Sugey de J. López Pérez![]()

OPEN ACCESS

The Covid-19 disruption in Mexico coincided with serious structural problems, intensifying the unexpected social and economic contraction. It created a rebound effect in which structural gaps accentuated the negative effects of the pandemic and vice-versa. Revenue collection is intended to ensure fulfilment of essential state spending and social welfare. In this study, tax revenues and public spending on health in Mexico were analyzed empirically and revenue efficiency was evaluated. Growth was observed in 2020 due to the elimination of universal VAT compensation, taxation of digital services and the fight against tax evasion and fraud. In 2021, IEPS collection plummeted and impacted the aggregate. Tax reform in Mexico remains an enigma. Should the pandemic reappear and structural gaps widen, spending provisions will require financing. The level of public spending is low compared to other LAC and OECD countries. Nonetheless, the efforts in health expenditure and provision amidst pandemic conditions should not be ignored, as it increased from 5.6 % to 6.24 % of the GDP between 2019 and 2020.

structural gaps, public spending, public health spending, tax revenues, Covid-19 pandemic

A tax system reflects a country’s socio-economic model and provides an instrument for transforming it [1]. Presumably, tax revenues guarantee the fulfilment of essential public functions, state services and social welfare. They strengthen public expenditure and investment, thereby generating performance expectations regarding state-provided public services. They also enhance a government’s capacity to promote economic development, combat inequality and respond to unforeseen global risks [2]. In Mexico, little of this is happening because tax revenues remain low and limit the welfare state [1].

The Covid-19 pandemic was one of the greatest recent threats to society and it uncovered worrying structural gaps in the country. The disruption it created took place against the backdrop of a stagnant or slow-growing economy in some sectors, and a clearly established crisis in some states [3, 4]. Meanwhile, the need for a national economic and social project for fairer distribution of welfare state benefits had already been noted [5]. The health crisis converged with serious structural problems in the country, unexpectedly intensifying social and economic contraction.

The Covid-19 crisis has exacerbated the major challenges associated with declining social cohesion, livelihoods and mental health [2]. It entered our lives in a context of global socio-ecological crisis on many fronts, including water, pollution, scarcity of natural resources and loss of biodiversity. These problems magnify public policy challenges and require more public commitment, not less. From an economic policy perspective, all this involves the public budget and inevitably requires a review of the state’s most important policy tool: taxation.

The pandemic aggravated the hidden but serious structural problems that affect much of Mexican society: inequality, unemployment, informality, the dismantling of public investment and infrastructures, public security, corruption, fragile global supply chains for food and other goods, gender inequality and poverty [6-12]. All these structural gaps reveal the pending issues for the state and society as a whole.

Despite the difficulties and against all odds, government performance enabled a favorable economic response [10, 13]. Revenue actually increased in 2020, the most critical year of the pandemic. Elimination of the universal Value Added Tax (VAT) compensation increased the Gross Domestic Product (GDP) by 0.5%, taxation of digital services was established, and supervisory and penalty measures were introduced to combat harmful tax practices (evasion, avoidance and fraud). Measures implemented alongside permanent social programs [13] also played a key role in the critical phase of the pandemic.

The Organisation for Economic Co-operation and Development (OECD) [10] reported that loans were granted to small and medium-sized enterprises (SMEs) and individuals (work credit); VAT returns processes were accelerated; development banks provided liquidity support and guarantees; temporary changes in accounting rules were implemented to allow credit providers to defer loans up to six months; and a three-month allowance was established for newly-unemployed workers with Infonavit credit / Infonavit mortgages.

While these palliative measures mitigated slight momentary issues, they did not solve the most substantive problems. Major challenges remain that will require significant spending. Mexico needs fiscal reform and transformation to reduce its structural gaps (and other challenges), ensure the provision of quality public services, finance sustainable and inclusive development, and withstand anticipated global risks from economic, social, environmental and technological stressors.

This study analyses Mexico’s tax revenue structure and the level of public spending in the key trending area of healthcare. An empirical study of tax revenue trends and evolution (2010 - 2021) and public spending on health (2010 - 2020) was carried out to enable reflection about fiscal reform in Mexico. The work is structured into five Sections. After this introduction, the second Section presents a review of the literature, the third Section describes the methodology, the fourth Section presents the outcomes of the empirical analysis, and the fifth Section offers final reflections.

High revenue collection is widely recognized as a key to the welfare state. In Mexico, however, fiscal reforms have historically been unable to improve collection levels and tax revenues are considered fragile [1, 14]. In a context of profound structural miscalculations [5, 15], reduced revenue collection capacity weakens the state’s ability to undertake strategic actions that would put Mexico on a path of economic development and social well-being.

According to López Pérez and Vence [1], Mexico’s systemically low tax burden makes it the country with the lowest tax collection in relation to GDP of all the OECD countries and places it among the four lowest in Latin America. This limits the state’s capacity to implement income redistribution strategies for both revenue and expenditure or finance public spending on strategic interests, security and social welfare.

Beyond the technical design of the system, state tax reform has been plagued by internal errors and historical failures since the time Mexico achieved its independence, which explains much of the current situation of low tax collection [16]. Additionally, most tax reforms in Mexico and other countries throughout Latin American and the Caribbean were generated during periods of economic reform [17], when temporary, internal phenomena conditioned tax system design [18]. Beteta and Yanes [13] have observed that such outcomes stem from a deep-rooted culture of privilege and the practices, rules and institutions that perpetuate it.

Clearly, these and other factors explain much of the current state of the Mexican tax system and its collection levels. The last tax reform in Mexico (implemented in 2014) failed to meet expectations of progress, and the current government remains indifferent. Mexican tax revenues are among the lowest in the LAC region [1, 19], a situation that conditions public spending performance. According to World Bank data [20], Mexico’s public spending is the fifth lowest in the region (22.4% of GDP in 2020), ahead of the Dominican Republic, Paraguay, Nicaragua and Guatemala (21.4%, 19.2%, 19.2% and 14.9% of GDP in 2020, respectively). Mexico ranks third lowest in public spending on health (6.2% of GDP in 2020) among OECD member countries. For the same period and indicator, the United States ranked highest (17.8%), followed by Germany (12.8%), France and Austria (12.2%) [21].

Thus, even in pandemic conditions, Mexico has continued to pursue a restrictive policy and a short-sighted strategy that relies on the recent and historical counter-cyclical policy of the United States [22]. The fiscal measures implemented (approximately 1% of GDP in 2020 [4, 23, 24]) were the smallest of all Latin American countries, demonstrating behavior similar to that of most African countries. As a result, the measures implemented lacked the scope and financing to cope with the immense needs generated by Covid-19 [4].

In a tragic downward spiral the structural gaps accentuated the negative effects of the pandemic [25, 26], creating a health crisis that in turn affected economic and social dimensions. Employment plummeted and poverty reduction was undermined as economic, social and environmental asymmetries worsened [26]. In Mexico, poverty increased at an accelerated rate due to the effect of containment measures on the economy and employment. CONEVAL [11] estimates indicate that extreme income poverty could increase by 4.9 to 8.5%, affecting 6.1 to 10.7 million people during the pandemic period.

Covid-19 infection frequency, severity and lethality was unevenly distributed and had greater impact on historically disadvantaged layers of society [26, 27]. The shock of the pandemic also affected the balance of supply and demand: as businesses were forced to close, supply shrank sharply and demand plunged even lower [22]. Informal economies were more vulnerable to contagion in the absence of health protection and levels of violence and insecurity became increasingly worrying.

The empirical analysis described here is based on the assumption that high levels of tax revenue would allow Mexico to apply fiscal tools and instruments for economic development and the management of extraordinary social and health contingencies such as the Covid-19 pandemic. This would include the direct impact on the public health system as well as economic paralysis, as occurred in 2020 and to a lesser extent in 2021. Accordingly, the analysis looks at the evolution of tax collection over the last decade, the impact of the Covid-19 crisis, tax structure trends and Mexico’s unfinished business in a context of social vulnerability.

An empirical analysis was carried out and compared with the relevant literature. Tax revenue statistics were obtained from the Open Data platform of the Tax Administration System (SAT in Spanish) and from the Public Finance Statistics portal of the Ministry of Finance and Public Credit (SHCP in Spanish). Information from the National Institute of Statistics and Geography (INEG, in Spanish) was also used to obtain the GDP indicator. Expenditure data were obtained from the OECD Data Indicators and in the DataBank portal of the World Bank.

The Mexican economy grew at an average annual rate of 1.9% from 1982 to 2020 and GDP by 0.32% for the same period [22]. The Economic Commission for Latin America and the Caribbean (ECLAC) [23] reported that in 2020, the Covid-19 pandemic caused Mexico’s GDP to contract 8.3% in real terms and with original series (compared to 0.2% in 2019). This figure represents the largest fall in the country’s economic activity since 1932. The fiscal deficit of the non-financial public sector rose to 2.9% of GDP (compared to 1.6% in 2019) and the 2020 target was abandoned. Mexico’s fiscal reform remains enigmatic, ineffective and weakened by crisis events, leaving public expenditure needs unresolved.

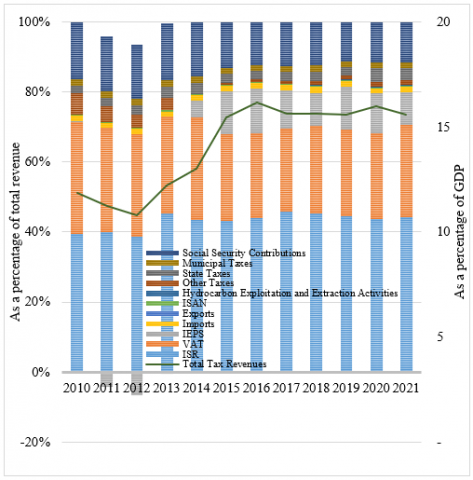

The 2010-2021 series indicates a slightly volatile tax structure across all revenue categories. Income tax (ISR), Value Added Tax (IVA), Special Tax on Production and Services (IEPS) and Social Security Contributions made up an average of 78% of total revenue. The revenue collection trend showed a decline in the final years, but the 2021 budget target proposed under the Law on Federation Income (LIF) was achieved [27, 28]. At the end of the period, total tax revenues represented just 15.59% of GDP in 2021: higher than the average 14.1% of GDP (2010-21), but lower than the 2016 maximum of 16.5% of GDP (Figure 1).

It is worth noting that despite the events related to COVID-19, revenue collection in relation to GDP grew 1.03% from 2019 to 2020 (Table 1, Table 2). Obviously, the cause lies in both increased revenue collection and the sharp contraction of GDP. The government strengthened collection capacity by applying technical and regulatory measures to eliminate the universal VAT offset, establishing a tax on digital services and combatting evasion practices. However, cautiousness of these tax changes combined with IEPS fuel subsidy policy reversals and the overall effects of the economy led to a decline in the 2021 results.

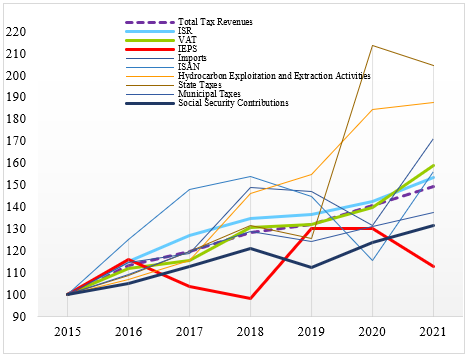

The evolution (base 100=2015) of revenue collection in absolute values shows a positive progression of tax revenues in 2021. Revenues rebounded from 140% in 2020 to their peak level of 149.34% in 2021 (Figure 2) and were manifested in all tax categories except the IEPS. Income tax increased markedly from 136.38% in 2019 to 142.4% in 2020 and continued to climb to 153.18% in 2021. VAT was more intense between 2020 (139.64%) and 2021 (158.89%) and in absolute terms exceeded one trillion pesos for the first time (SHCP & SAT), 2022).

Increased revenue collection amidst intense economic contraction resulting from the pandemic is a very relevant fact that reveals a notable improvement in collection efficiency.

Figure 1. Structure (left axis) and Evolution of Tax Revenues in % GDP (right axis), 2010 – 2021

Source: SAT Open Data [29], SHCP Statistics [30] and INEGI [31].

Table 1. Tax revenues as % of GDP

|

Tax Type |

As Percentage of GDP |

|||||||

|

2010 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

|

|

ISR |

4.69 |

6.67 |

7.09 |

7.15 |

7.07 |

6.96 |

7.00 |

6.90 |

|

VAT |

3.77 |

3.81 |

3.94 |

3.72 |

3.92 |

3.85 |

3.92 |

4.09 |

|

IEPS |

0.03 |

1.91 |

2.05 |

1.68 |

1.48 |

1.90 |

1.83 |

1.45 |

|

Imports |

0.18 |

0.24 |

0.25 |

0.24 |

0.28 |

0.27 |

0.23 |

0.28 |

|

Exports |

1E-06 |

6E-06 |

2E-06 |

2E-06 |

8E-07 |

2E-06 |

7E-07 |

4E-07 |

|

ISAN |

0.03 |

0.04 |

0.05 |

0.05 |

0.05 |

0.04 |

0.03 |

0.04 |

|

Hydrocarbon Exploitation and Extraction Activities |

- |

0.02 |

0.02 |

0.02 |

0.02 |

0.02 |

0.03 |

0.03 |

|

Other Taxes |

0.72 |

0.07 |

0.12 |

0.14 |

0.20 |

0.16 |

0.22 |

0.20 |

|

State Taxes |

0.25 |

0.41 |

0.41 |

0.41 |

0.42 |

0.39 |

0.64 |

0.56 |

|

Municipal Taxes |

0.22 |

0.25 |

0.25 |

0.26 |

0.26 |

0.24 |

0.24 |

0.23 |

|

Social Security Contributions |

1.95 |

2.05 |

1.98 |

1.95 |

1.95 |

1.76 |

1.86 |

1.81 |

|

Total Taxes Revenues |

11.85 |

15.46 |

16.15 |

15.62 |

15.63 |

15.60 |

16.00 |

15.59 |

Source: Based on SAT Open Data [29], SHCP Statistics [30] and INEGI [31].

Table 2. Collection by tax type (% of tax income)

|

Tax Type |

As A Percentage of Total Collection |

|||||||

|

2010 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

|

|

ISR |

39.56 |

43.15 |

43.90 |

45.80 |

45.22 |

44.63 |

43.73 |

44.26 |

|

IVA |

31.86 |

24.66 |

24.37 |

23.83 |

25.06 |

24.68 |

24.50 |

26.23 |

|

IEPS |

0.28 |

12.35 |

12.67 |

10.74 |

9.44 |

12.18 |

11.43 |

9.32 |

|

Imports |

1.55 |

1.54 |

1.56 |

1.53 |

1.78 |

1.71 |

1.44 |

1.76 |

|

Exports |

1E-05 |

4E-05 |

1E-05 |

1E-05 |

5E-06 |

1E-05 |

4E-06 |

2E-06 |

|

ISAN |

0.29 |

0.25 |

0.28 |

0.31 |

0.30 |

0.28 |

0.21 |

0.26 |

|

Hydrocarbon Exploitation and Extraction Activities |

- |

0.13 |

0.12 |

0.13 |

0.15 |

0.15 |

0.17 |

0.16 |

|

Other Taxes |

6.04 |

0.43 |

0.72 |

0.88 |

1.25 |

1.06 |

1.36 |

1.27 |

|

State Taxes |

2.15 |

2.63 |

2.53 |

2.63 |

2.70 |

2.50 |

4.00 |

3.60 |

|

Municipal Taxes |

1.83 |

1.63 |

1.57 |

1.64 |

1.63 |

1.54 |

1.52 |

1.50 |

|

Social Security Contributions |

16.43 |

13.23 |

12.28 |

12.51 |

12.47 |

11.28 |

11.65 |

11.64 |

Source: Based on SAT Open Data [29], SHCP Statistics [30] and INEGI [31].

Figure 2. Evolution of revenues by tax type in absolute values (millions of pesos). Base index 100=2015

Source: Based on SAT Open Data [29], SHCP Statistics [30] and INEGI [31].

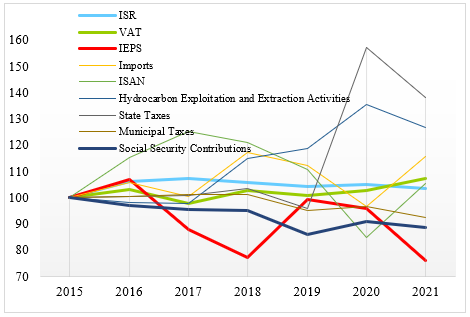

IEPS revenues continue to serve the policy of subsidies (incentives) for gasoline, diesel and fuel-oil. This has been the prevailing strategy since the 1980s, when the IEPS replaced the 1974 sales tax on gasoline [1]. The slump depicted in the IEPS corresponds to 100% subsidization of the contributions for gasoline and diesel [32]. The variation between budgeted and actual IEPS revenue was -21.8% in 2021, reflecting a drop from 96.59% of the base index (100=2015) in 2020 to 76.09% in 2021 (Figure 3).

Figure 3. Evolution of tax revenues by tax type as % of GDP. Base index 100=2015

Source: Based on SAT Open Data [29], SHCP Statistics [30] and INEGI [31].

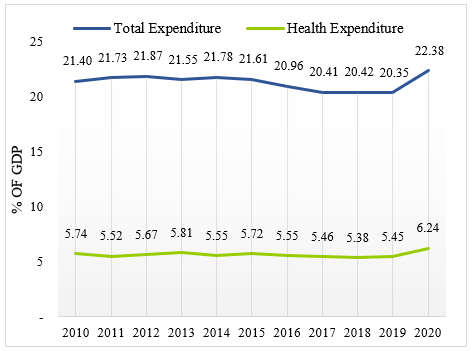

The analysis of public expenditure data for this period offers a complementary view. Total public expenditure was very modest compared to other OECD countries and had been declining relative to GDP since 2012. Then it increased significantly from 20.35% of GDP in 2019 to 22.38% in 2020, (Figure 4). Admittedly, this increase was due to both the increase in total expenditure and the contraction of GDP in that pandemic year. In any case, the increase in public expenditure exceeded the increase in revenue that year, causing the fiscal deficit to increase. This trend was observed in all OECD countries and Mexico was actually among those with the smallest deficit increase. It continues to have one of the lowest fiscal deficits and has contained public debt issuance.

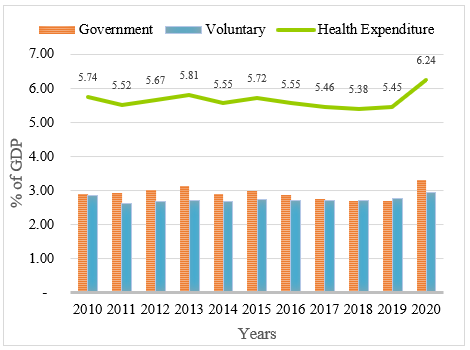

However, this is all a matter of perspective. Although Mexico’s health spending was the third lowest of all OECD countries, the effort made in the period under analysis cannot be underestimated. In 2020, government and voluntary health expenditure soared past its average of 5.6% of GDP to reach a historic 6.24% (Figure 5) in response to the pandemic emergency.

Figure 4. Total expenditure and health expenditure in Mexico as % of GDP, 2010 – 2020

Source: DataBank [20], OECD [21].

Figure 5. Trend in health expenditure (by financing schemes) as % of GDP

Source: OECD [21, 33]

Note: Government refers to mandatory financing schemes and Voluntary refers to direct household payment schemes.

Tackling current problems stemming from health, environmental, social and security challenges call for significant increases in public expenditure, which inevitably means strengthening public finances. Mexico finds itself in a situation of increasing vulnerability in the wake of the Covid-19 crisis and other clear global risks that require public resources to implement public policies.

In Mexico, relevant measures were applied in 2020-21, tax revenues did not fall and expenditure increased. However, it continues to be one of the LAC and OECD countries with the lowest tax collection and expenditure levels. Mexico has a weak welfare state with great challenges that were exposed and intensified by the Covid-19 crisis.

Improving the tax structure will be one of the most important tasks in the coming years. The fiscal changes that the current administration has quietly initiated should continue. In general terms, an improved tax system would: increase the effective rate for high incomes, advance tax progressivity, strengthen state and municipal finances, decouple the appropriation of economic resources from the exploitation of natural resources, eliminate subsidies, benefits and harmful incentives, address / consider social, health, ecological and gender trends.

This study makes a brief discussion and critical balance of the level of tax revenues and the capacity of the State to act in the time period of the coronavirus pandemic. However, despite being limited to that short period of time, it is important because it allows us to highlight some structural weaknesses of the Mexican fiscal system and the need for important fiscal reforms in Mexico to improve the welfare system of Mexican society.

Some issues that will require additional work is the analysis of the great inequality existing in Mexico and its consequences for the advancement of a robust taxation for an advanced welfare system. The work has shown the progress in tax collection through the prosecution of fraud and evasion; well, it is important to further analyze this aspect and the type of measures that could reduce this serious structural problem. The analysis of the different types of tax benefits in the major taxes is also necessary for this purpose.

This work was funded by the ICEDE research group, which includes the authors, as part of Galician Competitive Research Group ED431C 2022/15, financed by the Xunta de Galicia.

|

ISR |

Corporate Income Tax |

|

VAT |

Value Added Tax |

|

IEPS |

Special Tax on Production and Services |

|

ISAN |

New Car Tax |

|

SAT |

Tax Administration Service |

|

SHCP |

Secretary of Finance and Public Credit |

|

CONEVAL |

National Council for the Evaluation of Social Development Policy |

[1] López Pérez, S.D.J., Vence, X. (2021). Structure and evolution of tax revenues and tax benefits in Mexico. Analysis of the 1990-2019 period and evaluation of the 2014 fiscal reform. El Trimestre Económico, 88(350): 373-417. https://doi.org/10.20430/ETE.V88I350.1104

[2] World Economic Forum. (2022). The Global Risks Report 2022 17th Edition. https://www3.weforum.org/docs/WEF_The_Global_Risks_Report_2022.pdf.

[3] López Arevalo, J.A. (2022). Economic growth in Mexico and its dependence on US countercyclical policies within the context of integration. Revista Galega de Economía, 31(1): 1-22. https://doi.org/https://doi.org/10.15304/rge.31.1.8004

[4] Provencio, E. (2020). Política económica y Covid-19 en México en 2020/Economic Policy and Covid-19 in Mexico in 2020. Economíaunam, 17(51): 263-281. https://doi.org/10.22201/fe.24488143e.2020.51.563

[5] Torres, F., Rojas, A. (2015). Economic and social policy in Mexico: disparities and consequences. Problemas del desarrollo, 46(182): 41-66. https://doi.org/10.1016/j.rpd.2015.06.001

[6] Montes de Oca Zavala, V., Alonso Reyes, M.D.P., Montero-López Lena, M., Vivaldo-Martínez, M. (2021). Sociodemografía de la desigualdad por Covid-19 en México. Revista Mexicana de Sociología, 83(SPE2): 67-91. https://doi.org/10.22201/iis.01882503p.2021.0.60169

[7] CEPAL. (2020). El Desafío Social En Tiempos Del COVID-19. https://repositorio.cepal.org/items/01568fdc-9a77-4394-a792-079160eca4ec.

[8] Chiatchoua, C. (2022). Interdisciplinary dialogues during the context of covid-19. Instituto Universitario de Innovación Ciencia y Tecnología Inudi Perú, 10-22. https://doi.org/10.35622/inudi.cb1.1

[9] Juliá Igual, J.F., Bernal Jurado, E., Carrasco Monteagudo, I. (2022). Social Economy and Economic Recovery in the aftermath of the COVID-19 crisis. CIRIEC-España, Revista de Economía Pública, Social y Cooperativa, 104. https://doi.org/10.7203/ciriec-e.104.21734

[10] OECD. (2022). OECD Economic Surveys: Mexico 2022. OECD iLibrary. https://doi.org/https://doi.org/10.1787/2e1de26c-en

[11] The Social Policy in the Context of the Pandemic by the Virus SARS-CoV-2 (COVID-19) in Mexico. Consejo Nacional de Evaluación de la Política de Desarrollo Social (CONEVAL), México.

[12] De La Emergencia a La Recuperación de La Pandemia Por La COVID-19: La Política Social Frente a Desastres. CONEVAL: Ciudad de México 2021. https://www.coneval.org.mx/Evaluacion/IEPSM/Documents/Politica_social_atencion_a_desastres.pdf.

[13] Beteta, H., Yanes, P. (2022). ECLAC’S thought and the dilemmas for the transformation of Mexico. El Trimestre Económico, 89(353): 339-367. https://doi.org/10.20430/ete.v89i353.1412

[14] Tello, C., Hernández, D. (2010). Sobre la reforma tributaria en México. Economía unam, 7(21): 37-56.

[15] Barba, C.S. (2004). Welfare and Social Reform Regime in Mexico. Comisión Económica para América Latina y el Caribe, Mexico. https://repositorio.cepal.org/items/83591afd-9c1c-45a7-ac6d-ba790c60905c.

[16] Ríos Granados, G. (2013). Breve Historia Hacendaria de México, Series Est.; Ríos Granados, G., Santos Flores, I., Eds. Universidad Nacional Autónoma de Mexico: México. http://ru.juridicas.unam.mx/xmlui/handle/123456789/12128.

[17] Jáuregui, L. (2003). Old wine and new bottles. Tax history in Mexico. Historia Mexicana, 52(3): 725–771. https://historiamexicana.colmex.mx/index.php/RHM/article/view/1405.

[18] Gómez Sabaini, J.C., Morán, D. (2017). Consensus and confidence in Latin America's Tax Policy. Comisión Económica para América Latina y el Caribe (CEPAL), Santiago.

[19] OECD. (2021). Revenue Statistics in Latin America and the Caribbean 1990-2020. OECD Publishing, París. https://doi.org/https://doi.org/10.1787/58a2dc35-en-es

[20] Banco Mundial. DataBank https://datos.bancomundial.org/, accessed on Jun. 11, 2022.

[21] OECD. Health spending (indicator) https://data.oecd.org/healthres/health-spending.htm, accessed on Aug. 15, 2022.

[22] Arévalo, J.A.L. (2022). Economic growth in Mexico and its dependence on US countercyclical policies within the context of integration. Revista Galega de Economía, 31(1): 1-22. https://doi.org/https://doi.org/10.15304/rge.31.1.8004

[23] Economic Commission for Latin America and the Caribbean (ECLAC). Economic Survey of Latin America and the Caribbean 2021. México, Santiago de Chile. https://repositorio.cepal.org/server/api/core/bitstreams/3a2ed718-d1a6-48d6-88fa-8f2f1f7467e7/content.

[24] Fiscal Monitor Database of Country Fiscal Measures in Response to the COVID-19 Pandemic. https://www.imf.org/en/Topics/imf-and-covid19/Fiscal-Policies-Database-in-Response-to-COVID-19, accessed on Aug. 5, 2022.

[25] Jiménez, J.P., Podestá, A. (2009). Investment, tax incentives and tax expenditures in Latin America. Comisión Económica para América Latina y el Caribe (CEPAL).

[26] ECLAC. (2021). The recovery paradox in Latin America and the Caribbean: Growth amid persisting structural problems: Inequality, poverty and low investment and productivity. Special Report COVID-19, 11.

[27] Laurell, A.C. (2020). Dimensions of the Covid-19 Pandemic. Eltrimestre económico, 87(348): 963-984. https://doi.org/10.20430/ETE.V87I348.1153

[28] Diario Oficial de la Federación. (2021). Ley de Ingresos de la Federación para el Ejercicio Fiscal. México. https://www.diputados.gob.mx/LeyesBiblio/pdf/LIF_2023.pdf.

[29] Secretary of finance and public credit. (2012). https://imcp.org.mx/IMG/pdf/ANEXO_2_NOTICIAS_FISCALES_38.pdf, accessed on Jun. 6, 2012.

[30] SHCP. Finanzas Públicas. http://presto.hacienda.gob.mx/EstoporLayout/estadisticas.jsp, accessed on May 13, 2022.

[31] INEGI system of national accounts of Mexico. https://www.inegi.org.mx/temas/pibti/, accessed on Jun. 2, 2022.

[32] Decree for the establishment of complementary tax incentives to automotive fuels. Diario Oficial de la Federación. https://dof.gob.mx/nota_detalle.php?codigo=5644745&fecha=04/03/2022#gsc.tab=0.

[33] General government spending. OECD iLibrary. https://doi.org/10.1787/cc9669ed-en