Katrin Cintya Baboe![]() | S. Joy Laura Angelica

| S. Joy Laura Angelica![]() | Linda Kusumaning Wedari*

| Linda Kusumaning Wedari*![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study examines whether digital transformation and carbon emissions can be catalysts for ESG performance. The sample comprises 17 manufacturing companies, and a quantitative approach was used by analyzing data from several large manufacturing companies listed on the IDX in 2019 - 2023 that have implemented a digital transformation strategy. Our research uses the two-way GMM method with StataMP 17. The results of this study show a significant positive relationship between digital transformation and ESG performance and a significant negative relationship between carbon emissions and ESG performance. By integrating the analysis of digital transformation and carbon emissions, this study offers a new holistic view and provides strategic recommendations for companies to optimize ESG performance amidst the dynamic changing demands of the latest regulations, thus providing empirical guidance for policymakers and management in sustainability efforts.

digital transformation, carbon emissions, ESG performance, sustainability, innovation, SDG 9

The global corporate environment has changed significantly in the current Industry 4.0 era due to digital transformation towards sustainability and social responsibility. Digital transformation, which includes the use of technologies such as software, internet, big data, Internet of Things (IoT), and artificial intelligence (AI), has the potential to change the way businesses handle day-to-day operations, maximize cash flow, reduce energy consumption [1, 2], and can provide effective technical means to enhance a company's ESG capabilities [3]. Digital transformation not only revolutionizes the way companies operate but also paves the way for companies to take a more sustainable approach [4].

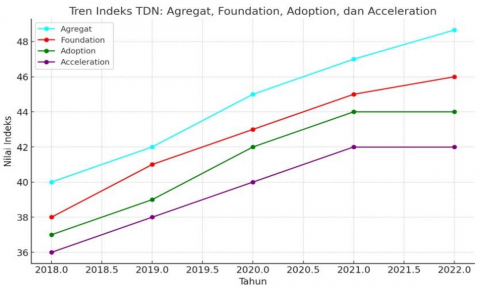

Indonesia is confronting difficulties in national growth, such as the COVID-19 pandemic and Megatrend 2045. This crisis has created motivation for Indonesia to acknowledge the importance of digital technology adoption in improving global competitiveness. This led to the Indonesian Digital Vision (hereafter-IDV) 2045 program, which intends to facilitate the development of Indonesia's national digital transformation to be implemented throughout 38 provinces, through the National Long Term Development Plan (NLTDP) 2025-2045 and National Medium Term Development Plan (NMTDP) 2025-2029 to assure competitiveness and national economic resilience [5]. Figure 1 depicts the results of the DT index test and shows a strong index (category B) in terms of understanding and utilizing digital in everyday life and the workplace. This indicates that Indonesian people are already quite aware of the development of digital transformation.

Figure 1. Indonesia digital transformation index [5]

The investigation on relationship between digital investment and ESG performance reveals that digital transformation can improve its ESG performance [5]. The inclusion of digital technology into the economy may cut costs, enhance operational efficiency, and strengthen the company's image as a leader in sustainability-oriented innovation [6]. A study discovered that integrating smart manufacturing technology can cut energy usage in large-scale manufacturing facilities by up to 15% through enhanced resource management and predictive maintenance processes [7].

The long-term (10-year) global risk rating by the World Economic Forum, such as cybersecurity and negative outcomes from AI technology indicates that digital transformation has significant effects on environmental, social, and governance (ESG) risks [8]. The existence of this data serves as a reference for identifying the potential of technology growth and focusing on how to utilize it rather than the drawbacks. Organizations can use digital transformation to meet sustainability goals such as lowering carbon emissions, boosting openness and trust through auditable data and expanding social access. Furthermore, digital transformation may aid in resource management by delivering data-driven solutions such as real-time emissions monitoring and supply chain optimization [9, 10].

The main environmental issue faced by many companies today is to meet carbon emissions reduction targets, especially in the heavy industry sector [11, 12]. World economic forum global risks perception survey shows 66% of survey participants focused on extreme weather as one of the major threats in 2024 [8]. Environmental problems, specifically carbon emissions, is blamed as one of the primary causes of climate change and contribute to extreme weather. Extreme weather may be resulting big impact on ESG achievement [9, 12]. As a result, businesses must control their carbon emissions released. Companies that successfully lowered environmental hazards, and manage carbon emissions efficiently can enhance ESG value, which can attract investor and creditor attention and improve the company's standing [12]. This issue forced all businesses in all countries worldwide to participate in carbon emissions mitigation [9]. Since Indonesia is one of the Kyoto Protocol signatories of the Framework Convention on Climate Change (UNFCCC), Indonesia Government has introduced the Minister of Environment and Forestry Regulation No. P.15/Menlhk/Setjen/Kum.1/4/2019 and Presidential Regulation (PP) No. 98 of 2021 on carbon reduction target [13].

Disclosure of carbon emissions positively affects firm value by promoting financial and operational sustainability [9], adds value for investors, since it shows the environmentally friendly business operation and sustainable [14, 15], and improve the company's ESG performance [3].

Companies with better ESG performance tend to have more efficient organizational procedures, fewer reputation-damaging incidents, and greater appeal to institutional investors [16]. Good ESG and corporate financial performance, may indicate that tend to be more financially successful [17] since it can balance environmental protection, responsibility fulfilment, and corporate governance, toward good sustainable corporate development [18]. Some prior studies have examined the relationship between digital transformation and investment in carbon reduction [3, 19, 20] green company and green innovation is measured by carbon intensity [21] and ESG score [22, 23] in China. However, no studies investigate digital transformation, carbon emissions, and ESG performance. ESG Performance in this study is measured by ESG Rating which is represented by A+ to D- grade and numerical score (0-100). ESG Rating Data was droned from Refinitiv database in Indonesia context. Studies in this area are conducted in Indonesia is lack of attention [24, 25]. Using data of manufacturing companies listed on the Indonesia Stock Exchange between 2019 and 2023, this study examines the impact of digital transformation and carbon emissions on ESG Performance using two-way GMM statistical analysis this approach differs from previous studies. In addition, since scope 1 carbon emissions are generated directly by companies, our studies use this scope to analyze how companies are responsible for carbon emissions and how the level of carbon emissions generated by companies directly impacts ESG performance.

This study provides a significant contribution that falls into four aspects. First, this research enriches the ESG and sustainability literature in relation to digital transformation to carbon emissions abatement. Digital transformation implemented by companies by adopting green technologies, such as, Internet of Thing (IoT) and blockchain, to monitor, manage and mitigated carbon emissions released from business operation. The use of cloud computing has replaced physical server that consumed much energy in its operation. The use of IoT may optimize the energy consumption in the manufacturing plant. Those green technologies contribute to good ESG score. Second, this study uses two-way Generalized Method of Moments (GMM) model in the analysis. This GMM model is claimed as a robust and bias-free model, in addressing endogeneity issues. This model has great ability to handle both measurement errors and simultaneity biases. Third, this study offers valuable data for policymakers to understand the interplay between technology adoption, emissions reduction, and ESG performance. Therefore, policymakers can design incentives for green technologies and regulations encouraging digital innovation that supports ESG targets.

Next section will explain the literature review on the context of digital transformation and carbon emissions on ESG performance. It will be followed by hypotheses development and the theories justification. Section 4 presents the research methodology and followed by the analysis results and discussion. Last section will explain conclusions and implications.

2.1 Digital transformation

Digital transformation (hereafter – DT) can be defined as a process that aims to improve an entity by driving major changes to its business processes through the utilization of a combination of information technology, computing, communication, and connectivity [26]. DT is an innovation for companies in increasing their business productivity by producing more products using lower cost management but in an environmentally responsible way, such as efficient energy use, supply chain optimization, and enhanced monitoring systems [4] DT allows a company to be able to optimize business operational processes, increase transparency, data collection, analysis and reporting, with technological innovations that affect the management of business practices and reporting, which in turn will have a positive impact on the company's ESG assessment. This DT integration process produces real-time and automated data analysis results, which may enhance investor confidence and stakeholder trust, since companies demostrate accountability and commitment to sustainability [24]. Some studies explain that DT business strategy [27], technology innovation [4] and DT help companies reduce costs, increase efficiency, and improve financial performance, capital market share, and other economic performance [1, 28]. This can be taken as evidence that digital transformation innovation is an important thing in improving the company's ESG performance, especially in the environmental field [4].

2.2 Hypothesis development

A hypothesis is a theoretically-based tentative answer to a problem.

2.2.1 Digital transformation and ESG performance

Previous studies have examined the relationship between digital transformation and company’s ESG performance [4, 11, 29]. DT innovation is motivated by company’s initiatives to increase efficiency and improve business performance. The use of digital technology as a strategic plan is aimed to increase operational efficiency and produce value for the company [28].

This DT innovation is consistent with stakeholder and resource-based view theory (hereafter-RBV). Stakeholder theory posits that company’s need to meet stakeholders’ expectations to ensure the success and sustainability of an organization [19, 30]. It also plays an important role in accountability or transparency, and legitimacy of corporate actions that are under social norms and expectations [31, 32]. Stakeholder theory believes that digital transformation can increase transparency and accountability, which may meet stakeholder’s demands, thus eventually enriching the ESG and corporate performance [33, 34]. In addition, DT can encourage innovation to improve enterprises' total productivity, which can enhance economic performance [34], improving enterprises' value chain position, value in management and training personnel, research and development projects, and infrastructure development [35].

Previous studies discussed the advantages of digital transformation, which can strengthen the relationship between companies and stakeholders through transparent and relevant information disclosure, which will build good internal governance with the participation of company stakeholders [24, 31]. In the tech industry [35] and financial industry [36] in China, digital transformation is a significant component in driving sustainable development and integration efficiency processes, also influencing corporate risk-taking. This is a line with the perspective of RBV theory, which explains that the company's competitive advantage comes from internal resources that are unique and difficult to imitate [33]. From the perspective of RBV theory, we can see that digital transformation becomes a strategic resource for companies to achieve competitive advantage while fulfilling ESG [7, 35]. Intelligent business processes will improve business efficiency, since it allows organizations to monitor each of their business processes while using energy efficiently. Therefore, it can be assumed that digital transformation may increase a company’s ESG performance [28]. Given this, stakeholder and RBV theories can justify the prediction of positive relationship between digital transformation and corporate ESG performance. Based on this, we proposed Hypothesis 1 for this study.

H1: Digital transformation is positively correlated with ESG performance.

2.2.2 Carbon emissions and ESG performance

The issue of corporate carbon emissions has become an important indicator in measuring corporate ESG performance, which is not only considered by investors and stakeholders but also by the public [10]. The lower carbon emissions produced, the better the company's ESG performance, this reflects the results of management activities in managing carbon emissions generated in the company [37]. The efficient carbon emission management will mitigate environmental risks and contribute to improving the company's ESG performance [32]. This result depending on the company's actions in managing carbon emission reduction and its commitment to sustainability [10].

This carbon emission management act also aligns with stakeholder and RBV theories. Based on the previous study [21, 32], stakeholder theory is related to how companies can fulfil stakeholder demands for social responsibility through efficient carbon emissions management [10]. Investors are more likely to consider companies that invest in low-carbon technologies [32, 37], as this not only enhances their reputation but also benefits other stakeholders through social and environmental aspects.

From the perspective of RBV theory, it explains that the company's ability to manage carbon emissions effectively becomes a strategic asset for the company in achieving competitive advantage [14]. Companies that actively report and take carbon emissions mitigation initiatives, demonstrate good governance and help companies meet ESG performance and provide significant superior competitive value [38]. The combination of more efficient management of carbon emissions with innovative environmentally friendly business practices is a unique corporate resource that is certainly difficult to replicate [32]. Companies with more ecologically friendly operational practices [39], such as efficient carbon emissions management, will tend to have better performance and market value and can increase competitiveness and create value for stakeholders and investors [40]. High carbon emissions do not have a good relationship on improving the company's ESG performance because the level of carbon emissions generated by the company demonstrates how the company manages its business operations by focusing not only on market value but also on managing its environment [14]. The company's lower carbon emissions can contribute to an increase in ESG performance [37].

H2: Carbon emission is negatively correlated to ESG performance.

3.1 Sample and data collection

The population for this study is manufacturing companies listed on the Indonesia Stock Exchange between 2019 and 2023 that have financial or sustainability reports available on the Indonesia Stock Exchange website (www.idx.co.id). Our initial sample includes 172 manufacturing companies in Indonesia from 2019 to 2023. However, two firms have been delisted from the IDX, and around 155 companies have been removed from the sample because no information available on their ESG performance and carbon emissions in Refinitiv database and sustainability reports for 2019-2023. Considering this database contains only a few organizations, our maximum sample size is 17 company-year.

The scope 1 carbon emissions and financial data are collected from Refinitiv, sustainability reports and company annual reports, while the ESG performance score is from Refinitiv and IDX web data.

3.2 Variables

The operational variables in this study consist of independent, dependent, and control variables as presented in Table 1.

Table 1. Variable definitions and measures

|

Variable |

Definition and Measure |

Predicted Direction |

|

|

Dependent Variable |

ESG |

Environmental, social, and governance (ESG) performance from Refinitiv score (A+ to D- grade and numerical score (0-100) |

|

|

Explanatory Variable |

DT |

Digital transformation, feature text analysis and word frequency statistics with Phyton, using Google Collab [24, 28] |

+ |

|

CE |

Carbon emissions: consists of (Scope 1 in tons CO2-e/total sales) from the company's sustainanility report |

- |

|

|

Control Variable |

DR |

Debt-to-assets ratio, measured as total liabilities(t) deflated by total assets(t) [32] |

- |

|

S_GrowthR |

Sales Growth Rate from 2019 - 2023, ((Sales(t) - Sales(t-1))/ Sales(t-1)* 100)) [32] |

+ |

|

|

Sales |

Total Sales |

+ |

|

|

Profitability |

Profitability, return on asset (ROA), measured as Net Income(t) deflated by Total Assets(t) |

- |

|

|

Year |

Year indicator |

+/- |

|

(1) Dependent variables: ESG performance. Some studies published in China utilize the Sino-Securities ESG Index [24, 26]. This research focuses on Indonesia context and uses data drawn from Refinitiv database to assess the ESG performance of listed manufacturing companies. ESG performance is measured by examining the A+ to D- grades in accordance with LSEG, however the ESG Performance grades we utilize for processing are numerical score (0-100) generated from data in Refinitiv’s database.

(2) The Explanatory variables include Digital Transformation and Carbon emissions. We collect data related to digital transformation following methods [24, 28, 35]. Data DT collected from annual reports with textual analysis and word frequency to construct digital transformation indicators to samples data. The measurement method is as follows [24]: first, we utilize Python on the Google Collab website to extract the full-text content of each company's annual report. Second, using the DT world map [24], the frequency of keywords found (refer to Table 2) in each yearly report was used to extract, filter, and analyze text from annual reports. The keywords we chose as reference appeared 10 times or more in each company's annual report from 2019-2023. Third, we continue to count and match the keywords from the Python run results, and the collected word frequencies serve as an indicator system for the company's digital transformation. Table 2 shows the specific keyword map.

The next explanatory variable is carbon emissions, which is measured by scope 1 carbon emissions in tons CO2-e divided by total sales. However, some annual reports and sustainability reports do not include carbon emissions number, researchers collected carbon emissions data from Refinitiv database.

(3) Control variables. To help increase the validity of the relationship between the independent variable and the dependent variable, we consider a series of control variables in the analysis. The control variables studied include debt-to-assets ratio (DR), sales growth rate (S_GrowthR), total sales (Sales), profitability, and year. Table 1 provides the definitions and measures of these variables.

Table 2. Digital transformation keywords

|

Digital Transformation Keywords |

|

|

Digital products |

Digital products, Data products, Smart wear, Smart home, Unmanned driving, 3D printing |

|

Digital production |

Digital manufacturing, Smart factory, Smart manufacturing, Smart management, Smart systems, Smart production, Smart equipment, Industrial robots, Smart workshop, Smart energy, Automatic production, Automatic control, Automatic detection, Automatic Numerical control |

|

Digital marketing |

Internet Model, Internet Business Model, Internet Business, E-commerce, B2B, B2C, C2B, C2C, O2O, Digital brand, Social media, Digital marketing, Online advertising, Smart recommendation |

|

Digital management |

Digital platform, Internet platform, Cloud platform, Data center, Data acquisition, Data mining, Data analysis, Data statistics, Digital operation, Smart operation, Data decision-making, Data driven, Data management, Digital governance, Digital control, Data warehouse |

|

Big data and technology |

Digital, Technology, Big data, Cloud computing, Blockchain, Artificial intelligence, Internet of Things, 5G, Mobile Internet, Deep learning, Machine learning, Digital twinning, Decentralized computing, Edge computing |

3.3 Model design

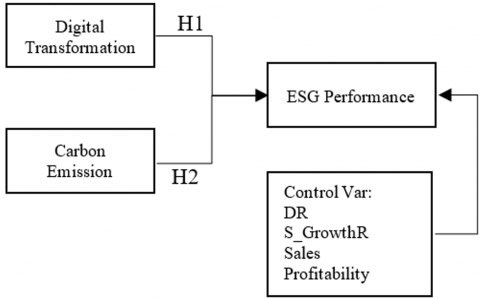

Figure 2 presents the research framework used in this research.

Figure 2. Research Framework

This study utilizes a regression model to analyze the impact digital transformation (DT) and carbon emissions on ESG performance, as follows:

$\begin{gathered}E S G_{i t}=\beta_0+\beta_1 D T_{i t}+\beta_2 C E_{i t}+\beta_3 D R_{i t}+\beta_4 S_{-} \text {Growth }_{i t} \\ +\beta_5 \text { Sales }_{i t}+\beta_6 \text { Profitability }_{i t}+\epsilon_{i t}\end{gathered}$

Information:

Two-step Generalized Method of Moments (GMM) models are claimed to be robust and bias-free models, overcoming endogeneity issues [41]. In this study, we use a two-way GMM analysis model using lag independent variables as instruments. This model is used to look at the impact of digital transformation and carbon emissions on ESG performance in manufacturing companies in 2019-2023.

4.1 Descriptive statistical results

Descriptive statistics are presented in Table 3 for 85 company-year observations. ESG performance has a mean value of 53.16, which indicates that, on average, companies in the sample exhibit moderate levels of ESG performance.

Table 3. Descriptive statistics

|

Variable |

Mean |

Std.Dev |

Min |

Max |

|

ESG |

53,16 |

17,22 |

21,00 |

76,00 |

|

DT |

4,59 |

0,86 |

2,64 |

5,83 |

|

CE |

1267 |

1888 |

596,43 |

6638 |

|

DR |

0,49 |

0,48 |

0,04 |

3,74 |

|

S_GrowthR |

0,05 |

0,19 |

-0,43 |

1,00 |

|

Sales |

24,49 |

1,13 |

22,16 |

29,99 |

|

Profitability |

0,10 |

0,19 |

0,00 |

1,40 |

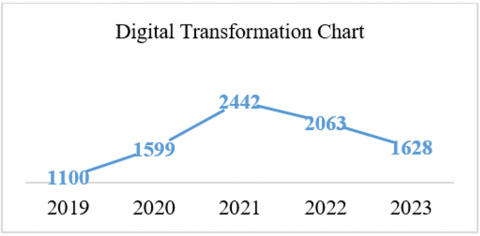

The digital transformation (DT) has a mean value of 4.59, indicating that most manufacturing industry companies have a moderate level of transformation. Figure 3 shows that there is a significant increase in the implementation of digital transformation until 2021, although in 2022 to 2023 there was a decrease, the implementation of digital transformation is still higher than previous years. This shows that the implementation of digital transformation in each manufacturing company still varies, where the highest level is in the pharmaceutical industry sub-sector (13%) and the lowest in the agribusiness sub-sector (1%).

Figure 3. Digital transformation chart

For carbon emissions, the mean value obtained is 1267, indicating that the carbon emission values generated by the 85 observed companies are moderate. Statistical analysis shows that there are fluctuations in the carbon emission data, with some companies having much higher carbon emission levels than the mean result, indicating that carbon emission reduction efforts within companies are not equally distributed.

Table 4 shows Pearson's correlations for all variables. Variance inflation factors (VIF) are checked in preliminary OLS regressions and the results are below 5, indicating that there is no multicollinearity problem.

Table 4. Pearson correlation matrix

|

ESG |

DT2 |

CE |

DR |

S_GrowthR |

Sales |

Profitability |

|

|

ESG |

1,0000 |

|

|

|

|

|

|

|

DT |

0,6372*** |

1,0000 |

|||||

|

CE |

-0.421*** |

0.3146*** |

1,0000 |

|

|

|

|

|

DR |

-0.1350 |

-0.0234 |

-1474 |

1,0000 |

|

|

|

|

S_GrowthR |

0.0036 |

-0.1403 |

-0.0827 |

-0.1540 |

1,0000 |

|

|

|

Sales |

0.1316 |

0.2905** |

0.1967 |

-0.0917 |

0.4378*** |

1.0000 |

|

|

Profitability |

0.2768*** |

-0.1668 |

-0.0959 |

-0.0184 |

0.0224 |

0.0776 |

1,0000 |

*Correlation is significant at the P < 0.10

**Correlation is significant at the P < 0.05

***Correlation is significant at the P < 0.01

4.2 Analysis based on two-way GMM

The use of two-way GMM results confirms the validity of the model, as shown in Table 5. The autocorrelation test on Arellano-Bond (2) results (p > 0.05) indicate that the model in this study is free from residual autocorrelation problems. Both Sargan and Hansen’s test results (p > 0.05) were insignificant. This indicates that the instruments used in the model are valid and free from overidentification issues, hence reinforcing the robustness of digital transformation (DT) and carbon emissions as independent variables in explaining ESG performance.

Table 5 shows the specific result between digital transformation and ESG performance, which has a coefficient value of 5.7047 and a p-value of 0.000. This indicates that H1 is not rejected, the higher implementation of digital transformation, the higher correlation with ESG performance. The positive relationship between digital transformation and ESG performance is consistent with the stakeholder theory that companies with digital transformation innovations can meet the stakeholders’ expectations and increase efficiency, transparency, and automation of business processes that are more sustainable [33, 34]. In addition, the result is also consistent with the RBV theory, where digital technology can be a strategic resource in gaining sustainable competitive advantage and improving company's ESG performance [33]. This shows that companies with a high level of digitalization tend to have better ESG performance [7].

Table 5 also shows that carbon emissions are significantly negatively correlated to ESG performance, which has a coefficient value of -1.54 and a p-value of 0.000. This indicates that H2 is not rejected, showing that scope 1 carbon emissions deflated by total sales is negatively correlated with ESG performance. The higher the carbon emissions released by company, the less company's ESG performance will be [14]. According to the stakeholder theory perspective, the efficiency of production and business process may meet stakeholder expectations, and the transparency on the implementation of carbon emission mitigation strategies can attract and strengthen relationships with investors, and governments, and increase consumer loyalty [10]. In addition, the RBV theory also explains that to achieve a competitive advantage, companies must maintain its strategic resources that can drive efficiency [14]. If company effectively manage its resources consumption through efficient business practice, they can participate in carbon mitigation dan establish a uniqueness that is certainly difficult to be replicated by its competitors [32]. The less carbon emissions released from its business operation, it may not only comply to environmental and government regulations but also gain strategic advantage by meeting stakeholder expectations and eventually contributing to superior ESG performance [37].

Regarding the control variables included in the regression model, only DR has a significant negative impact on ESG performance which can be seen in Table 5. This means that companies with low debt levels may show good risk management and strong ESG strategy that may enhance company’s ESG performance. In addition, low leverage may show financial stability that companies may be focusing more on ESG investments.

Table 5. Two-way GMM result

|

Corrected |

||

|

ESG |

Coefficient |

P> |z| |

|

ESG |

|

|

|

L1. |

,5895452 |

0.000 |

|

|

|

|

|

DT |

5,704,701 |

0.000 |

|

CE |

-,00000159 |

0.000 |

|

DR |

-3,199,906 |

0.000 |

|

S_GrowthR |

1,905,687 |

0.419 |

|

Sales |

,8416007 |

0.277 |

|

Profitability |

-,4584841 |

0.956 |

|

_cons |

-1,947.527 |

0.328 |

|

AR(1) p-value |

|

0.148 |

|

AR(2) p-value |

|

0.449 |

|

Sargan Test p-value |

0.210 |

|

|

Hansen Test p-value |

0.991 |

|

This study aims to identify the role digital transformation developments and carbon emissions management become the main drivers in improving the ESG performance. The results are as follows. First, this study shows that digital transformation positively correlated with ESG performance. Digital transformation may help in energy efficiency, environmentally friendly supply chain tracking, customer engagement improvement, transparency and accountability accelerated to support data-based decision-making process. Therefore, the use of some technologies such as IoT, data analytics, blockchain, cloud computing, may strengthening the positive impact on ESG. This result is consistent with previous studies from China [24, 35, 36] which find that digital transformation significantly improves ESG performance, and it plays an important role in sustainable development by leveraging digital technologies to optimize resource management in the three key aspects of corporate ESG performance. For the environmental side, digital transformation can increase transparency and accountability for corporate sustainability reporting using the Internet of Things (IoT) and big data analytics [28]. For the social side, digital transformation supports the use of a more efficient company work system, such as the implementation of remote working systems and indirect digital collaboration [24]. For the governance side, digital transformation increases the accountability of company reports through the use of enterprise resource systems that ensure that data recording is done more accurately [4].

Digital transformation may reduce information asymmetry, improve both operational and managerial efficiency, and serves as a strategic enabler to optimize business processes, specifically in enhancing energy efficiency and operational effectiveness. Aligned with the RBV theory, this digital transformation represents valuable, rare, inimitable, and non-substitutable (VRIN) resources that can provide a competitive advantage and strengthen a company's ESG performance [31].

Second, this study found that carbon emissions scope 1 relative to total sales had a significantly negative impact on company's ESG performance. This indicates that ESG performance is negatively affected by scope 1 carbon emissions, measured scope 1 in tons CO2-e divided by total sales. These emissions include direct sources such as fuel combustion from company-owned vehicles or industrial machinery, chemical processes in production, industrial boilers, and manufacturing processes. Since scope 1 carbon emissions released by companies has become one of the items measured in the ESG performance calculation, high scope 1 carbon emissions released may be seen as high-risk business and deteriorate its competitiveness, impacting the ESG performance negatively. The negative impact of carbon emissions on the company's ESG performance is also influenced by several factors, including the level of supervision from regulators on the company's carbon emissions. The study [10] explains that regulators play an essential role in the disclosure of carbon emissions, indicating that companies under close supervision tend to be more transparent in reporting their carbon emissions. In Indonesia, oversight related to carbon emissions is further strengthened by the implementation of a carbon tax, which has been regulated in the Harmonization of Tax Regulations (HPP Law) No. 7 of 2021, which explains that there is an application of carbon tax for companies that produce emissions exceeding the predetermined limit. This regulation, will certainly encourage companies to carry out carbon emission reduction strategies which will ultimately have a significant impact on the ESG performance.

These findings are also consistent with previous studies on LQ45-listed companies indicate that carbon emission reduction enhances firm value when backed by financial stability [42], regional carbon reduction also improve ESG performance by increasing access to green credits and investor scrutiny [40], and effective carbon disclosure in UK can strengthens market valuation. This explains that higher levels of carbon emissions are associated with weaker ESG performance which can make it more challenging for companies to meet environmental regulations, maintain company’s image, and stakeholders’ expectations. To overcome carbon emissions issue, companies are expected to implement some carbon mitigation strategies for enhancing sustainability and improving ESG performance [12, 14]. This perspective aligns with the RBV theory, which posits that a company can achieve a competitive advantage by effectively utilizing their unique resources [14]. Efficient management of carbon emissions is one approach for companies to emphasize strategic value, which ultimately leads to long-term sustainability and aligns with the improvement of the company’s ESG performance [32].

This study extends previous research by analyzing the relationship between implementation of digital transformation and carbon emissions, and corporate ESG performance. The results of this study show a significant positive relationship between digital transformation and corporate ESG performance and a significant negative relationship between carbon emissions and corporate ESG performance. From the study, we identified the role of digital transformation adoption and carbon emissions as catalysts for the ESG performance of manufacturing companies. This study highlights the strategic role of digital transformation and carbon emission management in improving corporate ESG performance.

In addition, it is important to carry out a proactive carbon emission management strategy involving digital transformation innovations that can become a corporate image and meet the expectations of its stakeholders [37]. Companies with high carbon emission levels need to focus on green technology conversion. This will improve their competitive advantage, corporate image and particularly their ESG performance, which in turn will contribute to long-term sustainability and increased stakeholder trust. Moreover, implementing digital transformation in carbon emissions strategies can optimize operational efficiency, drive innovation in business performance through greener practices, and enhance overall sustainability efforts that will strengthen their market presence, attract responsible investors, and align their operations with global sustainability goals.

From this perspective, the results of this study provide important implications for managers, companies, and policymakers regarding the important role of digital technologies and efficient carbon emissions as a catalyst for ESG performance that not only creates short-term value but contributes to broader sustainable development commitments.

For managers, the findings underline the importance of utilizing digital transformation and carbon emissions as a strategic tool to improve long-term ESG performance and stakeholder trust. Firms that align ESG performance goals by implementing efficiency of digital transformation and carbon emissions are more likely to increase business value and attract investors.

For companies, effectively utilizing advancements in digital technology while paying attention to managing their carbon emission may establish an advantage over their competitors, enhancing their corporate reputation and attracting investment.

Policymakers ought to understand the dual impact of digital transformation and efficiency carbon emission on ESG performance. Regulatory frameworks should incentivize companies to implement digital solutions that conserve energy and minimize their carbon emission. Furthermore, policies should help manufacturing sectors shift to low-carbon emissions and technology-driven sustainable practices to increase their ESG performance.

We acknowledge this study has some limitations. First, this study is limited and focused only on manufacturing companies. Therefore, additional studies in different sectors are required to get broader coverage. Thus, researchers can benefit from this study and explore their ideas in ESG performance and innovation development in other manufacturing sectors. Second, in terms of methodology, this study mainly used a textual analysis of keyword collection to build indicators of digital transformation in companies. While we can argue that this method is not the only way to measure digital transformation, it seems to be a relatively reliable proxy for our research. Future studies may use more new indicators and proxies to collect digital transformation data, such as leveraging detailed information on recognized digital intangible assets and "0-1" dummy variable to indicate if companies have experienced digital transformation [35].

Future research may find additional potential variables, such as independent, moderating, control, intervening, and should aim to include a wider range of companies to validate and expand these findings. Therefore, it can explain other variables such as firm value or corporate sustainability [14, 16, 42], corporate innovation, technological innovation, or green innovation [4, 20, 21], and it can be used to reexamine our studies. In addition, future research can use new proxies to determine the limit of carbon emission variables that have opposite effects on ESG performance, such as exploring linear curve models [11, 40].

This study was retrieved from authors’ thesis at Bina Nusantara University.

[1] Chen, X., Despeisse, M., Johansson, B. (2020). Environmental sustainability of digitalization in manufacturing: A review. Sustainability, 12(24): 10298. https://doi.org/10.3390/su122410298

[2] Hazar, A., Babuşcu, S. (2023). Financial technologies: Digital payment systems and digital banking. Today's dynamics. Journal of Research, Innovation and Technologies, 2(2): 162-178. https://doi.org/10.57017/jorit.v2.2(4).04

[3] Zhang, Y., Zhang, Y., Sun, Z. (2023). The impact of carbon emission trading policy on enterprise ESG performance: Evidence from China. Sustainability, 15(10): 8279. https://doi.org/10.3390/su15108279

[4] Kumar, A., Yadav, U.S., Mandal, M., Yadav, S.K. (2024). Impact of corporate innovation, technological innovation and ESG on environmental performance: Moderation test of entrepreneurial orientation and technological innovation as mediator using Sobel test. International Journal of Sustainable Development and Planning, 19(7): 2635-2650. https://doi.org/10.18280/ijsdp.190720

[5] Indonesia Digital 2045. (2024). Menguji Validitas Hasil Perhitungan Progres Transformasi Digital di Uji Publik Indeks TDN - Indonesia Digital 2045. https://digital2045.id/menguji-validitas-hasil-perhitungan-progres-transformasi-digital-di-uji-publik-indeks-tdn/.

[6] Lv, P., Xiong, H. (2022). Can FinTech improve corporate investment efficiency? Evidence from China. Research in International Business and Finance, 60: 101571. https://doi.org/10.1016/j.ribaf.2021.101571

[7] Khan, S.A.R., Yu, Z., Belhadi, A., Mardani, A. (2020). Investigating the effects of renewable energy on international trade and environmental quality. Journal of Environmental Management, 272: 111089. https://doi.org/10.1016/j.jenvman.2020.111089

[8] Worrell, E., Price, L., Neelis, M., Galitsky, C., Zhou, N. (2007). World best practice energy intensity values for selected industrial sectors. Lawrence Berkeley National Laboratory. https://escholarship.org/uc/item/77n9d4sp.

[9] Alhumoudi, H., Alakkas, A.A., Khan, S., Imam, A., Baig, A., Omer, A.M., Khan, I.A. (2024). Carbon management accounting considerations for corporate carbon reduction: The limitations and future of integrating life cycle assessment and material flow cost accounting. International Journal of Sustainable Development and Planning, 19(5): 1971-1979. https://doi.org/10.18280/ijsdp.190536

[10] Xie, H., Qin, Z., Li, J. (2024). ESG performance and corporate carbon emission intensity: Based on panel data analysis of A-share listed companies. Frontiers in Environmental Science, 12: 1483237. https://doi.org/10.3389/fenvs.2024.1483237

[11] Pang, H., Wu, C., Zhang, L. (2024). The impact of green bond issuance on carbon emission intensity and path analysis. PLoS ONE, 19(6): e0304364. https://doi.org/10.1371/journal.pone.0304364

[12] Zhang, Y.J., Sun, Y.F., Huang, J. (2018). Energy efficiency, carbon emission performance, and technology gaps: Evidence from CDM project investment. Energy Policy, 115: 119-130. https://doi.org/10.1016/j.enpol.2017.12.056

[13] Otoritas Jasa Keuangan. (2017). Sal Peraturan Otoritas Jasa Keuangan-Keuangan Berkelanjutan. https://ojk.go.id/id/regulasi/Pages/Penerapan-Keuangan-Berkelanjutan-bagi-Lembaga-Jasa-Keuangan,-Emiten,-dan-Perusahaan-Publik.aspx.

[14] Kurnia, P., Darlis, E., Putr, A.A. (2020). Carbon emission disclosure, good corporate governance, financial performance, and firm value. The Journal of Asian Finance, Economics and Business, 7(12): 223-231. https://doi.org/10.13106/Jafeb.2020.Vol7.No12.223

[15] Khairunnisa, A., Astuti, C.D., Hussein, M.A. (2024). The influence of board diversity and environmental committees on carbon emission disclosures in Southeast Asian corporations. Journal of Green Economy and Low-Carbon Development, 3(1): 26-35. https://doi.org/10.56578/jgelcd030103

[16] Eccles, R.G., Ioannou, I., Serafeim, G. (2014). The impact of corporate sustainability on organizational processes and performance. Management Science, 60(11): 2835-2857. https://doi.org/10.1287/mnsc.2014.1984

[17] Friede, G., Busch, T., Bassen, A. (2015). ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. Journal of Sustainable Finance & Investment, 5(4): 210-233. https://doi.org/10.1080/20430795.2015.1118917

[18] Jin, X., Wu, Y. (2023). The impact of digital investment on corporate ESG performance-the regulatory effect based on the market environment. In Digitalization and Management Innovation II, pp. 400-407. https://doi.org/10.3233/FAIA230753

[19] Peng, Y., Chen, H., Li, T. (2023). The impact of digital transformation on ESG: A case study of Chinese-listed companies. Sustainability, 15(20): 15072. https://doi.org/10.3390/su152015072

[20] Zhao, Q., Li, X., Li, S. (2023). Analyzing the relationship between digital transformation strategy and ESG performance in large manufacturing enterprises: The mediating role of green innovation. Sustainability, 15(13): 9998. https://doi.org/10.3390/su15139998

[21] Zheng, J., Khurram, M.U., Chen, L. (2022). Can green innovation affect ESG ratings and financial performance? Evidence from Chinese GEM listed companies. Sustainability, 14(14): 8677. https://doi.org/10.3390/su14148677

[22] Rossi, C., Byrne, J.G., Christiaen, C. (2024). Breaking the ESG rating divergence: An open geospatial framework for environmental scores. Journal of Environmental Management, 349: 119477. https://doi.org/10.1016/j.jenvman.2023.119477

[23] Zeng, M., Zhu, X., Deng, X., Du, J. (2024). ESG rating uncertainty and institutional investment—Evidence from China. Borsa Istanbul Review, 24(6): 1166-1178. https://doi.org/10.1016/j.bir.2024.07.001

[24] Yang, P., Hao, X., Wang, L., Zhang, S., Yang, L. (2024). Moving toward sustainable development: The influence of digital transformation on corporate ESG performance. Kybernetes, 53(2): 669-687. https://doi.org/10.1108/K-03-2023-0521

[25] Wang, J., Hong, Z., Long, H. (2023). Digital transformation empowers ESG performance in the manufacturing industry: From ESG to DESG. Sage Open, 13(4): 21582440231204158. https://doi.org/10.1177/21582440231 204158

[26] Vial, G. (2019). Understanding digital transformation: A review and a research agenda. The Journal of Strategic Information Systems, 28(2): 118-144. https://doi.org/10.4324/9781003008637

[27] Bharadwaj, A., El Sawy, O.A., Pavlou, P.A., Venkatraman, N.V. (2013). Digital business strategy: Toward a next generation of insights. MIS Quarterly, 37(2): 471-482. https://doi.org/10.25300/MISQ/2013/37:2.3

[28] Li, J.J. (2024). A study on the mechanism of the impact of digital transformation in manufacturing enterprises on sustainable development performance. International Journal of Environmental Impacts, 7(1): 81-92. https://doi.org/10.18280/ijei.070110

[29] Jin, X., Wu, Y. (2024). How does digital transformation affect the ESG performance of Chinese manufacturing state-owned enterprises?—Based on the mediating mechanism of dynamic capabilities and the moderating mechanism of the institutional environment. PLoS ONE, 19(5): e0301864. https://doi.org/10.1371/journal.pone.0301864

[30] Liesen, A., Hoepner, A.G., Patten, D.M., Figge, F. (2015). Does stakeholder pressure influence corporate GHG emissions reporting? Empirical evidence from Europe. Accounting, Auditing & Accountability Journal, 28(7): 1047-1074. https://doi.org/10.1108/AAAJ-12-2013-1547

[31] Zhang, M., Huang, Z. (2024). The impact of digital transformation on ESG performance: The role of supply chain resilience. Sustainability, 16(17): 7621. https://doi.org/10.3390/su16177621

[32] Wedari, L.K., Moradi-Motlagh, A., Jubb, C. (2023). The moderating effect of innovation on the relationship between environmental and financial performance: Evidence from high emitters in Australia. Business Strategy and the Environment, 32(1): 654-672. https://doi.org/10.1002/bse.3167

[33] Columbres, M.R.C., Victoriano, J.M. (2024). Cloud sustainability: An analysis and assessment of the plateau prediction of 2023 Gartner hype cycle for emerging technologies. International Journal of Sustainable Development and Planning, 19(8): 2881-2892. https://doi.org/10.18280/ijsdp.190807

[34] Brummel, L. (2025). Stakeholder involvement as a form of accountability? Perspectives on the accountability function of stakeholder bodies in Dutch public agencies. Public Policy and Administration, 40(1): 27-49. https://doi.org/10.1177/09520767231203283

[35] Xu, G., Ali, D.A., Bhaumik, A. (2023). Does digital transformation promote sustainable development of enterprises: An empirical analysis of a-share listed companies. International Journal of Sustainable Development and Planning, 18(12): 3703-3711. https://doi.org/10.18280/ijsdp.181202

[36] Sang, Y., Loganathan, K., Lin, L. (2024). Digital transformation and firm ESG performance: The mediating role of corporate risk-taking and the moderating role of top management team. Sustainability, 16(14): 5907. https://doi.org/10.3390/su16145907

[37] Houten, E.S., Wedari, L.K. (2023). Carbon disclosure, carbon performance, and market value: Evidence from Indonesia polluting industries. International Journal of Sustainable Development and Planning, 18(6): 1973-1981. https://doi.org/10.18280/ijsdp.180634

[38] Perera, K., Kuruppuarachchi, D., Kumarasinghe, S., Suleman, M.T. (2023). The impact of carbon disclosure and carbon emissions intensity on firms' idiosyncratic volatility. Energy Economics, 128: 107053. https://doi.org/10.1016/j.eneco.2023.107053

[39] Chapple, L., Clarkson, P.M., Gold, D.L. (2013). The cost of carbon: Capital market effects of the proposed emission trading scheme (ETS). Abacus, 49(1): 1-33. https://doi.org/10.1111/abac.12006

[40] Chen, X., Wang, J. (2024). The impact of regional carbon emission reduction on corporate ESG performance in China. Sustainability, 16(13): 5802. https://doi.org/10.3390/su16135802

[41] Basconcillo, J.A., Rimkute, A. (2022). GMM approach to residential electricity consumption in Indonesia. Energy Research Letters, 3: 1-7. https://doi.org/10.46557/001c.33899

[42] Probohudono, A.N., Sangka, K.B., Kurniawati, E.M., Putra, A.A. (2024). Carbon emission and firms' value: Moderating role of financial sustainability. International Journal of Sustainable Development and Planning, 19(10): 3979-3987. https://doi.org/10.18280/ijsdp.191026