Ibrahim Hassan Mohamud*![]() | Zakarie Abdi Warsame

| Zakarie Abdi Warsame![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study examines the effects of external debt (ED) and foreign direct investment (FDI) on economic growth in Somalia from 1990 to 2021, employing the autoregressive distributed lag (ARDL) model to analyze data sourced from the World Bank, SESRIC, and World Data. The ARDL model, chosen for its ability to handle the variables' integration properties, reveals significant long-term and short-term relationships between ED, FDI, and economic growth. In the long run, the findings indicate that both ED and FDI positively impact economic growth, with a 1% increase in ED and FDI associated with a 1.7939% and 0.0788% increase in GDP, respectively. Short-run results further suggest immediate adjustments towards long-term equilibrium, highlighted by the Error Correction Term, which corrects about 23.37% of disequilibrium annually. Policy implications drawn from the study emphasize the critical role of FDI and ED in fostering Somalia's economic development. The positive long-term effects of ED and FDI on GDP growth suggest that strategic management of external debt and encouraging foreign direct investment can significantly contribute to sustainable economic growth. Policymakers are advised to create favorable conditions for FDI and to utilize external debt responsibly, ensuring that borrowed funds are invested in productive sectors that stimulate economic expansion and development.

economic growth, external debt, foreign direct investment, ARDL model, Somalia

The nexus between external debt (ED), foreign direct investment (FDI), and economic growth has garnered substantial attention in development economics. Scholars and policymakers alike have explored how these financial variables interact to influence the trajectory of national economies, particularly in developing countries. The prevailing consensus underscores the complexity of these relationships, suggesting that while FDI is often seen as a catalyst for economic development, offering capital, technology, and managerial expertise [1], the impact of external debt is more nuanced, with potential to both support and hinder economic progress [2].

The discourse on external debt and FDI is enriched by the debate on their roles in promoting sustainable economic growth. On one hand, FDIs are posited to directly contribute to capital formation, job creation, and technology transfer [3]. Conversely, the accumulation of external debt raises concerns about debt sustainability and the risk of debt distress, which can deter investment and growth [4, 5]. The differential impacts of these financial inflows on economic growth underscore the importance of effective management and policy frameworks that can leverage their benefits while mitigating associated risks [6].

The interplay between external debt, FDI, and economic growth in Somalia presents a unique case study. Despite significant challenges, including political instability and security issues, Somalia has shown resilience and a potential for economic recovery [7]. External debt in Somalia has historically been burdensome, with the country making strides towards debt relief under the Heavily Indebted Poor Countries (HIPC) initiative to alleviate its debt overhang and free up resources for development [8]. FDI flows into Somalia have been modest but show growth, particularly in the telecommunications, agriculture, and energy sectors, indicating a slowly improving investor confidence [9].

The influx of foreign debt stands as the primary form of foreign capital in East Africa, contributing to the escalation of the region's external debt to $102.25 billion by the end of 2017. This surge resulted in a notable increase in the debt-to-GDP ratio for East African nations, rising from 40.1% in 2014 to 51.9% by 2018. For Somalia specifically, its external public debt in 2017 was estimated at US$2.8 billion. Within Somalia's 27 creditors, categorized into the non-Paris Club group (13.4%), multilateral group (32.8%), and Paris Club group (53.8%), key creditors include Italy (13%), the United States (22%), France (9%), the International Monetary Fund (7%), and the World Bank (11%). Noteworthy rescheduling and cancellations occurred, with Saudi Arabia rescheduling approximately US$106 million in 2016, while China has entirely annulled Somalia's debt [10].

However, the economic impact of these financial inflows has been mixed. While debt relief efforts are improving Somalia's fiscal space, utilizing these resources and managing new borrowing are critical for sustaining economic growth. Similarly, while FDI has the potential to contribute to economic development, its impact is contingent upon the stability of the investment climate and the effectiveness of policy frameworks in place [11].

Notwithstanding the growing body of literature on external debt, FDI, and economic growth, there remains a significant gap in the context of Somalia. Existing studies often lack a comprehensive analysis that integrates the effects of external debt and FDI with Somalia's unique socio-economic and political landscape. Moreover, there is a dearth of empirical research exploring how these financial inflows interact with domestic factors to influence economic growth in Somalia. This study aims to bridge this gap by providing an in-depth analysis of the effects of external debt and FDI on economic growth, considering the country's specific challenges and opportunities.

The relationship between external debt and economic growth has been extensively analyzed in the literature, revealing a multifaceted interaction. Hassan and Meyer [12], discuss how high levels of external debt, or a 'debt overhang,' can discourage investment by creating uncertainty over the economic future, potentially leading to higher taxes or inflation. This viewpoint is supported by the work of Casares [13], who argues that prudent management of external debt can, conversely, enable countries to finance development projects, boosting economic growth. The concept of a debt threshold, beyond which the impact of debt on growth turns negative, has been empirically supported by the study [14] and further examined by the study [15] who suggest that excessive debt levels are correlated with lower rates of economic growth.

Further exploration into the nuances of external debt's impact on growth has been undertaken by the study [16, 17] who emphasize the importance of how borrowed funds are utilized. Investments in productive public infrastructure, education, and health can yield positive returns and stimulate economic growth, suggesting that the quality of expenditure is crucial [18]. Delve into the conditions under which debt might foster growth, highlighting the roles of good governance, transparent financial management, and sustainable borrowing practices. These studies collectively underscore the delicate balance between leveraging external debt for development and avoiding the pitfalls of unsustainable debt accumulation.

The debate around external debt and growth also includes the impact of international debt relief initiatives. Research by Turan and Yanıkkaya [19] evaluates the effectiveness of debt relief programs in fostering economic growth in heavily indebted poor countries (HIPC), suggesting that debt relief can contribute to economic stability and growth by reducing debt service obligations and freeing up resources for development expenditure. However, Manasseh et al. [20] caution that debt relief alone is insufficient without accompanying structural reforms to improve fiscal management, governance, and investment in human capital. This body of literature indicates that while external debt has the potential to influence economic growth positively, its actual impact is contingent upon a complex interplay of factors, including debt levels, the use of debt-financed resources, and broader economic and policy contexts.

The impact of foreign direct investment (FDI) on economic growth has been a significant focus of development economics, with a consensus emerging on its potential benefits. Magazzino and Mele [21] provide evidence that FDI contributes to economic growth through mechanisms such as technology transfer, skill enhancement, and the creation of employment opportunities. These benefits, however, are not automatic and are influenced by the host country's absorptive capacity, including the level of education, infrastructure, and regulatory framework, as suggested by Wu et al. [22]. The role of policy and institutional frameworks in maximizing the benefits of FDI is further emphasized by the study [23], who argue that open trade policies, a stable macroeconomic environment, and strong legal institutions are crucial for attracting FDI and leveraging its growth-enhancing effects.

Despite the potential benefits, the impact of FDI on economic growth is not uniformly positive across all contexts. Sugiharti et al. [24] highlighted the potential for negative spillovers, where FDI might suppress local industries and adversely affect domestic firms. This perspective is balanced by the findings of Khan et al. [25], who argue that the net effect of FDI on economic growth depends significantly on the sectors receiving investment and the degree of competition within the domestic market. Further, Boswijk [26] explored the conditions under which FDI leads to positive spillovers, such as increased productivity and innovation in domestic industries, suggesting that the interplay between foreign investors and the domestic economy significantly shapes the outcomes of FDI.

The dynamic nature of FDI's impact on economic growth underscores the importance of nuanced policy frameworks that can navigate the challenges and opportunities presented by FDI. Banerjee et al. [27] argue for the importance of developing human capital and improving infrastructure to enhance the positive impacts of FDI. Additionally, the significance of sector-specific policies that encourage technology transfer and integration into global value chains is highlighted [28]. This expanded discussion reflects the broad consensus on FDI's potential to stimulate economic growth while also acknowledging the complexity of factors that influence the magnitude and direction of its impact.

The study focuses at how foreign debt and foreign direct investment affect Somalia's economic expansion. We used a time series of data from World Bank, SESRIC, and World Data spanning from 1990 to 2021. The analysis included three variables: GDP (gross domestic product) at constant 2015 prices; ED (external debt) at total (current prices in thousands); and FDI (foreign direct investment) at net inflows (current US dollars).

A linear representation of the relationship between external debt, foreign direct investment, and economic growth in Somalia is shown in Eq. (1):

InGDPt=F(InEDt,InFDIt,) (1)

InGDPt, InEDt, and InFDIt represent a natural logarithmic transformation of, GDP, ED, and FDI for a more stable data variance.

The empirical specifications for the model can be quantified as follows:

InGDPt=β0+β1InEDt+β2InFDIt+εt (2)

where, InGDPt is the dependent variable, while InEDt and InFDIt are the explanatory variables in year t, εt is the error term, and β0, β1, and β2 are the elasticities to be estimated.

Examining the variables' sequence of integration is the first step in determining cointegration. We use the Philips-Perron (PP) and enhanced Dickey-Fuller (ADF) stationarity tests to determine if the series shows cointegration. The lag order is established once the series reaches stationarity, and searches are made to find any possible cointegrating correlations between the variables. To investigate the long-term relationships between model variables, a number of cointegration tests are available. Applicable only to variables with the same order of integration, the commonly used Engle and Granger test is well-documented in the literature. Other methods have since been developed, such as the more adaptable Johansen's Error Correction Cointegration technique than the Engle and Granger method; the tests Johansen and Juselius; Phillips and Ouliaris; the Structural Error Correction Model by Boswijk [29]; and the test proposed by Banerjee et al. [30], which uses the t-test for the null hypothesis. These conventional methods have been criticized for their alleged unreliability in small sample sizes, inconsistent results with different-order integrated variables, and propensity to produce skewed and misleading results in opposition to rejection of the null hypothesis (no-cointegration). To improve test power, a more reliable cointegration method called autoregressive distributed lag (ARDL) bounds testing is used. To boost the test power, a more reliable cointegration method called autoregressive distributed lag (ARDL) bounds testing is applied.

Following the empirical works [31-34] the ARDL cointegration equation can be written as:

ΔGDPt=+α0+β1InEDt−1+β2InFDIt−1+q∑i=0Δα1InGDPt−k+p∑i=0Δα2InEDt−k+p∑i=0Δα3InFDIt−k+εt−k (3)

where, the constant term is represented by α0, the short-term variable coefficients are indicated by α1–α3, and the long-run parameter elasticities are indicated by β1–β2. The variables Δ indicates the initial difference sign depicting the short-run variables, εt represents the error term, and q indicates the ideal lags for the explained variables, p indicates the optimal lags for the explanatory variables.

Bound testing is the first step in the ARDL cointegration process. After that, Ordinary Least Squares (OLS) regression is applied. While the alternative hypothesis (H1): β1≠β2≠0 proposes the presence of long-run cointegration among variables, the null hypothesis (H0): β1=β2=0 asserts that the variables lack cointegration in the long run. Critical values and Wald-F statistics are used to evaluate the null hypothesis. When the Wald-F statistics exceed the upper bound critical values, the null hypothesis is rejected, indicating that the variables are long-term related and vice versa.

4.1 Descriptive analysis and correlation matrix

Table 1 presents descriptive statistics for a study analyzing the effects of external debt (ED) and foreign direct investment (FDI) on economic growth in Somalia, with GDP representing economic growth. A key observation is the differences in scale and distribution between the variables. The mean of lnGDP (21.97142) is significantly higher than that of lnFDI (2.581487) and lnED (14.88109), indicating a much larger average value for GDP in the logarithmic scale used. The standard deviation (Std. Dev.) values also reveal noteworthy contrasts: lnGDP and lnED exhibit relatively low variability (0.613856 and 0.234631, respectively), suggesting that these measures are more consistently distributed around their means. In contrast, lnFDI shows a high standard deviation (3.284436), indicating a wider spread of values and, thus, more variability in foreign direct investment.

Further analysis of skewness and the Jarque-Bera test provides insights into the distribution characteristics of these variables. The skewness values for lnGDP (0.340704) and lnFDI (-0.390866) are closer to zero, suggesting a more symmetric distribution around the mean, although lnFDI’s negative skew indicates a tail with smaller values. lnED, however, has a high positive skewness (1.701911), indicating a long tail towards higher values. The Jarque-Bera test, which assesses the normality of distribution, shows significantly different results for these variables. While lnGDP (2.851558) and lnFDI (3.308796) have relatively low Jarque-Bera values with high p-values (0.240321 and 0.191207, respectively), suggesting a distribution closer to normal, lnED has a high Jarque-Bera value (21.42793) with a very low p-value (0.000022). This indicates that the distribution of lnED significantly deviates from normal, also reflected in its high skewness. This divergence in distribution characteristics across the variables can affect the analysis and interpretation of the study’s findings.

Table 1. Descriptive statistics of variables

|

Stats |

lnGDP |

lnFDI |

lnED |

|

Mean |

21.97142 |

2.581487 |

14.88109 |

|

Median |

21.89335 |

4.465908 |

14.83168 |

|

Maximum |

22.95530 |

6.455199 |

15.54208 |

|

Minimum |

21.14602 |

-3.218876 |

14.62404 |

|

Std. Dev. |

0.613856 |

3.284436 |

0.234631 |

|

Skewness |

0.340704 |

-0.390866 |

1.701911 |

|

Jarque-Bera |

2.851558 |

3.308796 |

21.42793 |

|

P-value |

0.240321 |

0.191207 |

0.000022 |

Table 2. Correlation matrix

|

lnGDP |

lnFDI |

lnED |

|

|

lnGDP |

1 |

|

|

|

lnFDI |

0.8732 |

1 |

|

|

lnED |

0.7957 |

0.6575 |

1 |

Table 2 is a correlation matrix showing relationships between lnGDP, lnFDI, and lnED. Correlation coefficients range from -1 to 1, where 1 indicates a perfect positive correlation, and -1 is a perfect negative correlation. In this matrix, lnGDP and lnFDI have a high positive correlation (0.8732), implying that increases in foreign direct investment are generally associated with increases in economic growth. Similarly, lnGDP and lnED have a strong positive correlation (0.7957), suggesting that higher external debt is often linked with higher economic growth. The correlation between lnFDI and lnED is moderate (0.6575), indicating a positive but less strong relationship. This matrix suggests significant positive relationships among Somalia’s economic growth, foreign direct investment, and external debt.

4.2 Unit root test

Table 3 displays results from unit root tests (ADF and PP tests), which are statistical methods used to determine whether a time series is stationary. The variables lnGDP, lnFDI, and lnED, the tests are conducted at level and at first difference. At level, none of the variables are statistically significant, with their T-statistics being too small to reject the null hypothesis of a unit root (indicating non-stationarity). However, once differenced, all three variables show strong statistical significance, as indicated by the three asterisks (***), which denote significance at the 1% level. This implies that while the original data series are non-stationary, their first differences are stationary. In other words, the variables lnGDP, lnFDI, and lnED are integrated of order one, I(1), meaning they become stationary after differencing once. The T-statistics for the differenced series are well below the critical values for 1% significance, strongly rejecting the null hypothesis of a unit root at this level of differencing.

Table 3. Unit root

|

Variables |

T-Statistics at Level |

|

|

ADF |

PP |

|

|

lnGDP |

0.4809 |

0.7128 |

|

lnFDI |

-0.9506 |

-0.8063 |

|

lnED |

-1.3730 |

-1.2337 |

|

|

At First Difference |

|

|

lnGDP |

-3.9992*** |

-4.0171*** |

|

lnFDI |

-6.7139*** |

-6.9955*** |

|

lnED |

-4.9706*** |

-7.7755*** |

4.3 Cointegration test

Table 4 shows the results of a bounds-testing approach to cointegration, determining whether a long-term equilibrium relationship exists between variables in an autoregressive distributed lag (ARDL) model. The F-statistic value obtained from the test is 6.961454. This statistic is compared against a set of critical values for different levels of significance (1%, 5%, and 10%) and for different model specifications based on the integration order of the variables (I(0) and I(1), representing no integration and first-order integration, respectively). If the F-statistic exceeds the upper bound of the critical values, the null hypothesis of no cointegration is rejected, indicating a long-term relationship among the variables.

Table 4. F bounds test

|

F-Statistic |

Level of Significance |

Bounds Test Critical Values |

|

|

I (0) |

I (1) |

||

|

6.961454 |

1% |

4.13 |

5 |

|

5% |

3.1 |

3.78 |

|

|

10% |

2.63 |

3.35 |

|

In this case, the F-statistic is higher than both the upper I(1) bound at the 1% significance level (5) and the upper I(0) bound at the same level (4.13). Since the F-statistic is above the upper bounds for all three levels of significance, it strongly suggests the presence of cointegration among the variables in the model. This implies that the variables move together in the long run, and any short-term deviations will eventually adjust toward a long-term equilibrium.

4.4 ARDL long-run and short-run results with diagnostics

Table 5 outlines the long-run results from an Autoregressive Distributed Lag (ARDL) model, detailing the impact of foreign direct investment (lnFDI) and external debt (lnED) on economic growth, with 'C' representing the intercept of the model.

Table 5. Long-run results and diagnostics

|

Variables |

Coefficient |

|

C |

-5.3999 |

|

(-0.4947) |

|

|

lnFDI |

0.0788 |

|

(1.504239) ** |

|

|

lnED |

1.7939 |

|

(2.4631) ** |

|

|

Reset test |

1.3229 [0.2636] |

|

Serial correlation |

0.3811 [0.6340] |

|

Heteroskedasticity |

0.9690 [0.8088] |

|

Normality |

0.7342 [0.6927] |

In this model, the coefficient for 'C', which is -5.3999, represents the baseline level of economic growth when the independent variables, lnFDI and lnED, are zero. However, the T-statistic of -0.4947 indicates that this intercept is not statistically significant, suggesting that the baseline economic growth is not different from zero in a meaningful way.

The lnFDI coefficient is 0.0788, meaning that a 1% increase in foreign direct investment is associated with a 0.0788% increase in economic growth, holding other factors constant. This relationship is statistically significant at the 5% level, as denoted by the two asterisks (**), indicating that there is less than a 5% probability that this result is due to chance. Similarly, the coefficient for lnED is 1.7939, suggesting that a 1% increase in external debt is associated with a 1.7939% increase in economic growth, also statistically significant at the 5% level.

The diagnostic tests—RESET test, serial correlation, heteroskedasticity, and normality—are used to verify the model's validity. The p-values in parentheses indicate the probability of the test statistic under the null hypothesis. Since all these p-values are above common significance levels (0.05, 0.01), they suggest that the model does not suffer from specification error, serial correlation, or heteroskedasticity issues and that the residuals are normally distributed. This implies that the model is well-specified and the error terms do not violate the ordinary least squares regression assumptions, lending confidence to the interpretation of the coefficients.

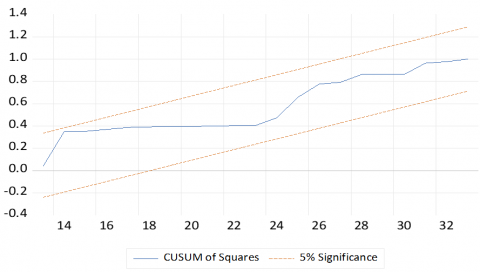

Moreover, Figures 1 and 2 illustrate the stability of the coefficients in a time series regression model. The first, displaying the CUSUM test, suggests the model's parameters are consistent over time as the plot stays within the 5% significance bounds. The second, showing the CUSUM of Squares, indicates stable variance in the residuals, with no structural breaks detected, as the plot also remains within the 5% significance limits. Together, they affirm the model's reliability throughout the observed period.

Figure 1. CUSUM test

Figure 2. CUSUM of squares test

The short-run ARDL results in Table 6 reveal that the immediate impact of changes in GDP (ΔlnGDP) is significantly positive, indicating that current economic activities strongly influence economic growth. The lagged effect of GDP (ΔlnGDPt-2) is not significant, suggesting that past values of GDP changes have no immediate influence. Changes in foreign direct investment (ΔlnFDI) initially have a detrimental effect on growth, but the positive coefficient of its lag (ΔlnFDIt-1) signifies a positive adjustment a period later. The initial impact (ΔlnED) is negative for external debt, while its lag (ΔlnEDt-1) shows a significant positive rebound effect. The Error Correction Term (ECTt-1) has a notably significant negative coefficient, confirming that deviations from long-term growth equilibrium are corrected each period by approximately 23.37%.

Table 6. Short-run results and diagnostics

|

Variables |

Coefficient |

|

ΔlnGDP |

14.1054 |

|

(4.7376)*** |

|

|

ΔInGDPt-2 |

0.2578 |

|

(1.3039) |

|

|

ΔInFDI |

-0.0395 |

|

(-3.5264) *** |

|

|

ΔInFDIt-1 |

0.0404 |

|

(3.9596) *** |

|

|

ΔInED |

-0.2641 |

|

(-3.0576) *** |

|

|

ΔInED t-1 |

0.5338 |

|

(3.8721) *** |

|

|

ECTt-1 |

-0.233722 |

|

(0.0021) *** |

The study aimed to explore the impact of external debt (ED) and foreign direct investment (FDI) on economic growth in Somalia, employing a comprehensive analytical framework from 1990 to 2021. Utilizing World Bank, SESRIC, and World Data, the research applied a linear model to examine the relationship between GDP, ED, and FDI. The methodology incorporated the use of Augmented Dickey-Fuller (ADF) and Philips-Perron (PP) tests for unit root analysis, followed by the autoregressive distributed lag (ARDL) bounds testing approach for cointegration, to assess both short-term and long-term dynamics among the variables.

The study's unit root tests revealed that the variables GDP, ED, and FDI were non-stationary at levels but achieved stationarity at first differences, indicating their integration of order one, I(1), which suggested a potential for a long-run relationship among them. The subsequent F-bounds testing underscored this potential by uncovering a significant long-term relationship, as evidenced by an F-statistic (6.961454) that surpassed the upper bounds of critical values at the 1% significance level, indicating a robust cointegration.

The ARDL long-run results further quantified these relationships, showing that external debt and foreign direct investment positively contribute to economic growth. Specifically, a 1% increase in FDI is associated with a 0.0788% increase in economic growth, while a 1% increase in external debt corresponds to a 1.7939% increase in economic growth. These findings underscore the significant role of external financial inflows in supporting Somalia's economic development.

The Error Correction Model (ECM) and short-run dynamics indicated a correction mechanism where deviations from long-term growth equilibrium are adjusted by approximately 23.37% yearly. This suggests that while short-term fluctuations exist, the economy tends to revert to its long-term growth path, demonstrating Somalia's economy's resilience and adaptive capacity in response to external financial inflows.

Diagnostics tests confirmed the model's robustness, showing no evidence of specification errors, serial correlation, heteroskedasticity issues, or deviations from normality in the residuals. The stability of the coefficients was affirmed by the CUSUM and CUSUM of Squares tests, indicating that the model's parameters remained consistent over the observed period.

This study provides valuable insights into the complex relationship between external debt, foreign direct investment, and economic growth in Somalia. The positive long-term impacts of ED and FDI on economic growth highlight the importance of these financial inflows in supporting the country's development trajectory. However, the findings also underscore the necessity for prudent management of external debt to avoid potential negative consequences associated with high debt levels.

The evidence of a significant adjustment mechanism through the ECM suggests that while Somalia's economy may experience short-term fluctuations due to external debt and FDI changes, it can adjust and maintain its growth trajectory over the long term. This resilience is crucial for economic planning and policy formulation.

Policymakers in Somalia and similar contexts can leverage these findings to formulate strategies that maximize the benefits of FDI and manage external debt in a way that supports sustainable economic growth. This could include measures to improve the investment climate, enhance the economy's absorptive capacity, and ensure that borrowed funds are directed towards productive uses that stimulate growth and development.

This work is supported by SIMAD University.

[1] Appiah, M., Gyamfi, B.A., Adebayo, T.S., Bekun, F.V. (2023). Do financial development, foreign direct investment, and economic growth enhance industrial development? Fresh evidence from Sub-Sahara African countries. Portuguese Economic Journal, 22(2): 203-227. https://doi.org/10.1007/s10258-022-00207-0

[2] Olorogun, L.A., Salami, M.A., Bekun, F.V. (2022). Revisiting the Nexus between FDI, financial development and economic growth: Empirical evidence from Nigeria. Journal of Public Affairs, 22(3): e2561. https://doi.org/10.1002/pa.2561

[3] Gomez-Puig, M., Sosvilla-Rivero, S., Martinez-Zarzoso, I. (2022). On the heterogeneous link between public debt and economic growth. Journal of International Financial Markets, Institutions and Money, 77: 101528. https://doi.org/10.1016/J.INTFIN.2022.101528

[4] Joshua, U., Babatunde, D., Sarkodie, S.A. (2021). Sustaining economic growth in Sub-Saharan Africa: Do FDI inflows and external debt count? Journal of Risk and Financial Management, 14(4): 146. https://doi.org/10.3390/JRFM14040146

[5] Al Barrak, T., Chebbi, K., Aljughaiman, A.A., Albarrak, M. (2023). Exploring the interplay between sustainability and debt costs in an emerging market: Does financial distress matter? Sustainability, 15(12): 9273. https://doi.org/10.3390/SU15129273

[6] Elkhishin, S., Mohieldin, M. (2021). External debt vulnerability in emerging markets and developing economies during the COVID-19 shock. Review of Economics and Political Science, 6(1): 24-47. https://doi.org/10.1108/REPS-10-2020-0155

[7] Ahmad, M., Peng, T., Awan, A., Ahmed, Z. (2023). Policy framework considering resource curse, renewable energy transition, and institutional issues: Fostering sustainable development and sustainable natural resource consumption practices. Resources Policy, 86: 104173. https://doi.org/10.1016/J.RESOURPOL.2023.104173

[8] Mohsin, M., Ullah, H., Iqbal, N., Iqbal, W., Taghizadeh-Hesary, F. (2021). How external debt led to economic growth in South Asia: A policy perspective analysis from quantile regression. Economic Analysis and Policy, 72: 423-437. https://doi.org/10.1016/j.eap.2021.09.012

[9] Warsame, Z.A., Ali Mohamed, I.S. (2024). On the determinants of unemployment in Somalia: What is the role of external debt? International Journal of Sustainable Development & Planning, 19(1): 161-165. https://doi.org/10.18280/ijsdp.190114

[10] Warsmame, Z.A., Abdi, A.O. (2024). Impact of external debt and energy consumption on environmental quality in Somalia. International Journal of Energy Economics and Policy, 14(5): 520-526. https://doi.org/10.32479/ijeep.15460

[11] Warsame, Z.A. (2023). The significance of FDI inflow and renewable energy consumption in mitigating environmental degradation in Somalia. International Journal of Energy Economics and Policy, 13(1): 443-453. https://doi.org/10.32479/ijeep.13943

[12] Hassan, A., Meyer, D. (2021). Exploring the channels of transmission between external debt and economic growth: Evidence from Sub-Saharan African countries. Economies, 9(2): 50. https://doi.org/10.3390/ECONOMIES9020050

[13] Casares, E.R. (2015). A relationship between external public debt and economic growth. Estudios Económicos (México, DF), 30(2): 219-243.

[14] Reinhart, C.M., Rogoff, K.S. (2010). Growth in a time of debt. American Economic Review, 100(2): 573-578. https://doi.org/10.1257/aer.100.2.573

[15] Cecchetti, S.G., Mohanty, M.S., Zampolli, F. (2011). The real effects of debt. In Economic Symposium Conference Proceedings, pp. 145-96.

[16] Heimberger, P. (2023). Do higher public debt levels reduce economic growth? Journal of Economic Surveys, 37(4): 1061-1089. https://doi.org/10.1111/JOES.12536

[17] Ndoricimpa, A. (2020). Threshold effects of public debt on economic growth in Africa: A new evidence. Journal of Economics and Development, 22(2): 187-207. https://doi.org/10.1108/JED-01-2020-0001

[18] Edo, S., Osadolor, N.E., Dading, I.F. (2020). Growing external debt and declining export: The concurrent impediments in economic growth of Sub-Saharan African countries. International Economics, 161: 173-187. https://doi.org/10.1016/J.INTECO.2019.11.013

[19] Turan, T., Yanıkkaya, H. (2021). External debt, growth and investment for developing countries: Some evidence for the debt overhang hypothesis. Portuguese Economic Journal, 20(3): 319-341. https://doi.org/10.1007/S10258-020-00183-3/TABLES/9

[20] Manasseh, C.O., Abada, F.C., Okiche, E.L., Okanya, O., Nwakoby, I.C., Offu, P., Ogbuagu, A.R., Okafor, C.O., Obidike, P.C., Nwonye, N.G. (2022). External debt and economic growth in Sub-Saharan Africa: Does governance matter? PLoS ONE, 17(3): e0264082. https://doi.org/10.1371/JOURNAL.PONE.0264082

[21] Magazzino, C., Mele, M. (2022). Can a change in FDI accelerate GDP growth? Time-series and ANNs evidence on Malta. The Journal of Economic Asymmetries, 25: e00243. https://doi.org/10.1016/J.JECA.2022.E00243

[22] Wu, W., Yuan, L., Wang, X., Cao, X., Zhou, S. (2020). Does FDI drive economic growth? Evidence from city data in China. Emerging Markets Finance and Trade, 56(11): 2594-2607. https://doi.org/10.1080/1540496X.2019.1644621

[23] Miao, M., Borojo, D.G., Yushi, J., Desalegn, T.A. (2021). The impacts of Chinese FDI on domestic investment and economic growth for Africa. Cogent Business & Management, 8(1): 1886472. https://doi.org/10.1080/23311975.2021.1886472

[24] Sugiharti, L., Yasin, M.Z., Purwono, R., Esquivias, M.A., Pane, D. (2022). The FDI spillover effect on the efficiency and productivity of manufacturing firms: Its implication on open innovation. Journal of Open Innovation: Technology, Market, and Complexity, 8(2): 99. https://doi.org/10.3390/JOITMC8020099

[25] Khan, M.T.I., Anwar, S., Sarkodie, S.A., Yaseen, M.R., Nadeem, A.M. (2023). Do natural disasters affect economic growth? The role of human capital, foreign direct investment, and infrastructure dynamics. Heliyon, 9(1): e12911. https://doi.org/10.1016/j.heliyon.2023.e12911

[26] Boswijk, H.P. (1994). Testing for an unstable root in conditional and structural error correction models. Journal of Econometrics, 63(1): 37-60. https://doi.org/10.1016/0304-4076(93)01560-9

[27] Banerjee, A., Dolado, J., Mestre, R. (1998). Error-correction mechanism tests for cointegration in a single-equation framework. Journal of Time Series Analysis, 19(3): 267-283. https://doi.org/10.1111/1467-9892.00091

[28] Sarkodie, S.A., Adams, S. (2018). Renewable energy, nuclear energy, and environmental pollution: Accounting for political institutional quality in South Africa. Science of the Total Environment, 643: 1590-1601. https://www.sciencedirect.com/science/article/pii/S0048969718323969.

[29] Boswijk, H.P. (1994). Testing for an unstable root in conditional and structural error correction models. Journal of Econometrics, 63(1): 37-60. https://doi.org/10.1016/0304-4076(93)01560-9

[30] Banerjee, A., Dolado, J.J., Mestre, R. (1998). Error-correction mechanism tests for cointegration in a single-equation framework. Journal of Time Series Analysis, 19(3): 267-283. https://doi.org/10.1111/1467-9892.00091

[31] Shahbaz, M., Nasreen, S., Abbas, F., Anis, O. (2015). Does foreign direct investment impede environmental quality in high-, middle-, and low-income countries? Energy Economics, 51: 275-287. https://doi.org/10.1016/j.eneco.2015.06.014

[32] Warsame, Z.A., Ali, M.M., Mohamed, L.B., Mohamed, F.H. (2023). The causal relation between energy consumption, carbon dioxide emissions, and macroeconomic variables in Somalia. International Journal of Energy Economics and Policy, 13(3): 102-110. https://doi.org/10.32479/ijeep.14262

[33] Nor, B.A., Yusof, Y., Warsame, Z.A. (2024). Exploring the potential for renewable energy consumption in reducing environmental degradation in Somalia. International Journal of Energy Economics and Policy, 14(5): 643-650. https://doi.org/10.32479/ijeep.15508

[34] Warsame, Z.A., Hassan, A.M., Hassan, A.Y. (2023). Determinants of inflation in Somalia: An ARDL approach. International Journal of Sustainable Development and Planning, 18(9): 2811-2817. https://doi.org/10.18280/ijsdp.180919