Suwinto Johan

© 2022 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study aims to establish a link between Sharia financing, the Sustainable Development Goals (SDG), and green financing. The relationship will be capable of resolving human challenges in the future. This study uses the qualitative normative descriptive. Both sharia and green finance contribute to the achievement of the SDGs. Sharia and green financing both contribute to increased welfare. The purpose of this research is to examine the development of shariah financing and the implementation of the Sustainable Development Goals in Indonesia. Indonesia is a developing country with the largest Muslim population in the world. The research findings will benefit bank executives and regulators of financial services. The research takes a novel approach to the Sustainable Development Goals, Sharia financing, and green financing. This study integrates three critical components: green financing, Sustainable Development Goals financing, and Sharia financing. Furthermore, this research examines the financial industry's role in fostering a more hospitable environment for human life. In order to achieve sustainable development goals, shariah financing and green financing are complementary, according to this study.

green financing, sharia financing, sustainable development goals

The Sustainable Development Goals (SDGs) are a collection of global objectives that all 193 United Nations member countries must strive to achieve. By 2030, the SDGs seek to achieve sustainable livelihoods [1]. The pandemic of COVID-19 has harmed the SDG targets (COVID-19). COVID-19 has harmed every country's economic structure [2, 3]. The state government has concentrated its efforts on recouping the impact of COVID-19. Indonesian President Joko Widodo has urged all stakeholders to work together to achieve the Sustainable Development Goals targets during the pandemic by leveraging the government and private sectors' respective knowledge and advantages [4]. Two of the private sector's responsibilities are profitability and social responsibility [5].

Financial services are one of the sectors that contribute to the achievement of the Sustainable Development Goals. Sustainable financing is financial assistance provided by a financial institution to promote economic, social, and environmental harmony [6]. The financial industry can contribute significantly to achieving the SDGs. The finance industry is classified as either conventional or Sharia-compliant. Conventional financial institutions provide credit, while Islamic financial institutions provide financing.

The Indonesian Central Bank has endorsed Sharia financing as a strategy for achieving the Sustainable Development Goals. The same principles guide sharia finance as the Sustainable Development Goals, namely ethics, justice, and equality [7]. According to the chairman of Indonesia's Financial Services Authority (OJK), Sharia financing is one of the global solutions for achieving the SDGs' target [8]. The Finance Minister of Indonesia, Sri Mulyani, stated that Islamic values are compatible with achieving the SDGs. Additional Sharia-compliant financial instruments are required urgently [9]. Additionally, the Sharia Capital Market plays a critical role in advancing the Sustainable Development Goals [10]. Eleven of the seventeen Sustainable Development Goals were directly related to Sharia financing [11].

There has been no previous research on this subject. This study delves deeply into three critical issues: green financing, Sustainable Development Goals, and Sharia financing. The purpose of this research is to reassure financial institution businesses of the critical importance of focusing on sustainable development via green and Sharia financing. Additionally, this research discusses the financial industry's role in creating a more hospitable environment for human life.

People still believe Sharia Financing and Green Financing are two separate concepts. There has been little debate about how Sharia Financing and Green Financing can be used to achieve long-term development goals. The goal of the study is to connect the two types of financing in order to achieve the Sustainable Development Goals. The goal of this study is to illustrate how the two types of finance contribute to accomplishing long-term development goals.

Research on SDGs, Sharia-compliant financing, and green financing are still rare. This research examines alternatives to Sharia-compliant and green financing for achieving the SDGs. At the moment, available research is limited to two variables. This study examines three variables. The studlies of [12-21] have all researched sharia financing.

Today's economic development is market-driven, whereas Sharia economics focuses on holistic human development. [22]. The financing method reflects the economic principle. While free-market economics emphasizes competition and profit or return on investment, Sharia economics emphasizes human development and community welfare.

Sharia financing research continues to be primarily concerned with comparing conventional and Sharia financing, as well as governance issues [5]. Numerous studies have concluded that Sharia financing violates the Sustainable Development Goals [19]. Sharia financing cannot be carried out correctly, and a gap exists between practice and theory [23, 24]. The discussion of Shariah Finance concerning the Sustainable Development Goals and Green Finance is an enticing area of research.

Along with zakat and adaqah, the Shariah-based financing institution of waqf can undoubtedly contribute significantly to resolving humanitarian crises caused by climate change [13]. These sectors face the most significant risk of economic disruption as a result of COVID-19. Sharia financing can be used to help resolve humanitarian crises [3]. Sharia-compliant financial products have the potential to assist in resolving socioeconomic issues. Sharia financing has been proven to be effective at empowering women and improving social welfare. Sukuk proceeds will improve education, health, and environmental conditions [20]. Sharia financing for productive sectors, such as micro, small, and medium-sized enterprises (MSMEs), contributes to the welfare and equality objectives of the Sustainable Development Goals (SDGs) [21]. Infaq, Waqf, and Zakat are all types of philanthropic funds that can help close the investment gap for the Sustainable Development Goals. Countries must work cooperatively to accomplish the SDGs [18]. Sharia financing enables countries to achieve their Sustainable Development Goals.

Sharia financing can be used to redistribute income through various mechanisms, including Sadaqah, Zakat, Waqf, Sukuk, Musharakah, and Murabahah. It may have beneficial consequences for the real sector of the economy that is capable of achieving SDGs' objectives [25]. Sukuk can help the world overcome socioeconomics inequalities [20]. The concept of Bai Salam in Sharia-based financing for SDGs implementation [26]. Sharia financing should aim to increase social inclusion and poverty reduction [27]. Several examples of Sharia financing’s contribution are the construction of restrooms by Indonesian Zakat distribution, which benefits its beneficiaries. This is consistent with SDG No. 6’s objectives [28].

The Sharia financing industry offers innovative products to help achieve these SDGs [12]. Economic growth is facilitated by a well-functioning Shariah financial system [17]. Sharia Financing can contribute to sustainable economic development by increasing access to finance, projects financing, and Takaful reaches. Productive businesses that are grounded in reality can have a beneficial effect on the development ecosystem. Sharia financing can help families meet unaffordable financial needs through conventional financing [14].

Sharia financing cannot be implemented without the cooperation of all interested parties [16]. Sharia is a novel economic model. Regulators, business actors, and all parties with knowledge must promote and educate the public about sharia financing. One of them is to incentivize conventional banks to spin off their sharia-compliant business. With a self-contained unit, the sharia business unit is distinct from its conventional business unit. The establishment of Sharia banks will ensure that SDGs principles adhere [15]. While conventional banks prioritize free markets, sharia banks prioritize human development.

A significant funding amount will be required to achieve the SDGs. A significant funding amount must be accompanied by a high level of customer satisfaction [16]. Financing is available in two forms: conventional and Sharia-compliant. Finance is the engine of the economy. Shariah Financing has the same effect on the national economy as conventional financing does.

Sharia Financing is available through a variety of financial institutions. Sharia finance can be conducted through sharia banking, sharia consumer finance institutions, sharia pawnshops, sharia microfinance, sharia capital markets, or sharia insurance. Sharia microfinance institutions have been shown to contribute positively to achieving the Sustainable Development Goals in four categories, namely Profit and Loss Sharing Financing, Loss Sharing Financing, Social Enterprises based on Financing, and Social Financing. The study in Bangladesh. Sharia financing is based on the concept of profit and loss sharing and is interest-free [29]. Sharia Financing is interest-free. Interest is a fee associated with traditional financing.

Sharia financing has the potential to empower women by enabling them to participate in sustainable development. Sharia financing has increased the number of women in the banking industry [30]. Sharia Financing contributes to one of the SGDs' primary objectives, gender equality. The SDGs aim to achieve gender equality.

Sharia banking must expand to the lower classes to finance poverty eradication [31]. Financing collaborative innovation between religious and non-religious institutions is one of the recommended strategies for achieving the SDGs. Historically, it has been challenging to bring Shariah financing to the local community. Financing shariah financial literacy through technology will be possible.

Additionally, Zakah can aid in the achievement of the Sustainable Development Goals [32]. The Zakat Fund is one method of alleviating poverty. Poverty eradication is one of the SDGs goals [33, 34].

Additionally, accountants contribute to the achievement of the SDGs. The Accountants Association has issued guidelines for Sharia Financing accounting [35]. Sharia financing businesses have unique accounting records. Accounting instructions are critical. Sharia accounting records are kept differently than conventional accounting records. One of the Sharia Financing requirements is that the method of accounting for Sharia Financing be followed. Current financing is interest-based, whereas sharing financing introduces profit- or loss-sharing financing.

Meanwhile, Sharia economy implementation is not guided by the SDGs. The SDGs are an approach based on accommodating modification that runs counter to Sharia epistemology. Sharia financing for development must be completely redefined. The SDG concept is incompatible with Sharia economics [19]. On the other hand, Sharia financing is an alternative financial system for assisting individuals with COVID-19 [36].

Sharia financing's success is contingent upon customer trust [37]. Additionally, Sharia financing has a more structured approach to implementing good corporate governance (GCG) [38]. Sharia financing is superior to conventional financing in terms of corporate governance. A Sharia Supervisory Board oversees the Sharia Institution. Shareholders appoint the Sharia Supervisory Board at the Annual General Meeting. The Sharia Supervisory Board is in charge of supervising the director's operations. The National Sharia Council must approve members of the Sharia Supervisory Board. The National Sharia Board will appoint the Sharia Supervisory Board. This Sharia Supervisory Board is responsible for supervising the entire day-to-day operation of the company's sharia business.

Sharia business growth is conditional on macroeconomic and microeconomic conditions. The sharia stock price index is negatively impacted by currency exchange rates, inflation, and gross domestic product. The study examined the Indonesian capital market [39]. Currency depreciation reduces the amount of Islamic financing. Meanwhile, rising inflation will result in a decline in sharia financing. Currency exchange rates and inflation affect business. When macroeconomic variables are unstable, the business world will halt expansion.

Sharia financing is a powerful tool for achieving Sustainable Development Goals. However, no instrument assessing Sharia financial literacy has been developed to date [40]. It is critical to developing a measurement matrix for Sharia financial literacy. Sharia financing continues to fall short of its stated objectives, and there is still a disconnect between theory and practice [22]. Non-Muslim countries such as Singapore face some challenges, including the absence of internationally standardized rules of engagement for Sharia financing and banking and a talent shortage [41]. Additionally, several barriers to Sharia crowdfunding, including regulatory issues, project management, secondary markets, fraud, and Shariah compliance [24].

Additionally, Sharia financing is instrumental in advancing the halal industry and achieving the SDGs' goals [42]. Sharia financing also helps mitigate CO2 emissions from transportation and other sectors, excluding residential buildings and commercial and public services. The residential building and commercial and public services sectors are strongly associated with the development of Sharia financing in Indonesia [43]. Sharia financing may be used as a substitute financial system to assist individuals and entrepreneurs affected by COVID-19 [38]. Shariah Financing is active in several industrial sectors. Shariah Financing makes a direct and indirect contribution. Shariah Financing can be used to promote green finance. Green Financing will result in a reduction in CO2 emissions. Shariah Financing also contributes to housing ownership. Shariah Financing offers fixed-rate financing, allowing Shariah Financing to contribute to sustainable development.

In conjunction with Sharia financing, green financing can be critical in facilitating rural farmers' access to cold storage [44]. Significant facets of green microfinance align with the SDGs [45]. Green and Sharia financing can be critical in developing agricultural storage facilities. This will mitigate the community's impact of poverty, hunger, and malnutrition. This will assist a country in achieving the SDGs [46].

The term "green financing" refers to a new type of finance that is used in the process of combining environmental conservation and financial gain. This phrase refers to a broad range of environmentally friendly technologies, projects, and industries, as well as the testing of concepts for balancing ecological depreciation in the carbon absorption process in the atmosphere [47]. Green banking is an important aspect of Islamic banking that helps to safeguard the environment. Islamic banks have made a substantial contribution to green banking, which benefits the environment through cost and energy savings, natural resource preservation, and the requirement to treat all living things with respect [48]. Green funding has a large and positive impact on environmental performance [49].

Increase the role of public financial institutions and non-banking financial institutions (pension funds and insurance companies) in long-term green investments, use the spillover tax to increase the rate of return on green projects, develop green credit guarantee schemes to reduce credit risk, establish community-based trust funds, and address green investment risks through financial and policy de-risking are all practical solutions in green financing [50]. It is anticipated that nearly half of China's annual gross domestic product (GDP) will be required to pay for environmental costs, hence shifting China's huge economy to a green economy is critical. The green financing system aids in the reduction of environmental risks around the world [51].

This research focuses on three areas: Sharia finance in a Sharia economy, sustainable development goals (SDGs), and green finance by Sharia financial institutions. How can financial institutions finance green projects within the Sharia framework to contribute to the SDGs' achievement? Discussions of green finance in conjunction with Sharia finance are still uncommon. Scientific research continues to link Sharia financing to the SDGs.

The following are the research questions: How is green financing being implemented in conjunction with Sharia financing? How can green and Sharia financing contribute to the achievement of the SDGs? Why will the spin-off of the sharia business unit benefit the development of sharia finance?

Normative, descriptive, or literature studies entail the examination of standards and conducting systematic research. The research method is a normative descriptive research technique or a literature search guided by the formulation of the research problem and its context. This research utilized secondary sources or library resources.

Qualitative research is the most frequently used method for examining the relationship between Sharia Financing and the Sustainable Development Goals. In the last four years, there has been an increase in research on Sharia Financing [52]. Sharia Financing and the Sustainable Development Goals have become a focus of research. This is consistent with the SDGs' problem.

The research's topic focuses on existing Sharia Finance and Green Financing standards. The experts' reasons for both methods of financing are the subject of this investigation. Descriptive discussion has additional benefits in terms of maximizing the topic's potential.

Primary, secondary, and tertiary or supporting materials are used in normative and descriptive research. The primary source material for this research is the Republic of Indonesia's 1945 Constitution and other Sharia-related regulations. The secondary legal material consists of journal articles, theories, scientific books pertinent to the research title, symposium/seminar proceedings, and scientific articles. Tertiary materials combine the characteristics of primary and secondary materials [53].

Sharia finance is an Islamic concept. Sharia financing is interest-free and is not permitted to finance specific sectors that Islam prohibits. Sharia principles include justice and balance ('adl wa tawazun), benefit (maslahah), and universalism (alamiyah), and are devoid of gharar, maysir, usury, injustice, and unlawful objects. Islamic finance does not charge interest and is based on the profit-sharing principle. Additionally, Islamic financing does not impose early payment penalties. Islamic financing is distinct from conventional financing in that it makes use of separate agreements. Sharia financing penalties are used to fund charitable endeavors.

In terms of equity holders, the relationship between Islamic financial institutions and their customers is a partnership (musyarakah and mudharabah), a seller-buyer relationship (murabahah, salam, and istishna), a lease relationship (ijarah), and a debtor-creditor relationship (qard). Sharia financing is a collaborative effort, not a transaction.

Meanwhile, the relationship between traditional financial institutions and their customers resembles that of creditors and debtors. Profits and losses are the basis for this relationship. Sharia financing, per religious principles, did not finance the prostitution industry and prohibited animal slaughter and derivatives.

Sharia financing is a non-traditional method of financing for small, medium, and micro-businesses. Sharia-compliant financing is available through banks, non-bank financial institutions, and pawnshops. Additionally, Islamic financial institutions include Sharia-compliant insurance and Sharia-compliant capital market investments. This financing mechanism has been developed in some countries with a predominantly Muslim population. Islamic finance has expanded faster than conventional banking, particularly during the COVID-19 Pandemic.

Green finance is an investment that goes toward sustainable development projects and initiatives, environmental products, and policies that promote economic sustainability . Green financing is a type of bank financing targeted at industries or activities that contribute to sustainable development. This financing is targeted at sectors that contribute to the achievement of sustainable development goals (SDGs).

Green financing is a way for financial institutions, mainly banks and lending institutions, to demonstrate their commitment to achieving sustainable development. The government has not mandated the distribution of green financing. Green financing will raise businesses' awareness of the importance of sustainable development. Every industry has the potential to be a green industry.

The SDGs are a 17-goal global action plan. The SDGs have evolved into a shared commitment among United Nations members. The 17 SDGs aim to improve the world's standard of living by eradicating poverty, preserving the environment, achieving gender and educational equality, and ending climate or environmental change.

The Sustainable Development Goals (SDGs) were announced on September 25, 2015, and are expected to be achieved by 2030. One hundred ninety-three member countries made this announcement at the United Nations office. The United Nations' primary focus is on the Sustainable Development Goals. Attaining SDG targets has become increasingly difficult in the aftermath of the COVID-19 pandemic. Additionally, the COVID-19 pandemic exemplifies one of the SDG issues, namely health and equity. The pandemic demonstrated that health issues are a source of contention for humanity. Vaccinating the entire world's population is also a challenge. SDGs are critical for achieving sustainable development.

Numerous financial institutions establish a Sharia business unit (UUS) early on. Traditional financial institutions have established a Sharia business unit to conduct Sharia business. Sharia financial institutions absorbed the Sharia business unit. An employee holds the position of head of the Sharia business unit. The Sharia Supervisory Board oversees the Sharia business unit process (DPS). Conventional financial institutions conventionally conduct business. By and large, conventional business activities refer to the operations of financial institutions. The financing is disbursed with an eye toward the financial institution's profit. The primary objective of conventional financial institutions is profit. Sharia is a business unit within conventional financial institutions.

Sharia business units are governed similarly to conventional financial institutions. The board of directors is composed of directors, and the board of commissioners is composed of commissioners. This governance includes the Sharia Supervisory Board. The Sharia Supervisory Board's primary responsibility is to oversee the Sharia business unit. Sharia Financing's implementation of good corporate governance (GCG) has a more robust structure [40].

Sharia Financing Institutions (LPS) can provide Sharia-compliant savings with an emphasis on green finance. This provides the Sharia Financing Institution with a competitive edge. Contribution to sustainable development through funding or customer savings the customer's contribution to sustainable development can be communicated as value to prospective customers. Customers can be educated that they have contributed to sustainable development by saving money at a Sharia Financing Institution. This may be an incentive for customers to use Sharia Financing Institutions to save money. Additionally, the Sharia Financing Institution can implement green banking practices to bolster its competitive advantage as a Sharia Financing Institution specializing in green financing [55].

Financial institutions or banks can impose some environmental requirements on any customer or business seeking to borrow money. Standardization of waste disposal, standardization of a safe working environment, and standardization of the use of recycled raw materials are all examples of environmental requirements. If a customer does not meet the requirements, the financial institution will deny them credit. Financial or banking institutions could concentrate their efforts exclusively on recycling and environmentally friendly industries.

Environmental factors can be included as a criterion in the corporate rating by government agencies or credit rating agencies. As a result, financial institutions and businesses will place a premium on this variable. Sharia Financing complies with all green financing requirements. Sharia Financing will be the preferred method of financing for financial business actors. Numerous forms of Sharia Financing satisfy the criteria for green financing.

Green financing can help achieve the Sustainable Development Goals by ensuring access to safe drinking water and adequate sanitation, clean energy, a healthy work environment, sustainable urban development, responsible consumption and production, a healthy land environment, peace, justice, and strong institutions. Robust institutions, both public and private, will expedite the implementation of SDG activities. A vital institution enables the implementation of SDGs, Sharia Financing, and Green Financing.

In the first stage, financial institutions distribute financing to customers after conducting due diligence. Due diligence is used to determine the customer's viability as a business owner and ability to repay the financing provided. Financial institutions have the authority to set the criteria for financing and disbursing funds. Additionally, financial institutions have the option of disbursing different types of financing.

Financing institutions can govern green financing at the time customer financing applications are accepted. In addition to green financing, financing institutions can distribute financing funds through Sharia financing. Early on, financing institutions will be able to establish these criteria. These criteria were validated as part of the due diligence process. Due diligence is accomplished by demonstrating the customer's capability and the nature of the customer's business to comply with financial institution requirements for disbursing funds.

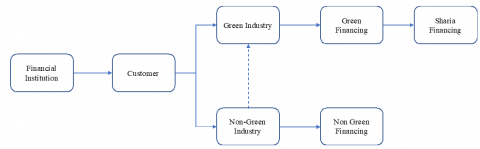

Financial institutions must establish policies governing funds disbursement. This policy applies to the industries that will be financed. Green financing enables financial institutions to assess the criteria for environmentally friendly industries. Financial institutions can also opt for environmentally friendly business models. The business model can be Sharia-compliant. Sharia Financing is the type of financing used in the Sharia business model. This is illustrated in Figure 1.

Certain financial institutions have difficulty determining the appropriate type of financing to disburse. Financial institutions have always faced a conflict between achieving objectives and adhering to the established business model. Financial institutions struggle to reconcile profitability with business model ideals.

Financial institution leaders, including shareholders, must establish business model policies that align with the institution's objectives. Financial institutions must maintain a long-term focus. Financial institutions should not make a trade-off between short- and long-term objectives.

Financing distribution strategies can be implemented. Eco-finance is one strategy that financial institutions can employ. Financial institutions can establish a competitive edge in the financial industry. Through Sharia financing, Sharia financial institutions can validate the Sharia business model. Financial institutions will be able to contribute to the achievement of the SDGs if they meet these two criteria. This procedure is illustrated in Figure 2.

Green finance contributes to the achievement of the Sustainable Development Goals, particularly the sixth goal on clean water and sanitation; the seventh goal on affordable and clean energy; the eighth goal on decent work and economic growth; the eleventh goal on sustainable cities and communities; the thirteenth goal on climate action; the fifteenth goal on life on land; and the seventeenth goal on partnerships for the goals.

Figure 1. Green financing business model

Figure 2. Combination of Sharia financing, green financing, and SDGs

On the other hand, Sharia financing can help achieve sustainable development goals, particularly the first goal of No Poverty, the third goal of Good Health and Well-Being, the eighth goal of Decent Work and Economic Growth, the tenth goal of Reduced Inequality, the sixteenth goal of Peace, Justice, and Strong Institutions, and the seventeenth goal of Partnerships for the Goals.

Sharia Finance is based on a profit-sharing or partnership model that emphasizes collaboration in the pursuit of a better living. Sharia finance will be able to alleviate poverty, grow the economy, restore economic equilibrium, build strong institutions, and collaborate to achieve common goals. The first, third, eighth, tenth, and seventeenth Sustainable Development Goals (SDGs) are listed here. Meanwhile, green funding will help to establish an environment with clean water, clean energy, environmentally conscious economic growth, sustainable cities, climate change action, and a better living. Both on land and in collaboration to achieve the SDGs. SDGs 6, 7, 8, 11, 13, 15, and 17 all aim to achieve this. The results are line with research of [3, 13, 20, 21, 27, 31-34]

Table 1 details the SDGs' achievement through Sharia and green financing.

Table 1. Achievement of SDGs by Sharia financing and green financing

|

No. |

Sustainable Development Goals |

Sharia Financing |

Green Financing |

|

1. |

Sustainable Development Goals |

1, 3, 8, 10, 16, 17 |

6, 7, 8, 11, 13, 15, 17 |

The SDG targets will be strengthened, and their achievement accelerated with the support of Sharia financial institutions. Green and Sharia financing are complementary and not mutually exclusive. Sharia financing's expansion will enable an increase in green financing. The combination of green and Sharia financing will enable the majority of SDG targets to be met.

Sharia Finance Institutions follow the same structure as conventional financial institutions. A special board supervises the Sharia Institution. This board ensures that sharia business is conducted per the sharia principles established by the Indonesian Ulama Council via the National Sharia Council. The National Sharia Board will appoint the Sharia Supervisory Board. This Sharia Supervisory Board is responsible for overseeing the company's sharia business. Figure 3 illustrates this.

Meanwhile, several financial institutions have established a Sharia-compliant business directly by establishing a Sharia-compliant financing institution. Sharia financial institutions entirely finance sharia financing. The criteria for financing must adhere to all Sharia principles. The Board of Directors and the Board of Commissioners are the governing bodies of a Sharia-compliant financing institution. The Sharia Supervisory Board is responsible for overseeing the operations of all Sharia financing institutions per Sharia principles. Sharia financing institutions conduct their operations per Sharia principles. Figure 4 demonstrates this.

The Sharia Business Unit, a division of a conventional financial institution, will face challenges in implementing the SDGs' principles. The Sharia business unit's mission is distinct from that of conventional financial institutions. Disparities in objectives affect the Sharia Business Unit's work processes.

The spin-off of the Sharia Business Unit to the Sharia Financing Institution will enable the Sharia Financing Institution to distribute Sharia financing in support of the SDGs' achievement. Sharia principles will guide the disbursement of financing. Besides the Sharia Financing Institution's shareholders target, Sharia Financing Institutions will have responsibilities and obligations per Sharia Principles. These distinctions are detailed in Table 2.

Figure 3. Governance of conventional financing institution with Sharia business unit

Figure 4. Governance of Sharia financing institution

Sharia Financing Institutions prioritize the distribution of Sharia financing based on Sharia principles. If the Sharia business unit becomes a subsidiary of a conventional financing institution, profit or profitability becomes the primary driver. Sharia business unit spin-offs will benefit Sharia Business Unit in achieving Sharia financing distribution by allowing it to become a Sharia Financing Institution. This division is backed up by the Republic of Indonesia's Law No. 21 of 2008 on Sharia Finance and Banking.

Green banking can be applied to service units in various ways, including the provision of digital-based services (e.g., SMS banking, mobile banking, and internet banking) and the reduction of plastics and other environmentally unfriendly materials. The same principle can be applied to operational units, for example, by reducing paper consumption and turning off air conditioners when not in use.

Figure 5. Sharia business model

Table 2. Comparison of Sharia business unit and Sharia financing institution

|

No. |

Item |

Sharia Business Unit |

Sharia Financing Institution |

|

1. |

Status |

Part of Conventional Financing Institution |

Sharia Institution |

|

2. |

Entities of Financing Institution |

The Board of Directors and the Board of Commissioners are entities of conventional financing institution |

The Board of Directors and the Board of Commissioners are the entities of the Sharia Financing Institution |

|

3. |

Position of Sharia Supervisory Board |

Overseeing Sharia Business Unit |

Overseeing Sharia Financing Institution as a whole |

The distribution of Sharia-compliant financing must follow this financing. Funding is targeted at environmentally conscious industries. Industries that care about the environment include those that prioritize reforestation, such as mining with a reforestation strategy, industries that recycle their production materials, sectors that use few chemicals, and initiatives that promote reforestation.

Allocation and distribution of Sharia-compliant financing, including financing for reforestation. The Sharia business model begins with Sharia-compliant financing. Following the funding, funds must be distributed according to Sharia principles. Sharia Financing Institutions will have a business model advantage over conventional financing institutions when Sharia Financing Institutions combine Sharia Financing and reforestation financing. Figure 5 depicts the Sharia business model.

Sharia financing, green financing, and SDGs are three distinct series that work in tandem to improve human life. Independent Sharia Financing enables a more effective implementation of the SDGs. Sharia financial institutions can develop strategies for achieving the Sustainable Development Goals through Sharia and green financing. The establishment of Sharia-compliant and green financing criteria for the distribution of financing funds will expedite the achievement of the SDGs. The combination of Sharia Financing and Green Financing has been described in research as a way to meet the Sustainable Development Goals. New research sheds light on how Sharia Financing and Green Financing can complement each other. Green financing requires regulatory incentives. This incentive contributes to the achievement of the SDGs. The SDGs will be achieved more quickly with the assistance of Sharia financial institutions. SDG research can be developed by examining the aggregate effect of profits on an economy. Additionally, additional analysis can be conducted to compare the quality of Sharia and green financing quality to conventional industry financing.

The funders had no role in study design, data collection, analysis, decision to publish, or manuscript preparation.

[1] Johan, S. (2021). Determinants of corporate social responsibility provision. The Journal of Asian Finance, Economics, and Business, 8(1): 891-899. https://doi.org/10.13106/jafeb.2021.vol8.no1.891

[2] Widodo, J. (2020). Jokowi Minta Infrastruktur Digital Dipakai untuk Hal Positif. Baca artikel CNN Indonesia.

[3] Miah, M.D., Suzuki, Y., Uddin, S.S. (2021). The impact of COVID-19 on Islamic banks in Bangladesh: a perspective of Marxian “circuit of merchant’s capital”. Journal of Islamic Accounting and Business Research, 12(7): 1036-1054. https://doi.org/10.1108/JIABR-11-2020-0345

[4] Sasongko, Y.A.T. (2021). Synergy between the Private and Government in Ensuring the Achievement of SDGs in the Midst of a Pandemic. https://nasional.kompas.com/read/2021/04/22/19390091/sinergi-swasta-dan-pemerintah-dalam-memastikan-pencapaian-.

[5] Biancone, P., Mohamed Radwan Ahmed Salem, M. (2019). Social finance and financing social enterprises: an Islamic finance prospective. European Journal of Islamic Finance, 1-7.

[6] Budiasa, I.W. (2020). Green financing for supporting sustainable agriculture in Indonesia. In IOP Conference Series: Earth and Environmental Science, 518(1): 012042. https://doi.org/10.1088/1755-1315/518/1/012042

[7] Ekonomi, W. (2018). BI: Sharia Economy is suitable for Sustainable Developement Indonesia. https://www.wartaekonomi.co.id/read199259/bi-ekonomi-syariah-cocok-untuk-pembangunan-berkelanjutan.html dated 19 June 2021.

[8] Republika.co.id. (2016). Sharia Finance solution for SDGs Target. https://www.republika.co.id/berita/koran/syariah-koran/16/10/12/oexlx62-keuangan-syariah-solusi-target-sdgs.

[9] Minister of Finance. (2017). Minister of Finance: Value of Islamic in line with SDG. https://www.kemenkeu.go.id/publikasi/berita/menkeu-nilai-nilai-islam-sejalan-dengan-sdg/.

[10] Arvian, Y. (2018). Sri Mulyani point that Sharia Capital Market Alternative for SDGs. https://bisnis.tempo.co/read/1076244/sri-mulyani-menilai-pasar-modal-syariah-alternatif-untuk-sdgs/full&view=ok.

[11] Gundogdu, A.S. (2018). An inquiry into Islamic finance from the perspective of sustainable development goals. European Journal of Sustainable Development, 7(4): 381-381.

[12] Gundogdu, A.S. (2018). An inquiry into islamic finance from the perspective of sustainable development goals. Eur. J. Sustain. Dev., 7(4): 381-390. https://doi.org/10.14207/ejsd.2018.v7n4p381

[13] Obaidullah, M. (2018). Managing climate change: The role of Islamic finance. IES Journal Article, 26(1): 31-62. https://doi.org/10.13140/RG.2.2.25535.51361

[14] Ismail, A.G., Shaikh, S.A. (2017). Role of Islamic economics and finance in sustainable development goals. IESTC Working Paper Series, 1(1). https://doi.org/10.13140/RG.2.2.14806.09288

[15] Mentari, N., Sutikno, F.M. (2019). Sustainable Development Goals (SDGs) Principle Towards Sharia Business Unit Pre-Spin Off 2023. UNIFIKASI: Jurnal Ilmu Hukum, 6(2): 199-208.

[16] Nugroho, L., Badawi, A., Hidayah, N. (2019). Discourses of sustainable finance implementation in Islamic bank (Cases studies in Bank Mandiri Syariah 2018). International Journal of Financial Research, 10(6): 108-117. https://doi.org/10.5430/ijfr.v10n6p108

[17] Nawaz, H., Abrar, M., Salman, A., Bukhari, S.M.H. (2019). Beyond finance: Impact of Islamic finance on economic growth in Pakistan. Economic Journal of Emerging Markets, 11(1): 8-18. https://doi.org/10.20885/ejem.vol11.iss1.art2

[18] Abduh, M. (2019). The role of Islamic social finance in achieving SDG number 2: end hunger, achieve food security and improved nutrition and promote sustainable agriculture. Al-Shajarah: Journal of the International Institute of Islamic Thought and Civilization (ISTAC).

[19] Saniff, S.M., Hasan, W.N.W., Salleh, M.S. (2020). Zakat and SDGs: A love story? PalArch's Journal of Archaeology of Egypt/Egyptology, 17(7): 10979-10988.

[20] Olaide, K.M., AbdulKareem, I.A. (2021). Islamic Financing as Mechanism for Socio-Economic Development: A Conceptual Approach. The Journal of Management Theory and Practice (JMTP), 94-98. https://doi.org/10.37231/jmtp.2021.2.1.96

[21] Trimulato, T., Syamsu, N., Octaviany, M. (2021). Sustainable Development Goals (SDGs) through productive financing of MSMEs in Islamic Banks. Islamic Review: Jurnal Riset dan Kajian Keislaman, 10(1): 19-38. https://doi.org/10.35878/islamicreview.v10i1.269

[22] Khan, T. (2019). Reforming Islamic finance for achieving sustainable development goals. Journal of King Abdulaziz University: Islamic Economics, 32(1): 3-21. https://doi.org/10.4197/Islec.32-1.1

[23] Saiti, B., Musito, M.H., Yucel, E. (2019). Islamic crowdfunding: Fundamentals, developments and challenges. Islam. Quartely, 62(3): 469-484.

[24] Azman, S.M.M.S., Ali, E.R.A.E. (2019). Islamic social finance and the imperative for social impact measurement. Al-Shajarah: Journal of the International Institute of Islamic Thought and Civilization (ISTAC), 43-68.

[25] Lawal, I.M., Imam, U.B. (2016). Islamic Finance; A Tool For Realizing Sustainable Development Goals (SDG) In Nigeria. International Journal of Innovative Research and Advanced Studies (IJIRAS), 3(9): 10-17.

[26] Putri, A.K., tir Razia, E., Muneeza, A. (2019). The potential of bai salam in islamic social finance to achieve united nations’ sustainable development goals. International Journal of Management and Applied Research, 6(3): 142-153. https://doi.org/10.18646/2056.63.19-010

[27] Mohamad, S., Borhan, N.A. (2017). Islamic finance and social sustainability: Parameters for developing a model for social impact measurement. Malaysian Journal of Sustainable Environment, 3(2): 81-103. https://doi.org/10.24191/myse.v3i2.5596

[28] Hudaefi, F.A., Saoqi, A.A.Y., Farchatunnisa, H., Junari, U.L. (2020). Zakat and SDG 6: A case study of BAZNAS, Indonesia. Journal of Islamic Monetary Economics and Finance, 6(4): 919-934. https://doi.org/10.21098/jimf.v6i4.1144

[29] Ghoniyah, N., Hartono, S. (2020). How Islamic and conventional bank in Indonesia contributing sustainable development goals achievement. Cogent Economics & Finance, 8(1): 1856458. https://doi.org/10.1080/23322039.2020.1856458

[30] Rashid, M., Ur, H., Uddin, M.J., Zobair, S.A.M. (2018). Islamic microfinance and sustainable development goals in Bangladesh. International Journal of Management and Business Research, 2(1): 67-80. https://doi.org/10.46281/ijibm.v2i1.53

[31] Shaikh, S.N., Ali, A. (2020). Islamic finance and empowerment of women: A Case study of Pakistan. Journal of Economics and Business, 16(4): 1-16. https://doi.org/10.9734/ajeba/2020/v16i430243

[32] Rifa'i, A., Ayu, P. (2019). Encouraging Islamic financing to achieve SDGs through poverty alleviation. Journal of Islamic Finance, 8(2): 10-20.

[33] Asmalia, S., Kasri, R.A., Ahsan, A. (2018). Exploring the potential of zakah for supporting realization of sustainable development goals (SDGs) in Indonesia. International Journal of Zakat, 3(4): 51-69. https://doi.org/10.37706/ijaz.v3i4.106

[34] Harahap, L.R. (2018). Zakat fund as the starting point of entrepreneurship in order to alleviate poverty (SDGs Issue). Global Review of Islamic Economics and Business, 6(1): 63-74. https://doi.org/10.14421/grieb.2018.061-05

[35] Alfiani, T., Akbar, N. (2020). Exploring strategies to enhance zakat role to support sustainable development goals (SDGs). In International Conference of Zakat, 295-310. https://doi.org/10.37706/iconz.2020.226

[36] Mauliyah, N.I. (2019). The role of sharia accountant for sustainable development goals (SDGs). Journal of Islamic Economics Perspectives, 1(1): 26-39. https://doi.org/10.35719/jiep.v1i1.4

[37] Hassan, M.K., Rabbani, M.R., Abdulla, Y. (2021). Socioeconomic Impact of COVID-19 in MENA region and the role of Islamic finance. International Journal of Islamic Economics and Finance (IJIEF), 4(1): 51-78. https://doi.org/10.18196/ijief.v4i1.10466

[38] Bananuka, J., Katamba, D., Nalukenge, I., Kabuye, F., Sendawula, K. (2020). Adoption of Islamic banking in a non-Islamic country: evidence from Uganda. Journal of Islamic Accounting and Business Research, 11(5): 989-1007. https://doi.org/10.1108/JIABR-08-2017-0119

[39] Priyono, S. (2019). Concept and implementation of good corporate governance in sharia banking in Indonesia. Jurnal Ekonomi dan Bisnis Islam, 3(2): 113-144. https://doi.org/10.30868/ad.v3i2.553

[40] Yurista, D.Y., Ayuningtyas, R.D. (2019). The role of macroeconomic variables on Islamic stocks for achieving SDGs in Indonesia. Jurnal Ekonomi dan Keuangan Islam, 5(2): 93-100. https://doi.org/10.20885/JEKI.vol5.iss2.art6

[41] Er, B., Mutlu, M. (2017). Financial inclusion and Islamic finance: A survey of Islamic financial literacy index. International Journal of Islamic Economics and Finance Studies, 3(2). https://doi.org/10.25272/j.2149-8407.2017.3.2.02

[42] Mani, A. (2008). The development of Islamic finance and banking in Singapore. Ritsumeikan Econ. Rev., 57(2): 349-363. http://id.ndl.go.jp/bib/9676800

[43] Mas’ad, M.A., Abd Wakil, N.A. (2020). Halal industry and Islamic finance institution’s role: Issues and challenges. INSLA E-Proceedings, 3(1): 643-659.

[44] Iskandar, A., Possumah, B.T., Aqbar, K. (2020). Islamic financial development, economic growth and CO2 emissions in Indonesia. Journal of Islamic Monetary Economics and Finance, 6(2): 353-372. https://doi.org/10.21098/jimf.v6i2.1159

[45] Julia, T., Noor, A.M., Kassim, S. (2020). Islamic social finance and green finance to achieve SDGs through minimizing post harvesting losses in Bangladesh. Journal of Islamic Finance, 9(2): 119-128.

[46] Uddin, M.N., Kassim, S., Hamdan, H., Saad, N.B.M., Embi, N.A.C. (2021). Green microfinance promoting sustainable development goals (SDGs) in Bangladesh. Journal of Islamic Finance, 10: 011-018.

[47] Ilić, B., Stojanovic, D., Pavicevic, N. (2018). Green financing for environmental protection and sustainable economic growth–a comparison of Indonesia and Serbia. Progress in Economic Sciences, 5(5): 181-200. https://doi.org/10.14595/PES/05/012

[48] Uddin, M.N., Ahmmed, M. (2018). Islamic banking and green banking for sustainable development: Evidence from Bangladesh. Al-Iqtishad Journal of Islamic Economics, 10(1): 97-114. htttp://dx.doi.org/10.15408/aiq.v10i1.4563

[49] Awawdeh, A.E., Ananzeh, M., El-khateeb, A.I., Aljumah, A. (2021). Role of green financing and corporate social responsibility (CSR) in technological innovation and corporate environmental performance: A COVID-19 perspective. China Finance Review International, 12(2): 297-316. https://doi.org/10.1108/CFRI-03-2021-0048

[50] Taghizadeh-Hesary, F., Yoshino, N. (2020). Sustainable solutions for green financing and investment in renewable energy projects. Energies, 13(4): 788. https://doi.org/10.3390/en13040788

[51] Li, M. (2019). Framework of China and Europe green financing for sustainable development. International Relations, 7(1): 37-47. https://doi.org/10.17265/2328-2134/2019.01.004

[52] Lanzara, F. (2021). Islamic Finance as Social Finance: A Bibliometric Analysis from 2000 to 2021. International Journal of Business and Management, 16(9). https://doi.org/10.5539/ijbm.v16n9p107

[53] Johan, S. (2021). Knowing company secrets through employee posts on social media. Diponegoro Law Review, 6(2): 203-216. https://doi.org/10.14710/dilrev.6.2.2021.203-216

[54] Hariyanto, E. (2018). Green Financing, Sharia and Sustainable Development. https://www.djppr.kemenkeu.go.id/page/load/2269.

[55] Erawati, D. (2018). A green banking for sustainable development in sharia banking. In Annual Conference on Social Sciences and Humanities (ANCOSH 2018) - Revitalization of Local Wisdom in Global and Competitive Era, pp. 82-86.