Neha Bansal![]() | Sanjay Taneja

| Sanjay Taneja![]() | Ercan Ozen*

| Ercan Ozen*![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Green banking (GB), which aligns financial practices with environmental sustainability, is becoming increasingly important in solving modern global concerns such as climate change and resource conservation. This research examines the notion of GB and its significant consequences for the environmental performance of the banking sector in Punjab (India). The unique economic and environmental characteristics of Punjab makes it an essential area for investigating the implementation of GB strategies. The research focuses on the intricate relationship between operations-related GB strategies and a bank's environmental performance, particularly emphasizing the mediation of banks’ green financing. Data for this study was meticulously gathered from public and private sector bank employees, comprising 290 participants. Structural Equation Modeling (SEM) method was utilised for the analysis and the findings demonstrate a statistically significant and positive relationship among the variables indicated above. Furthermore, the research reveals that green finance partially mediates this relationship. These results have far-reaching implications for the banking sector's various stakeholders. This research can help regulatory authorities and policymakers in the conceptualization of laws and regulations that encourage green banking adoption. Banking institutions, in turn, may use this knowledge to improve their strategies and operations, improving environmental performance while preserving financial stability.

green banking, green banking strategies, environmental performance, green financing, banking sector, Punjab, India, Structural Equation Modelling (SEM), PLS-SEM and mediation analysis

The modern world is at a crucial crossroads; it faces a wide range of environmental problems that go beyond regional and social lines and risk the sensitive balance of the planet as a whole [1]. As climate change gets worse, the world's temperature is going up, the weather is becoming more unpredictable, and natural disasters are getting worse [2]. Likewise, the rapidly occurring loss of ecological diversity caused by natural damage and pollution threatens the complex web of life that keeps the environment alive [3]. As the rate at which resources are used up exceeds the rate at which they are replaced, worries about resource shortage and loss are growing [4, 5]. Because of these problems, the attitude towards growth and success must change significantly, not just in small ways. In this time of severe environmental problems, finding new ways to balance the needs of economic growth and environmental protection has become more critical [6]. In this situation, the idea of green financing (GF) stands out as a ray of light, showing a way to a more sustainable future [7-9]. Therefore, considering the mounting environmental concerns worldwide, the present study aims to evaluate the impact of green banking (GB) strategies on the environmental performance (EP) of the banks. The authors also strive to analyse the role of the bank’s GF efforts in strengthening this relationship.

Based on sustainable finance concepts [10, 11] GF blurs the lines between economic activity and the environment, creating a mutually beneficial connection between the two [12-14]. It is a strategy for encouraging actions and endeavors that are good for the environment by tapping into the vast resources of the finance sector [15]. Financial capital is channeled into initiatives that mitigate climate change, boost energy efficiency, and promote sustainable land and water management [16-18] via methods such as sustainability-linked loans, green bonds and impact investments [19, 20].

Green banking (GB) is an essential component of the GF ecosystem since it integrates environmental concerns into the daily operations of banks [21-23]. GB involves a wide range of practices, from supporting sustainable operating methods within banks to implementing strict environmental standards for lending and investment choices [24, 25]. This shift in perspective reflects an acknowledgement that the financial sector can bring good change by distributing resources in ways that strengthen ecological resilience [26]. Stakeholders, from environmentally conscious consumers and impact investors to legislators seeking to achieve systemic sustainability, are finding common ground in the increasing convergence between financial systems and environmental imperatives [27]. This game-changing strategy is in synchronization with the worldwide drive towards the SDGs, and it tackles the associated problems of environmental degradation [22, 28].

As per the reports [29], India has emerged as the third-highest carbon emitter in the world after China and the USA. The increasing carbon emissions observed in India may be attributed to the fast industrialization and economic expansion experienced in the country [30]. This situation is further emphasized by the government's ambitious goals of cutting CO2 emissions by 50% by the year 2050 and attaining net-zero emissions by 2070 [31]. Given the huge financial requirements surpassing $10 trillion required to achieve these objectives [32], banks are required to bridge financial gaps and guarantee a consistent transition.

Punjab is an important state in India with significant strategic and economic significance. The state is known for its agricultural production, which is a significant contributor to the nation's food security. The state also has a well-developed industrial sector and a thriving service sector [33]. However, Punjab has a significant carbon footprint. The primary sources of carbon emissions in Punjab are industrial activity, transportation, and agricultural practices. To resolve the challenges of carbon emissions in Punjab, the need for green banking becomes prominent.

Banking institutions have the potential to make substantial contributions to carbon reduction and climate resilience by adopting GB strategies [22, 34, 35]. Banks intentionally adopt GB strategies to fulfill their duties as facilitators for sustainable development, thereby providing support for investments in energy efficiency, renewable resources, and environmental preservation [36, 37]. Additionally, GB serve as guards against environmentally harmful projects [23]. The Reserve Bank of India (RBI) has released guidelines for banks regarding the green deposits that are earmarked for environmental initiatives; this step of RBI will boost the GF ecosystem in the banking sector of India [38]. The central bank acknowledges that climate risk and GF are no longer isolated issues but require appropriate policy attention. GB strategies not just aid in lowering carbon emissions yet also establish banks as significant partners in India's pursuit of sustainable development and ecological welfare [39].

The literature shows that several researches were undertaken worldwide to interpret the influence of GB strategies on the environmental performance (EP) of banks [40-44]. However, there is a lack of research on GB in India [22, 45]. Moreover, limited studies are conducted in Punjab, India to assess the impact of the daily operations related GB activities on the bank's EP based on the primary data. Green financing is a way for banks to support projects and efforts that are beneficial for the environment [46, 47]. Moreover, there are few empirical studies that have attempted to examine the mediating role of the GF in the effective implementation of GB strategies and their subsequent impact on the EP of the banks. Therefore, there is a dire need to conduct a quantitative study to assess the interrelationship among the identified variables.

The present study seeks to resolve the identified research gaps by analyzing the impact of the operations-related GB strategies on the EP of the banks with the mediation of GF. The data included in this research was obtained from the public and private sector bank employees in Punjab state of India. The structural equation modeling (SEM) method was utilized to evaluate the established relationship. In contrast, previous studies on GB generally employed multiple regression technique to assess the relationship among the parameters under study [40, 43, 44]. Consequently, the following are the main research questions for the research:

• Does the adoption of GB strategies in daily operational activities have any impact on the EP of the banks?

• Does GF mediate the relationship between operation-related GB strategies and the EP of the banks?

The subsequent sections are organized as follows: Section 2 includes the review of studies related to the GB strategies, EP of banks and banks’ GF, along with the theoretical framework of the study and hypotheses formulation. Section 3 provides a comprehensive description of the methodology adopted in the present research. Section 4 depicts the significant outcomes of the research analysis, followed by the discussion about the findings in Section 5. Section 6 encompasses concluding remarks, theoretical and practical implications, limitations of the research, and potential future research directions.

2.1 Theoretical background

On the theoretical side of the implementation of GB, there is, nevertheless, a dearth of study. Further studies are required, particularly in emerging economies, to look into and comprehend the variables affecting the implementation of green banking. Socially Responsible Investing (SRI) theory, which is often known as ethical investments or sustainable investments, is a prominent theory in the field [48-50]. SRI is a method of investing that incorporates social, environmental, and ethical factors into decision-making [51-53].

The significance of SRI theory is amplified in emerging economies due to several factors. These economies confront various environmental and social issues, such as poverty, inequality, and environmental degradation. SRI provides a mechanism to tackle these challenges by promoting sustainable and responsible business practices [54]. Furthermore, emerging economies often require significant investments to support the development of infrastructure and environmental initiatives. SRI has the potential to allocate financial resources towards initiatives that actively support sustainable development [55].

Specifically, among financial institutions and socially motivated businesses, SRI theory emphasizes pursuing well-being as well as financial objectives to solve rising environmental issues, generate employment, and promote rural and urban development [56]. Within the realm of GB, financial institutions are incentivized to allocate resources towards renewable energy initiatives, extend support to environmentally conscious businesses, and offer financial instruments that foster sustainability. The investments are guided by the principles of SRI, which aim to ensure their alignment with environmental and social responsibility objectives [57, 58]. The adoption of GB strategies by financial institutions can be interpreted as the incorporation of SRI principles into their operational framework, with the goal of pursuing both financial and societal objectives concurrently. Rehman et al. [42] recently conducted a study based on the SRI theory to evaluate the impact of GB strategies on the bank's EP in Pakistan.

2.2 Green banking

Green banking is the practice of using financial services to safeguard the environment by focusing on socioeconomic and environmental concerns [45]. The "green" in "green banking" refers primarily to banks' performance and environmental responsibility in their commercial activities [59]. In 1980, Triodos Bank, a Dutch bank, initiated the idea of "green banking" [37]. It established a "Green Fund" for ecological initiatives, which in 1990 turned into a model for banks that were looking into green banking strategies [60]. As a result, this is an emerging idea in the banking industry, with a desire to develop sustainable and environment friendly procedures against the external pressures that banks are experiencing.

GB comprises implementing environmentally-friendly procedures and lowering internal as well as external CO2 emissions as a consequence [36]. A significant pillar of the GB agenda is corporate social responsibility (CSR) [26], which is why it is sometimes referred to as ethical banking [61, 62]. It is a type of banking carried out in a particular area and manner that aids in lowering internal and external carbon footprints [63, 64] highlighted that green banks are necessary for the transition of the economy towards sustainable energy and to control climate change.

2.3 Operations-related GB strategies and bank’s green financing

Banks, like other businesses, recognize the significance of CSR and are conscious about protecting the environment and the biodiversity [65]. The banks are mostly helped by the technological environment and services like e-banking in promoting the concept of green banking [46]. Due to the consciousness towards the environment customers and bankers are actively reducing paperwork at all levels [66]. GB strategies are admired by researchers due to their numerous advantages, including their role in reducing internal and external carbon footprint [49, 67] enhancing the bank image and providing a competitive edge [50, 68] and, with enhanced operational efficiency, a boost in both economic and social growth [69].

The influence of banks' daily operations on the environment is highlighted by the carbon emissions they produce. These emissions come from various sources, including energy use, transportation, and infrastructure [70]. Operations-related GB strategies refer to deliberate activities and practises implemented by banking institutions to effectively incorporate the concepts of environmental sustainability and responsible resource management into their day-to-day operations. By implementing operations related GB strategies, including maximising energy consumption via effective systems, boosting remote work to cut down on travel, encouraging paperless transactions, and embracing renewable energy sources for facility powering, banks may successfully handle carbon emission concerns [35, 61, 71-73]. These emission reduction measures are essential not just for the environment but also for the overall functioning of banks. Reduced energy use results in lower costs, more efficient operations, and a stronger sense of CSR [22, 74]. Furthermore, adopting green banking principles into daily operations is critical since it corresponds with global imperatives to address climate change, demonstrating the banking industry's commitment to sustainable practices [26]. In turn, this encourages a more sustainable market environment by increasing public trust and luring customers and investors concerned about the environment [34, 68]. As environmental concerns shape the financial industry, incorporating green banking practices into daily operations benefits the ecological cause and strengthens banks' long-term resilience, competitive edge, and reputation in an increasingly environmentally conscious market milieu [45, 75].

In the goal of sustainable economic growth and environmental protection, GF and GB techniques are closely related [57, 58, 76]. The phrase "green finance", often referred as "green investing” describes financial contributions made to initiatives that promote environmentally friendly living as well as the growth of a more sustainable society [77, 78]. GF is the force behind GB endeavor, which aims to combine economic benefits with environmental enhancements [79]. It aims for a country's sustainable economic development by balancing monetary advancement with environmental security [14, 80]. The contribution of banks in lowering their internal and external carbon footprint via green financing for GB operations is a significant component of this synergy [60, 81]. Banks provide funds to a range of green finance initiatives in the areas of waste management, green building, sustainable manufacturing, industrial safety, clean and alternate energy, energy efficiency, and green tourism, as part of their GB objectives [46, 57, 58, 76, 82, 83]. This interaction highlights financial organizations’ comprehensive approach to matching operations with sustainability objectives and promoting ethical environmental behavior. According to recent research performed by several studies [18, 84], adopting GB techniques would positively affect the GF operations of Bangladeshi banks. Taneja and Özen [46] conducted another research in India and assessed the significance of banks' GF efforts in raising their EP. These hypotheses developed in light of the discussion above:

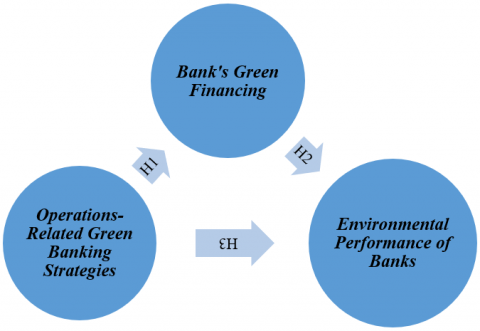

H1: There is relationship between the operations-related GB strategies and the bank's GF.

H2: There is a relationship between the bank’s GF and the EP of the banks.

2.4 Green banking strategies and the environmental performance of banks

Environmental sustainability has recently emerged as a critical concern for academics, regulators, and policymakers [85]. Target 13 of the SDGs calls for the creation of initiatives at all levels to reduce climate risks and save ecological resources [86]. The effect of an organization's activities on the environment is referred to as “Environmental Performance” [37]. To evaluate an organization's environmental performance, a multitude of indicators may be employed, such as reduced carbon emissions, pollution reduction, minimizing waste, and reusing materials [87, 88]. The assessment of reduced carbon emissions can be conducted by means of carbon footprint estimates, the monitoring of energy usage, and the utilisation of emission and conversion factors [89]. The process of reducing pollution entails the monitoring of effluents and emissions, as well as assuring adherence to environmental rules [18, 84]. The waste minimization can be assessed by means of waste audits, waste tracking, and reporting [90]. The assessment of material reuse can be conducted through the examination of material flow patterns and recycling rates [91]. These indicators offer significant insights into an organization's efforts towards environmental sustainability, facilitating better decision-making and goal-setting in order to mitigate environmental impact.

SBI, India's largest public sector bank, launched the "Yono SBI", an industry-first omnichannel digital platform, as part of its ongoing efforts to inform and transition its clients from paper-based banking to digital banking. Moreover, SBI introduced the "SBI Green Fund" to let consumers become involved in the sustainability objective. The SBI Green Fund intends to support initiatives that directly advance sustainability, such as planting trees, building bio-toilets, and offering solar lighting, lamps, and panels [92]. These initiatives by the bank significantly improved the EP of the bank.

Shaumya and Arulrajah [44] undertook a research in Sri Lanka to evaluate the influence of GB strategies on the EP of the banks. They applied univariate, bivariate, and multivariate analyses for assessing the collected data, and the findings depicted that there is a significant impact of the employee-related, daily operation- and policy-related GB strategies on the EP of the banks. Risal and Joshi [43] conducted a study in Nepal using multivariate analysis and concluded that the positive relationship between fuel efficiency and green policy had a significant impact on the EP of banks. A positive relationship among the GB initiatives and the EP of banks is also advocated in research conducted in Coimbatore city of India [40]. After the review of the existing studies, the research proposes the following hypotheses:

H3: There is a relationship between the operations-related GB strategies and the EP of the banks.

H4: The Bank's GF mediates the relationship between the operations-related GB strategies and the EP of the banks.

The study sets up a conceptual framework in which the bank's operations-related GB strategies acts as the “independent variable” and the bank's EP is the “dependent variable”. In this model, the bank's GF efforts play a key role as the "mediating variable". The relevance of GF efforts in influencing and mediating the influence on a bank's EP is highlighted by the framework, as shown in Figure 1. It shows the complex interactions between these variables and their contribution towards influencing the financial sector's environmental results.

Model of the study

The Figure 1 presents the Conceptual Framework of the study which was complied by the authors.

Figure 1. Conceptual framework

(Author's Compilation)

The current study is exploratory in nature, and the adapted questionnaire is used to gather the data from the employees of the banks (public and private sector) located in the Punjab state of India. The present research aims to investigate the relation among the operations-related GB strategies and the EP of the banks with the mediating role of the bank's GF. Construct validity evaluations and reliability metrics like Cronbach's alpha and Composite Reliability (CR) were used to thoroughly examine the adapted questionnaire's validity and reliability. The research methodology involves the application of SEM to rigorously test the formulated hypotheses and investigate the intricate relationships among these critical factors. The authors performed discriminant validity tests to confirm each construct's distinctiveness and meaningfulness. Direct effects were determined using path coefficient analysis, while multicollinearity was evaluated using the Variance Inflation Factor (VIF). A mediation study was carried out to comprehend both direct and indirect impacts to ensure an exhaustive evaluation of the SEM model.

3.1 Sample

The researchers employed the convenience sampling method to gather the data from the banks' employees in Punjab. The Punjab region has significantly aided the growth of the Indian economy, and it is known for its significant contributions to the country's agricultural and industrial sectors [93, 94]. Moreover, as per the RBI records, Punjab has a well-developed banking infrastructure with 6761 commercial, cooperative and regional rural bank branches serving customers across the state [38, 95]. Due to the significant number of operational bank branches of public and private sector banks, the researchers only collected data from these banking institutions. The generally accepted sample size is 150-400 for the SEM analysis [20, 96]. Additionally, the authors used the G*Power software to ascertain the minimal sample size needed [97] considering the effect size of 0.05 at a 95% confidence level. Thus, considering the suggested minimum level of power of 0.80 [98], the software proposed a sample size of 159. G*Power is utilised due to its efficacy in determining ideal sample sizes, facilitating a range of statistical tests, possessing a user-friendly interface, and offering cost-effectiveness [99]. Hence, in this context, the sample size of 290 is appropriate, as it effectively fulfils the minimum sample size requirements.

3.2 Data analysis

The authors used SEM technique to examine and model the intricate relationships among the variables under consideration. The research employs PLS-SEM, a robust and adaptable statistical approach well-suited for investigating latent components and their interdependencies [100]. The authors used PLS-SEM mediation analysis to dive further into the underlying processes and determine the presence of potential mediating components within the conceptual framework. This method evaluates the indirect impacts of variables, offering insight into the mediating mechanisms that underlie the relations noted in the study [101-103]. PLS-SEM, in conjunction with mediation analysis, provides a complete and rigorous framework for data analysis, ensuring a thorough exploration of the hypotheses and resulting in a deeper comprehension of the phenomenon being studied [104, 105].

3.3 Measurements

The researchers employed the adapted questionnaire to gather the data from the bank’s employees. In order to collect the relevant information, there are four sections in the questionnaire: demographic information, daily operations related GB strategies, the bank’s GF, and the EP of banks presents in Table A1. The information regarding the gender, age, and experience in number of years and educational qualification of the respondents are recorded in the demographic section. Three items in the construct of daily operations-related GB strategies were obtained from the work of [42]. The construct of the bank’s green financing was measured using the five items stemmed from the work of [57, 106]; however, one item, i.e., GF6, is deleted from the analysis due to the factor loadings below 0.5. The bank’s EP was assessed with four items adapted from the works [43, 44]. All the 12 items in the analysis are assessed on the 7-point Likert scale, with 1 indicating strongly disagree and 7 indicating strongly agree. The 7-point Likert scale was chosen because it strikes a balance between giving thorough answers and making them simple to comprehend, enabling nuanced participant feedback while keeping things simple for efficient data analysis.

4.1 Demographic information

Table 1 shows a thorough picture of the demographic landscape of respondents. The distribution of gender shows that Males account for 52% of the sample, while females account for 48%. The age distribution reflects a diversified workforce, with significant participation in the age group of 31-40 year (41.03%), followed by the age group of 18-30 year (26.55%), the 41-50 year age group (18.27%), and the 51 years and over (14.13%). The higher participation rate of those between the ages of 31-40 suggests that they may have a greater awareness of environmental issues due to their stage of life, which frequently involves career stability and responsibility, a period in which environmental concerns become more apparent. Due to the current global emphasis on sustainability in education, younger participants between the ages of 18-30 may exhibit a greater environmental consciousness. 43.79% have a bachelor's degree, 36.20% have a postgraduation degree, 4.48% have a PhD, and 15.51% are classified as "Others". In terms of experience, 52.75% have 1 to 5 years of work experience, 27.93% have more than 5 years, and 19.31% are younger entrants with less than 1 year. The notable proportion of participants with 1 to 5 years of experience suggests that this group is likely to be open to the emerging concept of environmental responsibility in banking operations. This inclination may affect their views on operations-related GB strategies and their impact on a bank's GF and EP.

Table 1. Demographic information

|

Variable |

Items |

Frequency |

Percent (%) |

|

Gender |

Male |

153 |

52.75 |

|

Female |

137 |

47.24 |

|

|

Age (Years) |

18-30 |

77 |

26.55 |

|

31-40 |

119 |

41.03 |

|

|

41-50 |

53 |

18.27 |

|

|

51 and above |

41 |

14.13 |

|

|

Academic Qualifications |

Graduation |

127 |

43.79 |

|

Postgraduation |

105 |

36.20 |

|

|

PhD |

13 |

4.48 |

|

|

Others |

45 |

15.51 |

|

|

Experience |

Upto 1 year |

56 |

19.31 |

|

1 to 5 years |

153 |

52.75 |

|

|

More than 5 years |

81 |

27.93 |

Source: Compiled by author

4.2 Descriptive statistics

The foundation of the employed model is measurement model, intended to examine the link between latent variables and corresponding measurements [107]. This crucial component is used to evaluate the constructs' reliability and validity. This is crucial in the context of PLS-SEM since it commences the evaluation of the precision and coherence exhibited by the indicators. The internal consistency was evaluated by employing Cronbach's alpha and Composite Reliability (CR), which has a limit of 0.70 [108]. The convergent validity was measured with average variance explained (AVE), which typically needs to be higher than 0.50 [101]. Figure 2 and Table 2 show the results of convergent validity and internal reliability. The constructs demonstrate strong internal consistency, with Cronbach's alpha and CR values exceeding the suggested limit of 0.70 for all three constructs. This implies that the items within each construct exhibit strong correlations and accurately assess the underlying construct. AVE values were also more than 0.5, this implies that the items within each construct converge well and measure the intended construct coherently, indicating a high level of convergent validity. These findings support the measurement model's robustness, which additionally indicate reliable and acceptable representations of the latent constructs.

Figure 2. Measurement model results

Table 2. Model estimates

|

Variables |

Cronbach's alpha |

CR |

AVE |

|

E |

0.868 |

0.91 |

0.716 |

|

GF |

0.822 |

0.877 |

0.592 |

|

OR |

0.81 |

0.887 |

0.723 |

Note: E = Environmental Performance, GF = Green Financing, OR = Operations- Related GB Strategies

4.3 Discriminant validity

After examining the model's convergent validity and construct reliability, the next stage was to determine its discriminant validity. To establish discriminant validity, two techniques were used: Fornell-Larcker method and the HTMT ratio. According to the study [109], method findings shown in Table 3 displays the square root of the AVE for each diagonal construct as well as the relationships between diagonal constructs. The data show that each construct has more variation with its indicators than other constructs' indicators, proving discriminant validity.

Table 3. Fornell–Larcker criterion

|

E |

GF |

OR |

|

|

E |

0.846 |

||

|

GF |

0.593 |

0.77 |

|

|

OR |

0.598 |

0.601 |

0.851 |

Note: E = Environmental Performance, GF = Green Financing, OR = Operations- Related GB Strategies

Table 4. HTMT ratio

|

E |

GF |

OR |

|

|

E |

|||

|

GF |

0.694 |

||

|

OR |

0.693 |

0.719 |

Note: E = Environmental Performance, GF = Green Financing, OR = Operations- Related GB Strategies

HTMT criteria may also be adopted to evaluate the discriminant validity of the constructs [110]. Table 4 Analysis shows that, all HTMT ratios were less than the suggested limit of 0.85. This means the correlations between constructs were considerably lower than the average correlations between construct indicators. As a result, the HTMT ratios support discriminant validity by demonstrating that the constructs are distinct and do not measure the same underlying concept.

4.4 Structural model

The structural model analysis was utilised to determine how well the independent constructs predicted the variability in the dependent construct [105]. Evaluation of collinearity is the first stage in structural model analysis. Collinearity is concern in structural model analysis related to significant intercorrelations among predictor variables, resulting in unstable and unreliable regression coefficient estimations mentioned in Table 5. The VIF is utilized in this study to assess multi-collinearity concerns. The test findings provided in Table 5 shows that all of the values were below the limit of 3.33 [108] and ranged from 1.18 to 2.46.

Table 5. Multi-collinearity test

|

Items |

VIF |

|

E1 |

1.961 |

|

E2 |

2.463 |

|

E3 |

1.811 |

|

E4 |

2.35 |

|

GF1 |

1.761 |

|

GF2 |

2.134 |

|

GF3 |

1.964 |

|

GF4 |

2.41 |

|

GF5 |

1.183 |

|

OR1 |

1.729 |

|

OR2 |

2.099 |

|

OR3 |

1.685 |

4.4.1 Path analysis

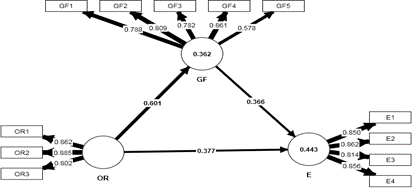

Path coefficients, often referred to as beta coefficients, are used in the structural model to depict the relationships among latent variables. The magnitude, direction, and importance of the relationship among the latent variables are shown by these path coefficients [111]. Typically, the appropriate range of statistical significance is defined as t-values of 1.96 or above. The model was assessed using PLS-SEM, which possesses all essential modelling and computing abilities. Figure 3 and Table 6 show the conclusions of the model evaluation.

Figure 3. Analysis of structural model

Table 6. Path analysis

|

β |

Mean |

Std. Dev. |

t-statistics |

p |

|

|

GF -> E |

0.366 |

0.368 |

0.06 |

6.071 |

0 |

|

OR -> E |

0.377 |

0.378 |

0.061 |

6.196 |

0 |

|

OR -> GF |

0.601 |

0.605 |

0.042 |

14.459 |

0 |

Note: E = Environmental Performance, GF = Green Financing, OR = Operations- Related GB Strategies

Table 7. Hypotheses testing

|

Hypotheses |

β |

t-statistics |

2.50% |

97.50% |

p |

Decision |

|

(H1) OR -> GF |

0.601 |

14.459 |

0.521 |

0.682 |

0 |

Supported |

|

(H2) GF -> E |

0.366 |

6.071 |

0.247 |

0.484 |

0 |

Supported |

|

(H3) OR -> E |

0.377 |

6.196 |

0.256 |

0.494 |

0 |

Supported |

Note: E = Environmental Performance, GF = Green Financing, OR = Operations- Related GB Strategies

Table 8. Mediation analysis

|

Path |

Total Effect |

Direct Effect |

Indirect Effect |

|||||||

|

β |

t-statistics |

p |

β |

t-statistics |

p |

β |

t-statistics |

p |

||

|

OR -> E |

0.598 |

14.162 |

0 |

0.377 |

6.196 |

0 |

OR -> GF -> E |

0.22 |

5.387 |

0 |

Note: E = Environmental Performance, GF = Green Financing, OR = Operations- Related GB Strategies

4.4.2 Hypotheses testing

The bootstrapping method was employed in this investigation to ascertain the significance of each structural path. The findings shown in Table 7 indicate a positive and significant relationship between the operations-related GB strategies and the GF by the banks (β = 0.601, t = 14.459, p < 0.000). The research results showed a significant and positive relationship between the operation-related GB strategies and the EP of the banks (β = 0.377, t = 6.196, p < 0.000). The impact of GF strategies of the banks on the EP of the banks is also significant and positive, as indicated by the findings of the study (β = 0.366, t = 6.071, p < 0.000).

4.3.3 Analysis of mediation

The inclusion of a mediation analysis was an essential component of this study, as it aimed to gain insight into the fundamental processes by which GF and operations-related GB strategies impact the EP of banks. Mediation analysis is a useful tool for investigating the indirect pathway through which a variable influences another, shedding light on the role of GF as a mediator in the relationship between operations-related GB strategies and EP (Table 8). The direct effects indicate that both GF and operation-related GB strategies have positive and significant impacts on EP, highlighting the importance of sustainable financing and banking practices in enhancing environmental performance. Specifically, these impacts demonstrate that both GF and operations-related GB policies independently lead to a better EP for banks. Additionally, the indirect effect reveals that GF partially mediates the relationship between Operations-related GB strategies and EP (β= 0.22, t= 5.387, p < 0.000), suggesting that it serves as a pathway through which banks can improve their environmental performance. This indicates that utilizing GF, in conjunction with implementing GB strategies, can have a more pronounced positive effect on the EP of banks. Findings shown in Table 8 emphasize the vital role of green banking strategies and eco-friendly financing options in driving positive environmental outcomes.

The hypotheses investigated in this research sought to elucidate the intricate relationships between Operation-Related GB Strategies, GF, and EP in the banking sector. The results of the extensive analysis utilizing PLS-SEM provide enlightening insights on the outcomes.

By showing a significant positive relationship between operation-related GB strategies and GF, the research offers findings in support of Hypothesis 1. According to the robust path coefficient, banks that adopt environmentally friendly operating strategies are more likely to provide green financing solutions. These results agree with those of previous research [42, 57, 58]. These researches also confirmed that reduced use of paper and e-banking services have positively impacted the financing of eco-friendly projects. In line with the expanding trend of incorporating green strategies into core banking operations, this research highlights the critical role that sustainable operational strategies play in promoting environmentally responsible financial products and services. Theoretical implications imply that incorporating environmental concerns into fundamental banking operations is consistent with a worldwide movement towards sustainable practices.

In line with Hypothesis 2, the findings show a favorable and substantial relationship between a bank's GF and EP. These results emphasize the critical role of GF in influencing banking industry environmental outcomes for the better. The results align with the existing studies [46, 57, 58]. Therefore, it can be asserted that GF has evolved as a catalyst for promoting sustainable economic growth, with a focus on social responsibility and environmental issues. In practical terms, the allocation of resources towards environmentally friendly initiatives not only improves ecological outcomes but also corresponds with worldwide sustainability goals, hence underscoring the need of incorporating sustainability into financial plans.

Hypothesis 3 is confirmed by the outcomes of the analysis, which show a significant relationship between Operation-Related GB Strategies and EP. The direct positive impact of green operating strategies on EP shows the significance of banks' internal environmental initiatives. Moreover, studies [40, 43, 44] also confirmed the significant relationship between banks' operation-related green strategies and EP. Theoretically, this is consistent with the prevailing society and industrial trends advocating for adopting sustainable practices. The implementation of green operational strategies, such as using energy-efficient technology and adopting ethical waste management practises, has been seen to significantly improve a bank's EP, hence facilitating the establishment of sustainable business practices.

The study supports Hypothesis 4 by showing that the relationship between operation-related GB strategies and EP is partially mediated by banks' GF. This emphasizes the function of green financing as an instrument for translating sustainable operational strategies into positive environmental outcomes. Banks that provide green finance may enable and incentivize investments in environmentally friendly initiatives, enhancing their contributions to improved environmental performance. This is the first study carried out in India, to the best of the researcher' knowledge that aims to evaluate the mediating role of GF on operation-related GB strategies and the banks' EP. This research distinguishes itself by placing emphasis on mediation within the Indian banking sector, providing a novel and valuable viewpoint on the relationship between sustainable practices, financing, and environmental impact. However, a study conducted in Bangladesh confirms the mediating role of GF on GB activities and EP [57, 58]. The confirmation of this study's regional significance is reinforced by its comparison with a comparable study conducted in Bangladesh, emphasizing its unique insights that are specifically adapted to the banking sector in India.

The research has revealed substantial relationships between GF, operation-related GB strategies, and EP in the banking sector of Punjab. The investigation of construct validity, reliability, and mediation pathways has generated valuable insights that benefit to the disciplines of GF, GB, and EP both at the practical and theoretical levels. The findings highlight the potential for banks to improve their environmental performance by implementing sustainable practices and strategically promoting eco-friendly financing options. The mediating role of Green Financing bolsters its significance as the pathway through which green banking strategies positively influence environmental outcomes. Overall, these findings represent significant progress in comprehending the mutually beneficial connection between sustainable banking practices, financing, and environmental accountability, as the results highlight the transformative potential of integrating sustainable practices and environmentally friendly financing into the banking sector.

This investigation has two theoretical implications: First, it helps to better explain the relationships between GF, Operation-Related GB Strategies, and EP, enriching existing theories in green finance and green banking by highlighting the importance of internal green initiatives within the banking sector. Second, the study expands the theoretical discourse on mediation mechanisms in sustainable finance by emphasizing the role of GF in mediating the relationship between operation-related GB strategies and EP. Furthermore, the study's context-specific insights from an emerging economy viewpoint contribute significantly to the theoretical generalizability of these relationships. This combination of green finance and banking practices adds to a comprehensive framework that spans these domains and provides insights for scholars and practitioners investigating the complexity of promoting environmental responsibility through banking strategies and financial mechanisms.

The research findings have practical relevance for both public and commercial banks. The results indicated that banks could improve their environmental performance by implementing sustainable practices such as eco-friendly financing and operation-related GB strategies through comprehensive construct validity and reliability tests and mediation studies. Green Financing emerges as a critical intermediary, allowing banks to enhance their positive impact on environmental performance. These findings highlight the potential for banks to not just conform to changing regulatory demands and boost stakeholder confidence but also to stimulate collaboration for collective sustainable banking efforts. Finally, the results of this research give practical recommendations to banks to take an active role in promoting environmental stewardship while portraying themselves as positive change agents in the banking industry and beyond. Policymakers and practitioners can utilise these findings to formulate policies and strategies that facilitate the adoption of sustainable banking practices and advocate for the incorporation of environmentally friendly initiatives within the banking industry. This alignment is crucial for the attainment of the broader sustainability goals.

Although this research gives significant insights, it is critical to recognize its limits. The study's emphasis on the Punjab region may limit its generalization while extrapolating findings to other geographic contexts, caution is advised because environmental dynamics and banking practices might differ. Second, relying on self-reported data may result in response biases. Awareness of these biases is essential for accurately interpreting observed relationships and their implications. Future research might include a larger range of financial institutions and areas to enhance the scope of the study, providing a more thorough knowledge of the relationships investigated. In addition, qualitative research could provide a deeper understanding of the mechanisms underlying the identified relationships. Future research might also examine the influence of regulatory settings and consumer perceptions in determining GB strategies and environmental impacts. Longitudinal research might also give information on the long-term effects of GB strategies on environmental performance. To summarize, this research provides the groundwork for further studies to better understand green finance mechanisms and their implications for environmental sustainability in the banking sector.

Table A1. Construct items

|

Variables |

Description |

Source |

|

Operations-related green banking strategies |

Reduction in the use of paper |

[42] |

|

Introduction of energy-efficient technology, like Internet banking and solar ATMs. |

||

|

Offering environmentally friendly banking services |

||

|

Bank's Green Financing |

Increasing the amount spent on environmentally beneficial projects |

[106, 111] |

|

Increasing the amount of money spent on recyclable and reusable products |

||

|

Increasing the amount spent on waste management and the production of green bricks |

||

|

Increasing the amount spent on energy-saving initiatives |

||

|

Increasing funding for the growth of the green industry development |

||

|

*Rise in funding for green advertising and other initiatives |

||

|

Banks’ Environmental Performance |

Energy consumption reductions from banking activities |

[43, 44] |

|

Reducing the level of carbon emissions produced by banking activities |

||

|

Increasing banks' adherence to environmental regulations |

||

|

Educating staff members in energy conservation and environmental protection |

*Deleted item from the final analysis

[1] Aubhi, R.U. (2016). The evaluation of green banking practices in Bangladesh. Research Journal of Finance and Accounting, 7(7): 93-125.

[2] Batten, S., Sowerbutts, R., Tanaka, M. (2016). Let’s talk about the weather: The impact of climate change on central banks. Bank of England Working Paper No. 6 (SSRN Electronic Journal). https://doi.org/10.2139/ssrn.2783753

[3] Nedopil, C. (2023). Integrating biodiversity into financial decision-making: Challenges and four principles. Business Strategy and the Environment, 32(4): 1619-1633. https://doi.org/10.1002/bse.3208

[4] Goglio, S., Catturani, I. (2019). Sustainable Finance: A Common Ground for the Future in Europe? In: Migliorelli, M., Dessertine, P. (eds) The Rise of Green Finance in Europe: Opportunities and Challenges for Issuers, Investors and Marketplaces, pp. 239-261. Springer International Publishing. https://doi.org/10.1007/978-3-030-22510-0_10

[5] Klaassen, G.A.J., Opschoor, J.B. (1991). Economics of sustainability or the sustainability of economics: Different paradigms. Ecological Economics, 4(2): 93-115. https://doi.org/10.1016/0921-8009(91)90024-9

[6] Hawkins, C.V., Kwon, S.W., Bae, J. (2016). Balance between local economic development and environmental sustainability: A multi-level governance perspective. International Journal of Public Administration, 39(11): 803-811. https://doi.org/10.1080/01900692.2015.1035787

[7] Fu, W., Irfan, M. (2022). Does green financing develop a cleaner environment for environmental sustainability: Empirical insights from association of Southeast Asian Nations Economies. Frontiers in Psychology, 13. https://doi.org/10.3389/fpsyg.2022.904768

[8] Hoshen, M., Hasan, M., Hossain, S., Abdullah, M., Mamun, A., Mannan, A. (2017). Green financing: An emerging form of sustainable development in Bangladesh. IOSR Journal of Business and Management (IOSR-JBM), 19(12): 24-30. https://doi.org/10.9790/487X-1912072430

[9] Mishra, K, Aithal, P.S. (2022). An imperative on green financing in the perspective of Nepal. International Journal of Applied Engineering and Management Letters (IJAEML), 6(2): 242-253. https://doi.org/10.2139/ssrn.4256184

[10] Kumar, S., Sharma, D., Rao, S., Lim, W.M., Mangla, S.K. (2022). Past, present, and future of sustainable finance: Insights from big data analytics through machine learning of scholarly research. Annals of Operations Research, 1-44. https://doi.org/10.1007/s10479-021-04410-8

[11] Ozili, P.K. (2022). Green finance research around the world: A review of literature. International Journal of Green Economics, 16(1): 56-75. https://doi.org/10.1504/IJGE.2022.125554

[12] Cen, T., He, R. (2018). Fintech, green finance and sustainable development. International Conference on Management, Economics, Education, Arts and Humanities (MEEAH 2018), pp. 222-225. https://doi.org/10.2991/meeah-18.2018.40

[13] Haigh, N., Hoffman, A. J. (2011). Hybrid organizations: The next chapter in sustainable business. Organizational Dynamics, 41(2): 126-134. https://doi.org/10.2139/ssrn.2933616

[14] Wang, Y., Zhi, Q. (2016). The role of green finance in environmental protection: Two aspects of market mechanism and policies. Energy Procedia, 104: 311-316. https://doi.org/10.1016/j.egypro.2016.12.053

[15] Zi, H. (2023). Role of green financing in developing sustainable business of e-commerce and green entrepreneurship: Implications for green recovery. Environmental Science and Pollution Research, 30: 95525-95536. https://doi.org/10.1007/s11356-023-28970-3

[16] Chang, L., Wang, J., Xiang, Z., Liu, H. (2021). Impact of green financing on carbon drifts to mitigate climate change: Mediating role of energy efficiency. Frontiers in Energy Research, 9: 785588. https://doi.org/10.3389/fenrg.2021.785588

[17] Chang, Y. (2019). Green finance in Singapore: Barriers and solutions. ADBI Working Paper 915. https://doi.org/10.2139/ssrn.3326

[18] Zhang, D., Awawdeh, A.E., Hussain, M.S., Ngo, Q.T., Hieu, V.M. (2021). Assessing the nexus mechanism between energy efficiency and green finance. Energy Efficiency, 14: 1-18. https://doi.org/10.1007/s12053-021-09987-4

[19] Kerr, T.M., Avendano, F. (2020). Green loans and multinational corporations. Natural Resources & Environment, 35(2): 46-49.

[20] Lee, H.Y., So, G., Tang, E., Lam, T., Cheng, V. (2020). Green finance performance and role of sustainability engineers in the Greater Bay Area. IOP Conference Series: Earth and Environmental Science, 588(2): 022063. https://doi.org/10.1088/1755-1315/588/2/022063

[21] Bose, S., Khan, H.Z., Rashid, A., Islam, S. (2018). What drives green banking disclosure? An institutional and corporate governance perspective. Asia Pacific Journal of Management, 35(2): 501-527. https://doi.org/10.1007/s10490-017-9528-x

[22] Mir, A.A., Bhat, A.A. (2022). Green banking and sustainability – A review. Arab Gulf Journal of Scientific Research, 40(3): 247-263. https://doi.org/10.1108/AGJSR-04-2022-0017

[23] Sahoo, P., Nayak, B.P. (2007). Green banking in India. The Indian Economic Journal, 55(3): 82-98. https://doi.org/10.1177/0019466220070306

[24] Fashli, A., Herdiansyah, H., Handayani, R.D. (2019). Application of green banking on financing infrastructure project industry: Environmental perspective. Journal of Physics: Conference Series, 1175(1): 012027. https://doi.org/10.1088/1742-6596/1175/1/012027

[25] Gunawan, J., Permatasari, P., Sharma, U. (2022). Exploring sustainability and green banking disclosures: A study of banking sector. Environment, Development and Sustainability, 24(9): 11153-11194. https://doi.org/10.1007/s10668-021-01901-3

[26] Park, H., Kim, J.D. (2020). Transition towards green banking: Role of financial regulators and financial institutions. Asian Journal of Sustainability and Social Responsibility, 5(1): 1-25. https://doi.org/10.1186/s41180-020-00034-3

[27] Nguyen, A. (2023). Theoretical framework for the influence of crucial factors on green banking strategy implementation. In International Conference on Emerging Challenges: Strategic Adaptation in the World of Uncertainties (ICECH 2022), pp. 253-269. https://doi.org/10.2991/978-94-6463-150-0_18

[28] Bukhari, S.A.A., Hashim, F., Amran, A. (2022). Green banking: A strategy for attainment of UN-Sustainable Development Goals 2030. International Journal of Environment and Sustainable Development, 22(1): 13-31. https://doi.org/10.1504/ijesd.2023.127419

[29] World Population Review. (2023). Carbon footprint by country 2023. https://worldpopulationreview.com/country-rankings/carbon-footprint-by-country.

[30] Patel, N., Mehta, D. (2023). The asymmetry effect of industrialization, financial development and globalization on CO2 emissions in India. International Journal of Thermofluids, 20: 100397. https://doi.org/10.1016/j.ijft.2023.100397

[31] NITI Aayog. (2022). Carbon capture, utilisation, and storage (CCUS) policy framework and its deployment mechanism in India. https://www.niti.gov.in/index.php/node/3486.

[32] The Economic Times. (2021). India needs $10.1 trillion investment to achieve net-zero emission by 2070. The Economic Times. https://economictimes.indiatimes.com/industry/renewables/india-needs-10-1-trillion-investment-to-achieve-net-zero-emission-by-2070-study/articleshow/87774598.cms.

[33] Government of Punjab. (2023). Punjab economic survey. Economic and Statistical Organisation, Department of Planning, Government of Punjab. https://esopb.gov.in/Static/PDF/EconomicSurvey2022-23.pdf.

[34] Chaurasia, A.K. (2014). Green banking practices in Indian banks. The Journal of Management and Social Science, 1(1): 41-54.

[35] Nath, V., Nayak, N., Goel, A. (2014). Green banking practices – A review. International Journal of Research in Business Management, 2(4).

[36] Bukhari, S.A.A., Hashim, F., Amran, A. (2020). Green Banking: A road map for adoption. International Journal of Ethics and Systems, 36(3). https://doi.org/10.1108/IJOES-11-2019-0177

[37] Yadav, R., Pathak, S. (2013). Environmental sustainability through green banking: A study of public and private sector banks in India. OIDA International Journal of Sustainable Development, 6: 37-48.

[38] RBI. (2023). Framework for acceptance of green deposits. https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=12487.

[39] Menon, D.G., Sreelakshmi, S.G., Shivdas, A. (2017). Green banking initiatives: A review of Indian banking sector. International Conference on Technological Advancements in Power and Energy (TAP Energy), pp. 1-7. https://doi.org/10.1109/TAPENERGY.2017.8397303

[40] Kala, K.N. (2020). A study on the impact of green banking practices on bank’s environmental performance with special reference to Coimbatore City. African Journal of Business and Economic Research, 15: 2020. https://doi.org/10.31920/1750

[41] Karyani, E., Obrien, V.V. (2020). Green banking and performance: The role of foreign and public ownership. Jurnal Dinamika Akuntansi Dan Bisnis, 7(2). https://doi.org/10.24815/jdab.v7i2.17150

[42] Rehman, A., Ullah, I., Afridi, FA., Ullah, Z., Zeeshan, M., Hussain, A., Rahman, H.U. (2021). Adoption of green banking practices and environmental performance in Pakistan: A demonstration of structural equation modelling. Environment, Development and Sustainability, 23(9): 13200-13220. https://doi.org/10.1007/s10668-020-01206-x

[43] Risal, N., Joshi, S.K. (2018). Measuring green banking practices on bank’s environmental performance: Empirical evidence from Kathmandu valley. Journal of Business and Social Sciences, 2(1): 44-56. https://doi.org/10.3126/jbss.v2i1.22827

[44] Shaumya, S., Arulrajah, A. (2017). The impact of green banking practices on banks environmental performance: Evidence from Sri Lanka. Journal of Finance and Bank Management, 5(1): 77-90. https://doi.org/10.15640/jfbm.v5n1a7

[45] Sharma, M., Choubey, A. (2022). Green banking initiatives: A qualitative study on Indian banking sector. Environment, Development and Sustainability, 24(1): 293-319. https://doi.org/10.1007/s10668-021-01426-9

[46] Taneja, S., Özen, E. (2023). To analyze the relationship between banks green financing and environmental performance. International Journal of Electronic Finance, 1(1): 163-175. https://doi.org/10.1504/ijef.2023.10050554

[47] Özen, E., Yıldırım, A.E. (2023). How digital banking affects greenhouse gas emissions in Turkey? An Empirical Investigation. Statistika: Statistics & Economy Journal, 103(1): 101-112. https://doi.org/10.54694/stat.2022.37

[48] Alshebami, A.S. (2021). Evaluating the relevance of green banking practices on Saudi Banks’ green image: The mediating effect of employees’ green behaviour. Journal of Banking Regulation, 22(4): 275-286. https://doi.org/10.1057/s41261-021-00150-8

[49] Bhardwaj, B.R., Malhotra, A. (2013). Green banking strategies: Sustainability through corporate entrepreneurship. Greener Journal of Business and Management Studies, 3(4): 180-193. https://doi.org/10.15580/GJBMS.2013.4.122412343

[50] Ibe-enwo, G., Igbudu, N., Garanti, Z., Popoola, T. (2019). Assessing the relevance of green banking practice on bank loyalty: The mediating effect of green image and bank trust. Sustainability, 11(17): 17. https://doi.org/10.3390/su11174651

[51] Richardson, B.J. (2009). Climate finance and its governance: Moving to a low carbon economy through socially responsible financing? International and Comparative Law Quarterly, 58(3): 597-626. https://doi.org/10.1017/S0020589309001213

[52] Wagemans, F.A.J., van Koppen, C.S.A., Mol, A.P.J. (2013). The effectiveness of socially responsible investment: A review. Journal of Integrative Environmental Sciences, 10(3-4): 235-252. https://doi.org/10.1080/1943815X.2013.844169

[53] Ziolo, M. (2021). Business models of banks toward sustainability and ESG risk. In Sustainability in Bank and Corporate Business Models: The Link between ESG Risk Assessment and Corporate Sustainability, pp. 185-209. Springer International Publishing. https://doi.org/10.1007/978-3-030-72098-8_7

[54] Tripathi, V., Kaur, A. (2022). Does socially responsible investing pay in developing countries? A comparative study across select developed and developing markets. FIIB Business Review, 11(2): 189-205. https://doi.org/10.1177/2319714520980288

[55] Tripathi, V., Kaur, A. (2020). Socially responsible investing: Performance evaluation of BRICS nations. Journal of Advances in Management Research, 17(4): 525-547. https://doi.org/10.1108/JAMR-02-2020-0020

[56] Risi, D. (2020). Time and business sustainability: Socially responsible investing in Swiss banks and insurance companies. Business and Society, 59(7). https://doi.org/10.1177/0007650318777721

[57] Zhang, W., Liu, X., Liu, J., Zhou, Y. (2022). Endogenous development of green finance and cultivation mechanism of green bankers. Environmental Science and Pollution Research, 29(11): 15816-15826. https://doi.org/10.1007/s11356-021-16933-5

[58] Zhang, X., Wang, Z., Zhong, X., Yang, S., Siddik, A.B. (2022). Do green banking activities improve the banks’ environmental performance? The Mediating Effect of Green Financing. Sustainability (Switzerland), 14(2): 989. https://doi.org/10.3390/su14020989

[59] Shakil, M.H., Azam, Md. K.G., Tasnia, M., Munim, Z.H. (2014). An evaluation of green banking practices in Bangladesh. IOSR Journal of Business and Management, 16(11): 67-73. https://doi.org/10.9790/487X-161146773

[60] Tara, K., Singh, S., Kumar, R. (2015). Green banking for environmental management: A paradigm shift. Current World Environment, 10(3): 1029-1038. https://doi.org/10.12944/cwe.10.3.36

[61] Bihari, S.C. (2010). Green banking-towards socially responsible banking in India. International Journal of Business Insights & Transformation, 4(1).

[62] Hoque, N., Mowla, Md. M., Uddin, M.S., Mamun, A., Uddin, M.R. (2019). Green banking practices in Bangladesh: A critical investigation. International Journal of Economics and Finance, 11(3): 58. https://doi.org/10.5539/ijef.v11n3p58

[63] Shayana, A., Raj, A.N., Rai, S. (2017). A study on problems and prospects of green banking with reference to coastal regions, Karnataka, India. International Journal of Research in Finance and Marketing (IJRFM), 7(1): 141-151.

[64] Selvaraj, S. (2022). A conceptual study on factors influencing green banking facilities in India. Journal of Corporate Finance Management and Banking System, 31: 17-22. https://doi.org/10.55529/jcfmbs.31.17.22

[65] Siddique, M.N.E.A., Nor, S.M., Senik, Z.C., Omar, N.A. (2023). Corporate social responsibility as the pathway to sustainable banking: A systematic literature review. Sustainability (Switzerland), 15(3): 1807. https://doi.org/10.3390/su15031807

[66] Sangisetti, M., Kumari, P.V.P. (2023). Green banking practices and strategies for sustainable. Res Militaris, 13(1): 380-392.

[67] Rai, R., Kharel, S., Devkota, N., Paudel, U.R. (2019). Customers perception on green banking practices: A desk review. The Journal of Economic Concerns, 10(1): 82-95.

[68] Sun, H., Rabbani, M.R., Ahmad, N., Sial, M.S., Guping, C., Zia-Ud-din, M., Fu, Q. (2020). CSR, co-creation and green consumer loyalty: Are green banking initiatives important? A moderated mediation approach from an emerging economy. Sustainability (Switzerland), 12(24): 10688. https://doi.org/10.3390/su122410688

[69] Khairunnessa, F., Vazquez-Brust, D.A., Yakovleva, N. (2021). A review of the recent developments of green banking in Bangladesh. Sustainability (Switzerland), 13(4): 1904. https://doi.org/10.3390/su13041904

[70] Mozib Lalon, R. (2015). Green banking: Going green. International Journal of Economics, Finance and Management Sciences, 3(1): 34-42. https://doi.org/10.11648/j.ijefm.20150301.15

[71] Chitra, V., Gokilavani, R. (2020). Green banking trends: Customer knowledge and awareness in India. Shanlax International Journal of Management, 8(1): 54-60. https://doi.org/10.34293/management.v8i1.2486

[72] Fernando, P.M.P., Fernando, K.S.D. (2017). Study of green banking practices in the Sri Lankan context: A critical review. In Selected Papers from the Asia-Pacific Conference on Economics & Finance (APEF 2016), pp. 125-143. https://doi.org/10.1007/978-981-10-3566-1_10

[73] Manolas, E., Tsantopoulos, G., Dimoudi, K. (2017). Energy saving and the use of “green” bank products: The views of the citizens. Management of Environmental Quality: An International Journal, 28(5): 745-768. https://doi.org/10.1108/MEQ-05-2016-0042

[74] Biswas, N. (2011). Sustainable green banking approach: The need of the hour. Business Spectrum, 1(1): 32-38.

[75] Ellahi, A., Jillani, H., Zahid, H. (2021). Customer awareness on green banking practices. Journal of Sustainable Finance and Investment, 13(3): 1377-1393. https://doi.org/10.1080/20430795.2021.1977576

[76] Akomea-Frimpong, I., Adeabah, D., Ofosu, D., Tenakwah, E.J. (2022). A review of studies on green finance of banks, research gaps and future directions. Journal of Sustainable Finance and Investment, 12(4): 1241-1264. https://doi.org/10.1080/20430795.2020.1870202

[77] Ali, E.B., Anufriev, V.P., Amfo, B. (2021). Green economy implementation in Ghana as a road map for a sustainable development drive: A review. Scientific African, 12: e00756. https://doi.org/10.1016/j.sciaf.2021.e00756

[78] Yu, X., Mao, Y., Huang, D., Sun, Z., Li, T. (2021). Mapping global research on green finance from 1989 to 2020: A bibliometric study. Advances in Civil Engineering, 2021: 9934004. https://doi.org/10.1155/2021/9934004

[79] Rahman, S.M.M., Barua, S. (2016). The design and adoption of green banking framework for environment protection: Lessons from Bangladesh. Australian Journal of Sustainable Business and Society, 2(1): 1-19.

[80] Dikau, S., Volz, U. (2021). Central bank mandates, sustainability objectives and the promotion of green finance. Ecological Economics, 184: 107022. https://doi.org/10.1016/j.ecolecon.2021.107022

[81] Tu, T., Dung, N.T.P. (2017). Factors affecting green banking practices: Exploratory factor analysis on Vietnamese banks. Journal of Economics Development, 24(2): 4-30. https://doi.org/10.24311/jed/2017.24.2.05

[82] Rahman, S., Moral, I.H., Hassan, M., Hossain, G.S., Perveen, R. (2022). A systematic review of green finance in the banking industry: Perspectives from a developing country. Green Finance, 4(3): 347-363. https://doi.org/10.3934/GF.2022017

[83] Sarkar, D., Latta, A. (2022). Role of banking system in green finance in the context of India: An analysis. Asian Journal of Management, 13: 227-234. https://doi.org/10.52711/2321-5763.2022.00040

[84] Zhang, S., Wu, Z., Wang, Y., Hao, Y. (2021). Fostering green development with green finance: An empirical study on the environmental effect of green credit policy in China. Journal of Environmental Management, 296: 113159. https://doi.org/10.1016/j.jenvman.2021.113159

[85] Dimmelmeier, A. (2021). Sustainable finance as a contested concept: Tracing the evolution of five frames between 1998 and 2018. Journal of Sustainable Finance & Investment, 13(4): 1600-1623. https://doi.org/10.1080/20430795.2021.1937916

[86] Raper, R., Boeddinghaus, J., Coeckelbergh, M., Gross, W., Campigotto, P., Lincoln, C.N. (2022). Sustainability budgets: A practical management and governance method for achieving goal 13 of the sustainable development goals for AI development. Sustainability (Switzerland), 14(7): 4019. https://doi.org/10.3390/su14074019

[87] Feng, H., Liu, Z., Wu, J., Iqbal, W., Ahmad, W., Marie, M. (2022). Nexus between government spending’s and Green Economic performance: Role of green finance and structure effect. Environmental Technology and Innovation, 27: 102461. https://doi.org/10.1016/j.eti.2022.102461

[88] Rahman, S.M., Haque, M., Miah, M.D. (2018). Factors affecting environmental performance: Evidence from banking sector in Bangladesh. International Journal of Financial Services Management, 9(1). http://doi.org/10.1504/IJFSM.2018.089917

[89] Pandey, D., Agrawal, M., Pandey, J.S. (2011). Carbon footprint: Current methods of estimation. Environmental Monitoring and Assessment, 178(1): 135-160. https://doi.org/10.1007/s10661-010-1678-y

[90] Zorpas, A.A., Lasaridi, K. (2013). Measuring waste prevention. Waste Management, 33(5): 1047-1056. https://doi.org/10.1016/j.wasman.2012.12.017

[91] Soundarrajan, P., Vivek, N. (2016). Green finance for sustainable green economic growth in India. Agricultural Economics, 62(1): 35-44. https://doi.org/10.17221/174/2014-AGRICECON

[92] SBI. (2022). Setting new standards in banking excellence- SBI annual report. https://bank.sbi/documents/17836/29141285/SBI_Annual_Report_2022.pdf.

[93] Gulati, A., Roy, R., Hussain, S. (2021). Performance of agriculture in Punjab. In: Gulati, A., Roy, R., Saini, S. (eds) Revitalizing Indian Agriculture and Boosting Farmer Incomes, pp. 77-112. Springer Nature. https://doi.org/10.1007/978-981-15-9335-2_4

[94] IBEF. (2022). Punjab state presentation report. India Brand Equity Foundation (IBEF). https://www.ibef.org/states/punjab-presentation.

[95] RBI. (2022). DBIE-RBI: Database on Indian economy. https://dbie.rbi.org.in/DBIE/dbie.rbi?site=publications#!4.

[96] Lee, H.W. (2011). An application of latent variable structural equation modeling for experimental research in educational technology. Turkish Online Journal of Educational Technology - TOJET, 10(1): 15-23.

[97] Faul, F., Erdfelder, E., Lang, A.G., Buchner, A. (2007). G*Power 3: A flexible statistical power analysis program for the social, behavioral, and biomedical sciences. Behavior Research Methods, 39(2): 175-191. https://doi.org/10.3758/BF03193146

[98] Cohen, J. (1988). Statistical power analysis for the behavioural sciences. Lawrence Erlbaum Associates, 56: 102.

[99] Kang, H. (2021). Sample size determination and power analysis using the G*Power software. Journal of Educational Evaluation for Health Professions, 18: 17. https://doi.org/10.3352/jeehp.2021.18.17

[100] Lowry, P.B., Gaskin, J. (2014). Partial least squares (PLS) structural equation modeling (SEM) for building and testing behavioral causal theory: When to choose it and how to use it. IEEE Transactions on Professional Communication, 57(2): 123-146. https://doi.org/10.1109/TPC.2014.2312452

[101] Hair, J.F., Ringle, C.M., Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2): 139-152. https://doi.org/10.2753/MTP1069-6679190202

[102] Hair, J.F., Risher, J.J., Sarstedt, M., Ringle, C.M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1): 2-24. https://doi.org/10.1108/EBR-11-2018-0203

[103] Nitzl, C., Roldan, J.L., Cepeda, G. (2016). Mediation analysis in partial least squares path modeling: Helping researchers discuss more sophisticated models. Industrial Management & Data Systems, 116(9): 1849-1864. https://doi.org/10.1108/IMDS-07-2015-0302

[104] Hair Jr, J.F., Howard, M.C., Nitzl, C. (2020). Assessing measurement model quality in PLS-SEM using confirmatory composite analysis. Journal of Business Research, 109: 101-110.

[105] Hair Jr, J.F., Hult, G.T.M., Ringle, C.M., Sarstedt, M., Danks, N.P., Ray, S., Hair, J.F., Hult, G.T.M., Ringle, C.M., Sarstedt, M. (2021). Mediation analysis. Partial Least Squares Structural Equation Modeling (PLS-SEM) Using R: A Workbook, 139-153.

[106] Akter, N., Siddik, A., Mondal, M. (2018). Sustainability reporting on green financing: A study of listed private commercial banks in Bangladesh. Journal of Business and Technology (Dhaka), XII: 14-28.

[107] Sarstedt, M., Ringle, C.M., Smith, D., Reams, R., Hair, J.F. (2014). Partial least squares structural equation modeling (PLS-SEM): A useful tool for family business researchers. Journal of Family Business Strategy, 5(1): 105-115. https://doi.org/10.1016/j.jfbs.2014.01.002

[108] Hair Jr, J., Hair Jr, J.F., Hult, G.T.M., Ringle, C.M., Sarstedt, M. (2021). A primer on partial least squares structural equation modeling (PLS-SEM). Sage Publications.

[109] Fornell, C., Larcker, D.F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Journal of Marketing Research, 18(3): 382–388. https://doi.org/10.1177/002224378101800313

[110] Henseler, J., Ringle, C.M., Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1): 115-135. https://doi.org/10.1007/s11747-014-0403-8

[111] Henseler, J., Fassott, G. (2010). Testing moderating effects in PLS path models: An illustration of available procedures. In: Esposito Vinzi, V., Chin, W.W., Henseler, J., Wang, H. (eds) Handbook of Partial Least Squares: Concepts, Methods and Applications, pp. 713-735. Springer. https://doi.org/10.1007/978-3-540-32827-8_31

[112] Zheng, G.W., Siddik, A.B., Masukujjaman, M., Fatema, N., Alam, S.S. (2021). Green finance development in Bangladesh: The role of private commercial banks (PCBs). Sustainability (Switzerland), 13(2): 1-17. https://doi.org/10.3390/su13020795