Nicken Destriana*![]() | Rudi Zulfikar

| Rudi Zulfikar![]() | Windu Mulyasari

| Windu Mulyasari![]() | Iis Ismawati

| Iis Ismawati![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study aims to provide an analysis of research trends on financial sustainability for sustainable development, with a particular focus on identifying global trends in the relevant literature. The study used bibliometric methodology to map and analyze the scientific literature on financial sustainability. Extensive bibliographic data was extracted from the Scopus database and 4,836 documents from 2014-2024 were identified. The data was analyzed using the Scopus publication analyzer feature and publication metadata was further mapped using VOSviewer and thesaurus to identify the patterns. The results of the study conclude that the most significant contributors in the field of financial sustainability were Buallay, A. from the authorship with 13 publications, Universiti Teknologi MARA from the institution criteria with 42 publications, and United State by country (560 publications). Moreover, the results revealed a growing trend for financial sustainability research showing an increased interest in the topic and positive growth over the past decade. The analysis identified several key research themes, including sustainability, sustainable development, financial performance, corporate social responsibility, and sustainability reporting. The findings highlight important areas for future research, such as further investigating topics that have the potential to be linked to financial sustainability such as transparency, cost, risk management.

financial sustainability, bibliometric, Scopus, VOSviewer

The issue of financial sustainability has become a major concern in various disciplines, especially in the wake of increasing global economic uncertainty, environmental change and social tensions. The concept is not only relevant to companies, but also non-profit organizations, governments and individuals, given the importance of long-term financial stability to support sustainable growth. Financial sustainability encompasses an entity's ability to maintain financial balance without relying excessively on external funding, while continuing to meet future needs and obligations. Financial sustainability is the maximum growth rate of operating income that can be achieved provided that the company maintains operating efficiency targets and financial policies without issuing new shares [1]. Financial sustainability is not merely about staying afloat; it's about an organization's capacity to maintain its financial footing while adapting and thriving over the long haul. This involves a strategic approach to managing financial resources that balances current needs with the imperative for future viability. In a world grappling with dwindling resources, the concept of sustainability takes center stage. Businesses and individuals alike must embrace sustainable practices to ensure their own longevity. Organizations aiming for enduring financial success must embed economic, social, and environmental sustainability into their core strategies [2, 3].

Achieving true financial sustainability requires a paradigm shift. It necessitates a business strategy that transcends organizational self-interest and prioritizes the protection, enhancement, and development of both human capital and natural ecosystems. This holistic approach safeguards the well-being of present and future generations. The term financial sustainability first emerged and gained attention in various contexts, including business, economics and non-profit organizations, in the late 20th century. The concept evolved with the increasing focus on sustainability in the global economy and financial sector. In the literature, financial sustainability is often associated with an entity's ability to manage financial resources sustainably, without over-reliance on external funding, while ensuring long-term operational continuity.

More specifically, the term financial sustainability became visible in the context of academic research and literature since the 1990s, especially in relation to non-profit organizations and the public sector. For example, influential articles [4] helped build an understanding of how non-profit entities maintain their financial viability. Meanwhile, articles in the business context have also begun to focus on the importance of financial sustainability in maintaining corporate stability and growth, especially after the various global financial crises. The study [5] discusses the role of financial sustainability in the context of social entrepreneurship and how social entities can continue to operate in a financially sustainable manner.

Furthermore, financial sustainability research spans various disciplines, focusing on the ability of organizations to cover costs, repay debts, and maintain assets [6]. Key areas include financial literacy, inclusion, behavior, and decision-making [7]. Sustainable finance research has evolved to encompass socially responsible investment, climate change, and green finance [8]. Studies emphasize the importance of contingency planning and innovative management for long-term financial sustainability [9]. The relationship between monetary factors and sustainability remains understudied in top academic journals [10]. Project complexity, trust in leadership, and employee readiness impact financial sustainability in project management [11]. Microfinance institutions face challenges in achieving financial sustainability, with various models proposed to measure it [12]. Research on financial behavior related to education, savings, and consumption has grown exponentially, contributing to sustainable development goals [13].

A recent literature review of sustainability-related research shows an increasing interest in sustainable finance and financial services. Studies show exponential growth in sustainability publications over the past decade, with key focus areas including environmental sustainability, climate change, and sustainable development [14]. The UK, China, and the US are emerging as major research centers for sustainable finance [15]. Financial reporting via the internet and FinTech is increasingly linked to sustainability practices [16, 17]. However, sustainability transformation in financial services has been slow, with limited research [18]. Auditing plays an important role in ensuring compliance with sustainability accounting standards, although it is still a specialized field [19]. These studies highlight the need for further research and practical implementation of sustainability principles in finance. Table 1 describes the research results on literature review of each article.

Table 1. Previous research on literature review of financial sustainability

|

No. |

Title |

Author (year) |

Journal |

Findings |

|

1 |

Scientific Literature Analysis on Sustainability with the Implication of Open Innovation |

Cano, J.A., Londoño-Pineda, A. (2020) [14] |

Journal of Open Innovation: Technology, Market and Complexity |

(1) Sustainability research tackles the interconnected environmental, economic, and social aspects of meeting present and future needs. This holistic approach has fueled its rapid growth, particularly in the 21st century, with a marked surge in the past decade. (2) The most impactful sustainability researchers often focus on areas like engineering, energy, environmental science, business, management, and accounting. This reflects the complex and multifaceted nature of sustainability challenges. (3) Journals like "Sustainability Switzerland" and the "Journal of Cleaner Production" consistently rank among the leading publications in sustainability research. Their commitment to publishing work that bridges traditional disciplinary boundaries has solidified their prominent position in the field. |

|

2 |

Bibliometric Review on Sustainable Finance |

Kashi, A., Shah, M.E. (2023) [15] |

Sustainability |

(1) The leading research hubs for sustainable finance are primarily located in the UK, China, the USA, Switzerland, and Japan. (2) Transdisciplinary journals have stronger co-citation links than mainstream finance and economics journals, indicating the prevalence of interdisciplinary research in sustainable finance. |

|

3 |

Public Debt Sustainability: A Bibliometric Co-citation Visualization Analysis |

Kaur, A., Prof Kumar, V., Sindhwani, R., Singh, P.L., Behl, A. (2022) [20] |

International Journal of Emerging Markets |

(1) Research on public debt sustainability can be grouped into three main themes: fiscal sustainability and the policies that support it, empirical methods for assessing sustainability, and the relationship between debt and economic growth. (2) The majority of research on public debt sustainability relies on analytical and empirical approaches, with fewer studies focusing on descriptive analysis. (3) The challenges associated with public debt sustainability have evolved over time, reflecting the dynamic nature of economies and their diverse structures. |

|

4 |

Auditing and Sustainability Accounting: A Global Examination Using the Scopus Database |

Thottoli, M.M., Islam, M.A., Sobhani, F.A., Rahman, S., Hassan, M.S. (2022) [19] |

Sustainability |

(1) While compliance auditing is an emerging field, it still encounters obstacles and hasn't garnered sufficient attention within mainstream accounting and auditing research. (2) The specialized nature of compliance auditing is evident in the fact that a small number of authors account for a large portion of the frequently cited articles. (3) There has been a marked increase in the volume of research articles on compliance auditing and sustainability accounting, particularly from 2009 to 2021. |

|

5 |

Is There Any Association Between FinTech and Sustainability? Evidence from Bibliometric Review and Content Analysis |

Ellili, N. (2022) [16] |

Journal of Financial Services Marketing |

(1) Three main themes have emerged in research exploring the connection between FinTech and sustainability: how well sustainability efforts are performing, the role of blockchain technology, and the impact of digital transformation. (2) There's been a notable increase in research examining the link between FinTech and sustainability, particularly in 2021. This highlights the growing recognition of how financial technologies and innovations are shaping sustainable business practices. (3) This research has important implications for both FinTech and sustainability, emphasizing how FinTech can contribute to developing and implementing effective sustainability strategies, practices, and research methods. |

|

6 |

Sustainable Financial Services: Reflection and Future Perspectives |

Tuyon, J., Onyia, O.P., Ahmi, A., Huang, C.H. (2022) [18] |

Journal of Financial Services Marketing |

(1) There has been a recent growth in academic publications on sustainable financial services, but relatively low implementation of sustainability practices in the financial services sector globally. (2) The study focused on three key areas related to sustainable financial services: sustainable financial products, sustainable service delivery, and sustainable marketing strategies. (3) The study aimed to provide insights to encourage more action and development of sustainable practices in the financial services industry by various stakeholders. |

Based on the above findings, most literature review on financial sustainability tends to focus on a limited time span. Therefore, this study will extend the time span of analysis to 2024 to understand the evolution of the concept of financial sustainability in the context of broader global economic changes, as well as how this trend is affected by the financial crisis since it uses the span during the COVID-19 pandemic. Research related to financial sustainability is often triggered by the global financial crisis. However, there is still a gap in bibliometric analysis that examines how global crises, such as the COVID-19 pandemic or climate change, affect research trends and thematic focus in the financial sustainability literature. This research can help identify topics that have emerged due to the global crisis and how this has affected the understanding of financial sustainability.

Over the past decade, there has been a significant increase in research developments related to financial sustainability, reflecting the urgency and complexity of this issue. One of the main platforms for reviewing research trends is academic databases such as Scopus, which includes scientific publications from various fields and regions. Bibliometric analysis is an effective method to evaluate these research trends, as it allows researchers to identify publication patterns, collaboration between authors, as well as the development of major themes within a given topic. Furthermore, in an effort to measure and see the productivity and development of scientific publications, several aspects are used, namely co-occurrence (keywords) from year to year quantitatively based on data obtained and processed using VOSviewer software. VOSviewer or "visualization of similarity" is a software that aims to build and visualize bibliometric networks.

This study aims to conduct a bibliometric analysis of scientific publications focusing on financial sustainability during the period 2014-2024 using data from the Scopus database. Through this analysis, global trends in related literature will be identified, including the geographical distribution of research, collaboration between institutions, and the most discussed topics. Therefore, this study conducted a bibliometric analysis to quantitatively determine the publications that contain financial sustainability. In addition, this study aims to find out: (a) year of publications on financial sustainability; (b) top 10 journals of scientific publications on financial sustainability; (c) productive authors of financial sustainability based on citation; (d) top 10 scientific publications on financial sustainability by universities; (e) top 10 scientific publications by country; (f) scientific publications on financial sustainability by subject; and (g) the frequency of occurrence of the most keywords in scientific publications on financial sustainability. By understanding these patterns, it is expected to provide insight into the development and research gaps in the field of financial sustainability that still need to be explored further in the future. In addition, the results of this study will show the main areas and current developments/trends of financial sustainability research so that thematic and potential future research directions in the field of financial sustainability can be seen.

Bibliometric analysis is a statistical method used to analyze bibliographic data such as authors, articles, citations, institutions, and countries. This quantitative approach helps evaluate research trends by examining publication and citation patterns. It has been widely adopted across various fields to investigate published information and assess studies based on citations and publications. By utilizing bibliometric analysis, researchers can identify emerging trends, evaluate journal performance, explore specific research topics, and understand research collaborations and mechanisms. Tools like VOSviewer further enhance this analysis by visually representing citation networks and relationships, including co-citations and co-occurrences, as demonstrated by the study [21]. The software can depict the strength of these links, such as the total number, as highlighted by the study [22].

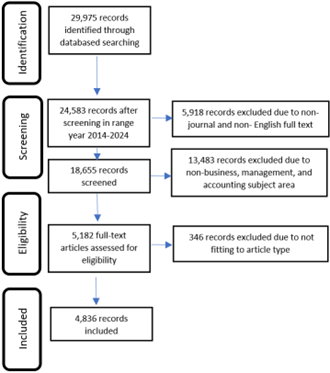

The population used is scientific publications on financial sustainability that have been published scientifically and indexed by Scopus. The reason for selecting the Scopus database was determined purposively and saw consideration of the quality and reputation that has been recognized internationally. The sample used in this study is scientific publications on financial sustainability that have been indexed by Scopus and published between 2014-2024, found 4,836 documents. This research was conducted on September 25, 2024. The sample selection process is presented in Figure 1.

Bibliometric analysis begins by searching for publications in the Scopus database www.scopus.com. using keywords (financial AND sustainability). Then the search results taken are in the title, abstract, and keywords with advanced queries in the Scopus database search as follows:

TITLE-ABS-KEY (financial AND sustainability) AND (LIMIT-TO (SRCTYPE, "j")) AND (LIMIT-TO (SUBJAREA, "BUSI")) AND (LIMIT-TO (DOCTYPE, "ar")) AND (LIMIT-TO (PUBYEAR, 2014) OR LIMIT-TO (PUBYEAR, 2015) OR LIMIT-TO (PUBYEAR, 2016) OR LIMIT-TO (PUBYEAR, 2017) OR LIMIT-TO (PUBYEAR, 2018) OR LIMIT-TO (PUBYEAR, 2019) OR LIMIT-TO (PUBYEAR, 2020) OR LIMIT-TO (PUBYEAR, 2021) OR LIMIT-TO (PUBYEAR, 2022) OR LIMIT-TO (PUBYEAR, 2023) OR LIMIT-TO (PUBYEAR, 2024)) AND (LIMIT-TO (LANGUAGE, "English")).

Figure 1. Sample selection process

The publications found were analyzed using the Scopus publication analyzer feature and the publication metadata was exported in CSV form for further mapping using VOSviewer software and a thesaurus was created for each keyword. After obtaining the search results, researchers began to explore the data in the Scopus database to see the growth of scientific publications in the financial sustainability literature, core journals, researcher productivity and collaboration, publication growth by institution or affiliation, and the number of publications by country. Furthermore, researchers made efforts to visualize the development of research on financial sustainability using VOSviewer software by creating keyword maps by exporting search results from the Scopus database into CSV format, after which the CSV data was inputted into the VOSviewer software [23].

The data analysis technique of this research is descriptive quantitative and descriptive qualitative. Through Scopus publication analyzer feature, researchers get output in the form of statistical data or statistical processing results in the form of graphs with image format (JPEG) Meanwhile, another output from Scopus is secondary data in CSV format. Furthermore, researchers conducted data processing with MS. Excel and VOSviewer devices. In the last stage, researchers analyzed the Scopus and VOSviewer outputs descriptively and qualitatively.

3.1 Year of publication

The number of publications about financial sustainability indexed in the Scopus database from 2014-2024 was 4,836 documents. Figure 2 presents the distribution pattern of research results on financial sustainability. The growth of research publications on financial sustainability indexed on Scopus where the peak occurred in 2024 with 937 publications (19.38%). The number of research publications on repositories in the second rank occurred in 2023 with 815 publications (16.85%), followed by successively in 2022 with 638 publications (13.19%), 2021 with 493 publications (10.19%), 2020 as many as 478 publications (9.88%), 2019 as many as 388 publications (8.02%), 2018 as many as 308 publications (6.37%), 2017 as many as 234 publications (4.84%), 2016 as many as 205 publications (4.24%), 2015 as many as 187 publications (3.87%) and 2014 as many as 153 publications (3.16%).

Figure 2. Number of publications per year on financial sustainability

3.2 Top 10 journals of scientific publications on financial sustainability

The search results show that based on 4,836 publications on financial sustainability indexed in the Scopus database, the publications were published in 464 journals. Of the 464 journals that have published research on financial sustainability, there are 10 top journals about 1.425 of all financial sustainability research as presented in Table 2. Of the 10 highest journals that publish research results on financial sustainability, the Journal of Cleaner Production is the most numerous, namely 413 publications (8.54%), followed by Business Strategy and The Environment as many as 183 publications (3.78%), Corporate Social Responsibility and Environmental Management as many as 122 publications (2.52%), Journal of Risk and Financial Management as many as 77 publications (1.59%), Sustainability Accounting Management and Policy Journal with 74 publications (1.53%), Journal of Sustainable Finance and Investment with 66 publications (1.36%), Technological Forecasting and Social Change with 63 publications (1.30%), Cogent Business and Management with 50 publications (1.03%), Journal of Business Ethics with 48 publications (0.99%), and Meditari Accountancy Research with 44 publications (0.91%).

Table 2. Top 10 journals publishing financial sustainability

|

Ranking |

Journal |

Count |

|

1 |

href="https://remote-lib.ui.ac.id:2120/sourceid/19167?origin=resultsAnalyzer&zone=sourceTitle" title="View documents by source" Journal of Cleaner Production |

413 |

|

2 |

Business Strategy and the Environment |

183 |

|

3 |

Corporate Social Responsibility and Environmental Management |

122 |

|

4 |

Journal of Risk and Financial Management |

77 |

|

5 |

Sustainability Accounting Management and Policy Journal |

74 |

|

6 |

Journal of Sustainable Finance and Investment |

66 |

|

7 |

Technological Forecasting and Social Change |

63 |

|

8 |

Cogent Business and Management |

50 |

|

9 |

Journal of Business Ethics |

48 |

|

10 |

Meditari Accountancy Research |

44 |

Source: Scopus, Processed

3.3 Productive authors of financial sustainability based on citation

Table 3 shows that there are ten researchers who are most productive in publishing research results on financial sustainability. It was found that Buallay from Ahlia University, Bahrain is the most productive researcher who has published about financial sustainability as many as 13 publications and has been cited 1,763 times. Velte from Leuphana Universitat Luneberg, Germany has published 12 publications and has been cited 2,821 times. Garcia-Shanchez from IME Business School, Spain, Luthra from All India Council of Technical Education, India, de Villiers from The University of Auckland Business School, New Zealand. There are ten publications of financial sustainability research results with 12,189, 14,684, and 6,514 citations respectively.

Table 3. Top 10 authors of financial sustainability

|

Author |

Documents |

Citations |

|

Buallay, A. |

13 |

1,763 |

|

Velte, P. |

12 |

2,821 |

|

Garcia-Shanchez, I.M. |

10 |

12,189 |

|

Luthra, S. |

10 |

14,684 |

|

de Villiers, C. |

10 |

6,514 |

|

Adhariani, D. |

9 |

406 |

|

Pizzi, S. |

9 |

2,191 |

|

Rezaee, Z. |

9 |

3,461 |

|

Dollery, B. |

8 |

4,194 |

|

Kuzey, C. |

8 |

3,132 |

Source: Scopus, Processed

3.4 Top 10 scientific publications by universities

Based on Figure 3, the most productive institution for scientific publications on financial sustainability based on affiliation/institution is Universiti Teknologi MARA with 42 publications, then, in a row, Universiti Sains Malaysia with 36 publications, followed by Universiti Utara Malaysia with 34 publications, University of Johannesburg and Sapienza Università di Roma with 31 publications each, Universidad de Granada with 12 publications, Brunel University London, Università del Salento 27 publications each and The Hong Kong Polytechnic University, RMIT University 26 publications each.

Figure 3. Top 10 of scientific publications by universities

3.5 Top 10 scientific publications by countries

Research publications on financial sustainability indexed in the Scopus database are published by 130 countries, of which the United States has 560 publications, the United Kingdom has 508 publications, India has 464 publications, and Italy has 426 publications. Meanwhile, China and Australia published 337 and 302 publications respectively. Table 4 shows the distribution of countries that publish research on financial sustainability.

Table 4. Top 10 scientific publications by countries

|

Ranking |

Country |

Count |

|

1 |

United State |

560 |

|

2 |

United Kingdom |

508 |

|

3 |

India |

464 |

|

4 |

Italy |

426 |

|

5 |

China |

337 |

|

6 |

Australia |

302 |

|

7 |

Spain |

287 |

|

8 |

Malaysia |

267 |

|

9 |

Indonesia |

239 |

|

10 |

Germany |

191 |

3.6 Scientific publications on financial sustainability by subject

Table 5 illustrates the distribution of publications on financial sustainability across different academic disciplines. The field of Business, Management, and Accounting clearly dominates the research landscape with a substantial 2.074 publications, representing the largest share. Economics, Econometrics, and Finance form the second largest area of focus with 739 publications. Social Science and Environmental Science also contribute significantly to the literature, with 589 and 391 publications. Engineering, Decision Science, and Energy each have a moderate number of publications, with 309, 246 and 287 publications.

Table 5. Scientific publications on financial sustainability by subject

|

Subject |

Count |

|

Business, Management and Accounting |

2,074 |

|

Economics, Econometrics and Finance |

739 |

|

Social Science |

589 |

|

Environmental Science |

391 |

|

Engineering |

309 |

|

Decision Science |

246 |

|

Energy |

287 |

|

Computer Science |

62 |

|

Arts and Humanities |

58 |

|

Psychology |

53 |

|

Agricultural and Biological Science |

46 |

|

Medicine |

33 |

|

Mathematics |

25 |

|

Materials Science |

15 |

|

Nursing |

9 |

|

Biochemistry, Genetics and Molecular Biology |

8 |

|

Earth and Planetary Sciences |

7 |

|

Veterinary |

6 |

|

Physics and Astronomy |

3 |

|

Chemical Engineering |

2 |

|

Health Professions |

2 |

|

Multidisciplinary |

2 |

|

Pharmacology, Toxicology and Pharmaceutics |

2 |

A noticeable drop-off occurs after Energy, with the remaining subjects having considerably fewer publications. Computer Science and Arts and Humanities both have 58-62 publications. Psychology, Agricultural and Biological Science, and Medicine have between 33 and 53 publications. Fields like Mathematics, Materials Science, and Nursing have a much smaller presence, with publications in the single digits or low teens. Finally, several disciplines, including Biochemistry, Genetics and Molecular Biology, Earth and Planetary Sciences, Veterinary, Physics and Astronomy, Chemical Engineering, Health Professions, Multidisciplinary, and Pharmacology, Toxicology and Pharmaceutics, have the fewest publications, each with only 2-8 entries. This suggests that research on financial sustainability is less prevalent in these areas.

3.7 Keywords

Bibliometric analysis, particularly using VOSviewer software, provides valuable insights into the research landscape of financial sustainability from 2014 to 2024. By analyzing frequently used keywords, this study utilizes three visualizations: Network Visualization, Overlay Visualization, and Density Visualization. VOSviewer also divides frequently used keywords for the emergence of co-citations of sources into clusters (Table 6).

Figure 4, a Network Visualization, represents keywords as circles, with size indicating frequency of occurrence. Larger circles represent more frequently used keywords, highlighting prominent research topics. The software automatically groups related keywords into clusters, each represented by a distinct color. For instance, the keyword "sustainability," being a central theme, appears as a larger circle due to its high occurrence.

Keywords for the emergence of co-citations of sources have been determined as shown in Table 6. The result using the VOSviewer indicates 109 items in 6 clusters, 2,466 links, and 11,400 total link strength.

Figure 4. Trending research topics in the field financial sustainability Scopus database processed with VOSviewer

Table 6. Cluster of financial sustainability

|

Cluster 1 |

Red |

34 Keywords |

Accountability, Accounting, Agency theory, Assurance, Board of Directors, Corporate Governance, Corporate Social Responsibility, Disclosure, Earnings management, ESG, ESG Disclosure, Financial reporting, Fintech, Firm performance, Firm value, Global Reporting Initiative, GRI, Institutional theory, Integrated reporting, Legitimacy theory, Non-financial information, Non-financial reporting, Reporting, Social responsibility, Stakeholders engagement, Stakeholders theory, Stakeholders, Sustainability accounting, Sustainability disclosure, Sustainability report, Sustainability reporting, Sustainability development, Sustainable finance, Transparency. |

|

Cluster 2 |

Green |

22 Keywords |

Cost benefit analysis, Costs, Decision making, Developing countries, Economics analysis, Economics and social effects, Economic development, Economic growth, Economic sustainability, Economics, Energy policy, Environmental sustainability, Environmental technology, Finance, Financial development, Financial markets, Global warming, Investments, Planning, Sustainable development, Technological innovation, Waste management. |

|

Cluster 3 |

Blue |

20 Keywords |

Banking, COVID-19, Development, Emerging markets, Entrepreneurship, Financial crisis, Financial management, Financial stability, Financial sustainability, Human resource managements, Intellectual capital, Leadership, Performance, Risk, Risk assessment, Risk management, Social enterprise, Social entrepreneurship, Sustainability, Value creation. |

|

Cluster 4 |

Yellow |

15 Keywords |

Business development, Competitiveness, Corporate strategy, Environmental economics, Financial system, Governance approach, Green economy, Green innovation, Industrial performance, Innovation, Performance assessment, Small and medium-sized enterprise, Stakeholder, Stock market, Sustainable development. |

|

Cluster 5 |

Purple |

10 Keywords |

Business sustainability, Corporate financial performance, Corporate social performance, Environmental management, Environmental performance, Financial performance, Profitability, Social performance, Sustainability performance, Sustainability practices. |

|

Cluster 6 |

Neon Blue |

8 Keywords |

Balanced scorecard, Business performance, Competition, Corporate sustainability, Corporate-sustainability, Social sustainability, Sustainable supply chains, Triple bottom line. |

Figure 5 visually illustrates the publication years of 4,836 articles, using a color gradient where brighter yellow hues represent more recent publications. The visualization highlights key topics such as waste management, ESG disclosure, industrial performance, governance approaches, environmental economics, planning, environmental technology, stakeholders, corporate governance, financial development, and economics.

Figure 6, generated using VOSviewer, provides a visual representation of research density within the field of financial sustainability. The color intensity reflects the occurrence of keywords, with darker shades indicating areas with substantial research and lighter shades highlighting less explored areas. This visualization Allows researchers to quickly identify areas where further investigation is needed, revealing potential research gaps and opportunities for contributing to new trends within the field of financial sustainability.

Figure 5. Overlay visualization of the Scopus database processed with VOSviewer

Figure 6. Potential trending topics for future research

Financial sustainability is a complex and multidimensional concept that has been the subject of extensive scholarly discourse. At its core, financial sustainability refers to the ability of an organization to maintain its financial viability and resilience over the long term, while simultaneously considering its environmental, social, and governance impacts. Existing research has highlighted various aspects and characteristics of financial sustainability, including the integration of sustainability considerations into financial decision-making, the alignment of financial performance with broader sustainability objectives, and the adoption of sustainable business practices that ensure long-term profitability and growth [24, 25]. The extant literature on financial sustainability draws from a range of theoretical frameworks, including stakeholder theory, resource-based view, and institutional theory, which shed light on the multifaceted nature of this concept and the various factors that influence an organization's financial sustainability [26-29].

The integration of sustainability into finance has been a gradual and complex process, as evidenced by the diverse body of literature on the subject. Researchers have explored the shift towards sustainable finance and financial reporting, examining emerging trends, research patterns, and implications for global sustainable development. The profusion of environmental, social, and governance data and the growing number of companies reporting on these metrics have been instrumental in facilitating this transition, as investors and companies alike seek to evaluate the financial viability an as well as the broader sustainability impact of their operations. Existing research has highlighted the importance of this topic, indicating that corporate sustainability has already become a central issue for the practice of strategic management, with a significant proportion of large companies worldwide incorporating sustainability information into their annual financial reports [30-33].

The conceptualization of financial sustainability is further enriched by the exploration of various aspects, characteristics, and influencing factors that shape an organization's long-term financial well-being. These include the integration of sustainability considerations into financial decision-making, the alignment of financial performance with broader sustainability objectives, the adoption of sustainable business practices, and the impact of external factors such as regulatory environments, stakeholder expectations, and market dynamics.

Since 2014, according to Scopus, 4,836 papers have been published in this field between 2014 and 2024. It has published the most with 560 studies in United State. The United Kingdom and India each contributed 508 and 464 studies to the field on financial sustainability. This research shows that, 210 organizations have been actively conducting studies in this field, Universiti Tekonologi MARA has published a maximum of 42 documents. The leading journals “Journal of Cleaner Production” and “Business Strategy and The Environment” have published the most journals in this field. Of the top 10 authors who have contributed to this field, such as Buallay, A. (13 documents with 1,763 citations), Velte, P. (12 documents with 2,821 citations), Garcia-Shanchez, I.M. (10 documents with 12,189 citations).

The growth trend in the distribution of scientific publications on financial sustainability indexed in the Scopus database peaks in 2024, which is 937 publications (19.38%). Of the ten highest journals that carry out scientific publications on financial sustainability, the Journal of Cleaner Production is the most numerous, namely 413 publications (8.54%). The most productive author of scientific publications on financial sustainability is Buallay from Ahlia University, Bahrain. The most productive affiliation/institution for scientific publications on financial sustainability is Universiti Teknologi MARA with 42 publications. Judging by country, the most productive in publishing about financial sustainability is the United States with 560 publications. By using VOSviewer software, it is found that the development map of financial sustainability publications is divided into six clusters. The most used keywords in the literature are sustainability, sustainable development, financial performance, corporate social responsibility, and sustainability reporting. Research topics that are the center of attention are sustainability and sustainable development and there are topics that have the potential to be associated with financial sustainability, such as cost, transparency, ESG disclosure, risk management, waste management. The conclusion of this study is that the development of scientific publications in the field of Scopus-based financial sustainability from 2014-2024 has experienced positive growth, especially from 2021-2024, which has experienced a sharp increase from year to year, which means that this topic is still in demand from various subjects.

This research acknowledges several limitations. Firstly, relying solely on article titles, abstracts, and keywords for journal discovery may exclude relevant articles outside the defined search scope. Secondly, limiting the analysis to publications within the last decade provides an incomplete historical context of the research field's development. Thirdly, restricting the study to English language publications within the Scopus database excludes potentially valuable research in other languages, such as Chinese, Arabic, or Indonesian, potentially impacting the findings. Lastly, while bibliometric data identifies the United States and the United Kingdom as major contributors to research, the limited availability of publications specifically addressing "Financial Sustainability" suggests a need for further exploration within this field.

This research provides valuable insights for academics and practitioners. For academia, the growth in publications, especially the recent surge, signals a burgeoning interest in financial sustainability. This presents opportunities for researchers to delve deeper into unexplored areas and contribute to the expanding body of knowledge. The identified keywords and research topics provide a roadmap for future research directions. For example, exploring the intersection of financial sustainability with cost, transparency, ESG disclosure, risk management, and waste management could yield valuable insights. For practice, the increasing research focus reflects the growing importance of financial sustainability in the business world. Companies need to be aware of this trend and integrate financial sustainability principles into their operations and decision-making processes. Practitioners can benefit from the insights generated by academic research to develop and implement effective financial sustainability strategies. The research findings can inform best practices in areas such as cost management and risk management.

The findings highlight important areas for future research, such as further investigating topics that have the potential to be linked to financial sustainability such as cost, transparency, risk management. Future research could develop a comprehensive financial sustainability measurement framework. In addition, there is room for further research that compares publication trends related to financial sustainability in different regions, especially in developing countries.

[1] Xue, W.Z., Li, H., Ali, R.W., Rehman, R.U. (2020). Knowledge mapping of corporate financial performance research: A visual analysis using cite space and ucinet. Sustainability, 12(9): 3554. https://doi.org/10.3390/su12093554

[2] Iotti, M., Bonazzi, G. (2023). Financial sustainability in agri-food companies: The case of members of the PDO Parma ham consortium. Sustainability, 15(5): 3947. https://doi.org/10.3390/su15053947

[3] Wang, H., Huang, J.Y., Yang, Q. (2019). Assessing the financial sustainability of the pension plan in China: The role of fertility policy adjustment and retirement delay. Sustainability, 11(3): 883. https://doi.org/10.3390/su11030883

[4] Bowman, W. (2011). Financial capacity and sustainability of ordinary nonprofits. Nonprofit Management and Leadership, 22(1): 37-51. https://doi.org/10.1002/nml.20039

[5] Thompson, J., Doherty, B. (2006). The diverse world of social enterprise: A collection of social enterprise stories. International Journal of Social Economics, 33(5/6): 361-375. https://doi.org/10.1108/03068290610660643

[6] Kakati, S., Roy, A. (2021). Financial sustainability: An annotated bibliography. Economics and Business Review, 7(3): 35-60. https://doi.org/10.18559/ebr.2021.3.4

[7] Ahmad, I., Alni, R., Arni, S. (2023). Financial literacy to improve sustainability: A bibliometric analysis. Studies in Business and Economics, 18(3): 24-43. https://doi.org/10.2478/sbe-2023-0043

[8] Luo, W.B., Tian, Z.Y., Zhong, S.H., Lyu, Q.K., Deng, M.J. (2022). Global evolution of research on sustainable finance from 2000 to 2021: A bibliometric analysis on WoS database. Sustainability, 14(15): 9435. https://doi.org/10.3390/su14159435

[9] Smith, A.D. (2009). Financial sustainability through contingency planning: Multi-case study. International Journal of Sustainable Economy, 1(4): 317-334. https://doi.org/10.1504/IJSE.2009.02476

[10] Aspinall, N.G., Jones, S.R., McNeill, E.H., Werner, R.A., Zalk, T. (2018). Sustainability and the financial system review of literature 2015. British Actuarial Journal, 23: e10. https://doi.org/10.1017/S1357321718000028

[11] Princes, E., Said, A. (2022). The impacts of project complexity, trust in leader, performance readiness and situational leadership on financial sustainability. International Journal of Managing Projects in Business, 15(4): 619-644. https://doi.org/10.1108/IJMPB-03-2021-0082

[12] Rai, A., Kanwal, A., Sharma, M. (2010). Financial sustainability of microfinance institutions: A new model approach. Asia Pacific Business Review, 6(4): 12-17. https://doi.org/10.1177/097324701000600402

[13] López-Medina, T., Mendoza-Ávila, I., Contreras-Barraza, N., Salazar-Sepúlveda, G., Vega-Muñoz, A. (2021). Bibliometric mapping of research trends on financial behavior for sustainability. Sustainability, 14(1): 117. https://doi.org/10.3390/su14010117

[14] Cano, J.A., Londoño-Pineda, A. (2020). Scientific literature analysis on sustainability with the implication of open innovation. Journal of Open Innovation: Technology, Market, and Complexity, 6(4): 162. https://doi.org/10.3390/joitmc6040162

[15] Kashi, A., Shah, M.E. (2023). Bibliometric review on sustainable finance. Sustainability, 15(9): 7119. https://doi.org/10.3390/su15097119

[16] Ellili, N.O.D. (2022). Is there any association between FinTech and sustainability? Evidence from bibliometric review and content analysis. Journal of Financial Services Marketing, 1: 1-15. https://doi.org/10.1057/s41264-022-00200-w

[17] Murdayanti, Y., Khan, M.N.A.A. (2021). The development of internet financial reporting publications: A concise of bibliometric analysis. Heliyon, 7(12): e08551. https://doi.org/10.1016/j.heliyon.2021.e08551

[18] Tuyon, J., Onyia, O.P., Ahmi, A., Huang, C.H. (2023). Sustainable financial services: Reflection and future perspectives. Journal of Financial Services Marketing, 28: 664-690. https://doi.org/10.1057/s41264-022-00187-4

[19] Thottoli, M.M., Islam, M.A., Sobhani, F.A., Rahman, S., Hassan, M.S. (2022). Auditing and sustainability accounting: A global examination using the Scopus database. Sustainability, 14(23): 16323. https://doi.org/10.3390/su142316323

[20] Kaur, A., Kumar, V., Sindhwani, R., Singh, P.L., Behl, A. (2024). Public debt sustainability: A bibliometric co-citation visualization analysis. International Journal of Emerging Markets, 19(4): 1090-1110. https://doi.org/10.1108/IJOEM-04-2022-0724

[21] Rafols, I. (2014). Knowledge integration and diffusion: Measures and mapping of diversity and coherence. Measuring scholarly impact: Methods and practice, Springer International Publishing, USA, pp. 169-190. https://doi.org/10.1007/978-3-319-10377-8_8

[22] Donthu, N., Kumar, S., Mukherjee, D., Pandey, N., Lim, W.M. (2021). How to conduct a bibliometric analysis: An overview and guidelines. Journal of Business Research, 133: 285-296. https://doi.org/10.1016/j.jbusres.2021.04.070

[23] Van Eck, N.J., Waltman, L. (2011). Text mining and visualization using VOSviewer. arXiv preprint arXiv: 1109.2058. https://doi.org/10.48550/arXiv.1109.2058

[24] Hutchinson, D., Singh, J., Walker, K. (2012). An assessment of the early stages of a sustainable business model in the Canadian fast food industry. European Business Review, 24(6): 519-531. https://doi.org/10.1108/09555341211270537

[25] Alshehhi, A., Nobanee, H., Khare, N. (2018). The impact of sustainability practices on corporate financial performance: Literature trends and future research potential. Sustainability, 10(2): 494. https://doi.org/10.3390/su10020494

[26] Sempere-Ripoll, F., Estelles-Miguel, S., Rojas-Alvarado, R., Hervas-Oliver, J.L. (2020). Does technological innovation drive corporate sustainability? Empirical evidence for the European financial industry in catching-up and central and eastern Europe countries. Sustainability, 12(6): 2261. https://doi.org/10.3390/su12062261

[27] Salzmann, A.J. (2013). The integration of sustainability into the theory and practice of finance: An overview of the state of the art and outline of future developments. Journal of Business Economics, 83: 555-576. https://doi.org/10.1007/s11573-013-0667-3

[28] Gupta, S., Kumar, V. (2013). Sustainability as corporate culture of a brand for superior performance. Journal of World Business, 48(3): 311-320. https://doi.org/10.1016/j.jwb.2012.07.015

[29] Mujiani, S. (2023). Exploring the shift toward sustainable finance and financial reporting: An extensive analysis of emerging trends, research patterns, and implications for global sustainability. West Science Accounting and Finance, 1(2): 52-58. https://doi.org/10.58812/wsaf.v1i02.111

[30] Ioannou, I., Serafeim, G. (2019). Corporate sustainability: A strategy? Harvard Business School Accounting & Management Unit Working Paper, (19-065): 1-55. https://doi.org/10.2139/ssrn.3312191

[31] Nugrahani, T.S., Kusuma, H., Arifin, J., Muhammad, R. (2023). Determinants of sustainability report quality in Indonesian public companies: An isomorphism theory approach. International Journal of Sustainable Development and Planning, 18(12): 3909-3921. https://doi.org/10.18280/ijsdp.181222

[32] Ali, A. (2022). Sustainability of financial soundness of banks: An evidence form public and private sector banks. International Journal of Sustainable Development and Planning, 17(8): 2463-2473. https://doi.org/10.18280/ijsdp.170814

[33] Stefany, J., Agustina, L. (2022). Do corporate social responsibility and political connections matter to financial performance and financial stability in the banking sector? Evidence from Indonesia. International Journal of Sustainable Development and Planning, 17(8): 2445-2452. https://doi.org/10.18280/ijsdp.170812