W Muhammad Zainuddin B Wan Abdullah* | Wan Nur Rahini Aznie Bt Zainudin | Sarina Binti Ismail | Norhaziah Nawai | Hafiz Muhammad Zia-ul-haq

© 2022 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Households’ socio-economic outcomes are considered a significant component of sustainable development. In this regard, public and private organizations are constantly devising several microfinance and development strategies to tackle economic deprivation. There exists a conflict in the literature regarding the role of such a strategy in enhancing households’ socio-economic outcomes. In addition, researchers are also struggling to identify crucial factors that could improve poor households’ socio-economic performance. However, the lack of established measuring instruments for various microfinance and households’ socio-economic factors is the major hurdle in conducting quality research. Hence, this study intends to develop and validate measurements for microfinance and households’ socio-economic model. By employing an Exploratory Factor Analysis (EFA) and Parallel Analysis as factor retention techniques, this research provides measuring constructs for microfinance financial services, business coaching, training programs, microfinance institutions’ efficiency, households’ entrepreneurial competencies, households’ financial management practices, and households’ socio-economic performance. Based on the results, it is proved that the developed instrument of the microfinance and households’ economic model is valid and reliable to be used in future related research.

microfinance, financial management, entrepreneurial competencies, household socioeconomic performance

Poverty has remained a longstanding issue in the developing world. Globally, approximately 9.4% of the world's total population is suffering from extreme poverty, earning less than $1.9 per day [1]. Recently, world leadership has initiated an international agenda for sustainable development to tackle poverty, economic inequality, and environmental adversities [2]. Increasing levels of population and unemployment in developing countries are causing disruptions in household well-being. Therefore, developing countries prioritize alleviating poverty and enhancing household well-being [3]. Consecutive events of socio-economic crises such as the global financial crisis of 2008 and, recently, the COVID-19 pandemic have elevated poverty rates and economic deprivation, thus, severely affecting millions of households across the globe. According to World Bank report [1], COVID-19 is expected to push an additional approximately 115 million people into the circle of extreme poverty by the end of the year 2021.

Malaysia is one of the emerging developing nations that has been experiencing rapid socio-economic transition over many years [4]. It has achieved remarkable socio-economic development goals and economic growth in the last few decades. In essence, such economic growth and socio-economic development have brought significant improvements in poverty eradication and Malaysia's quality of human life. However, poverty and economic deprivation remain major socio-economic problems [3]. Notably, certain pockets, such as urban slums and remote rural areas, still suffer from severe poverty [5]. In addition, the urban and middle-income population is also suffering from economic deprivation because of the high cost of living. However, the low-income group is the one who is severely being affected by poverty [4]. This population group is generally referred to as the Bottom forty percent of the Malaysian household income (B40), consisting of approximately 2.91 million households with a monthly income threshold of less than RM4849 [6]. According to Household Income and Basic Amenities Survey Report for year 2019 and Household Income Estimates and Incidence of Poverty Report for year 2020 [6, 7], total B40 income had decreased from 16.4% of total revenue in 2016 to 16% of total income in 2019 and then further to 15.9% in 2020 after the spread of COVID-19 pandemic [6, 7]. Due to this, most B40 households are bound to spend unsatisfactory lives with a poor quality because of the rising cost of living and decreasing income level. Hence, authorities are strongly required to make aggressive efforts to help and uplift B40 households in escaping from the vicious cycle of poverty and economic vulnerability.

Households’ socioeconomic performance reflects their ability to meet essential life needs and survive during adverse economic situations. Therefore, household economic vulnerability and well-being have become a great concern for the authorities after the spread of the COVID-19 pandemic. Therefore, researchers and authorities have been continuously exploring effective solutions to help households enhance their socioeconomic outcomes. Malaysia has made aggressive efforts to achieve the status of a developed nation. However, concerns need to be resolved, such as poverty and income inequality [5]. Recently, the Department of Statistics Malaysia released a report on household income estimates and incidence of poverty analyzing the impact of COVID-19. This report reveals that absolute poverty in Malaysia has increased from 5.6% in 2019 to 8.4% in 2020. Meanwhile, extreme poverty had also increased from 0.4% in 2019 to 1.0% in 2020. Based on this report, approximately 640 thousand households are suffering from poverty in Malaysia [7]. In this regard, the government of Malaysia has initiated its twelfth Malaysia plan to set the way forward and recover the Malaysian economy [8].

One of the twelfth Malaysia plan [8] is devoted to provide financial facilities to Small and Medium Enterprises (SMEs) in catering their financing needs across a growth cycle. This would lead to adequate alternative financing to complement the traditional banking system in outreaching low-income consumers. Alternative financing would ultimately play a crucial role in creating opportunities for microbusinesses through efficient savings mobilization into high potential economic activities. Likewise, the twelfth plan of Malaysia also addresses socioeconomic deprivation and inequality by improving the income and wellbeing of the poor. On this matter, authorities intend to promote various socioeconomic interventions such as microfinancing and entrepreneurial training to strengthen home-based microbusinesses. Meanwhile, community-based economic activities like urban farming and childcare services would be promoted to help the poor generate extra income. Poverty eradication initiatives under the twelfth Malaysia Plan mainly target uplift extreme poor groups such as Orang Asli to become micro-entrepreneurs and improve their socioeconomic status. Similarly, the New Economic Model (NEM) developed by the government of Malaysia also focuses on a new approach towards development by enhancing the income level of the poor population. Likewise, the financial inclusion agenda was also designed to strengthen socioeconomic outcomes and improve quality of life [9]. These plans set the future direction of the Malaysian economic and financial system as it prepares to recover its socioeconomic conditions to become a high-income economy. The goal is to promote financial inclusion that will help all citizens undertake financial services and prepare themselves against future financial risks.

Microfinance, as an effective tool to tackle poverty, also serves a similar notion to uplift poor clients by extending various financial facilities that ultimately help poor individuals achieve better socioeconomic outcomes. The provision of microfinance services allows households to participate in entrepreneurial and other economic activities, which subsequently help them increase their income level [4]. Microfinance is also adopted in Malaysia as a key strategy to help low-income households increase their income and improve their quality of life. Microfinance generally provides various financial services (FS) that play a crucial role in the well-being of poor households [10]. The famous ones would be microcredit, micro-insurance, and micro-savings. Microcredit is considered an effective financial service that involves providing small loans to poor individuals for smoothening their consumption and enhancing income levels [11]. By utilizing microcredit, poor households can better avail profitable opportunities [4]. The literature strongly believes that economic deprivation and income inequality can be resolved through effective microcredit schemes [12]. Similarly, micro-saving is another critical financial service that is also considered crucial for poor individuals. It strengthens the capability to secure viable financial capital, thus enabling individuals to deal with future adverse events. Maintaining saving accounts also helps microfinance clients avail large-size loans with flexible repayments that assist them in conducting various income-generating activities [11]. Thus, micro-savings service is considered significant for wealth accumulation, a crucial element in socioeconomic development. This is the reason poor households are always advised to maintain savings to prepare themselves against adverse situations. In addition to these, death-benefit fund as a micro-insurance service is also offered to the poor individuals that provide financial security against future unforeseen events such as natural disasters, accidents, and economic losses [13].

The Malaysian government established various microfinance organizations intending to alleviate poverty and enhance poor households’ well-being. One of them is Amanah Ikhtiar Malaysia (AIM), the primary development organization in Malaysia that provides various financial and non-financial services to poor households and facilitates them in developing microbusinesses. AIM as the largest microfinance institution offering services to approximately 80% of poor households in Malaysia [9]. Apart from financial services, AIM has also started to offer various non-financial services to the poor population of Malaysia, such as trainings and business coaching [5].

The microfinance training programs (TP) are considered as primary non-financial services targeting clients' human capital development [3]. With the lack of specific capabilities and financial awareness, poor households cannot effectively manage their financial capital and microbusinesses [14]. Microfinance training generally targets the development of such capabilities that are considered crucial for improving the socio-economic conditions of poor households [3]. Likewise, business coaching (BC) has recently emerged as an essential non-financial service AIM offers to poor households in Malaysia. It refers to the collaboration between clients and coaches, where coaches attempt to help clients develop effective strategies to achieve better socio-economic outcomes [15].

1.1 Research gap

Although the impact assessment of microfinance has received significant attention from the researchers, there is a lack of consensus in the existing literature regarding its successful influence on households’ socio-economic outcomes and poverty alleviation. Despite literatures indicating the positive impact of microfinance, researchers have raised concerns on the diversity of empirical results that range from no impact, negative, to positive [16]. Some studies state that microfinance drags the poor into indebtedness and vulnerability instead of achieving its prime goal of helping them against poverty [17]. In contrast, many studies have found the positive influence of microfinance on households’ economic well-being and women empowerment [10, 11]. Thus, there is a lack of specific evidence on the relationship of microfinance with poverty and households’ socio-economic performance [16].

Similarly, there is a gap in the existing literature on how microfinance services empower households to achieve socioeconomic success [18]. Most of the current literature [10, 19] has mainly focused on impact assessment, thus, ignoring the underlying mechanisms that can clarify the pathway towards improved socioeconomic performance. Existing studies have overlooked identifying factors that could help enhance the impact of microfinance schemes in eradicating poverty and enhancing households' socioeconomic outcomes. Hence, there is a strong need to explore the empowering capabilities developed by microfinance to improve poor households' entrepreneurial performance and well-being. Moreover, the microfinance literatures have ignored the role of microfinance institutions' service efficiency (MIE) in the context of services effectiveness to socioeconomic development [20]. Most of the existing studies have only focused on technical efficiency measurements [21], thus, leaving a gap in the literature regarding the service delivery measurement and its role in the microfinance mechanism. Further, there is also a lack of established constructs for microfinance research [22]. Most of the literature has used diverse objective and subjective measures for microfinance impact assessment. For instance, some studies [3, 15] have used objective measures such as length of participation in microfinance, amount of loan, and training hours as proxies for the microfinance services. On the other hand, some researchers [19, 23] have also used diverse subjective scales to measure microfinance factors in Malaysia. A reliable and valid measuring instrument is always considered a crucial element in achieving accurate and unbiased results. Hence, there is a strong need to develop a reliable and valid research instrument to measure various essential factors involved in microfinance interventions and household socioeconomic mechanisms.

1.2 Aim and contribution of the research

Therefore, this research develops a research instrument and undertakes parallel and exploratory factor analysis (EFA) techniques to explore potential factors that have some relevance in the success of microfinance programs. The research also uncovers various potential financial and non-financial microfinance services offered by AIM and households’ socioeconomic factors in influencing household socioeconomic wellbeing and entrepreneurial success. Microfinance interventions such as financial services (FS), training programs (TP), and business coaching (BC) are the main explanatory variables. At the same time, households’ social wellbeing (SW), economic wellbeing (EW), and entrepreneurial success (ES) constitute outcome variables of the model. In addition, the model includes household entrepreneurial competencies (EC) and financial management practices (FMP) as the mediating mechanism that can explain the relationship pathway of microfinance towards the improving socioeconomic performance of households. Further, the MIE is selected as a potential moderator to enhance the impact of microfinance on household socioeconomic outcomes. Instrument validation is considered an essential element to ensure the quality of exploratory research. Hence, this study also intends to examine the validity and reliability of the developed instruments for the factors associated with the household socioeconomic mechanism.

This research provides multiple valuable contributions to the existing body of knowledge. Mainly, it provides a valid and reliable research instrument that can be used in future research involving microfinance and household socioeconomic factors. Previous studies [3, 10] have mainly used microfinance financial and training services as independent factors. In this regard, our research included a new microfinance factor i.e. BC, along with FS and TP, in the explanatory set of variables. Similarly, this research has also incorporated household FMP as a new mediating factor along with previously used EC in the context of the microfinance model [24]. Next, the novelty of this research also lies in introducing another vital factor MIE as a potential moderator in the relationship of microfinance services with households’ socioeconomic outcomes. Considering the dual objective of microfinance institutions, they have to be more efficient in delivering services for the betterment of their clients [25]. Therefore, MIE is expected to play a crucial role in helping households achieve their social and financial goals. At last, considering multidimensional aspects of a household, it is essential to incorporate multiple elements of the socioeconomic performance. Hence, this research has included three primary household outcomes, SW, EW, and ES separately in the model to understand better and compare the socioeconomic impacts of microfinance interventions. Overall, this research implies that microfinance services assist households in developing effective human capabilities such as financial management practices and entrepreneurial competencies. In turn, these capabilities help households efficiently manage their financial and business operations, thus, enhancing their socioeconomic performance.

This paper is organized in the following order. The second section provides a detailed discussion on materials and methods whereas the third section presents this study's results. In the subsequent sections, the paper presents discussion on the results and conclusions.

This study has followed a comprehensive methodology to develop and validate instrument for microfinance and household socioeconomic model. A complete stepwise explanation for questionnaire development is discussed based on methodology presented in Figure 1 below.

Figure 1. Methods diagram

2.1 First stage: Questionnaire development

The first stage of questionnaire development is referred to identification of theoretical support and essential factors to establish a conceptual model of this study. The ultimate purpose was to explore all related variables and develop their measuring items. Hence, an extensive literature review and discussion with team members were conducted to identify related theoretical foundation and crucial factors improving households’ socioeconomic performance.

2.1.1 Theoretical foundation

The Household Economic Portfolio (HEP) Model developed by Chen and Dunn [26] was found to be the most widely accepted theoretical work in the literature of microfinance impact assessment. Hence, this study has used the theoretical model of HEP as foundation to develop its framework. The HEP model discourses the question that how micro-financial interventions impact various households’ outcomes. According to the HEP model, a household’s economic mechanism consists of economic resources, set of economic activities, and interconnection between them. The HEP model theorizes that financial interventions directly contribute to the set of households’ economic resources which further influence socioeconomic outcomes through set of certain economic activities.

The HEP model proposes that financial and social are the two major external factors that contribute to the households’ resources and indirectly influence their socioeconomic outcomes through certain actions such as investment, production, and consumption activities. In the HEP framework, financial capital is considered as major input factor that can help households to enhance their socioeconomic performance [20]. Mainly, allocation of financial capital to different economic activities is influenced by various factors such as decision-making structure, preferences, opportunities, and constraints [27]. Likewise, allocation of financial capital has significant consequences for the effectiveness of financial interventions in achieving improved socioeconomic outcomes. For example, allocating funds to investing and production activities can boost economic performance, whereas spending more on consumption activities does not provide similar outcomes.

In this regard, the HEP model considers allocation of financial capital towards different economic activities as a crucial phenomenon in improving socioeconomic performance. This indicates the importance of decision-making process that is determined by several individual and household specific attributes in enhancing socioeconomic outcomes. Likewise, the HEP model also highlights the importance of external market factors in improving the success of microfinance interventions. However, the HEP model has a limitation as it does not provide sufficient detail on such factors that might shape households’ decision-making and influence their socioeconomic outcomes. In this regard, the current study has introduced human capital factors in the HEP model to explore their role in enhancing the effectiveness of microfinance interventions. In addition, this study also contributes to the HEP model by introducing microfinance institutions’ service efficiency as institutional factor in the household economic framework.

2.1.2 Developing theoretical and conceptual framework

Following the theoretical literature, the theoretical (initial) structure of the framework was obtained which consisted of (1) microfinancing as independent variable with two dimensions that were financial literacy (financial services, financial management, and social capital) and entrepreneurship (entrepreneurial competencies and entrepreneurial environment), (2) Institutional factors as moderation with two variables of microfinance’ efficiency and government support policy, and (3) household socioeconomic well-being as dependent variable with two dimensions that are social well-being and economic well-being (refer Figure 2).

Figure 2. Theoretical framework (Initial)

Next, an extensive discussion was conducted with industry players to gain more details and confirmation on research areas (variables). Hence, revisions were made to develop the final conceptual framework. Mainly, two new independent variables were included, such as TP and BC. Similarly, FMP and EC were reclassified as mediation variables whereas variables of social capital, entrepreneurial environment, and government support policy were dropped from the model. At the same time, ES was also added to the existing dependent variables. Thus, new research areas of Quality Educational Provision framework presented in Figure 3 were completely endorsed by the experts. The final developed model includes three main microfinance services such as FS, TP, and BC as independent variables. Next, two human capital factors which are FMP and EC are incorporated as mediation variables to explore the impact pathway of microfinancing towards improved socioeconomic outcomes. Then, considering the importance of service delivery, MIE is considered as moderation variable that might play vital role in enhancing the effectiveness of microfinance. At last, household socio-economic performance is included as dependent variable with three dimensions, that are SW, EW, and ES (refer Figure 3). Overall, this study implies that microfinance financial and non-financial services help clients to develop their capabilities such as entrepreneurial and financial management skills. These capabilities ultimately assist them to make effective decisions in selecting and managing their economic activities, thus, resulting in improved socioeconomic outcomes. The list of these variables and their respective dimensions are presented in Table 1.

Figure 3. Conceptual framework of quality educational provision

2.1.3 Items development

This study developed questionnaire items in four steps. First, measuring items were acquired from the literature for all identified variables. Then, industry experts were consulted to ensure relevancy of the items (statements) and specific dimensions of the framework. Next, statistical methods were applied to examine validity of the constructs. At last, all developed items were cross-checked against their concepts and objectives of this study.

In this regard, a questionnaire used as instrument was initially designed by acquiring all the items (statements) for each dimension from the initial framework. The process of adoption (i.e. retain original items) and adaption (i.e. change the actual items) approaches from literature were used to create all the items. At the initial stage, this study developed a total of two hundred six items from various existing studies and authors’ discussions. In terms of the principle of wording, several principles had been considered such as no double barrel, no ambiguous statement, no bias (race or group), and appropriate length of the questionnaire (ideal answering time). Likewise, the criteria of minimum three items for each dimension was also followed in developing items.

Then, after extensive discussion with industry representatives, this study developed final framework and concepts presented in the Figure 3. Consequently, 110 items were deleted from 206 of the original items, and then 30 new items were added; hence, leaving a total of 126 items in the questionnaire. Then, various statistical tests were employed to assess quality and authenticity of the measurements. These data analysis steps are discussed in the next section. After conducting statistical methodology, final 125 items are validated in this study. The detail of these items is discussed below whereas actual items are listed in the Table 4 of the results section.

The first independent variable of the study i.e. FS was measured using three main financial services of five items each. These services include microcredit, micro-savings, and death-benefit fund. The measuring items were adapted from the existing literature [22]. Then, second independent variable i.e. TP was measured on the basis of basic training as its major dimension. Total 5 items were developed and designed following the industry inputs and program features. Similarly, third independent variable i.e. BC was captured on the basis of two classifications; service coaching and product development coaching. It was measured using a total of 10 items developed from the industry input.

Next, first mediating variable of FMP was measured using five major financial management practices found in the literature including basic finance, budgeting and cash management, credit management, risk management, and capital accumulation. These practices were measured by adapting 27 items from the various existing studies [28-32]. Likewise, next mediating variable of the model i.e. EC was measured using six dimensions given by Man et al. [33]. These include commitment competency, conceptual competency, organizing competency, relationship competency, opportunity recognition competency, and strategic competency. Total 33 items were adapted following the previous literature [33] to measure EC.

Table 1. Variable description

|

Variable |

Dimension |

Number of Items |

|

Financial Services (FS) |

Microcredit (MC); Micro-savings (MS); and Death benefit Fund (DF) |

15 |

|

Training Programs (TP) |

Basic Entrepreneurship Training (BE) |

5 |

|

Business Coaching (BC) |

Service coaching (SC); and Product Development Coaching (PC) |

10 |

|

Financial Management Practices (FMP) |

Basic Finance (BF); Budgeting and Cash Management (BCM); Credit Management (CM); Risk Management (RM); and Opportunity Awareness (OA) |

27 |

|

Entrepreneurial Competencies (EC) |

Commitment Competency (CMC); Conceptual Competency (CC); Organizing Competency (OC); Opportunity Recognition Competency (ORC); Relationship Competency (RC); and Strategic Competency (SC) |

33 |

|

Microfinance Institutions’ Efficiency (MIE) |

Credibilty (CR); and Responsiveness (RS) |

14 |

|

Households’ Social Wellbeing (SW) |

Level of Satisfaction (LS); and Provision of Opportunities (PO) |

10 |

|

Households’ Economic Wellbeing (EW) |

Econoomic Performance (EP) |

5 |

|

Households’ Entrepreneurial Success (ES) |

Business success (BS) |

7 |

|

Total Items |

126 |

|

Then, this study measured its moderating variable i.e. MIE, using two main dimensions of credibility, and responsiveness. Total 14 items were developed by adapting from the study of [25]. Further, dependent variable of the study that is household socioeconomic performance was classified into three major dimensions including SW, EW, and ES. Specifically, EW was measured by developing 5 items of different household economic performance outcomes such as income level, asset possession, expenditures, savings, and confidence. The SW was measured using two social development dimensions; level of satisfaction and provision of opportunities. Following the existing literature [34], 7 items were adapted to measure satisfaction level in meeting basic needs, and 3 items were used to measure provision of opportunities. Finally, ES was measured using 7 items of business performance developed and adapted from the previous literature and industry input [22].

2.2 Second stage: Questionnaire testing (data analysis)

In the second stage, this research conducted a detailed data analysis to test questionnaire’s reliability and validity. First, reliability of the data was assessed for all the measuring constructs. At the same time, validity of the constructs was also examined. For this, factor analysis and parallel analysis techniques were applied to extract the significant number of factors and explore underlying patterns of the variables. Lastly, reliability of the developed scale was again assessed in this stage. A detail of various steps conducted at this stage is given below.

2.2.1 Content validity

The initial process in the second stage began with content validation assessment when a group of experts from industry and academic was sought to assess the instruments. Based on the assessment, the content validity index (CVI index) has been calculated using a 4-point ordinal rating scale ranging from irrelevant to very relevant (1= Irrelevant, 2 = Not Important, 3 = Relevant with correction, and 4 = Very relevant). The scales of one and two represent disagreement, while scales of three and four represent agreement. All 126 items received a score above 96%, indicating congruence between the six reviewers. Hence, no items were deleted, while items revision was conducted to alleviate inaccurately and out-of-context sentences.

2.2.2 Pretesting

Under the pretesting step, the subsequent version of the questionnaire was pretested on six respondents of AIM clients (sahabat) from different districts of Negeri Terengganu Malaysia. From the respondents' feedback, the questionnaires are reorganized as follows: Part A consists of Demographic information, and Part B consists of structured and semi-structured questionnaires. Since no item being deleted in the pretesting step, 126 items were maintained. In this step, any comments and suggestions were obtained to ensure the clarity, relevancy, an understanding of the statement, vague sentences, and answering time of the questionnaire.

2.2.3 Construct reliability and validity (pilot study)

Examining construct validity is a crucial step in the process of scale development. It refers to the extent to which measuring constructs represent their respective theoretical concepts [35]. Hence, this study conducted factor and parallel analyses techniques to examine construct validity. A survey method was used as it is considered more appropriate to collect large amounts of quantitative data.

Respondents and sample size: The target population is comprised of all B40 households receiving microfinance services offered by AIM in Malaysia. Regarding the sample, AIM clients (sahabat) were chosen as respondents from all Malaysian states to ensure that results represent the population. The convenience sampling approach was adopted to collect the data. Determining sample size is one of the important steps while conducting an empirical study. Usually, the sample size is determined based on the minimum sample required to achieve reliable results. Particularly, the problem of sample size is more crucial in case of factor analysis because it involves greater level of subjectivity [36].

This study determined its sample size following the stable factor structure (SFS) recommendations. The SFS recommends sample size based on two crucial aspects that are mathematical overdetermination and size of communalities. In order to reduce standard errors of correlations, SFS suggests a sample size of at least 100 to 200 and respondent variable ratio of 2 to 1 [37, 38]. Hence, a total of 200 respondents were selected using a convenient sampling method. Data were collected from respondents through telephone calls because of COVID-19 related restrictions. All data were collected anonymously, and all confidentiality and privacy were maintained. In addition, this study also conducted a manual filtering and screening to remove any inappropriate questionnaire scripts from the collected data. The next step is performing the data analysis.

Reliability analysis: Before performing factor analysis, this study examined the reliability of the data. For this, four commonly used criteria are followed to ensure the reliability of the data. These criteria include testing standard deviation (SD), inter-item correlations, corrected items total correlations, and internal consistency using Cronbach alpha. Hence, the reliability of data is ensured as per the following conditions:

Factor analysis: This research employed the factor analysis method, an important statistical technique wisely adopted for scale development. This method has three primary uses. First, it is employed to reduce a large set of variables into a small number of factors. Next, it facilitates the formation of the model by determining underlying associations between latent variables and their measurements. At last, it also examines the validity of the scale. As the purpose of this study is to develop scale and model; therefore, it applies an exploratory method of factor analysis.

This research has conducted exploratory factor analysis (EFA) for developing a questionnaire to explore underlying patterns of variables. This EFA test also was conducted to reduce larger data set into smaller sets of variables and to discover underlying theoretical structures. Three comprehensive steps involved: factor suitability, factor extraction, and rotation.

First step, factor suitability test was conducted. Existing literatures indicate that most researchers ignored assessing factor suitability before conducting factor analysis [39]. However, testing factor suitability is crucial as it confirms that factor analysis should be applied to the data. Therefore, this study examined factor suitability by conducting Kaiser-Meyer-Olkin (KMO) test [40] and Bartlett’s test [41]. The threshold values for these tests are as follow; KMO value should be greater than or equal to 0.6, and Bartlett test’s probability value should be significant at 0.05 or less [2].

Second step, factor extraction was conducted. For this purpose, Principle Component Analysis (PCA) was conducted, which is the most widely adopted method. Most existing studies suggest using multiple criteria for determining and retaining a total number of factors [42]. Most commonly used methods include Kaiser’s eigenvalue criteria [43] and Cattell’s scree test [44]. It is observed that both methods are being widely adopted in the research because of their simplicity and easiness. However, both methods have been criticized because of certain serious deficiencies in their performance [42]. On the other hand, Horn’s Parallel Analysis (PA) [45] has been developed to overcome these deficiencies. PA involves a complex procedure; therefore, it has less popularity among researchers. However, PA is considered the most appropriate method for determining total number of factors [42]. In this study, a modification of Horn's parallel analysis based on Monte Carlo simulation is used to improve the analysis further and accuracy of the results.

Hence, for factor extraction, this study has applied all three methods, i.e. Kaiser’s eigenvalue criteria, Cattell’s scree test, and Horn’s parallel analysis, to determine a total number of factors to be retained. For Kaiser’ Criterion, best fitted line was determined on the basis of largest sum squared of distance (SSD). Then, Singular Value Decomposition (SVD) method was used to scale the line into one unit. Hence, this transformation (new results with same proportion) is termed loading proportion (eigenvector). These eigenvectors can be viewed as weights of the variables. The highest eigenvalue related with each eigenvector shows substantive importance for each variable or component. Under Kaiser Criterion, the basic rule is to retain factors with eigenvalue of greater than 1 and ignore factors with eigenvalue less than 1 [43].

Next, this study also incorporated Scree test to determine and retain total number of factors. The Scree test proposed by Cattell is a well-known factor retention method which refers to the visual examination of eigenvalues. In this method, eigenvalues are graphically represented in the descending order where breakpoint is used to determine retaining factors. The rationale behind this test is that breakpoint on the graph separates the trivial factors from non-trivial factors [44]. It indicates that the steep part of the graph before the breakpoint shows major factors which account for the most of variance whereas after breakpoint represent those minor factors which relatively account for smaller variance.

Under Scree Plot test, this study reconfirmed the results from Kaiser’s criterion by plotting eigenvalues on y-axis and their respective components on x-axis. For illustration purpose, an example of Scree plot is shown in Figure 4 [44]. Hence, the number of components and variables are determined based on points that appear to be on the left side of inflection (also called as elbow); however, the inflection point itself is not to be considered. In the given illustration, two points i.e. 1 and 2 can be considered for selection.

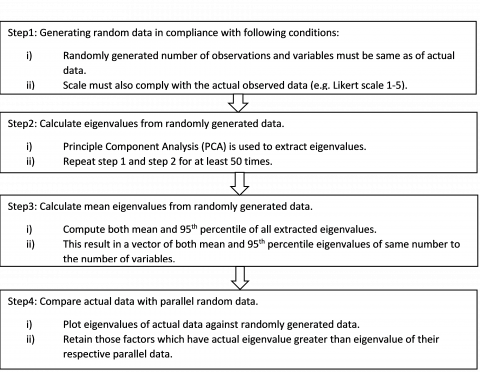

While Horn’s Parallel Analysis (PA) [45] was performed on all items to double check results from Kaiser’s criterion and scree plot by producing more accurate and reliable factors. Literature suggests that Horn’s parallel analysis is a sample-based method that provides superior results to other widely used techniques such as eigenvalue criteria and scree test [42]. This study has developed a simple approach, adapting from the previous literature to conduct PA using SPSS [46]. PA is undertaken in four simple steps shown in Figure 5 below. In the first step, this study has generated random data of the same number of variables and sample size as the actual observed data. And this is to comply with the condition that a random dataset must have a similar number of variables and observations. In the next step, principle component analysis was performed on the randomly generated data to compute eigenvalues.

Figure 4. Scree plot (developed based on Field, 2013) [38]

Figure 5. Steps to conduct parallel analysis (Monte Carlo Simulation)

Further, Horn [45] suggests that the number of random data matrices must be of sufficient size to avoid biasness. Hence, following the existing literature, both the first step and second step were repeated fifty times to collect adequate observations. Then, in the next step, mean eigenvalues and 95th percentile eigenvalues of fifty random data sets were computed with average eigenvalue and 95th percentile value for each factor. In the last step, eigenvalues of actual observed data were compared with these computed mean eigenvalues and 95th percentile eigenvalue of randomly generated data. For instance, the first real eigenvalue is compared with the first mean eigenvalue from random data, and then the second real eigenvalue is compared with the second mean eigenvalue. However, this comparison could be easily performed by comparing scree plots. Under this method, a factor is selected if its eigenvalue of actual data is greater than the mean eigenvalue and 95th percentile eigenvalue of randomly generated parallel data. Moreover, the number of factors to be considered also relies on the basic objective of the analysis.

Third step is factor rotation. The Direct Oblimin method is incorporated for producing correlated factors. This study retained factors/items on the basis of factor loadings from this process. Hence, authors retained factor/items with factor loading of 0.3 and above whereas redundant items between the components (cross loading) were deleted. Under Direct Oblimin method, two tables have been conferred, i.e. Pattern Matrix and Component Matrix (Factor Transformation Matrix Table and Varimax/Orthogonal – Rotated Factor Matrix Table). A detailed assessment of both tables was performed to select components and items.

At this stage, the following procedures were used to do factor rotation and to complete the EFA process in this study:

After the required validity is achieved for all the factors and components, this study conducted final test, i.e. to determine reliability of the developed scale. Reliability testing was performed to examine the consistency between items/attributes [47]. The purpose behind this test is to ensure reliability of indicators for measuring their respective latent variables. Specifically, Cronbach’s Alpha values were used to assess reliability of the factors.

2.3 Third stage: Questionnaire cross checking

The last stage in the process of instrument development refers to the verification of the results. Particularly, final factors are cross-examined at this stage to confirm their accuracy and efficiency. Hence, after proving validity and reliability of the constructs through statistical analysis, this study also conducted questionnaire cross checking in the final stage to ensure further accuracy for the final data collection. Questionnaire items cross checking is a crucial step to avoid mistakes and achieve accuracy in the results. In this regard, all final retained items of the instrument were cross checked against their specific theoretical concepts and research areas identified by the experts. The purpose is to prove that the variables sufficiently reflect their conceptual meanings. It would indicate that all the developed constructs and their items incorporate their respective research areas of the specific variables. This study identified four main research areas including; 1) microfinance effectiveness, 2) human capital development, 3) service efficiency, and 4) sustainable socioeconomic development. Remaining 125 items covering eight measuring constructs were cross-examined by the researchers against these specific research areas.

For instance, FS was cross-checked against facilitating clients by providing specific financial benefits. The strength of non-financial services such as TP and BC is determined on the basis of ability to enhance human capabilities of their clients. All together both financial and non-financial services mainly address effectiveness of microfinance interventions. Whereas, non-financial services also play a vital role in addressing human capital development. Likewise, the mediating variables such as FMP and EC have strength in providing benefits to the micro-entrepreneurs in form of their improved capabilities. As adoption of FMP and improved EC can help clients to efficiently manage their economic matters. Thus, these both constructs measure human capabilities which further contribute in enhancing households’ socioeconomic outcomes. Furthermore, the items of MIE were cross-examined with their ability to capture the fact that how efficiently microfinance institutions are providing their services to the clients. Hence, it specifically addresses efficiency of microfinance service providers and play vital role in the effectiveness microfinance to achieve sustainable socioeconomic development. At last, items of households’ socioeconomic performance indicators (SW, EW, and ES) address a broader research area of sustainable socioeconomic development covering households’ social status and economic performance. In addition, all steps of instrument development and validation were also revisited to confirm accuracy of the results. Hence, after this stage, final validated and reliable instrument for the specific variables are reported in this study.

3.1 Reliability tests before EFA

This study has conducted reliability testing to determine the reliability of indicators for measuring related latent variables. Specifically, internal consistency among various items of the specific constructs is assessed at this stage. Different steps have been performed to assess reliability: i) testing standard deviation (SD), ii) inter-item correlations, iii) corrected items total correlations, and iv) internal consistency using Cronbach alpha. The results confirmed that standard deviation values for all items are greater than zero (S.D > 0); all inter items correlations are between 0.3 to 0.9, and corrected items total correlations are greater than 0.3. All results support the reliability of the items. Similarly, results reported in Table 2 also reveal that all Cronbach alpha values are greater than 0.7, which proves the reliability of the items.

3.2 Exploratory factor analysis (EFA)

The EFA is mainly performed for the scale development to decide whether the group of questions precisely measure their respective variables or, in other words, which variable is measured by which group of items. Results for the various steps of EFA are reported in Table 2 and Table 3. In the following section, results from the various EFA processes are being explained in detail.

Table 2. Summary of reliability test and EFA results

|

Construct |

Dimension |

Reliability Results before Factor Analysis |

Factor Suitability |

Factor Extraction |

|||||

|

Number of items |

Cronbach Alpha |

Bartlet Test (p<0.05) |

Kaiser- Mayer- Olkin (KMO> 0.6) |

Eigenvalues |

Variance Explained (%) |

Scree Plot |

|||

|

FS |

MC |

5 |

0.930 |

.000 |

0.897 |

Factor 1 |

3.919 |

78.371 |

One Factors |

|

MS |

5 |

0.925 |

.000 |

0.900 |

Factor 1 |

3.854 |

77.075 |

One Factor |

|

|

DS |

5 |

0.943 |

.000 |

0.912 |

Factor 1 |

4.079 |

81.581 |

One Factor |

|

|

TP |

BE |

5 |

0.941 |

.000 |

0.912 |

Factor 1 |

4.052 |

81.033 |

One Factor |

|

BC |

PC |

5 |

0.946 |

.000 |

0.911 |

Factor 1 |

4.114 |

82.289 |

One Factor |

|

SC |

5 |

0.948 |

.000 |

0.910 |

Factor 1 |

4.417 |

82.932 |

One Factor |

|

|

FMP |

BF |

6 |

0.948 |

.000 |

0.938 |

Factor 1 |

4.765 |

79.421 |

One Factor |

|

BCM |

5 |

0.932 |

.000 |

0.873 |

Factor 1 |

3.942 |

78.850 |

One Factor |

|

|

CM |

5 |

0.946 |

.000 |

0.901 |

Factor 1 |

4.120 |

82.402 |

One Factor |

|

|

RM |

6 |

0.881 |

.000 |

0.870 |

Factor 1 |

3.548 |

70.967 |

One Factors |

|

|

OA |

5 |

0.829 |

.000 |

0.804 |

Factor 1 |

3.036 |

60.723 |

One Factor |

|

|

EC |

CMC |

5 |

0.874 |

.000 |

0.882 |

Factor 1 |

3.349 |

66.971 |

One Factor |

|

CC |

6 |

0.902 |

.000 |

0.852 |

Factor 1 |

4.042 |

67.371 |

One Factor |

|

|

ORC |

5 |

0.902 |

.000 |

0.826 |

Factor 1 |

3.497 |

69.945 |

One Factor |

|

|

OC |

7 |

0.892 |

.000 |

0.937 |

Factor 1 |

4.763 |

68.050 |

One Factor |

|

|

RC |

5 |

0.861 |

.000 |

0.863 |

Factor 1 |

3.220 |

64.391 |

One factor |

|

|

|

SC |

5 |

0.801 |

.000 |

0.811 |

Factor 1 |

2.839 |

56.771 |

One Factor |

|

MIE |

CR |

8 |

0.951 |

.000 |

0.933 |

Factor 1 |

5.963 |

74.539 |

One Factors |

|

RS |

6 |

0.914 |

.000 |

0.906 |

Factor 1 |

4.208 |

70.137 |

One Factor |

|

|

SW |

LS |

7 |

0.949 |

.000 |

0.949 |

Factor 1 |

5.361 |

76.579 |

One Factor |

|

PO |

3 |

0.835 |

.000 |

0.720 |

Factor 1 |

2.256 |

75.190 |

One Factor |

|

|

EW |

EP |

5 |

0.940 |

.000 |

0.907 |

Factor 1 |

4.045 |

80.892 |

One Factor |

|

ES |

BS |

7 |

0.887 |

.000 |

0.770 |

Factor 1 |

4.363 |

62.326 |

One factor |

Table 3. Parallel analysis and final reliability test

|

Constructs |

Dimensions |

Factors Extraction using Parallel Analysis |

Reliability Results After Factor Analysis |

||||

|

Factors to be Retained |

Actual Data |

Random Data |

Number of items |

Cronbach Alpha |

|||

|

Eigenvalues |

Mean Eigenvalues |

95th Percentile |

|||||

|

FS |

MC |

Factor 1 |

3.918 |

1.199 |

1.294 |

5 |

0.930 |

|

MS |

Factor 1 |

3.853 |

1.199 |

1.294 |

5 |

0.925 |

|

|

DF |

Factor 1 |

4.079 |

1.199 |

1.294 |

5 |

0.943 |

|

|

TP |

BE |

Factor 1 |

4.051 |

1.199 |

1.294 |

5 |

0.941 |

|

BC |

PC |

Factor 1 |

4.114 |

1.199 |

1.294 |

5 |

0.946 |

|

SC |

Factor 1 |

4.147 |

1.199 |

1.295 |

5 |

0.948 |

|

|

FMP |

BF |

Factor 1 |

4.765 |

1.239 |

1.337 |

6 |

0.948 |

|

BCM |

Factor 1 |

3.942 |

1.199 |

1.295 |

5 |

0.932 |

|

|

CM |

Factor 1 |

4.120 |

1.199 |

1.294 |

5 |

0.946 |

|

|

RM |

Factor 1 |

3.548 |

1.199 |

1.294 |

5 |

0.882 |

|

|

OA |

Factor 1 |

3.036 |

1.199 |

1.294 |

5 |

0.829 |

|

|

EC |

CMC |

Factor 1 |

3.348 |

1.199 |

1.294 |

5 |

0.874 |

|

CC |

Factor 1 |

4.042 |

1.239 |

1.337 |

6 |

0.902 |

|

|

ORC |

Factor 1 |

3.497 |

1.199 |

1.294 |

7 |

0.902 |

|

|

OC |

Factor 1 |

4.763 |

1.276 |

1.383 |

5 |

0.892 |

|

|

RC |

Factor 1 |

3.219 |

1.199 |

1.294 |

5 |

0.861 |

|

|

|

SC |

Factor 1 |

2.838 |

1.199 |

1.294 |

5 |

0.801 |

|

MIE |

CR |

Factor 1 |

5.963 |

1.302 |

1.404 |

8 |

0.951 |

|

RS |

Factor 1 |

4.208 |

1.239 |

1.337 |

6 |

0.914 |

|

|

SW |

LS |

Factor 1 |

5.360 |

1.276 |

1.383 |

7 |

0.949 |

|

PO |

Factor 1 |

2.256 |

1.112 |

1.204 |

3 |

0.835 |

|

|

EW |

EP |

Factor 1 |

4.044 |

1.199 |

1.294 |

5 |

0.940 |

|

ES |

BS |

Factor 1 |

4.362 |

1.276 |

1.276 |

7 |

0.887 |

3.2.1 Factor suitability

First of all, this study has performed factor suitability analysis which indicates the suitability of variables for conducting factor analysis. The results reported in Table 2 reveal that Kaiser-Mayer-Olkin (KMO) values are greater than 0.6 for all variables, supporting factor suitability for conducting EFA. Similarly, Bartlett test p-values are less than 0.05 for all variables. Hence, these results indicate that all variables are appropriate for conducting factor analysis techniques.

3.2.2 Factor extraction

This study has applied PCA to analyze the factor structure of the 126 items of microfinance and household economic portfolio model included in this study. This study has used three major factor extraction methods to determine and retain the total number of factors. The results reveal that Kaiser’s eigenvalue greater than one criterion produces one factor for all variables except the risk management dimension of financial management practices which has two factors (factor 1 – eigenvalue (3.879), variance explained (64.642); factor 2 – eigenvalue (1.246), variance explained (20.773). Then, Cattell’s scree test was conducted to confirm the results, which confirmed and produced precisely consistent results. As per both criteria, all study variables have one factor each except for the risk management dimension of financial management practices, which has two components.

3.2.3 Rotation

The direct Oblimin method was chosen instead of Orthogonal Rotation. The rotation process was performed for the variables with more than one component to ease the interpretation and refining of the item with respect to the particular construct. Hence, this is a solid ground to believe that human data are mostly associated to each other and related to underlying factors. A detailed discussion on such statement is available in methodology section. Findings from the Pattern Matrix table indicate that for construct risk management, most of the items are grouped under component one and the second component has only two unrelated items. An item with the lowest factor loading was first deleted. The EFA test has been re-run for the risk management dimension. The results show that all five items were grouped under one component, which perfectly measures the risk management dimension. The final results for EFA are reported in Table 2. Next, Horn’s Parallel analysis was performed following the four steps approach discussed in the previous section. Results for the Parallel analysis are reported in Table 3, where eigenvalues of actual data are compared with the eigenvalues of randomly generated parallel data. These results reveal that all variables have one factor each.

3.3 Reliability test (Cronbach’s alpha) after EFA

After performing EFA, this study again conducted reliability testing to determine the consistency between questions/items. A detailed results is shown in Table 3. The values of Cronbach’s Alpha after EFA are well above 0.7, which shows that all variables are consistent. Hence, after the item-deletion process, the reliability test results prove that the reliability coefficients for each construct are achieved.

3.4 Final factor structure of instrument

After the rotation process, all the obtained items under six variables were found similar to the originally adapted instrument from the literature. The researcher retained only those items which have factor loading greater than 0.3. Hence based on EFA testing, this research retained total 125 items of the instrument. Further, all 125 items covering eight constructs were cross-checked against four research areas identified by the experts such as microfinance effectiveness, human capital development, service efficiency, and sustainable socioeconomic development. This was done to ensure further efficacy of the instrument for future use.

At the end, the final items retained for the study variables are as follows; Microcredit with five items, Micro-savings with five items, Death-Benefit Fund with five items, Basic Entrepreneurship with five items, Service Coaching with five items, Product Development Coaching with five items, Basic Finance with six items, Budgeting and Cash Management with five items, Credit Management with five items, Risk Management with five items, Opportunity Awareness with five items, Commitment Competency with five items, Conceptual Competency with six items, Organizing Competency with five items, Opportunity Recognition Competency with seven items, Relationship Competency with five items, Strategic Competency with five items, Credibility with eight items, Responsiveness with six items, Level of Satisfaction with seven items, Provision of Opportunity with three items, Economic Performance with five items, and Entrepreneurial Success with seven items.

As far as individual item loadings are concerned, Table 4 shows that all three dimensions of financial services; Microcredit, Micro-savings, and Death-Benefit Fund have all items with higher loads of greater than 0.8. Similarly, all items of Basic Entrepreneurship, Service Coaching, and Product Development Coaching also have higher individual loads (greater than 0.8). Within Financial Management Practices; Basic Finance, Budgeting and Cash Management, and Credit Management also have all items with high individual loads (greater than 0.8). Whereas, dimensions of Risk Management and Opportunity Awareness have one of five (item 1: 0.575) and two out of five items (item 1: 0.714, item 4: 0.573), respectively with relatively low individual loads. In addition, measuring constructs of Credibility, Level of Satisfaction, Provision of Opportunity, and Economic Performance also have high individual loads for all items (greater than 0.8).

Table 4. Factor structure from EFA operation

|

Microfinance Financial Services |

|

|

Microcredit Factor loading |

|

|

“Management charges are reasonable” |

0.924 |

|

“The loan application procedure is simple” |

0.862 |

|

“The loan amount approved is sufficient” |

0.841 |

|

“The loan repayment tenor is adequate” |

0.855 |

|

“The loan repayment procedure is easy” |

0.940 |

|

Micro-savings |

|

|

“The savings interest rate is reasonable” |

0.825 |

|

“The procedures for opening savings are simple” |

0.881 |

|

“The savings withdrawal is easy” |

0.836 |

|

“The compulsory savings amount is reasonable” |

0.921 |

|

“Mandatory savings are affordable” |

0.921 |

|

Death-Benefit Fund |

|

|

“TKK benefits are comprehensive” |

0.906 |

|

“Method of contributing in TKK is simple” |

0.885 |

|

“Contributing to TKK is mandatory” |

0.863 |

|

“TKK contribution premium is affordable” |

0.932 |

|

“TKK claims are paid within a reasonable period” |

0.928 |

|

Training Program |

|

|

Basic Entrepreneurship |

|

|

“Motivational courses are useful in managing my business” |

0.907 |

|

“Basic business training is effective in running my business” |

0.905 |

|

“Basic account training is beneficial for my business” |

0.873 |

|

“Basic marketing training is useful in running a business” |

0.886 |

|

“Basic digital marketing training is beneficial for my business” |

0.928 |

|

Business Coaching |

|

|

Service Coaching |

|

|

“Start-up business assistance is very helpful in starting up my business” |

0.912 |

|

“Business recovery assistance helps to overcome my business challenges” |

0.899 |

|

“Scaling-up business assistance really helps my business to grow” |

0.898 |

|

“Business transformation assistance is effective in helping my business to diversify products” |

0.890 |

|

“Digital marketing assistance is very important in helping my business keep pace with technological developments” |

0.953 |

|

Product Development Coaching |

|

|

“Product development coaching is useful in helping me improving product innovation” |

0.905 |

|

“Product promotion and rebranding coaching is done adequately” |

0.867 |

|

“Product exhibition is an important platform to boost my business sales” |

0.888 |

|

“The use of online applications by Bazar Sahabat and Pasar Sahabat helps in increasing product sales” |

0.926 |

|

“Coaching in building business networks is useful to increase business profits” |

0.946 |

|

Financial Management Practices |

|

|

Basic Finance |

|

|

“I was able to set short term financial goals” |

0.917 |

|

“I was able to plan long term financial goal” |

0.873 |

|

“I was able to compare multiple options for a financial transaction” |

0.900 |

|

“I was able to make good financial decisions” |

0.879 |

|

“I was able to review my financial situation on a regular basis” |

0.868 |

|

“I was able to discuss my financial problems and goals with others” |

0.909 |

|

Budgeting and Cash Management |

|

|

“I was able to make a business budget” |

0.879 |

|

“I was able to estimate income and expenditures” |

0.889 |

|

“I was able to keep a record for expenditures” |

0.884 |

|

“I was able to compare actual expenditures to the budget” |

0.902 |

|

“I was able to keep business records” |

0.886 |

|

Credit Management |

|

|

“I was able to spend business cash flow wisely” |

0.905 |

|

“I was able to monitor loan status efficiently” |

0.895 |

|

“I was able to assess expense status effectively” |

0.890 |

|

“I was able to avoid additional cost of credit” |

0.938 |

|

“I was able to plan a clear credit control process” |

0.911 |

|

Risk Management |

|

|

“I was able to adequately insure our important assets” |

0.575 |

|

“I was able to minimize risk impact to my business” |

0.905 |

|

“I was able to do risk assessment for business benefit” |

0.906 |

|

“I was able to establish procedures to avoid potential risks” |

0.884 |

|

“I was able to create a safe project environment for all staff and clients” |

0.892 |

|

Opportunity Awareness |

|

|

“I was regularly able to allocate money for savings” |

0.714 |

|

“I was regularly able to allocate money for investments” |

0.878 |

|

“I was regularly able to look for investment opportunities” |

0.861 |

|

“I was able to take advantage of the marketing opportunity to improve sales” |

0.573 |

|

“I was able to diversify my investment opportunities” |

0.829 |

|

Entrepreneurial Competencies |

|

|

Commitment Competency |

|

|

“I was able to strive for business success” |

0.807 |

|

“I was able to allocate time and resources to keep the business running smoothly” |

0.801 |

|

“I was able to maintain high internal motivation” |

0.793 |

|

“I was committed to long-term business goals” |

0.857 |

|

“I was able to face stiff competition” |

0.832 |

|

Conceptual Competency |

|

|

“I was able to apply ideas, issues and views in business dealings” |

0.875 |

|

“I was able to accept a job with reasonable risk” |

0.785 |

|

“I was able to monitor risk to achieve business goals” |

0.759 |

|

“I was able to solve problems with new methods” |

0.886 |

|

“I was able to explore new ideas” |

0.880 |

|

“I was able to create opportunities out of problems” |

0.725 |

|

Organizing Competency |

|

|

“I was able to plan the operations of the business” |

0.863 |

|

“I was able to use a variety of resources to plan a business” |

0.850 |

|

“I was able to keep the enterprise run smoothly” |

0.885 |

|

“I was able to organize resources” |

0.873 |

|

“I was able to coordinate my work” |

0.865 |

|

“I was able to handle my staff” |

0.526 |

|

“I was able to give priority to business matters” |

0.852 |

|

Opportunity Recognition Competency |

|

|

“I was able to identify goods and services that customers want” |

0.904 |

|

“I was able to discover unfulfilled customer needs by others” |

0.890 |

|

“I was able to provide products and services that provide real benefit to customers” |

0.914 |

|

“I was able to seize profitable business opportunities” |

0.778 |

|

“I was able to understand the use of new technological tools to improve business performance” |

0.668 |

|

Relationship Competency |

|

|

“I was able to build trust for long -term business with others” |

0.654 |

|

“I was able to easily negotiate with others” |

0.862 |

|

“I was able to interact with others” |

0.821 |

|

“I was able to maintain good relationships with business partners” |

0.817 |

|

“I was able to understand the meaning of others through their words and actions” |

0.841 |

|

Strategic Competency |

|

|

“I was able to prioritize work in line with business goals” |

0.803 |

|

“I was able to act in line with business goals” |

0.721 |

|

“I was able to monitor the progress of the business to achieve goals” |

0.754 |

|

“I was able to compare actual business results with goals” |

0.739 |

|

“I was able to take action after considering all matters” |

0.748 |

|

Microfinance Institutions’ Efficiency |

|

|

Credibility |

|

|

“AIM provides all services in a timely manner (e.g. loan disbursement)” |

0.856 |

|

“AIM genuinely tries to resolve problems” |

0.846 |

|

“AIM regularly shares information through fieldworkers” |

0.857 |

|

“AIM is fair in decision-making” |

0.836 |

|

“AIM fulfil its promises” |

0.876 |

|

“AIM maintains quality services” |

0.877 |

|

“AIM staff are responsive to any queries” |

0.902 |

|

“AIM maintains transparency in the transaction processes” |

0.856 |

|

Responsiveness |

|

|

“AIM listens to our suggestions” |

0.888 |

|

“AIM helps us in dealing with other organizations” |

0.861 |

|

“AIM gives attention towards our welfare” |

0.902 |

|

“AIM’s staff gives attention towards our problems” |

0.887 |

|

“AIM’s staff understand the needs of the individual beneficiary” |

0.918 |

|

“AIM’s location is convenient” |

0.485 |

|

Households’ Social Well-being |

|

|

Level of satisfaction |

|

|

“I was satisfied with my Family’s level of income” |

0.887 |

|

“I was satisfied with my family’s level of savings” |

0.879 |

|

“I was satisfied with my family’s standards of living” |

0.860 |

|

“I was satisfied with my family’s level of employment” |

0.895 |

|

“I was satisfied with my children’s education” |

0.875 |

|

“I was satisfied with my family’s health status” |

0.883 |

|

“I was satisfied with my family's supply of daily goods” |

0.846 |

|

Provision of Opportunities |

|

|

“My Project was able to provide employment opportunities to family members” |

0.877 |

|

“I was able to provide financial resources for my children’s education” |

0.878 |

|

“I had the opportunity to gain knowledge and skills” |

0.845 |

|

Households’ Economic Well-being |

|

|

Economic Performance |

|

|

“My income keeps increasing” |

0.896 |

|

“My household expenditure keeps increasing” |

0.909 |

|

“My assets keep increasing” |

0.904 |

|

“My savings keep increasing” |

0.878 |

|

“My confidence level keeps increasing” |

0.910 |

|

Households’ Entrepreneurial Success |

|

|

Entrepreneurial Success |

|

|

“The profits from my project keep increasing” |

0.888 |

|

“The sales from my project keep increasing” |

0.899 |

|

“The number of employees from my project starting to increase” |

0.642 |

|

“The total products from my project keep increasing” |

0.915 |

|

“The number of buyers from my project keeps increasing” |

0.927 |

|

“My entrepreneurship skills keep increasing” |

0.513 |

|

“The use of technological equipment keeps increasing” |

0.629 |

On the other hand, results provide mix individual loads for the constructs of Commitment Competency (1 item: less than 0.8 and 4 items: greater than 0.8), Conceptual Competency (3 items: less than 0.8 and 3 items: greater than 0.8), Organizing Competency (1 item: less than 0.8 and 6 items: greater than 0.8), Opportunity Recognition Competency (1 item: less than 0.8 and 4 items: greater than 0.8), Relationship Competency (1 item: less than 0.8 and 4 items: greater than 0.8), Strategic Competency (4 items: less than 0.8 and 1 item: greater than 0.8), Responsiveness (1 item: less than 0.8 and 6 items: greater than 0.8), and Entrepreneurial Success (3 items: less than 0.8 and 4 items: greater than 0.8). The detailed items and their loading are displayed in Table 4.

The primary purpose of this study is to develop a new measuring tool for microfinance and household economic portfolio model in Malaysia. Therefore, the research aims to develop and validate the factor structure and dimensionality of the constructs in microfinance and household economic portfolio model. This study has followed standard methodology that involves an extensive review of existing constructs and appropriate statistical analysis. Specifically, EFA is employed to validate and assess the instrument's factor structure.

Considering the longstanding issue of humankind’s economic deprivation and poverty, authorities continue to search for effective tools that can help in uplifting the socioeconomic status of poor individuals. Similarly, researchers continue to investigate various socioeconomic interventions and their role in enhancing individuals’ socioeconomic performance. Hence, this research has significant contribution towards a newly developed microfinance and households’ socioeconomic model, which emphasizes assessing the role of various microfinance services and household specific factors in eradicating poverty. In addition to developing a reliable measuring instrument for this microfinance and household socioeconomic model, this research has uncovered a number of crucial variables that could significantly help to improve households’ socioeconomic status and reduce poverty in the world. Based on the EFA’s result, the study found that there are seven factors namely financial services (FS), training programs (TP), business coaching (BC), financial management practices (FMP), entrepreneurial competencies (EC), microfinance institutions’ service efficiency (MIE), and households’ socioeconomic performance (SW, EW, and ES) that meet the reliability and validity test.

Moreover, to ensure further accuracy, all final items covering eight constructs were cross-checked against research areas suggested by the industry experts. Microfinance factors were cross-checked against their effectiveness in helping clients to avail maximum benefits. For instance, the final factor structure indicates that all items under microcredit and micro-savings represent financial services’ accessibility and adequacy, which helps poor clients promptly meet their financial needs. Similarly, items under the death-benefit fund cover contribution aspects and claim delivery, influencing the client’s participation in the program. Next, all items under constructs of basic entrepreneurship, service coaching, and product development; capture the effectiveness of training and coaching programs in developing capabilities among clients to improve their business performance.

Furthermore, the variables of financial management practices and entrepreneurial competencies were cross-checked against the research area of human capital development. Here, the items under various constructs of financial management measure the extent to which clients were able to manage their financial matters after participating in microfinance programs. Likewise, items under the constructs of entrepreneurial competencies measure improvement in clients’ capabilities relating to enterprise management and entrepreneurial strategies. In addition, the constructs of microfinance service efficiency have significant role in the success of microfinance services to help uplift poor clients. In this regard, the items under the construct of credibility represent the client’s level of trust in the microfinance institutions and their employees. Similarly, the items under the construct of responsiveness represent the response efficiency of microfinance institutions toward clients’ problems.

Finally, the constructs of households’ social wellbeing, economic wellbeing, and entrepreneurial success were cross-checked against the concept of sustainable socioeconomic development. Expressly, the items under social wellbeing represent clients’ level of satisfaction in meeting their social needs after participating in microfinance schemes. In a similar manner, the items under economic wellbeing and entrepreneurial success represent improvement levels in clients’ economic and business performances, respectively.

Consequently, given all discussion regarding final items and their respective constructs, this study shows that the developed instrument is consistent with the industry experts' research areas. Hence, this instrument is proved valid and effective to be applied in future related research.

4.1 Contributions to the literature

This research provides significant contributions to the existing body of literature. Most importantly, it offers an instrument to assess the impact of microfinance services on household socioeconomic performance. This instrument is proved valid and reliable in measuring various important microfinance and household specific factors. Hence, this study opens great opportunities for the researchers to incorporate these constructs in the future empirical research. Results from this study provide measuring constructs for three types of microfinance services including FS, TP, and BC. Existing literature in Malaysia [10, 19] has mostly focused on microfinance financial interventions and trainings. Hence, this research introduces a new explanatory factor that is business coaching (BC) in the microfinance and household economic model. Introducing business coaching service as input factor would have significant implications in the context of human capital development in Malaysia. Particularly, business coaching could be a vital factor for low-income business holders as such individuals usually have insufficient capabilities to compete in the market as mentioned in the past studies that business coaching is an effective tool in enhancing business performance [48]. Hereafter, provided with proper consultation and support from microfinance coaches, microbusiness holders could develop effective skills and strategies to achieve their business goals.

Furthermore, both mediating factors; FMP and EC are also proved valid and reliable. Most of the existing empirical studies [4, 10] are limited to the microfinance impact assessment, thus, ignoring the underlying mechanisms that can explain the impact pathway towards improved socio-economic outcomes. Hence, this research highlights two potential mediating factors; entrepreneurial competencies and financial management practices explaining the impact pathway from microfinance to household socioeconomic performance. Entrepreneurial competencies have been discussed vastly in the entrepreneurship literature [49]. Same as financial management practices in the relationship to SME business performance [50]. Thus, these both factors have significant implications for the authorities and low-income households. This research identifies these both factors as empowering capabilities that could help in enhancing the effectiveness of microfinance to eradicate poverty.