Syarief Gerald Prasetya*![]() | Syamsu Alam

| Syamsu Alam![]() | Julia Safitri

| Julia Safitri![]() | Andi Harmoko Arifin

| Andi Harmoko Arifin![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study empirically examines the relationship between risk-taking behavior, green finance, and corporate sustainability performance. Using quantitative methods with Partial Least Square (PLS) analysis, it analyzes 99 observations from 25 companies listed on the Indonesia Stock Exchange (IDX) that published Sustainability Reports during 2013-2022. The results reveal a negative, significant relationship between risk-taking and green finance, but no significant impact on sustainability performance. This suggests that risk-taking hinders green finance effectiveness but does not directly affect sustainability outcomes. The study highlights the need for robust risk management within sustainability frameworks, emphasizing the model's strong predictive power. It provides insights into the interplay between risk-taking and green finance effectiveness, advocating for aligning financial goals with environmental responsibilities. Practically, managers should integrate sustainability into strategic planning, adopt transparent decision-making, and incentivize eco-friendly initiatives. Collaboration with regulators and financial institutions, such as issuing guaranteed green bonds, can mitigate risks and promote green finance adoption. Balancing risk-taking with sustainability is essential to creating long-term corporate and environmental value.

risk-taking, green finance, sustainability performance, IDX, partial least square (PLS)

Environmental degradation arises from humanity's unrestrained exploitation of natural resources to meet its needs. These demands are often addressed through production mechanisms by companies, which frequently overlook environmental sustainability. This neglect is evident in the acquisition of raw materials and the disposal of production waste, which, when untreated, pollutes water, soil, and air. The phenomenon reflects a willingness to take risks in environmental conservation, driven by the goal of maximizing profits [1]. A Gartner survey [2] of 402 American companies revealed that 8% of corporate leaders do not perceive sustainability as important. Regulatory frameworks and legal provisions are essential to raise awareness of the broader impacts of production activities, not only on society but also on managerial and economic decisions [3].

Risk-taking behavior is often regarded as a key driver of innovation, which is critical for achieving sustainability. Sustainable innovation requires courage to explore new approaches, technologies, and processes that enhance resource efficiency, reduce environmental impacts, and create social value. Studies indicate that risk-taking companies are more innovative and achieve better sustainability performance. For instance, Neves et al. [4] demonstrated that companies embracing risk-taking are more likely to invest in sustainable technologies and practices that improve sustainability outcomes. Furthermore, effective risk management is essential for achieving sustainability performance. Companies must identify, assess, and manage environmental, social, and economic risks. Risk-taking in this context involves preparedness to face uncertainty and implement mitigation strategies. Effective risk management enables companies to anticipate sustainability-related risks, ensuring long-term operational stability [5]. However, while risk-taking can drive innovation and sustainability improvements, it also entails challenges and trade-offs. Not all risks yield positive outcomes, and some may result in significant losses. Therefore, balancing risk-taking with careful evaluation is crucial to mitigate unintended negative consequences [2].

In the entrepreneurial context, entrepreneurial orientation as encompassing innovation, risk-taking, and proactiveness relative to competitors [6]. The relationship between entrepreneurial orientation and sustainability performance is complex, with ecological value emerging as a key factor in shaping sustainable businesses. Research by Lüdeke‐Freund [7] shows that entrepreneurship focused on sustainability can drive innovations that address market imperfections, replace unsustainable practices, and create value for various stakeholders.

Achieving sustainability requires decisions about sustainable financing sources, relying on internal and external information at macro and microeconomic levels. This includes financial and non-financial information related to environmental and social issues. Green finance as a foundational tool for building sustainable businesses, facilitating social and economic transformation while mitigating existential threats from climate change [8, 9]. Financial institutions recognize that climate-related risks affect the stability of the financial system [10]. Green finance supports environmentally friendly projects, providing incentives for sustainable investments that not only reduce climate change impacts but also enhance long-term profitability. Recent research indicates that green finance policies improve companies' environmental, social, and governance (ESG) performance, strengthening their sustainability outcomes [6]. Companies that prioritize environmental issues are more proactive in adopting sustainable practices, further reinforcing the link between green finance and sustainability performance [11].

Wales [12] identified five common mediating variables in entrepreneurial orientation research: networking, strategy, organizational structure, organizational learning, and performance. Similarly, studies on sustainable entrepreneurial orientation (GEO) by Amankwah et al. [13] and Olawale [14] use technology, operations, and product variables as mediators. However, prior research has limited exploration of the role of sustainable financial management as a mediator in entrepreneurial orientation studies for achieving sustainable performance. Therefore, this study aims to analyze the influence of risk-taking willingness on sustainable performance, with green finance as a mediating variable.

2.1 Literature review

The sustainability theory developed by Meadows [15] refers to "The Limits to Growth," a report published in 1972 by a team of researchers from the Massachusetts Institute of Technology (MIT). In "The Limits to Growth," Meadows and his team used mathematical models to examine the impact of economic and population growth on natural resources and the environment. They estimated how sustainable economic and population growth would interact with the availability of limited resources and various environmental constraints. This approach emphasizes that there are physical and environmental limits to endless economic growth.

According to sustainability theory, companies must respond to societal expectations, including social, environmental, and economic well-being. This response should meet the needs of both the current and future generations. The concept of sustainability is currently applied in the corporate context. Businesses and investments will thrive through balancing the needs of current and future stakeholders [16, 17]. Sustainability performance measurement is provided by a series of disclosure standards created by the Sustainability Accounting Standards Board (SASB). Corporate sustainability is considered a business and investment strategy that aims to use best business practices to meet and balance the needs of current and future stakeholder.

Henry Mintzberg, one of the first experts to recognize the benefits of strategic models in entrepreneurial organizations, was followed by Miller, who stated that the idea of corporate entrepreneurship deserves scientific attention [18]. Miller argued that corporate entrepreneurship is identified in companies engaged in product-market innovation, undertaking risky ventures, and being pioneers in innovation. The three basic elements—innovation, proactivity, and risk-taking—were identified by Miller [18] as fundamental components of entrepreneurial orientation and are often integrated to create a higher level of entrepreneurial dimensions within a company [19].

Regarding green entrepreneurial orientation, green financing refers to financial investments flowing into sustainability development projects and initiatives, environmental products, and policies that encourage more sustainable economic development [20]. Green funding involves financing climate-related issues but is not limited to them. It also encompasses broader environmental goals such as reducing industrial pollution, providing water sanitation, and protecting biodiversity. The goal of green finance is to mobilize financial resources to address environmental challenges, support sustainable development, and promote the transition to a low-carbon and resource-efficient economy [21].

The strategy of integrating environmental aspects into corporate financial decision-making through green finance does not always produce positive outcomes in generating financial profits [1]. Green finance faces inherent challenges, particularly in developing countries like Indonesia, where regulatory frameworks for environmental and energy policies are frequently revised. For instance, recent changes in renewable energy subsidies and carbon tax regulations have created uncertainty for investors, who often prefer stable long-term returns. This instability discourages companies from fully committing to green finance projects.

According to stakeholder theory, companies prioritize meeting the expectations of key stakeholders, including governments, investors, and the public, by aligning with sustainability standards. While this alignment can drive compliance, it often leads to risk-averse behavior, particularly in adopting innovative but uncertain green initiatives. Legitimacy theory further suggests that companies aim to maintain social legitimacy, prioritizing reputation and regulatory compliance over exploring high-risk, high-reward green innovations. For example, a 2021 study by Smith and Brown found that firms in regulated industries were more likely to invest in incremental improvements rather than disruptive innovations in renewable energy technologies [22].

This approach, while reducing short-term risks, limits the potential for long-term sustainability innovation. By focusing on administrative compliance and reputation management, companies may miss opportunities to develop proactive strategies that could accelerate climate change mitigation and the achievement of sustainable development goals. In the Indonesian context, this risk aversion is exacerbated by the lack of financial incentives and regulatory clarity, further hindering green finance adoption. To overcome these challenges, companies must integrate risk management frameworks with green finance strategies. Collaborations with financial institutions to develop tailored risk mitigation instruments, such as green bonds or climate resilience funds, can provide stability for investors. Additionally, consistent and transparent regulatory frameworks from policymakers are essential to foster confidence in long-term green investments. These measures can shift corporate priorities from mere compliance to innovation-driven strategies, accelerating the sustainability transition and balancing financial and environmental objectives.

Risk management is a structured approach to handling the uncertainties associated with threats [23]. Risks arise from activities undertaken by a company to achieve its strategic objectives. Risks must be managed well to minimize the impact of losses, the primary goal of a company is to seek profit for its owners [24, 25]. However, this pursuit is accompanied by costs and risks that the company must face. Some of these risks include interest rate risk, credit risk, liquidity risk, foreign exchange risk, country or political risk, market risk, off-balance-sheet risk, technological risk, operational risk, and bankruptcy risk [26].

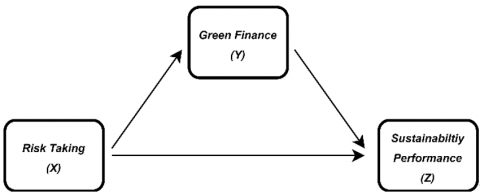

The impact of risks on financial performance shows that complex business development requires a more sophisticated risk management framework at the top organizational level [27, 28]. Companies always aim for growth in their corporate value, and to achieve this, management must face various risks. If a company manages risks well, it faces smaller losses. If risk control is poor, the company will face significant losses, which can cause problems for the company, lead to a decline in business, and ultimately result in bankruptcy. The model of the relationship between variables can be seen in Figure 1 below.

Figure 1. Model of the relationship between variables

Risk management, green finance, and sustainability theory are closely related in the effort to create economically, socially, and environmentally sustainable businesses. Risk management helps companies identify and manage risks associated with unsustainable practices, while green finance mobilizes financial resources for projects that support sustainable environments and communities. Sustainability theory provides a conceptual framework for companies to integrate sustainable practices into their overall business strategies, ensuring that economic, social, and environmental considerations are factored into decision-making. Thus, these three elements work together to help companies achieve their sustainability goals by managing risks, allocating capital, and integrating sustainable values into the corporate structure.

2.2 Research hypotheses

The willingness to take risks plays a significant role in corporate decision-making, particularly in the adoption of green finance and sustainability practices. According to stakeholder theory, companies are motivated to address the expectations of key stakeholders, including investors, regulators, and the public, by integrating sustainable practices into their operations. However, legitimacy theory suggests that companies often prioritize maintaining social legitimacy over exploring risky and innovative solutions, particularly in areas like green finance. This tension between risk-taking and regulatory compliance forms the basis for the hypotheses proposed in this study.

Taking risks in green finance involves investing in initiatives that are often fraught with uncertainty, such as market acceptance, financial risks, and regulatory fluctuations. These uncertainties may deter companies from allocating significant resources to green projects, leading to excessive caution and slowing the flow of capital into sustainable initiatives. Challenges such as information asymmetry and inconsistent standards exacerbate these risks, reducing investor interest and undermining the perceived stability of green finance. Therefore, it is hypothesized that:

H1: There is a negative influence of risk-taking willingness on green finance.

On the other hand, risk-taking is also a critical factor in driving sustainability performance. Companies that embrace risk-taking tend to adopt innovative sustainable practices, such as renewable energy systems or low-carbon production methods, which create long-term value through operational efficiency and reduced environmental impact. Proper risk identification and management allow companies to address uncertainties while setting ambitious goals, such as achieving net-zero emissions or transitioning to 100% renewable energy use. These efforts can also enhance customer trust and investor confidence, providing a competitive advantage. Therefore, it is hypothesized that:

H2: There is a positive influence of risk-taking willingness on sustainability performance.

Green finance serves as a critical enabler in transforming risk-taking behavior into tangible sustainability outcomes. By channeling financial resources into sustainable projects, green finance helps companies address environmental and social risks proactively, avoiding crises such as environmental disasters or regulatory penalties. Additionally, green finance promotes transparency and innovation, fostering long-term growth and competitiveness. It is proposed that green finance acts as a mediating factor, strengthening the relationship between risk-taking willingness and sustainability performance. Hence, the third hypothesis is as follows:

H3: There is a positive influence of risk-taking willingness on sustainability performance through green finance.

The three hypotheses proposed in this study aim to address the complex interplay between risk-taking willingness, green finance, and sustainability performance. The first hypothesis (H1) examines the potential barriers created by risk-taking behavior in the adoption of green finance, highlighting the challenges associated with uncertainty and regulatory inconsistencies. The second hypothesis (H2) shifts the focus to the potential benefits of risk-taking in driving sustainability performance, particularly through innovative practices and ambitious sustainability goals. The third hypothesis (H3) explores the mediating role of green finance, positing that it enables companies to convert risk-taking behaviors into measurable sustainability outcomes.

By integrating these hypotheses, this study seeks to provide a holistic understanding of how risk-taking willingness influences corporate sustainability practices directly and indirectly through green finance. The findings are expected to offer valuable insights for corporate decision-makers and policymakers in designing strategies that balance risk management with the pursuit of sustainability objectives. Moreover, the results will contribute to the existing body of literature on corporate sustainability by elucidating the mechanisms through which risk-taking and green finance interact to shape sustainability performance. This conceptual framework lays the groundwork for the empirical analysis in subsequent sections, where the relationships proposed in these hypotheses will be tested using data from companies listed on the Indonesia Stock Exchange (IDX) that have published sustainability reports. The goal is to generate actionable recommendations for fostering sustainable business practices while mitigating the risks associated with green finance investments.

The population in this study consists of all companies listed on the Indonesia Stock Exchange (IDX) in 2022, totaling 825 issuers. The research sample was selected using non-probability sampling with a purposive sampling method, which involves non-random sample selection based on the following criteria: (1) listed on the Indonesia Stock Exchange in 2022, (2) issued a Sustainability Report from 2013-2022, and (3) included in the SRI-KEHATI index. Based on these predetermined criteria, only 25 out of the 825 listed issuers met the criteria. Data analysis utilized secondary company data obtained through library research sourced from the Sustainability Reports of companies listed on the IDX from 2013 to 2022, resulting in a total of 250 observations from 25 companies.

The data analysis used in this research is Partial Least Square Path Modeling with a Structure Variance approach, specifically Structural Equation Modeling (SEM) using the Partial Least Square (PLS) method. The Partial Least Squares Structural Equation Modeling (SEM PLS) analysis in this study is employed to analyze panel data, aiming to model and understand the relationships between observed variables consisting of several business units over multiple time periods. The structural model testing aims to determine the percentage of variation explained by the exogenous variables for each endogenous variable in the model. The assessment of the structural model can be done by considering the significance probability. This serves as a reference for accepting or rejecting statistical hypotheses. In this case, a significance level of 5% or P < 0.05 is used, and the critical ratio (c.r) value must be greater than 1.96. The goodness of fit (GoF) value is used as an indicator for comparing the specified model with the covariance matrix between the indicators or observed variables. If the GoF produces a good value, then the results of the model are accepted. However, if the GoF value is not good, the model results must be rejected or the model needs to be revised. Variable measurement in this study uses proxy values, which can be seen in Table 1.

Table 1. Measurement of research variables

|

Variables |

Proxy |

Information |

|

Sustainability Performance |

Disclosure score = the total number of items disclosed divided by the total number of core items disclosed based on the type of GRI index used. |

|

|

Green Finance [29] |

environmental and climate investment proportionTotal Asset |

|

|

Taking Risk [30] |

Debt-to-Equity Ratio Total DebtEquity |

|

The econometric equation model of the influence of risk-taking willingness on sustainability performance through green finance is as follows:

GF=−β1TR+ε (1)

CSP=β2TR+ε (2)

CSP=β3GF+δ2TR+ε (3)

CSP=β4GF+ε (4)

TR : Risk-taking willingness (independent variable).

GF : Green finance (mediating variable).

CSP : Sustainability performance (dependent variable).

ε : Error term.

β1 : The direct influence of TR on GF.

β2 : The direct influence of TR on CSP without passing through GF.

β3 : The influence of GF on CSP.

δ2 : The combined direct and indirect influence of TR on CSP through GF.

The Q-square (Q²) test is used to measure how well a statistical model or predictive model generates observed values and estimates the parameters within the model [31]. The Robustness test is used to assess the reliability and consistency of findings by testing various model specifications or methodological changes [32]. This test is crucial for evaluating the sensitivity of results to different assumptions or parameters in the analysis, ensuring the robustness and generalizability of the conclusions [33].

The mediation model test aims to understand the extent to which a mediating variable influences the relationship between the independent variable and the dependent variable [34]. A variable acts as a mediator when the previously significant relationship between the independent and dependent variables is no longer significant, with the strongest demonstration of mediation occurring when the indirect path is zero [35].

4.1 Results

This research uses panel data, a statistical approach that allows the analysis of data from various units over one or several periods. The balanced panel data used in this study includes 250 observations. However, the presence of many empty cells in the data requires special handling steps. Removing incomplete data is crucial to ensure the accuracy of the analysis and the interpretation of the research results. By using only complete samples, researchers can avoid biases that may arise from incomplete or invalid data [36]. Consequently, the number of observations is reduced to 99, making the analysis more focused and concentrated on relevant information.

Data analysis in this research employs SEM PLS (Structural Equation Modeling Partial Least Squares) [37-39]. SEM PLS is chosen because it can maximize the use of available data and reduce the impact of missing data. According to Memon et al. [40], a practical rule in statistical analysis is to have at least 10 samples per independent variable. Therefore, with 99 observations, the use of SEM PLS is recommended in this study. The results of the descriptive statistical processing can be seen in Table 2.

Table 2. Descriptive statistics

|

Variable |

N |

Min |

Max |

Mean |

Std. Deviation |

Variance |

|

Risk Taking |

99 |

.153 |

7.257 |

2.59092 |

2.469482 |

6.098 |

|

Green Finance |

99 |

.010 |

.930 |

.14725 |

.220067 |

.048 |

|

Sustainablity Performace |

99 |

3.000 |

77.000 |

25.9899 |

15.348001 |

235.561 |

|

Valid N (listwise) |

99 |

|

|

|

|

|

In the analysis of the risk-taking level, it was found that the minimum value in the sample is 0.153, which is quite low and indicates cases with very minimal risk levels. Conversely, the maximum value reaches 7,257, indicating cases with high-risk levels. The average risk-taking level is approximately 2.59092, reflecting the median value of the data collected. A standard deviation of 2.4694 indicates some variation in risk-taking levels among the data, although this variation is not very large. Overall, the risk-taking level in the sample shows moderate variation, with the average being at a medium level.

Table 3. Correlation results

|

Variables |

Risk Taking |

Green Finance |

Sus. Perform |

|

|

Risk Taking |

Pearson Correlation |

1 |

|

|

|

Sig (2-tailed) |

|

|

|

|

|

N |

99 |

|

|

|

|

Green Finance |

Pearson Correlation |

-.429** |

1 |

|

|

Sig (2-tailed) |

.000 |

|

|

|

|

N |

99 |

99 |

|

|

|

Sustainablity Performance |

Pearson Correlation |

-.284** |

.141 |

1 |

|

Sig (2-tailed) |

.004 |

.164 |

|

|

|

N |

99 |

99 |

99 |

|

In Table 3, it can be seen that there is a significant negative relationship between the risk-taking level and green finance of (-0.429), indicating that the higher the risk-taking level, the lower the implementation of green finance. It should be noted that there is a significant negative correlation between the risk-taking level and the Sustainability Performance variable of -0.284 with a significance value of 0.004. In this context, the analysis results show that changes in the risk-taking level significantly affect the Sustainability Performance variable. The correlation analysis shows weak and insignificant coefficients, indicating that the relationships between these variables are not strong, thus avoiding multicollinearity issues. This helps prevent problems in model interpretation, such as unstable estimation coefficients and increased standard variability, which can interfere with the assessment of statistical significance.

Table 4. Hypothesis testing

|

Hypothesis |

Path Coef |

P |

Stat Test |

Concl |

|

- Risk willingness towards green finance |

-0.349 |

0.000 |

Ho: βx ≤ 0<br>Ha: βx > 0 |

Accepted |

|

- Risk willingness towards sustainability performance |

-0.038 |

0.769 |

Ho: βx ≤ 0<br>Ha: βx > 0 |

Rejected |

|

- Green finance towards sustainability performance |

0.075 |

0.518 |

Ho: βy ≤ 0<br>Ha: βy > 0 |

Rejected |

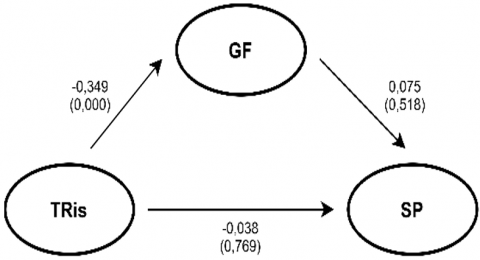

In Table 4, it can be seen that there is a significant influence between Risk Taking and Green Finance with a regression coefficient of -0.349, indicating that an increase in Risk Taking is significantly associated with a decrease in the implementation of Green Finance. The t-statistic value of 7.536 and p-value of 0.000 (less than 0.05) indicate a statistically significant influence. These results are consistent with the study by Zhang et al. [41] and Strategic Management Theory by Henry [42], showing a significant influence between Risk Taking and Green Finance. There is not enough evidence to state a significant relationship between Risk Taking and Sustainability Performance, with a coefficient of -0.038, t-statistic value of 0.296, and p-value of 0.769 indicating that an increase in Risk Taking does not significantly affect Sustainability Performance. The influence of Green Finance on Sustainability Performance is also not significant, with a regression coefficient of 0.588, a t-statistic value of 0.647, and a p-value of 0.518 (greater than 0.05), indicating insufficient evidence to state a statistically significant influence between Green Finance and Sustainability Performance.

Table 5. Sobel test

|

Structural Model |

+/- |

β |

Sobel Test Stat |

Sig |

Conclusion |

|

|

One-tailed Prob |

Two-tailed Prob |

|||||

|

Tris → GF →SP |

- |

0.026 |

-0.644 |

0.2597 |

0.5194 |

Rejected |

Table 5 presents the hypothesis testing, which examines the influence of risk-taking willingness on sustainability performance through green finance (GF), the Sobel statistical test result shows a value of -0.644 with a one-tailed significance value of 0.2597 and a two-tailed significance value of 0.5194, both of which are greater than 0.05. Therefore, the statistical hypothesis (H0) is accepted, and the research hypothesis is rejected.

Table 6. Results of direct and indirect influence

|

Structural Model |

Direct |

Indirect |

Total |

|

TRis → SP |

-0.038 |

- |

-0.038 |

|

TRis → GF |

-0.349 |

- |

-0.349 |

|

GF → SP |

0.075 |

- 0.026 |

0.049 |

Table 6 shows that green finance (GF) has both a direct and an indirect impact on sustainability performance (SP), with values of 0.075 and -0.026, respectively. The total impact of green finance (GF) on sustainability performance (SP) is 0.049, and the direct influence of decision-making willingness (TRis) on sustainability performance (SP) is -0.038. In the mediation test, as shown in Figure 2, it is found that there is no mediation of the GF variable explaining the influence of risk-taking on sustainability performance.

Figure 2. No mediation

Based on the Q-square (Q²) test in Table 7, it can be inferred that both variables have sufficiently good predictive validity, with Q2 values > 0, although there may be differences in the strength of their predictions.

Table 7. Q-square test

|

Variables |

Q-Square |

|

Green Finance |

0.148 |

|

Sus Performance |

0.062 |

The Goodness-of-Fit (GOF) test is a process to evaluate how well a hypothesis model fits the observed data. This test is used to assess whether the statistical model used is compatible with the actual data distribution. In Figure 3 below, the results of the data processing are as follows:

Figure 3. Hypothesis model

Table 8. Goodness of fit model test

|

|

Saturated Model |

Estimated Model |

|

SRMR |

0.000 |

0.007 |

|

d_ULS |

0.000 |

0.001 |

|

d_G |

0.000 |

0.000 |

|

Chi-Square |

|

0.207 |

|

NFI |

1.000 |

0.998 |

The GOF test in Table 8 demonstrates that the estimated hypothesis model effectively represents the data. The SRMR, d_ULS, d_G, Chi-Square, and NFI values all support the model's fit with the data.

In this study, a robustness test was conducted by replacing the Sustainability Performance variable with an alternative proxy, namely Return on Investment (ROI). The argument that ROI has a close relationship with a company's sustainability performance is explained by the benefits obtained by companies that focus on sustainability. Sustainable companies tend to reduce waste, save resources, and lessen environmental impact through improved operational processes. These measures not only have a positive impact on the environment but also improve the company's financial reports, thereby increasing ROI.

Table 9. Robustness test in the structural model

|

Variable |

Estimate |

S.E. |

C.R. |

P-Value |

Conclusion |

||

|

Taking Risk |

→ |

Green Finance |

-0.349 |

0.044 |

7.945 |

0.000* |

Accepted |

|

Taking Risk |

→ |

ROI |

-0.279 |

0.098 |

2.841 |

0.005 |

Accepted |

|

Green Finance |

→ |

ROI |

-0.028 |

0.122 |

0.232 |

0.816 |

Rejected |

|

SRMR |

|

|

0.007 |

|

|

|

Fit |

|

Chi-Square |

|

|

0.207 |

|

|

|

Fit |

|

NFI |

|

|

0.998 |

|

|

|

Fit |

The data processing results in Table 9 show that the TRis variable on GF exhibits high significance with a p-value of 0.000 and a negative direction, indicating a significant negative influence. This result is consistent with previous analysis, thus the hypothesis is accepted and the results are robust. The TRis variable on ROI also shows significance with a p-value of 0.005 and a negative direction, indicating a significant negative influence. This hypothesis is accepted and the coefficient direction is consistent, although previous analyses showed a p-value of 0.769 and a negative direction, remaining consistent in the coefficient direction. Testing GF on ROI shows a p-value of 0.816 with a negative direction, leading to the conclusion that GF does not have a significant influence on ROI. This result is consistent with previous analyses which showed a positive but not significant influence on SP, thus the hypothesis is not accepted and the results remain consistent (robust).

4.2 Discussion

The results show a significant negative influence between risk-taking willingness and green finance, with a regression coefficient of -0.349 (p-value = 0.000). This indicates that higher levels of risk-taking in companies are associated with lower implementation of green finance. These findings align with Fernandes et al. [43], who suggest that high-risk behavior can create an unstable business environment and reduce commitment to sustainable financial practices. Factors such as the long-term nature of green finance returns, information asymmetry, inconsistent standards, and psychological barriers exacerbate these challenges. As a relatively new concept, green finance faces substantial competition from well-established conventional finance, particularly in markets like Indonesia, where supporting policies remain underdeveloped. This condition slows the flow of capital to sustainable projects. To address these issues, it is recommended to implement strategic measures, including creating a supportive business climate, providing financial incentives, and clarifying green finance standards to build investor trust.

Meanwhile, no significant influence was found between risk-taking willingness and sustainability performance, with a coefficient of -0.038 (p-value = 0.769). This result indicates that risk-taking behavior does not directly impact a company’s sustainability performance. Furthermore, this finding aligns with the study by He et al.[44], which highlights a trade-off between sustainable growth and corporate risk-taking behavior. Companies with high-risk tendencies often suffer significant losses that undermine their sustainability efforts, such as bankruptcy risks caused by excessive debt. Historical examples, such as the 2008 financial crisis and the collapse of Enron, illustrate how uncontrolled risk-taking can have severe consequences for companies, society, and the environment. Additionally, financial institutions and credit rating agencies tend to assign lower ratings to high-risk companies, making it difficult for them to access affordable capital for sustainability investments.

In the mediation test, green finance did not significantly mediate the relationship between risk-taking willingness and sustainability performance. The Sobel test result showed a value of -0.644 with a p-value > 0.05, indicating that the mediation hypothesis was rejected. This suggests that green finance is not a primary determinant of a company’s sustainability performance. Instead, internal factors such as management commitment, environmental policies, and energy efficiency play a more significant role in driving sustainability [45]. In Indonesia’s banking sector, while some banks, such as BNI and BRI, have limited credit allocations to unsustainable sectors, most financing still supports industries such as coal. For instance, Bank Mandiri remains the largest financier of the coal industry, with total financing of IDR 69.3 trillion during 2018-2020. This underscores that while green finance is relevant, it is yet to become a core strategy in business practices.

The findings of this study carry several important implications. First, clearer regulations and financial incentives are needed to attract private capital into sustainable projects, such as renewable energy and energy efficiency initiatives. Second, companies must integrate better risk management practices with sustainable financial strategies to balance growth with environmental responsibility. Third, collaboration among governments, regulators, and industries is crucial to develop tailored financial instruments and reduce investment barriers for sustainable projects. Overall, this study highlights the complexity of the relationship between risk-taking, green finance, and sustainability performance. While green finance is important, its effectiveness is heavily influenced by external factors, such as government regulations and market dynamics. Therefore, collaborative efforts are needed to create a more conducive investment ecosystem for sustainability.

This study emphasizes the need to balance short-term financial gains with long-term sustainability. Managers can adopt a more measured, risk-based approach by incorporating long-term environmental and social impact analyses into strategic planning. Integrating sustainability factors into investment decision-making ensures that financial decisions consider long-term benefits, even if these take longer to materialize. Additionally, incentive-based approaches, such as subsidies for environmentally friendly projects, can motivate investors and stakeholders to prioritize sustainability.

Promoting the adoption of green finance in risk-averse environments requires specific strategies. Collaborative efforts with regulators and financial institutions to develop safer and more secure financial instruments, such as green bonds with guarantees or insurance, can help reduce uncertainty. These strategies provide evidence that the long-term benefits of green investments can outweigh concerns over short-term risks.

The limitations of this study must be acknowledged. The findings primarily reflect trends in economically and governance-established companies with high levels of disclosure, making the conclusions less applicable to companies with limited sustainability reporting. The reliance on disclosure scores as indicators could be strengthened by integrating actual performance data for a more comprehensive analysis.

Future research could expand the scope by including companies outside the SRI-KEHATI index. Developing research instruments to assess sustainability practices in organizations without formal sustainability reports would provide valuable insights. Additionally, future studies could incorporate primary data, such as surveys or interviews, to include companies with limited disclosure and better understand the challenges they face in sustainability reporting.

[1] Prasetya, S.G., Safitri, J. (2023). The effect of environmental management accounting (EMA) on financial performance and working capital management (WCM) as mediating variables. Jurnal Manajemen, 14(1): 14. https://doi.org/10.32832/jm-uika.v14i1.9778

[2] Gartner. (2021). Sustainability in corporate decision-making. https://investor.gartner.com/static-files/fbdcd9d0-f76f-494e-807b-f6b0ee89995a.

[3] Statovci, B., Asllani, G., Zeqaj, B., Avdyli, E., Grima, S. (2023). The impact of corporate governance practices on financial performance in Western Balkan countries. International Journal of Sustainable Development and Planning, 18(9): 2635-2642. https://doi.org/10.18280/ijsdp.180902

[4] Neves, C., Oliveira, T., Santini, F. (2022). Sustainable technologies adoption research: A weight and meta-analysis. Renewable and Sustainable Energy Reviews, 165: 112627. https://doi.org/10.1016/j.rser.2022.112627

[5] Settembre-Blundo, D., González-Sánchez, R., Medina-Salgado, S., García-Muiña, F.E. (2021). Flexibility and resilience in corporate decision making: A new sustainability-based risk management system in uncertain times. Global Journal of Flexible Systems Management, 22(S2): 107-132. https://doi.org/10.1007/s40171-021-00277-7

[6] Ruiz-Ortega, M.J., Parra-Requena, G., García-Villaverde, P.M. (2021). From entrepreneurial orientation to sustainability orientation: The role of cognitive proximity in companies in tourist destinations. Tourism Management, 84: 104265. https://doi.org/10.1016/j.tourman.2020.104265

[7] Lüdeke‐Freund, F. (2020). Sustainable entrepreneurship, innovation, and business models: Integrative framework and propositions for future research. Business Strategy and the Environment, 29(2): 665-681. https://doi.org/10.1002/bse.2396

[8] Chuahan, R., Chavda, K. (2024). Unveiling the nexus: Exploring the impact of behavioral finance on green finance initiatives. Journal of Environmental Economics and Sustainability, 1(2): 1-12. https://doi.org/10.47134/jees.v1i2.181

[9] Li, W. (2024). Energy finance and carbon finance: Key roles of the financial community in addressing climate change. International Journal of Social Sciences and Public Administration, 2(2): 307-316. https://doi.org/10.62051/ijsspa.v2n2.43

[10] Chabot, M., Bertrand, J.-L. (2023). Climate risks and financial stability: Evidence from the European financial system. Journal of Financial Stability, 69: 101190. https://doi.org/10.1016/j.jfs.2023.101190

[11] Hussain, S., Rasheed, A., ur Rehman, S. (2024). Driving sustainable growth: Exploring the link between financial innovation, green finance and sustainability performance: Banking evidence. Kybernetes, 53(11): 4678-4696. https://doi.org/10.1108/K-05-2023-0918

[12] Wales, W.J. (2013). Entrepreneurial orientation and performance: Mediating variables in sustainability. Journal of Business Venturing, 28(1): 69-85.

[13] Amankwah, A., Sarfo, D., Asante, E. (2018). Mediating variables in sustainable entrepreneurial orientation. Journal of Business and Sustainability, 12(3): 211-229.

[14] Olawale, O. (2019). Sustainable entrepreneurial orientation and firm performance. African Journal of Business Management, 13(5): 122-130.

[15] Meadows, D.H. (1972). The limits to growth: A report for the Club of Rome’s project on the predicament of mankind. Universe Books.

[16] Kumar, V., Ramachandran, D. (2021). Developing firms’ growth approaches as a multidimensional decision to enhance key stakeholders’ wellbeing. International Journal of Research in Marketing, 38(2): 402-424. https://doi.org/10.1016/j.ijresmar.2020.09.004

[17] Allioui, H., Mourdi, Y. (2023). Exploring the full potentials of IoT for better financial growth and stability: A comprehensive survey. Sensors, 23(19): 8015. https://doi.org/10.3390/s23198015

[18] Miller, D. (1978). Entrepreneurship as a process of innovation, risk-taking, and proactivity. Strategic Management Journal, 9(2): 165-180.

[19] Hamdan, Y., Alheet, A.F. (2020). Influence of organisational culture on pro-activeness, innovativeness and risk-taking behaviour of SMEs. Entrepreneurship and Sustainability Issues, 8(1): 203-217. https://doi.org/10.9770/jesi.2020.8.1(13)

[20] Zi, H. (2023). Role of green financing in developing sustainable business of e-commerce and green entrepreneurship: Implications for green recovery. Environmental Science and Pollution Research, 30(42): 95525-95536. https://doi.org/10.1007/s11356-023-28970-3

[21] Bai, C. (2024). Financial development for sustainable resource efficiency: Fostering green growth in natural resource markets. Resources Policy, 89: 104539. https://doi.org/10.1016/j.resourpol.2023.104539

[22] Kivimaa, P., Laakso, S., Lonkila, A., Kaljonen, M. (2021). Moving beyond disruptive innovation: A review of disruption in sustainability transitions. Environmental Innovation and Societal Transitions, 38: 110-126. https://doi.org/10.1016/j.eist.2020.12.001

[23] Smith, P.G., Merritt, G.M. (2020). Proactive risk management. Productivity Press. https://doi.org/10.4324/9780367807542

[24] Mayer, C. (2021). The future of the corporation and the economics of purpose. Journal of Management Studies, 58(3): 887-901. https://doi.org/10.1111/joms.12660

[25] George, G., Haas, M.R., McGahan, A.M., Schillebeeckx, S.J.D., Tracey, P. (2023). Purpose in the for-profit firm: A review and framework for management research. Journal of Management, 49(6): 1841-1869. https://doi.org/10.1177/01492063211006450

[26] Zekos, G.I. (2021). Risk management developments. In Economics and Law of Artificial Intelligence (pp. 147-232). Cham: Springer International Publishing. https://doi.org/10.1007/978-3-030-64254-9_5

[27] Dvorsky, J., Belas, J., Gavurova, B., Brabenec, T. (2021). Business risk management in the context of small and medium-sized enterprises. Economic Research-Ekonomska Istrazivanja, 34(1): 1690-1708. https://doi.org/10.1080/1331677X.2020.1844588

[28] Saeidi, P., Saeidi, S.P., Gutierrez, L., Streimikiene, D., Alrasheedi, M., Saeidi, S.P., Mardani, A. (2021). The influence of enterprise risk management on firm performance with the moderating effect of intellectual capital dimensions. Economic Research-Ekonomska Istrazivanja, 34(1): 122-151. https://doi.org/10.1080/1331677X.2020.1776140

[29] Mohsin, M., Dilanchiev, A., Umair, M. (2023). The impact of green climate fund portfolio structure on green finance: Empirical evidence from EU countries. Ekonomika, 102(2): 130-144. https://doi.org/10.15388/Ekon.2023.102.2.7

[30] Gunawan, R., Widiyanti, M., Malinda, S., Adam, M. (2022). The effect of current ratio, total asset turnover, debt to asset ratio, and debt to equity ratio on return on assets in plantation sub-sector companies listed on the Indonesia stock exchange. International Journal of Economic, Business, Accounting, Agriculture Management and Sharia Administration, 2(1): 19-28. https://doi.org/10.54443/ijebas.v2i1.139

[31] Hermansyah, M., Santoso, I., Wijana, Sucipto, Fudholi, A. (2021). Implementation of participatory rural appraisal (PRA) in empowering gaplek SMEs using partial least square (PLS) analysis. International Journal of Sustainable Development and Planning, 16(3): 543-550. https://doi.org/10.18280/ijsdp.160315

[32] Subbaswamy, A., Adams, R., Saria, S. (2021). Evaluating model robustness and stability to dataset shift. In Proceedings of Machine Learning Research, 130: 2611-2619.

[33] Karunarathna, I., Gunasena, P., Hapuarachchi, T., Ekanayake, U., Rajapaksha, S., Gunawardana, K., Aluthge, P., Bandara, S., Jayawardana, A., De Alvis, K., Gunathilake, S. (2024). The crucial role of data collection in research: Techniques, challenges, and best practices. ResearchGate. https://www.researchgate.net/publication/383155720.

[34] Abu-Bader, S., Jones, T.V. (2021). Statistical mediation analysis using the Sobel test and Hayes SPSS process macro. SSRN. https://ssrn.com/abstract=3799204.

[35] Tofighi, D., Kelley, K. (2020). Indirect effects in sequential mediation models: Evaluating methods for hypothesis testing and confidence interval formation. Multivariate Behavioral Research, 55(2): 188-210. https://doi.org/10.1080/00273171.2019.1618545

[36] Mirzaei, A., Carter, S.R., Patanwala, A.E., Schneider, C.R. (2022). Missing data in surveys: Key concepts, approaches, and applications. Research in Social and Administrative Pharmacy, 18(2): 2308-2316. https://doi.org/10.1016/j.sapharm.2021.03.009

[37] Ringle, C.M., Sarstedt, M., Mitchell, R., Gudergan, S.P. (2020). Partial least squares structural equation modeling in HRM research. The International Journal of Human Resource Management, 31(12): 1617-1643. https://doi.org/10.1080/09585192.2017.1416655

[38] Lin, H., Lee, M., Liang, J., Chang, H., Huang, P., Tsai, C. (2020). A review of using partial least square structural equation modeling in e‐learning research. British Journal of Educational Technology, 51(4): 1354-1372. https://doi.org/10.1111/bjet.12890

[39] Hair, J., Alamer, A. (2022). Partial least squares structural equation modeling (PLS-SEM) in second language and education research: Guidelines using an applied example. Research Methods in Applied Linguistics, 1(3): 100027. https://doi.org/10.1016/j.rmal.2022.100027

[40] Memon, M.A., Ting, H., Cheah, J.-H., Thurasamy, R., Chuah, F., Cham, T.H. (2020). Sample size for survey research: Review and recommendations. Journal of Applied Structural Equation Modeling, 4(2): i-xx. https://doi.org/10.47263/JASEM.4(2)01

[41] Zhang, S., Wu, Z., Wang, Y., Hao, Y. (2021). Fostering green development with green finance: An empirical study on the environmental effect of green credit policy in China. Journal of Environmental Management, 296: 113159. https://doi.org/10.1016/j.jenvman.2021.113159

[42] Henry, A. (2021). Understanding Strategic Management. Oxford University Press.

[43] Fernandes, D., Lynch Jr., J.G., Netemeyer, R.G. (2014). Financial literacy, financial education, and downstream financial behaviors. Management Science, 60(8): iv-vii, 1861-2109. https://doi.org/10.1287/mnsc.2013.1849

[44] He, F., Qian, C., Liu, Y. (2023). Balancing risk and sustainability in corporate finance. Journal of Financial Studies, 27(4): 315-332. https://doi.org/10.1016/j.fin.2023.06.003

[45] Akbar, Salam, M., Arsyad, M., Rahmadanih. (2023). The role of human capital in strengthening horticultural agribusiness institutions: Evidence from structural equation modeling. International Journal of Sustainable Development and Planning, 18(9): 2839-2846. https://doi.org/10.18280/ijsdp.180922