Nazim Hajiyev*![]() | Tarana Karimova

| Tarana Karimova![]() | Lesya Bozhko

| Lesya Bozhko![]() | Tatyana Sakulyeva

| Tatyana Sakulyeva![]() | Dmitrii Babaskin

| Dmitrii Babaskin![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Today, businesses are actively optimizing their financial structures, which places new demands on investors and managers. These professionals must execute transactions while considering the specific characteristics of the target market. This study's aim is to develop a typology of key strategies for cross-border mergers and acquisitions (M&As), which are common in today's competitive financial market environment. It relies on the main indicators of foreign direct investment (FDI) to monitor M&A activity in both developed and developing economies. By employing this strategy, the study was able to assess the competitive state of financial markets and provide a basis for managerial investment decisions. Using analytical methods, as well as micro- and macroeconomic approaches, the study analyzed the M&A process in the context of modern business practices. It then constructed a universal typology of key strategies based on the findings. The study highlights the importance of FDI inflows in M&As for driving growth, facilitating technology transfer, and promoting market development. This is particularly relevant in light of the pandemic and the distinctions between developed and developing markets. The practical value of the proposed typology is that it considers global policy priorities and the dynamic capabilities of national economies, offering a universal approach to investment. The results suggest that successful M&As, with an appropriate choice of strategies, lead to a robust economy. Further, the study improves our knowledge of global financial markets and business strategies, enhancing professional engagement with investment and capital management. The research contributes to our understanding of the conceptual structure of M&As within the broader context of global politics and financial integration.

transaction, financial market, corporate finance, strategic approach, cooperation, M&A strategies, mergers and acquisitions typology, market leadership

The economic development of different countries around the world for several decades has depended on attracting foreign direct investment, encouraging investment in the Sustainable Development Goals sectors [1], as well as the update and spread of digital technologies by the largest companies in the world [2].

However, the emergence of the COVID-19 crisis determined the need for the reformation of financing, supervision and implementation of the Sustainable Development Goals [3].

Along with existing challenges, such as the new industrial revolution, economic globalization, and sustainability trends, financial markets will also be transformed soon. Many investors have changed their approaches, recognizing that maximizing short-term growth cannot be achieved at the expense of clean air, water, a stable climate, peaceful communities and sustainable ecosystems alone. It becomes necessary to include social and environmental goals in financial instruments and investment impact [3].

These challenges will present new opportunities for financial markets, for example: facilitating investments focused on sustainability; creating regional value chains; and accessing new markets through digital platforms. At the same time, it is necessary to consider the dynamic capabilities of national economies - their capability to transform, modify and redistribute existing resources and technologies into qualitatively new sources of competitive advantages [4].

Seizing these opportunities will require investors and managers to change their development strategies [5].

The beginning of the 21st century’s third decade with the shocks of the pandemic, military conflicts, and economic sanctions marks the end of the seventh and the beginning of a new eighth wave of mergers and acquisitions [6].

In 1893-1904, the first wave, which is characterized by increased capital concentration and monopolization in the US economy (horizontal mergers in metallurgy, the oil industry and food production, coal mining, and mechanical engineering). The collapse of the stock market in 1904 and the crisis of financial support for mergers led to the first wave’s completion.

In 1919-1929, the second wave and the beginning of oligopolization and vertical mergers (especially in the engineering and oil and gas industries), focused on efficiency, cost optimization and partnership of companies increasing their competitive advantages, especially in the supply and logistics sectors. The Great Depression of 1929 put an end to the second wave.

In 1955-1970, the expansion of new markets by American companies and the diversification of their revenues became the drivers of management decisions after the protracted crisis. These processes marked the beginning of the third M&A wave. It implied mergers and acquisitions of conglomerates - companies from various business areas. The oil crisis and the stock market crash brought this wave to an end.

In 1974-1989, the fourth wave represented the emergence of corporate raiders and "hostile takeovers", which were occasionally carried out without the consent of company owners. During this wave, investment banks strengthened their role, increasing the financial support of corporate raiders. The markets of so-called "junk bonds" developed at the same time. They sold bonds of low credit quality. The stock market crash of 1989 led to the end of the fourth wave.

In 1993-2000, the fifth wave period with its "mega-deals", when companies tried to save more money by scaling. It resulted in numerous multinational conglomerates with foreign investors entering the American markets and vice versa. The phenomenon of cross-border mergers became widespread when foreign investors received a controlling stake in an integrated company. The bankruptcies of large companies (Worldcom, Enron) and the bursting of dot-com bubbles marked the end of this wave.

In 2003- the beginning of 2008, this is the sixth wave period characterized by increased globalization, the role of private capital and the activity of shareholders. The power of the latter increased in the management of companies, and this led to the diffusion of ownership rights among management and investors. All these processes have intensified the processes of private capital inflows and leveraged buyouts. The mortgage lending crisis of December 2007, coinciding with the recession of the US economy, led to the end of the sixth wave and the extinction of mergers and acquisitions. The most high-profile deal of this wave was the purchase of Time Warner by American Online for 164 billion. However, this transaction turned out to be "the biggest mistake in the history of corporate mergers" and failed with $100 billion in losses a year later.

In 2011- the beginning of 2020, the seventh wave and the beginning of the M&A activation. The BRICS countries (five developing and densely populated economies of the world: Brazil, Russia, India, China, and South Africa) were coming to the forefront in the field of mergers and acquisitions, intensifying commercial and corporate cooperation. The COVID-19 pandemic has suspended the activity of mergers and acquisitions, but the next eighth M&A wave begins at the end of 2020.

A new review of global mergers and acquisitions (M&A) revived the American economy: at the end of 2020, the largest number of M&A took place in American markets - \$1.4 trillion, European markets - \$989 billion, and Asian markets - \$872 billion [7]. Global M&A deals between \$5 billion and \$10 billion increased by 36%, whereas mega deals decreased by 21% compared to the last year. The value of transactions between \$5 and \$10 billion totaled \$514.6 billion, while the value of mega deals was \$913.7 billion. Cross-border deals totaled \$1.3 trillion, up 12% from 2019. Consumer markets and industry accounted for the largest number of these deals - 40% compared to 28% in 2019 - among all economic sectors. Two record-breaking deals were recorded: the technology sector had \$\684.3 billion in transactions, an increase of 50% from 2019, and the private equity sector (private equity buyouts) had 8,800 deals, an increase of 27% from last year. M&As are a key tool of companies’ integration investments, and they make a significant contribution to global connectivity of the world, providing benefits from globalization through waves of acquisitions [8].

At the same time, in the context of cross-border M&A, national governments intervene in these processes to "protect" large domestic firms and their industries from foreign bidders [9].

Moreover, UNCTAD 2021 experts note that many countries, especially the post-Soviet ones, witness a continuous growth of economic protectionism, measures of "harmful interference": subsidies, import and trade protection control instruments, public procurement, and localization [10]. Through creating barriers to financial transactions, these governments attempt to block foreign bidders, preventing foreign companies from participating in cross-border M&A deals. The official position concerning this intervention is the protection of national interests in the field of economy.

In 2021, global mergers and acquisitions (M&A) reached new highs, significantly beating the previous ones. The number of announced deals exceeded 62,000 worldwide in 2021, which is 24% more than in 2020 [11]. The main factors of such growth were intensive demand for technology and a focus on digital assets. The main industries in the mergers and acquisitions market in 2021 were information technology and healthcare [11].

Mergers and acquisitions represent strategic corporate endeavours aimed at fortifying a company's market position and achieving leadership. It is noteworthy that the choice of a merger or acquisition strategy hinges upon a company's objectives, its extant market standing, the competitive milieu, and sundry other determinants. Enterprises endeavour to deploy these strategies to attain market dominance, consolidate their footholds, and engender added value for their shareholders.

Microeconomic approaches encompass an analytical framework within economics that concentrates on the study of conduct exhibited by individual economic agents, such as households, firms, and markets for discrete goods and services. This framework delves into decision-making at the micro-level, encompassing facets like production, consumption, pricing mechanisms, and resource allocation.

Macroeconomic approaches encompass methodologies within economics that are directed towards the comprehensive study of the economy as a whole rather than isolated constituents. These approaches scrutinize aggregated variables, such as national income, unemployment, inflation, and overall production volume. Macroeconomic approaches endeavour to apprehend overarching regularities and interrelationships within the economy and formulate policies that may exert influence over overall economic outcomes.

The typology of merger and acquisition strategies denotes a classification of diverse approaches and objectives that companies may pursue when engaging in mergers and acquisitions. These strategies can range from horizontal mergers (where companies in the same industry merge) to vertical mergers (involving companies at different stages of the production chain) to conglomerate mergers (encompassing companies from disparate industries). This typology serves to delineate various forms of mergers and acquisitions and facilitate an understanding of the underlying motives and strategies that may underscore them.

1.1 Literature review

Mergers and acquisitions (M&A) constitute a multifaceted process of significance within the purview of companies' strategic development under the stewardship of their leadership cadre. The objective of such transactions frequently revolves around the enhancement of financial metrics, augmentation of market share, and the attainment of competitive advantages [12].

In business, the M&A definition includes the merging of companies or assets through various types of financial transactions: mergers, acquisitions, consolidations, tender offers, asset purchases, and management acquisitions [12].

These financial transactions are more effective when they maximally consider the so-called dynamic capabilities of the countries’ economies of investor companies and capital recipients. In 1997, Teece et al. [4] formulated the theory of dynamic capabilities, which are organizational procedures through which managers influence a company’s resource base (buy or sell resources, combine and blend them) to form new strategies. It can be argued that the dynamic capabilities of the economy lie in its potential to transform, modify and redistribute hidden and explicit resources into the latest sources of competitive advantages. At the same time, the dynamic capabilities of a company are considered by the authors as some kind of "organizational procedures for the utilization of resources to comply with market interpellation, as well as to implement market changes”. Through these procedures, it is possible to combine resources in the most efficient and high-tech way to meet the dynamic market requirements as much as possible.

Mergers and acquisitions have become an effective way of strategic business alliances and geographical tactics in the global market [13, 14]. Consequently, both research and practical work have a crucial task to identify the motives, methods of evaluating mergers and acquisitions, sources of financing, announcement effects, cross-border competition, and successes or failures of these alliances [15].

Within the ambit of typology, eight distinct categories of mergers and acquisitions are discerned, predicated upon an analysis of three pivotal facets: the external environmental milieu, firm-level acquisition strategy, and the chief executive officer's motivations. The findings of the investigation by Bettinazzi et al. [16] underscored substantive differentials in market efficacy and account for risks contingent upon the specific genre of mergers and acquisitions. This attests to the capricious nature of merger and acquisition outcomes, thus necessitating supplementary scrutiny.

According to Chiu et al. [17], an integrated typology that considers the substantial influence of diverse factors on the strategic congruence underpinning the success of mergers and acquisitions resolves a paradox. This paradox resides in the phenomenon that, despite the prevalent perception of a high likelihood of unfavourable outcomes, experts in mergers and acquisitions persistently engage in such transactions. This assertion addresses the seeming contradiction by emphasizing a comprehensive approach that accommodates multifarious determinants.

Lin et al. [18] asserts the existence of overarching trends that elucidate the manners in which niche players, market leaders, and contenders engage with mergers and acquisitions:

Niche Players and Technological Resources. Niche enterprises frequently harness their technological advantages actively in effecting mergers and acquisitions. They aspire to access external founts of knowledge and resources that can complement their specialized capabilities.

Leaders and Market Dominance. Leaders endowed with a resilient market stance often employ mergers and acquisitions to fortify their position. Their objectives may encompass expanding market influence, diminishing competitive pressures, and engendering supplementary scale.

Contenders and External Environment. Contenders positioned amidst an unfavourable market context incline towards engagement in mergers and acquisitions to ameliorate their positions. They seek opportunities for resource reallocation and risk mitigation amid challenging external conditions.

Contenders and Technological Burden. Contenders operating within technologically saturated domains might exhibit a reduced proclivity towards mergers and acquisitions. This propensity could stem from their extant access to requisite technologies, coupled with a focus on internal innovation endeavours.

Overall, merger and acquisition strategies are intricately intertwined with the context within which firms operate and their market objectives. Niche players, leaders, and contenders may leverage these instruments to attain their distinctive business goals and to adapt to the evolving milieu [18].

Generally, there are traditionally two motives for mergers and acquisitions. The first motive is when companies decide to merge to save on production costs. The second motive is when companies want to get enough capital to enter new markets or launch new products. Based on a sample of 3,520 internal mergers and acquisitions in the United States, the authors found the following distribution of motives and reasons for such transactions: 73% are related to the timing of market entry, 59% - agency motives and ambitions, 3% - reaction to industry and macroeconomic shocks. At the same time, 80% of mergers in this sample were associated with several of the mentioned motives [19].

Achievement of M&A motives is provided by strategies, which is the general plan of the M&A process. Cirjevskis [20] allowed one to evaluate the reserves and potential of the company in the current economic environment, which contributes to the overall competitiveness.

Researchers analyzed the types of financial organizations’ M&A strategies about to their effects on the shareholder value of bidders. With the strategy of market penetration, mergers of financial organizations reduce the share value of companies participating in the auction. Market development and product development strategies allow the creation of shareholder value in the short and long term. Diversification strategies do not affect shareholder value. Internal mergers create shareholder value and increase liquidity and economic value in the short term. Cross-border mergers create value for bidders in the long term but are associated with higher costs and risks [21]. The motivation for mergers and acquisitions is much broader than the realization of cost reduction and entry into new markets [22]. The main groups of motives for mergers and acquisitions are the acquisition of undervalued firms, operational and financial synergy, and personal ambitions of management [23]. Other sources mention the economic growth of companies, the expansion of their market power, the acquisition of unique opportunities and resources and the disclosure of the hidden value of acquired firms, the diversification of assets, investments and risks, income growth, tax optimization, personal management incentives again, and synergy effect [24].

The CFI team's analytical study for 2022, the most common reasons for mergers and acquisitions are promising growth in the value of companies, diversification, reduction of tax liabilities, and incentives for managers [25].

Among other motives for mergers and acquisitions, in addition to financial and operational synergy, modern literature presents the managerial synergy concept, when the joint competencies of managers and the initiation of acquisitions contribute to a company's efficiency growth [26]. Ray [26] addressed M&A motives through the prism of company empire-building theories, value theory, process theory, disturbance theory, efficiency theory, and monopoly theory. Operational and financial synergy embody two objectives of acquisitions. Thus, the desire for operational synergy in a takeover is a motivation to gain value through the joint creation of products or joint innovations. At the same time, an attempt at financial synergy is a motive to increase value due to financial benefits that result from the acquisition, i.e., diversification of an MNC portfolio [27].

Sergeevna [28] considered M&A to be the main way to merge the capital of two or more companies in order to maximize their opportunities and potentials in achieving a common goal. The M&A process itself is a tool to gain a competitive advantage in the market, which includes a business development strategy. The main motive behind the transaction is to reach synergy [20]. In this case, the cooperating companies can expect a greater market value compared to what they can achieve without cooperation. Feldman and Hernandez [29] classified three types of cooperation arising from the synergistic combination of an acquirer and a target: relational (contractual partnership with external parties), network (direct and indirect ties between collaborationist firms), and non-market (arise from external institutional relations). Huhtilainen et al. [30] reviewed the prerequisites and conditions for an M&A transaction. It seems that these transactions require a competitive environment with a corporate governance system to implement the transaction mechanism. Currently, these demands are met by Western economies, such as the USA, the UK, the Netherlands, and Germany [7, 31]. These financial markets have a long history of development and exist for more than a century. On the other side of the scale are financial markets that emerged less than 30 years ago [32-34]. The gap between developed and emerging financial markets is the reason behind the slow pace of M&A. The post-Soviet countries demonstrate similar changes in their financial markets, as they gravitate more to a planned economy where the state-owned companies dominate in the field of capital transactions [33, 34]. Pashtova and Maimulov [35] highlighted three main barriers to trade transactions in developing financial markets. The first barrier is the poor-quality acquisition transactions that slow down the growth of the company's value. The second obstacle is the high growth rate in the company’s value before the transaction. Finally, the market may not be ready to increase the volume of transactions due to specific conditions, such as pressure from the state-owned corporations, tax reforms, and declining foreign direct investment. On the other hand, market globalization, saturation, and consolidation processes alongside rising competition force Western companies to seek access to emerging financial markets, thereby encouraging acquisition [36]. For example, the state-owned oil company in Azerbaijan called SOCAR and the State Oil Fund (SOFAZ) of the Republic invested in the gas pipeline network, which also includes Italy, Greece, and the United States [33], boosting the growth of transactions involving the state-owned companies.

In a methodological context, it is advisable to distinguish micro- and macroeconomic approaches to the analysis of mergers and acquisitions. From the macroeconomic perspective, mergers and acquisitions are analyzed in the works by Golbe and White [37]; Fred Weston [38]; Burke and Nelson [39]; Chang and Ki [40]. Thus, the ratio of micro- and macro-aspects of mergers and acquisitions is determined by the number of transactions and the purchase price. Researchers studied the history of large companies’ mergers (General Electric & RCA), hostile tender offers (Mesa % Unocal), and buyouts (Beatrice). They also analyzed the chronology of quarterly issues of the periodic M&A list and the number of M&A significant in value for the entire US economy. To be included in the list of periodic mergers and acquisitions published by The periodical Mergers and Acquisitions since 1967, the lower threshold of the transaction’s purchase price in 1980 increased from 700 thousand to 1 million dollars.

The economists study mergers and acquisitions in the context of stock market capitalization. Based on data from the US M&A market, they found a correlation between the stock market capitalization growth, the industrial production growth, and the volume of mergers and acquisitions [38, 39].

Other authors have found a correlation between the mergers and acquisitions market and the GDP dynamics. Thus, Chang and Ki [40] revealed a positive relationship between the M&A market and the difference in the rate of return on highly rated corporate bonds and junk bonds. The researcher also established a connection between this market and the GDP growth rate.

In 1986, Beketti found the connection of the M&A market with the debt burden growth, the GDP growth rate, and nominal interest rates [41]. The economists Golbe and White [42] indicated a positive relationship between the volume of M&A transactions and the level of real interest rates, the economy level, the Q-Tobin coefficient, the taxation system, and the asymmetry level in the information distribution between potential M&A market participants. In the context of corporate finance, mergers and acquisitions are investigated by DePamphilis [43], Gohan [44], Breili and Maiers [45] at the microeconomic level.

The motives of participants in integration transactions at the company level are analyzed by Vorotnikova and Pshipiy [46]. In the literature, there is a term "public utility" of mergers and acquisitions, meaning the positive effects of these processes on macroeconomic development. They include the growth of tax revenues to the state budget, technological re-equipment of production and labor productivity growth, changes in the wage fund, changes in company expenditures for social purposes, monopolization of markets, integration options, and increase in net profit of merged companies [47].

This article addresses the processes of mergers and acquisitions in micro- and macro-perspectives interrelated and correlated with each other in a certain way. Mergers and acquisitions with macroeconomic roots result in their reorganization and consolidation of capital, and capitalization growth, which is the main goal of corporate development (micro-perspective). The dominant idea of mergers and acquisitions relates to the term "synergy" [48].

1.2 Problem statement

An extremely important methodological task of the present study is to substantiate the correlation of micro- and macroeconomic approaches in constructing the typology of M&A strategies. A review of sources shows that mergers and acquisitions are both a micro- and macro-economic process. Starting from the level of individual companies, the consolidation and concentration of capital extends to the industry and further to the country's economy, affecting capital markets, technology, labor, and the number of tax revenues to the state budget. Due to the synergy effect, when companies' access to new resources, markets, and technologies expands, the cost of integrated companies increases and exceeds their individual cost. New management decisions and the attraction of new capacities contribute to the streamlining of the organizational and production cycle. Mergers and acquisitions are characterized by the withdrawal of capital from depressed industries. This process contributes to a change in the concentration of the industry where the transaction is concluded and accelerated economic development of promising industries most prone to mergers and acquisitions. In addition, in some countries, particularly the Russian Federation, there is a tendency for the state to increase its share in mergers and acquisitions. Mergers and acquisitions naturally cause changes in the outflow and inflow of capital abroad, that is, they affect the conjuncture of capital markets in the countries whose companies are involved in the transaction. Moreover, these transactions also have an impact on the labor market, since when a merger is concluded, one of the companies closes, which leads to mass layoffs. The growth in the scale of mergers and acquisitions in industries prone to capital consolidation (biopharmaceuticals, IT, agriculture, chemistry, and metallurgy - starting from the microeconomic level) causes transformations of the technical and technological basis of capital concentration and production and transitions from one technological mode to another. The very ratio of micro and macro aspects of mergers and acquisitions, a transaction’ capability to affect the macro level is determined by the weight of the transaction, its purchase price, and the total number of large transactions.

Based on the literature review, investment flows are vital for economic development and constitute a global policy priority. At the same time, the strategic M&A plan discussed in the previous studies has become generally accepted in economic practice. Therefore, there is a need to develop a universal typology of M&A strategies in a world of unprecedented change. This study aims to outline a typology of key M&A strategies that are typical for the competitive environment of financial markets today.

The research objectives are (1) to monitor M&A markets in emerging economies; (2) to develop a universal typology of basic M&A strategies that will enable optimum investment decisions; and (3) to apply the proposed typology within the model of global politics and financial integration.

This study contributes an instrument for strategically managing investment in the environment with dynamic capabilities. This framework represents a universal approach for traders in a changing external environment to achieve leading positions in the market.

Strategy is the process of implementing management solutions for the long-term development of companies. Depending on a company’s financial well-being and capital structure, the strategy is carried out according to the organic (evolutionary) or inorganic (through purchasing by another company, mergers, and acquisitions) type of growth. Organic growth is a necessary condition for maintaining the current activity of a company for a long period. However, within the framework of M&A, organic growth is also possible when the merger has already occurred. Inorganic growth should be understood as an emergency measure caused by the urgent need to promptly solve the managerial, organizational, and financial problems of a company. This requires the desire of partners to successfully implement the alliance.

Mergers and acquisitions strategies are based on a strategic goal of the company planning to conclude an M&A transaction. In a broad context, the goal of any company is the development of its business processes with an increase in their efficiency, the growth of a market niche, and the acquisition of leadership positions in the industry, region, country, and worldwide. This requires scaling the business. In a narrow context, the goals of companies differ. Some of them experience a long evolutionary path to expand the scale of their business, while others purchase ready-made profile businesses. The strategy of mergers and acquisitions is based on economic intentions, considered in terms of both the corporate strategy type and an investment type. One way or another, the main corporate effect of the transaction is the increase in market capitalization for state-owned companies and the increase in business value for commercial companies. The latter is initiated by the implementation of mergers and acquisitions synergy. To assess macroeconomic efficiency, the results of the transaction are heterogeneous and have consequences in terms of both reducing real production costs and changing the competitive space. Since mergers and acquisitions are also a type of investment, standard measures for assessing the merger consequences for commercial and state-owned companies, effective investment projects are useful considering their specifics [49]. Mergers and acquisitions often become the inevitable and only way for a company to continue business in the industry. At the same time, companies can pursue the goals of strengthening their positions, sustainable development, and effective resource management. In the merger markets, not only large companies absorb small ones, but also many large companies integrate to scale their business and achieve better financial results [50]. The organizational effect of M&A is a new company transformed through the synergy of capacities and resources, research potential growth, expansion of business processes in new segments, and increase in shareholder value [51].

The subject matter of the paper is two dynamically developing countries of the former USSR: Russia and Azerbaijan. The countries have the same classification category of the World Bank (upper-middle-income countries) and industries as close as possible for investment cooperation: oil and gas, IT, and financial market. Moreover, the trends of foreign direct investment, mergers, and acquisitions in these countries generally reflect global trends related to the growing demand for technology and focus on digital assets, and the development of industries such as pharmaceuticals, healthcare, IT, and telecommunications services.

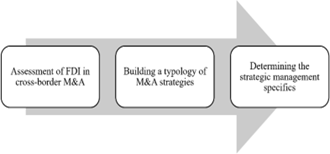

The framework of this study has three steps. The first step is to analyze relevant data and assess changes in foreign direct investment (FDI) reflecting trends in cross-border mergers and acquisitions over time in and developing economies with an upper-middle income. This study is limited to two countries, namely Russia and Azerbaijan. The second step is to build a universal typology of M&A strategies that fit financial markets. The final step is to define the features of strategic management within the model of global politics and financial integration (Figure 1).

Figure 1. The stages of the study

The analysis of inflows and outflows of foreign direct investment (FDI) in Russia and Azerbaijan can furnish valuable insights for the formulation of a typology of merger and acquisition strategies. In this context, foreign direct investments serve as indicators of trends and shifts within international business transactions, encompassing mergers and acquisitions. The scrutiny of FDI data can facilitate the discernment of overarching behavioural patterns and investment trajectories between countries of varying income levels and developing.

The analysis of FDI in Russia and Azerbaijan unveils the following:

Investment Trends and Magnitude: Scrutinizing the dynamics of FDI inflows and outflows facilitates the identification of temporal trends and investment volumes in these nations. This may delineate periods of heightened and diminished activity within the sphere of mergers and acquisitions.

Sectoral Composition: An examination of investment distribution across industries permits the identification of sectors most appealing to investors, shedding light on which business domains might be most susceptible to mergers and acquisitions.

Geographical Dynamics: Investigating investment partner countries can aid in elucidating regional preferences of investors and partners for transactions.

Transaction Structure: Analyzing the scales, types, and attributes of transactions (e.g., international or domestic, horizontal or vertical) can provide insights into strategies employed in business transactions.

The sources of information used herein are Deloitte [52] and UNCTAD [53, 54]. Both sources, Deloitte and UNCTAD, are esteemed entities within the realm of research and analysis about economic and business trends. Their publications encompass data, statistics, and analytics across a spectrum of subjects, encompassing mergers and acquisitions, economic growth, international trade, and investments.

Furthermore, for obtaining financial and business information, analytical platforms and databases were utilized, including Bloomberg Terminal [55] and Thomson Reuters Eikon [56], in addition to reports and research from consulting firms such as McKinsey & Company [57] and PricewaterhouseCoopers [58]. These consulting firms routinely publish reports and studies concerning trends and strategies within the domain of mergers and acquisitions.

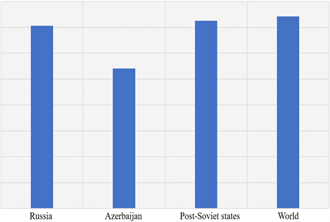

Previous research mostly focuses on different types of economies, developing economies with an upper-middle income, such as Russia (higher GDP volumes and economic growth rates) and Azerbaijan (lower GDP volumes and economic growth rates) [59].

In the context of the GDP volume and its dynamics, Russia is a country with greater economic potential (resource, production, technological) than Azerbaijan. Over the past decade, Russia’s economic growth rates have become closest to the average for the former Soviet republics and the world rate. Thus, in 2010, Azerbaijan's GDP was \$135.2 billion, while Russia's was \$2927.0 billion; in 2020, it was \$146.1 billion and \$4133.1 billion, respectively [60, 61] (Figure 2).

Figure 2. Economic growth rates in 2010-2020 (%)

Source: The World Bank [60]

This approach helps to identify macroeconomic development vulnerabilities and integrate strategic management into global policy priorities as a universal configuration.

The study covers the period between 2017 and 2022. First, we examined FDI flows and outflows in Russia and Azerbaijan in 2017/2021 using data from the UNCTAD report published in 2022 [53]. The results serve as a rationale for managerial decision-making in the field of investment. The findings are presented as histograms comparing values across several categories. Then, we built a concept map in Visio using information from these two sources: Askerov et al. [34] and Deloitte [52]. The concept map denotes the outcomes of strategic cooperation in the M&A market through the current business strategies (Figure 3).

Figure 3. Business strategies and outcomes in the M&A market

The utilization of a conceptual map serves as a valuable instrument in systematically organizing the typology of merger and acquisition strategies. This approach aids in arranging a wide array of transactional patterns and characteristics into a cohesive framework, enhancing the clarity of comprehension and analytical exploration. In this context, the map's function is to categorize different strategies according to shared attributes and factors, thus unveiling general patterns and specific nuances. The concept map was later used as a platform for defining the structure of the universal strategy typology. The potential usage trends of the proposed topology were identified in the thirds stage of the study concerning global politics and financial integration [53]. The trends were presented on a histogram with a linear trend line.

Russia and Azerbaijan found themselves at the forefront of the global economic upheaval triggered by the COVID-19 pandemic, rendering an analysis of these ramifications an integral facet of the research endeavour. The economic downturn resulting from diminished consumer demand and disruptions in production chains exerted adverse effects on the core sectors of both nations' economies. Significantly noteworthy was the sharp decrease in oil prices, which had a pronounced effect on their oil sectors, coupled with limitations in global trade that influenced the flow of exports and imports. In response to these challenges, Russia and Azerbaijan were compelled to reassess their budgetary strategies, reforms, and developmental trajectories to surmount the economic aftermath of the pandemic and adapt to the novel realities.

Figure 4 shows changes in the inward and outward flows of FDI in the studied countries over the past five years. As can be seen, Russia experienced an uneven distribution of investment activity across the years, but the effects of FDI were inherently positive. Azerbaijan, on the other hand, saw a reduction in FDI over time and its negative impact.

FDI inflows into Russia increased from 25954 million US dollars in 2017 to 38240 million US dollars in 2021, highlighting a 147.3% growth over five years. During the same period, the outflows of FDI in the country decreased by 186.2%, to 34153 US dollars from 63602 US dollars. Azerbaijan witnessed the opposite trend: FDI inflows into the country reduced by 59.5% hitting -1708 million US dollars in 2021 as against 2867 US dollars in 2017, while FDI outflows accounted for 3.0% of that in 2017. These findings suggest that M&A markets in Russia and Azerbaijan have different development trajectories. For instance, during the COVID-19 pandemic, Russia was likely to enjoy a positive investment activity, while Azerbaijan lost competitiveness.

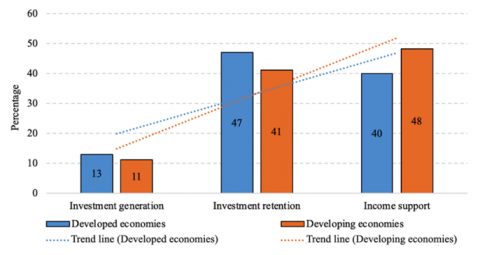

Companies can gain and keep leading positions in the financial market if they chose their management strategies wisely. Figure 5 presents a strategic management framework with a universal M&A strategy topology at its core. The presented strategies vary in their organizational form, expectations, and response to the external challenges (Figure 5).

The proposed M&A strategy topology reveals the relation between four different management strategies and external challenges. For instance, organizational and innovation strategies can help businesses enter the global market, whilst investment and financial strategies enable the optimal combination of risky assets. From the managerial perspective, the proposed topology is expected to allow effective investment decisions, better management, rapid response to changes in the business environment, and economic risk forecasting. From the economic perspective, it follows the global policy priorities and takes into account the dynamic capabilities of the national economy. As of 2022, the global policy trend defining the potential usage of the proposed topology is investment retention, the process most affected by the global recession. The retention of investments, particularly during periods of economic uncertainty, can emerge as a strategic objective for both corporations and nations. Political decisions about investment support may encompass tax incentives, subsidies, streamlining bureaucratic procedures, and fostering a favourable investment climate. These measures serve as incentives for companies to devote increased attention to investment activities, including merger and acquisition transactions.

The selection of specific merger and acquisition strategies may hinge upon a company's objectives and the broader context. For instance, the strategy of a horizontal merger (merging companies within the same industry) might be chosen to fortify market position and reduce competition. Meanwhile, a strategy involving vertical integration (merging companies engaged in different stages of production) could enhance the vertical supply chain and resource control.

These strategies, in turn, can contribute to sustainable company growth. Strengthening market position, optimizing business processes, expanding customer bases, and gaining access to novel technologies can lead to augmented revenue and profits. This, in effect, can foster financial stability, encourage investments in innovation, and facilitate long-term expansion.

Hence, the interrelation between policy trends, the selection of merger and acquisition strategies, and sustainable growth are underscored by the fact that sound strategic decisions in the domain of mergers and acquisitions, reinforced by a favourable investment policy, can facilitate the realization of a company's potential, risk mitigation, and attainment of sustainable and enduring growth (Figure 6).

Figure 4. Inward (a) and outward (b) FDI flows in Russia and Azerbaijan (2017/2021)

Source: based on UNCTAD [53]

Figure 5. Management decision-making process tree in M&A specific to financial markets in post-pandemic conditions

Figure 6. Global policy trends concerning investment as of 2022

Source: based on UNCTAD [53]

In order to attract greater volumes of foreign direct investment (FDI) and foster sustainable growth post the COVID-19 pandemic, both companies and governments can employ the following strategies:

For companies:

Innovations and Technologies: The development and implementation of novel technologies and innovations can render a company more appealing to foreign investors who seek access to cutting-edge knowledge and resources.

Risk Management: Companies must proactively engage in risk reduction associated with investment, such as enhancing transparency, adhering to laws and regulations, and improving governance practices.

Partnerships and Cooperation: Establishing partnerships with local firms or other investors can facilitate the exchange of experiences and resources, fostering increased confidence in the investment climate.

For governments:

Investment Policy: The creation of a conducive investment environment through the reduction of bureaucratic barriers, and streamlining of registration and licensing procedures, can stimulate the inflow of foreign direct investment (FDI).

Incentive Measures: Governments can provide various incentives such as tax exemptions, subsidies, grants, and other forms of financial support to attract foreign investors.

Infrastructure and Education: Developing infrastructure and education helps establish a favourable business environment, attract skilled professionals, and ensure sustainable growth.

Political Stability: Ensuring political stability and legal certainty is crucial for investment attraction, as investors seek reliable environments for long-term plans.

The overarching approach encompasses a harmonious blend of innovation, stability, support, and openness to international collaboration. The adaptation of policies and strategies at both the corporate and governmental levels will serve to incentivize the inflow of foreign direct investment (FDI), sustain growth, and facilitate recovery post the pandemic.

In 2022, M&A traders were interested in retaining investments. This is true for both the developed economy and the developing economy. To achieve this goal, developed countries have to focus on enhancing financial growth through investment and financial strategies. Emerging economies, on the other hand, need to create a viable portfolio of investment-attractive projects through organizational and innovation strategies. As can be seen, the proposed strategic management framework is capable of facilitating sustainable growth in the post-pandemic world.

Hence, the study's findings affirm that mergers and acquisitions remain a pivotal instrument for fostering growth, unlocking fresh opportunities, and facilitating technology transfer, particularly in developed countries. However, in emerging financial markets, a contraction in direct investments and diminished competitiveness might be observed. The proposed universal typology of M&A strategies, grounded in global policy and economic dynamics, will aid in enhancing managerial decision-making amid crisis conditions.

Modern mergers and acquisitions occur against the background of ambivalent trends of increasing globalization [8] and protectionism by national governments [9]. The uniqueness of M&A lies in the fact that, starting at the microeconomic level and the level of corporate finance [43], they move to the level of the industry and eventually the level of the entire national economy. The weight of each M&A transaction for the macroeconomic level can be determined by its purchase price [37], the capability to affect stock markets Fred Weston [38] and GDP dynamics [40]. The transition of mergers and acquisitions from the micro- to the macro-economic level is due to the effects of financial synergy, operational synergy [39], and managerial synergy [26].

The M&A market analysis contained in this study shows that countries with great economic potential actively engaged in deal-making during the COVID-19 pandemic. Mergers and acquisitions serve as a means to achieve and create an active competitive environment for effective transactions [62, 63]. The present findings support this statement. The evaluation of financial market dynamics involved the analysis of market strategies exploited in Russia and Azerbaijan. Russia demonstrated external stability against the backdrop of COVID-19-induced economic challenges, while Azerbaijan revealed the non-competitive quality of the current market model. Baik et al. [64] and Ganbarov et al. [65] found that the country’s market environment influences the profitability of the facility and its strategic behavior. The researchers identified culture, quality of accounting standards, and political and legal environment as influential factors. According to their hypothesis, a non-transparent institutional environment (countries with low political stability, democracy, press freedom, and high levels of corruption) helps to controls the market conditions of the country and gives the transaction participants incentives to increase profits up to cross-border mergers [66]. The central element of the study is the M&A process in business. There are many approaches to its study in the international practice. Hečková et al. [67] examined the process of mergers and acquisitions through the study of the goals and basic needs of the company. Gaughan [68] reviewed the financial analysis of public and private companies. Ali and Bansal [5] studied M&A through the lens of motive, management synergy, and factors affecting the economy. King et al. [69] focused on organizational change and the history of acquisitions that can have different configurations of sub-processes and affect the outcome of the transaction. Adequate M&A strategies can serve as a potent tool for attaining heightened corporate efficiency and catalyzing sustainable economic development within nations. The consensus is that the right strategies in M&A transactions play a key role in both improving the performance of companies and the country’s economy by ensuring its sustainability. Hossain [15] applied a scientific generalization approach and identified motives, methods, funding sources, synergies, cross-border competition, and business strategies of the M&A process. The researcher concluded that M&A are a business tool through which strategic alliances in business, new products, and geographical tactics in the global market are formed. Thus, in the last decade, the M&A process has attracted a lot of attention in academia which all comes down to the understanding that choosing the right development strategy remains one of the highest priorities to accomplish effective M&A deals [70]. Note that resource complementarity is an important aspect to consider when rescheduling mergers and acquisitions, as it has a significant impact on the company’s performance [71, 72]. This suggestion is consistent with the present study.

The study has confirmed that the decision regarding the choice of a merger or acquisition strategy is intricate and strategic, demanding an assessment of various elements, including risks and opportunities, market and competitor reactions, and the internal capacities of the company.

In our study, we have directed our attention towards the diversity of merger and acquisition strategies adopted by companies during their journey to market leadership. Particularly, strategies of horizontal integration, vertical integration, and diversification are discernible. Horizontal integration, as revealed through our analyses, is frequently employed to augment market share and enhance market position by amalgamating with competitors. Such transactions have the potential to yield synergies in sales and marketing domains.

Furthermore, the findings have also demonstrated that vertical integration can serve as an effective avenue for companies to attain market leadership. This facilitates control over production processes and cost reduction, ensuring more dependable supplies and enhanced quality control.

Diversification strategies, while holding potential benefits, can entail a risky approach. It allows companies to expand their operations into novel markets and industries, mitigating risks associated with reliance on a single domain. Nonetheless, it is imperative to acknowledge that successful diversification mandates an in-depth comprehension of the new industry and effective management of the diversified businesses [16].

The success of a strategy hinges not only on the choice of transaction type but also on how it integrates within the overall corporate strategy. Mergers and acquisitions must be well-aligned with the company's business model, values, and objectives. Instances of unsuccessful deals, as unveiled in our study, underscore the significance of integration at all levels [17].

This study took an analytical method to investigate the M&A process and used it to outline the commonly used key strategies that work in the competitive environment of financial markets. An identical approach was taken in by Lüdeke-Freund et al. [73], who developed a typology of a circular business model. Katz [74] believed that innovative strategies ensure a dominant position in the M&A market. Considering the external challenges, market conditions, global policy priorities, and the dynamic capabilities of the national economy, the strategic management framework will have a four-strategy topology underpinning it, as revealed in this study. Note that resource complementarity is an important aspect to consider when rescheduling mergers and acquisitions, as it has a significant impact on company’s performance [71, 72]. This suggestion is consistent with the present study. Finally, the results of this study suggest that in the post-pandemic world, M&A traders will be oriented towards investment retention, regardless of the economic activity level in the country. Consequently, developed economies need to direct their focus towards financial growth through the use of investment and financial strategies. The developing economies, on the other hand, bear the brunt of investment downturn, which requires them to implement organizational and innovation strategies.

This study aimed to develop a practical foundation for strategic investment management and to implement it into business practice through a universal framework. The flows of foreign direct investment (FDI) within the context of mergers and acquisitions play a pivotal role, in supporting the growth of companies and national economies while also facilitating technology transfer, innovation, and global market penetration. FDI has a broader impact beyond mere capital integration via M&A. Comparative analysis of FDI inflows in Russia and Azerbaijan revealed common trends in the development of mergers and acquisitions markets, including during the COVID-19 pandemic.

The research findings confirm that mergers and acquisitions (M&A) remains a significant instrument for stimulating growth and exploring new opportunities, especially in developed countries. However, in emerging financial markets, a reduction in direct investments and diminished competitiveness may be observed. The proposed universal typology of M&A strategies, rooted in global policy and economic dynamics, will contribute to enhancing managerial decision-making in crises.

The study further provides a decision-making process framework for M&A in financial markets post-pandemic. The obtained results have led to the development of a comprehensive typology of M&A strategies, enriching the comprehension of merger and acquisition structures within a global context. The application of the research outcomes enhances the efficacy of M&A activities and contributes to ensuring long-term business sustainability across diverse economies.

Suggested future research endeavours may extend the current work by broadening its scope of application and delving deeper into various facets of merger and acquisition strategies. They can build upon the present study's findings, utilizing its data and conclusions as a foundational point while delving into narrower thematic areas or more intricate aspects. Novel inquiries could encompass the analysis of international and sectoral variations, the impact of social and environmental dimensions, and a more profound understanding of management's role, temporal factors, and the enduring repercussions in successful M&A deals. Such investigations will serve to complement and enrich the general comprehension of the strategic facets of mergers and acquisitions, offering more precise recommendations and insights for business, academia, and practice.

[1] United Nations. The 17 goals. https://sdgs.un.org/goals.

[2] Magomedov, I.A., Murzaev, H.A., Bagov, A.M. (2020). The role of digital technologies in economic development. IOP Conference Series: Materials Science and Engineering, 862(5): 052071. https://doi.org/10.1088/1757-899X/862/5/052071

[3] Naidoo, R., Fisher, B. (2020). Reset sustainable development goals for a pandemic world. Nature, 583(7815): 198-201. https://doi.org/10.1038/d41586-020-01999-x

[4] Teece, D., Pizano, G., Shuen, A. (1997). Dynamic capabilities and strategic management. Strategic Management Journal, 18(7): 509-533. https://doi.org/10.1002/(SICI)1097-0266(199708)18:7<509::AID-SMJ882>3.0.CO;2-Z

[5] Ali, D.S.A., Bansal, A. (2020). An impact of Mergers and Acquisitions (M&A) to achieve inexpensive advantage in the economy of Bahrain. Journal of Critical Reviews, 7(3): 4-16. http://doi.org/10.31838/jcr.07.03.02

[6] Belyh, A. (2019). A historical analyses of M&A waves. https://www.cleverism.com/historical-analysis-ma-waves-mergers-acquisition.

[7] Global Mergers & Acquisitions Review, Full year 2020. https://thesource.refinitiv.com/TheSource/getfile/download/41c601c5-db24-469e-bfc4-197c5482c79d.

[8] Meglio, O. (2020). Towards more sustainable M&A deals: Scholars as change agents. Sustainability, 12(22): 9623. https://doi.org/10.3390/su12229623

[9] Alcalde, N., Powell, R. (2022). Government Intervention in European mergers and acquisitions. The North American Journal of Economics and Finance, 61: 101689. https://doi.org/10.1016/j.najef.2022.101689

[10] Dadush, U. (2022). Deglobalisation and protectionism. Working paper 18/2022. Bruegel, Brussels.

[11] PwC Global M&A Industry Trends: 2023 Outlook. https://www.pwc.com/gx/en/services/deals/trends.html.

[12] Suryaningrum, D.H., Abdul Rahman, A.A., Meero, A., Cakranegara, P.A. (2023). Mergers and acquisitions: Does performance depend on managerial ability? Journal of Innovation and Entrepreneurship, 12: 30. https://doi.org/10.1186/s13731-023-00296-x

[13] Patel, K. (2021). The ultimate guide to mergers and acquisitions. M&A Management Software. https://dealroom.net/faq/mergers-and-acquisitions-m-a-meaning.

[14] Yelchibayeva, A., Ryskulova, A.-G., Baimuratova, M., Kapanov, G., Sharipova, G., Maksutova, A. (2021). Analysis of financial and economic aspects of company functioning and their influence on the tourist cluster. Journal of Environmental Management and Tourism, 12(8): 2157-2167. https://journals.aserspublishing.eu/jemt/article/view/6659

[15] Hossain, M.S. (2021). Merger & Acquisitions (M&As) as an important strategic vehicle in business: Thematic areas, research avenues & possible suggestions. Journal of Economics and Business, 116: 106004. https://doi.org/10.1016/j.jeconbus.2021.106004

[16] Bettinazzi, E.L., Miller, D., Amore, M.D., Corbetta, G. (2020). Ownership similarity in mergers and acquisitions target selection. Strategic Organization, 18(2): 330-361. https://doi.org/10.1177/1476127018801294

[17] Chiu, W.H., Shih, Y.S., Chu, L.S., Chen, S.L. (2022). Merger and acquisitions integration, implementation as innovative approach toward sustainable competitive advantage: A case analysis from Chinese sports brands. Frontiers in Psychology, 13: 869836. https://doi.org/10.3389/fpsyg.2022.869836.

[18] Lin, B.W., Chen, W.C., Chu, P.Y. (2015). Mergers and acquisitions strategies for industry leaders, challengers, and niche players: “Interaction effects of technology positioning and industrial environment”. Transactions on Engineering Management, 62(1): 1-9. https://doi.org/10.1109/TEM.2014.2380822

[19] Nguyen, H.T., Yung, K., Sun, Q. (2012). Motives for mergers and acquisitions: Ex-post market evidence from the US. Journal of Business Finance & Accounting, 39(9-10): 1357-1375. https://doi.org/10.1111/jbfa.12000

[20] Cirjevskis, А. (2022). Valuing collaborative synergies with real options application: from dynamic political capabilities perspective. Journal of Risk and Financial Management, 15(7): 281. https://doi.org/10.3390/jrfm15070281

[21] Hassan, M., Giouvris, E. (2020). Financial institutions mergers: A strategy choice of wealth maximisation and economic value. Journal of Financial Economic Policy, 12(4): 495-529. https://doi.org/10.1108/JFEP-06-2019-0113

[22] Barykin, S.E., Kapustina, I.V., Korchagina, E.V., Sergeev, S.M., Yadykin, V.K., Abdimomynova, A., Stepanova, D. (2021). Digital logistics platforms in the BRICS countries: Comparative analysis and development prospects. Sustainability, 13(20): 11228. https://doi.org/10.3390/su132011228

[23] Saratovsky, A.D. (2014). Motives of mergers and acquisitions. Problems of Economics and Management, 9(37): 1-4. https://cyberleninka.ru/article/n/motivy-sdelok-sliyaniy-i-pogloscheniy

[24] CFA Institute. (2022). Mergers and Acquisitions. https://www.cfainstitute.org/en/membership/professional-development/refresher-readings/mergers-acquisitions#:~:text=The%20motives%20for%20M%26A%20activity,possibilities%20of%20uncovering%20hidden%20value.

[25] CFI team (2023). Motives for Mergers. The most common reasons for M&A deals. https://corporatefinanceinstitute.com/resources/valuation/motives-for-mergers/.

[26] Ray, K.G. (2022). Mergers and Acquisitions: Strategy, Valuation and Integration. PHI Learning Pvt. Ltd., Delhi.

[27] Rabier, M.R. (2017). Acquisition motives and the distribution of acquisition performance. Strategic Management Journal, 38(13): 2666-2681. https://doi.org/10.1002/smj.2686

[28] Sergeevna, B.L. (2019). Features assessment of Russia financial performance of mergers and acquisitions. International Transaction Journal of Engineering, Management, & Applied Sciences & Technologies, 10(7): 987-996. https://doi.org/10.14456/ITJEMAST.2019.94

[29] Feldman, R., Hernandez, Е. (2021). Synergy in mergers and acquisitions: Typology, lifecycles, and value. Academy of Management Review, 47(4): 1-57. https://doi.org/10.5465/amr.2018.0345

[30] Huhtilainen, М., Saastamoinen, J., Suhonen, N. (2022). Determinants of mergers and acquisitions among Finnish cooperative and savings banks. Journal of Banking Regulation, 23: 339-349. https://doi.org/10.1057/s41261-021-00170-4

[31] Van Dijk, В. (2020). S&P Global Market Intelligence. https://inventure.com.ua/analytics/investments/obzor-mirovogo-rynka-manda:-3-kvartal-2020.

[32] Junzhi, D., Chakrabarti, R., de Moraes, K.M.K., Gomes, L.F.A.M., Skvortsova, I. (2020). M&As trends in emerging capital markets. Strategic Deals in Emerging Capital Markets, pp. 3-31. https://doi.org/10.1007/978-3-030-23850-6_1

[33] Rohrich, K. (2020). 2020 Investment Climate Statements: Azerbaijan. https://www.state.gov/reports/2020-investment-climate-statements/azerbaijan/.

[34] Askerov, I., Janmammadov, А., Hasanova, L., Kamal Huseynli, K. (2020). Doing Business in Azerbaijan: Overview. MGB Law Offices, Baku.

[35] Pashtova, L.G., Maimulov, M.S. (2020). M&A market efficiency in Russia: Problems and prospects. Finance: Theory and Practice, 24(1): 76-86. https://doi.org/10.26794/2587-5671-2020-24-1-76-86

[36] Ivashkovskaya, I., Grigorieva, S., Nivorozhkin, E. (2020). Strategic Deals in Emerging Capital Markets. Springer International Publishing, Cham.

[37] Golbe, D.L., White, L.J. (1987). Mergers and acquisitions in the US economy: An aggregate and historical overview. University of Chicago Press.

[38] Fred Weston, J. (2001). Merger and acquisitions as adjustment processes. Journal of Industry, Competition and Trade, 1(4): 395-410. https://doi.org/10.1023/A:1019518909366

[39] Burke, R.J., Nelson, D. (1998). Mergers and acquisitions, downsizing, and privatization: A North American perspective. The New Organizational Reality: Downsizing, Restructuring, and Revitalization, pp. 21-54. https://doi.org/10.1037/10252-001

[40] Chang, B.H., Ki, E.J. (2004). A longitudinal analysis of mergers and acquisitions patterns of radio companies in the US. Journal of Radio Studies, 11(2): 194-208. https://doi.org/10.1207/s15506843jrs1102_5

[41] Guardin, S.V., Chekun, I.N. (2007). Mergers and acquisitions: An effective strategy for Russia. Peter, St. Petersburg.

[42] Golbe, D.L., White, L.J. (1993). Catch a wave: The time series behavior of mergers. The Review of Economics and Statistics, 75(3): 493-499. https://doi.org/10.2307/2109463

[43] DePamphilis, D. (2019). Mergers, Acquisitions, and Other Restructuring Activities: An Integrated Approach to Process, Tools, Cases, and Solutions. Academic Press.

[44] Gohan, P.A. (2007). Mergers, acquisitions and restructuring of companies. Trans. from English, Alpina Business Books, Moscow.

[45] Breili, R., Maiers, S. (2008). Principles of corporate finance. ZAO “Olimp-Biznes”, Moscow.

[46] Vorotnikova, I., Pshipiy, I. (2015). Mergers and acquisitions: Motives, approaches. Risk: Resources, Information, Supply, Competition, 3: 336-339. https://cyberleninka.ru/article/n/sliyaniya-i-pogloscheniya-utochnenie-terminologii-1

[47] Terekhin, V.I., Pronin, M.V. (2007). Problems and the method of economic evaluation of mergers and acquisitions. Socio-Economic Phenomena and Processes. https://cyberleninka.ru/article/n/problemy-i-sposob-ekonomicheskoy-otsenki-sliyaniy-i-pogloscheniy.

[48] Bauer, F., Friesl, M. (2022). Synergy evaluation in mergers and acquisitions: An attention-based view. Journal of Management Studies. https://doi.org/10.1111/joms.12804

[49] Kwilinski, A., Slatvitskaya, I., Dugar, T., Khodakivska, L., Derevyanko, B. (2020). Main effects of mergers and acquisitions in international enterprise activities. International Journal of Entrepreneurship, 24: 1-8. https://www.proquest.com/openview/3026494f5a03ac14846c9581394d4d09/1?pq-origsite=gscholar&cbl=29727

[50] Zhou, X., Zhang, X.Z. (2011). Strategic analysis of synergistic effect on M&A of volvo car corporation by geely automobile. I-Business, 3(1): 5-15. https://doi.org/10.4236/ib.2011.31002

[51] Mergers and acquisitions. WallStreetMojo. https://www.wallstreetmojo.com/mergers-and-acquisitions/.

[52] Deloitte. (2020). The state of the deal M&A trends. https://www2.deloitte.com/content/dam/Deloitte/us/Documents/mergers-acqisitions/us-mna-trends-2020-report.pdf.

[53] UNCTAD. (2020). World Investment Report 2020. International Production Beyond the Pandemic. United Nations Conference on Trade and Development, Geneva and New York, NY.

[54] UNCTAD. (2021). The least developed countries in the post-COVID world: Learning from 50 years of experience. United Nations. https://unctad.org/system/files/official-document/ldc2021overview_ru.pdf.

[55] Bloomberg Terminal. (2023). Bloomberg. https://www.bloomberg.com/professional/solution/bloomberg-terminal.

[56] Thomson Reuters Eikon. (2023). https://citing.bceln.ca/index.php/Thomson_Reuters_Eikon_-_Data.

[57] McKinsey & Company. (2023). https://www.mckinsey.com/.

[58] PwC. (2023). https://www.pwc.com/.

[59] International Monetary Fund. (2022). World Economic Outlook Database. https://www.imf.org/en/Publications/WEO/weo-database/2022/.

[60] The World Bank. (2022). Industry (including construction), value added (% of GDP). https://data.worldbank.org/indicator/NV.IND.TOTL.ZS.

[61] Ridevsky, G. (2022). Post-Soviet states: Demography, economy, standards of living. https://www.np-aaii.ru.

[62] Levy, В. (2021). Global M&A Industry Trends. https://www.pwc.com/gx/en/services/deals/trends.html.

[63] Petrashova, L. (2021). The M&A market in Russia in 2020. KPMG in Russia and the CIS. https://www.epravda.com.ua/rus/tags/m-a/.

[64] Baik, B., Cho, K., Choi, W., Kang, J. K. (2015). The role of institutional environments in cross-border mergers: A perspective from bidders’ earnings management behavior. Management International Review, 55(5): 615-646. https://doi.org/10.1007/s11575-015-0249-4

[65] Ganbarov, F., Smoląg, K., Muradov, R., Aghayeva, K., Jafarova, R., Mammadov, Y. (2020). Sustainable development of the mortgage market in Azerbaijan: Commercial risks of housing construction, social vision, and state influence. Sustainability, 12(12): 5116. https://doi.org/10.3390/su12125116

[66] Bukharbayeva, A.Z., Nauryzbayev, A.Z., Jrauova, K.S., Oralbayeva, K., Aimagambetova, A.D. (2020). Formation of the transport and logistics system as the basis for rice production development in the Kazakhstan Aral Sea region in the context of the EAEU economic integration. Academy of Strategic Management Journal, 19(3): 1-7.

[67] Hečková, J., Štefko, R., Frankovský, M., Birknerová, Z., Chapčáková, A., Zbihlejová, L. (2019). Cross-border mergers and acquisitions as a challenge for sustainable business. Sustainability, 11(11): 3130. https://doi.org/10.3390/su11113130

[68] Gaughan, P.A. (2018). Mergers, acquisitions and restructuring of companies. Wiley Corporate F&A.

[69] King, D.R., Bauer, F., Schriber, S. (2018). Mergers and Acquisitions: A Research Overview. Routledge, London.

[70] Freshfields Bruckhaus Deringer. (2021). M&A monitor of 2021. https://www.freshfields.com/4966f0/globalassets/our-thinking/campaigns/ma-monitor/21q1/ma_monitor-q1-2021.pdf.

[71] Guliyev, Z. (2019). Current state and development of the manufacturing industry in the Republic of Azerbaijan. Gorizonty ekonomiki (The Horizons of Economy), 35(51): 60-70 (in Russian, print).

[72] Prayogi, J., Wibowo, А. (2022). The effect of resource complementarity on a company's performance post-merger and acquisition in the Southeast Asia Region: The moderating role of the merger and acquisition experience. Gadjah Mada International Journal of Business, 24(2): 223-244.

[73] Lüdeke-Freund, F., Gold, S., Bocken, N.M. (2019). A review and typology of circular economy business model patterns. Journal of Industrial Ecology, 23(1): 36-61. https://doi.org/10.1111/jiec.12763

[74] Katz, M.L. (2021). Big Tech mergers: Innovation, competition for the market, and the acquisition of emerging competitors. Information Economics and Policy, 54: 100883. https://doi.org/10.1016/j.infoecopol.2020.100883