Yozi Aulia Rahman*![]() | Dwi Rahmayani

| Dwi Rahmayani![]() | Bayu Bagas Hapsoro

| Bayu Bagas Hapsoro![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The Developing countries are particularly vulnerable to shocks, such as the global financial crisis and the COVID-19 pandemic. The economic crisis increased external public debt to stabilize the economy and improve people's welfare. High external debt puts the debt in an unsustainable condition. This study aims to measure the debt sustainability of external public debt in Indonesia from 2008-2020. We used the Threshold Value of The Debt Sustainability Framework for Low-Income Countries (LIC-DSF) and the Solvency Rate of External Debt (SRED) as a better combination for measuring debt sustainability in Indonesia. The results showed external public debt was at a low-risk threshold after the global financial crisis. However, the impact of COVID-19 has caused the ratio of external public debt interest payment to tax revenue to be within a high-risk threshold value. The SRED value shows a minus number from 2012-2020 caused by the worsening current account balance and net capital account values. The analysis of debt sustainability may be able to encourage a prudent and sustainable the Indonesian budget management policy.

debt sustainability, threshold value, solvency rate, external public debt

The global financial crisis in 2008-2009 harmed the economies of developing countries in Asia. An important question from the 2008 global economic and financial crisis was how to restore economic growth while stabilizing a country's fiscal health [1]. When turmoil in the economy occurred, the Government made many adjustments to its fiscal policy, such as increasing spending to boost the economy. On the other hand, tax revenues failed to reach the target due to weak economic activity. The global recession led to an increase in fiscal deficits because both developed and developing countries owed large amounts of debt and raised concerns about the importance of fiscal sustainability [2]. The crisis increased government debt and raised concerns about the impact of high debt on economic growth [3]. The government must make some adjustments in fiscal policy for macroeconomic stability. Post-crisis, countercyclical policies to increase government spending significantly increased the budget deficit and central government debt levels [4].

Government debt is a serious problem for many countries and can potentially negatively impact the government if it is not managed properly and transparently. Various efforts must be made to improve the ability to repay debt. Therefore, debt sustainability should concern governments, especially in developing countries. Debt will be sustainable if a country does not restructure and renegotiate its debt [5]. Many developed and developing countries have failed to manage their debts, especially external debts obtained from countries and donor agencies. Consequently, they are unable to pay their obligations and potentially fall into a debt trap.

Debt sustainability is an important condition for macroeconomic stability and sustainable economic growth. High levels of public debt create a flow of payments that can stifle much-needed public spending and can generate adverse incentives for private investors [6]. High debt occurs in many developing countries, one of which is Indonesia. One way to see a country can pay debts is the ratio of external debt to Gross Domestic Bruto (GDP). Table 1 shows the development of Indonesia's external debt ratio during 2008-2020. After the 2008-2009 global crisis, the Indonesian government's external debt has been steadily increasing for a decade.

In 2010, the external debt to GDP ratio increased to 15.05% due to an external debt growth of 17.6%. From 2012-2013, the growth of EXTDEBT showed improvement with minus -0.19 and -1.09%, respectively. The debt-to-GDP ratio decreased to 11.75%, which was the best condition after the 2008 global crisis. However, from 2014-2017, the government's plan to develop the country, especially its physical infrastructure, increased the debt-to-GDP ratio to 19.17%. In 2018, better debt management resulted in the growth of EXTDEBT being only 3.32%. After the global financial crisis of 2008-2009, the economic recovery was successful, and Indonesia's macroeconomic conditions were in good condition.

However, in March 2020, the COVID-19 pandemic hit all countries and had a negative impact on public health and safety, as well as the collapse of the country's economy. Social restrictions lead to reduced business and economic transaction activities, increasing poverty and unemployment rates. The COVID-19 pandemic caused the need for government spending to increase to handle the impact of the pandemic on the community and pushed the debt-to-GDP ratio to increase to 21.46%. The increase in external government debt was exacerbated by the decline in GDP due to the economic recession.

Table 1. The development of Indonesia external public debt, 2008-2020

|

Period |

External Public Debt (Million USD) |

Product Domestic Bruto (Million USD) |

Ratio EXTDEBT/GDP (%) |

Growth of EXTDEBT (%) |

|

2008 |

85.136 |

639.782 |

13,30 |

- |

|

2009 |

90.853 |

606.747 |

14,97 |

6,72 |

|

2010 |

106.860 |

709.848 |

15,05 |

17,6 |

|

2011 |

116.410 |

814.197 |

14,30 |

8,94 |

|

2012 |

116.187 |

900.517 |

12,90 |

-0,19 |

|

2013 |

114.924 |

977.961 |

11,75 |

-1,09 |

|

2014 |

123.806 |

1.049.229 |

11,80 |

7,73 |

|

2015 |

137.396 |

1.011.433 |

13,58 |

11 |

|

2016 |

154.875 |

942.117 |

16,44 |

12,7 |

|

2017 |

177.318 |

925.119 |

19,17 |

14,5 |

|

2018 |

183.197 |

966.188 |

18,96 |

3,32 |

|

2019 |

199.876 |

998.391 |

20,01 |

9,1 |

|

2020 |

206.375 |

961.669 |

21,46 |

3,25 |

Source: Author's calculations based on data from; Central Bank of Indonesia, Ministry of Finance, Statistics of Indonesia and World Development Indicators

This condition raises concerns about the sustainability of the Indonesian government's debt and the ability to repay the debt when it is due. Several previous studies have discussed debt sustainability in developing countries. However, there is little literature that combines two measures of debt sustainability, namely threshold value based on the IMF's Debt Sustainability Framework and debt solvency measurement using SRED (Solvency Rate of External Debt). Therefore, the purpose of this paper is to analyze the sustainability of Indonesia's public debt after the 2008-2020 financial crisis period and during the COVID-19 pandemic with these two measurements. The structure of this paper consists of; section 2 explains the literature review on debt sustainability, section 3 presents the methodology, section 4 shows the results and discussion, and section 5 presents the conclusions.

In 1996, the IMF and the World Bank initiated The Heavily Indebted Poor Countries (HIPC) to ensure that no developing countries owed more than their ability to repay debt. The IMF and the World Bank define the concept of debt sustainability, namely the ability of a country to meet its current and future debt repayment obligations without resorting to debt rescheduling programs and compromising economic growth [7]. The sustainability of public debt means that the accumulated public debt must be repaid at any time by the government [8].

The Payment of these debts can be made by maximizing their income from taxes. However, the crisis period has an impact on the decline in individual and company income. A country's public debt condition becomes chronic and unsustainable when the ratio of public debt rises above the Gross Domestic Product [9]. Debt sustainability can be achieved when there are no major changes in fiscal policy that have a negative impact on society and economic conditions [2]. An increase in the debt burden can have medium to long-term negative impacts on the balance of the government budget. The government should design a strategy after injecting liquidity to encourage expansionary policies [10].

Several previous studies related to the analysis of debt sustainability in developing countries [11-23]. In analyzing debt sustainability in Kazakhstan and the Russian Federation, Mukhtarkhan [11] applies the threshold value of public debt in both countries. The results show that from 2007 to 2019, the ratio of public debt to GDP in the Republic of Kazakhstan tripled from 6% to 18%. The ratio of the public external debt of the Russian Federation to GDP does not exceed 4%. In 2019 it was 3%, while the minimum threshold for reduced risk zones was 30%. Both countries are in debt stability, and public debt is shifting towards domestic debt.

Previous research examined debt sustainability in West African countries for the period 2010-2017 [12]. The measurement of debt sustainability uses various ratios; present value approach, debt policy rating ratings of State and Institutional Policy Assessments, and external debt solvency ratios- SRED. The results show that the debt burden threshold measured by the ratio of external debt to exports implies that the accumulation of external debt in the Ivory Coast and Niger is moderate. Ghana is in a weak position and has the potential to fall into a debt trap. The increase in the present value of the debt-to-exports ratio in these countries indicates a tendency for unsustainable debt. Based on the results of SRED, Most West African countries are in a negative position and are at risk of defaulting on debt in the future.

Used SRED as an indicator to analyze the debt crisis in Turkey in the 1980-2009 period [13]. The results show that SRED is positive between 1980-84, 1991, 1994, and 2000-2001. However, SRED is negative in the period 1985-1990, 1992-1993, 1995-1999, 2002, and 2004-2007 indicating that Turkey is experiencing difficulties in repaying debt. abroad. Previous research examined debt sustainability in SAARC countries; Pakistan, India, Sri Lanka, and Bangladesh for the period 1995-2012 [14]. The researcher concludes that the four countries have experienced unsustainable debt burdens due to large fiscal and current account imbalances. If there is no corrective policy to address this imbalance, then government debt will become a serious problem in the future.

Previous research examined the sustainability of Jamaican government debt over the period 1996 to 2018 with quarterly data [15]. The analytical method used is unit root testing, cointegration testing, and fiscal reaction function. The results show that cash flow problems in state finances and debt restructuring has been carried out. However, the fiscal policy response has succeeded in making public debt in Jamaica on sustainable condition. However, the state's financial condition is still vulnerable to shocks, including the COVID-19 pandemic.

Previous research investigated debt sustainability in Brazil in the period December 1997 to June 2018 [16]. This study applies the econometric multicointegration method to analyze the long-term correlation between government spending, tax revenue, and government debt. The results show that the deteriorating fiscal conditions since 2014 have made government debt unsustainable. The increase in government spending is not matched by tax revenues, causing the primary deficit to increase.

Previous research examined the solvency analysis of Indonesia's foreign debt from 2009 to 2012 [17]. The results show that Indonesia's foreign debt is in a solvency condition in the external debt to GDP ratio, and external debt to export ratio. However, Indonesia's foreign debt is not in a solvency condition in the external debt service to export ratio. Previous research estimated domestic debt and foreign debt to measure fiscal solvency in Indonesia from the period 1999-2009 [18]. The result shows that the central government budget on unsustainable conditions. Previous research investigated debt sustainability in Turkey related to solvency analysis in 2000-2020 [19]. The results argue that it is complex and difficult to achieve public debt sustainability, which entails meeting solvency and liquidity constraints in nations where real interest rates are higher than the real growth rate.

Previous research examined public debt sustainability under COVID-19 uncertainty in Côte d'Ivoire [20]. The results showed that there was a controlled risk between 16% - 27% in the debt forecasting period 2021-2024. However, Côte d'Ivoire remains vulnerable to the risk of debt difficulties due to COVID-19 uncertainty. The government must encourage a sound and reliable debt management system to mitigate these risks.

Previous research investigated public debt sustainability during the pandemic COVID-19 in South Africa [21]. The result shows that the debt/GDP ratio is budgeted at 81.8% in 2020/21, which due to the Covid-19 crisis, is almost 15% higher than the public budget in the February 2020 budget. The projected public debt/GDP ratio will increase to 140.7% in 2028/29. In contrast, the active scenario projects the debt burden to peak at 87.4% in 2023/24, and then decline to 73.5% in 2028/29.

Previous research estimated fiscal sustainability post-Covid 19 recoveries in Afrika. The result shows the COVID-19 contraction caused an economic recession in Africa and pushed up fiscal and current account deficits [22]. The government has issued a fiscal stimulus package in response to the impact of the COVID-19 pandemic. Paczos and Shakhnov [23] analyzed a framework to study debt sustainability in 24 emerging economies under the COVID-19 crisis. The results concluded that The Covid shock, which reduced output and increased government spending, brought the economy closer to total default.

This study uses secondary data from various institutions: Bank of Indonesia, Ministry of Finance, Statistics Indonesia, and World Bank. The data required starts from the period 2008-2020. There are two methods of analysis: The Threshold Value of The Debt Sustainability Framework for Low-Income Countries (LIC-DSF) and the Solvency Rate of External Debt (SRED). The first objective of this paper is to measure the sustainability of government debt using the Threshold Value from The Debt Sustainability Framework for Low-Income Countries (LIC-DSF) from the International Monetary Fund (IMF) and the World Bank [24] and to develop from Mukhtarkan's research [11]. The data needed for The Threshold Value of The Debt Sustainability Framework (LIC-DSF) are external public debt, GDP, external public debt interest payment, total of export, and tax revenue in Indonesia from 2008-2020.

Table 2 presents 4 (four) indicators that are used as measurements; (a) The ratio of external public debt to GDP (%), (b) The ratio of external public debt to export (%), (c) The ratio of external public debt interest payment to export (%), (d) The ratio of external public debt interest payment to tax revenue (%).

The second objective of this paper is to measure the sustainability of the government's external debt using the SRED adopted from Omotor [12] and Ulca and Oksay [13]. The data needed for SRED analysis are Current Account Balanced, Net Capital Account, External Debt Interest Payments, and External Debt Principal Payment in Indonesia from 2008-2020.

SRED$=\frac{\text { Current } \text { Account } \text { Balance }+\text { Net } \text { Capital } \text { Account }}{\text { External Debt } \text { Interest } \text { Payments }+\text { External Debt} \text { Principal } \text { Payments }}$ (1)

The ability to pay external debt increases if the SRED value is close to 1 or more than 1. The minus SRED value indicates a potential decline in the ability to repay external debt in the next few years.

Table 2. Threshold value of the debt sustainability

|

The Indicators of debt sustainability |

Debt Sustainability Treshold |

||

|

Small (%) |

Medium (%) |

High (%) |

|

|

The ratio of external public debt to GDP (%) |

30 |

40 |

50 |

|

The ratio of external public debt to export (%) |

140 |

180 |

240 |

|

The ratio of external public debt interest payment to export (%) |

10 |

15 |

21 |

|

The ratio of external public debt interest payment to tax revenue (%) |

14 |

18 |

23 |

Source: International Monetary Fund (IMF) dan World Bank [17] and Mukhtarkan [11]

4.1 Fiscal and economic indicators

Before measuring debt sustainability, it is necessary to analyze Indonesia's fiscal and economic indicators. Fiscal indicators include Government Debt, Primary Balance to GDP, Fiscal Balance to GDP, and Tax Revenue. The economic indicator is the value of exports. Table 3 shows the development of economic and fiscal indicators during 2008-2022. The global financial crisis caused an increase in debt and a decrease in the value of exports and tax revenues since 2009. Government debt has increase doubled from 2008-2020, from 85.14 billion USD to 206.38 billion USD. The government increases debt due to a budget deficit for expanding physical infrastructure development, human development, and energy & non-energy subsidies to the poor. The Indonesian government's external debt is in the form of bonds purchased by external communities and loans from international institutions (IMF & World Bank) and other countries.

The fiscal capacity of the Indonesian government tends to weaken, which can be seen in the primary balance to GDP and fiscal balance to GDP. The primary balance is the difference in state income minus state spending, excluding debt payments. During 2008-2020, most of the primary and fiscal balance to GDP was minus. The low fiscal capacity is caused by the increasing need for development funding but is not matched by satisfactory tax revenues. Tax revenues declined in 2009 and increased after the global financial crisis. The crisis affected the ability of many domestic and multinational to pay their tax obligations.

From 2010-2015, tax revenues increased from 72.33 billion USD to 118.95 billion USD. Economic recovery makes economic activities and companies return to normal and can carry out their tax obligations to the Government. In encouraging tax compliance, the Government issued policies to improve tax services, supervision, and law enforcement. Indonesia's exports tend to fluctuate from 2008-2020, from 249.54 billion USD to 257.47 billion USD.

Most export products are natural resource commodities whose market prices fluctuate greatly, such as coal, palm oil, rubber, iron, and steel. The latest global crisis, namely COVID-19, also worsened things and caused all economic and fiscal indicators to deteriorate in 2020. Government debt grew 3.14%, tax revenues grew -17.34%, and exports grew -7.28%. The primary balance is -3.8%, and the fiscal balance is -5.867 due to the weakening economy, and the Government must increase government spending. Tax revenues also weakened, and exports' value deteriorated and threatened the balance of payments.

4.2 Measurement of the debt sustainability of external public debt using threshold value LIC-DSF

The measurement of debt sustainability with the threshold value for LIC-DSF uses four indicators. Table 4 shows that the results of all indicator calculations for LIC-DSF in Indonesia during the period 2008-2020 are at low risk. The first indicator is the ratio of external public debt to GDP (%) in 2008 (13.31%) and increased by 2020 (21.46%). The ratio does not exceed 25%, for the low-risk threshold is 30%. However, there is an upward trend after the global financial crisis and the impact of the COVID-19 pandemic. The second indicator, the ratio of external public debt to export (%), is also at low risk, although there is an upward trend, such as in 2008 (34.12%) and 2020 (80.15%). This ratio is still at the low-risk threshold of 140%. The third indicator, The ratio of external public debt interest payments to export (%) in 2008 (3.89%) and 2020 (9.14%) 2020. This ratio is still below the low-risk threshold of 10%.

Table 3. Fiscal and economic indicators in Indonesia, 2008-2020

|

Period |

Government Debt (billion USD) |

Primary Balance to GDP (%) |

Fiscal Balance to GDP (%) |

Tax Revenue (billion USD) |

Export (billion USD) |

|

2008 |

85,14 |

1,687 |

0,054 |

72,38 |

249,54 |

|

2009 |

90,85 |

-0,084 |

-1,644 |

59,04 |

218,12 |

|

2010 |

106,86 |

0,045 |

-1,242 |

72,33 |

259,45 |

|

2011 |

112,43 |

0,488 |

-0,703 |

87,39 |

218,53 |

|

2012 |

116,19 |

-0,42 |

-1,586 |

108,95 |

207,86 |

|

2013 |

114,92 |

-1,033 |

-2,217 |

115,84 |

219,07 |

|

2014 |

123,81 |

-0,883 |

-2,146 |

109,07 |

232,87 |

|

2015 |

137,40 |

-1,25 |

-2,604 |

118,05 |

211,99 |

|

2016 |

154,88 |

-1,013 |

-2,486 |

92,22 |

212,9 |

|

2017 |

177,32 |

-0,915 |

-2,509 |

100,93 |

236,36 |

|

2018 |

183,2 |

-0,011 |

-1,75 |

113,29 |

263,81 |

|

2019 |

199,88 |

-0,489 |

-2,229 |

107,97 |

277,7 |

|

2020 |

206,38 |

-3,832 |

-5,867 |

89,25 |

257,47 |

Sources: Bank of Indonesia, Ministry of Finance, Statistics Indonesia, and World Bank

Table 4. Indicators of debt sustainability in Indonesia with threshold value LIC-DSF, 2008-2020

|

Period |

Ratio of external public debt to GDP (%) |

Ratio of external public debt to export (%) |

The ratio of external public debt interest payment to export (%) |

The ratio of external public debt interest payment to tax revenue (%) |

|

2008 |

13,31 |

34,12 |

3,89 |

13,41 |

|

2009 |

14,97 |

41,65 |

4,09 |

15,13 |

|

2010 |

15,05 |

41,19 |

3,41 |

12,22 |

|

2011 |

14,3 |

53,27 |

4,27 |

10,67 |

|

2012 |

12,9 |

55,9 |

5,37 |

10,25 |

|

2013 |

11,75 |

52,46 |

5,55 |

10,49 |

|

2014 |

11,8 |

53,17 |

5,44 |

11,62 |

|

2015 |

13,58 |

64,81 |

7 |

12,58 |

|

2016 |

16,44 |

72,74 |

6,17 |

14,25 |

|

2017 |

19,17 |

75,02 |

6,89 |

16,13 |

|

2018 |

18,96 |

69,44 |

7,3 |

16,99 |

|

2019 |

20,02 |

71,98 |

6,93 |

17,82 |

|

2020 |

21,46 |

80,15 |

9,14 |

26,36 |

Source: author’s calculations based on data from; Bank of Indonesia, Ministry of Finance, Statistics Indonesia, and World Bank

Based on the three indicators of threshold value LIC-DSF, The external public debt on sustainable condition. But, the fourth debt sustainability indicators are at low risk despite the impact of the global financial crisis and the COVID-19 pandemic. However, the ratio of external public debt interest payments to tax revenue (%) worsened due to the impact of the COVID-19 pandemic, which was 26.36%. This ratio exceeds the high-risk threshold (over 23%). Indonesia is very dependent on tax revenue, but tax revenue has failed to reach its target in recent years. Various tax policies are encouraged, such as tax amnesty, and have not been effective in overcoming the problem of tax evasion and tax avoidance.

The non-optimal tax revenue impacts the budget deficit, increasing government debt. The COVID-19 shock to debt will put emerging market and development economies at higher risk of serious debt difficulties and a possible wave of recession in the longer term [25]. The estimated results of the study [26] show that the government's external debt will continue to grow to meet the growing need for health spending due to the COVID-19 pandemic. Total debt and the debt-to-GDP ratio will continue to increase during and after the COVID-19 pandemic and its impact on a heavy fiscal burden for the government and threatens fiscal sustainability in the long term [27].

The results of these calculations require massive efforts from the government to stabilize debt in the short and long term. Efforts to stabilize the public debt at a sustainable level depend on three conditions: (a) the capacity of the economy to generate a primary surplus, (b) the interest rate on state loans in financial markets, (c) the rate of economic growth in the country [28].

4.3 Measurement of the debt sustainability of external public debt using SRED

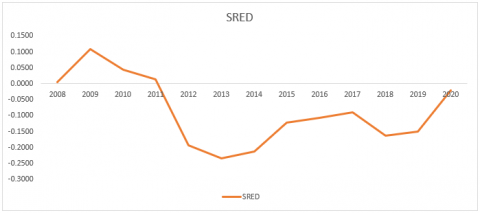

Table 5 shows the measurement of government debt sustainability using SRED from 2008-2020. The data are used to measure SRED, namely Current Account Balance, Net Capital Account, External Debt Interest Payments, and External Public Debt Principal Payments. The current account balance is positive between 2008-2011, but it is negative for the 2012-2020 period. Net Capital Account tends to decrease from 294 Million USD (2008) to 37 Million USD (2020). Interest payments on debt have doubled from 2008-2020, from 9,709 Million USD to 23,527 Million USD.

The principal repayments also doubled from 85,136 Million USD to 206,375 Million USD. The principal and interest payment on the debt is very burdensome to the national budget, and the government must make some savings and program adjustments. External Debt Interest Payments and External Public Debt Principal Payments tend to increase yearly and are not matched by the improving Current Account Balance and Net Capital Account values. The Current Account Balance is getting worse due to high import needs and the need to pay services and dividends to external households. This situation makes the SRED value minus from 2012 to 2020, which can be seen in Table 5 and Figure 1.

Table 5. Measurement of external public debt using the solvency rate of external debt (SRED), 2008-2020

|

Period |

Current Account Balance (Million USD) |

Net Capital Account (Million USD) |

External Debt Interest Payments (Million USD) |

External Public Debt Principal Payments (Million USD) |

SRED |

|

2008 |

0,125 |

294 |

9.709 |

85.136 |

0,0049 |

|

2009 |

10.630 |

96 |

8.932 |

90.853 |

0,1080 |

|

2010 |

5.144 |

50 |

8.838 |

106.860 |

0,0438 |

|

2011 |

1.685 |

33 |

9.326 |

116.410 |

0,0145 |

|

2012 |

-24.418 |

51 |

11.168 |

116.187 |

-0,1932 |

|

2013 |

-29.109 |

45 |

12.154 |

114.924 |

-0,2340 |

|

2014 |

-27.510 |

27 |

12.679 |

123.806 |

-0,2118 |

|

2015 |

-17.519 |

17 |

14.846 |

137.396 |

-0,1227 |

|

2016 |

-16.952 |

41 |

13.146 |

154.875 |

-0,1068 |

|

2017 |

-16.195 |

46 |

16.277 |

177.318 |

-0,0894 |

|

2018 |

-30.633 |

97 |

19.250 |

183.197 |

-0,1639 |

|

2019 |

-30.279 |

39 |

19.240 |

199.876 |

-0,1491 |

|

2020 |

-4.433 |

37 |

23.527 |

206.375 |

-0,0210 |

Source: Author’s calculations based on data from; Bank of Indonesia, Ministry of Finance, Statistics of Indonesia and World Bank

Figure 1. SRED Indonesia, 2008-2020

Based on SRED calculations, the external public debt is in an unsustainable condition. A minus SRED value for nine consecutive years implies an increased risk of default on public debt repayments in the future. This condition was caused by an expansionary fiscal policy which increased imports from other countries and solvency risk [29]. The demand for imported goods is very high and is exacerbated by insufficient efforts to substitute imports of goods and services. The government must improve the investment climate to reduce the high of capital flight.

Low solvency risk is also related to fiscal sustainability. Fiscal policy is considered sustainable when it can be maintained long-term and does not violate solvency constraints [30]. The minus SRED value can also be caused by the depreciation of the domestic currency against external currencies, especially the US Dollar. Currency depreciation makes import payments and dividends more expensive and reduces the availability of US dollars in the domestic money market.

The impact of the global financial crisis and the COVID-19 pandemic has pushed the government's external debt to grow. The increase in debt has generated tremendous concern from politicians, economists, and the public about the government's ability to repay debt in the future. One way to analyze the ability to pay the debt is by analyzing debt sustainability. This study aims to measure Indonesia's debt's sustainability after the global financial crisis and during the COVID-19 pandemic with the Threshold Value from The Debt Sustainability Framework for Low-Income Countries (LIC-DSF) and the Solvency Rate of External Debt (SRED).

Based on the LIC-DSF Threshold Value, three indicators are below the low-risk threshold and the external public debt on sustainable condition. However, the COVID-19 pandemic has caused the external public debt interest payment ratio to tax revenue to be above the high-risk threshold. The minus value of SRED shows the external public debt in Indonesia on unsustainable condition. The SRED results indicate a risk to government’s ability to repay the debt in the future because the balance of payments and capital account have an unsatisfactory performance and the impact of the domestic currency depreciation against the US Dollar. The insufficient research of this paper and the prospect of future research is to expand many samples in others developing countries with the same characteristics. This further research is expected to be able to have a positive impact on countercyclical policies to reduce the risk of external debt default in developing countries during the COVID-19 pandemic.

We thank Universitas Negeri Semarang for providing material and non-material support. With this support, our research team was able to complete this article properly and smoothly.

[1] Brady, G.L., Magazzino, C. (2017). The sustainability of italian public debt and deficit. International Advances in Economic Research, 23(1): 9-20. https://doi.org/10.1007/s11294-016-9623-7

[2] Mahmood, T., Rauf, S.A. (2012). Public debt sustainability: Evidence from developing country. Pakistan Economic and Social Review, 50(1): 23-40. https://www.jstor.org/stable/24398815

[3] Law, S.H., Ng, C.H., Kutan, A.M., Law, Z.K. (2021). Public debt and economic growth in developing countries: Nonlinearity and threshold analysis. Economic Modelling, 98: 26-40. https://doi.org/10.1016/j.econmod.2021.02.004

[4] Makin, A.J., Pearce, J. (2014). How sustainable is sub-national public debt in Australia? Economic Analysis and Policy, 44(4): 364-375. https://doi.org/10.1016/j.eap.2014.10.001

[5] Dakhlallah, K.M. (2020). Public debt and fiscal sustainability: the cyclically adjusted balance in the case of Lebanon. Middle East Development Journal, 12(2): 340-359. https://doi.org/10.1080/17938120.2020.1773076

[6] Islam, M.E., Biswas, B.P. (2005). Public debt management and debt sustainability in bangladesh. The Bangladesh Development Studies, 31(1): 79-102. https://www.jstor.org/stable/40795703

[7] Mahmood, T., Rauf, S.A., Khalil Ahmad, H., Rauf, A., Khaul Ahmad, H. (2009). Public and external debt sustainability in pakistan (1970s-2000s). Pakistan Economic and Social Review, 47(2): 243-267. https://www.jstor.org/stable/25825355

[8] Teică, R.A. (2012). Analysis of the public debt sustainability in the economic and monetary union. Procedia Economics and Finance, 3: 1081-1087. https://doi.org/10.1016/s2212-5671(12)00277-8

[9] Marquez, N. (2000). Debt sustainability in the eccb area. Social and Economic Studies, 49(2): 77-108. https://www.jstor.org/stable/27865196

[10] Bui, D.T. (2019). Fiscal sustainability in developing Asia - new evidence from panel correlated common effect model. Journal of Asian Business and Economic Studies, 27(1): 66-80. https://doi.org/10.1108/jabes-01-2019-0001

[11] Mukhtarkhan, A. (2022). Formation and management of public debt sustainability on the example of the Republic of Kazakhstan and the Russian Federation. International Journal of Organizational Analysis, 30(2): 542-567. https://doi.org/10.1108/IJOA-10-2020-2453

[12] Omotor, D. (2021). External debt sustainability in west african countries. Review of Economics and Political Science, 6(2): 118-141. https://doi.org/10.1108/reps-11-2019-0144

[13] Ucal, M., Oksay, S. (2011). The Solvency ratio of external debt (SRED) as an indicator of debt crisis: the case of Turkey. Int. J. Eco. Res, 2(1): 166-172. http://www.tcmb.gov.tr/research/discus/8810eng.pdf.

[14] Mahmood, T., Farooq, M., Sherazi, H. (2014). Debt sustainability: A comparative analysis of SAARC countries. Pakistan Social Dan Economic Review, 52(1): 15-34. https://www.jstor.org/stable/24398845

[15] Clarke, C., Whitely, P., Reid, T. (2022). Fiscal sustainability in highly indebted countries: Evidence from Jamaica. International Journal of Development Issues, (ahead-of-print). https://doi.org/10.1108/IJDI-01-2022-0003

[16] Campos, E.L., Cysne, R.P. (2022). Sustainability of Brazilian public debt: A structural break analysis. International Journal of Emerging Markets, 17(3): 645-663. https://doi.org/10.1108/IJOEM-11-2019-0936

[17] Nasir, M. (2014). Solvency analysis on indonesia's external debt. Kajian Ekonomi dan Keuangan, 18(2): 99-118. https://doi.org/10.31685/kek.v18i2.149

[18] Kuncoro, H. (2011). The sustainability of state budget in debt repayment. Bulletin of Monetary and Banking, 13(4): 415-434. https://doi.org/10.21098/bemp.v13i4.400

[19] Eğrican, A.T., Caner, S., Togan, S. (2022). Reforming public debt governance in Turkey to reach debt sustainability. Journal of Policy Modeling, 44(5): 1057-1076. https://doi.org/https://doi.org/10.1016/j.jpolmod.2022.07.004

[20] Napo, S. (2022). Assessing public debt sustainability under COVID‐19 uncertainty: Evidence from Côte d'Ivoire. African Development Review, 34(1): S141-S160. https://doi.org/10.1111/1467-8268.12649

[21] Burger, P., Calitz, E. (2021). COVID-19, economic growth and south african fiscal policy. South African Journal of Economics, 89(1): 3-24. https://doi.org/10.1111/saje.12270

[22] Sennoga, E., Balma, L. (2022). Fiscal sustainability in Africa: Accelerating the post‐COVID‐19 recovery through improved public finances. African Development Review, 34(1): S8-S33. https://doi.org/10.1111/1467-8268.12649

[23] Paczos, W., Shakhnov, K. (2022). Defaulting on covid debt. Journal of International Financial Markets, Institutions and Money, 77: 101516. https://doi.org/10.1016/j.intfin.2022.101516

[24] Kappagoda, N. (2007). Debt sustainability framework for low-income countries. In Workshop on Debt, Finance and Emerging Issues in Financial Integration, London. https://static.un.org/esa/ffd/wp-content/uploads/2007/03/20070306.

[25] Elkhishin, S., Mohieldin, M. (2021). External debt vulnerability in emerging markets and developing economies during the COVID-19 shock. Review of Economics and Political Science, 6(1): 24-47. https://doi.org/10.1108/reps-10-2020-0155

[26] Pratibha, S., Krishna, M. (2022). The effect of COVID-19 pandemic on economic growth and public debt: an analysis of India and the global economy. Journal of Economic and Administrative Sciences. https://doi.org/10.1108/jeas-01-2022-0018

[27] Liao, W.J., Kuo, N,L., Chuang, S.H. (2021). Taiwan’s budgetary responses to COVID-19: The use of special budgets. Journal of Public Budgeting, Accounting & Financial Management, 33(1): 24-32. https://doi.org/10.1108/JPBAFM-07-2020-0128

[28] Apostol, L.M. (2019). Evolution of the main indicators of public debt sustainability in the period 2014-2018 in romania. Scientific Bulletin - Economic Sciences, 18(2): 36-47. http://economic.upit.ro/repec/pdf/2019_2_5.pdf.

[29] Beetsma, R. (2022). The economics of fiscal rules and debt sustainability. Intereconomics, 57(1): 11-15. https://doi.org/10.1007/s10272-022-1021-1

[30] Esteve, V., Prats, M.A. (2022). Testing for multiple bubbles: historical episodes on the sustainability of public debt in Spain, 1850-2020. Applied Economic Analysis. https://doi.org/10.1108/AEA-01-2021-0003