Maruli Sitompul![]() | Arif Imam Suroso*

| Arif Imam Suroso*![]() | Ujang Sumarwan

| Ujang Sumarwan![]() | Nimmi Zulbainarni

| Nimmi Zulbainarni![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This research aims to examine how the integration of corporate carbon strategies can impact company performance, particularly in terms of sales growth and profitability. Through the analysis of sustainability reports and integrated reports from Indonesian Food and Beverage companies listed on the Indonesian Stock Exchange (IDX), the results reveal a positive correlation between the adoption of carbon management strategies and increases in both sales growth and profits. The findings suggest that implementing carbon management strategies to reduce corporate greenhouse gas emissions is linked to enhanced sales growth and profitability. This study can contribute to answering the question posed by researchers and the business community regarding whether it pays to be environmentally responsible within a company. Additionally, this research formulates a framework for carbon management practices and provides an overview of carbon strategy adoption in Indonesian Food and Beverage companies. Furthermore, it summarizes benchmarked practices from leading global companies in integrating their carbon management strategies into their core business operations. It is expected that this framework can assist practitioners and corporate managers in facilitating their company's transition to adopt net-zero emissions goal.

climate action, clean energy, corporate carbon management, net zero emissions, carbon reduction practices, corporate performance, carbon performance, sales growth, profitability, carbon strategies

Climate change presents an immediate and profound systemic challenge to the world, necessitating urgent action. It stands out as a prominent environmental concern for the global community. Study findings indicate that climate change is primarily driven by human activities, notably the burning of fossil fuels, unsustainable energy practices, changes in land use, and global consumption and production patterns [1]. These factors, in turn, have a significant impact on weather and climate extremes worldwide, leading to extensive detrimental effects on food and water security, human health, and society as a whole [1, 2].

A broad spectrum of stakeholders, including regulatory bodies, customers, and shareholders, anticipates that the private sector will take assertive measures to mitigate the risks associated with climate change [3, 4]. Furthermore, there is a growing demand from various stakeholder groups for companies to publicly disclose information regarding their business practices related to climate change [5, 6]. This information includes details on the companies' energy consumption, greenhouse gas (GHG) emissions, and their efforts to reduce GHG emissions throughout their value chain. Such information encompasses both direct emissions (Scope 1) and indirect emissions (Scope 2 and Scope 3) [7]. For most Food and Beverage (F&B) companies, Scope 3 emissions, which are indirect, constitute the most significant contributors to their total emissions [8]. Typically, these emissions originate from sourcing materials from farmers, suppliers, and distribution and logistics processes, both upstream and downstream [8].

As noted by Haque and Deegan [9], managers in corporations are increasingly acknowledging climate change and its related risks as one of the foremost business challenges they confront in the twenty-first century. However, not all companies have embraced the commitment and strategies required to embark on this climate change strategy [10]. Some companies remain slow to initiate this journey [9], particularly in developing countries where specific climate change regulations may still be absent [11]. Additionally, there is a perception from managers that a substantial investment is required to adopt carbon management strategies and can potentially erode companies' profits [12]. The business community may not yet understand the direct correlation between responsible business practices and their impact on business performance.

Okereke [10] identifies several key motivations driving companies to implement carbon management strategies. The primary and most significant motivation is aligning profits with carbon management. The second motivation is to gain credibility and leverage, enabling active participation in determining the direction of change. The third motivation is to anticipate future business risks resulting from climate change, such as safeguarding agriculture-related supply chains. The fourth motivation is the need for companies to fulfill internal fiduciary obligations and engage in ethical business practices.

Companies must align their carbon management strategies with their business model and product portfolio to seamlessly integrate all carbon reduction activities into their business operations [13]. This approach is exemplified by global companies like Nestlé and Danone, which promote regenerative agriculture practices. Being food and beverage (F&B) companies, they rely heavily on agricultural supply chains. Additionally, they introduce innovations in plant-based products to provide low-carbon alternatives to their existing dairy and meat-based products. These strategies effectively reduce their carbon footprint, particularly in their highest GHG emission source, known as Scope 3. It's important to note that other industry sectors, such as mining, technology, or automotive, may prioritize different strategies as their primary focus.

To date, there have been relatively few studies exploring the integration of carbon management strategies into corporate strategies within the F&B industry, the link between the adoption of these strategies and enhancing business performance, and the appropriate strategies that companies should initiate on the journey toward achieving net-zero emissions. The central question posed by both researchers and business practitioners is whether adopting and implementing carbon management strategies positively impacts a company's financial performance [14, 15]. This paper represents an analysis aimed at exploring and investigating this type of study. It is highly relevant to the current international business commitment to mitigate climate change and transition toward achieving net-zero emissions by 2050. Ultimately, this research is expected to provide valuable insights for researchers, managers, sustainability professionals, and policymakers, enriching their perspectives on recent practices and strategies related to corporate-level carbon management. Consequently, this study can guide managers in embarking on the journey toward achieving net-zero emissions, while policymakers can contribute to the development of relevant and impactful national policies aimed at accelerating efforts to reduce carbon emissions and achieve the Paris Agreement's target of limiting global temperature rise to 1.5 degrees Celsius by 2050 [16].

To outline the objectives of this research article, several key research questions have been formulated for investigation in this study, as follows:

RQ1: What carbon management practices are undertaken by corporations to facilitate the achievement of low-carbon business operations, as identified in the literature?

RQ2: What is the landscape of carbon management practices among F&B companies in Indonesia?

RQ3: What is the correlation between carbon performance and corporate performance, as evidenced by empirical data obtained from companies' sustainability reports?

RQ4: What benchmarks can be derived from world-leading F&B companies with notable carbon emissions strategies?

RQ5: What implementation strategies should companies adopt when embarking on a journey towards a net-zero target? The answer will be explored based on corporate empirical strategies and relevant existing literature, providing a robust guideline for industry peers looking to initiate similar initiatives.

The article's structure is as follows: It starts with the introduction and research questions, setting the study's context and objectives (Section 1). Then, the methodology is outlined (Section 3). Section 4 presents the findings with detailed explanations. Section 5 provides a comprehensive discussion addressing research questions. Finally, Section 6 concludes the research, suggests future research opportunities, and discusses the research limitations.

2.1 Carbon management strategies and financial performance

A carbon management strategy can be defined as a deliberate effort by a company to minimize the impact of all aspects of its business activities on climate change [17]. This strategy focuses on reducing carbon emissions stemming from all aspects of a company's supply chain, encompassing Scope 1, Scope 2, and Scope 3 emissions, as guided by the GHG Protocol [7]. Numerous global companies have made enduring commitments to reduce carbon emissions within their business operations, with the ultimate objective of achieving net-zero emissions by 2050 or even earlier. These commitments are in alignment with the goals established by the Paris Agreement in 2015.

The scope of carbon management strategy has evolved over time. It has moved beyond the sole focus on carbon reduction related to efficiency and process improvement within manufacturing and the supply chain [18]. Instead, it now encompasses carbon governance and carbon competitiveness [19].

Carbon governance includes the establishment of carbon policies, carbon accounting and inventory, leadership engagement, organizational involvement, and risk management. On the other hand, carbon competitiveness involves activities such as new market and product development, stakeholder engagement, corporate communication, and carbon disclosure [20]. Ultimately, these efforts contribute to improving a company's reputation [21], enhancing carbon performance [22], and yielding financial benefits [23]. Kolk and Pinkse [24] have observed that a company's environmental activities related to climate change mitigation directly enhance its competitive advantage.

Several studies have delved into the connection between carbon management strategies and their influence on financial performance [25-28]. Within the realm of research, an ongoing debate revolves around a fundamental question: Does the adoption of environmentally friendly practices make financial sense for businesses [15]? While researchers ardently argue for the moral imperative of embracing sustainability practices, practitioners and business managers are primarily concerned with understanding how their initiatives, such as implementing a carbon management strategy, can tangibly impact the growth and profitability of their businesses [23, 29, 30].

2.2 The relationship of carbon management strategies on sales growth

Recent trends reveal an increasing consumer preference for environmentally friendly or "green" products. Environmentally conscious consumers expect companies to demonstrate responsibility and commitment in addressing environmental concerns, particularly the urgent issue of climate change, and to contribute to its mitigation [3]. The adoption of carbon reduction strategies to lower GHG emissions represents a crucial commitment that many companies should consider nowadays [31]. These efforts should be effectively communicated to ensure that stakeholders and consumers comprehend and are informed about the actions taken by the companies that produce the products they consume to address global environmental issues.

Companies' commitment to mitigating environmental issues enhances their image and reputation [32], simultaneously fostering greater consumer loyalty to their brands, fosters consumer trust, and encourages repurchase intentions [33]. Previous research, as conducted by Lewandowski [27], involving 1640 international companies from 2003 to 2015, demonstrated a significant positive linear relationship between carbon emission mitigation and return on sales (ROS).

In a separate study by Chaudary et al. [33], focusing on UK FTSE 350 listed companies spanning from 2004 to 2018, the findings indicated a positive correlation between sales growth and carbon performance. This study suggests that companies with stronger carbon performance tend to attract environmentally conscious consumers, leading to increased sales growth [33].

Rokhmawati et al. [34] investigates publicly accessible financial reports and annual reports of 134 listed manufacturing firms in Indonesia Stock Exchange (IDX) in 2011 shows a result that reduction GHG emissions has a positive and significant effect on return on sales (ROS).

2.3 The relationship of carbon management strategies on profitability

Companies are currently emphasizing the promotion of various environmental actions as part of their efforts to minimize their impact. They do this by communicating their endeavors in their sustainability reports to the public. This environmental information holds significant importance for a wide range of stakeholders, including businesses, government agencies, employees, investors, the financial sector, and consumers, as it contributes to the advancement of community development [35].

Most companies' initiatives to reduce greenhouse gas (GHG) emissions primarily stem from operational enhancements within their facilities and throughout the value chain. These endeavors are typically associated with reducing energy consumption, enhancing manufacturing efficiency, optimizing supply chain logistics, and using low-carbon materials. Ultimately, these efforts result in more efficient operational costs, which, as indicated by Hoffman [23], have a positive impact on profitability.

Boiral et al.'s [36] study, which examined 319 Canadian manufacturing firms, revealed a noteworthy connection between the dedication to reduce GHG emissions and financial performance.

Gallego-Álvarez et al. [35] discovered a positive connection between emission reduction and financial performance using data from 89 international companies during 2006-2009. This suggests that companies with lower emissions tend to have better financial performance, incentivizing environmentally friendly practices. Their findings support and extend prior research indicating a positive impact of emission reduction on financial performance.

As per Okereke [10], the primary and seemingly the most significant driving force behind a company's carbon management programs is profitability. Nearly 100% of the FTSE companies he examined, which report their climate change initiatives on their websites, establish a connection between profit and carbon management. According to these companies, these efforts have led to substantial financial savings for the organization

To summarize the literature suggests that there is a link between a commitment to reducing emissions and financial performance, with companies that have lower emissions tending to have better financial performance. The motivation behind companies' carbon management programs is primarily driven by profitability, with many companies reporting substantial financial savings resulting from their efforts.

In conclusion, the literature suggests that adopting carbon management strategies can positively impact both financial performance and sales growth. These strategies not only contribute to mitigating climate change but also enhance a company's reputation, attract environmentally conscious consumers, and lead to financial benefits.

3.1 Research design

This research employs a content analysis approach to examine corporate carbon strategies outlined in corporate sustainability reports or integrated reports. These sources are essential for uncovering a company's environmental commitments and tracking the progression of corporate environmental performance indicators. In numerous studies related to disclosures, sustainability reports have frequently served as the primary source of data [37]. Content analysis is chosen as the research method in this study due to its suitability for systematically analyzing textual data, enabling the identification of trends, patterns, and key themes in sustainability disclosures [38].

3.2 Data collection

3.2.1 Data sources and sample selection

The two primary types of documents analyzed in this study were "literature reviews" and "sustainability reports". Firstly, the literature review was conducted to select research articles from Scopus database that had conducted empirical studies on carbon management strategies within corporations. This was done to identify common carbon strategies implemented by industries discussed in the research articles. Secondly, sustainability reports were obtained from the Indonesian Stock Exchange (IDX) website or companies' websites. The data collection followed specific criteria, including industry type, reporting year, and report availability. The sustainability reports considered were from the two most recent fiscal years (2021-2022) to analyze the companies' recent strategies. This data collection process took place from August 20th to 25th, 2023.

To do the process, the authors initially checked the list of F&B companies listed on the IDX. The authors then excluded agriculture companies from the list to focus specifically on F&B manufacturing companies. Finally, the authors checked the availability of their sustainability reports or integrated reports and excluded companies without such reports. Out of the 44 F&B companies listed on the IDX, only 27 companies met our criteria. The selection process is outlined in Table 1 below.

Table 1. Criteria for sample selection

|

Sample Collection Criteria |

Number of Samples |

|

Food and Beverage companies listed on IDX |

44 |

|

Exclusion of Agriculture Food Product Companies |

-8 |

|

Exclusion of F&B Companies without sustainability report or integrated report |

-9 |

|

Final Number of F&B Companies Samples with sustainability report or integrated report |

27 |

Note: data are compiled by the authors.

3.3 Procedure for data analysis

Content analysis is a systematic and objective technique used to identify and categorize communication themes or characteristics [39]. In this study, conceptual analysis was employed to identify coding criteria and quantify their presence in selected documents, following the coding protocol [40, 41]. The coding criteria were coded as "Yes" or "No" to indicate their presence or absence. For instance, one coding criterion focused on the presence of specific carbon-related practices. The coders will review the company's sustainability reports, searching for relevant terms or information related to the analyzed carbon practices, and assign a "Yes" code if they are present and a "No" code if they are absent. Each content of the sustainability reports will be thoroughly reviewed and analyzed using the coding criteria. This process will be carried out for all 27 documents of the company's sustainability reports to check the presence of the coding criteria.

In conducting the data analysis, two coders were trained to analyze the content of the company's sustainability reports using pre-set coding criteria. The purpose of the training was to familiarize the coders with the coding protocol and its implementation. To assess the effectiveness of the coding criteria, a pretest was conducted on a sample of sustainability reports from various companies. The selection of these reports was based on their content complexity and potential difficulties.

During the coding process, the coders assigned codes to indicate the presence of specific practices in the company's sustainability reports. The results of the coding were captured and saved in an Excel spreadsheet. They also engaged in discussions to address any issues or concerns that arose during the coding process. Subsequently, the coders reviewed any discrepancies that emerged from the initial coding and made efforts to resolve them. They sought guidance from the researchers to ensure consistency in their coding approach. Through this collaborative process, the coders reached a consensus on any discrepancies, ensuring that the analysis maintained a high level of consistency.

Codes criteria were created by drawing on carbon strategies and practices in industry identified from empirical research literature (Table 2). This coding process will answer the landscape of carbon practices in Indonesian F&B companies.

Table 2. Strategic objectives and related practices for corporate carbon strategies used for coding

|

Strategic Objectives |

Corporate Practices (Coding) |

References |

|

Carbon Governance |

Organization Involvement |

[31, 54] |

|

Carbon Target & Policy |

[23, 48, 54, 55] |

|

|

Carbon Accounting |

[14, 56] |

|

|

Climate Risk |

[57] |

|

|

Carbon Reduction |

Energy Efficiency in Operations |

[44, 58] |

|

Renewable Technology |

[4, 10, 27] |

|

|

Eco-design Product Innovation |

[10, 59] |

|

|

New markets and products |

[19, 54, 17] |

|

|

Low Carbon Labeling |

[14, 17] |

|

|

Carbon-Neutral |

[14, 17] |

|

|

Supplier & Customer Involvement |

[31] |

|

|

Carbon Removal |

Reforestation |

[4, 48, 60] |

|

Conservation |

[4, 60] |

|

|

Regenerative Agriculture |

[61, 62] |

|

|

Carbon Capture & Sequestration |

[45] |

|

|

Carbon Compensation |

Emission Trading |

[48, 49, 50, 63] |

|

Carbon Credit |

[50, 64] |

|

|

Carbon Competitiveness |

Sector and Stakeholder Corporation |

[31] |

|

Company Reporting and Disclosure |

[19, 48, 50, 52, 65] |

|

|

Corporate Communication |

[19, 50, 52] |

|

|

Carbon Legitimation |

Stakeholder Engagement |

[3, 19] |

|

Lobbying & Influencing Activities |

[49, 53, 66] |

Note: data are compiled by the authors.

Table 3. The criteria used to define qualitative results

|

Indicators |

Definitions |

If the Result in Y > Y-1 (Code) |

If the Result in Y < Y-1 (Code) |

Expected Result |

|

Carbon Intensity |

Absolute annual GHG emitted per Net Sales (tons/trillion IDR) of year Y and year Y-1 |

Increased |

Decreased |

The lower carbon intensity is preferred. |

|

Sales Growth |

Absolute Revenues of year Y and year Y-1 |

Increased |

Decreased |

The higher sales are preferred |

|

Profitability |

Absolute Profit of year Y and year Y-1 |

Increased |

Decreased |

The higher Profit is preferred |

Note: data are compiled by the authors.

The other process of analysis involves extracting and organizing numerical data related to GHG emissions, sales growth, and profitability from sustainability reports to analyze the correlation. The same procedure is applied, and the coding criteria are coded as "Increased" or "Decreased". This coding process will provide insights into the relationship between Carbon Intensity, Sales Growth, and Profitability in Indonesian F&B companies. The criteria used to define qualitative results can be found in Table 3.

The final analysis process involves summarizing qualitative data to identify noteworthy practices, challenges, and emerging trends in corporate carbon strategies. This data is gathered from company websites, sustainability databases, and online news media and other credible organization website related to climate change such as WRI and CDP. It is important to note that no coding criteria were provided for this descriptive analysis.

4.1 The mapping of carbon management strategies and practices in corporates

The study on several seminal research articles that conduct empirical studies on carbon management strategies within corporations or on an industry-wide level has provided the summary of corporate carbon management strategies that encompass six key strategic objectives: Carbon governance [19, 23, 42, 43]; Carbon reduction [18, 27, 44]; Carbon removal [45-47]; Carbon compensation [48-51]; Carbon competitiveness [19, 48, 52]; Carbon legitimation [3, 19, 53].

A comprehensive list of these practices, alongside the corresponding articles wherein they are discussed, can be found in Table 2.

4.2 The landscape of carbon management strategies and practices in Indonesian F&B companies

The corporate carbon practices listed in Table 2 are utilized to analyze and assess the current landscape of carbon practices adopted by 27 selected Indonesian F&B companies. Each practice, as detailed in their disclosure reports, is thoroughly reviewed, organized, and summarized for each of these companies. The resulting summary creates a comprehensive map of the carbon management strategies employed by the Indonesian F&B companies, providing an illustrative overview of the carbon management landscape in Indonesia. This mapped data is visualized in Figure 1.

Figure 1. Mapping of the latest carbon management practices among studied F&B companies in Indonesia

4.3 The relationship between carbon intensity, sales growth and profitability in Indonesian F&B companies

To structure these assessments, as defined by Busch et al. [67] and Sitompul et al. [68], this study adopted the indicators of Carbon Intensity to represent Carbon Performance and Sales Growth and Profitability to represent Corporate Performance. In conducting this analysis, information regarding carbon intensity, sales growth, and profitability was extracted from the sustainability reports of companies for the years 2021-2022 to compare the actual performances between those two consecutive years. The criteria in Table 3 were developed and applied to categorize the results of the indicators into qualitative outcomes: increases or decreases. This approach aims to establish a standardized basis for comparative analysis, mitigating the impact of variations in company size.

The criteria definitions provided in Table 3 are applied to convert the values of the performance indicators, namely Carbon Intensity, Profitability, and Sales, which are extracted from sustainability reports, into qualitative indicators for each observed company. The results of this analysis are compiled in Table 4 for reference.

4.3.1 Carbon Intensity and Sales Growth

From the results in Table 4, a positive correlation was identified between Carbon Intensity and Sales Growth, as illustrated in Figure 2. Out of the total 27 companies studied, 22 companies (81%) showed a positive correlation between carbon performance and sales growth. This shows that as GHG emissions decrease, sales growth increases. This finding suggests that improving carbon performance through the adoption of carbon reduction strategies can have a positive impact on sales growth.

Table 4. The result analysis of Carbon Intensity, Profitability and Sales Growth during the period 2021-2022

|

No. |

Companies Name |

Carbon Intensity |

Profitability |

Sales Growth |

|

1 |

ICBP |

Decreased |

Increased |

Increased |

|

2 |

MYOR |

Decreased |

Increased |

Increased |

|

3 |

INDF |

Decreased |

Increased |

Increased |

|

4 |

CMRY |

Decreased |

Increased |

Increased |

|

5 |

MLBI |

Decreased |

Increased |

Increased |

|

6 |

ULTJ |

Decreased |

Increased |

Increased |

|

7 |

ROTI |

Decreased |

Increased |

Increased |

|

8 |

CEKA |

Decreased |

Increased |

Increased |

|

9 |

CLEO |

Increased |

Increased |

Increased |

|

10 |

ADES |

Increased |

Increased |

Increased |

|

11 |

IBOS |

Decreased |

Increased |

Increased |

|

12 |

CAMP |

Decreased |

Increased |

Increased |

|

13 |

KEJU |

Increased |

Decreased |

Increased |

|

14 |

TRGU |

Decreased |

Increased |

Increased |

|

15 |

SKLT |

Decreased |

Decreased |

Increased |

|

16 |

WINE |

Decreased |

Increased |

Increased |

|

17 |

BUDI |

Decreased |

Increased |

Increased |

|

18 |

HOKI |

Increased |

Decreased |

Decreased |

|

19 |

PMMP |

Decreased |

Decreased |

Increased |

|

20 |

SKBM |

Increased |

Increased |

Decreased |

|

21 |

AISA |

Decreased |

Decreased |

Increased |

|

22 |

GULA |

Increased |

Decreased |

Decreased |

|

23 |

TAYS |

Decreased |

Increased |

Increased |

|

24 |

PSDN |

Increased |

Decreased |

Decreased |

|

25 |

NAYZ |

Increased |

Increased |

Increased |

|

26 |

FOOD |

Decreased |

Decreased |

Decreased |

|

27 |

NASI |

Decreased |

Increased |

Increased |

Note: data are compiled by the authors.

Figure 2. The correlation between Carbon Intensity and Sales Growth in the period of 2021 – 2022

The initiative to reduce GHG emissions and communicate these environmental efforts can significantly influence consumers' perceptions, especially in the fast-moving consumer goods sector, where products and brands have a direct connection with consumers. Consumers are familiar with these brands; therefore, any positive actions taken by these brands that align with consumer expectations can enhance brand integrity, image, and reputation. This, in turn, fosters loyalty among existing consumers, builds consumer trust, and encourages repeat purchases [33]. Furthermore, these efforts can also attract new consumers, especially those with environmentally conscious inclinations [69].

4.3.2 Carbon intensity and profitability

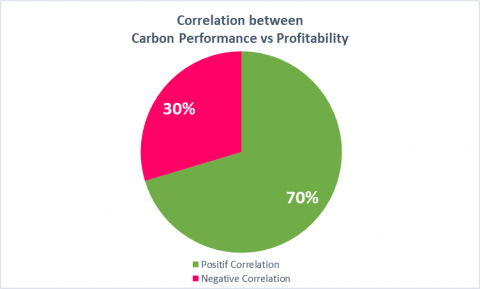

When evaluating the relationship between carbon intensity and profitability among the companies listed in Table 4, it was observed that out of the 27 companies studied, 19 companies (70%) displayed a positive correlation between Carbon Intensity and Profitability. This finding implies that as GHG emissions decrease, profits tend to increase, and conversely, when GHG emissions increase, profits tend to decrease. The majority of the studied companies that consistently work to reduce their GHG emissions tend to experience improved profitability. This relationship is illustrated in Figure 3.

Figure 3. The correlation between Carbon Intensity and Profitability in the period of 2021 - 2022

Hoffman [23] conducted a study that specifically examined the implementation of GHG emissions reduction initiatives by multinational companies. He found that these initiatives not only led to reductions in GHG emissions but also resulted in significant cost savings for the companies involved. The core of their efforts focused on reducing energy consumption, optimizing supply-chain logistics, developing more efficient manufacturing processes, utilizing greener materials and processes, and implementing energy efficiency programs.

These focused efforts on efficiency and conservation offer dual benefits. In addition to their contribution to reducing GHG emissions, they provide substantial cost-saving advantages to the company. This efficiency results in reduced operational costs, subsequently exerting a significant positive impact on the company's overall profitability [68].

4.4 The benchmark on how leading global F&B companies integrate carbon management strategies in their corporate strategy

To benchmark the best carbon strategies among F&B companies, this study uses specific criteria to identify ideal reference companies. These companies must demonstrate leadership in sustainability or Environmental, Social, and Governance (ESG) commitments compared to their peers, as assessed by global ESG index raters such as MSCI ESG Rating. Additionally, they should voluntarily disclose their climate practices to a credible global climate database like CDP. Furthermore, these companies must demonstrate that their carbon reduction targets are calculated according to science-based targets and approved by the SBTi (Science-based Target Initiative) standard.

Table 5 outlines the criteria applied to select three global F&B companies. The information is sourced from MSCI ESG Rating (www.msci.com, accessed on September 10, 2023) for ESG commitment ratings and the companies' climate change reports submitted to CDP. Companies categorized as LEADERS (rated AA to AAA) that submitted climate change disclosure reports to CDP between 2021 and 2022 are considered. Based on these criteria, Nestlé, Danone, and Coca-Cola Europacific Partners PLC are identified as exhibiting the highest standards of carbon strategy implementation.

The three selected companies have subsidiaries operating in Indonesia and are categorized as multinational companies. Although they are not publicly listed in Indonesia, the study of these three companies—Nestlé, Danone, and Coca-Cola European Partners (CCEP)—involved a comprehensive analysis of their corporate websites (www.nestle.com; www.danone.com; www.cocacolaep.com accessed on October 16, 2023), national online media channels, and their global sustainability reports. The findings reveal several key observations:

Table 5. The summary of the selection criteria used to choose the referenced companies as the best benchmarks for implementing carbon strategies

|

Company Names |

MSCI ESG Ratings |

Having the Decarbonization Target |

GHG Reduction Target is Approved by SBTi Standard? |

Net Zero Carbon Target Year |

% of Company Footprint Covered by the Target |

Projected Reduction per Year to Meet Stated Target |

Climate Change Report Submitted to CDP (2021-2022) |

|

Nestlé SA |

Leader |

Yes |

Yes |

2050 |

100% |

-3.57% p.a. |

Yes |

|

Danone SA |

Leader |

Yes |

Yes |

2050 |

100% |

-3.45% p.a. |

Yes |

|

Coca-cola Europacific Partners PLC |

Leader |

Yes |

Yes |

2030 |

100% |

-11.23% p.a. |

Yes |

Note: data are compiled by the authors.

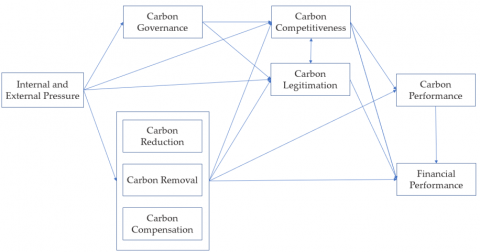

5.1 Framework of carbon management strategies in corporations

The review of empirical research articles has identified six interconnected strategic objectives within corporate carbon management strategies: carbon governance, carbon reduction, carbon removal, carbon compensation, carbon competitiveness, and carbon legitimation.

Carbon governance encompasses the initial steps and direction a company takes when embarking on its carbon reduction journey. This action entails setting company policies, defining a low-carbon roadmap, establishing priorities, and providing the necessary resources and change agents to facilitate the deployment of actions and priorities.

The action roadmap created within carbon governance is implemented through various carbon reduction strategies, including internal value chain carbon reduction and extending beyond the value chain with carbon removal and carbon compensation. These strategic approaches offer key benefits in terms of carbon competitiveness. These benefits include economic viability and cost savings resulting from the adoption of energy-efficient technologies and practices, waste reduction, and operational efficiency improvements. Carbon competitiveness also involves meeting consumer expectations and accessing markets where sustainability is a compelling selling point. Companies that align with environmental principles often gain increased access to capital and reduced financial risk from investors. Ultimately, compliance with government regulations and emission reduction targets helps mitigate the risk of penalties and ensures the sustainability of operating licenses.

Figure 4. Framework of carbon management strategies in corporations

Companies that assume responsibility for their carbon emissions and commit to reducing their environmental impact are perceived as more legitimate. This commitment encompasses the establishment and achievement of emissions reduction targets, along with regular progress reporting through sustainability reports and carbon emissions disclosures. These efforts are integral to carbon legitimacy, which can, in turn, enhance carbon competitiveness and vice versa.

The six strategic carbon objectives can be developed as interconnected carbon variables. This study develops a framework of carbon management strategies that consolidate all the variables. The elements of these variables are depicted in Figure 4.

5.2 Benchmarked practices and implementation framework

5.2.1 Benchmarked practices for future adoption for Indonesia companies.

Taking the summary in Table 5, the global F&B companies (Nestlé, Danone, and Coca-Cola) demonstrate a strong commitment to integrating carbon management strategies into their business operations. Being Fast-Moving Consumer Goods (FMCG) companies with a global consumer base, they recognize that adopting carbon management strategies is crucial for gaining a competitive advantage [50]. This adoption leads to several benefits, including enhancing their corporate reputation [85], strengthening their brand trust [86], motivating employees [87], improving operational efficiency [15], and fostering consumer loyalty [88].

Some benchmark practices highlighted from our review of sustainability reports and publicly available company information include:

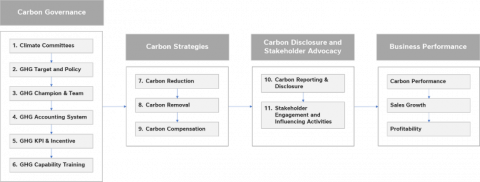

5.2.2 Implementation framework of carbon management strategies

The research investigates best practices adopted by global companies that have successfully integrated corporate carbon management strategies into their core business operations. The study develops a framework for implementing carbon management strategies, providing step-by-step strategies linked to the goal of enhancing business performance. Based on the corporate carbon management strategies of companies that have successfully integrated them into their business operations, the framework aims to guide other organizations considering a similar approach, as illustrated in Figure 5.

Figure 5. Framework for implementing carbon management strategies in corporations

This research demonstrates a significant association between Carbon Performance and Business Performance (Sales growth and Profit). Most of the studied companies show that implementing carbon emissions reduction initiatives, which reduce the company's GHG emissions, positively impacts profitability and sales growth. This provides further evidence for the questions posed by researchers and practitioners about the financial benefits of environmentally friendly practices for corporations.

The contribution of this study can be categorized into two aspects: theoretical and managerial. In terms of theoretical contributions, this research presents a framework for carbon management strategies, encompassing six strategic objectives or carbon variables and 22 strategic practices in carbon management. This strategic framework enhances theoretical understanding of the factors and variables involved in carbon management strategies within a corporate context. Another theoretical contribution is identifying a positive association between carbon performance and business performance (sales growth and profitability). In terms of managerial contributions, this research provides an overview of the carbon management strategy landscape in Indonesia. It benchmarks the best practices of carbon management strategies employed by leading F&B companies. Furthermore, it offers a framework for implementing carbon management strategies into core business operations, which can assist practitioners or business managers.

The study reveals that many F&B companies in Indonesia are currently operating at a compliance level concerning their initiatives to achieve net-zero emissions. Their efforts for emission mitigation primarily focus on improving operational efficiency and saving energy within their owned facilities (Scope 1 emissions). However, there is a lack of visible efforts to address Scope 3 emissions, which are the most significant contributors to emissions for most F&B companies. Furthermore, these companies have not declared ambitious targets with fixed timelines, especially targets approved by SBTi (Science-based Target Initiative), which would ensure that their efforts align with the goals of the Paris Agreement to limit global temperature rise to no more than 1.5 degrees Celsius.

This research has a limitation that could impact its outcomes. The study's sample is limited to listed F&B companies, which may only partially represent the practices of F&B companies in Indonesia. There are other significant companies in Indonesia, including some multinational ones, that have a substantial impact on carbon management strategies but are not listed on the IDX (Indonesia Stock Exchange). Therefore, they cannot be represented in the results of this research. For future research, it is essential to include more companies, both locally based and multinational, outside the listed ones that demonstrate commitment to adopting carbon emission reduction practices.

Additionally, this research relied on secondary data obtained from sustainability reports or integrated reports. For future research, it is necessary to gather information from primary data sources, such as interviews with company practitioners or the use of questionnaires. This approach would provide up-to-date information on companies' efforts and strategies to reduce their GHG emissions and their journey toward achieving net-zero emissions.

Another potential area for future research is to examine the impact of ESG Committees on company leadership and the integration of carbon targets into the company's incentive system to enhance Carbon Performance and Business Performance in F&B companies in Indonesia. ESG Committees at the leadership level are believed to strongly drive improvements in Carbon Performance and Business Performance. The integration of incentives related to carbon emission reduction targets has a significant influence on organizations' commitment to achieving their carbon emission reduction goals.

Furthermore, this article can serve as a reference for corporate practitioners to develop their carbon reduction strategies and guide them on a similar journey toward achieving net-zero operations.

[1] IPCC (Intergovernmental Panel on Climate Change). (2023). Sections. Climate Change 2023: Synthesis Report. Contribution of Working Groups I, II, and III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. http://doi.org/10.59327/IPCC/AR69789291691647

[2] Thomas, K., Hardy, D., Lazrus, H., Mendez, M., Orlove, B., Rivera-Collazo, I., Roberts, T., Rockman, M., Warner, B.P., Winthrop, R. (2018). Explaining differential vulnerability to climate change: A social science review. Wiley Interdisciplinary Reviews: Climate Change, 10(2): e565. https://doi.org/10.1002/wcc.565

[3] Buysse, K., Verbeke, A. (2003). Proactive environmental strategies: A stakeholder management perspective. Strategic Management Journal, 24(5): 453-470. https://doi.org/10.1002/smj.299

[4] Hoffman, A.J., Glancy, D. (2006). Getting ahead of the curve: Corporate strategies that address climate change, Arlington, VA: Pew Center on Global Climate Change, pp. 21-51. https://www.pewtrusts.org/~/media/legacy/uploadedfiles/wwwpewtrustsorg/reports/global_warming/pewclimatecorpstrategies1006pdf.pdf.

[5] Haque, S., Deegan, C., Inglis, R. (2016). Demand for, and impediments to, the disclosure of information about climate change-related corporate governance practices. Accounting and Business Research, 46(6): 620-664. http:// doi.org/10.1080/00014788.2015.1133276

[6] Dhanda, K.K., Malik, M. (2020). Carbon management strategy and carbon disclosures: An exploratory study. Business and Society Review 125(2): 225-239. https://doi.org/10.1111/basr.12207

[7] Wbcsd, W.R.I. (2004). The greenhouse gas protocol. A corporate accounting and reporting standard, Rev. ed. Washington, DC, Conches-Geneva.

[8] Schulman, D.J., Bateman, A.H., Greene, S. (2021). Supply chains (Scope 3) toward sustainable food systems: An analysis of food & beverage processing corporate greenhouse gas emissions disclosure. Cleaner Production Letters, 1: 100002. https://doi.org/10.1016/j.clpl.2021.100002

[9] Haque, S., Deegan, C. (2010). Corporate climate change-related governance practices and related disclosures: Evidence from Australia. Australian Accounting Review, 20(4): 317-333. https://doi.org/10.1111/j.1835-2561.2010.00107.x

[10] Okereke, C. (2007). An exploration of motivations, drivers and barriers to carbon management: The UK FTSE 100. European Management Journal, 25(6): 475-486. https://doi.org/10.1016/j.emj.2007.08.002

[11] Studer, S., Welford, R., Hills, P. (2006). Engaging Hong Kong businesses in environmental change: drivers and barriers. Business Strategy and the Environment, 15(6): 416-431. https://doi.org/10.1002/bse.516

[12] Slawinski, N., Pinkse, J., Busch, T., Banerjee, S.B. (2017). The role of short-termism and uncertainty avoidance in organizational inaction on climate change: A multi-level framework. Business & Society, 56(2): 253-282. https://doi.org/10.1177/0007650315576136

[13] DiBella, J. (2020). The spatial representation of business models for climate adaptation: An approach for business model innovation and adaptation strategies in the private sector. Business Strategy & Development, 3(2): 245-260. https://doi.org/10.1002/bsd2.92

[14] Orsato, R.J. (2006). Competitive environmental strategies: When does it pay to be green? California Management Review, 48(2): 127-143. https://doi.org/10.2307/41166341

[15] Ambec, S., Lanoie, P. (2008). Does it pay to be green? A systematic overview. Academy of Management Perspectives 22: 45–62. https://doi.org/10.5465/amp.2008.35590353

[16] UNFCCC (United Nations Framework Convention for Climate Change). (2015). Paris Agreement. United Nations Framework Convention for Climate Change. Available online: https://unfccc.int/sites/default/files/english_paris_agreement.pdf.

[17] Busch, T., Schwarzkopf, J. (2013). Carbon management strategies–A quest for corporate competitiveness. Progress in Industrial Ecology, an International Journal, 8(1-2): 4-29. https://doi.org/10.1504/PIE.2013.055053

[18] Böttcher, C.F., Müller, M. (2015). Drivers, practices, and outcomes of low-carbon operations: Approaches of German automotive suppliers to cutting carbon emissions. Business Strategy and the Environment, 24(6): 477-498. https://doi.org/10.1002/bse.1832.

[19] Damert, M., Paul, A., Baumgartner, R.J. (2017). Exploring the determinants and long-term performance outcomes of corporate carbon strategies. Journal of Cleaner Production 160: 123-138. http://doi.org/10.1016/j.jclepro.2017.03.206

[20] Dangelico, R.M., Pujari, D., Pontrandolfo, P. (2017). Green product innovation in manufacturing firms: A sustainability-oriented dynamic capability perspective. Business strategy and the Environment, 26(4): 490-506. https://doi.org/10.1002/bse.1932

[21] Kumar, A. (2018). Environmental reputation: Attribution from distinct environmental strategies. Corporate Reputation Review, 21(3): 115-126. https://doi.org/10.1057/s41299-018-0047-6

[22] Hoffmann, V.H., Busch, T. (2008). Corporate carbon performance indicators: Carbon intensity, dependency, exposure, and risk. Journal of Industrial Ecology, 12(4): 505-520. https://doi.org/10.1111/j.1530-9290.2008.00066.x

[23] Hoffman, A.J. (2005). Climate change strategy: The business logic behind voluntary greenhouse gas reductions. California Management Review, 47(3): 21-46. https://doi.org/10.2307%2F41166305

[24] Kolk, A., Pinkse, J. (2004). Market strategies for climate change. European Management Journal, 22(3): 304-314. https://doi.org/10.1016/j.emj.2004.04.011

[25] Busch, T., Hoffmann, V.H. (2011). How hot is your bottom line? Linking carbon and financial performance. Business & Society, 50(2): 233-265. https://doi.org/10.1177/0007650311398780

[26] Wang, L., Li, S., Gao, S. (2014). Do greenhouse gas emissions affect financial performance? An empirical examination of Australian public firms. Business Strategy and the Environment, 23(8): 505-519. https://doi.org/10.1002/bse.1790

[27] Lewandowski, S. (2017). Corporate carbon and financial performance: The role of emission reductions. Business Strategy and the Environment, 26(8): 1196-1211. https://doi.org/10.1002/bse.1978

[28] Naranjo Tuesta, Y., Crespo Soler, C., Ripoll Feliu, V. (2021). Carbon management accounting and financial performance: Evidence from the European Union emission trading system. Business Strategy and the Environment, 30(2): 1270-1282. https://doi.org/10.1002/bse.1790

[29] Bansal, P., Hoffman, A.J. (Eds.). (2012). The Oxford Handbook of Business and the Natural Environment. Oxford University Press, USA.

[30] Ganda, F. (2018). The effect of carbon performance on corporate financial performance in a growing economy. Social Responsibility Journal, 14(4): 895-916. https://doi.org/10.1108/SRJ-12-2016-0212

[31] Damert, M., Baumgartner, R.J. (2018). Intra-sectoral differences in climate change strategies: Evidence from the global automotive industry. Business Strategy and the Environment, 27(3): 265-281. https://doi.org/10.1002/bse.1968

[32] Gangi, F., Daniele, L.M., Varrone, N. (2020). How do corporate environmental policy and corporate reputation affect risk-adjusted financial performance? Business Strategy and the Environment, 29(5): 1975-1991. https://doi.org/10.1002/bse.2482

[33] Chaudary, S., Zahid, Z., Shahid, S., Khan, S.N., Azar, S. (2016). Customer perception of CSR initiatives: Its antecedents and consequences. Social Responsibility Journal, 12(2): 263-279. https://doi.org/10.1108/SRJ-04-2015-0056

[34] Rokhmawati, A., Gunardi, A., Rossi, M. (2017). How powerful is your customers' reaction to carbon performance? Linking carbon and firm financial performance. International Journal of Energy Economics and Policy, 7(6): 85-95. https://econjournals.com/index.php/ijeep/article/view/5752.

[35] Gallego-Álvarez, I., Segura, L., Martínez-Ferrero, J. (2015). Carbon emission reduction: The impact on the financial and operational performance of international companies. Journal of Cleaner Production, 103: 149-159. https://doi.org/10.1016/j.jclepro.2014.08.047

[36] Boiral, O., Henri, J.F., Talbot, D. (2012). Modeling the impacts of corporate commitment on climate change. Business Strategy and the Environment, 21(8): 495-516. https://doi.org/10.1002/bse.723

[37] Dragomir, V.D. (2012). The disclosure of industrial greenhouse gas emissions: A critical assessment of corporate sustainability reports. Journal of Cleaner Production, 29: 222-237. http://dx.doi.org/10.1016/j.jclepro.2012.01.024

[38] Duriau, V.J., Reger, R.K., Pfarrer, M.D. (2007). A content analysis of the content analysis literature in organization studies: Research themes, data sources, and methodological refinements. Organizational Research Methods 10(1): 5-34. https://doi.org/10.1177/1094428106289252

[39] Weber, R.P. (1985), Basic Content Analysis, Sage, Newbury Park, CA.

[40] Stemler, S. (2001). An overview of content analysis: Practical assessment. Research & Evaluation. A Peer Reviewed Electronic Journal. Yale University. http://www.qualitative-research.net/index.php/fqs/article/view/75/153.

[41] Forman, J., Damschroder, L. (2007). Qualitative content analysis. In Empirical methods for bioethics: A primer, Emerald Group Publishing Limited, pp. 39-62. http://doi.org/10.1016/S1479-3709(07)11003-7

[42] Elsayih J., Datt R., Tang Q. (2021). Corporate governance and carbon emissions performance: Empirical evidence from Australia, Australasian Journal of Environmental Management 28(4): 433-459. https://doi.org/10.1080/14486563.2021.1989066

[43] Tang, Q., Luo, L. (2014). Carbon management systems and carbon mitigation. Australian Accounting Review 24(1): 84-98. https://doi.org/10.1111/auar.12010.

[44] Pinkse, J., Busch, T. (2013). The emergence of corporate carbon norms: Strategic directions and managerial implications. Thunderbird International Business Review 55: 633-645. https://doi.org/10.1002/tie.21580.

[45] Bowen, F. (2011). Carbon capture and storage as a corporate technology strategy challenge. Energy Policy, 39(5): 2256-2264. https://doi.org/10.1016/j.enpol.2011.01.016

[46] Coffman, D.M., Lockley, A. (2017). Carbon dioxide removal and the futures market. Environmental Research Letters, 12(1): 015003. https://doi.org/10.1088/1748-9326/aa54e8

[47] Markusson, N. (2022). Natural carbon removal as technology. Wiley Interdisciplinary Reviews: Climate Change, 13(2): e767. https://doi.org/10.1002/wcc.767

[48] Jeswani, H.K., Wehrmeyer, W., Mulugetta. Y. (2008). How warm is the corporate response to climate change? Evidence from Pakistan and the UK. Business Strategy and the Environment, 17(1): 46-60. https://doi.org/10.1002/bse.569

[49] Kolk, A., Pinkse, J. (2005). Business responses to climate change: Identifying emergent strategies. California Management Review, 47(3): 6-20. https://doi.org/10.2307/41166304

[50] Schultz, K., Williamson, P. (2005). Gaining competitive advantage in a carbon-constrained world: Strategies for European business. European Management Journal, 23(4): 383-391. https://doi.org/10.1016/j.emj.2005.06.010

[51] Trouwloon, D., Streck, C., Chagas, T., Martinus, G. (2023). Understanding the use of carbon credits by companies: A review of the defining elements of corporate climate claims. Global Challenges, 7(4): 2200158. https://doi.org/10.1002/gch2.202200158

[52] Thaker, J. (2020). Corporate communication about climate science: A comparative analysis of top corporations in New Zealand, Australia, and Global Fortune 500. Journal of Communication Management, 24(3): 245-264. https://doi.org/10.1108/JCOM-06-2019-0092

[53] Hrasky, S. (2011). Carbon footprints and legitimation strategies: Symbolism or action? Accounting, Auditing & Accountability Journal, 25(1): 174-198. http://dx.doi.org/10.1108/09513571211191798

[54] Lee, S.Y. (2012). Corporate carbon strategies in responding to climate change. Business Strategy and the Environment, 21(1): 33-48. https://doi.org/10.1002/bse.711

[55] Galán-Valdivieso, F., Saraite-Sariene, L., Alonso-Cañadas, J., Caba-Pérez, M.D.C. (2019). Do corporate carbon policies enhance legitimacy? A social media perspective. Sustainability, 11(4): 1161. https://doi.org/10.3390/su11041161

[56] Gibassier, D., Schaltegger, S. (2015). Carbon management accounting and reporting in practice: A case study on converging emergent approaches. Sustainability Accounting, Management and Policy Journal, 6(3): 340-365. https://doi.org/10.1108/SAMPJ-02-2015-0014

[57] Weinhofer, G., Busch, T. (2013). Corporate strategies for managing climate risks. Business Strategy and the Environment, 22(2): 121-144. https://doi.org/10.1002/bse.1744

[58] Doda, B., Gennaioli, C., Gouldson, A., Grover, D., Sullivan, R. (2016). Are corporate carbon management practices reducing corporate carbon emissions? Corporate Social Responsibility and Environmental Management, 23(5): 257-270. https://doi.org/10.1002/csr.1369

[59] García-Sánchez, I.M., Gallego-Álvarez, I., José-Luis Zafra-Gómez, J.L. (2021). Do independent, female and specialist directors promote eco-innovation and eco-design in agri-food firms? Business Strategy and the Environment 30(2): 1136-1152. https://doi.org/10.1002/bse.2676

[60] Boiral, O. (2006). Global warming: Should companies adopt a proactive strategy? Long Range Planning, 39(3): 315-330. https://doi.org/10.1016/j.lrp.2006.07.002

[61] Khangura, R., Ferris, D., Wagg, C., Bowyer, J. (2023). Regenerative agriculture-A literature review on the practices and mechanisms used to improve soil health. Sustainability, 15(3): 2338. https://doi.org/10.3390/su15032338

[62] Schattman, R.E., Rowland, D.L., Kelemen, S.C. (2023). Sustainable and regenerative agriculture: Tools to address food insecurity and climate change. Journal of Soil and Water Conservation, 78(2): 33A-38A. https://doi.org/10.2489/jswc.2023.1202A

[63] Kolk, A., Mulder, G. (2011). Regulatory uncertainty and opportunity seeking: The case of clean development. California Management Review, 54(1): 88-106. https://doi.org/10.1525/cmr.2011.54.1.88

[64] Butler, R.A., Laurance, W.F. (2008). New strategies for conserving tropical forests. Trends in Ecology & Evolution, 23(9): 469-472. https://doi.org/10.1016/j.tree.2008.05.006

[65] Qian, W., Schaltegger, S. (2017). Revisiting carbon disclosure and performance: Legitimacy and management views. The British Accounting Review, 49(4): 365-379. https://doi.org/10.1016/j.bar.2017.05.005

[66] Engau, C., Hoffmann, V.H. (2009). Effects of regulatory uncertainty on corporate strategy-An analysis of firms’ responses to uncertainty about post-Kyoto policy. Environmental Science & Policy, 12(7): 766-777. https://doi.org/10.1016/j.envsci.2009.08.003

[67] Busch, T., Bassen, A., Lewandowski, S., Sump, F. (2022). Corporate carbon and financial performance revisited. Organization & Environment, 35(1): 154-171. https://doi.org/10.1177/1086026620935638

[68] Sitompul, M., Suroso, A.I., Sumarwan, U., Zulbainarni, N. (2023). Revisiting the impact of corporate carbon management strategies on corporate financial performance: A systematic literature review. Economies, 11(6): 171. https://doi.org/10.3390/economies11060171

[69] Shrum, L.J., McCarty, J.A., Lowrey, T.M. (1995). Buyer characteristics of the green consumer and their implications for advertising strategy. Journal of Advertising, 24(2): 71-82. https://doi.org/10.1080/00913367.1995.10673477

[70] Coca-cola EP Integrated Report. (2022). Coca-Cola EP 2022. https://www.cocacolaep.com/assets/IR-Documents/2022/2022-CCEP-Integrated-Report-and-Form-20-F.pdf.

[71] Nestlé Creating Shared Value and Sustainability Report. (2022). https://www.nestle.com/sites/default/files/2023-03/creating-shared-value-sustainability-report-2022-en.pdf.

[72] Danone Integrated Annual Report. (2022). Danone Sustainability Performance. https://www.danone.com/content/dam/corp/global/danonecom/rai/2022/danone-integrated-annual-report-2022.pdf.

[73] Coca-Cola Business and Sustainability Report. (2022). Refresh the world. Make a difference. https://www.coca-colacompany.com/content/dam/company/us/en/reports/coca-cola-business-sustainability-report-2022.pdf.

[74] Danone Climate Policy. (2023). Target Zero Net Carbon. Through Solutions Co-created with Danone’s Ecosystem. https://www.danone.com/content/dam/corp/global/danonecom/about-us-impact/policies-and-commitments/en/2016/2016_05_18_ClimatePolicyFullVersion.pdf.

[75] Nestlé’s Net Zero Roadmap 2050: Accelerate, Transform, Regenerate. (2023). https://www.nestle.com/sites/default/files/2020-12/nestle-net-zero-roadmap-en.pdf.

[76] Coca-Cola Sustainability Group Data. (2022). https://www.cocacolaep.com/assets/Sustainability/Documents/2022/2022-Sustainability-Group-data.pdf.

[77] Nestlé’s Climate Risk and Impact Report. (2022). https://www.nestle.com/sites/default/files/2023-03/2022-tcfd-report.pdf.

[78] Danone’s Exhaustive 2022 Environmental Data. (2023). https://www.danone.com/content/dam/corp/global/danonecom/investors/en-sustainability/reports-and-data/cross-topic/2023/danoneenvironmental2022extrafinancialdata.pdf.

[79] Nestlé Towards a Forest Positive Future. (2021). https://www.nestle.com/sites/default/files/2021-06/nestle-towards-forest-positive-future-report.pdf.

[80] Danone’s Forest Annual Update. (2022). https://www.danone.com/content/dam/corp/global/danonecom/about-us-impact/policies-and-commitments/en/2023/danone-forest-annual-update-2022.pdf.

[81] Coca-Cola’s Our Approach to Biodiversity and Forest Stewardship. (2022). https://www.cocacolaep.com/assets/Sustainability/Documents/2021/Our-approach-to-biodiversity-and-forest-stewardship-2022.pdf.

[82] CDP Nestlé Climate Change. (2022). https://www.nestle.com/sites/default/files/2022-12/cdp-nestle-answers-climate-change-2022.pdf.

[83] Brittlebank, William. (2016). Coca-Cola, Starbucks joined the Beijing emissions trading system. ClimateAction. https://www.climateaction.org/news/coca_cola_starbucks_join_beijing_emissions_trading_system.

[84] Danone Annual Integrated Report. (2021). Methodology Note. https://www.danone.com/content/dam/corp/global/danonecom/investors/en-sustainability/reports-and-data/cross-topic/methodologynote2021.pdf.

[85] Hasseldine, J., Salama, A.I., Toms, J.S. (2005). Quantity versus quality: The impact of environmental disclosures on the reputations of UK Plcs. The British Accounting Review, 37(2): 231-248. https://doi.org/10.1016/j.bar.2004.10.003

[86] Akbari, M., Nazarian, A., Foroudi, P., Seyyed Amiri, N., Ezatabadipoor, E. (2021). How corporate social responsibility contributes to strengthening brand loyalty, hotel positioning and intention to revisit? Current Issues in Tourism, 24(13): 1897-1917. https://doi.org/10.1080/13683500.2020.1800601

[87] Haque, F. (2017). The effects of board characteristics and sustainable compensation policy on carbon performance of UK firms. The British Accounting Review, 49(3): 347-364. http://dx.doi.org/10.1016/j.bar.2017.01.001

[88] Puriwat, W., Tripopsakul, S. (2023). Sustainability matters: Unravelling the power of ESG in fostering brand love and loyalty across generations and product involvements. Sustainability, 15(15): 11578. https://doi.org/10.3390/su151511578

[89] Borghei, Z., Leung, P., Guthrie, J. (2018). Voluntary greenhouse gas emission disclosure impacts on accounting-based performance: Australian evidence. Australasian Journal of Environmental Management, 25(3): 321-338. https://doi.org/10.1080/14486563.2018.1466204

[90] Alsaifi, K., Elnahass, M., Salama, A. (2020). Carbon disclosure and financial performance: UK environmental policy. Business Strategy and the Environment, 29(2): 711-726. https://doi.org/10.1002/bse.2426