Agung Nur Probohudono*![]() | Khresna Bayu Sangka

| Khresna Bayu Sangka![]() | Estetika Mutiaranisa Kurniawati

| Estetika Mutiaranisa Kurniawati![]() | Adhitya Agri Putra

| Adhitya Agri Putra![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This research aims to examine the moderating role of financial sustainability in the effect of carbon emission reduction on firms’ value. In detail, this research examines the moderating role of solvency performance, firms’ growth, and business risk reduction between the effect of carbon emission reduction on firms’ value. The research sample includes 171 firm-years listed on the index of LQ45 in 2022-2024. Firms’ value is measured by Tobin’s Q. Carbon emission reduction is measured by a dummy variable. Financial sustainability includes solvency performance, firms’ growth, and business risk reduction. Data analysis uses firm-fixed and industry-fixed effects regression. Based on data analysis, carbon emission increases firms’ value when firms have better solvency performance, higher growth, and lower business risk. This research gives a literature contribution by capturing signaling theory comprehensively. It also provides new evidence of financial sustainability as a moderating role between carbon emission reduction and firms’ value and fills the previous gap of findings.

carbon emission, firms’ value, financial sustainability

Climate change has become one of the most pressing global challenges of the 21st century, manifesting in issues such as global warming, pollution, environmental degradation, and carbon emissions [1, 2]. These issues have spurred international efforts to mitigate the adverse effects of climate change, with global bodies such as the United Nations spearheading initiatives like the United Nations Framework Convention on Climate Change (UNFCCC) [3]. This convention plays a crucial role in guiding countries toward adopting policies aimed at reducing carbon emissions, with the ultimate goal of preventing further environmental damage.

Indonesia, as a signatory to the UNFCCC, has been actively involved in these international efforts. The government has introduced a series of regulatory measures designed to align with global environmental goals, such as Presidential Regulation (PP) No. 98 of 2021 and Ministry of Environment and Forestry Regulation (PERMEN LHK) No. 21 of 2022. These regulations are part of a broader framework for reducing carbon emissions, specifically addressing the economic value of carbon emissions and promoting the reduction of greenhouse gases. The pressure from international bodies, coupled with the increasing scrutiny from local stakeholders, has pushed Indonesian businesses to engage in carbon emission reduction initiatives [4].

Carbon emission reduction gives benefits to firms’ value. Based on signaling theory, carbon emission reduction is a signal of business development such as green customer segment creation [5, 6], expense efficiency for energy usage [5-7], and conflict reduction between firms and regulators [6, 8]. Carbon emission reduction also can compose business sustainability [4]. Some studies find that value creation by carbon emission reduction only happens in Western countries such as in the US [9-12] and Europe [13]. On the other hand, carbon emission reduction promotes investment risk in Asian countries [14], including India [15].

In Indonesia, the relationship between carbon emission reduction and firms’ values is also mixed. Kurnia et al. [16] found a positive relationship between carbon emission reduction and firms’ values while Mahmudah et al. [17] found the negative one. Furthermore, Ramadhan et al. [18] did not find a significant relationship between carbon emission reduction and firms’ values.

Zheng and Jin [19] suggested that carbon emission reduction can create value for firms if carbon emission reduction constructs the development of business sustainability, including sustainable finance. In this case, inconsistent findings of carbon emission reduction and firms’ value [9-18] come from the absence of a financial sustainability factor to determine whether carbon emission reduction promotes financial sustainability to create value for the firms. Since carbon emission reduction relates to financial sustainability [4], it is important to explain carbon emission reduction contribution to value creation by improving financial sustainability. This research determines that financial sustainability is an important factor to explain the relationship between carbon emission reduction and firms’ value.

This research follows Gleißner et al. [20] to determine financial sustainability factors including solvency performance, firms’ growth, and business risk reduction. Solvency performance suggests financial sustainability as the aspect of firms’ ability to fulfil the future obligation to pay the liabilities so that in the future, firms have no financial problems [21]. In the context of firm’ growth, growing firms promote financial sustainability by creating expense efficiency and revenue growth persistently [22, 23]. Business risk is an indicator of financial sustainability since business risk captures uncertainty and losses in the future [24].

There are some urgencies for carbon emission reduction in Indonesia. First, there are regulations of PP no. 98 2021 and PERMEN LHK no. 21 2022 that regulate firms to reduce carbon emissions. Second, in 2016, Indonesia contributed to 5% of total carbon emissions globally, or 1,841.14 MtCO2 that put Indonesia in the top five most carbon emission producers after Russia. Third, Sustainable Development Goals (SDGs) No. 13 suggests climate change mitigation by reducing carbon emissions. Fourth, there are inconsistent findings of carbon emissions reduction and firms’ value between Western countries [9-13], and Asian countries [14, 15], including Indonesia [16-18].

This research aims to examine whether solvency performance, firms’ growth, and business risk reduction moderate the effect of carbon emission reduction on firms’ values in the index of LQ45, Indonesian Stock Exchange. First, the Indonesian Stock Exchange launched the index of Low Carbon Leader LQ45 in 2022 as a derivative index from the index of LQ45. Index of Low Carbon Leader LQ45 aims to accommodate green investors to invest in stocks where the firms have commitment in carbon emission reduction. Second, the index of LQ45 provides stocks that have the most liquid transactions. It leads to the update of shareholders’ wealth changes since stock transaction leads to the stock price change and shareholders’ wealth indicator to capture firms’ value [25].

This research has some contributions. First, this research gives a literature contribution by capturing signaling theory comprehensively. Financial sustainability is examined as an interpretation of signal of carbon emission reduction for firms’ value improvement. Second, this research provides new evidence of financial sustainability as a moderating role between carbon emission reduction and firms’ value. Third, this research fills the previous gap of findings in Western countries [9-13] and Asian ones [14-18].

2.1 Signaling theory

Signaling theory is widely utilized in corporate finance and organizational studies to explain how firms communicate information about their quality, prospects, and intentions to external stakeholders, particularly investors. Initially developed in the context of labor markets [26], signaling theory has since been adapted to various fields, including corporate governance, sustainability, and environmental responsibility.

In the context of environmental management, firms that engage in activities such as carbon emission reduction send positive signals to the market, reflecting their commitment to sustainability and responsible corporate practices. These signals are intended to differentiate the firm from competitors, thereby enhancing its reputation, attracting socially conscious investors, and potentially improving financial performance.

This research captures the relationship among carbon emission reduction, financial sustainability, and firms’ value by using signaling theory. Lee et al. [27] explained signaling theory as a concept to shows the signaling process by the firms to give information of firms; quality to the external parties. Signaling process consists of signal creation by signaler, signal interpretation by external parties, and external parties’ responses [28-31]. In this case, firms give signal of financial sustainability to create values for the firms [27].

According to signaling theory, firms convey important information about their quality through their actions, including carbon emission reduction efforts. These actions signal to investors and stakeholders that the firm is committed to long-term sustainability and financial health [32]. This study expands on the current understanding by showing how financial sustainability acts as a moderating factor in this signaling process.

The impact of such signals is influenced by external elements, including the company's financial health and the overall market environment. Matsumura et al. [9] observed that in Western markets, investors tend to reward companies for reducing carbon emissions, as it aligns with long-term environmental objectives and helps manage risks. Likewise, Clarkson et al. [13] suggest that cutting carbon emissions boosts a firm's value by decreasing the likelihood of regulatory disputes and minimizing the risk of environmental fines.

2.2 Financial sustainability

In general, financial sustainability captures firms’ performance in the fields of economics, society, environment, and governance [33]. In the context of this research, financial sustainability relates to how carbon emission reduction can give financial benefit to firms to ensure that firms can generate sustain and persistent good financial performance in the future [20].

In this research, financial sustainability includes solvency performance, firms’ growth, and business risk reduction [20]. Solvency performance shows that firms can fulfil future obligation to pay liabilities in the future and can mitigate the default risk. Roy and Bandopadhyay [33] find that better solvency can mitigate financial risk and increase firms’ value. Gleißner et al. [20] explains that firms that always grow persistently indicates that firms can ensure business sustainability in the future. Yadav et al. [34] suggest that growing firms can generate more profits. Business risk shows that there are uncertainties in the future, so firms that can reduce the business risk can mitigate uncertainties in the future and increase firms’ value. Roy and Bandopadhyay [33] find that risk reduction is followed by value creation. This research argues that carbon emission reduction that promotes solvency performance, firms’ growth, and business risk reduction can increase firms’ value.

2.3 Carbon emission and firms’ values

In the context of firms’ and stocks’ values, there are some studies of carbon emissions. Figure 1 shows the scheme of carbon emission studies based on the last 1,000 researches.

Figure 1 shows bibliometric analysis with the keywords of “carbon emission”, “stock value”, and “firm value”. Studies of carbon emissions mostly relate to stock valuation on the stock market. Most topics that have been examined are carbon emission reduction, carbon exchange, carbon-based stock, sustainability, and corporate social responsibility.

Figure 1. Carbon emission studies

Some studies of carbon emission and value creation lead to inconsistent findings, especially the gap between Western countries and Asian ones. Matsumura et al. [9] examine carbon emissions and firms’ value in the US. Matsumura et al. [9] found that for every carbon emission reduction of 1,000 metric tons, firms can maintain firms’ value as 212,000 USD. Clarkson et al. [13] examine European firms and find that carbon emission reduction leads to efficiency of conflict expenditure. Cooper et al. [11] find that carbon emission reduction in the US can increase firms’ value through the improvement of firms’ reputation. Griffin et al. [10] found that carbon emission disclosure in the US gets a positive response from investors. Ott and Schiemann [12] also found the positive relationship between carbon emission reduction and firms’ value.

On the other hand, in Asian countries, carbon emission reduction is not followed by value improvement. Feng et al. [14] found that carbon emission reduction in Asia increases investment risk. Manchiraju and Rajgopal [15] also find that carbon emission reduction in India gets a negative response from investors. In Indonesia, there are inconsistent findings, for example, Kurnia et al. [16] found the positive relationship between carbon emission reduction and firms’ value while Mahmuda et al. [17] found the negative relationship, moreover, Ramadhan et al. [18] find no significant relationship between carbon emission reduction and firms’ value. Han et al. [35] explained that Asian investors still consider carbon emission reduction only to give benefits to other stakeholders that relate to social and environmental aspects, while investors get no benefits from carbon emission reduction. This research considers financial sustainability as a signal that investors can get benefits from carbon emission reduction.

2.4 Hypotheses development

On one hand, carbon emission reduction can increase firms’ value. First, carbon emission reduction captures the mitigation of damage risk to the environment [36]. Environmental damage can disturb firms’ business in the future and lead to potential losses. The potential of losses can reduce the potential of dividends and gain in the future for investors. When investors experience potential losses, firms’ value will be reduced. In contrast, when firms mitigate the environmental damage by carbon emission reduction, investors can get more potential profits.

Second, carbon emission reduction can reduce conflict expenses. The conflict can come from the regulator and society [37]. Carbon emission reduction can reduce penalties and punishment from regulators. Carbon emission reduction can also mitigate the protests from society and the community. Firms can avoid expenses from the conflict and generate more profits that can lead to more potential investors' gains.

Third, carbon emission reduction can promote a good reputation for the firms [38]. Good reputation can increase stock price in the market. Higher stock price promotes more shareholders’ wealth for investors and increases firms’ value. Matsumura et al. [9], Clarkson et al. [13], Cooper et al. [11], Griffin et al. [10], and Ott and Schiemann [12] find that carbon emission reduction improves firms’ value.

On the other hand, carbon emission reduction can also reduce firms’ value. First, firms pay more expenses for carbon emission reduction [39]. Higher expenses can generate lower profits. Second, investors assume that carbon emission reduction gives benefits more to other stakeholder (regulators and society) than investors [35]. Third, the main motivation for carbon emission reduction, especially in Indonesia, is only to avoid punishment and penalty for regulation violations [40]. Feng et al. [14], Manchiraju and Rajgopal [15], and Mahmuda et al. [17] find that carbon emission reduction has a negative effect on firms’ valuation.

One of the benefits of the implementation of carbon emission reduction is financial sustainability. Matsumura et al. [9] explained that carbon emission reduction is responded positively by investors because carbon emission reduction promotes risk reduction. However, Matsumura et al. [9] do not examine the risk reduction that leads to financial sustainability. Conflict reduction and reputation only occur in the current period and do not ensure the sustain and persistent performance in the future. In this case, conflict reduction and reputation fail to capture benefits of carbon emission in the future. Han et al. [35] explain that carbon emission reduction can only give benefit when financial sustainability occurs, especially for value creation.

This research argues that carbon emission reduction with financial sustainability can increase firms’ value. First indicator of financial sustainability in solvency performance. Solvency level shows the ability to pay liabilities in the future to mitigate default risk and ensure sustain and persistent financial performance in the future. Firms with green investment and reduce carbon emission can increase long-term profits and ensure future payment of liabilities [41]. Magnanelli and Izzo [42] and Oware et al. [43] find that environmental responsibility without better solvency performance gives no benefits to firms’ performance. Roy and Bandopadhyay [33] also find that better solvency performance reduces financial risk and creates firms’ value.

H1: Solvency performance moderates the effect of carbon emission reduction on firms’ value.

Second indicator of financial sustainability is firms’ growth. Gleißner et al. [20] explain that growing firms can bring better performance in the future. Carbon emission reduction that is based on growth can bring competitive advantages for the firms including a new market segment of green customers [5, 6] and efficiency of energy [5-7]. Growing segment and energy efficiency lead to higher profits [44, 45]. Yadav et al. [34] find that firms’ growth increase firms’ value.

H2: Firms’ growth moderates the effect of carbon emission reduction on firms’ value.

Third indicator of financial sustainability is business risk reduction. Business risk capture business uncertainty in the future that can disturb firms’ sustainability. If carbon emission is not managed sufficiently, firms can bear higher environmental risk in the future and interfere firms’ business [46]. This research argues that carbon emission reduction can increase firms’ value if firms can get benefit of business risk. Ding et al. [46] find that carbon emission reduction relates to risk mitigation. Roy and Bandopadhyay [33] also find that business risk reduction can improve firms’ value.

H3: Business risk reduction moderates the effect of carbon emission reduction on firms’ value.

2.5 Theory framework

Figure 2. Theory framework

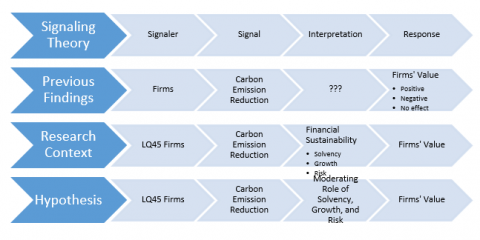

Figure 2 captures the theory framework of this research. Based on signaling theory, signaler gives signal to external parties to be interpreted and responded to. Previous research examines the effect of carbon emission reduction as a signal of firms’ quality and responded by investors as firms’ value. Previous finding gap is that there is no interpretation of financial sustainability from signal of carbon emission reduction. In this case, previous findings give mixed and inconsistent evidence. In the context of this research, signalers are LQ45 firms that give signal of carbon emission reduction. Carbon emission reduction is interpreted as financial sustainability (solvency performance, firms’ growth, and business risk reduction). If carbon emission reduction is followed by financial sustainability, firms’ value will be increased. This argument is taken down to research hypotheses that argue solvency performance, firms’ growth, business risk reduction moderates the effect of carbon emission reduction on firms’ value.

3.1 Research sample

This research uses purposive sampling method to choose research sample. Purposive sampling method allows this research to choose sample with certain criteria. First, this research chooses firms listed on the Indonesian Stock Exchange, especially those listed on the index of LQ45. The Indonesian Stock Exchange launched Low Carbon Leader LQ45 as a derivative index of LQ45. The index of Low Carbon Leader LQ45 facilitates green investors to invest in firms that are involved in implementation of carbon emission reduction. Index of LQ45 also accommodates stocks with active and liquid transactions that can reduce bias firms’ value determination [25]. Second, this research chooses firms listed on the index of LQ45 in the period of 2022-2024. The index Low Carbon Leader LQ45 is launched in 2022. Based on purposive sampling method, there are 171 firm-years as research sample. Sample selection can be seen in Table 1.

Table 1. Research sample

|

Criteria |

Period of Index LQ45 |

Total |

|||

|

Aug. 2022 |

Feb. 2023 |

Aug. 2023 |

Jan. 2024 |

||

|

Listed firms on the LQ45 |

45 |

45 |

45 |

45 |

180 |

|

Incomplete data |

- |

- |

- |

(9) |

(9) |

|

Net sample |

45 |

45 |

45 |

36 |

171 |

Table 1 shows there are 4 periods of index of LQ45 in 2022-2024 which are August 2022, February 2023, August 2023, and January 2024. Each period consists of 45 firms where the total listed firms on the index of LQ45 are 180 firm-years. In the period of January 2024, there are 9 firms which have no interim financial report. Net samples are 171 firms-years.

3.2 Research variables

Full Dependent variable is firms’ value. Firms’ value is an indicator of shareholders’ wealth that can be seen by stock value. Firms’ value is measured by Tobin’s Q. Based on Yoon and Chung [47] Tobin’s Q is an indicator that determine investors’ perception of the firms in the future. In this research, investors’ perception on future firms’ performance captures the firms’ sustainability valuation by the investors. Tobin’s Q is calculated as in Eq. (1) [47].

Tobin's Q= Market Value of Equity + Book Value of Liability Book Value of Assets (1)

Based on Eq. (1), market value of equity is calculated by stock price multiplied by number of outstanding stocks. Stock price refers to the price when the list of Low Carbon Leaders LQ45 is published with consideration of investors’ valuation of carbon emission reduction to the future firms’ performance happens when investors know the list of Low Carbon Leaders LQ45.

Independent variable is carbon emission reduction. Carbon emission reduction is measured by a dummy variable where score 1 for firms that are listed on the Low Carbon Leaders LQ45 and score 0 if otherwise. Listed firms on the Low Carbon Leaders LQ45 show that firms already implement carbon emission reduction above average of all listed firms on the index of LQ45.

Moderating variable is financial sustainability. Financial sustainability includes solvency performance, firms’ growth, and business risk reduction [20]. Solvency performance is measured by debt-to-equity ratio. Firms’ growth is measured by sales growth in the last 5 years. Business risk is measured by volatility of net income in the last 5 years. Measurements of solvency performance, firms’ growth, and business risk reduction can be seen in Eqs. (2)-(4) [20].

Debt to Equity Ratio = Book Value of Liability Book Value of Equity (2)

Firms ′ Growth =( Sales t Sales t−5)15−1 (3)

Business Risk=Standard Deviation of Net Incomet to Net Incomet−5Average of Net Incomet to Net Incomet−5 (4)

Based on Eq. (2), lower debt-to-equity ratio leads to better solvency performance and better financial sustainability. Based on Eq. (3), higher firms’ growth leads to better financial sustainability. Based on Eq. (4), lower business risk leads to better financial sustainability.

3.3 Data analysis

Full Data analysis uses moderating regression analysis by considering firm-fixed effect and industry-fixed effect. Firm-fixed effect aims to control that each firm has a different strategy to reduce carbon emission. Industry-fixed effect aims to control that each industry has different business characteristics that lead to different levels of carbon emission. Regression model is as shown in Eq. (5).

Value =a+b1 CARBON +b2 CARBON x SOLVENCY +b3 CARBON x GROWTH +b4 CARBON x RISK +b5 SOLVENCY + b6 GROWTH +b7 RISK +∑ Firm +∑ Industry +e (5)

Value is firms’ value. CARBON is carbon emission reduction. SOLVENCY is solvency performance. GROWTH is firms’ growth. RISK is business risk. ΣFirm is firm-fixed effect. ΣIndustry is industry-fixed effect. Hypothesis of H1 is accepted if coefficient of b2 is negative and significant. Hypothesis of H2 is accepted if coefficient of b3 is positive and significant. Hypothesis of H3 is accepted if coefficient of b4 is negative and significant.

4.1 Descriptive statistics

Table 2 shows that the lowest firms’ value (Value) is 0.43 and the highest is 10.24. On average, firms’ value is 1.72 with a deviation of 1.49. There are 64% of all 117 firm-years that have carbon emission reduction (CARBON). The highest solvency performance (SOLVENCY) is 0.03 while the lowest performance is 14.52. On average, solvency performance is 1.72 with a deviation of 2.49. The lowest firms’ growth (GROWTH) is -0.65 while the highest is 1.14. On average, firms’ growth is 0.15 with a deviation of 0.86. The lowest business risk (RISK) is -5.78 while the highest is 10.67. On average, business risk is 0.86 with a deviation of 1.19.

Table 2. Descriptive statistics

|

Statistics |

Value |

CARBON |

SOLVENCY |

GROWTH |

RISK |

|

Minimal |

0.43 |

0.00 |

0.03 |

-0.65 |

-5.78 |

|

Maximal |

10.24 |

1.00 |

14.52 |

1.14 |

10.67 |

|

Average |

1.72 |

0.64 |

1.72 |

0.15 |

0.86 |

|

Standard Deviation |

1.49 |

0.48 |

2.49 |

0.34 |

1.19 |

4.2 Classical assumption

Table 3 shows that significance value of Jarque Bera is above 0.05 which indicates that there is no normality problem. Significance value of Glejser is above 0.05 which indicates that there is no heteroscedasticity problem. Values of VIF are below 10 which indicates that there is no multicollinearity problem. Significance value of Serial Correlation LM is above 0.05 which indicates that there is no autocorrelation problem.

Table 3. Classical assumption

|

Test |

Result |

Notes |

|

Jarque Bera |

> 0.05 |

There is no normality problem |

|

Glejser |

> 0.05 |

There is no heteroscedasticity problem |

|

VIF |

< 10 |

There is no multicollinearity problem |

|

Serial Correlation LM |

> 0.05 |

There is no autocorrelation problem |

4.3 Regression analysis

Table 4 shows the interaction of carbon emission reduction and solvency performance (CARBON x SOLVENCY) has a coefficient value of -0.883 with a t-statistic of -3.435 (significant in 0.01). It indicates that H1 is accepted where solvency performance moderates the effect of carbon emission reduction on firms’ value. Interaction of carbon emission reduction and firms’ growth (CARBON x GROWTH) has a coefficient value of 0.831 with a t-statistic of 3.289 (significant in 0.01). It indicates that H2 is accepted where firms’ growth moderates the effect of carbon emission reduction on firms’ value. Interaction of carbon emission reduction and business risk (CARBON x RISK) has a coefficient value of -0.163 with a t-statistic of -1.888 (significant in 0.05). It indicates that H3 is accepted where business risk reduction moderates the effect of carbon emission reduction on firms’ value.

Table 4. Regression analysis

|

Variable |

Coefficient |

T-Statistics |

Significance |

|

CARBON |

0.630 |

1.579 |

0.116 |

|

CARBON x SOLVENCY |

-0.883 |

-3.435* |

0.001 |

|

CARBON x GROWTH |

0.831 |

3.289* |

0.001 |

|

CARBON x RISK |

-0.363 |

-1.888** |

0.041 |

|

SOLVENCY |

-0.659 |

-0.957 |

0.340 |

|

GROWTH |

0.411 |

0.800 |

0.425 |

|

RISK |

-0.312 |

-2.068** |

0.040 |

|

Constant |

1.217 |

||

|

Adjusted R-Squared |

0.073 |

||

|

F-Statistics |

2.915* |

Notes: *Significant in 0.01, **Significant in 0.05.

4.4 Discussion

This research aims to examine the moderating role of financial sustainability in the effect of carbon emission reduction on firms’ value. Financial sustainability includes solvency performance, firms’ growth, and business risk reduction.

First, this research shows that solvency performance moderates the effect of carbon emission reduction on firms’ value. Carbon emission reduction can improve firms’ value if carbon emission reduction promotes better solvency performance. Carbon emission reduction that promotes better firms’ ability to fulfil future obligation can reduce default risk and increase firms’ value. This result is consistent with Roy and Bandopadhyay [33] who find that solvency performance can reduce firms’ risk and create value.

Second, this research finds that firms’ growth moderates the effect of carbon emission reduction on firms’ value. Carbon emission reduction can improve firms’ value if carbon emission reduction promotes better firms’ growth. Carbon emission reduction leads firms to grow and ensure business sustainability in the future. This result is consistent with Yadav et al. [34] who find that firms’ growth can improve firms’ value.

Third, this research finds that business risk reduction moderates the effect of carbon emission reduction on firms’ value. Carbon emission reduction can improve firms’ value if carbon emission reduction promotes better business risk reduction. Carbon emission reduction allows firms to mitigate uncertainty in the future and improve value creation. This result is consistent with Roy and Bandopadhyay [33] who find that risk reduction leads to better firms’ value. This research confirms signaling theory where carbon emission reduction is interpreted as a signal of financial sustainability to improve firms’ value.

Research findings contribute to the growing body of literature on the financial implications of carbon emission reduction by highlighting the moderating role of financial sustainability. Firms that demonstrate strong solvency and growth prospects while reducing carbon emissions tend to experience enhanced firm value, suggesting that investors should prioritize companies with robust sustainability frameworks.

This research aimed to investigate the moderating role of financial sustainability—specifically solvency performance, firm growth, and business risk reduction—in the relationship between carbon emission reduction and firm value. By analyzing firms listed on the LQ45 index of the Indonesian Stock Exchange from 2022 to 2024, the study sheds light on the factors that influence the value creation potential of carbon emission reduction efforts.

The results indicate that carbon emission reduction can positively affect firm value, but only when accompanied by strong financial sustainability. Firms that demonstrate high solvency performance, consistent growth, and effective management of business risk are better positioned to capitalize on the benefits of carbon emission reduction initiatives. These findings emphasize that carbon emission reduction is not an isolated effort but should be integrated into a broader framework of financial and operational sustainability to enhance firm value.

Furthermore, this study provides new empirical evidence that supports the notion of carbon emission reduction as a signal of financial sustainability. Investors and stakeholders respond positively to firms that align their environmental strategies with long-term financial health, indicating that sustainability initiatives must be backed by sound financial practices to generate tangible benefits. By incorporating financial sustainability into the analysis, this research contributes to resolving the mixed findings reported in previous studies, particularly in the context of developing economies such as Indonesia.

From a theoretical perspective, this study extends the application of signaling theory by demonstrating that carbon emission reduction can act as a signal of financial sustainability, which in turn enhances firm value. The findings suggest that investors and stakeholders interpret carbon emission reduction efforts not only as a means of fulfilling regulatory obligations but also as an indicator of a firm’s overall financial health and future profitability. This expanded understanding helps reconcile the divergent results found in previous studies, particularly those that focused exclusively on the environmental aspects of carbon reduction without considering the financial context.

In practical terms, the findings of this research carry significant implications for corporate managers, policymakers, and investors. For corporate managers, the results highlight the importance of embedding carbon emission reduction within a larger strategy of financial sustainability. Firms that successfully align their environmental goals with strong solvency, growth, and risk management practices are more likely to achieve enhanced firm value and attract investor support. This underscores the necessity of integrating environmental, social, and governance (ESG) considerations into corporate strategy, particularly as global market trends increasingly favor sustainable business models.

Policymakers can also benefit from these insights by recognizing the critical role that financial sustainability plays in enabling firms to realize the full value of their carbon emission reduction efforts. Regulatory frameworks should, therefore, be designed to incentivize not only carbon reduction but also the adoption of broader financial sustainability practices. This would help ensure that firms are not only meeting environmental targets but are also building a solid foundation for long-term growth and resilience.

For investors, the study suggests that firms demonstrating both environmental responsibility and financial sustainability should be prioritized in investment portfolios. This alignment signals a firm’s commitment to sustainable development and provides greater assurance of long-term returns. Green investors, in particular, can use this framework to identify firms that balance carbon reduction with financial soundness, maximizing both environmental impact and financial performance.

Despite its contributions, this research has several limitations that should be acknowledged. First, the study focuses on firms listed on the LQ45 index of the Indonesian Stock Exchange, which may limit the generalizability of the findings to other contexts. The LQ45 index primarily consists of large, liquid firms that may have better access to resources for implementing carbon emission reduction and financial sustainability strategies. As such, the results may not be fully applicable to smaller firms or those operating in less developed markets. Future research should aim to include a broader range of firms, both in terms of size and sector, to validate and expand upon these findings.

Second, this study examines a relatively short time frame, from 2022 to 2024. While the findings provide valuable insights into the short-term impact of carbon emission reduction on firm value, they may not capture the long-term effects of such initiatives. Future research could benefit from longitudinal studies that track the long-term financial performance of firms engaging in carbon emission reduction over extended periods. This would provide a more comprehensive understanding of the sustainability benefits and financial implications of carbon reduction efforts.

Lastly, the study's reliance on Tobin's Q as a measure of firm value, while widely used, may not fully capture all dimensions of firm performance, particularly those related to non-financial metrics such as corporate reputation or stakeholder engagement. Future research could incorporate alternative measures of firm value, such as market capitalization or earnings per share, as well as qualitative assessments of firm reputation and stakeholder satisfaction to provide a more holistic view of the impacts of carbon emission reduction.

This research was supported by the Universitas Sebelas Maret through Fundamental Research Scheme (194.2/UN27.22/PT.01.03/2024).

[1] Larasati, R., Seralurin, Y.C., Sesa, P.V.S. (2020). Effect of profitability on carbon emission disclosure. The International Journal of Social Sciences World, 2: 182-195.

[2] Egbunike, F.C., Emudainohwo, O.B. (2017). The role of carbon accountant in corporate carbon management systems: A holistic approach. Indonesian Journal of Sustainability Accounting and Management, 1(2): 90. https://doi.org/10.28992/ijsam.v1i2.34

[3] Directorate General of Climate Change, Ministry of Environment and Forestry. (2021). Indonesia: Third biennial update report under the United Nations Framework Convention on Climate Change. Directorate General of Climate Change and Ministry of Environment and Forestry, Jakarta.

[4] Alsaifi, K., Elnahass, M., Salama, A. (2020). Carbon disclosure and financial performance: UK environmental policy. Business Strategy and the Environment, 29: 711-726. https://doi.org/10.1002/bse.2426

[5] Broadstock, D.C., Matousek, R., Meyer, M., Tzeremes, N.G. (2020). Does corporate social responsibility impact firms’ innovation capacity? The indirect link between environmental & social governance implementation and innovation performance. Journal of Business Research, 119: 99-110. https://doi.org/10.1016/j.jbusres.2019.07.014

[6] Baier, P., Berninger, M., Kiesel, F. (2020). Environmental, social and governance reporting in annual reports: A textual analysis. Financial Markets, Institutions & Instruments, 29(3): 93-118. https://doi.org/10.1111/fmii.12132

[7] Zhang, F., Qin, X., Liu, L. (2020). The interaction effect between ESG and green innovation and its impact on firm value from the perspective of information disclosure. Sustainability, 12(5): 1866. https://doi.org/10.3390/su12051866

[8] Alamillos, R.R., de Mariz, F. (2022). How can European regulation on ESG impact business globally? Journal of Risk and Financial Management, 15(7): 291. https://doi.org/10.3390/jrfm15070291

[9] Matsumura, E.M., Prakash, R., Vera-Muñoz, S.C. (2014). Firm-value effects of carbon emissions and carbon disclosures. The Accounting Review, 89(2): 695-724. https://doi.org/10.2308/accr-50629

[10] Griffin, P.A., Lont, D.H., Sun, E.Y. (2017). The relevance to investors of greenhouse gas emission disclosures. Contemporary Accounting Research, 34(2): 1265-1297. https://doi.org/10.1111/1911-3846.12298

[11] Cooper, S.A., Raman, K.K., Yin, J. (2018). Halo effect or fallen angel effect? Firm value consequences of greenhouse gas emissions and reputation for corporate social responsibility. Journal of Accounting and Public Policy, 37(3): 226-240. https://doi.org/10.1016/j.jaccpubpol.2018.04.003

[12] Ott, C., Schiemann, F. (2023). The market value of decomposed carbon emissions. Journal of Business Finance & Accounting, 50(1-2): 3-30. https://doi.org/10.1111/jbfa.12616

[13] Clarkson, P.M., Li, Y., Pinnuck, M., Richardson, G.D. (2015). The valuation relevance of greenhouse gas emissions under the European Union carbon emissions trading scheme. European Accounting Review, 24(3): 551-580. https://doi.org/10.1080/09638180.2014.927782

[14] Feng, Z.Y., Wang, M.L., Huang, H.W. (2015). Equity financing and social responsibility: Further international evidence. The International Journal of Accounting, 50(3): 247-280. https://doi.org/10.1016/j.intacc.2015.07.005

[15] Manchiraju, H., Rajgopal, S. (2017). Does corporate social responsibility (CSR) create shareholder value? Evidence from the Indian Companies Act 2013. Journal of Accounting Research, 55(5): 1257-1300. https://doi.org/10.1111/1475-679X.12174

[16] Kurnia, P., Darlis, E., Putra, A.A. (2020). Carbon emission disclosure, good corporate governance, financial performance, and firm value. The Journal of Asian Finance, Economics and Business, 7(12): 223-231. https://doi.org/10.13106/JAFEB.2020.VOL7.NO12.223

[17] Mahmudah, H., Yustina, A.I., Dewi, C.N., Sutopo, B. (2023). Voluntary disclosure and firm value: Evidence from Indonesia. Cogent Business & Management, 10(1): 2182625. https://doi.org/10.1080/23311975.2023.2182625

[18] Ramadhan, P., Rani, P., Wahyuni, E.S. (2023). Disclosure of carbon emissions, COVID-19, green innovations, financial performance, and firm value. Jurnal Akuntansi dan Keuangan, 25(1): 1-16. https://doi.org/10.9744/jak.25.1.1-16

[19] Zheng, S., Jin, S. (2023). Can companies reduce carbon emission intensity to enhance sustainability? Systems, 11(5): 249. https://doi.org/10.3390/systems11050249

[20] Gleißner, W., Günther, T., Walkshäusl, C. (2022). Financial sustainability: Measurement and empirical evidence. Journal of Business Economics, 92(3): 467-516. https://doi.org/10.1007/s11573-022-01081-0

[21] Odhiambo, S.P.O., Kobia, P.M. (2020). Solvency management and financial sustainability of supermarkets in Kenya. The International Journal of Business Management and Technology, 4(5): 226-234. https://doi.org/10.5281/zenodo.7668850

[22] Xie, Z., Liu, X., Najam, H., Fu, Q., Abbas, J., Comite, U., Cismas, L.M., Miculescu, A. (2022). Achieving financial sustainability through revenue diversification: A green pathway for financial institutions in Asia. Sustainability, 14(6): 3512. https://doi.org/10.3390/su14063512

[23] Remeňová, K., Kintler, J., Jankelová, N. (2020). The general concept of the revenue model for sustainability growth. Sustainability, 12(16): 6635. https://doi.org/10.3390/su12166635

[24] Almayyahi, A.R.A. (2023). The role of financial risks and financial sustainability in the Iraqi stock markets during COVID-19 pandemic. Journal of Asian Multicultural Research for Economy and Management Study, 3(3): 37-47. https://doi.org/10.47616/jamrems.v3i3.369

[25] Suhadak, Kurniaty, Handayani, S.R., Rahayu, S.M. (2019). Stock return and financial performance as moderation variable in influence of good corporate governance towards corporate value. Asian Journal of Accounting Research, 4(1): 18-34. https://doi.org/10.1108/ajar-07-2018-0021

[26] Spence, M. (1973). Job market signaling. The Quarterly Journal of Economics, 87(3): 355-374. https://doi.org/10.2307/1882010

[27] Lee, M.T., Raschke, R.L., Krishen, A.S. (2022). Signaling green! Firm ESG signals in an interconnected environment that promote brand valuation. Journal of Business Research, 138: 1-11. https://doi.org/10.1016/j.jbusres.2021.08.037

[28] Puspitaningtyas, Z. (2019). Empirical evidence of market reactions based on signaling theory in Indonesia Stock Exchange. Investment Management and Financial Innovations, 16(2): 66-77. https://doi.org/10.21511/imfi.16(2).2019.06

[29] Guest, D.E., Sanders, K., Rodrigues, R., Oliveira, T. (2021). Signalling theory as a framework for analysing human resource management processes and integrating human resource attribution theories: A conceptual analysis and empirical exploration. Human Resource Management Journal, 31(3): 796-818. https://doi.org/10.1111/1748-8583.12326

[30] Pernkopf, K., Latzke, M., Mayrhofer, W. (2021). Effects of mixed signals on employer attractiveness: A mixed-method study based on signalling and convention theory. Human Resource Management Journal, 31(2): 392-413. https://doi.org/10.1111/1748-8583.12313

[31] Kharouf, H., Lund, D.J., Krallman, A., Pullig, C. (2020). A signaling theory approach to relationship recovery. European Journal of Marketing, 54(9): 2139-2170. https://doi.org/10.1108/EJM-12-2018-0870

[32] Nogueira, E., Gomes, S., Lopes, J.M. (2023). Triple bottom line, sustainability, and economic development: What binds them together? A bibliometric approach. Sustainability, 15(8): 6706. https://doi.org/10.3390/su15086706

[33] Roy, K., Bandopadhyay, K. (2022). Financial risk and firm value: Is there any trade-off in the Indian context? Rajagiri Management Journal, 16(3): 226-238. https://doi.org/10.1108/RAMJ-03-2021-0021

[34] Yadav, I.S., Pahi, D., Gangakhedkar, R. (2022). The nexus between firm size, growth and profitability: New panel data evidence from Asia-Pacific markets. European Journal of Management and Business Economics, 31(1): 115-140. https://doi.org/10.1108/EJMBE-03-2021-0077

[35] Han, Y.G., Huang, H.W., Liu, W.P., Hsu, Y.L. (2023). Firm-value effects of carbon emissions and carbon disclosures: Evidence from Taiwan. Accounting Horizons, 37(3): 171-191. https://doi.org/10.2308/HORIZONS-2021-112

[36] Jiang, L., Zhang, Q., Wang, Y., Li, Z. (2022). Carbon emission risk and governance. International Journal of Disaster Risk Science, 13(2): 249-260. https://doi.org/10.1007/s13753-022-00411-8

[37] Rennert, K., Errickson, F., Prest, B.C., Rennels, L., Newell, R.G., Pizer, W., Kingdon, C., Wingenroth, J., Cooke, R., others. (2022). Comprehensive evidence implies a higher social cost of CO2. Nature, 610(7933): 687-692. https://doi.org/10.1038/s41586-022-05224-9

[38] Saha, A.K., Dunne, T., Dixon, R. (2021). Carbon disclosure, performance and the green reputation of higher educational institutions in the UK. Journal of Accounting & Organizational Change, 17(5): 604-632. https://doi.org/10.1108/JAOC-09-2020-0138

[39] Gillingham, K., Stock, J.H. (2018). The cost of reducing greenhouse gas emissions. Journal of Economic Perspectives, 32(4): 53-72. https://doi.org/10.1257/jep.32.4.53

[40] Fajar, M. (2018). Corporate social responsibility in Indonesia: Regulation and implementation issues. Journal of Legal, Ethical and Regulatory Issues, 21: 1-12.

[41] Safiullah, M., Houqe, M.N., Ali, M.J., Azam, M.S. (2023). Debt overhang and carbon emissions. International Journal of Managerial Finance. https://doi.org/10.1108/IJMF-06-2023-0305

[42] Magnanelli, B.S., Izzo, M.F. (2017). Corporate social performance and cost of debt: The relationship. Social Responsibility Journal, 13(2): 250-265. https://doi.org/10.1108/SRJ-06-2016-0103

[43] Oware, K.M., Mallikarjunappa, T., Praveena, A. (2023). Corporate social responsibility (CSR) expenditure and debt financing. Do the unspent CSR expenditure and firm age of public sector enterprises in India matter? Public Organization Review, 23(4): 1591-1610. https://doi.org/10.1007/s11115-023-00657-3

[44] Yang, Y., Xue, R., Yang, D. (2020). Does market segmentation necessarily discourage energy efficiency? Plos One, 15(5): e0233061. https://doi.org/10.1371/journal.pone.0233061

[45] Yao, L., Luo, R., Yi, X. (2024). A study of market segmentation, government competition, and public service efficiency in China: Based on a semi-parametric spatial lag model. PLOS ONE, 19(1): e0297446. https://doi.org/10.1371/journal.pone.0297446

[46] Ding, X., Li, J., Song, T., Ding, C., Tan, W. (2023). Does carbon emission of firms aggravate the risk of financial distress? Evidence from China. Finance Research Letters, 56: 104034. https://doi.org/10.1016/j.frl.2023.104034.

[47] Yoon, B., Chung, Y. (2018). The effects of corporate social responsibility on firm performance: A stakeholder approach. Journal of Hospitality and Tourism Management, 37: 89-96. https://doi.org/10.1016/j.jhtm.2018.09.001