Hasdi Aimon![]() | Anggi Putri Kurniadi*

| Anggi Putri Kurniadi*![]() | Sri Ulfa Sentosa

| Sri Ulfa Sentosa![]() | Yahya Yahya

| Yahya Yahya![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study explores the correlation between economic growth and financial stability among upper-middle-income countries in APEC, such as Indonesia, China, Malaysia, Mexico, Peru, Russia, and Thailand from 2013 to 2023. It employs a simultaneous equation approach. The motivation for this research lies in securing the well-being of future generations, as effectively managing current economic growth and financial stability will foster investment in future welfare. This lays the groundwork for sustainable and inclusive economic progress over time. Key findings indicate a mutually beneficial relationship between financial stability and economic growth. The study underscores the importance of bolstering financial stability through measures like increasing capital adequacy ratios and credit private sector, while also managing credit card usage and interest rates. Moreover, it suggests that fostering economic growth requires enhancing credit private sector, alongside managing interest rates, unemployment, and poverty. The study recommends that governments of upper-middle-income APEC countries implement macroprudential policies effectively. This strategic approach aims to uphold both financial stability and interconnected economic growth, thereby mitigating systemic risks that could otherwise harm the economy.

financial stability, economic growth, credit card, capital adequacy ratio, credit private sector, interest rate, unemployment, poverty

The financial stability (FS) plays a crucial role in fostering a country's economic growth (EG) by mobilizing savings and facilitating capital accumulation in the real sector [1, 2]. Moreover, a robust FS stimulates investment activities within a country, thereby accelerating EG [3]. However, disruptions in the FS can undermine economic stability (ES) and efficiency because restricted access to financing sources curtails business activities, leading to reduced productivity [4, 5]. Conversely, a well-functioning financial condition enhances a country's FS, enabling it to withstand internal and external vulnerabilities that could otherwise disrupt EG [6, 7]. This, in turn, promotes effective allocation of funds that contribute positively to EG. The more effectively FS fulfills its core functions, the greater its role in supporting EG.

Based on theoretical considerations, there is a plausible relationship between FS and EG, which increases the demand for financial products (FP), leading to heightened activity in financial markets (FM). Therefore, the development of FS can be seen as a derivative of EG. Different studies present varying perspectives on the relationship between FS and EG. Some assert that FS development is a determinant of EG [8-11]. Conversely, conflicting findings suggest ambiguity in this relationship, with some studies indicating that FS has no significant impact on EG [12, 13], while others argue that FS acts as a driving force behind EG [14, 15]. Additionally, certain studies suggest that FS in the short term may actually hinder EG [16]. Empirical evidence tends to support the hypothesis that FS plays a catalytic role in fostering EG [17]. Furthermore, research indicates that using a longer sample period of FS data demonstrates a stronger correlation with EG compared to shorter periods [18, 19].

Based on the findings of previous literature studies, it appears that the focus has predominantly been on analyzing FS effects on EG, rather than the reverse. However, achieving successful economic performance in a country necessitates recognizing the interdependence between EG, which shapes FS. Addressing this research gap, the novelty of this study lies in examining the mutual relationship between FS and EG, incorporating several other external factors. This analysis aims to yield specific policy implications for government use. Apart from that, the analysis that will be carried out as the novelty of this research is also supported by two hypotheses, namely supply leading and demand following [20]. First, the supply-leading approach emphasizes the influence of FS on EG, where relatively stable FS will increase the supply of FP services which will contribute to creating better EG. Second, the demand-following approach explains the influence of EG on FS because an increase in demand for FP services tends to encourage an increase in FM when EG occurs.

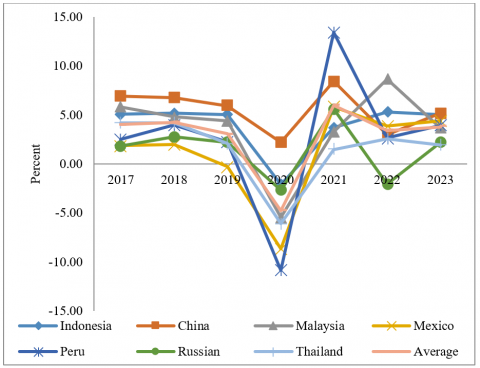

The selection of indicators for FS and EG needs to be emphasized to sharpen the focus on factual phenomena in this study. This research employs the bank z-score indicator to evaluate FS, as it measures the level of risk-adjusted profitability achievement within the banking sector [21, 22]. Additionally, the bank z-score serves as a benchmark for assessing the likelihood of banking insolvency, thereby influencing FS outcomes. Meanwhile, EG in this study is assessed using the annual percentage growth rate of gross domestic product (GDP) [23]. By establishing these indicators, the current state of factual phenomena related to FS and EG in each country can be assessed. However, the research primarily concentrates on upper-middle-income countries (UMIC) within the Asia-Pacific Economic Cooperation (APEC), as depicted in Figures 1 and 2.

Figure 1. The conditions of bank z-score in UMIC in APEC [24]

Figure 2. The conditions of EG in UMIC in APEC [25]

Based on the data from Figures 1 and 2 for the past few years, the average conditions in the seven selected in UMIC in APEC. From 2017 to 2018, an increase in EG corresponded with a decrease in FS. Conversely, in 2019 and 2020, there was an opposite trend where an increase in FS coincided with a decrease in EG. Specifically, in 2020, EG plummeted by -5.23% due to the COVID-19 pandemic, while FS only declined slightly by 0.21 points, indicating a limited impact on FS. Moving to 2021, FS saw a modest increase of 0.02 points, while EG showed a notable rise of 5.96%. Looking ahead to 2022, a decrease in EG is expected to coincide with an increase in FS. Conversely, in 2023, the relationship between FS and EG is projected to follow a similar trend observed previously. Based on the analysis of these trends, it is crucial to conduct a focused review of the study on FS and EG in UMIC in APEC framework. This study will incorporate additional exogenous variables gathered from relevant research to include other indicators that may contribute to explaining the inconsistencies observed in FS and EG trends.

Several researchers have previously examined the link between FS and EG. They found that financial instability can disrupt the relationship between financial development and EG [26]. Additionally, a stable banking sector significantly contributes to EG in Europe [27]. During crises, EG tends to decline, underscoring the importance of a resilient banking system. Research indicates that reduced banking competition can support EG and improve FS. Moreover, EG has a long-term negative and a moderate short-term positive impact on real loan terms, suggesting that higher EG may reduce loan defaults [12]. Factors such as financial crises, bank liquidity reserves, and non-performing loans adversely affect FS, development, and EG [28]. The study revealed that banking system development can hinder EG, indicating inefficiencies in private credit allocation [29]. Market developments also have varied impacts; for instance, stock market size positively affects EG, while market liquidity has a negative effect. Effective financial regulation is essential for achieving higher EG through monetary policies, fiscal policies, and market discipline [30]. Causality analysis shows complex relationships between banking sector stability indicators and EG, highlighting the hierarchical and multidimensional nature of banking stability [31]. Shocks to non-performing loans can reduce profitability, loan growth, and EG [32]. Financial inclusion (FI) can either enhance or hinder the effectiveness of central bank monetary policy tools in achieving FS and EG goals [33]. Increasing FI across populations can significantly boost EG, as it generally has positive impacts across models [34]. A well-functioning financial system is crucial for sustained EG, with components like financial leverage, capital adequacy ratio (CAR), asset quality, and liquidity playing pivotal roles [35]. In European countries, banking competition and stability are key drivers of long-term EG [36]. FS and EG are complementary rather than mutually exclusive, as a stable financial system supports prosperity and growth [37]. Macroeconomic variables typically respond negatively to financial stress shocks [38]. FS enhances economic development by facilitating efficient capital allocation, as evidenced by research highlighting its positive impact on economic performance [39]. Regulatory capital plays a critical role in maintaining high levels of economic output and banking stability simultaneously [40]. Conversely, financial instability impedes EG [41].

The literature review section is structured around two primary focal points: FS and EG. The emphasis in this section is on identifying the factors influencing each of these main areas. Additionally, a selection of exogenous variables will be identified based on a review of pertinent studies to bolster the analysis in this research.

2.1 Determination of FS

FS is characterized by the effective functioning of economic mechanisms such as price determination, resource allocation, and risk management, which are crucial for supporting EG. Understanding the importance of FS involves identifying factors that could potentially destabilize the financial sector, thus anticipating future risks.

Previous research has identified several exogenous factors that influence FS. First, investigations into the relationship between credit cards (CC) and FS reveal a significant long-term negative impact of CC on FS, although short-term effects are negligible [42]. Other studies highlight a pronounced short-term negative effect as well [43], and further confirm that high CC usage tends to exacerbate financial instability [44]. Secondly, the relationship between the Capital Adequacy Ratio (CAR) and FS shows a consistently positive influence, indicating that higher CAR levels are associated with stronger FS [45]. Long-term studies underscore the importance of maintaining a balanced CAR to sustain FS [46], emphasizing its critical role as an indicator for FS [47]. Thirdly, the credit private sector (CPS) has been studied in relation to FS, revealing that increased CPS tends to reduce non-performing loans (NPL) and strengthen FS [48]. Similar research underscores CPS as a stabilizing factor against financial instability [49], and underscores its importance as a governmental instrument for achieving FS [50]. Fourthly, interest rates (IR) have a notable impact on FS, with increasing rates generally correlating with reduced FS [51]. High IR can discourage loan uptake and strain borrowers' ability to make timely credit payments, thereby heightening financial instability [52]. Consistent findings across studies reaffirm IR's significant negative effect on FS [53].

In summary, this research identifies CC, CAR, CPS, and IR as key variables influencing FS alongside EG. Understanding these relationships is crucial for policymakers aiming to maintain and enhance FS in the economy.

2.2 Determination of EG

EG signifies the sustained increase in production over time and serves as a pivotal indicator of a country's development progress. It is closely tied to the expansion of goods and services within an economy's activities. Understanding the factors influencing EG involves examining various economic indicators.

Research highlights several exogenous factors that significantly impact EG. Firstly, CPS exhibits a positive correlation with EG, indicating that increased CPS fosters EG [54]. Similar studies reinforce CPS as a leading driver of EG [55], emphasizing its role in stimulating economic activity [56]. Secondly, IR demonstrate a notable negative influence on EG [57]. Higher IR can constrain production expansion and subsequently reduce EG [58]. Optimal IR settings are crucial for sustaining a steady output increase and promoting EG [59]. Thirdly, unemployment (UE) is identified as a critical factor hindering EG, as high UE levels lead to lower output and EG [60]. Addressing UE is therefore essential for achieving targeted EG [9, 61]. Fourthly, poverty (P) negatively impacts EG by reducing people's welfare and aggregate demand [9]. Increased P levels are associated with decreased EG [62, 63], underscoring the need to alleviate P to bolster EG.

In summary, alongside FS, this research identifies CPS, IR, UE, and P as key variables influencing EG. Understanding these relationships is crucial for policymakers aiming to promote sustainable EG and development.

3.1 Data and variable

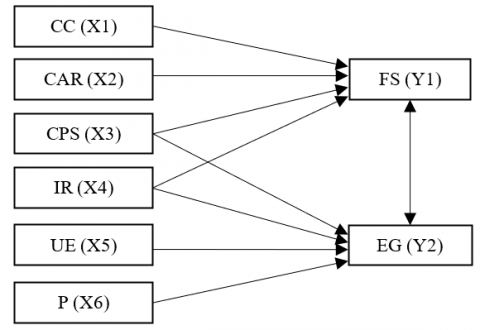

This study utilizes secondary data comprising time series from 2013 to 2023 and cross-sectional data across Indonesia, China, Malaysia, Mexico, Peru, Russia, and Thailand. The research categorizes variables into two types: endogenous and exogenous. Endogenous variables include FS (Y1) and EG (Y2). Exogenous variables consist of CC (X1), CAR (X2), CPS (X3), IR (X4), UE (X5), and P (X6). Based on this variable categorization, a conceptual research framework is developed and summarized in Figure 3.

Figure 3. A framework for research

According to Figure 3, the indicators corresponding to each variable are detailed in Table 1.

Table 1. Indicator of variables

|

Variable |

Indicator |

Source |

|

FS (Y1) |

Assessing the potential for bankruptcy in a financial institution using the bank's z-score, measured by an index |

[24] |

|

EG (Y2) |

The annual percentage growth rate of gross domestic product (GDP) at market prices, measured using constant local currency |

[25] |

|

CC (X1) |

A non-cash payment method utilizing a bank-issued card, measured per 1,000 people |

[25] |

|

CAR (X2) |

The bank's ability to assess and manage the risk of potential losses, ensuring it meets the needs of depositors and other creditors, measured as a percentage |

[25] |

|

CPS (X3) |

The proportion of credit extended by banks or other financial institutions to private parties, measured as a percentage |

[25] |

|

IR (X4) |

Lending rates adjusted for inflation, measured by the GDP deflator |

[25] |

|

UE (X5) |

The percentage of the labor force that is UE and actively seeking work, measured by the total |

[25] |

|

P (X6) |

The percentage of the population living below the national P line, measured by the percentage of the population |

[25] |

3.2 Simultaneous equation model (SEM)

This study employs the SEM, characterized by multiple equations that establish causal relationships between endogenous variables (Y1 and Y2) and their exogenous counterparts (X1, X2, X3, X4, X5, and X6). Moreover, the study includes two SEM, outlined in Eqs. (1) and (2).

$\begin{array}{r}\mathrm{Y} 1_{\text {it }}=\alpha_{1.0}+\alpha_{1.1} \mathrm{Y} 2_{i t}+\alpha_{1.2} \mathrm{X} 1_{i t}+\alpha_{1.3} \mathrm{X}_{\text {it }}+\alpha_{1.4} \mathrm{X3}_{{ }^{i t}}+\alpha_{1.5} \mathrm{X} 4_{\text {it }}+\varepsilon 1_{\text {it }}\end{array}$ (1)

$\begin{array}{r}\mathrm{Y} 2_{\text {it }}=\alpha_{2.0}+\alpha_{2.1} \mathrm{Y}1_{\text {it }}+\alpha_{2.2} \mathrm{X3}_{\mathrm{it}}+\alpha_{2.3} \mathrm{X} 4_{\mathrm{it}} +\alpha_{2.4} \mathrm{X} 5_{\mathrm{it}}+\alpha_{2.5} \mathrm{X} 6_{\text {it }}+\varepsilon 2_{\text {it }}\end{array}$ (2)

where, α: parameters, t: time series, i: cross section, ε: error term.

3.2.1 Identification test

SEM necessitate identification procedures, such as determining the order condition, which is crucial for establishing whether the i-th equation meets the identification criteria correctly. This involves ensuring that the number of predetermined variables not included in the i-th equation is at least equal to the number of endogenous variables in that equation minus one [64]. The identification test in SEM aims to ensure the model can yield consistent and efficient parameter estimates that are interpretable. Mathematically, this is expressed as:

(K – K*) ≥ (G* – 1) (3)

where, G* is the number of endogenous variables contained in the i-equation, K* is the number of predetermined variables contained in the i-equation, and K is the number of predetermined variables contained in the model.

Identification conditions in Eq. (1):

$\begin{gathered}\left(\mathrm{K}-\mathrm{K}^*\right)=(6-4)=2 \\ \left(\mathrm{G}^*-1\right)=(2-1)=1 \\ \text { Obtained: }\left(\mathrm{K}-\mathrm{K}^*\right)>\left(\mathrm{G}^*-1\right)\end{gathered}$ (4)

Based on Eq. (4), it can be inferred that Eq. (1) is part of the SEM, indicating that it is over-identified.

Identification conditions in Eq. (2):

$\begin{gathered}\left(\mathrm{K}-\mathrm{K}^*\right)=(6-4)=2 \\ \left(\mathrm{G}^*-1\right)=(2-1)=1 \\ \text { Obtained: }\left(\mathrm{K}-\mathrm{K}^*\right)>\left(\mathrm{G}^*-1\right)\end{gathered}$ (5)

Based on Eq. (5), it can be concluded that Eq. (2) is included in the SEM, indicating that it is over-identified.

3.2.2 Two-stage least square method (TSLS)

TSLS method is employed when parameter estimation in SEM indicates over-identification. Over-identification occurs when the number of predetermined variables not included in the i-th equation exceeds the number of endogenous variables in that equation minus one [65]. TSLS is a method used to address endogeneity issues in SEM, where endogenous variables are influenced by other variables within the model. By employing appropriate instrumental variables in the first stage, TSLS aims to produce unbiased and consistent parameter estimates. When TSLS is applied separately to each structural equation, it helps mitigate SEM bias. In TSLS, endogenous variables that are correlated with error terms are replaced with predicted values derived from instrumental variables. This approach is particularly effective in models where identification conditions are over-identified.

The TSLS method involves two main stages for estimating SEM. In the first stage, each endogenous variable is regressed on all exogenous variables, including instrumental variables that are uncorrelated with the disturbance term of the structural model. This regression yields predicted values for the endogenous variables. In the second stage, these predicted values replace the original endogenous variables in the structural equations, and the model is re-estimated. The coefficients obtained from this re-estimation represent the TSLS estimates of the model parameters.

4.1 SEM analysis for FS

SEM analysis for FS is encapsulated in Eq. (6). According to Eq. (6), the influence of Y2, X2, and X3 positively contributes to the increase in Y1. Conversely, the impact of X1 and X4 is described as having a negative effect on Y1.

$\mathrm{Y}1_{\mathrm{it}}=-2.65+\underset{(0.02)}{0.36 \mathrm{Y2}_{\mathrm{it}}{ }^{* *}-}-\underset{(0.03)}{0.02 \mathrm{X1}_{ \mathrm{it}}{ }^{* *}}$+$\underset{(0.00)}{+0.11 \mathrm{X2}_{\mathrm{it}}^{* * *}}+\underset{(0.02)}{0.73 \mathrm{X3}_{\mathrm{it}}{ }^{* *}}-\underset{(0.03)}{0.16 \mathrm{X4}_{\mathrm{it}}{ }^{* *}}$ (6)

*** significant at α=1%, ** significant at α=5%, * significant at α=10%.

Firstly, increased EG positively influences various macroeconomic components, including FS. High EG signifies achieved ES, which forms the foundation for enhancing people's welfare. Economic stability is attained through maintaining a balance or continuity between domestic demand, expenditure, savings, and investment. Strengthening the resilience of the domestic economy against both domestic and international shocks is crucial in sustaining ES. Achieving ES benefits FS by ensuring it remains robust and capable of performing intermediary functions, facilitating payments, and managing risks effectively. A resilient and stable EG environment fosters a strong financial system. This study's findings align with research by Creel et al. [6], which underscores that FS can be attained through maintaining ES.

Secondly, the use of CC tends to be oriented more towards consumptive activities rather than productive ones that contribute to real sector development. Despite its direct impact on people's daily lives, the broader implications of a widespread CC payment system can affect the FS. The payment system is integral to FS alongside FI, users (households and corporations), and FM. Disruption in any of these elements can potentially disrupt the entire FS. A significant increase in CC usage can lead to a CC crisis originating from CC issuers, which could spread to banks and capital markets, potentially evolving into a systemic crisis. Such a scenario would threaten FS. The findings of this study align with previous researches [42-44], emphasizing the importance of monitoring CC usage to safeguard FS.

Thirdly, CAR indicates the bank's capacity to supply funds to mitigate potential losses. This criterion demonstrates that enhancing CAR safeguards customers and preserves overall FS. A higher CAR signifies a stronger ability of the banking system to confront potential losses, thereby maintaining FS. Efficient operational activities within banks are contingent upon well-managed CAR, fostering stable financial conditions. Moreover, a robust CAR ratio enhances bank performance, boosting profitability and indicating sound health. Thus, effective management of bank capital influences efficiency through creditor interest. These findings align with prior researches [45-47] which asserts that augmenting CAR is pivotal in sustaining FS.

Fourthly, CPS plays a crucial role in empowering micro, small, and medium enterprises (MSMEs), a strategic initiative aimed at bolstering economic prospects for many by generating jobs, supporting business groups, and aiding government efforts to enhance community welfare. Unlike larger enterprises that rely heavily on bank loans and face bankruptcy during economic downturns and IR, MSMEs, which often lack access to bank capital, remain relatively unaffected. Thus, distributing CPS to MSMEs during economic crises helps sustain FS. This study's findings align with previous researches [48-50], highlighting that increased CPS contributes significantly to FS by fostering economic development.

Fifthly, monetary policy can either stimulate or suppress economic activity through IR. Tight monetary policies, characterized by high IR, tend to stifle EG, while loose policies, with lower IR, can spur economic activity. To ensure monetary stability, central banks employ an inflation targeting framework (ITF). This framework guides monetary policy towards achieving future inflation targets, publicly demonstrating the central bank's commitment and accountability. ITF utilizes policy IR as signals and interbank money market rates as operational targets. Drawing from lessons learned during the global financial crisis, it's crucial for central banks to maintain flexibility in responding to complex economic dynamics and the influential role of the financial sector in macroeconomic stability, thus ensuring FS. This study's findings are consistent with prior researches [51-53], which suggests that high IR can hinder economic vitality by increasing costs for businesses seeking expansion through bank loans.

4.2 SEM analysis for EG

SEM analysis for EG is encapsulated in Eq. (7). According to Eq. (7), the influence of Y1 and X3 positively contributes to the increase in Y2. Conversely, the impact of X4, X5, and X6 is described as having a negative effect on Y2.

$\mathrm{Y}2_{\mathrm{it}}=-1.85+\underset{(0.04)}{0.73 \mathrm{Y}1_{\mathrm{it}}{ }^{* *}}+\underset{(0.03)}{0.25 \mathrm{X}3_{ \mathrm{it}}{ }^{* *}}-\underset{(0.02)}{0.14 \mathrm{X4}_{\mathrm{it}}^{* * *}}+\underset{(0.00)}{0.09 \mathrm{X5}_{\mathrm{it}}{ }^{* *}}-\underset{(0.04)}{0.10 \mathrm{X6}_{\mathrm{it}}{ }^{* *}}$ (7)

*** significant at α=1%, ** significant at α=5%.

Firstly, a stable FS effectively distributes funds and absorbs shocks, thereby preventing disruptions to real sector activities and the broader economy. FS ensures that economic mechanisms such as pricing, fund allocation, and risk management operate efficiently, thereby supporting EG. The FS plays a crucial role within the economy by facilitating the allocation of funds from surplus to deficit entities. An unstable FS hampers this function, potentially hindering EG. Historical evidence indicates that an unstable FS, especially if it leads to a crisis, necessitates costly interventions to stabilize it. This study's findings corroborate research [6], demonstrating that FS fosters EG.

Secondly, the distribution of CPS is closely tied to the development of MSMEs, which play a pivotal role in the economy by employing a significant portion of the workforce compared to larger businesses. MSMEs contribute more substantially to EG than their larger counterparts. Additionally, MSMEs can thrive in diverse regions and adapt flexibly to local economic practices. They contribute to more equitable distribution of goods and services, reducing disparities between urban and rural areas. This decentralization helps in circulating money more evenly across regions, benefiting economically disadvantaged areas where residents do not need to travel to urban centers for their shopping needs. From this perspective, MSMEs also serve as conduits for products from less developed areas to reach urban markets. The findings of this study align with previous researches [54-56], indicating that increasing CPS facilitates the growth of MSMEs, which in turn promotes EG.

Thirdly, an increase in IR dampens both consumer spending and investment enthusiasm. This reduction in consumption and investment diminishes aggregate demand overall. The impact of rising IR is notably felt in the banking sector, where individuals tend to favor depositing funds rather than borrowing, leading to slower credit growth. At the macroeconomic level, higher IR affects all sectors within a country. It curtails bank lending as higher borrowing costs discourage people and businesses from seeking loans, thereby diminishing their purchasing power and hindering national economic expansion. Consequently, EG contracts. These findings align with previous researches [57-59], which underscores that elevated IR undermine EG.

Fourthly, an increase in UE poses significant challenges to achieving EG goals, as it lowers the actual national income potential of communities and subsequently reduces overall prosperity. High UE rates lead to decreased economic activity, resulting in lower individual incomes and reduced tax revenues for governments. This decline in tax revenue limits funding available for economic initiatives, further exacerbating the economic downturn. Moreover, reduced purchasing power among consumers decreases demand for goods and services, discouraging investors from expanding or establishing new industries. Consequently, this diminished investment environment stifles EG. These findings align with previous researches [60-62], which underscores that rising UE rates negatively impact EG.

Fifthly, P exerts a detrimental impact on EG because high P rates diminish people's purchasing power, thereby reducing domestic consumption of goods and services. P reflects economic incapacity, as individuals struggle to meet basic needs due to insufficient income. Several factors contribute to P, including low income levels that limit purchasing power. Additionally, high P rates inflate costs associated with economic development, indirectly impeding progress in economic development initiatives. These findings are consistent with previous researches [9, 63-65], which highlights that increasing P levels undermine EG.

FS and EG have a positive and significant relationship. Furthermore, FS can be achieved by increasing the CAR and CPS, in addition to controlling CC and IR. Then, EG can be achieved through controlling IR, UE, P, as well as increasing CPS. This conclusion cannot be applied in different conditions because it is strictly limited by the type of methodology and panel data set used.

This research recommends that the governments of UMIC in APEC implement macroprudential policies controlled by the central bank. The macroprudential policies carried out lead to an analysis of the entire FS of each financial institution in UMIC in APEC, such as the FS intermediation such as payment services, credit intermediation, and risk financing. Furthermore, the formation of a FS coordination forum can save a country's economic condition in the financial sector. Apart from that, the governments of UMIC in APEC must be able to synergize the three pillars of macroprudential policy, including balanced intermediation, financial system resilience, and FI. This is based on the fact that intermediation aims to ensure that credit growth is not excessive and is sufficient for EG. The contribution of macroprudential policy is also expected to be able to maintain inflation so that it can provide ES in UMIC in APEC.

On the other hand, policies that can be considered to promote FS and EG in UMIC in APEC are that building strong financial infrastructure is the key to supporting sustainable EG. This includes strengthening financial institutions, improving access to financial services, and developing efficient capital markets. Furthermore, the government needs to maintain a balance between income and expenditure to avoid large budget deficits that could disrupt ES. In addition, prudent fiscal policy can also be used to stimulate EG through investment in infrastructure and other development programs. Then, the central bank must implement a monetary policy that is appropriate to current economic conditions. This may include keeping IR low to stimulate investment and consumption, as well as adopting loose quantitative policies when necessary to support EG.

One weakness of this research lies in the challenge of identification within the simultaneous equation model, where causal effects between variables are complex to discern due to their simultaneous relationships. This complicates determining the direction of causality between these variables. To address these limitations, future research is recommended to employ instrumental variables. Instruments are variables that are correlated with endogenous variables but are not influenced by them. Selecting suitable and valid instruments is crucial for achieving robust identification in the model.

[1] Bhargava, M., Sharma, A., Mohanty, B., Lahiri, M.M. (2022). The moderating role of personality in relationship to financial attitude, financial behavior, financial knowledge, and financial capability. International Journal of Sustainable Development and Planning, 17(6): 1997-2006. https://doi.org/10.18280/ijsdp.170635

[2] Stefany, J., Agustina, L. (2022). Do corporate social responsibility and political connections matter to financial performance and financial stability in the banking sector? Evidence from Indonesia. International Journal of Sustainable Development and Planning, 17(8): 2445-2452. https://doi.org/10.18280/ijsdp.170812

[3] Parubets, O., Shyshkina, O., Sadchykova, I., Yevtushenko, Y., Tarasenko, A., Potseluiko, I. (2023). Dynamics of the development of the credit services market in the conditions of financial instability: A case of Ukraine. International Journal of Sustainable Development and Planning, 18(9): 2733-2745. https://doi.org/10.18280/ijsdp.180912

[4] Zhavoronok, A. Popelo, O., Shchur, R., Ostrovska, N., Kordzaia, N. (2022). The role of digital technologies in the transformation of regional models of households’ financial behavior in the conditions of the national innovative economy development. Ingénierie des Systèmes d’Information, 27(4): 613-620. https://doi.org/10.18280/isi.270411

[5] Kelmendi, V. (2024). Impact of macroeconomic factors on bank financial performance: A Turkey and Kosovo comparative study. International Journal of Sustainable Development and Planning, 19(1): 229-235. https://doi.org/10.18280/ijsdp.190121

[6] Creel, J., Hubert, P., Labondance, F. (2015). Financial stability and economic performance. Economic Modelling, 48: 25-40. https://doi.org/10.1016/j.econmod.2014.10.025

[7] Baily, M.N., Klein, A., Schardin, J. (2017). The impact of the Dodd-Frank Act on financial stability and economic growth. RSF: The Russell Sage Foundation Journal of the Social Sciences, 3(1): 20-47. https://doi.org/10.7758/RSF.2017.3.1.02

[8] Ratnawati, K. (2020). The impact of financial inclusion on economic growth, poverty, income inequality, and financial stability in Asia. The Journal of Asian Finance, Economics and Business, 7(10): 73-85. https://doi.org/10.13106/jafeb.2020.vol7.no10.073

[9] Kurniadi, A.P., Aimon, H., Amar, S. (2021). Determinants of biofuels production and consumption, green economic growth and environmental degradation in 6 Asian Pacific countries: A simultaneous panel model approach. International Journal of Energy Economics and Policy, 11(5): 460-471. https://doi.org/10.32479/ijeep.11563

[10] Batuo, M., Mlambo, K., Asongu, S. (2018). Linkages between financial development, financial instability, financial liberalization, and economic growth in Africa. Research in International Business and Finance, 45: 168-179. https://doi.org/10.1016/j.ribaf.2017.07.148

[11] Yakubu, Z., Loganathan, N., Mursitama, T.N., Mardani, A., Khan, S.A.R., Hassan, A.A.G. (2020). Financial liberalisation, political stability, and economic determinants of real economic growth in Kenya. Energies, 13(13): 3426. https://doi.org/10.3390/en13133426

[12] Alsamara, M., Mrabet, Z., Jarallah, S., Barkat, K. (2019). The switching impact of financial stability and economic growth in Qatar: Evidence from an oil-rich country. The Quarterly Review of Economics and Finance, 73: 205-216. https://doi.org/10.1016/j.qref.2018.05.008

[13] Jima, M.D., Makoni, P.L. (2023). Causality between financial inclusion, financial stability and economic growth in sub-Saharan Africa. Sustainability, 15(2): 1-13. https://doi.org/10.3390/su15021152

[14] Kurtoglu, B., Durusu-Ciftci, D. (2024). Identifying the nexus between financial stability and economic growth: the role of stability indicators. Journal of Financial Economic Policy, 16(2): 226-246. https://doi.org/10.1108/JFEP-09-2023-0260

[15] Nasir, M.A., Ahmad, M., Ahmad, F., Wu, J. (2015). Financial and economic stability as 'two sides of a coin': Non-crisis regime evidence from the UK based on VECM. Journal of Financial Economic Policy, 7(4): 327-353. https://doi.org/10.1108/JFEP-01-2015-0006

[16] Safi, A., Chen, Y., Wahab, S., Ali, S., Yi, X., Imran, M. (2021). Financial instability and consumption-based carbon emission in E-7 countries: The role of trade and economic growth. Sustainable Production and Consumption, 27: 383-391. https://doi.org/10.1016/j.spc.2020.10.034

[17] Hasni, R., Dridi, D., Ben Jebli, M. (2023). Do financial development, financial stability and renewable energy disturb carbon emissions? Evidence from Asia–Pacific economic cooperation economics. Environmental Science and Pollution Research, 30(35): 83198-83213. https://doi.org/10.1007/s11356-023-28418-8

[18] Oyedokun, G.E., Orenuga, B. (2023). Effect of financial stability on Nigerian economic growth: An empirical investigation. Technology, 29(11s): 467-479. https://doi.org/10.26458/23432

[19] Ma, C. (2020). Financial stability, growth and macroprudential policy. Journal of International Economics, 122: 103259. https://doi.org/10.1016/j.jinteco.2019.103259

[20] Chow, S.C., Vieito, J.P., Wong, W.K. (2019). Do both demand-following and supply-leading theories hold true in developing countries? Physica A: Statistical Mechanics and its Applications, 513: 536-554. https://doi.org/10.1016/j.physa.2018.06.060

[21] Kasman, S., Kasman, A. (2015). Bank competition, concentration and financial stability in the Turkish banking industry. Economic Systems, 39(3): 502-517. https://doi.org/10.1016/j.ecosys.2014.12.003

[22] Kumar, V. (2016). Evaluating the financial performance and financial stability of national commercial banks in the UAE. International Journal of Business and Globalisation, 16(2): 109-128. https://doi.org/10.1504/IJBG.2016.074477

[23] Feldstein, M. (2017). Underestimating the real growth of GDP, personal income, and productivity. Journal of Economic Perspectives, 31(2): 145-164. https://doi.org/10.1257/jep.31.2.145

[24] Fred Economic Data. https://fred.stlouisfed.org/, accessed on Jan. 11, 2024.

[25] World Bank Data. https://data.worldbank.org/, accessed on Jan. 11, 2024.

[26] Carbó-Valverde, S., Sánchez, L.P. (2013). Financial stability and economic growth. In Crisis, Risk and Stability in Financial Markets: 8-23. London: Palgrave Macmillan UK. https://doi.org/10.1057/9781137001832_2

[27] Ijaz, S., Hassan, A., Tarazi, A., Fraz, A. (2020). Linking bank competition, financial stability, and economic growth. Journal of Business Economics and Management, 21(1): 200-221. https://doi.org/10.3846/jbem.2020.11761

[28] Younsi, M., Nafla, A. (2019). Financial stability, monetary policy, and economic growth: Panel data evidence from developed and developing countries. Journal of the Knowledge Economy, 10(1): 238-260. https://doi.org/10.1007/s13132-017-0453-5

[29] Wang, S., Chen, L., Xiong, X. (2019). Asset bubbles, banking stability and economic growth. Economic Modelling, 78: 108-117. https://doi.org/10.1016/j.econmod.2018.08.014

[30] Apostolakis, G., Papadopoulos, A.P. (2019). Financial stability, monetary stability and growth: A PVAR analysis. Open Economies Review, 30(1): 157-178. https://doi.org/10.1007/s11079-018-9507-y

[31] Pal, S., Bandyopadhyay, I. (2022). Impact of financial inclusion on economic growth, financial development, financial efficiency, financial stability, and profitability: An international evidence. SN Business & Economics, 2(9): 1-29. https://doi.org/10.1007/s43546-022-00313-3

[32] Papadamou, S., Papadopoulos, S., Pitsilkas, K. (2022). The distorting effects of corruption on financial stability and economic growth: Evidence from Russian banks using a PVAR approach. Eastern European Economics, 60(3): 192-216. https://doi.org/10.1080/00128775.2022.2040366

[33] Gbenga, O., James, S.O., Adeyinka, A.J. (2019). Determinant of private sector credit and its implication on economic growth in Nigeria: 2000-2017. American Economic & Social Review, 5(1): 10-20. https://doi.org/10.46281/aesr.v5i1.242

[34] Stewart, R., Chowdhury, M., Arjoon, V. (2021). Bank stability and economic growth: Trade-offs or opportunities? Empirical Economics, 61(2): 827-853. https://doi.org/10.1007/s00181-020-01886-4

[35] Jayakumar, M., Pradhan, R.P., Dash, S., Maradana, R.P., Gaurav, K. (2018). Banking competition, banking stability, and economic growth: Are feedback effects at work? Journal of Economics and Business, 96: 15-41. https://doi.org/10.1016/j.jeconbus.2017.12.004

[36] Guru, B.K., Yadav, I.S. (2019). Financial development and economic growth: Panel evidence from BRICS. Journal of Economics, Finance and Administrative Science, 24(47): 113-126. https://doi.org/10.1108/JEFAS-12-2017-0125

[37] Paun, C.V., Musetescu, R.C., Topan, V.M., Danuletiu, D.C. (2019). The impact of financial sector development and sophistication on sustainable economic growth. Sustainability, 11(6): 1-21. https://doi.org/10.3390/su11061713

[38] Dritsakis, N., Stamatiou, P. (2018). Causal nexus between FDI, exports, unemployment and economic growth for the old European union members. Evidence from panel data. International Journal of Economic Sciences, 7(2): 35-56. https://doi.org/10.20472/ES.2018.7.2.002

[39] Kim, D.W., Yu, J.S., Hassan, M.K. (2018). Financial inclusion and economic growth in OIC countries. Research in International Business and Finance, 43: 1-14. https://doi.org/10.1016/j.ribaf.2017.07.178

[40] Prochniak, M., Wasiak, K. (2017). The impact of the financial system on economic growth in the context of the global crisis: Empirical evidence for the EU and OECD countries. Empirica, 44(2): 295-337. https://doi.org/10.1007/s10663-016-9323-9

[41] Amar, S., Satrianto, A., Ariusni, Kurniadi, A.P. (2022). Determination of poverty, unemployment, economic growth, and investment in West Sumatra province. International Journal of Sustainable Development and Planning, 17(4): 1237-1246. https://doi.org/10.18280/ijsdp.170422

[42] Hamid, F.S., Loke, Y.J. (2021). Financial literacy, money management skill and credit card repayments. International Journal of Consumer Studies, 45(2): 235-247. https://doi.org/10.1111/ijcs.12614

[43] Agarwal, S., Chomsisengphet, S., Mahoney, N., Stroebel, J. (2015). Regulating consumer financial products: Evidence from credit cards. The Quarterly Journal of Economics, 130(1): 111-164. https://doi.org/10.1093/qje/qju037

[44] Pham, M.H., Doan, T.P.L. (2020). The impact of financial inclusion on financial stability in Asian countries. The Journal of Asian Finance, Economics and Business, 7(6): 47-59. https://doi.org/10.13106/jafeb.2020.vol7.no6.047

[45] Dafermos, Y., Nikolaidi, M., Galanis, G. (2018). Climate change, financial stability and monetary policy. Ecological Economics, 152: 219-234. https://doi.org/10.1016/j.ecolecon.2018.05.011

[46] Tangngisalu, J., Hasanuddin, R., Hala, Y., Nurlina, N., Syahrul, S. (2020). Effect of CAR and NPL on ROA: Empirical study in Indonesia Banks. Journal of Asian Finance, Economics and Business, 7(6): 9-18. https://doi.org/10.13106/jafeb.2020.vol7.no6.009

[47] Köhler, M. (2015). Which banks are more risky? The impact of business models on bank stability. Journal of Financial Stability, 16: 195-212. https://doi.org/10.1016/j.jfs.2014.02.005

[48] Gross, M., Semmler, W. (2019). Inflation targeting, credit flows, and financial stability in a regime change model. Macroeconomic Dynamics, 23(S1): 59-89. https://doi.org/10.1017/S136510051700102X

[49] Morgan, P.J., Pontines, V. (2018). Financial stability and financial inclusion: The case of SME lending. The Singapore Economic Review, 63(1): 111-124. https://doi.org/10.1142/S0217590818410035

[50] Minetti, R., Peng, T. (2018). Credit policies, macroeconomic stability and welfare: The case of China. Journal of Comparative Economics, 46(1): 35-52. https://doi.org/10.1016/j.jce.2016.11.005

[51] Coimbra, N., Rey, H. (2024). Financial cycles with heterogeneous intermediaries. Review of Economic Studies, 91(2): 817-857. https://doi.org/10.1093/restud/rdad039

[52] Acharya, V.V., Ryan, S.G. (2016). Banks’ financial reporting and financial system stability. Journal of Accounting Research, 54(2): 277-340. https://doi.org/10.1111/1475-679X.12114

[53] Saha, M., Dutta, K.D. (2021). Nexus of financial inclusion, competition, concentration and financial stability: Cross-country empirical evidence. Competitiveness Review: An International Business Journal, 31(4): 669-692. https://doi.org/10.1108/CR-12-2019-0136

[54] Samargandi, N., Kutan, A.M. (2016). Private credit spillovers and economic growth: Evidence from BRICS countries. Journal of International Financial Markets, Institutions and Money, 44: 56-84. https://doi.org/10.1016/j.intfin.2016.04.010

[55] Cecchetti, S.G., Kharroubi, E. (2019). Why does credit growth crowd out real economic growth? The Manchester School, 87: 1-28. https://doi.org/10.1111/manc.1229

[56] Ibrahim, M., Alagidede, P. (2018). Effect of financial development on economic growth in sub-Saharan Africa. Journal of Policy Modeling, 40(6): 1104-1125. https://doi.org/10.1016/j.jpolmod.2018.08.001

[57] Suprihatin, L., Andrian, T. (2024). The effect of economic growth, interest rates, remittances, and green investment on foreign direct investment in Indonesia. International Journal of Social Science, Education, Communication and Economics (SINOMICS JOURNAL), 2(6): 1777-1788. https://doi.org/10.54443/sj.v2i6.268

[58] Ductor, L., Grechyna, D. (2015). Financial development, real sector, and economic growth. International Review of Economics & Finance, 37: 393-405. https://doi.org/10.1016/j.iref.2015.01.001

[59] Tariq, R., Khan, M.A., Rahman, A. (2020). How does financial development impact economic growth in Pakistan?: New evidence from threshold model. The Journal of Asian Finance, Economics and Business, 7(8): 161-173. https://doi.org/10.13106/jafeb.2020.vol7.no8.161

[60] Kurniadi, A.P., Aimon, H., Amar, S. (2022). Analysis of green economic growth, biofuel oil consumption, fuel oil consumption and carbon emission in Asia Pacific. International Journal of Sustainable Development and Planning, 17(7): 2247-2254. https://doi.org/10.18280/ijsdp.170725

[61] Aimon, H., Putri, K.A., Ulfa, S.S. (2022). Employment opportunities and income analysis before and during COVID-19: Indirect least square approach. Studies in Business and Economics, 17(2): 5-22. https://doi.org/10.2478/sbe-2022-0022

[62] Aimon, H., Kurniadi, A.P., Amar, S. (2021). Analysis of fuel oil consumption, green economic growth and environmental degradation in 6 Asia Pacific countries. International Journal of Sustainable Development and Planning, 16(5): 925-933. https://doi.org/10.18280/ijsdp.160513

[63] Sasmal, R., Sasmal, J. (2016). Public expenditure, economic growth and poverty alleviation. International Journal of Social Economics, 43(6): 604-618. https://doi.org/10.1108/IJSE-08-2014-0161

[64] Lee, N., Sissons, P. (2016). Inclusive growth? The relationship between economic growth and poverty in British cities. Environment and Planning A: Economy and Space, 48(11): 2317-2339. https://doi.org/10.1177/0308518X16656000

[65] Mignon, V. (2024). Simultaneous Equations models. In Principles of Econometrics. Classroom Companion: Economics. Springer, Cham. https://doi.org/10.1007/978-3-031-52535-3_8