close to the average value.

Table 2. Results of descriptive statistical

|

Cluster |

Variables |

Mean |

Sd. |

Skewness |

Kurtosis |

|

Full Sample |

LPDRB |

5.201 |

0.494 |

0.493 |

2.569 |

|

LJPP |

3.644 |

0.437 |

0.579 |

3.073 |

|

|

LHDI |

1.854 |

0.025 |

-0.337 |

4.148 |

|

|

LINV |

4.093 |

0.564 |

-0.109 |

2.605 |

|

|

LJUB |

4.025 |

0.465 |

0.376 |

3.716 |

|

|

KBI |

LPDRB |

5.465 |

0.481 |

0.160 |

2.039 |

|

LJPP |

3.873 |

0.438 |

0.356 |

2.298 |

|

|

LHDI |

1.866 |

0.019 |

0.839 |

3.185 |

|

|

LINV |

4.268 |

0.563 |

-0.106 |

2.047 |

|

|

LJUB |

4.269 |

0.451 |

0.427 |

2.759 |

|

|

KTI |

LPDRB |

4.937 |

0.345 |

0.319 |

2.677 |

|

LJPP |

3.416 |

0.294 |

-0.192 |

2.160 |

|

|

LHDI |

1.841 |

0.024 |

-0.655 |

3.501 |

|

|

LINV |

3.919 |

0.512 |

-0.370 |

2.892 |

|

|

LJUB |

4.060 |

0.335 |

-0.784 |

3.995 |

4.2 Dynamic panel estimation results

Table 3 reports the estimation results of FD-GMM, Fixed Effect, and PLS for three models: Western Indonesia region (KBI), Eastern Indonesia region (KTI), and the entire sample of 34 provinces in Indonesia.

For the Western Indonesia region (KBI) model, the validity test using the Sargan test in FD-GMM shows a value of 0.656 > 0.05, indicating that the model is valid. Next, the consistency test using AR (2) has a value of 0.023 < 0.05, meaning the model is inconsistent. To assess the goodness of fit, the lag coefficient of LPDRB in FD-GMM is 0.361, which is lower than the lag coefficient in the Fixed Effect Model. This indicates that the estimation result is biased. Since the FD-GMM model for KBI does not meet the criteria, the estimation proceeds to SYS-GMM. As shown in Table 3, the Sargan test value for SYS-GMM is 0.975 > 0.05, confirming that the model is valid. The AR (2) test value is 0.119 > 0.05, indicating that the model is consistent. Furthermore, the lag coefficient of LPDRB in SYS-GMM is 0.963, which is higher than the lag coefficient in the Fixed Effect Model (0.661) but lower than the PLS (0.988), confirming that the model is unbiased. Thus, it can be concluded that the best model for Western Indonesia region (KBI) is SYS-GMM.

For the Eastern Indonesia region (KTI) model, the validity test using the Sargan test in FD-GMM shows a value of 0.661 > 0.05, indicating that the model is valid. The consistency test using AR (2) has a value of 0.161 > 0.05, meaning the model is consistent. To check for bias, the lag coefficient of LPDRB in FD-GMM is 0.975, which is higher than in the Fixed Effect Model but lower than in the PLS method. Next, the SYS-GMM estimation results are examined. The lag coefficient of LPDRB is farther from 1 compared to the FD-GMM lag coefficient, indicating better long-term stability. The Sargan test p-value (0.973) is higher than that of FD-GMM (0.661), showing that the instrument is more valid. Based on these criteria, SYS-GMM is determined to be the better estimation model for Eastern Indonesia region (KTI).

Table 3. Dynamic panel estimation results

|

|

Western Indonesia (KBI) |

Eastern Indonesia (KTI) |

Full Sample |

|||||||||

|

Variables |

Fixed Effect |

Pool LS |

FD-GMM |

Sys- GMM |

Fixed Effect |

Pool LS |

FD-GMM |

Sys- GMM |

Fixed Effect |

Pool LS |

FD-GMM |

Sys- GMM |

|

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

(7) |

(8) |

(9) |

(10) |

(11) |

(12) |

(13) |

|

Constant |

- |

0.345 |

- |

- |

- |

0.279 (0.95) |

- |

- |

- |

0.248 (1.29) |

- |

- |

|

LPDRB (-1) |

0.661 (7.76) *** |

0.988 (102.80) *** |

0.361 (2.85) *** |

0.963 (65.20)*** |

0.967 (17.48)*** |

0.981 (106.92)*** |

0.975 (10.13)*** |

0.955 (44.71)*** |

0.918 (21.38)*** |

0.977 (157.01)*** |

0.839 (9.76) *** |

0.933 (44.03) *** |

|

LJPP |

0.4481 (3.44) *** |

0.003 (0.42) |

0.807 (3.49) *** |

0.017 (3.09 ) *** |

0.327 (3.71) *** |

0.004 (0.43) |

0.664 (2.25) ** |

0.006 (0.52) |

0.326 (4.92) *** |

0.002 (0.48) |

0.623 (2.88) *** |

0.021 (2.09) ** |

|

LHDI |

0.211 (0.70) |

-0.071 (-0.90) |

1.002 (2.63) *** |

0.023 (2.42) ** |

-0.688 (-2.33)** |

-0.033 (-0.45) |

-1.275 (-1.76)* |

0.053 (3.12) ** |

-0.535 (-2.74) *** |

-0.034 (-0.73) |

-0.583 (-1.50) |

0.049 (4.19) *** |

|

LINV |

0.020 (2.73) *** |

0.004 (0.89) |

0.017 (1.31) |

0.011 (1.96) ** |

0.026 (4.01) *** |

0.024 (6.29)*** |

0.018 (4.28) *** |

0.026 (5.29) *** |

0.025 (5.24) *** |

0.018 (6.42)*** |

0.020 (4.26) *** |

0.027 (4.63) *** |

|

LJUB |

0.021 (1.88) * |

0.008 (1.37) |

0.038 (1.59) |

0.014 (1.6)* |

-0.002 (-0.08)

|

-0.015 (-1.28) |

0.009 (0.58) |

0.004 (0.19) |

0.009 (0.91) |

0.002 (0.32) |

0.016 (1.31) |

0.020 (1.65) * |

|

Sargan test |

- |

- |

0.656 |

0.975 |

- |

- |

0.661 |

0.973 |

- |

- |

0.033 |

0.326 |

|

AR-test [18] |

- |

- |

0.023 |

0.119 |

- |

- |

0.161 |

0.394 |

- |

- |

0.069 |

0.149 |

The conclusion from the full sample model testing (34 provinces in Indonesia) shows that SYS-GMM is the best model based on validity, consistency, and bias criteria. FD-GMM Testing; the Sargan test indicates a value of 0.033 < 0.05, meaning the model is not valid. AR (2) test has a value of 0.069 > 0.05, indicating the model is consistent. Lag LPDRB in FD-GMM is 0.839, which is lower than Fixed Effect (0.918) and PLS (0.977), indicating a downward bias. SYS-GMM Testing; Sargan test indicates a value of 0.326 > 0.05, meaning the model is valid. AR (2) test has a value of 0.149 > 0.05, indicating the model is consistent. Lag LPDRB in SYS-GMM is 0.933, which falls between Fixed Effect (0.918) and PLS (0.977), meaning it is not biased. From these results, SYS-GMM meets the criteria as the best model for the full sample.

Regression estimation results with the best model presented on Table 3. The short-term regression results for Western Indonesia (KBI), Eastern Indonesia (KTI), and the Full Sample (34 provinces) are presented in columns (5), (9), and (15). The LPDRB lag coefficient shows a positive and significant value, meaning current economic growth is influenced by previous period growth. The LJPP coefficient (population) is positive and significant for economic growth, except in KTI, where its effect is not significant. This finding aligns with Malthusian theory, which states that an increase in population will raise demand for goods and services, thus driving economic growth. However, the labor force will only have a significant impact if accompanied by high productivity [33, 34]. If not, the demographic bonus that occurs in Indonesia in 2020-2023 or the increase in population will lead to increased productivity inequality and high unemployment.

The LHDI coefficient (Human Capital/Human Development Index) is positive and significant for economic growth. This is consistent with endogenous growth theory, which states that human capital accumulation through education and training enhances productivity and long-term economic growth [13-16, 41]. Qualified human capital will strengthen Indonesia's position in global competition, especially amid the development of the digital economy. In addition, this human capital very crucial to be the foundation of inclusive growth, social stability, and economic resilience in the future. In addition to the Human Development Index as a proxy for human capital, labor productivity is also an important aspect in promoting economic growth, because a productive workforce will certainly increase production efficiency which will ultimately result in higher economic growth. This labor productivity is also associated with the level of education, the higher the level of education will be able to create a skilled and productive workforce.

The LINV coefficient (Investment) is positive and highly significant for economic growth. This aligns with previous studies [36, 37]. However, the government needs to pay special attention to investments that excessively exploit natural resources, as this could lead to long-term environmental damage [42].

The LJUB coefficient (Money Supply) is positive but not significant for economic growth. This is in line with Keynesian theory, which suggests that an increase in the money supply does not automatically boost investment and consumption if demand remains low. In KTI, the economy still relies on the primary sector (agriculture and mining), making it less responsive to monetary policy. The heterogeneous regional economic structure limits the impact of increased money supply across different sectors [12]. The weakness of using the money supply variable as a proxy for monetary policy is that the money supply becomes less relevant in influencing economic growth due to financial innovations such as digital payment technology in this modern era. Therefore, it is necessary to look at the effect of monetary policy on regional economic growth using the instruments of interest rates, inflation and lending. Changes in interest rates more directly affect aggregate demand and do not require changes in the money supply directly.

The main difference between Western Indonesia and Eastern Indonesia is in terms of population. The majority of Indonesia's population is concentrated in Western Indonesia, so that there is an abundant labor force and a large market, while Eastern Indonesia has a smaller population so that purchasing power and market demand are lower, so that automatically the money supply is more in Western Indonesia than in Eastern Indonesia.

Thus, this study concludes that Human Capital, Investment, and Population Size play a crucial role in regional economic growth in Indonesia. However, the effectiveness of monetary policy remains limited, especially in regions with less flexible economic structures.

4.3 Convergence coefficient

The GMM estimation model used in this study also provides a convergence coefficient, which is presented in Table 4.

Table 4. Convergence result

|

Region |

Convergence Coefficient |

|

Western Indonesia |

0.03747333 |

|

Eastern Indonesia |

0.04615788 |

|

Full Sample |

0.06902704 |

Economic convergence speed measures how quickly regions with lower income or productivity levels grow compared to more developed regions, thus reducing economic disparities. Eastern Indonesia (KTI) has a higher convergence coefficient than Western Indonesia (KBI), meaning that Eastern regions are experiencing faster economic growth relative to the national average compared to Western Indonesia. The full sample (34 provinces) has the highest convergence coefficient, indicating that the economic convergence process is faster when all regions are considered together rather than separately. The reasons for the higher coefficient of convergence in the eastern region are: 1) Bonus demography - many young people in this region have entered the productive workforce, which encourages faster economic growth, 2) government investment, the government has invested heavily in the construction of toll roads, ports, airports, and electricity networks in the eastern region so as to encourage faster economic growth, 3) migration and labor mobility - many job seekers in the western region have moved to the eastern region due to increased employment opportunities, especially in the mining and plantation sectors. In recent years, the government has also increased access to vocational education and training in the eastern region, thereby accelerating productivity.

4.4 Long run estimation result

Based on Table 5, in the long run, Human Capital (LHDI) contributes the most to regional economic growth compared to other variables. Impact of human capital (LHDI) is stronger in Eastern Indonesia (1.18) than in Western Indonesia (0.63), this can be said that the eastern region of Indonesia experiences “the catch-up effect," namely the ability of Eastern Indonesia to catch up with the western region because it experiences a surge in productivity that comes from increasing access to education and vocational training as well as the absorption of educated labor from the Western region and investment made by the government. This suggests that government and other stakeholders need to invest in human capital development to sustain economic growth.

Table 5. Long run-coefficient result

|

Variables |

Western Indonesia |

Eastern Indonesia |

Full Sample |

|

LJPP |

0.46195 |

0.143561 |

0.3188624 |

|

LHDI |

0.6320668 |

1.180964 |

0.7383601 |

|

LINV |

0.306524 |

0.5969426 |

0.409417 |

|

LJUB |

0.3719151 |

0.09272492 |

0.3069657 |

This research assesses the nexus of human capital, monetary policy, and population size on regional economic growth in Indonesia, dividing the country into two sub-regions: Western Indonesia (KBI), Eastern Indonesia (KTI), and Full Sample (34 provinces in Indonesia). This research focuses on human capital, monetary policy, and regional economic growth from 2016 to 2023 using panel data.

Key Findings are human capital has a positive and significant impact on regional economic growth. Monetary policy has a positive but insignificant impact on economic growth. Previous period economic growth positively and significantly influences current economic growth. Population and investment also have a significant impact on regional economic growth.

In general, the results indicate that previous-period regional economic growth, human capital, investment, and population size influence economic growth across all provinces, as well as in the western and eastern sub-regions. However, the magnitude of change varies across sub-regions. In the eastern region, monetary policy and population size do not have a significant impact on economic growth.

In the long term, it was also found that there is a “catch-up effect” in Eastern Indonesia, namely the ability to catch up with Western Indonesia, especially in terms of human capital.

These findings reinforce the role of human capital in endogenous growth theory. However, this theory is not fully applicable if the economy relies only on the exploration and exploitation of natural resources. Policy implications in human capital development; The Government should increase investment in education and training, provide incentives for companies engaged in Research & Development (R&D), encourage industry-academia collaboration to develop applied research that benefits the industrial sector, and improve infrastructure that supports innovation, such as fast and widespread internet access. Implications in monetary policy; monetary policy currently does not significantly support economic growth, the government should increase financial literacy and reduce inequality in access to credit and investment.

Limitations and future research directions in this study are this study is limited by the short period of data (2016–2023) and does not include the four newest provinces in Indonesia. Future research should expand the study period for a more comprehensive analysis and include fiscal policy variables to examine the interaction between fiscal, monetary; and macroeconomic policies in supporting regional economic growth and incorporate external factors, such as global instability affecting domestic supply chains.

[1] Ali, S., Masih, M. (2021). The determinants of economic growth: The Malaysian case. Munich Personal RePEc Archive. https://mpra.ub.uni-muenchen.de/107859/1/MPRA_paper_107859.pdf.

[2] Hamdi, Hasyim, S., Syafii, M., Tanjung, A.A. (2024). The effect of economic growth, imports and exports on food inflation in ASEAN countries: Case study of Timor Leste, Laos, Cambodia, and Myanmar. International Journal of Sustainable Development and Planning, 19(9): 3689-3698. https://doi.org/10.18280/ijsdp.190937

[3] Tanjung, A.A., Ruslan, D., Lubis, I., Pratama, I. (2022). Stock market responses to COVID-19 pandemic and monetary policy in Indonesia: Pre and Post Vaccine. Cuadernos de Economia, 45(127): 120-129. https://doi.org/10.32826/cude.v1i127.610

[4] Wartoyo, W., Haida, T.A.F.F.N. (2024). Fiscal and monetary policy synergy in the context of national economic recovery after the COVID-19 pandemic. Indonesian Journal of Islamic Business and Economics, 6(1): 26-36. https://doi.org/10.32424/1.ijibe.2024.6.01.9941

[5] Nopeline, N., Sirojuzilam, Tanjung, A.A., Syafii, M. (2024). The j-curve of Indonesia trade balance with his trading partners: Autoregressive Distributed lag method. Montenegrin Journal of Economics, 20(4): 113-122. https://doi.org/10.14254/1800-5845/2024.20-4.10

[6] Osiobe, E.U. (2019). A literature review of human capital and economic growth. Business and Economic Research, 9(4): 179. https://doi.org/10.5296/ber.v9i4.15624

[7] Javed, F., Khan, M.S.A., Gul, B. (2019). Asymmetric effects of monetary policy shocks on output growth: Evidence from nonlinear ARDL and Hatemi-J causality tests. Global Economics Review, IV(IV): 157-181. https://doi.org/10.31703/ger.2019(iv-iv).14

[8] Tanjung, A.A., Afifuddin, S., Daulay, M., Ruslan, D. (2017). Relationship between monetary policy, fiscal, country risk and macroeconomic variable in Indonesia. International Journal of Economic Research, 14(15): 207-220.

[9] Morwat, A.F. (2021). Study of population growth impact on economic growth during (2003-2017) in Afghanistan. International Journal for Research in Applied Sciences and Biotechnology, 8(1): 49-56. https://doi.org/10.31033/ijrasb.8.1.6

[10] Shuyong, F., Shuyu, C., Maimaituxun, M. (2024). Discussion on the relationship between Chinese government’s investment in health human capital and economic growth. Journal of the Knowledge Economy, 15: 19183-19202. https://doi.org/10.1007/s13132-024-01771-w

[11] Yang, X. (2020). Health expenditure, human capital, and economic growth: An empirical study of developing countries. International Journal of Health Economics and Management, 20(2): 163-176. https://doi.org/10.1007/s10754-019-09275-w

[12] Gabriel, E.M., Darcilio, V.M. (2024). The impact of monetary policy on economic growth: A case study of Mozambique. Modern Economy, 15: 1112-1146. https://doi.org/10.47191/ijmei/v10i6.05

[13] Sebki, W. (2021). Education and economic growth in developing countries: Empirical evidence from GMM estimators for dynamic panel data. Economics and Business, 35(1): 14-29. https://doi.org/10.2478/eb-2021-0002

[14] Fashina, O.A., Asaleye, A.J., Ogunjobi, J.O., Lawal, A.I. (2018). Foreign aid, human capital and economic growth nexus: Evidence from Nigeria. Journal of International Studies, 11(2): 104-117. https://doi.org/10.14254/2071-8330.2018/11-2/8

[15] Han, J.S., Lee, J.W. (2020). Demographic change, human capital, and economic growth in Korea. Japan and the World Economy, 53: 100984. https://doi.org/10.1016/j.japwor.2019.100984

[16] Sultana, T., Dey, S.R., Tareque, M. (2022). Exploring the linkage between human capital and economic growth: A look at 141 developing and developed countries. Economic Systems, 46(3): 101017. https://doi.org/https://doi.org/10.1016/j.ecosys.2022.101017

[17] Opoku, E., Poku, K., Domeher, D. (2024). Financial inclusion, human capital development and economic growth in Africa: An examination of the transmission channel. SAGE Open, 14(3): 1-19. https://doi.org/10.1177/21582440241271285

[18] Akalpler, E., Duhok, D. (2018). Does monetary policy affect economic growth: Evidence from Malaysia. Journal of Economic and Administrative Sciences, 34(1): 2-20. https://doi.org/10.1108/JEAS-03-2017-0013

[19] Michael, A., Owusu Oppong, E., Gulnabat, O. (2020). Effects of monetary policy on economic growth; Evidence from five (5) African countries (Mauritius, Nigeria, South Africa, Namibia and Kenya) from 1980 to 2019. Scholars Journal of Economics, Business and Management, 7(9): 293-298. https://doi.org/10.36347/sjebm.2020.v07i09.002

[20] Agustina, C.R., Daryono, D. (2022). The role of monetary policy on economic growth: Evidence from Indonesia. Wiga: Jurnal Penelitian Ilmu Ekonomi, 12(4): 264-271. https://doi.org/10.30741/wiga.v12i4.881

[21] Islam, M.S., Hossain, M.E., Chakrobortty, S., Ema, N.S. (2022). Does the monetary policy have any short-run and long-run effect on economic growth? A developing and a developed country perspective. Asian Journal of Economics and Banking, 6(1): 26-49. https://doi.org/10.1108/ajeb-02-2021-0014

[22] Matousek, R., Tzeremes, N.G. (2021). The asymmetric impact of human capital on economic growth. Empirical Economics, 60(3): 1309-1334. https://doi.org/10.1007/s00181-019-01789-z

[23] Awan, A.G., Naseem, R. (2019). The impact of government expenditures on economic development in Pakistan. Global Journal of Management, Social Sciences and Humanities, 5(1): 22-35.

[24] Zuhroh, I. (2022). The nexus of monetary policy and economic growth: Empirical study from Indonesia. Journal of Innovation in Business and Economics, 5(2): 61-70. https://doi.org/10.22219/jibe.v5i02.20539

[25] Utami, F., Putri, F.M.E., Wibowo, M.G., Azwar, B. (2021). The effect of population, labor force on economic growth in OIC countries. Jurnal REP (Riset Ekonomi Pembangunan), 6(2): 144-156. https://doi.org/10.31002/rep.v6i2.3730

[26] Zardoub, A., Sboui, F. (2023). Impact of foreign direct investment, remittances and official development assistance on economic growth: Panel data approach. PSU Research Review, 7(2): 73-89. https://doi.org/10.1108/PRR-04-2020-0012

[27] Harahap, N.J., Rafika, M. (2020). Industrial Revolution 4.0 : And the impact on human. Ecobisma (Jurnal Ekonomi, Bisnis Dan Manajemen), 7(1): 89-96. https://doi.org/10.36987/ecobi.v7i1.1545

[28] Albloush, A., Alharafsheh, M., Hanandeh, R., Albawwat, A., Shareah, M.A. (2022). Human capital as a mediating factor in the effects of green human resource management practices on organizational performance. International Journal of Sustainable Development and Planning, 17(3): 981-990. https://doi.org/10.18280/ijsdp.170329

[29] Ernanto, Sriyana, J., Hakim, A., Sidiq, S. (2024). Enhancing human capital in Indonesia: Does economic policy work? International Journal of Sustainable Development and Planning, 19(5): 1963-1969. https://doi.org/10.18280/ijsdp.190535

[30] Sarwar, A., Khan, M.A., Sarwar, Z., Khan, W. (2021). Financial development, human capital and its impact on economic growth of emerging countries. Asian Journal of Economics and Banking, 5(1): 86-100. https://doi.org/10.1108/ajeb-06-2020-0015

[31] Duan, C., Zhou, Y., Cai, Y., Gong, W., Zhao, C., Ai, J. (2022). Investigate the impact of human capital, economic freedom and governance performance on the economic growth of the BRICS. Journal of Enterprise Information Management, 35(4-5): 1323-1347. https://doi.org/10.1108/JEIM-04-2021-0179

[32] Senbet, D. (2011). The relative impact of fiscal versus monetary actions on output: A Vector Autoregressive (VAR) approach. Business and Economic Journal, 25: 1-11.

[33] Brida, J.G., Alvarez, E., Cayssials, G., Mednik, M. (2024). How does population growth affect economic growth and vice versa? An empirical analysis. Review of Economics and Political Science, 9(3): 265-297. https://doi.org/10.1108/REPS-11-2022-0093

[34] Cayssials, G., Antonio, F., González, I., London, S. (2024). Population and economic growth: A panel causality analysis. Population and Economics, 8(3): 220-240. https://doi.org/10.3897/popecon.8.e109133

[35] Romer, P.M. (1986). Increasing returns and long-run growth. Journal of Political Economy, 94(5): 1002-1037. https://doi.org/10.1086/261420

[36] Nguyen, K.T., Nguyen, H.T. (2021). The impact of investments on regional economic growth. Journal of Asian Finance, Economics and Business, 8(8): 0345-0353. https://doi.org/10.13106/jafeb.2021.vol8.no8.0345

[37] Hayat, A. (2019). Foreign direct investments, institutional quality, and economic growth. Journal of International Trade and Economic Development, 28(5): 561-579. https://doi.org/10.1080/09638199.2018.1564064

[38] Van, L.T.H., Vo, A.T., Nguyen, N.T., Vo, D.H. (2021). Financial inclusion and economic growth: An international evidence. Emerging Markets Finance and Trade, 57(1): 239-263. https://doi.org/10.1080/1540496X.2019.1697672

[39] Arellano, M., Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2): 277-297. https://doi.org/10.2307/2297968

[40] Blundell, R., Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1): 115-143. https://doi.org/10.1016/S0304-4076(98)00009-8

[41] Altiner, A., Toktas, Y. (2017). Relationship between human capital and economic growth: An application to developing countries. Eurasian Journal of Economics and Finance, 5(3): 87-98. https://doi.org/10.15604/ejef.2017.05.03.007

[42] Andrasari, M., Sirojuzilam, Tanjung, A.A., Syafii, M. (2024). Investigate the different impacts of tourism on the economy and carbon emissions of high income and middle-income countries in Asia. Journal of Ecohumanism, 3(6): 1328-1339. https://doi.org/10.62754/joe.v3i6.4106