Tatyana Kovshova*![]() | Abilmazhin Ayulov

| Abilmazhin Ayulov![]() | Oksana Lomakina

| Oksana Lomakina![]() | Artem Smirnov

| Artem Smirnov![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The development of venture capital in the post-Soviet countries has features of its historical formation. This field of activity is relatively new in the region, although it has deep roots in the history of such developed economies as the United States, the European Space, and Japan. However, the relevance of the research lies in the study of this phenomenon in the region of Central Europe, Asia, and the Caucasus. The paper aims to assess the benefits, risks, and prospects associated with venture capital in the post-Soviet space. The methods and materials used in the study included statistical material processed with statistical programs (SPSS) and mathematical modeling of forecasting results; calculations of economic indicators (ROE, IRR) and the level and required size of venture capital for business development; and the consideration of hypothetical situational models and the level and number of innovations. The chaotic and unstable development of the economic state of the EECCA countries creates various contradictions. Nevertheless, the study confirms the need for venture capital as a driving factor in the development of these economies. This research also covered such categories as crowdfunding and angel investors at the initial stages, even before venture investment. The results of the study find practical applications in stimulating business organizations that, for various reasons, search for new business methods. Venture organizations encourage entrepreneurs to open new business units to solve existing problems in society and various spheres of its functioning. These also organizations motivate investors to promote innovative enterprises in the developing economies of the studied region.

business angels, crowdfunding, diversification, foreign direct investment, post-Soviet states, profitability, return on investment

Venture capital is a component of the successful development of new business organizations. Today, it is the most important aspect in the studies and detailed analyses of developing countries, such as EECCA (Eastern Europe, Caucasus and Central Asia regions). Typically, venture capital implies the investments of interested parties in the form of banks, foundations, and private and public investments for the development of business organizations at various levels of their activities [1]. Venture capital is not always monetary, it can also be managerial or technical. For most investors, venture capital investments involve great risks. According to statistics, the payback of these investments is only about twenty percent [2]. However, the financial size of investments tends to increase. The diversification of venture capital investment sites is also growing [2].

To better understand the concept of venture capital, it is now necessary to study its origins. In one form or another, venture capital and venture funds existed in all developed economies. However, as a concept, venture capital first originated in the USA. Back in the 1945-50s, the USA corporations made the first attempt to research and further invest in small businesses [3]. This period underlined the development of venture capitalism [4]. Indeed, the process of forming a new financial institution developed in leaps and bounds. However, technological progress and innovations contributed to rapid turnovers after the devastating consequences of the Second World War. At the same time, venture capital allowed for the development of such well-known organizations as Xerox, Apple, Yahoo (which also bought the Summly app from the youngest recipient of venture investments, Nick D'Aloisio, Compaq, Microsoft, Amazon, Cisco, Genentech, Federal Express, and other modern giants. The emergence of venture capital was a painful process for many conglomerates already existing in the country since the late 19th century. At the end of the 80s of the 20th century, venture capital experienced a sharp jump (boom) in its development history. Consequently, this phenomenon has made irreversible changes not only in economic development but also in public consciousness and the social sphere [5].

Venture capital in post-Soviet countries was initially represented by external investments in undervalued areas of the economy or transit opportunities, since the technical and scientific remains did not allow classical venture investment. The formation of large national capital in the EECCA countries led to the emergence of domestic venture investment [6]. The amount of direct investment in this region remained noticeably lower compared to Europe or even Latin America. These were mainly investments in commodity markets and transit potential [7]. In 2000s, venture capital was formed in the region as a form of medium-term investment in promising entrepreneurial projects in the hope of faster high profits. Most often, for this purpose, small, specialized venture companies are created that are part of the ecosystems of large enterprises or financial holdings [7].

In post-Soviet countries, other forms of investment similar to venture capital also developed. Angel investors offer their personal funds in exchange for a share in a promising startup and can also offer their own mentoring and expertise for its development. In most post-Soviet countries in the region, such methods could be used back in the 90s of the 20th century, but more often for additional control of the investor over his money and the real operational activities of a young company. Since we are talking about private funds from investors, it is very difficult to assess the volume and real impact of this type of investment on business development. Obviously, it is small [7].

Crowdfunding was used to a greater extent during the initial capital accumulation stage to create first entrepreneurial solutions when other sources of financing were problematic. Now this form is becoming increasingly popular thanks to the technical support of online platforms. It should be noted that there are very few studies on the history and influence of venture investment capital in the countries of the region under study, and reliable data on the activities of related businesses, unlike Western countries, are not readily available, which forces one to turn to the study of more general economic indicators.

The relevance of the research lies in the need to determine the risks and benefits of venture capital development. To this end, the study analyzes various assumptions and mathematical calculations of statistical data. Thus, the study determines the effectiveness of venture capital for the development of various spheres of modern society. As for the scientific novelty, the research identifies modern ways of using venture capital in the context of the digital transformation of society.

1.1 Literature review

The model of venture capital development in the USA became a basic example for the developing and developed economies of the world [8]. After the 1990s, venture capital began to develop in Russia, Kazakhstan, China, India, and a little earlier in the EU. As a result, the economies of these countries expanded in terms of small businesses and new startups [9]. This time entailed instability of the economic system and, accordingly, instability in business development. As a direct investment, venture capital was the most operational means of direct assistance to companies [3]. It was the most effective tool in many countries during the active transformation of both the economic system and society as a whole [10]. For developing countries, which are the EECCA countries (in particular Central Asia and the Caucasus) with great potential in economic development, venture capitalization develops slowly [11]. Nevertheless, there are new achievements, including new legislation regarding intellectual property, innovation centers, and venture funds aimed at direct investment [12]. In this regard, an example can be the case of the Republic of Kazakhstan, where the development of venture institutions is under the direct control of President K. Tokayev. As he stated at the Digital Bridge International Forum (Astana, October 2023), "Kazakhstan is consistently improving the institutional and legislative framework to stimulate investment in startups. We are pleased to have recorded a doubling of the average size of venture capital deals last year. At the same time, our regulatory framework needs to be aligned with best practices implemented in the USA, Singapore, and Hong Kong. It is also important to attract international players to our venture capital market" [13].

In the historical perspective of venture capital development in the post-Soviet space, there are several significant aspects. After all, the problems of the post-Soviet space in the transition from socialism to capitalism included complex and multifaceted issues. This process was fundamentally different from the initial venture capital development in the USA. Thus, the transition from a planned economy to a market economy was challenging. Many post-Soviet countries (former USSR countries) have faced the inefficiency of state-owned enterprises, inflation, and other economic problems. Therefore, the current task of venture capital in the region is to stimulate innovation and support those new enterprises, which are extremely necessary. In addition, in this region, venture capital can contribute to entrepreneurial activity and the creation of innovative companies. It provides financial support to startups and young enterprises that may face difficulties in obtaining traditional loans. Venture capital fosters the development of high-tech sectors of the economy, thereby improving the competitiveness of the country. However, due to the peculiarities of its formation, the domestic market in post-Soviet countries may not be as developed as in more developed economies. This feature may complicate the process of finding investors and clients for startups. In this regard, regulatory and institutional aspects are crucial. Effective regulation and government support can considerably improve venture capital. This support can include a favorable environment for investment, improvements in the legal system, intellectual property protection, and measures against bureaucratic barriers.

In the context of the EECCA countries, venture capital took its forms in conditions of predominantly high corruption and high tax pressure on business. A number of major economic shocks in 1998, 2008, the implementation of several large “bubbles” in the real estate markets, Internet companies led to instability in economic development. The high level of populism and the paternalistic nature of state policy in most countries of the region, including Russia, created conditions for the draining of funds from high-tech industries with delayed production. Often, venture investments in this context were used as one of the means of tax optimization [14].

For a deep understanding of venture capital, it is necessary to understand its phases (stages) of development [15]. The seed stage is typically the start of the development and creation of an organization. The following stage is the so-called startup stage. It encompasses the development of the main activity direction and the creation of a working staff for the implementation of its specific (or general) idea [16]. Further developing, the organization creates a product (technology, service, or product). This period is an early stage followed by an expansion stage. The latter is one of the most important in terms of visibility since the organization begins to offer its goods on the market [17]. The final stage is the creation of sale instruments using a public offer (IPO) or interim financing [18]. In the final phase, new organizations that have used venture capital may no longer need additional financial resources due to the funds received during the sale of shares [19].

Venture capital in the EECCA countries mainly focuses on the developing sector of startups that experience a turbulent time in the context of digital transformation [20]. Venture capital is designed for the 5-10-year development cycle of the main areas represented in developing economies [21]. Examples of these areas are tourism services and hotel business, political and non-governmental organizations (addressing human rights, gender equality, and other socio-economic aspects), the technological sphere, and industrial development (in particular, agro-industry and animal husbandry) [22, 23]. Basically, venture capital focuses on human abilities. It serves as a stimulating factor for generating ideas in the EECCA region, which has a huge potential for development [24]. In particular, it is worth noting venture capital development in environmental protection and a green economy system in the region, as well as at the global level [25]. In addition, during the COVID-19 pandemic, venture capital was crucial in certain areas of social activities [26], such as health and environmental protection [27].

In most cases in the countries of the studied region, venture investments are an area of stimulating small startups in areas where very rapid capitalization is possible or expected, for example, IT, AI. Despite the larger number of startups being invested, only a few achieve success and capitalization. A striking example of successful venture investment is the global company Grammarly, created in Ukraine, which provides services to improve writing, spelling, etc. online. Perfumery and cosmetics factory "Ural Gems" (Russia), which, with the help of a venture investor, was able to overcome strong international competition.

This study attempts to fill the scientific gap in research into the main risks and benefits of venture capital in the developing economy of the post-Soviet space. The paper supports its conclusions with quantitative and qualitative empirical data. The purpose of the study is to describe the prospects for venture capital development in the post-Soviet space and EECCA. The research objectives are hypothetical analyses of modeled situations that may result from the activities of a venture organization (the introduction of venture capital) on the territory of the EECCA region (and post-Soviet countries).

2.1 Research hypotheses

In the course of the study, it was necessary to develop hypotheses (H) that could justify (or vice versa) the use of venture capital in the post-Soviet countries. These hypotheses addressed the processes taking place in the developing economies of the studied region and the importance of direct investment in the development of a particular sphere.

H1 suggests that venture capital is necessary for the development of startups and innovative enterprises in the EECCA region.

H2 refers to the fact that the role of venture capital is not as important as the role of business angels or crowdfunding, which fill the financial gap between venture investments and their financing.

H3 refers to the assumption that venture capital does not justify its purpose for the region and cannot contribute to its further development.

2.2 Research design

The research sample included the countries of the EECCA region and the post-Soviet space, such as Kazakhstan, Tajikistan, Armenia, Georgia, Azerbaijan, Kyrgyzstan, Ukraine, Moldova, Belarus, Russia, China and some others. The study used data from various companies (venture funds) operating in the countries for more than 10 years, as well as data from newly formed ones. The sample rested on such parameters as the level of innovative organizations (the growth of their number); the number of startups that depend on venture capital; the number of products (goods, services); the number of economic development indicators (such as ROE, IRR) depending on the region; and other parameters obtained through mathematical and economic calculation of efficiency, optimal financing, correlation with errors, etc. [28]. The calculations for the sample covered a period of more than 10 years (12 years) for accurate data analysis and obtaining correct results. The data set was calculated in stages for a period of up to five years. Aggregated indicators were calculated for each year, as well as for every five and ten years, followed by a current calculation for the year. The data processing involved the database of the computer program, which processed the obtained data (AMOS24) [29].

Arrays for the analysis of the investment period and investment quantity were data from WorldBankOpenData, IMFData, Quandl, marketing and sociological research in Forbes, and AEA (AmericanEconomicAssociation). The parameters of presenting and calculating the data in the tables and graphs were the amount of venture capital in certain periods (up to 12 years), expressed in standard units. Further, the study used statistical indicators processed in AMOS24, the indicators of innovative business development in the regions, and the relevant economic parameters for determining profitability and profitability from the investment. The data covered a period exceeding a decade (twelve years) to form a statistical relationship and obtain more accurate quantitative information.

2.3 Sample

The study applied a thorough analysis of co-investment based on the calculation of the Internal Return Rate (IRR). The research methods included the calculations of sales growth indicators, ROE, market share, earnings rate, and innovation effectiveness rates. These indicators determine whether the introduction and use of venture capital were correct. The statistical data that served as the basis for the calculation were processed in SPSS/Amos-24. The basis for statistical data and further calculations were the data from Flint, iTech, RedSeed, RunaCapital, RBK, EagleKazakhstanFund, SilkRoadFundAIG, UzVc, SemurgVC, RT Assistance Fund, RedSharksVentures, UltimateCapital, Microsoft (Armenia), Cisco, Siemens (with representative offices in the studied region), Founder Institute, and an accelerator Orion Worldwide Innovations. The sample rested on data from open information and statistical sources of official digital resources (IMF, UNECE, Environment EU). The parameters of the analysis were the innovative development level, the number of innovative organizations, the income level, the percentage of innovations, economic indicators IRR, ROE, and others. The data covered a period of up to 12 years (from 2011 to 2022).

2.4 Intervention

Before calculating the data, it is necessary to determine the venture capital that has already been redistributed (or will be redistributed) in a particular region:

Venture capital=total investments amount in the period T/total number of operation organizations in period Y (1)

At the same time, the study tests the hypotheses (H1, H2, H3). If the ways of applying venture capital are determined, the hypotheses will be considered as factors of further business development in the EECCA region.

2.5 Statistical analysis

Further testing of the hypotheses implied the comparison of venture capital indicators depending on the region. This stage allowed for assessing the effectiveness of aggregated economic indicators (H1):

$\gamma_a+\gamma_b=1$ (1)

where, Y is the total income.

However, it is also necessary to calculate an aggregated economic indicator. It can act as an average link when calculating the price of venture capital required to finance a business in the region.

$\left(\partial_a \partial_b\right)=\operatorname{argmax}(\mathrm{Y})=\alpha \beta\left(\gamma_a+\gamma_b\right)$ (2)

To simplify visualization, aggregated indicators can be substituted with yi(which is equal to $\partial_a \partial_b$) and f(vi) equal to ($\gamma_a+\gamma_b$). Venture capital can be denoted by a conditional unit K:

$K=\mathrm{f}(\mathrm{vi})-\mathrm{yi}$ (3)

Accordingly, to determine the most profitable region for investment, it is necessary to make a calculation according to the formula:

$y_i=f^{\prime}\left(v_i\right)-K$ (4)

For testing (H2), another indicator is calculated. It determines the return on investment:

$R O E=\frac{ { NetIncome }}{{ OwnCapital }}$ (5)

In this calculation, equity value often coincides with K. This coincidence indicates the right direction for investing. The next step is the calculation of the internal return rate. This indicator is closely related to the NPV indicator by an inversely proportional relationship. Only when reaching zero, it shows the required level:

$\sum_{i=1}^N \frac{C F_i}{(1+d)^i}=0$ (6)

When calculating these indicators for testing (H3), it is necessary to analyze the effectiveness of venture capital by calculating the effectiveness of innovation.

$\begin{aligned} { Innovation\,\,Rate } & =100 \% * \frac{{ revenue\,\,share\,\,of\,\,innovations }}{ { total\,\,revemue }}\end{aligned}$ (7)

For the subsequent analysis of the performed calculation, the data are examined according to the formula:

$\begin{aligned} & { Innovation\,\,Ration } =\frac{ { Number\,\,of\,\,Innovations }}{ { Number\,\,of\,\,products }} * 100 \%\end{aligned}$ (8)

At the same time, the readings of formulas can greatly vary depending on the region of their research and testing. To test the third hypothesis (H3) and conduct a correlation analysis, the study used the following formula:

$\operatorname{corr}(\mathrm{X}, \mathrm{Y})=\operatorname{corr}(\mathrm{a} 0+\mathrm{a} 1 \mathrm{X}, \mathrm{b} 0+\mathrm{b} 1 \mathrm{Y}), \mathrm{a} 1, \mathrm{~b} 1=0$. (9)

At this stage, the study searches for a correlation between the tested variables that are interdependent in this aspect of venture capital development.

2.6 Research limitations

The problems with applying the research methods concerned the use of statistical data. Due to its diversity, it was difficult to find any identical signs for investing and applying venture capital to another similar organization. Although the economy in the post-Soviet countries is rapidly developing, it remains less developed compared with Western countries. Therefore, only some processes can proceed automatically, according to a pre-calculated condition. Many processes are chaotic. The legislation does not provide for the encouragement of small startups. At this stage of development, organizations largely rely on business angels. It is challenging to trace their permanent activities and put them under any conditional framework. In this regard, business angels fill the financial gap that business structures need before directly obtaining venture capital. These gaps prevent the research from covering all innovative startups to see the picture of venture capital development more clearly.

The applied methodology allowed for testing the hypotheses that suggested different ways of developing venture capital in the region. It was possible to reveal the most applicable hypothesis among the proposed ones. At the same time, venture capital was calculated. The calculations of aggregated economic indicators determined the effectiveness of venture capital. The parameters that were essential for calculations and obtaining results relate to digital data reflected in standard units. These parameters included the period (of investment), the amount of investment, and venture capital. Table 1 shows the results of the mathematical calculations. It presents venture capital data expressed in standard units. Venture capital data was constantly changing due to the growing need for business development in the emerging economies of the studied countries. The investment period, expressed in years, served as the basis of calculations. This indicator is crucial for the compilation of analytical data expressed in graphical form. It shows sequentially considered years to reflect the processes that took place in the considered period. The basis for the calculation was the invested amount expressed in standard units. This amount reflected the venture capital allocated to finance innovative enterprises and startups of various directions. Aggregated indicators $y_a, y_b, \partial_a \partial_b$ were directly used to analyze the main indicators of investment capital, investment period, and venture capital, with correlation for statistical errors.

The data sources on current aggregated indicators were open digital resources of EU websites in the field of ecology and socio-economic development. Mathematical operations and formulas revealed that the indicators of venture capital grow over time. This fact indicates that the H1 hypothesis is relevant, excluding the other assumptions. The period of 12 years more clearly showed the dynamics of venture capital development during a certain period. Only a period of more than 5 years would reveal the long-term prospects for development and identify a certain pattern according to five or seven-year business development cycles. Therefore, it was reasonable to choose this period for the study.

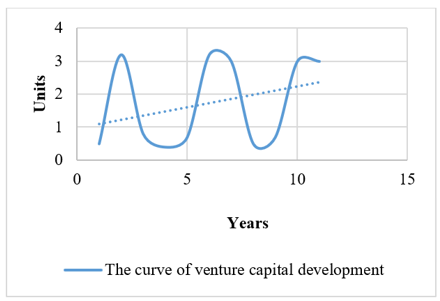

As can be seen, venture capital indicators increased from 0.08 to 1.13 with time (from the 1st to the 12th year). Aggregated indicators of economic efficiency in connection with the growth of venture capital showed different abrupt values of growth and decline. Thus, for example, there was growth from 0.02 to 0.03, a decline from 0.03 to 0.021, then the indicators rose to 0.6 again, fell to 0.45, and experienced the subsequent resulting rise to 0.87. In turn, the inverse indicators of venture capital’s inability to develop in the studied region, respectively, decreased (from 0.98 to 0.13). The aggregated performance indicator, depending on the number of periods and the regional coefficient of venture capital activity, showed different values. These variations were due to the differences in the economic condition of the EECCA countries. Nevertheless, the indicator showed constant average values of about 150 units. The indicator did not show a strong spread of data from the median, indicating the safe development of venture capital with the least amount of risky investments. This factor confirms the first hypothesis (H1), rejecting the third assumption (H3). When visualizing K according to the derivative function of the aggregated indicators, one can obtain the following graph of venture capital development depending on the years of operation (Figure 1).

This graph shows that the development of venture capital takes place in leaps and bounds. In one segment, there is a rise in development, in the second and fourth segments, there is a decline. Some segments represent a constant peak point in the decline or the rise in venture capital development. These segments confirm the hypothesis (H2). Business angels become necessary to support the development of enterprises (in particular, startups and innovative enterprises). The OY axis shows values of $f^{\prime}\left(v_i\right)$ expressed in units. The OX axis shows $y_i$ expressed in units of time. The indicators show a smooth rise to 3.5 units, then drop to 0.5 units. The indicators repeat their cycle of decline and rise along the sinusoid.

Figure 1. The dependence of the venture capital development indicator on the period of business operation (years)

Source: developed by the author

The next step is to confirm the hypothesis (H3), which assumes the inefficiency of venture capital development with direct investments in the business environment of developing countries. In this case, it is necessary to calculate the return on direct investment and the ratio of innovative enterprises (quantity and productivity). Table 2 shows calculations based on statistical data, which indicate that the third hypothesis was not reflected in practical data.

Table 1. The dependence of venture capital on aggregated economic indicators

|

Venture Capital, Standard Units |

Investment Period, T, Years |

Inv. Amount, Y, Standard Units |

$y_a$ , Units |

$y_b$ , Units |

$\partial_a \partial_b$, Units |

|

0.08117 |

1 |

12.32 |

0.02 |

0.98 |

147.84 |

|

0.17841 |

2 |

11.21 |

0.01 |

0.99 |

134.52 |

|

0.13857 |

3 |

21.65 |

0.03 |

0.97 |

259.8 |

|

0.03247 |

4 |

123.2 |

0.021 |

0.979 |

1478.4 |

|

0.41632 |

5 |

12.01 |

0.034 |

0.966 |

144.12 |

|

0.41322 |

6 |

14.52 |

0.45 |

0.55 |

174.24 |

|

0.6917 |

7 |

10.12 |

0.61 |

0.39 |

121.44 |

|

0.4902 |

8 |

16.32 |

0.21 |

0.79 |

195.84 |

|

0.5291 |

9 |

17.01 |

0.32 |

0.68 |

204.12 |

|

0.73855 |

10 |

13.54 |

0.45 |

0.55 |

162.48 |

|

0.99909 |

11 |

11.01 |

0.65 |

0.35 |

132.12 |

|

1.13852 |

12 |

10.54 |

0.87 |

0.13 |

126.48 |

Source: developed by the author

Table 2. The ratio of the economic indicators in innovative enterprises of the post-Soviet countries

|

ROE |

IRR |

Innovation Rate |

Revenue Share of Innovations |

Total Revenue |

Number of Innovations |

Number of Products |

Innovation Ration |

|

0.02 |

0.01 |

0.00187 |

0.21 |

112.3 |

135.54 |

220.2 |

0.61553 |

|

0.085 |

0.02 |

0.00165 |

0.365 |

221.3 |

178.21 |

245.3 |

0.7265 |

|

0.087 |

0.03 |

0.00241 |

0.54 |

224.2 |

179.32 |

324.2 |

0.55312 |

|

0.097 |

0.034 |

0.00191 |

0.64 |

335.6 |

181.25 |

326.4 |

0.5553 |

|

0.12 |

0.05 |

0.0022 |

0.74 |

337.12 |

182.2 |

451.03 |

0.40396 |

|

0.16 |

0.06 |

0.00095 |

0.325 |

341.2 |

184.5 |

532.1 |

0.34674 |

|

0.16 |

0.07 |

0.00154 |

0.546 |

354.2 |

186.2 |

534.2 |

0.34856 |

|

0.15 |

0.0745 |

0.0026 |

0.94 |

361.2 |

189.3 |

621.45 |

0.30461 |

|

0.174 |

0.079 |

0.00114 |

0.478 |

421.1 |

189.9 |

632.22 |

0.30037 |

|

0.0181 |

0.0765 |

0.00124 |

0.65 |

526.2 |

191.2 |

745.56 |

0.25645 |

|

0.183 |

0.08 |

0.001 |

0.78 |

784.2 |

192.5 |

854.67 |

0.22523 |

|

0.198 |

0.091 |

0.00115 |

0.96 |

836.3 |

195.5 |

956.23 |

0.20445 |

Source: developed by the author

This table provides statistical data from the economic sphere calculated using the SPSS program in the EECCA region. It presents the values of the internal return on venture capital, the return on venture capital, as well as the norms of investment in innovative enterprises for their effective operation. As the calculations show, with an increase in the ROE indicator, the IRR value similarly increases (from 0.02 to 0.198, and 0.01 to 0.091, respectively). The increase in these indicators refers to percentage indicators, such as the level of innovation. The latter similarly grows, although at a small pace and rather abruptly (from 0.001 to 0.002, and again to 0.001). Therefore, this indicator shows that this area in developing economies needs financing and investment. It has stable development dynamics, but there is no sharp growth. It is obvious in the indicators of Innovation Ration, which falls in its percentages (from 0.6 to 0.2). Accordingly, venture capital is often insufficient for the development of startups, causing the need for business angels. Thus, the study confirms the second hypothesis (H2) about the need to develop the institute of business angels at a certain development stage of innovative enterprises. Indeed, these indicators may confirm the third hypothesis (H3). However, due to the difficulties in collecting the necessary statistical information in the developing economic segment of the region, an unambiguous conclusion is impossible. In this case, a correlation is possible between the venture capital development pace and the ability to target it with the countries of the post-Soviet space. In addition, the remaining indicators of economic growth, as well as economic activity (in the form of ROE, IRR, NPV), characterizing the development processes, continue to increase. These factors refute the hypothesis (H3). Figure 2 illustrates a comparative analysis of the economic development indicators of innovative startups, namely, the correlation between the rate and their rations.

Figure 2. The dependence of the percentage ratio of business effectiveness on the number of innovative organizations

Source: developed by the author

The graph shows how the indicators, despite some declines, still tend to increase. Thus, the OX axis shows the number of prospective operating enterprises, expressed in quantitative units (numbers). The OY axis shows the estimated percentage of effective startups. There are three main economic indicators highlighted in different colors for ease of perception. At the same time, it is noticeable that all three indicators characterize one pattern – they rise in their values over time. There were some sharp declines in ROE and IRR, caused by economic crises in the economy of the post-Soviet space, as well as the coronavirus pandemic. However, after the economy came to a state of stability, the indicators again began to show increasing values on the graph. It is necessary to note some moments of decline from 4.5% to 1.5% on the IRR graph, as well as a decline from 4.5% to 2.5% on the ROE graph. Nevertheless, the indicator of innovation growth is increasing, first showing a constant value, and then growing from 2% to 5%.

Based on the foregoing, it can be assumed that if the pandemic crisis was a general phenomenon, then other crisis phenomena in post-Soviet countries are largely due to problems in economic administration. Venture capital is rapidly developing due to the rapid growth of the innovation rate, leading to an increase in ROI. From a political point of view, the states of the region should optimize venture capital as much as possible with the help of tax mechanisms, but at the same time promote a more uniform attraction of such capital in various sectors of the economy, and not just the traditionally most profitable ones. Limits to natural growth in raw materials, transport, etc. sectors may lead to new economic problems.

The obtained results indicate that innovative and new economies and enterprises develop at an accelerated pace in the EECCA region [30, 31]. At the same time, the difficulties in achieving possible effects at the proper level of internationalization necessitate investments and funding for organizations in this field [32]. Typically, venture capital acts as such investments (direct investments) [33, 34]. Due to the development of venture capital in the studied region, a country becomes competitive in the international arena. It can also contribute to solving problems related to climate change, environmental and social challenges, and healthcare [35].

Venture capital is a prerequisite for business development, especially in fast-growing economies [36]. As the results show, the sphere of startups and innovative enterprises is rapidly developing in some regions [37]. However, these startups are often underestimated and recognized as risky investments [38]. Nevertheless, due to its nature, venture capital (with the help of venture organizations engaged in a particular field) is still invested in business [39]. Venture funds support the economies of developing countries and, at the same time, stimulate existing or newly formed businesses. These funds conduct the calculations aimed at support and assistance [40]. Frequently, for instance, in Kazakhstan, venture funds involve the participation of businesses and relevant ministries as public-private partnerships. Thus, business attracts money to venture funds, and the state creates appropriate conditions for its work and provides certain guarantees [41]. The obtained results emphasized this aspect and confirmed the first hypothesis (H1) that venture capital is necessary for the development of the EECCA region [42]. Venture capital fosters the development of non-governmental organizations engaged in activities that are new in this region, (and, therefore, are not of interest to the population or other circles), environmental protection, and other spheres [43].

The value of developments in the conducted research lies in the analysis of benefits from venture capital in countries with developing economies. In particular, some results of the study are extremely important. These results indicate the need to use venture capital during the development of digital technologies when innovative areas of economic and technological development become crucial.

Currently, venture capital often occurs to be designed for a larger amount of funding than a startup organization requires [44]. These situations contribute to other niches of financing, including crowdfunding and investments by business angels [45]. Indeed, each of these methods entails certain challenges [46]. These challenges include insufficient experience base, high liquidity risk, uncertainty when choosing an investment object, possible risk of plagiarism, and other difficulties [47]. The development of digital technologies and platforms has considerably facilitated the functioning of this approach in business [48]. Blockchain technologies and the transparency of many transactions had the most significant effects [49]. The second hypothesis of the study (H2) referred to the development of crowdfunding and the activities of business angels in the developing countries of the post-Soviet space [50]. That is, these methods of financing fill the niche formed before venture financing [51]. These methods, among other things, contribute to the development of venture capital in the EECCA region [35]. Alternative ways of investing in the economic sector are necessary for the formation and functioning of startups and enterprises with innovative products (services). These types of financing support these organizations until they can use venture capital [52]. According to the results of the study, this field currently shows increasing economic indicators in terms of profitability, internal rate of return, and prospects for venture investment [53].

However, there are certain risks associated with the activities of organizations in need of venture financing. This aspect revealed the weak side of the study, such as difficulties in calculating and determining the occurrence time of risky cases. Thus, the considered methods calculate only hypothetical models of using venture capital for resolving important issues related to some innovative areas of society in a region with a developing economy. These methods poorly account for force majeure situations. The risks include instability in the economic system and unforeseen problems with innovative organizations in an unpredictable business sphere. In addition, another risk for venture capital is that the investments may not be realized for a long time before the venture organization reaches the IPO. The results of research by Facebook, Apple, Xerox, and other well-known companies revealed the prospects of using venture capital long before these organizations reached the IPO level. In these cases, venture capital brings investors income that is many times higher than the initial investment [54].

The risks associated with venture capital development also lie in the inappropriate spending of financial resources on organizations that are not a priority for a particular region. The study of the third hypothesis (H3) confirmed this fact. In this case, the indicators of economic efficiency and expediency of projects and businesses began to fall. The works on venture capital describe the principles of how investment processes develop in stages. However, in practice, according to the results of the study, the conclusions are rather contradictory [55]. Mathematical calculations and statistical data often fail to forecast the economic processes in developing countries. Consequently, it is difficult to accurately predict how venture capital will develop in the studied region in conditions of instability. It is also challenging to forecast the reverse process of the risks that may hinder the development of venture capital. Nevertheless, this study significantly differs from the previous ones. It assumes that forecasting and assessing the prospects for venture capital development may show an approximate framework that helps to assess the situation with the greatest probability. According to the results, the venture capital development market (as well as crowdfunding and business angels) has obvious benefits for the development of the region and, therefore, is promising.

Currently, venture capital focuses not only on technological areas, as it used to do. Now, venture capital aims to support various fields related to diverse business activities. Throughout its development, venture capital helps mature organizations issue securities on the market (IPO). After its final prerequisite for use is achieved, venture capital is subject to diversification. This approach allows venture capital to develop further over a period most often covering from 5 to 10 years, with the addition or reduction of up to 3 years.

In the post-Soviet space, with the formation of a new economic system with a rapidly developing digital market of the latest technologies, venture capital begins to occupy new positions. It is a direct investment in areas that are too risky for public or private financing. However, according to this study, despite the risks of venture capital development in the EECCA region (such as the extremely unstable development and unpredictable economic system), it has some advantages and prospects in development. Venture capital provides benefits through new opportunities in the development of social, economic, environmental, and other spheres. The study concludes that venture capital cannot develop and contribute to the development of some startups due to the chaotic processes that are almost impossible to systematize to predict future development. At the same time, this paradox of contradictions is a prerequisite for the development of the entire economic system, which depends on new promising business units. In the future, such approaches as crowdfunding and financing from business angels will develop venture capital at the seed stage. Thus, the general trend in venture capital development in the region is a promising direction for maintaining the economic system.

The practical application of venture capital occurs in venture companies. These companies use material incentives to stimulate capable entrepreneurs to show a creative approach to finding new ways to solve existing problems in various spheres of society. Thus, it is possible to create public goods without, for instance, the necessary participation of the state. The latter could complicate all processes and fail to meet the requirements of the modern rapidly developing world. Venture capital allows individual new business units to develop in the studied region. As a result, these business units independently set goals, and achieve them using direct investments (for example, options) in their current and often risky stages of development. Consequently, these units can produce considerably more income in the future after a certain period. This approach is common in developed economies (for example, the USA, Japan, and EU members). The countries of the post-Soviet space (Ukraine, Kazakhstan, Russia, and others) have also turned to it. Thus, this practice of using venture capital, historically proven in developed countries, has found its application in the countries of the EECCA region.

The practical significance of the article lies in its application in the field of modeling situations to assess the risks and benefits of certain innovative solutions in the economy. The paper can be useful in sociology in the study of the impact on social processes of venture capital. Venture organizations can also use the described methods to make decisions about the organization of a venture fund in some country or region. The research limitations of this study encompass the possibility of applying the results at the external regional level. The aggregated indicators mostly concern the intraregional context of the EECCA countries and the post-Soviet space. To improve the current model, it is necessary to further research the potential and capacity of the market niche in the field of innovative enterprises in the post-Soviet countries (the EECCA region). Additional studies can allow for a more complete analysis of the prospects for further venture capital application in the region.

[1] Welter, C., Holcomb, T.R., McIlwraith, J. (2023). The inefficiencies of venture capital funding. Journal of Business Venturing Insights, 19: e00392. https://doi.org/10.1016/j.jbvi.2023.e00392

[2] Tenca, F., Croce, A., Ughetto, E. (2018). Business angels research in entrepreneurial finance: A literature review and a research agenda. Journal of Economic Surveys, 32(5): 1384-1413. https://doi.org/10.1002/9781119565178.ch7

[3] Bugl, B.M., Balz, F.P., Kanbach, D.K. (2022). Leveraging smart capital through corporate venture capital: A typology of value creation for new venture firms. Journal of Business Venturing Insights, 17: e00292. https://doi.org/10.1016/j.jbvi.2021.e00292

[4] Neville, C., Lucey, B.M. (2022). Financing Irish high-tech SMEs: The analysis of capital structure. International Review of Financial Analysis, 83: 102219. https://doi.org/10.1016/j.irfa.2022.102219

[5] Nahata, R. (2019). Success is good but failure is not so bad either: Serial entrepreneurs and venture capital contracting. Journal of Corporate Finance, 58: 624-649. https://doi.org/10.1016/j.jcorpfin.2019.07.006

[6] Welter, F., Smallbone, D. (2011). Post-Soviet societies and new venture creation. In Handbook of Research on New Venture Creation. Edward Elgar Publishing. https://doi.org/10.4337/9780857933065.00027

[7] Makhmadisuf, S., Umarov, H., Muhammadfiruz, Q. (2022). The impact of foreign direct investment on post-soviet union countries economic growth evidence in Tajikistan, Turkmenistan, Uzbekistan, and the Kyrgyz Republic. Minhaj International Journal of Economics and Organization Sciences, 2(1): 44-63.

[8] Hasan, I., Jackowicz, K., Kowalewski, O., Kozłowski, Ł. (2019). The economic impact of changes in local bank presence. Regional Studies, 53(5): 644-656. https://doi.org/10.1080/00343404.2018.1475729

[9] Grilli, L., Latifi, G., Mrkajic, B. (2019). Institutional determinants of venture capital activity: An empirically driven literature review and a research agenda. Journal of Economic Surveys, 33(4): 1094-1122. https://doi.org/10.1111/joes.12319

[10] Van den Heuvel, M., Popp, D. (2023). The role of venture capital and governments in clean energy: Lessons from the first cleantech bubble. Energy Economics, 124: 106877. https://doi.org/10.1016/j.eneco.2023.106877

[11] Luo, R., Zhao, B., Han, C., Wang, S. (2023). Does venture capital improve corporate social responsibility performance? International Review of Economics & Finance, 88: 1138-1150. https://doi.org/10.1016/j.iref.2023.07.070.

[12] Wang, L., Lang, Z., Duan, J., Zhang, H. (2023). Heterogeneous venture capital and technological innovation network evolution: Corporate reputation as mediating variable. Finance Research Letters, 51: 103478. https://doi.org/10.1016/j.frl.2022.103478

[13] Kapital.kz. (2023). President Tokayev: We must develop the venture capital market. https://kapital.kz/tehnology/119834/my-dolzhny-razvivat-rynok-venchurnogo-kapitala-prezident.html.

[14] Riethmueller, S. (2021). Rise of the zombies: The significance of venture capital investments that are not profitable. Houston Business and Tax Law.

[15] EU4Environment. (2021). The environmental compliance assurance system in the Republic of Moldova: Current situation and recommendations. https://www.eu4environment.org/the-environmental-compliance-assurance-system-in-the-republic-of-moldova/.

[16] EU4Environment. (2021). The environmental compliance assurance system in Armenia: Current situation and recommendations. https://www.eu4environment.org/the-environmental-compliance-assurance-system-in-armenia.

[17] UNECE. (2022). Environmental Performance Reviews Publications. Geneva: United Nations Economic Commission for Europe. https://unece.org/publications/environmental-performance-reviews.

[18] Holovko, I. (2021). Ukraine and the European green deal guiding principles for effective cooperation. Heinrich Böll Foundation. https://ua.boell.org/sites/default/files/2022-01/E-Paper_Ukraine_and_the_European_Green_Deal.pdf.

[19] OECD. (2021). OECD/GREEN action task force event: Is a green COVID-19 economic recovery possible? Perspectives for Eastern Europe, the Caucasus and Central Asia (25 June 2021), Summary Zoom Talk. Paris: OECD. https://www.oecd.org/environment/outreach/Summary-Record-Green-Recovery-EECCA.pdf.

[20] Andrusevych, A., Andrusevych, N., Kozak, Z., Mishchuk, Z. (2020). European green deal: Shaping the eastern partnership future. Resource and Analysis Center Society and Environment. https://www.rac.org.ua/uploads/content/593/files/webeneuropean-green-dealandeapen.pdf.

[21] IMF. (2021). Policy Responses to COVID-19. https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19.

[22] Neuweg, I., Michalak, K. (2022). The environmental effects of COVID-19 related recovery measures in the EECCA region. Paris: OECD. https://www.oecd.org/environment/outreach/ENV-EPOC-EAP(2022)4%20GreenRecovery.pdf.

[23] Wang, S., Wareewanich, T., Chankoson, T. (2023b). Factors influencing venture capital perforsmance in emerging technology: The case of China. International Journal of Innovation Studies, 7(1): 18-31. https://doi.org/10.1016/j.ijis.2022.08.004

[24] Meng, F., Tian, Y., Han, C., Band, S.S., Arya, V., Alhalabi, M. (2023). Study on value symbiosis and niche evolution of the corporate venture capital ecological community for innovation and knowledge. Journal of Innovation & Knowledge, 8(3): 100363. https://doi.org/10.1016/j.jik.2023.100363

[25] Gupta, B.B., Gaurav, A., Panigrahi, P.K., Arya, V. (2023). Analysis of artificial intelligence-based technologies and approaches on sustainable entrepreneurship. Technological Forecasting and Social Change, 186: 122152. https://doi.org/10.1016/j.techfore.2022.122152

[26] Kim, J.Y., Steensma, H.K., Park, H.D. (2019). The influence of technological links, social ties, and incumbent firm opportunistic propensity on the formation of corporate venture capital deals. Journal of Management, 45(4): 1595-1622. https://doi.org/10.1177/0149206317720722

[27] Maiti, M. (2022). Does development in venture capital investments influence green growth? Technological Forecasting and Social Change, 182: 121878. https://doi.org/10.1016/j.techfore.2022.121878

[28] Döll, L.M., Ulloa, M.I.C., Zammar, A., do Prado, G.F., Piekarski, C.M. (2022). Corporate venture capital and sustainability. Journal of Open Innovation: Technology, Market, and Complexity, 8(3): 132. https://doi.org/10.3390/joitmc8030132

[29] Skare, M., Gavurova, B., Polishchuk, V. (2023). A decision-making support model for financing start-up projects by venture capital funds on a crowdfunding platform. Journal of Business Research, 158: 113719. https://doi.org/10.1016/j.jbusres.2023.113719

[30] Cai, W., Polzin, F., Stam, E. (2021). Crowdfunding and social capital: A systematic review using a dynamic perspective. Technological Forecasting and Social Change, 162: 120412. https://doi.org/10.1016/j.techfore.2020.120412

[31] Lomakina, O., Kookueva, V., Makarenko, A. (2021). Redistribution of economic resources in the digital society. Business and Society Review, 126(1): 25-35. https://doi.org/10.1111/basr.12220

[32] Chandna, V. (2022). Social entrepreneurship and digital platforms: Crowdfunding in the sharing-economy era. Business Horizons, 65(1): 21-31. https://doi.org/10.1016/j.bushor.2021.09.005

[33] Bakici, T. (2020). Comparison of crowdsourcing platforms from social-psychological and motivational perspectives. International Journal of Information Management, 54: 102121. https://doi.org/10.1016/j.ijinfomgt.2020.102121

[34] Dong, L., Yang, Z. (2023). Investment and financing analysis for a venture capital alternative. Economic Modelling, 126: 106394. https://doi.org/10.1016/j.econmod.2023.106394

[35] Bhanot, K., Kadapakkam, P.R. (2022). Pay for performance, partnership success, and the internal organization of venture capital firms. Journal of Corporate Finance, 75: 102246. https://doi.org/10.1016/j.jcorpfin.2022.102246

[36] Batabyal, A.A., Yoo, S.J. (2022). Tax policy and interregional competition for mobile venture capital by the creative class. The North American Journal of Economics and Finance, 61: 101690. https://doi.org/10.1016/j.najef.2022.101690

[37] Lerner, J., Nanda, R. (2023). Venture capital and innovation. In Handbook of the Economics of Corporate Finance. Elsevier, North-Holland. https://doi.org/10.1016/bs.hecf.2023.02.002

[38] Bonini, S., Capizzi, V. (2019). The role of venture capital in the emerging entrepreneurial finance ecosystem: Future threats and opportunities. Venture Capital, 21(2-3): 137-175. https://doi.org/10.1080/13691066.2019.1608697

[39] Vogelaar, J.J., Stam, E. (2021). Beyond market failure: Rationales for regional governmental venture capital. Venture Capital, 23(3): 257-290. https://doi.org/10.1080/13691066.2021.1927341

[40] Park, S., LiPuma, J.A. (2020). New venture internationalization: The role of venture capital types and reputation. Journa lof World Business, 55(1): 101025. https://doi.org/10.1016/j.jwb.2019.101025

[41] Forbes.kz. (2023). Kazakhstan has created a new venture fund with a capital of $50 million. https://forbes.kz/finances/investment/v_kazahstane_sozdali_novyiy_venchurnyiy_fond_s_kapitalom_v_50_mln/.

[42] Nazarov, Z., Obydenkova, A.V. (2020). Democratization and firm innovation: Evidence from European and Central Asian post-communist states. Post-Communist Economies, 32(7): 833-859. https://doi.org/10.1080/14631377.2020.1745565

[43] Rapacki, R., Gardawski, J., Czerniak, A., Horbaczewska, B., Karbowski, A., Maszczyk, P., Prochniak, M. (2020). Emerging varieties of post-communist capitalism in Central and Eastern Europe: Where do we stand? Europe-Asia Studies, 72(4): 565-592. https://doi.org/10.1080/09668136.2019.1704222

[44] Abrardi, L., Croce, A., Ughetto, E. (2019). The dynamics of switching between governmental and independent venture capitalists: Theory and evidence. Small Business Economics, 53: 165-188. https://doi.org/10.1007/s11187-018-0047-z

[45] Bellucci, A., Borisov, A., Gucciardi, G., Zazzaro, A. (2023). The reallocation effects of COVID-19: Evidence from venture capital investments around the world. Journal of Banking & Finance, 147: 106443. https://doi.org/10.1016/j.jbankfin.2022.106443

[46] Bock, C., Watzinger, M. (2019). The capital gains tax: A curse but also a blessing for venture capital investment. Journal of Small Business Management, 57(4): 1200-1231. https://doi.org/10.1111/jsbm.12373

[47] Moedl, M.M. (2021). Two’s a company, three’s a crowd: Deal breaker terms in equity crowdfunding for prospective venture capital. Small Business Economics, 57(2): 927-952. https://doi.org/10.1007/s11187-020-00340-0

[48] Pavlova, E., Signore, S. (2021). The European venture capital landscape: An EIF perspective. Volume VI: The impact of VC on the exit and innovation outcomes of EIF-backed start-ups (No. 2021/70). EIF Working Paper. Luxembourg: European Investment Fund. https://www.econstor.eu/handle/10419/231445.

[49] Lerner, J., Nanda, R. (2020). Venture capital’s role in financing innovation: What we know and how much we still need to learn. Journal of Economic Perspectives, 34(3): 237-261. https://doi.org/10.1257/jep.34.3.237

[50] Jeon, E., Maula, M. (2022). Progress toward understanding tensions in corporate venture capital: A systematic review. Journal of Business Venturing, 37(4): 106226. https://doi.org/10.1016/j.jbusvent.2022.106226

[51] Barg, J.A., Drobetz, W., Momtaz, P.P. (2021). Valuing start-up firms: A reverse-engineering approach for fair-value multiples from venture capital transactions. Finance Research Letters, 43: 102008. https://doi.org/10.1016/j.frl.2021.102008

[52] Janeway, W.H., Nanda, R., Rhodes-Kropf, M. (2021). Venture capital booms and start-up financing. Annual Review of Financial Economics, 13: 111-127. https://doi.org/10.1146/annurev-financial-010621-115801

[53] Yao, T., O'Neill, H. (2022). Venture capital exit pressure and venture exit: A board perspective. Strategic Management Journal, 43(13): 2829-2848. https://doi.org/10.1002/smj.3432

[54] Zhang, Y., Zhang, X. (2020). Patent growth and the long-run performance of VC-backed IPOs. International Review of Economics & Finance, 69: 33-47. https://doi.org/10.1016/j.iref.2020.04.006

[55] Prado, T.S., Bauer, J.M. (2022). Big Tech platform acquisitions of start-ups and venture capital funding for innovation. Information Economics and Policy, 59: 100973. https://doi.org/10.1016/j.infoecopol.2022.100973