Ashish Kumar![]() | Uma Shankar Yadav*

| Uma Shankar Yadav*![]() | Mitu Mandal

| Mitu Mandal![]() | Sanjay Kumar Yadav

| Sanjay Kumar Yadav![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This research investigates how technological innovation and other core factors such as related to entrepreneurial orientation, corporate innovation, environment, society, governance (ESG) and their impact on the environmental performance (EP) of publicly small industry corporations. This study also examines the moderating impact of entrepreneurial orianation and mediating impact of technological innovation on EP. These businesses were selected because they strike a good mix of entrepreneurial orientation, financial success and social responsibility in the handicraft industry. Scholars and legislators alike are becoming increasingly concerned about the long-term viability of small scale business and environmental sustainability in the face of the escalating difficulties arises and resulted in climate change. Because of their outsized influence on emissions worldwide and consumption of resources, businesses worldwide have a responsibility to ensure environmental stability while also working to improve their practices to improve the craft industry as part of the small industry. Therefore, the study was well-suited to this type of exploratory research since it used the PLS-SEM software to examine several correlations simultaneously. These findings prove that adopting ESG principles and the impact of technological innovation supports the environment's performance. The development of eco-friendly goods and procedures, the enhancement of energy efficiency, and the evolution of waste management strategies are all greatly aided by technological innovation. This study is unique in the sense that it apply the impact of corporate innovation on ESG and proposed Digital Dynamic capability concept in this study. The research shows that firms' environmental performance can be significantly improved by emphasising ESG factors, corporate innovation, and embracing technological advancements and entrepreneurial orientation.

corporate innovation, ESG, technology innovation, handicraft industry, sustainable development, environmental performance

Innovation in technology is widely acknowledged as a critical driver of economic progress [1]. However, environmental and social ramifications are essential to a complete understanding of the financial landscape in the current setting. Therefore, developing socially responsible investment considering ESG elements (social, environmental, and governance) has gained prominence [2-8]. According to Yadav et al. [3], businesses now have more opportunities than ever to improve their environmental performance due to the intersection of technical advancement and ESG standards. Technological advances that make creating environmentally friendly products and processes easier may enhance environmental performance [9].

In many studies, strong ESG practices and technological innovation have been shown to improve environmental performance [8, 10]. Technology advancement, especially in the field of green technologies, has been shown to increase energy efficiency, decrease emissions of greenhouse gases, and improve waste management [4]. Technology advancement has also been considered crucial in enhancing ESG performance [11, 12], especially in the environment.

However, studies on the association of ESG practices with technology innovation and how they interact to affect the environmental performance of companies are lacking, especially in the Indian setting. Because of severe ecological threats, India must undergo a radical shift in its economic landscape, making this knowledge gap even more distressing.

Our primary objective is to determine if technological development mediates the connection between ecological performance and ESG practices for small industry businesses. As we know, ESG practices affect micro, small and medium enterprises as they adopt cutting-edge technologies. To accomplish our objective, we will build a solid research model based on the currently available literature and generate hypotheses to fill in the gaps we find therein. We will create a thorough survey questionnaire to explore these hypotheses. Companies in India adopting ESG procedures will form the study's sample population [13].

Business growth is fundamentally driven by corporate innovation. It might be anything as significant as developing an entirely new product line or as modest as boosting a production process's effectiveness [14, 15] also entails implementing cutting-edge technology, developing an inventive culture, and testing new business strategies. Corporate innovation is about creating an atmosphere that allows new ideas to flourish, resulting in tangible business improvements for better environmental performance.

Businesses can better compete by implementing new ideas, strategies, procedures, or products using corporate innovation tools. This strategy encourages innovative rethinking and reframing of enterprises' performance to accomplish organisational goals more effectively and efficiently [16].

Corporate innovation is important because, according to [17], it increases total factor productivity and enables businesses to produce more products at lower costs in an environmentally responsible and efficient manner. Innovation also introduces new growth engines into various industries, which raises demand in most developed economies [18, 19]. Even though corporate innovation is crucial to businesses and economies overall, it is costly because it necessitates large upfront fixed investments and may need significant long-term capital and human resource support from national institutions or the businesses themselves. As a result, several factors have been researched in the literature to determine corporate innovation, including hostile takeover stock liquidity [20]. This study examines how industry-level technical copying affects businesses' incentive to innovate and industry-level innovation activity.

Many academics have examined the connection between corporate innovation and technology copying, but there is disagreement on these studies' theoretical predictions and empirical findings. According to the first perspective, technology copying fosters business innovation because innovation has positive externalities [21]. For example, they contend that technological imitation will increase an inventor's potential profits if innovation is complementary that is, each potential innovator pursues a different research avenue and sequentially—based on the earlier innovations of its predecessors. In this instance, business innovation may not benefit from patent protection, a barrier to copying. The second opinion holds that because of issues with free-riding, technology emulation hinders corporate innovation. For instance, Soewarno [16] discovered that more significant subsidies for technical imitation would result in higher investment in imitation technology and lower investment in innovation technology. Unlike the assumptions provided by Bodhanwala and Bodhanwala [22], technical imitation is predicated on the idea that innovation is independent. This means a firm's innovation incentives will be diminished due to technology copying. According to the third perspective, business innovation and technology imitation have an inverse U-shaped relationship. Up to a high degree of technological imitation, firms' innovation activities and incentives to innovate are negatively impacted by free-riding concerns; however, when technological imitation reaches an extreme degree, free-riding concerns outweigh the positive externalities [23]. These differences occur because of the interactions among firms during the innovation process. In this spirit, Reboredo and Sowaity [24] contended that while extremely high imitation inhibits growth due to free-riding issues, a moderate amount of imitation nearly always adds to growth since it encourages more frequent close competition.

1.1 Indian handicraft industry and ESG

We know that India is an agriculture-rich country. Here, most of the population is involved in agriculture and related sectors. Within their free time of agriculture work, they make and sell/purchase handmade products and sell locally. Their handmade products are utility, religious, decorative, and sustainable. It started during the Mughal Period and spread out throughout the whole country. Handmade products are varied in quality, so they are famous worldwide. Most of the renowned handicraft product are Carpet of Bhadohi, Bras metal of Moradabad, Pottery of Khurza, Terracotta of Gorakhpur, Moonj craft of Prayagraj, Banarshi Saari, Bamboo basket of Bareilly, Jaunpuri Jalebi, Emeriti, Madhubani Paintings, Kolhapur Chappell, Saharanpur wood and paper work are famous in all over India. So, these products are environmentally and socially related to society. The government cares about these craft products' global production, marketing, and export. Due to their sustainable nature and social-cultural value, these are close to ESG, and most of the CSR work will focus on ESG and the craft industry. So, this study has focused on handicraft products related to ESG and some factors like technology innovation, corporate innovation, and entrepreneurial orientation that affect the craft product for better environmental performance in the craft industry [25].

The following are the primary driving forces and contributions of this research. Firstly, this work contributes to the growing body of research on how corporate innovation is affected by ESG notions. Fewer studies have examined the processes behind the relationship between ESG performance and corporate innovation, despite the majority of existing research focusing on the viability of ESG performance as a corporate innovation [21, 26]. This study closes this gap by using ESG ratings from numerous reliable organisations and examining the precise mechanisms through which ESG performance links to corporate innovation—the evaluation centres on agency problem views, information transparency, and corporate governance level. Given the recent emphasis on investment orientation, multinational corporations can proactively contemplate maintaining their market share.

Secondly, it discloses diverse elements impacting the connection between corporate innovation and environmental, social, and governance performance. One the one hand, different business contexts may have other incentives associated with ESG performance and corporate innovation. However, investors' perception of a firm's sustainability [27], linked to obtaining funding for innovation, is also influenced by the features of the firm's industry. As a result, we add to the body of literature by performing a cross-sectional analysis from the viewpoints of industry characteristics and geographic location [26]. As international investors work to improve their investment strategies based on ESG performance and global regulatory agencies continuously improve their ESG rating systems, assessing the possible heterogeneity in the innovative effects of ESG performance has substantial reference value for international markets, especially in emerging market countries.

1.2 Research question

Based on the upper study, the following research question has been raised.

(1) What is the impact of ESG, corporate innovation (CIN) and EO on environmental performance?

(2) Why EO is mediating between TIN and ESG?

(3) What is the mediating role of TIN among ESG and EP?

(4) How ESG is affecting EP in the handicraft industry?

However, studies on the association of ESG practices with technology innovation and how they interact to affect the environmental performance of companies are lacking, especially in the Indian setting [28].

Several studies have been done on small industry, ESG, and environmental performance. However, by focusing on corporate innovation and entrepreneurial orientation in the handicraft industry, there is no such evidence available in the previous study, and there is also a lack of mediating impact of technological innovation between ESG and EP in the craft sector. Because of severe ecological threats, India must undergo a radical shift in its economic landscape, making this knowledge gap even more distressing. Our study seeks to fill this knowledge vacuum by probing a critical question on ESG, technology innovation, and corporate innovation. That is our primary objective is to determine if technological development mediates the connection between ecological performance and ESG practices for small industry businesses. As we know, ESG practices affect the handicraft industry, especially the handicraft industry, as now they are adopting cutting-edge technologies.

To accomplish our goals, we will build a solid research model based on the currently available literature and generate hypotheses to fill in the gaps we find therein. We will create a thorough survey questionnaire to explore these hypotheses. Companies in India adopting ESG procedures will form the study sample population.

The results of our research should aid India's ongoing transformation to a greener economy. As part of our effort to promote sustainable development in Moradabad, Khurja, Bhadohi, and Gorakhpur in Uttar Pradesh, India, this study also plans to offer concrete suggestions to legislators, business leaders, and investors. This suggestion is mentioned in the conclusion section as theoretical, policymaker, managerial, and social implication. We intend to promote an approach that takes the long view. These policies and managerial implications will enhance the Indian regional market of the Indian craft industry, such as Hunnar Haat and SARAS fair, a local name of the Indian handicraft trade field at the national level.

These trade fairs are now exploring their centre at the Global level. For example, in 2022, BRICS organized craft fairs in different cities in China, Brazil, South Africa, and India, such as Bejing, Shanghai, Durban, and Saopol in Brazil and New Delhi in India. This is now popularized as Globalization (local to the global expansion of the craft market). So, through Glocalisation, these markets can prove better opportunities for the BRICS craft market organized in Bejing, Durban, and Saopolo, Brazil.

1.3 Contribution of study

Hence, this paper provides fresh, reliable information that helps businesses make strategic choices. India, the largest developing nation in the world, is moving its economy from rapid expansion to high-quality development. India has followed the global ESG development frontier in search of a sustainable development model, which has resulted in the creation of many ESG rating organisations. This is useful for examining the efficacy of soft environmental performance and the use of technological innovation in the Indian environment, and it serves as a guide for allocating resources and businesses in the direction of long-term growth. Moreover, it offers significant perspectives for other developing nations to thoroughly integrate the notion of entrepreneurial orientation.

This essay will give a thorough theoretical foundation for our study subject by analysing essential concepts and filling in the gaps in the current literature. We will also describe our methodology, which includes our study model and the steps we took to obtain data from our respondents using a predetermined questionnaire. In addition, we will present a comprehensive assessment of the findings, emphasising the study's limitations and potential future avenues for investigation, as well as exploring the practical and theoretical implications of the results.

The organisation of the study is categorized in the following section. Section 2 explores the theoretical background, literature review, and proposed hypothesis. Section 3 discusses research design, data collection and applied tools. Section 4 results are analysed, and validated data has been reported and interpreted. Section 5 contains the discussion and finding neighbourhood. Section 6 includes the conclusion and implications of the research.

2.1 Stakeholder theory

After a literature study, we developed a theoretical framework that will serve as the foundation for our future research. Stakeholder theory is, first and foremost, one of the accepted theories in ESG subject research [29]. In contrast to traditional shareholder domination, it holds that a company's ability to survive and grow depends on the involvement and input of a wide range of stakeholders and that businesses actively seek out the interests of all stakeholders [30]. Shareholders, creditors, workers, customers, suppliers, and other business partners are examples of stakeholders. External entities include government agencies, local citizens, communities, the media, and the environment, which is impacted by the companies' operations either directly or indirectly. They supervise each other and share commercial risks. Thus, when making business decisions, companies need to consider their interests, acknowledge their limitations, and foster a healthy relationship with stakeholders to advance sustainability. In contrast to the conventional theory, which holds that a company's only goal is to maximise financial gains, stakeholder theory offers a more comprehensive viewpoint [31]. Businesses need to focus on social and environmental issues in addition to economic ones to achieve sustainability.

2.2 Backgrounds of theory: ESG criteria

To achieve long-term sustainability, a set of business procedures known as the ESG criteria are considered [16, 32]. The relative importance of these three factors in business management aims to analyse operations holistically rather than just from a financial and economic value perspective [33-36]. Economic and moral principles are defined through transparency to ensure a company's competitiveness and long-term viability [37].

The environmental dimension includes evaluating the company's carbon footprint, use of natural resources (energy use and efficiency), recycling practices, waste management, and initiatives to reduce environmental impact [38-40]. The company's interactions with partners, customers, suppliers, employees, and communities are all included in the social dimension. It entails anti-discrimination, diversity promotion, pay parity for men and women, employee education, and equal opportunity [41]. The governance dimension concerns internal controls, management, audits, executive compensation, accountability practices, shareholder rights, transparency, and anti-corruption policies [42-47]. ESG criteria, usually socially responsible or sustainable investments, let investors gauge a small company's commitment and ESG initiatives. The management of a corporation may use these criteria internally or internationally [48-50].

Having said that, investors, staff, and consumers place an increasing amount of value on a company's adherence to ESG policies and practices, which affects how those companies are perceived and how well they perform beyond financial metrics [39]. There are developing best practices in the corporate sector, although ESG indicators may differ by country, market, and industry [12, 16, 33, 51, 52]. As a result, the Principles for Responsible Investment (PRI), developed by investors in collaboration with the United Nations Environment Program, and this illustrate ESG practices. The PRI aims to direct the market toward responsible development [42, 43, 47, 51, 53]. Therefore, assessing an organisation's performance using ESG indices is one technique used to determine its sustainability. These indices may not fully represent the multifaceted features of ESG criteria, which is one of its drawbacks. Therefore, a broader focus on ESG criteria is required, considering environmental performance [13, 37].

2.3 Theory of the technology organisation environment and extenion of digital dynmaic capbility concept

A multidimensional framework of Hair Jr et al. [17], known as the Technology-Organization-Environment (TOE), has been frequently used to study factors affecting ESG and EP [21, 54]. The TOE framework provides a flexible method for learning how three unique factors— organisational context, technological context [55], innovative, digital, entrepreneurial context [33] and environmental context—impact the managerial decision of small firms to adopt and deploy environmental performance and ESG. The postulated general elements influencing new technological tools, mainly digital technology adoption, improve this framework as per the demand of time in the digital era. Adopting this digital technology and enterprise context makes this framework one of the most dominating, specific and valid for ESG and EP. This is famous as an entrepreneurial and digitalisation-based view [39-41].

The TOE framework can be improved by considering the entrepreneurial orientation (EO) and Entrepreneurial leadership (EL), especially in tiny enterprises owned by the owner, the expectation of the decision maker about the future and the repercussions of adopting e-commerce might influence the adoption attracting toward this EL and are applying in ESG. These theory finally will turn towards a new proped theury where digital age will work with social meaid ESG EL Innovation, Technilogical innovation. Theyr is called “Digital Dynamic Capability Theory” (DDCT) where all capability along with digital technology and resources such as AI, capacity building, ICT, EO, EL, AC, ML Social media, and digitalisation will support the employee and business also in small industry as this theory has been proposed by Yadav and Tripathi [56].

The peculiarities largely shape the enterprise's strategic and tactical focus. Handicraft business owners are inextricably bound to their firms since they control all aspects of the businesses, from day-to-day operations to long-term investments. According to the authors of this research, companies can foster an entrepreneurial mindset by tapping into the inherent capabilities of their owners, despite claims by scholars that the decision-makers' perceptual idiosyncrasies [12, 17, 28, 40, 57, 58] and their feelings about the technology's usefulness and effortlessness directly shape the enterprise's strategy [58-60].

Investors and consumers increasingly demand sustainable business practices. Thus, companies are paying more attention to ESG initiatives and sustainable development [6, 27, 30, 61-63]. ESG practices have been linked to various benefits, including lower costs, higher quality output, and happier customers [7, 33, 64]. Businesses' dedication to ESG is driven by stakeholder pressure and the growing market for eco-friendly goods, and it yields critical information for effective waste management [11].

The broader effects of ESG practices include [11] bolstering business performance and governance, improving environmental outcomes, and aiding sustainable development. Positive environmental and economic impact can be generated by ESG practices, which are also recognized as a substantial route to competitive advantage [9, 10, 48].

However, further research is required to determine the link between ESG performance and innovation, especially technical innovation [8, 65]. According to the OECD, technological innovation is made up of process innovation, organizational innovation, and product innovation. Nevertheless, marketing, process, and product innovation are the most essential parts of innovative technology [12, 66]. By developing products that require fewer resources, are energy-efficient, or are easily recyclable [ 57, 61, 63, 67, 68] and using creative production processes and equipment [14], these forms of innovation attempt to lessen their adverse effects on the environment.

The importance of technological advancement as a link between ESG practices and environmental performance cannot be overstated. According to Porter's premise [15, 44], strict ecological rules can inspire creativity, reduce compliance costs and boost business output. Environmental practices improve companies' competitiveness and productivity by encouraging technical innovation [45, 69]. Some studies [19, 20, 70] have also acknowledged the connection between ESG practices and better environmental performance through technology innovation. Therefore, the following hypotheses are presented in light of the previous discussion:

(H1): ESG practices encourage technological innovation (TIN).

2.4 Technological innovation and environmental performance

As a "double-edged sword," technological innovation is seen as a significant cause of problems, including climate change, ecological imbalances, and increasing pollution. It is also a helpful tool for resolving environmental and sustainable development challenges [25, 71-74]. When a company designs and manufactures new items, it increases its technological capability [12, 42, 43, 47, 51, 53, 75-78]. In addition, it represents the firm's accumulated knowledge and skill in resolving issues throughout its history. Therefore, boosting its technological capacity necessitates better data collecting and processing. Because of its intangible nature, technology can thrive even in intensely competitive markets. Being a good representative of a company's production competence is not only the consequence of experience in production, manufacturing, and R&D but also a good indicator of the quality of the company's management and internal communication [43, 47, 51, 53, 12, 75, 76].

As Yadav and Yadav [43] outlined, technology is a crucial source of competitive advantage. Companies with a technological advantage within their business tend to generate higher profits and are more likely to introduce groundbreaking new products and services. Many resource-based theory studies conclude that technical innovation is essential to a minor business completion [75, 76], either small or craft industry [75]. Say it's the most vital primary resource [49]. A corporation needs to sharpen its competitive edge to achieve sustainable advantages in the market. To thrive, businesses must be keenly aware of and invest in emerging technological trends. Research variables the four things listed below: factors such as (1) technical staff experience, (2) output quality, (3) available machinery, and (4) allocated funds.

According to research done by Yadav et al. [6], a firm technological innovation is the exclusive method or production process that it owns and uses to respond rapidly to changes in the company's external environment. According to Triguero et al. [65], technological innovation refers to an organisation's prowess in selecting, adopting, disseminating, and perfecting new technologies. This prowess is developed through a series of steps, including the organisation's actual engagement with these technologies and observing how they are used and might be improved.

(H2): TIN improves companies' environmental performance.

(H2a): TIN is mediating between ESG and EP.

2.5 Performance of environment

Measures form the basis for evaluating environmental effectiveness [64]. The questionnaire has eight questions about ecological performance. First, the extent to which the company is pleased with its current efforts to decrease pollution and production costs [79, 80]. Second, the time to which it is satisfied with its recent efforts to reduce environmental fines. Third, the extent to which it is pleased with its current efforts to enhance relations with the local community. Fourth, the period to which it is happy with its recent efforts to decrease workplace accidents. Fifth, the extent to which it is pleased with its current efforts to enhance its image as a leader in environmental protection; thus second hypothesis is as:

(H3): There is a favourable association between EP and ESG practices.

Entrepreneurial orientation (EO) is an essential strategic resource, according to RBV, and extension of RBV is dynamic capability theory where Innovation is crucial capability and its extension is digital dynamic capability theory (DDCT) as proposed by Yadav and Tripathi [56], which will focused on digital and advanced technological skill and tools applying in current scenario and environmental management is a strategic tool. Positive disclosure of data related to the EO promotes the capability of the corporate sector to do new or creative things for the handicraft sector between businesses, local governments, the media, and the public, maintains a good reputation, and boosts legitimacy [81]. Environmentally friendly practices encourage enterprises to eliminate high-energy-consuming and high-polluting production methods and backward production capacity and communicate to the capital market that the firm is socially responsible. It also shows the firm's dedication and ability to develop sustainably, boosting investor confidence and lowering corporate innovation costs [82].

Undoubtedly, human capital drives enterprise innovation. Specialized workers help companies create more competitive products and services [82]. Organizations can boost employee innovation and job excitement through reward systems, team-building activities, staff training, etc. [44]. Maintaining a steady supplier connection helps organizations ensure product quantity and quality and saves time and energy in finding new suppliers and negotiating contracts. Reducing transaction costs and supplier uncertainties helps corporate innovation [79].

An efficient corporate governance system encourages managers to take risks and aligns manager and shareholder interests [80]. Overconfidence corrects risk-averse managers' underinvestment in innovation and catches investment projects with good return prospects, increasing innovation output [83]. Shareholder meetings, boards of directors, supervisory boards, and senior management create strategic plans and provide financial, human, and technological resources for innovation. The signals of social responsibility sent by ESG practices can also increase external stakeholders' risk tolerance and trust [78]. Finally, many ESG indices help companies innovate, such as H4, H5, and H5a.

Hypothesis H4: EO is positively associated with CIN.

Hypothesis H5: EO is related to corporate innovation.

H5a: There is a positive relationship between EO, EP, and CIN.

2.6 Moderating effect of EO between ESG and TIN

Apart from governance performance, the moderating role of EO affects ESG and TIN and enhances technological innovation, which involves positive environmental performance. A positive and statistically significant relationship between environmental performance and firm value has been revealed. On the other hand, a positive but negligible correlation was discovered in the moderating results between the TIN and ESG. So, it has been seen that there is a positive relationship between EO along with ESG and TIN [12, 24].

Hypothesis H6: EO is moderating between ESG and TIN.

Based on the proposed hypothesis, we have proposed the following model and conceptual form through Smart PLS software. For this, please see Figures 1 and 2.

Figure 1. Proposed model

Sources: Designed by Authors

Figure 2. Model derived through Smart PLS 4.0

Sources: Figure design through Smart PLSE software

3.1 Collecting a sample and information

Distributing structured questionnaires through email to Indian craft firms doing business as local entrepreneur was part of the quantitative method used in this study. The primary goal was to collect responses from managers and executives with a craft firm grasp of environmental and social concerns related to their organisation's innovation, ESG practices, EO and ecological performance in producing goods and services processes. The time frame for gathering this information was one months, from December 2023 to January 2024. Ninety-five businesses were contacted through email and asked to participate in the survey. Eighty per cent of the questionnaires were returned afterwards, totaling 76 responses. Eleven of the first responses were disregarded as they included errors or were unsatisfactory. Therefore, 65 complete surveys served as the basis for this research (see Table 1).

Table 1. Respondent profile

|

Element |

Items |

Frequency |

|

|

registered firm |

83.30% |

|

Firms type |

non-registered firms |

18.70% |

|

|

job |

5.10% |

|

|

business |

1.80% |

|

|

small industry |

55.40% |

|

|

real state |

4.90% |

|

Business line |

energy |

7.10% |

|

|

finance |

2.40% |

|

|

health and hygiene |

15.70% |

|

|

client insurance |

4.60% |

|

|

10-50 or less than |

10.10% |

|

|

51-100 |

31.60% |

|

Number of employees |

101-200 |

4.80% |

|

|

200 and above |

13.50% |

Sources: Table compiled by authors

Most of these businesses (81.3%) were in business, while the rest (18.7%) were not. These businesses came from various industries, but 53.4% were in the handicraft sector.

According to the results, most businesses surveyed had between 51 and 200 artisans/entrepreneurs. Most companies in the survey sample had between 50 and 2 00 entrepreneurs who were small firms involved owners, primarily in the handicraft sector.

3.2 Reason for sample selection and period

This period was due to the suitability of selling and producing handicraft products locally. Artisans, after 2022, suddenly changed to sailing and making in massive amounts. Their mindset has also transformed into environmental protection, and consumers are now becoming aware of the use of handmade products. Therefore, the authors have taken samples during this time in 2023. The reason for selecting the current methodology is an irregular distribution of artisan craft clusters for different reasons; it was impossible to collect from one side to the other [84]. So, the authors have selected respondents from an accessible group. Another reason was that these industries face promotion problems due to a lack of digital technology and infrastructure.

Initially, the authors sent the questionnaire to 150 people, but only 95 responded. After coding and correcting their proper answer, only 76 were found suitable. However, 11 had some errors, so 65 were finally taken as the final sample.

Ninety-five businesses were contacted through email and asked to participate in the survey. Eighty per cent of the questionnaires were returned afterwards, totaling 76 responses. Eleven of the first responses were disregarded as they included errors or were unsatisfactory. Therefore, 65 complete surveys served as the basis for this research.

This was either due to the income of the answer or they refused to give a response to some questions. So, one of those questions was taken for analysis that fulfilled the criteria.

3.3 Variables

PE is a dependent variable, and ESG TIN, EO is the independent variable. Some variables that were constant during the analysis were called controlled variables. Firm size, gender, education, and work experience e were used as control variables for this study.

3.4 Measuring scale and data

The study variables were measured by having participants fill out a multiple-choice questionnaire. A 5-point Likert scale was used for this evaluation, with responses possible on a scale from 1 (strongly disagree) to 5 (completely agree).

The questionnaire's questions were revised in light of earlier studies on ESG procedures, technological advancement, and environmental effectiveness [16, 32]. The questionnaire was divided into two sections: the first offered basic demographic information, while the second comprised more in-depth questions. In total, there were 17 inquiries in the survey.

4.1 PLS-SEM (Measurement model)

PLS-SEM overcomes the given limitation by dealing only with structural models in a simple form. However, SEM using PLS can estimate multivariate integration, coating measurement, and structural models. SEM is available in two states: PLS-SEM and CB–SEM methods. If we compare it to PLS-SEM with CB–SEM, PLS-SEM is much more advanced in flexible modelling and algorithm. It can be handled with small data if no extensive data is available with a different skewness and normality [17, 26, 85, 86]. PLS-SEM has been adapted for empirical study and is currently used in business management and the construction of tools. This is why we have used PLS-SEM in our research for data analysis [17, 26, 27, 34, 52, 57, 61, 63, 67, 68, 85-88].

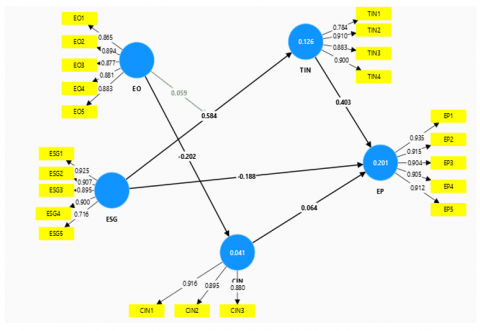

The Smart PLS 4.0 software was used to conduct a PLS-SEM analysis, which allowed for the development of a causal model. Measurement and structural models were just two statistical techniques better to understand this study's interplay between predictors and outcomes. Table 2 and Figure 3 show that all are given about the construct's Cronbach alpha and composite reliability according to earlier studies [6, 59, 87].

Table 2. Factor loading and reliability test

|

Variable |

Items |

Loading |

Cronbach alpha |

Composite Reliability |

AVE |

|

ESG practices |

EG1 |

0.768 |

|

|

|

|

|

EG2 |

0.776 |

0.834 |

0.910 |

0.760 |

|

|

EG3 |

0.786 |

|

|

|

|

|

EG4 |

0.678 |

|

|

|

|

|

EG5 |

0.765 |

|

|

|

|

|

EG6 |

0.678 |

|

|

|

|

Entrepreneurial Orientation |

EO1 |

0.765 |

|

|

|

|

|

EO2 |

0.763 |

0.812 |

0.892 |

0.783 |

|

|

EO3 |

0.785 |

|

|

|

|

|

EO4 |

0.765 |

|

|

|

|

|

EO5 |

0.678 |

|

|

|

|

Technological Innovation |

TN1 |

0.876 |

|

|

|

|

|

TN2 |

0.679 |

0.817 |

0.877 |

0.730 |

|

|

TN3 |

0.768 |

|

|

|

|

Environmental Performance |

EP1 |

0.765 |

|

|

|

|

|

EP2 |

0.933 |

|

|

|

|

|

EP3 |

0.789 |

|

|

|

|

|

EP4 |

0.933 |

0.920 |

0.910 |

0.746 |

|

Corporate Innovation |

CIN1 |

.916 |

.941 |

.810 |

0.651 |

|

|

CIN2 |

0.895 |

|

|

|

|

|

CIN3 |

0.880 |

|

|

|

Sources: Authors compilation

4.2 Convergent validity and reliability

Figure 3 shows the item loading factor and path coefficient for each variable. When developing new items or scales, it is best practice to remove an item if the estimated model has loadings below 0.707. All of our loadings are higher than the maximum allowed. All questionnaire items used to measure the variables are valid since the validity test showed a composite reliability of between 0.8708 and 0.927. Information is summarized in the table below.

Figure 3. Measurement and path coefficient model

Sources: Smart PLS 4.0 output

4.3 Common method bias (CMB)

Studies utilizing mediation and moderation analysis typically do not indicate common method bias (CMB) [89]. Podsakoff et al. [89] proposed several statistical and procedural remedies we used throughout the instrument design and administration phase to make the scale concise, easy to understand, and straightforward. With a threshold of 50%, the study used single-factor and factor analysis tests, and the variance came out as 27.25 per cent. This proved that there was no CMB in the research. The approach compares them to ensure there wasn't a big gap between early and late responses. Our study used the total number of employees and annual revenue to compare. For the respondent profile, please refer to Table 1.

In Tables 3 and 4, the discriminant validity value is given. Table 3 has a DV Value through Fornell Larcker (1981) and a dark diagonal relationship showing their worth. It is evident in Table 4 that discriminant validity has been calculated using HTMT criteria. They are under standard weight. It means all factors support the dependent variable. According to the HTMT criteria, the values (in bold) in Table 2 show discriminant validity issues, which is suitable for 0.85. This suggested that the HTMT criterion could identify instances of multicollinearity due to collinearity among latent components.

Table 3. Calculation of discriminant validity

|

|

Discriminant validity from Fornell –Larcker Criteria |

||||

|

|

ESG |

TIN |

PE |

EO |

CIN |

|

ESG |

0.779 |

|

|

|

|

|

TIN |

0.459 |

0.834 |

|

|

|

|

PE |

0.489 |

0.456 |

0.851 |

|

|

|

EO |

0.760 |

0.769 |

0.789 |

0.893 |

|

|

CIN |

.876 |

0.768 |

0.892 |

0.786 |

0.854 |

Sources: Authors' compilation

Table 4. Discriminant validity by HTMT

|

Calculation of Discriminant Validity by HTMT |

|||||

|

|

ESG |

TIN |

PE |

EO |

CIN |

|

ESG |

|

|

|

|

|

|

TIN |

0.549 |

0.732 |

|

|

|

|

PE |

0.768 |

0.702 |

0.690 |

|

|

|

EO |

0.556 |

0.560 |

0.546 |

0.756 |

|

|

CIN |

.896 |

0.654 |

0.840 |

0.783 |

0.789 |

Sources: Authors' compilation

From Tables 3 and 4, the correlations between the various sets of variables are below the square root of the average variance extracted (AVE). None of the Heterotrait-Monotrait (HTMT) values were more than 0.90, indicating that discriminant validity was not compromised. All values were satisfied, and this proves that the factors are valid.

4.4 Model-fit statistics

A structural model was used for the path analysis, and model fit must be verified. Numerous capabilities in PLS-SEM can test the goodness of fit.

Due to the method's differing underlying principles, PLS-SEM falls short in this area. It is advised against using model fit indices to conclude because the PLS-SEM literature is still developing in this area [84].

PLS model fit indices provide fewer possibilities. There are just a few approximations, including SRMR, NFI, and Chi2. PLS also offers precise measurements such as d_ULS (i.e., the squared Euclidean distance) and dG (i.e., the geodesic length [87, 67]. Nearly all GoF metrics exceed the bar established by earlier literary works (see Table 5). The NFI & CFI scores are above the threshold. The SRMR is 0.4, and the RMSEA is 0.7. In this investigation, SRMR was 0.06, and NFI was 0.89, according to PLS-SEM. PLSc reported a higher SRMR than PLS (0.05), demonstrating a more accurate model fit. Indicating a solid model appropriate (for both PLS and PLSc), both d_ULS (i.e., the squared Euclidean distance) and d_G (i.e., the geodesic distance) yield values that are not significant [86]. However, numerous scholars have suggested estimated model values for these measures in PLS. There is uncertainty surrounding the selection of saturated and estimated model values. Comparing these results to the thorough CB-SEM, these conclusions should be disregarded. Model fit indices must be considered collectively rather than separately to evaluate the model and gain a better understanding [72].

So, in Table 5, the Goodness of Fit test findings are fully summarized and discussed. Regarding Table 5, it is possible to state that, in general, all Goodness of Fit requirements have already been met for both the structural (inner) model and the outer model [26, 61]. The research model is deemed fit based on the goodness of fit test findings, and a hypothesis test can be conducted.

Now, there is also a need to check its goodness of fit by calculating the standard fit index (NFI), the baseline proportion. The threshold value should be above 0.90, and the average value is .90. The reflective appropriate index (RFI) that is the degree of freedom, incremental suitable index (IFI) shows the improvement of model fitness CFI assumption of the distribution of baseline for factors it also calculates the SRMR (standardized root mean squire residual that should be between (0 and 1). So, it is above 0.4 and sometimes shows a value of 0.6 in the case of advanced PLS. All these values in this study are satisfied, so construct the excellent fit. For this, please see Table 5.

Table 5. Goodness of fit test in PLS-SEM

|

Empty Cell |

Normal Range |

Observed It Value |

|

The Chi-square |

** |

** |

|

NFI |

.93 |

.89 |

|

CFI |

.95 |

0.91 |

|

TLI |

.94 |

0.92 |

|

SRMR |

.04 |

.05 |

|

d_ULS |

0.58 |

.56 |

|

d_G |

0.23 |

.22 |

Sources: Authors' compilation

This investigation's findings point to interdependencies across environmental performance, ESG practices, and technological innovation.

4.5 Result validity test

First, it shows that ESG practices have a statistically significant beneficial effect on technological innovation (beta = 0.584, p = 0.000, and the impact of TIN on EP is (0.188, p = 0.0001). Put another way, businesses with better ESG processes are more likely to develop groundbreaking new products. This may be because handmade industries that follow excellent ESG policies are more likely to adopt new technologies, especially those that improve their social and environmental performance.

Second, the beta coefficient for the association between environmental performance and TIN and EP practices is 0.436 (p0.001). This indicates that handicraft organizations with higher standards of EP performance also produce better ecological results with the support of technological innovation. As for the third discovery, researchers discovered that technological innovation ESG-TIN-EP (H2a) indirectly and positively correlates with environmental performance and ESG (beta coefficient = 0.532, p = 0.007). Companies on the cutting edge of technological innovation usually do a better job of protecting the environment. This could be because technical advancements help businesses run more efficiently, causing them to have less of an impact on the environment [19, 20, 70, 90].

The fourth outcome directly links EO to CIN. This indicates that EO supports corporate innovation in the energy sector, whether in the craft or machine-made industry. Previous studies also support this view [78]. In the case of CIN-EP, it has been observed from the table that Beta value = 0.064 is insignificant for EP and has no direct impact on performance. It argues that ESG practices may improve environmental performance by encouraging technical innovation. This result is supported by the beta coefficient of EO-CIN (H6) as moderator impact of EO with a p-value of 0.134.

Similarly, moderating the impact of EO on EP and CIN strengthens the value of environmental performance as a beta value = 0.135 and p-value 0.012 to enhance business performance. EO is also motivated to improve environmental performance with the help of TIN.

The significance test of indirect effects and the route coefficient are shown in Table 6. The following conclusions are drawn from Table 7: In hypothesis H7a, we postulated that TIN would serve as a mediator between (ESG) and EP (beta coefficient = 0.532 at p-value = 0.034), which is the acceptable range and fully mediating. The mediating impact of EO between CIN and EP (beta value = 0.101 at p vale = 0.006, which is less than p-value = .05. So H5a is fully mediating and accepted.

Table 6. p-value and path coefficient (indirect effects) and the mediating effect

|

Hypothesis |

Original Sample (O) Path Coefficient (Beta) |

Sample Mean (M) |

SD (STDEV) |

t-statistics (|O/STDEV|) |

Mediation |

p-values |

Decision to Hypotheses |

|

|

ESG→TIN→EP |

H2a |

0.532 |

0.091 |

0.039 |

2.303 |

Full mediation |

0.034 |

Accepted |

|

CIN→EO→EP |

H5a |

0.101 |

0.046 |

0.024 |

2.016 |

No mediation |

0.141 |

rejected |

The significance test of indirect effects and the route coefficient are shown in Table 6. The following conclusions are drawn from Table 6: In hypothesis H7a, we postulated that TIN would serve as a mediator between ESG and EP (beta coefficient = 0.532 at p-value = 0.034), which is the acceptable range and fully mediating. The mediating impact of EO between CIN and EP (beta value =0.101 at p vale = 0.006, which is less than p-value = .05. So H5a is fully mediating and accepted.

4.6 Meditating impact of TIN (indirect effect) using the Sobel test

R2 is the only measure of how much independent variables may be explained by predictive factors. Effect size f2 can be used to calculate a mediating variable's contribution to R2 of the environmental performance (DV). Table 6 demonstrates that while the effect size of EO is minimal on PE (f2 0.15), it is substantial on entrepreneurial orientation (f2 > 0.35). Be aware that the impact of TIN on PE is moderate (f2 = 0.186, or greater than 0.15 but less than 0.35). It is followed by performance-related criteria, such as technological innovation and PE (f2 = 0.040 and f2 = 0.135, respectively).

As suggested, the test was created by Sobel and his colleagues in 1982 [19, 79]. This test can be used to evaluate the relevance of mediating effects.

4.7 Reason for using the Sobel test

This is the most suitable test when we analyse the mediating impact of the higher construct as if there are different small, medium and significant values in mediation. In comparison to the bootstrap test, we use the Sobel test. This Sobel test assesses the direct and indirect effects of the IV on the DV to ascertain whether a mediator is involved. The test result can be interpreted in one of five ways: Four different types of mediation exist: (1) Direct-only or no mediation at all (in which the indirect effect is not significant and the direct effect is significant); (2) Neither the indirect effect nor the direct effect is significant; (3) when both are significant and move in the same direction, we refer to this as complementary mediation; and (4) when both move in the opposite direction, we refer to this as competitive mediation. Table 8 demonstrates that although EO directly impacts the environment's performance in craft enterprises, this impact is statistically insignificant. PE is indirectly affected by technological innovation. The mediator technological innovation indirect-effect path coefficients of 0.071 and 0.315 (H4, H6) are all positive because there is no direct relationship between TIN and PE.

On the other hand, a positive but negligible correlation was discovered in the moderating results between the business value and government performance in models 3 and 4. Thus, the results confirm that, when implementing environmentally friendly initiatives and evaluating the social responsibility performance of the sampled organisations, it is necessary to consider successful research and development investment. The moderating results indicate that R&D investment substantially impacts social and environmental performance and company value. As a result, the sampled enterprises should make effective R&D investments to advance social and ecological goals. On the other hand, government performance showed a small but positive coefficient. The positive slope suggests that including research and development spending will boost GP's impact on the sampled enterprises' firm values.

4.8 Moderating the impact of EO (H6)

To investigate the moderating impact of EO, this study adopted a product indicator (PI) strategy. The PI method is used in structural equation modelling to predict latent interactions. Positive correlations between ESG and TIN were shown to be moderated by EO (beta coefficient = 0.077, t = 2.905, p = 0.002), so indirectly, it is according to the normal range. And it is moderating at the given TIN. In addition, the moderating influence is shown in Figure 4: EO enhances the relationship between TIN ESG [12, 82]. So, we can say that H6 is moderating and enhancing the EP with the support of ESG.

Figure 4. Measurement model internal path structure

Sources: Smart PLS-SEM output

EO was also recognized as a moderator. With EO, an enterprise can strengthen its relationship with ESG and TIN by aligning entrepreneurial orientation and reducing conflicts. This enables members to think and work together to enhance their processes to meet problems and seize opportunities. EO is a style of willing ness that helps business participants grasp the results of an integrated performance of the environment [24]. Hence, hypothesis H6 supports and enriches the TIN (Table 7).

However, the significance level was too low to be considered (Beta = 0.040, p > 0.05), as given in Table 4 and the simple screen plot in Figure 4.

From Figure 5, it is clear that EO moderates ESG and TIN. This investigation's findings point to interdependencies across environmental performance, ESG practices, and technological innovation.

Figure 5. Screen plot figure showing the moderating impact of EO on ESG and TIN

First, it shows that ESG practices have a statistically significant beneficial effect on technological innovation (beta = 0.481, p = 0.000 and the impact of EO on PE is 0.556, p = 0.0001). Put another way, businesses with better ESG processes are more likely to develop groundbreaking new products. This may be because companies that follow excellent ESG policies are more likely to adopt new technologies, especially those that improve their social and environmental performance.

Second, the beta coefficient for the association between environmental performance and ESG practices is 0.363 (p0.001). This indicates that organisations with higher standards of ESG performance also produce better ecological results. The 'E' in ESG stands for 'environmental,' so it's unsurprising that environmentally conscious business practices are a hallmark of ESG-focused organisations.

As for the third discovery, researchers discovered that technological innovation positively correlates with environmental performance (beta coefficient = 0.289, p = 0.007). Companies on the cutting edge of technological innovation usually do a better job of protecting the environment. This could be because technical advancements help businesses run more efficiently, causing them to have less of an impact on the environment [25].

The fourth and final outcome indirectly links ESG to environmental performance through technological advancement. It argues that ESG practices may improve environmental performance by encouraging technical innovation. This result is supported by the beta coefficient of 0.142 and the p-value of 0.015. Similarly, in the case of EO and TIN, the beta value is 0.135, and the p-value is 0.012, so the result is supported. In the real world, this might mean that a company's efforts to boost its ESG rating could spur more environmentally beneficial innovation. EO is also motivated to improve environmental performance with the help of TIN.

5.1 About H1 and H2 and H3

The country's dedication to innovation and technology highlights the necessity of incorporating ESG practices and EO into India's ongoing economic transformation. Indian businesses can improve their bottom lines and affect the world by embracing ESG principles. ESG is positively associated with TIN, so H1 is accepted similarly to H2, and H3 also supported the positive relationship between TIN and EP, ESG and EP [8, 54]. It also supports the idea that ESG has a positive relationship with TIN.

5.2 About H4

Further, Yadav et al. [78] also discussed a positive relationship between EO and CIN in the manufacturing sector. So, when this study is applied in the handicraft sector, it also proves that CIN and EO have a positive relationship. Even CIN mediates between PE and EO. Previous studies prove that the role of corporate innovation is factoring in this digital era [28, 41]. Table 6 and Table 7 clearly explain that it has been observed that even H4 is entirely associated with the EO, so we can say that the impact of corporate innovation supports better performance if there is good support towards government and society as ESG has a positive effect and enhances the sustainability of the craft industry.

Table 7. Validation of hypothesis and result

|

Hypothesis |

Paths |

Beta value |

Std. Error |

T-value |

P-value |

Signification |

|

H1 |

ESG-TIN |

0.584 |

0.082 |

5.781 |

0.000 |

Accepted |

|

H3 |

ESG-EP |

0.188 |

0.101 |

3.421 |

0.002 |

Accepted |

|

H2 |

TIN-EP |

0.407 |

0.103 |

2.690 |

0.005 |

Accepted |

|

H2a |

ESG-TIN-EP |

0.532 |

0.213 |

2.245 |

0.034 |

Fully mediating |

|

H6 |

EOXESG-EP |

0.135 |

0.091 |

2.432 |

0.012 |

Moderating |

|

H4 |

EO-CIN |

.202 |

0.054 |

3.213 |

0.004 |

Accepted |

|

H5 |

CIN-EP |

0.064 |

0.078 |

1.234 |

0.134 |

Not accepted |

|

H5a |

CIN-EO-EP |

0.058 |

0.421 |

2.234 |

0.141 |

No mediation |

As one strategy, Indian companies might work to reduce their use of fossil fuels and increase their reliance on energy-efficient technologies. Plus, they may focus on developing clean technology to improve areas like waste management, air quality, and carbon footprint [24, 52, 54, 87, 91, 92].

Collaboration between various players in India's innovation system is bolstered by incorporating EO and ESG practices into technology innovation. Innovation and sustainability in technology can be achieved through partnerships between businesses, academic institutions, and other interested parties. Sharing information, conducting research together, and forming sustainable development-focused technology hubs are all made more accessible by this partnership [37].

5.3 About H5a and 2a as mediating impact

The results indicate that corporate innovation indirectly and considerably impacts EP and EO when considering the mediator variable. The analyzed indirect paths are longer statistically significant (0.71 and 0.135, respectively, at p 0.01) when the mediating variable is present. However, the anticipated indirect impacts are more critical when the mediating variable is included. The putative mediating function of CIN was investigated using Sobel tests for H5a [14, 33, 93].

Business performance, corporate risk, and information asymmetry are higher in organizations with poor ESG performance than those with strong EP; external investors are less worried about the firm's solvency and growth capability.

In the case of H2a, ESG aids in boosting the small industry's bottom line. TIN has a mediating impact between ESG and EP. Tin is supporting the EP through TIN. Clients that place a premium on corporate social responsibility will pay more for goods and services produced by companies with strong ESG performance. Firms gain a competitive advantage through differentiation, which can result in more significant product premiums if they address the needs of these consumers by enhancing their ESG performance [94].

Second, ESG contributes to decreased corporate risk. The moral and reputational capital that may be amassed through effective ESG performance can be considered the application of technological innovation (TIN) for businesses. This impact helps companies weather unexpected setbacks. Customers lost, finance issues encountered, and a stock price drop are all more likely in the event of a deteriorating external environment. In terms of ESG performance, successful businesses have built up sufficient stakeholder confidence to count on that confidence to see them through tough times [11]. The insurance effect can help mitigate the financial fallout from unlucky occurrences. Investors are more forgiving of companies with strong ESG performance and are more likely to attribute adverse events to inadvertence rather than malice [14, 15, 44].

In conclusion, there will be numerous gains from incorporating ESG practices and EO into corporate and technology innovation within the Indian handicraft sector. This approach fosters an environment where new ideas can flourish and be implemented. This innovative spirit is directed toward answers that satisfy the immediate demands of business and the larger societal and environmental context, as EO, TIN and ESG and CIN practices intrinsically favour socially responsible and sustainable ways.

Incorporating ESG principles and EO also boosts business competitiveness. Small firms that adopt EO and ESG are in a stronger position to satisfy stakeholders' expectations and react to shifting landscape regulation in today's business environment, which places a premium on sustainability. In addition, craft artisans and corporate investors are more likely to invest in such firms because of the value they place on eco-friendly methods of operation. These businesses ensure long-term profitability while contributing to sustainable development by servicing the vital core of profit, people's gain.

Integrating ESG standards and entrepreneurial orientation into corporate processes fosters collaboration in the handicraft industry. EO and ESG principles encourage collaboration within the craft organisation and with external stakeholders related to the craft business. By working together, more significant progress can be made than is possible individually.

India may position its businesses as leaders in the movement toward a socially responsible and green economy if it adopts this strategy for technology innovation. Taking the lead in this transition has enormous potential for international recognition and growth in an era when social equality and climate change are severe global challenges.

This work has advanced our theoretical knowledge of the interaction among environmental performance, EO and ESG practice with innovation. It has illuminated how crucial technical advancement is to optimise the beneficial effects of EO and ESG practices on environmental performance. These discoveries may guide future study in this fascinating and vital area, creating new opportunities in the handicraft industry to boost economies.

This study emphasizes the value of ESG principles in promoting innovation and enhancing environmental performance from a practical aspect with the support of EO. This should motivate more businesses to invest in green technologies and other cutting-edge ESG-compliant solutions.

It's crucial to recognize the limits of this study, though. The study's narrow emphasis on the Indian environment would limit how broadly its conclusions can be applied, and additional influencing elements might be overlooked. In the future, it will be crucial to replicate this research in various economic and cultural settings and investigate different factors like industry sector or company size [49, 71, 72].

In conclusion, incorporating ESG principles and EO into technological advancement is an intelligent corporate move and a critical step towards building a more just and sustainable world. This study demonstrates that when companies adopt sustainability, they invest in their long-term performance and benefit society.

6.1 The implication of the research

This research can contribute to various sectors. It is helpful for managers and entrepreneurs/ owners and supports policymakers in small industries and the registered or unregistered handicraft industry.

6.2 Implications for theory

Stakeholder theory and the TOE model form the basis for investigating the influence of ESG performance on EP and technological innovation on EP through ESG. This not only enhances the body of theoretical knowledge about the microeconomic effects of ESG but also adds to the body of study on the variables influencing business innovation. The fixed-effect adjustment outperforms the truncation bias in the number of citations [95]. It provides significant implications for future research on enhancing the innovation effects of ESG. It validates the association between ESG and environmental performance, TIN and ESG EO on corporate innovation found in earlier studies employing a better measure of corporate innovation. Even after empirical research, it has been proved that EO has an insignificant and negative impact on CIN [96-98].

This article examines how ESG performance impacts environmental performance and technological innovation from three angles: corporate governance, agency difficulties, and information disclosure. The results support the theory which states that increased social responsibility performance can lessen agency issues and satisfy shareholders' demands for creative endeavours [99]. Furthermore, it has been demonstrated that introducing ESG ratings encourages businesses to enhance internal corporate governance, promote information transparency, and aggressively use corporate innovation to promote sustainable development.

This study also adds to the body of knowledge. Researchers have examined corporate innovation elements such as executive traits, small-scale industry, and especially handicraft industry structure.

6.2.1 Managerial implication

This study has managerial implications; they can make decisions to develop their strategy for the growth of businesses and the welfare of their employees working in the firms. This study also supports the manager to utilise the resources, protect the environment, support society, and help the government in income generation, GDP increases, etc., when the orientation of entrepreneurship is developing in mind with better ESG practices by the support of new technical innovation then craft industry can compete with other manufacture craft product.

6.2.2 Policy implication

This study is helpful for policymakers in predating stratus and robust government schemes for industry support and social income generation, with care of environment protection. Technology development and entrepreneurial orientation also support ESG development in achieving SDGs. It will improve the environmental performance. Policymakers can make policies for the use of systematic data digital technology.

Even this study has focused on critical factors affecting the environmental performance of the handicraft industry, and ESG, EO and TIN support green development to achieve sustainability. However, this is limited and focused only on the handicraft industry, not other sectors. Therefore, there is a need for further study in different sectors. Thus, the researcher can take help from this study and explore their ideas in ESG and innovation development in other manufacturing sectors.

Future work will be favour and support to Digital dynamic capability theory (DDCT) where “Digital Dynamic Capability Theory” (DDCT) supports all capability along with digital Technology and resources such as AI, capacity building, ICT, EO, EL, AC, ML social media, Innovation and digitalisation will support the employee and business also in small industry. This is the extension of dynamic capability theory and will close support to entrepreneurial event model (EEM). So future research will be towards these variables in small industry manufacturing industry service sector Gig economy, where all workers as well as firms will connect and take support of digital technology, artificial technology, innovation and will create new leader in supply chain market at global level.

|

ESG |

Environment, Social and Government |

|

TIN |

Technological Innovation |

|

EO |

Entrepreneurial Orientation |

|

EP |

Environmental Performance |

|

MSME |

Micro, Small, and Medium Enterprises |

|

GDP |

Gross Domestic Product |

|

AVE |

Average Variance Extracted |

|

HTMT |

Heterotrait-Monotrait |

|

DDCT |

Digital Dynamic Capability Theory |

|

PLS-SEM |

Partial Least Square – Structural Equation Modelling |

|

CB-SEM |

Covariance Based Structural Equation Modelling |

|

TOE |

Theory of the Technology Organisation Environment |

|

UNEP-FI |

United Nations Environment Programme Finance Initiative |

|

OECD |

Organisation for Economic Cooperation Development |

|

PRI |

Principles for Responsible Investment |

[1] Magon, A., Kalra, D., Dadwal, S.S. (2018). Understanding E-commerce quality, customer satisfaction, loyalty, and culture moderation: A cross-national study. Journal of Retailing and Consumer Services, 44: 101-117.

[2] Fernandez, I., Junquera, B., Ordiz, M. (2010). Organizational culture and human resources in the environmental issue: A review of the literature. International Journal of Human Resource Management, 14(4): 634-656. https://doi.org/10.1080/0958519032000057628

[3] Yadav, U.S., Yadav, G.P., Tripathi, R. (2023). New sustainable ideas for materialistic solutions of smart city in India: A review from Allahabad city. Materials Today: Proceedings. https://doi.org/10.1016/j.matpr.2023.08.057

[4] Kumar, A., Mandal, M., Yadav, U.S. (2023). Role of women in micro or unorganised entreprises by the use of fin-tech for sustainable development India and effect of digital and financial awareness: Investigation of the Relation with (Utaut) Model. Academy of Marketing Studies Journal, 27(2): 1-10.

[5] Rushita, D., Sood, K., Yadav, U.S. (2023). Cryptocurrency and digital money in the new era. In Digital Transformation, Strategic Resilience, Cyber Security and Risk Management, pp. 179-190. https://doi.org/10.1108/S1569-37592023000111B013

[6] Yadav, U.S., Sood, K., Tripathi, R., Grima, S., Tripathi, M.A. (2023). An analysis of the impact on India's sustainable development resulting from women in small enterprises' fin-tech and financial awareness during COVID-19 using the (UTAUT) model. In Digital Transformation, Strategic Resilience, Cyber Security and Risk Management, pp. 71-85. https://doi.org/10.1108/S1569-37592023000111B005

[7] Kaur, H., Sodhi, D., Aggarwal, R., Yadav, U.S. (2023). Managing human resources in digital marketing. In Digital Transformation, Strategic Resilience, Cyber Security and Risk Management, pp. 155-162. https://doi.org/10.1108/S1569-37592023000111C009

[8] Tripathi, M.A., Tripathi, R., Yadav, U.S. (2022). Prospects of impending digital platform economy: Rise of GIG work. International Journal of Early Childhood Special Education, 14(3). http://doi.org/10.9756/INT-JECSE/V14I3.646

[9] Aureli, S., Magnaghi, E., Salvatori, G. (2020). Does gender matter for corporate sustainability? Corporate Social Responsibility and Environmental Management, 27(1): 166-176.

[10] Shive, S.A., Forster, M.M. (2019). The revival of large corporations and the decline of the labor share in the U.S. Economy. Journal of Financial and Quantitative Analysis, 54(4): 1655-1684.

[11] Galena, A., Lopez, I., Rodriguez, L. (2008). Social information transparency: A critical factor in improving social responsibility. Business Ethics: A European Review, 17(4): 379-392. https://doi.org/10.1016/j.ecolecon.2013.04.009

[12] Yadav, U.S., Tripathi, R., Tripathi, M.A. (2022). The adverse impact of lockdown during COVID-19 pandemic on micro-small and medium enterprises (Indian handicraft sector): A study on highlighted exit strategies and essential determinants. Future Business Journal, 8(1): 1-10. https://doi.org/10.1186/s43093-022-00166-0

[13] Jung, J.H., Chowdhury, I., Wu, A. (2020). The role of sense of mission within the interaction of the founder's human capital, social capital and new technology ventures' performance. Journal of Business Venturing, 35(5): 106006.

[14] Yadav, N., Yadav, U.S., Singh, A.B., Yadav, G. (2022). Antecedents and consequences of public interest litigations in sustainable environment protection in India. In IOP Conference Series: Earth and Environmental Science, 1057(1): 012004.

[15] Hisellini, P., Scarfato, A., Petrillo, A. (2018). Towards zero energy-smart buildings: A literature review. Renewable and Sustainable Energy Reviews, 94: 551-563.

[16] Soewarno, N. (2019). Environmental, social, and governance (ESG) and financial performance: A literature review. Journal of Sustainable Finance & Investment, 9(1): 1-13.

[17] Hair Jr, J.F., Sarstedt, M., Ringle, C.M., Gudergan, S.P. (2023). Advanced Issues in Partial Least Squares Structural Equation Modeling. Sage Publications.

[18] Ingley, C.B., Van Der Walt, N.T. (2004). Corporate governance, institutional investors and conflicts of interest. Corporate Governance: An International Review, 12(4): 534-551. https://doi.org/10.1111/j.1467-8683.2004.00392.x

[19] Yadav, U.S., Tripathi, R., Tripathi, M.A. (2023). Adverse impact of lockdown during the COVID-19 pandemic on MSME (Especially the Indian handicraft sector): A study on highlighted exit strategies and important determinants. Vision, Article Number: 09722629231172570. https://doi.org/10.1177/09722629231172570

[20] Alkaraan, F., Albitar, K., Hussainey, K., Venkatesh, V.G. (2022). Corporate transformation toward Industry 4.0 and financial performance: The influence of environmental, social, and governance (ESG). Technological Forecasting and Social Change, 175: 121423. https://doi.org/10.1016/j.techfore.2021.121423

[21] Suttipun, M., Yordudom, T. (2022). Impact of environmental, social and governance disclosures on market reaction: An evidence of top50 companies listed from Thailand. Journal of Financial Reporting and Accounting, 20(3/4): 753-767. https://doi.org/10.1108/JFRA-12-2020-0377

[22] Bodhanwala, S., Bodhanwala, R. (2018). Does corporate sustainability impact firm profitability? Evidence from India. Management Decision, 56(8): 1734-1747. https://doi.org/10.1108/MD-04-2017-0381

[23] Kumar, A., Mandal, M., Yadav, U.S. (2022). Motivation and challenges in career choice and well being of women entrepreneurs; Experiences of small businesses of lucknow, uttar pradesh. Journal of Positive School Psychology, 6(4): 10890-10906.

[24] Reboredo, J.C., Sowaity, S.M. (2021). Environmental, social, and governance information disclosure and intellectual capital efficiency in Jordanian listed firms. Sustainability, 14(1): 115. https://doi.org/10.3390/su14010115

[25] Yadav, U.S., Sood, K., Tripathi, R., Grima, S., Tripathi, M.A. (2023). An analysis of the impact on india's sustainable development resulting from women in small enterprises' fin-tech and financial awareness during COVID-19 using the (UTAUT) model. In Digital Transformation, Strategic Resilience, Cyber Security and Risk Management, pp. 71-85. https://doi.org/10.1108/S1569-37592023000111B005

[26] Hair, J.F., Ringle, C.M., Sarstedt, M. (2012). Partial least squares: The better approach to structural equation modeling? Long Range Planning, 45(5-6): 312-319. https://doi.org/10.1016/j.lrp.2012.09.011

[27] Beretta, V., Demartini, C., Trucco, S. (2019). Does environmental, social and governance performance influence intellectual capital disclosure tone in integrated reporting? Journal of Intellectual Capital, 20(1): 100-124. https://doi.org/10.1108/JIC-02-2018-0049

[28] Bolis, I., Morioka, S.N., Sznelwar, L.I. (2014). When sustainable development risks losing its meaning. Delimiting the concept with a comprehensive literature review and a conceptual model. Journal of Cleaner Production, 83: 7-20. https://doi.org/10.1016/j.jclepro.2014.06.041

[29] Krolikowski, M., Yuan, X. (2017). Friend or foe: Customer-supplier relationships and innovation. Journal of Business Research, 78: 53-68. https://doi.org/10.1016/j.jbusres.2017.04.023

[30] Sarfraz, M., Ozturk, I., Yoo, S., Raza, M.A., Han, H. (2023). Toward a new understanding of environmental and financial performance through corporate social responsibility, green innovation, and sustainable development. Humanities and Social Sciences Communications, 10(1): 1-17. https://doi.org/10.1057/s41599-023-01799-4

[31] Donaldson, T., Preston, L.E. (1995). The stakeholder theory of the corporation: Concepts, evidence, and implications. Academy of Management Review, 20(1): 65-91. https://doi.org/10.5465/amr.1995.9503271992

[32] Alabi, A. (2022). ESG practices, technological innovation and environmental performance: Evidence from Nigeria. International Journal of Sustainable Development & World Ecology, 29(1): 1-11.

[33] Alkaraan, F., Albitar, K., Hussainey, K., Venkatesh, V.G. (2022). Corporate transformation toward Industry 4.0 and financial performance: The influence of environmental, social, and governance (ESG). Technological Forecasting and Social Change, 175: 121423. https://doi.org/10.1016/j.techfore.2021.121423

[34] Henseler, J., Sarstedt, M. (2013). Goodness-of-fit indices for partial least squares path modeling. Computational Statistics, 28: 565-580. https://doi.org/10.1007/s00180-012-0317-1

[35] Duan, J., Zhuang, X. (2021). Financial investment behavior and enterprise technological innovation: Motivation analysis and empirical evidence. China Industrial Economics, 1: 155-173.

[36] Atif, M., Ali, S. (2021). Environmental, social and governance disclosure and default risk. Business Strategy and the Environment, 30(8): 3937-3959. https://doi.org/10.1002/bse.2850