Hakeem Hammood Flayyih*![]() | Karrar Kareem Jawad

| Karrar Kareem Jawad![]() | Thamer Kadhim Al-Abedi

| Thamer Kadhim Al-Abedi![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The present study tackles the complex issue of the urgent need for Environmental Auditing (EA) in Iraq in the absence of laws that support environmental management and in the light of the high rates of cancerous diseases in Iraq, which coincided significantly with the increase in oil production, according to the numbers indicated in the Iraqi Ministry of Health. The study aimed to investigate the mediating role of Management Systems (MS) related to the role of EA supporting sustainability reports concerning the reduction of the negative effects of gas emissions from oil companies. We adopted the descriptive approach which relies on studying relationships through a questionnaire that was distributed to a group of workers at Doura Refinery in Baghdad for refining oil. The number of workers was 155 people who are specialized in administrative and financial aspects, let alone some other supporting specializations in the refinery selected. In designing the questionnaire. This organization was chosen due to its being one of the organizations that cause significant pollution in Baghdad depending on government reports, which indicate the lack or weak weakness of the procedures taken by the refinery administration to reduce carbon dioxide emissions. The study reached the conclusion that MS mediate the relationship between EA and sustainable development (SD). The EA also has a significant impact on achieving SD. Depending on the bibliometric survey conducted, this study is the first in Iraq, a matter that gives the research a great interest in the field of research on SD topics.

Environmental Auditing, sustainable development, Management Systems, toxic gases, global warming

The concept of “Sustainable Development” is the holy grail of contemporary environment. Critics, planners, and politicians have relied on it to provide credibility to this concept, which is described as a hard target to identify. The word “sustainability” is taken to refer to the global long-term health, therefore, SD is related to enhancing human social and economic well-being in the long term, and what threatens it at the time being is the global warming [1]. The World Commission of Environment and Development in a year 1987 identified the term SD as that which meets the needs of the current generation without compromising the ability of future generations to meet their needs. This definition in the UK Government Policy in 1990 was mixed with the UK SD Strategy for the year 1994. Fulfilling the objectives of SD relies mainly on the integration of economic, environmental, and social objectives [2]. Global warming phenomenon is one of the important phenomena that the whole world is witnessing, as the significant rise in the Earth’s temperature poses a threat with a wide impact at the present time and future. The phenomenon of global warming is not new. In 1920, Fourier found out that this phenomenon is related to the changes occurring in the atmosphere [3]. Throughout ages, the Earth has witnessed many changes, and man has been able to justify most of them due to natural causes, in contrast to changes such as the sudden increase in temperatures in the world, especially in the past two centuries, which scientists could not be able to justify relying on the same natural causes. Human activity and work had the most significant impact during this period, a matter that might justify this rise in temperatures. This rise may have many causes, chief of which was the accumulation of greenhouse gases in the atmosphere and led to climate change [4]. The phenomenon of global warming occurs because of natural factors in addition to other human factors that arise through various industrial human activities. Natural factors can be included due to rising temperatures in the atmosphere surrounding the Earth [5]. The atmosphere has a rise in heat, which leads to a rise in the temperature of the oceans and the Earth's surface [6]. To add more, there is an increase in the number of disasters resulting from environmental and climatic conditions around the world. As far as human factors are concerned, it can be attributed to an increase in fumes and gases from transportation (land, Marine and Air) that occupy the forefront of pollutants that arise because of the internal combustion process of transportation engines (cars), i.e. carbon monoxide and lead compounds, which greatly contribute in large proportions of pollution [6, 7]. The danger of aircraft to the air is also noticeable, especially when regarding the upper atmosphere layers, which are represented by the existence of ozone gas made from the short rays. As for the means of transportation, i.e. (trains), they contribute to air pollution processes through their passing within cities, especially for trains that operate with poor fuel-quality [5, 8]. Fumes rising from industrial institutions may lead to air pollution [9]. Examples of such activities that are made are the manufacturing of metallic materials, the production of fertilizers and organic compounds, wood and forest burning operations, detergent factories, iron and steel factories, factories for the production of acids, salts and gases, and electric power generation stations, in addition to the most important pollutants that affect the atmosphere due to industry, such as (sulfur oxides, carbon compounds, nitrogen, chlorine, water vapor, incompletely combusted particles, phosphorus). This is what has greatly contributed to the rise in atmospheric temperatures because of the high rate of carbon dioxide in it. The rate of temperature rise equaled half a Celsius degree over the past three decades. This acceleration in temperature rise is unnatural and portends major climatic and environmental consequences that will affect the lives of all creatures [10]. What is more, is that there are several negative effects that can be located. They are represented by an increase in the stock of these gases in the atmosphere from 280 - 560 parts per million, which will lead to an increase in the Earth’s temperature at a rate of 3℃ above the natural rates that range between 13℃ - 19℃. The temperatures that will be maintained in the atmosphere will also be high, a matter that may lead to noticeable shifts in weather, and these shifts will have major repercussions and effects that threaten human life on the Earth and their various fields such as those of food, health, sea level, increasing hurricane intensity, ocean acidification [11, 12]. The other impact of global warming that threatens human life is the health impact. The latter can either be directly reflected through floods, pollution, and exposure to different temperatures, or indirectly because of the decline in the individual’s standard of living and the spread of epidemics such as malaria, diarrhea, and malnutrition. There are many forward-looking studies that indicate that if it is impossible to have control over the heat emissions in the coming years, this will affect the seas and oceans, a matter that leads to its acidification because of the dissolution of these gases in it. This in turn will lead to a reduction in the density of calcium carbonate, which is considered as the food for most marine creatures. A rise in sea level over than seven meters in the next fifty years will pose a threat to inhabitants who live near to the coasts. This will call for migration or the construction of dams and sea barriers to be protected from the danger of rising sea levels. Many companies face noticeable pressure from the parties who are concerned with sustainability. They insist on the necessity of maintaining SD by issuing environmental reports acknowledging their commitment to this, especially in oil companies, because of the great importance this sector has for many countries that depend in their economy on oil they produce, and also due to this great role of oil sector on environment and the role of EA in protecting the environment by verifying the environmental reports issued by the company, and to ensure their compliance with environmental legislation. Accordingly, the research problem can be formulated with the following question: What is the role of EA in reducing the fulfillment of SD by reducing the risks of greenhouse gas emissions for oil companies and what are its tools? The importance of the research stems from the importance of the role of EA in reducing the risks resulting from oil companies’ emissions and showing the oil companies compliance to the governmental laws and legislations and global guidelines issued by entities concerned with sustainability in the oil and gas sector. The aim of the research is to determine the cognitive foundations of EA concept and the phenomenon of global warming, let alone being acquainted with the nature of the role of EA in supporting sustainability reports by reducing the negative effects of gas emissions of oil companies. The study also discussed several previous related studies and develop hypotheses. Then We presented the research methodology, implications and finally the conclusions.

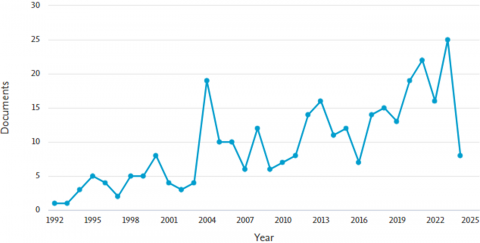

During the last century, interest in EA has emerged [13]. According to the European Union Commission, EA is “an examination process aimed at ensuring the compliance with environmental regulations and ensuring that the data and information given in the environmental list are reliable and that all details have been provided on all important and appropriate environmental issues” [14]. EA is defined under the Environmental Protection Law (EPA) as a systematic, documented, periodic and objective audit process by a regulating body of the company’s operations and practices related to meeting environmental requirements. The definition, identified by the US Environmental Protection Agency mentioned above, indicates that EA includes a systematic, documented, and periodic audit process by those who implement the commercial activities of the companies and practices to meet environmental requirements [15]. As a result, EA can be defined as an organized and objective audit process adopted by the company to follow up on environmental issues that have a significant impact on the efficiency and quality of environmental reports. The aim of EA is to measure the impact of the company’s operations on the environment, via a set of pre-determined standards as much as possible since EA primarily focuses on two areas: assessing the impact of the environmental policies followed by the company through its activities and services and auditing the environmental impacts through conducting analyses and some other actions [16]. Some researchers point to the most important objectives of EA such as examining and auditing the financial statements related to activities and procedures followed by the company for the purpose of protecting and improving the environment and determining the degree of their impact on business results and financial position. To add more, it also aims at examining and evaluating the internal control system and ensuring the validity of the control procedures followed by the company to control the implementation processes of programs established to protect the environment and its activities, in addition to examining the documents and tables that contain the results of laboratory tests and ensuring their conformity with the standards set by laws and instructions [17]. In fact, EA is not a particularly new specialization. However, its popularity as a means of evaluating environmental performance has recently increased significantly [18]. The first compliance audits can be traced back to the USA. Companies adopted this methodology during the early 1970s in response to their local liability laws. The importance of EA has gained significant momentum over the past few years, with the launch of the Environmental Management and Audit System (EMAS) in 1993 and the publication of ISO 14001 in 1996. A great number of companies find it useful to audit their accounts [12]. Surveying the results of the previous studies depending on the bibliometric-analysis method in Scopus databases indicates an increasing number of research papers that examined the relationship between SD and EA. The results show that there were 350 articles indexed in Scopus from the years 1993 to 2024 that investigated this relationship. Figure 1 shows the development of research over the past 33 years.

Figure 1. Annual and cumulative number of research articles in the field of SD and EA

Figure 2. The study distribution among the top 10 countries in the world

Figure 1 shows us the highest percentage of studies in this field was in 2023. Figure 2 on the other hand, shows us the distribution of these studies among the top 10 countries in the world.

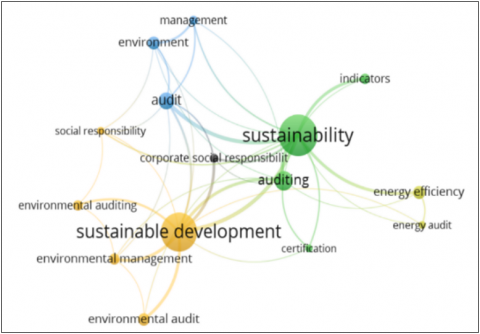

The results indicate that the USA, UK, and China are among the most highly interested countries in this field. When examining any of the keywords that link the research variables, the result appeared as shown in Figure 3.

Figure 3. Bibliometric map analysis based on the number of times the author used the same keywords

It can be seen from Figure 3. It has been divided into five groups. The first group included topics related to environmental and administrative auditing, social responsibility, and SD. This group of keywords included the largest number of studies. The next group focused on the terms of audit and development. The third group was the result of the studies that focused on auditing, environment and development. The penultimate group studied energy and efficiency audits. Finally, the last group focused on the social responsibility of companies. These results encouraged We are to study the mediating role of MS concerning the relationship between EA and SD. EA primarily focuses on two areas, namely assessing the impact of environmental policies adopted by a company through its activities and services and auditing environmental impacts through analysis and specific procedures [16]. Some researchers shed light on the main objectives of EA, including examining and auditing financial statements related to the activities and procedures adopted by the company for the purpose of protecting and improving the environment and also determining their effect on business results and financial position. It also includes examining and evaluating the internal control system and ensuring the accuracy of the control procedures followed by the company to regulate the implementation of programs whose aim is to protect the environment, in addition to reviewing documents and tables that contain the laboratory test results to ensure that they conform to the standards set by laws and regulations [17]. In fact, EA is not a particularly new discipline, but its popularity as a means of assessing environmental performance has recently increased significantly [19, 20]. The initial adoption of compliance audits can be traced back to the USA, where companies adopted this methodology in the early 1970s in response to their own local liability laws. EA-review has gained significant interest in recent years with the launch of the EMAS in 1993 and the publication of ISO 14001 in 1996. An increasing number of companies find it useful to review their environmental impacts [12]. The study [21] investigated the ways to develop EA as a self-regulatory tool in response to the increasing public and business awareness of environmental issues. The study concluded that there is a growing consensus on a wide range of standards included within the types of comprehensive auditing. Conversely, there are some activities that are inappropriately referred to as environmental reviews. It also indicated that the credibility of EA can help stakeholders conduct an evaluation for the companies’ performance in achieving sustainable profits in the future. A study [2] aimed at investigating the relationship between environmental-auditing standards and SD within various supreme audit institutions in developing countries that only meet the requirements of these supreme audit and accounting institutions for SD requirements compared to developed/advanced countries that meet most of those requirements. The study was based on analyzing previous literature, and it came to a result that the SAIs in developing countries are lagging as far as the field of EA is concerned. A study [22] shed light on the role of accounting and EA in fulfilling the SD objectives. The study was based on a questionnaire distributed among a sample of accountants and auditors working in the General Company for Northern Cement and the General Company for Ready-made Garments in Iraq. Their number reached 40 people. It was concluded here that environmental disclosure plays a role in supporting SD via notifying company management and relevant parties of the extent of depletion of natural resources resulting from the company’s work, and that the participation of the environmental accounting system contributes to achieving the requirements of measuring development within the national accounts. A study [23] investigated the role of environmental managerial accounting in oil refinery factories in northern Iraq. The study was conducted depending on a questionnaire, i.e. by interviewing accountants, auditors, and members of the board of directors, numbering 57 people. The study concluded that there are many positive reasons for applying environmental managerial Accounting to raise the level of SD. A study [24] aimed to identify the current and emerging issues for the role of EA in achieving SD. The study was based on the analysis of previous knowledge contributions and interviews with auditors. It was concluded here that the Supreme Audit and Accounting Institutions contributed to providing more guidance related to auditing standards and requirements through developing the procedures that ensure compliance with legal rules for environmental standards and requirements, let alone their important role in training auditors, a matter that helps in providing them with the skills and knowledge necessary for effectively responding to the complex changing environmental issues. A study [25] aimed at providing a strategic perspective on how to use Artificial Intelligence (AI) in conducting EA on a group of companies in Middle Asia with the aim of enhancing EA in achieving a sustainable future. The study concluded that it was necessary to use artificial intelligence in the effective implementation of laws that protect the environment from global warming. A study [26] investigated the role of EA in improving environmental quality. We have used a sample of data collected from 76 Chinese cities for the period from 2006 to 2017. The study concluded that the general impact of EA on water quality was positive, though not important. The study did not find out or identify the role of municipal councils in reducing pollution sources and improving water quality fundamentally. It was suggested here that strengthening EA might contribute to increasing the regulation-reinforcement and constantly improving water quality. A study [27] tackled the requirements that policy makers, financial parties, and investors from the public and private sectors need in order to increase financial flows aiming at achieving SD goals. The study concluded that resources represented by labor, equipment, and technology played a fundamental role in addressing the climate crisis and achieving SD-objectives. A study [28] aimed to evaluate the reality of the SD agenda in Iraq. The study concluded that Iraq could fulfill its objectives and society’s aspirations in keeping pace with the global development movement in the areas of SD through its governmental plans and programs, its sectorial strategies, and national reports concerning sustainable human development. A study [29] searched the extent of companies’ compliance with the principles of SD. The study employed a group of 131 Ukrainian companies for the year 2020. The study reached a conclusion that SD activities should be appropriate to ensure effective implementation or compliance with the objectives of SD. The management's effective approach to implementing the SD objectives is based on coordination with sub-systems to support information, control, analysis, planning and motivation for the comprehensive implementation of specific functions. A study [30] aimed at demonstrating the impact of applying green Accounting on SD in companies that have a significant impact on pollution. The study employed a group of 212 Bangladeshi companies listed on the Dhaka Stock Exchange for the period 2010 - 2019. The study concluded that the effective implementation of green Accounting led to a significant improvement in the SD capabilities of highly polluting companies. To add more, there was a statistically significant positive relationship between the quality of disclosure about the social responsibility information and SD capabilities. A study [31] investigated the practices of disclosing SD objectives. Dependence for measuring environmental performance was on throughout three sustainability-indicators: emissions, environmental innovation, and resource employment. The study sample included 336 companies affiliated with the EusToxx600 stock indices for the period 2010-2020. It was concluded that limited disclosure of SD objectives could lead to better environmental performance in light of voluntary sustainability reporting. A study [32] developed a model for managing profits that guarantees total profits, target income, and surplus to investigate the possibility of sustaining profits. The study sample included a group of joint-stock companies during the year 2022. The study concluded that external incentives had an important role in affecting companies to contribute to fulfilling sustainability. Depending on what was presented in previous literature, we hypothesize the following:

H1. EA has a significant effect on SD.

H2. EA has a significant effect on MS.

H3. MS has a significant effect on SD.

H4. MS can mediate the effect of EA on SD.

3.1 Sample

The research community is represented by Iraqi Oil and Gas Companies, while the research sample is restricted to Daura refinery. The reasons behind the choice of this refinery are that in its mission, this refinery seeks to make quality, continuous improvement, and creativity a daily-work culture, a matter that contributes to achieving its objectives in occupying a recognizable position among refineries locally and globally. Despite this, this organization is considered one of the organizations that cause significant pollution in Baghdad according to the governmental reports, which point out the weakness of the procedures taken by the refinery management to reduce carbon dioxide emissions. To measure the variables of the study, a questionnaire was distributed among a group of 155 workers in this refinery under study. The questionnaire included 27 questions distributed among three axes. The one was devoted to questions related to EA. The next axis was related to SD, while the last one included MS. The following Table 1 shows a description of the sample characteristics:

Table 1. Sample characteristics description

|

Sample |

Details |

Number |

Ratio |

|

Gender |

Female |

40 |

25.81% |

|

Male |

115 |

74.19% |

|

|

Certificate |

Bachelor’s degree |

96 |

61.94% |

|

Diploma |

35 |

22.58% |

|

|

Master’s degree |

20 |

12.90% |

|

|

PhD |

4 |

2.58% |

|

|

Experience |

Less than 5 years |

7 |

4.52% |

|

From 5 to 10 years |

26 |

16.77% |

|

|

from 11 to 15 years 15 |

44 |

28.39% |

|

|

from 16 to 20 years 20 |

49 |

31.61% |

|

|

From 21 to 25 years 25 |

21 |

13.55% |

|

|

From 26 years and over |

8 |

5.16% |

|

|

Specialization |

Accountant |

21 |

13.55% |

|

auditor |

19 |

12.26% |

|

|

Administrative employee |

75 |

48.39% |

|

|

IT |

18 |

11.61% |

|

|

other |

22 |

14.19% |

3.2 Methods of variables measurement

The descriptive approach was relied upon in investigating the role of EA in reducing the negative effects of the Doura refinery through showing the extent to which it complies with the laws, standards and guidelines issued by the authorities concerned with environmental sustainability. The study also relied on a questionnaire form that was designed depending on several studies. Table 2 below clarifies the designing process of the questionnaire form:

Table 2. Method of measuring variables

|

Source |

Variables |

No. |

|

[23, 25] |

EA |

1 |

|

[33] |

SD |

2 |

|

[34-36] |

MS |

3 |

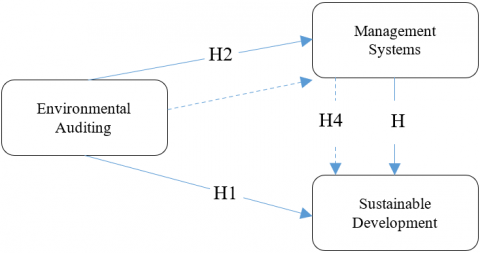

Figure 4 shows the model of the study.

Figure 4. The model of study

4.1 Descriptive statistics

The study aimed to measure the overall impact of EA on SD within the framework of an intermediary model in which MS plays an intermediary role. Reliance in building the study-model was on four models. The first one included a study of measuring the impact of EA in SD. The next was to measure the impact of MS on development. The penultimate model was to measure the impact of EA on MS. Finally, reliance was on structural equation modeling to measure the mediating role of MS in the relationship between EA and SD. To make sure of the model reliability and suitability before conducting the statistical analysis, it was necessary to ensure the validity of the statistical tests through goodness-of-fit tests for the structural model, in order to confirm the stability of the statistical model design or the presence of a weakness in the proposed model. Depending on (Model Fit Summary Test), results indicate that the CMIM for the Default model was 0.000, and the CFI value was 1.000, while the RMSEA value was not calculated from the program because the value of (Chi-square=.000). Depending on the results, we have concluded that the proposed model has great power and has the possibility of analyzing the results. Table 3 below displays the results of descriptive statistics for the variables.

Table 3. Descriptive statistics results

|

Descriptive Statistics |

EA |

SD |

MS |

|

|

N |

Valid |

155 |

155 |

155 |

|

Missing |

0 |

0 |

0 |

|

|

Mean |

4.61 |

4.46 |

4.39 |

|

|

Std. Deviation |

.43 |

.42 |

.47 |

|

Table 4. Correlations among variables

|

Correlation |

1 |

2 |

3 |

|

|

1 |

EA |

1.000 |

|

|

|

Sig. |

||||

|

2 |

SD |

0.334** |

1.000 |

|

|

Sig. |

0.000 |

|||

|

3 |

MS |

0.241** |

0.378** |

1.000 |

|

Sig. |

0.003 |

0.000 |

||

Results indicated in Table 3 show that the value of the arithmetic mean for EA, the administrative system, and SD was 4.6, 4.3 and 4.4, respectively, which is greater than the weighted arithmetic mean of 3, with a standard deviation of 0.43, 0.42, and 0.47, respectively, which indicate low dispersion in the sample members’ answers. Table 2 displays the descriptive statistics for the correlation between the variables.

The results in Table 4 indicate that the relationship between EA and SD was significant, reaching a level of 0.000 with a significant level of 0.01, while the correlation was positive though weak since the Spearman test coefficient reached a value of 0.33. As for the value of the correlation between EA and MS at a level of significance 0.003, which is also a significant correlation, the strength of the relationship was also weak, as the correlation coefficient reached 0.24, and at the same time, it is also positive. Finally, the value of the correlation between MS and SD was significant at the level of 0.000, and the value of the correlation was also weak, as it reached 0.37. Despite the correlation between the variables, the results were weak, but, they were positive. Therefore, other tests related to measuring regression can be conducted to judge the extent of the level of influence of the variables among them.

4.2 Inferential statistics for the structural model

Table 5 shows the results of studying the relationship among the three variables with the aim of determining the amount of the relationship directly or indirectly through the variable of MS as a mediator in the relationship between EA and SD, which can be noticed in Table 5.

Table 5. Testing the relationship among variables for the structural model

|

Hypothesis |

Dep. Variable |

Path |

Ind. Variable |

Estimate |

R2 |

F |

C.R. |

P |

|

H1 |

MS |

<--- |

EA |

.300 |

0.07 |

12.4 |

3.539 |

*** |

|

H2 |

SD |

<--- |

EA |

.293 |

0.16 |

29.5 |

4.284 |

*** |

|

H3 |

SD |

<--- |

MS |

.312 |

0.19 |

36.4 |

4.989 |

*** |

Notes: - ***, ** and * are significant at the 1%, 5% and 10% levels respectively.

The above table clarifies the following:

4.2.1 Relationship between EA and MS

The results for the third model indicate that the value of R2 was 0.07, which means that EA affects MS by 7%, while the remaining value of 93% is due to other contributions that were not studied here, The P value of 12.4 indicates that it is greater than the tabular value of 4.19. which indicates the effect of the explanatory variable on the dependent variable, and the beta coefficient value of 0.3 indicates that any change in the explanatory variable by one unit, the dependent variable will be affected by 30%, while the result of the effect size has been statistically complete, which amounted to (***). Accordingly, the model quality can be judged and the existence of an influential relationship for EA in MS. The result of (C.R) indicates that it was greater than the standard value of (1.94), which also indicates the strength of the model.

4.2.2 Relationship between EA and SD

The results for the first model indicate that the value of R2 was 0.16, which means that EA affects SD by 16%, while the remaining value of 84% is due to other contributions that were not studied in the study model. The P value of 29.5 indicates that it is greater than the tabular value of 4.19. which indicates the effect of the explanatory variable on the dependent variable. Beta coefficient value of 0.29 has indicated that any change in the explanatory variable by one unit, the dependent variable will be affected by 29%, while the result of the effect size was statistically complete, which amounted to (***), and therefore the quality of the model and the existence of an influential relationship for EA in SD can be judged. The result of (C.R) indicates that it was greater than the standard value of 1.94, which also indicates the strength of the model. This result is consistent with the findings of the study (Hillary, 1998).

4.2.3 Relationship between MS and SD

The results for the second model indicate that the value of R2 was 0.19, which means that EA affects SD by 19%, while the remaining value of 81% is attributed to other contributions that were not studied here. The P value of 36.4 indicates that it is greater than the tabulated value of 4.19. Which indicates the effect of the explanatory variable on the dependent variable, and the beta coefficient value of 0.38 indicated that with any change in the explanatory variable by one unit, the dependent variable will be affected by 38%, while the result of the effect size was statistically complete, which amounted to (***). Accordingly, the quality of the model and the existence of an influential relationship for EA in SD can be judged. The result of (C.R) indicates that it was greater than the standard value of 1.94, which also indicates the strength of the model.

4.2.4 Relationship among EA, MS, and SD

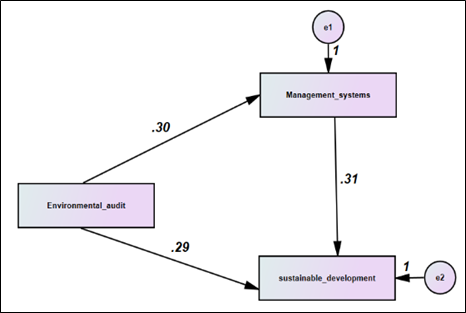

Below is the final structural equation model shown in Figure 5.

Figure 5. Structural model: EA, SD, and MS as a mediating variable

To test mediation, the path must be divided into two parts. The first part is related to the Baron & Kenny test through three paths. The first path is the effect of the independent variable (X) on the proposed mediator variable (M). The second path is the effect of the mediator variable (M). on the dependent variable (Y). Finally, the third path is represented by the effect of the independent variable (X) on the dependent variable (Y). The other part is represented by determining the extent of the presence of complete or partial mediation or the absence of mediation by determining the direct and indirect effect of EA on SD through the mediation of MS, a process that aims at verifying the acceptance or rejection of the main hypothesis of the study regarding the mediating role between the independent and dependent variables.

Table 6. Barron's and Kenny's approach to testing mediation of the structural model

|

F |

R2 |

Type of Mediation |

X $\rightarrow$ Y |

M $\rightarrow$ Y |

X $\rightarrow$ M |

Paths |

||

|

29.33 |

0.27 |

Complete |

0.097*** |

0.29*** |

0.30*** |

SD |

MS$\rightarrow$ |

EA$\rightarrow$ |

Notes: - ***, ** and * are significant at the 1%, 5% and 10% levels respectively

Depending on the results in Table 6, we note that the mediating role is achieved due to the presence of an effect (statistical significance) in the first and second paths together, which means that the variable (M) enjoys complete mediation. The table below shows the results of Barron's and Kenny's test to test the mediation of the model. The results for the fourth model indicate that the value of R2 reached 0.27, which means that EA affects SD by mediating MS by 27%, while the remaining value of 73% is attributed to other contributions that were not studied in the study model. The F value of 29.33 indicates that it is greater than the tabular value, which is 4.19, a matter that indicates the effect of an independent, mediating relationship that affects the dependent variable. The value of the beta coefficient is 0.29. Any change in the explanatory variable by mediating the relationship between the two variables with one unit, the dependent variable will be affected by 29%, while the result of the model was statistically complete, which amounted to 0.000. Accordingly, the quality of the model and the existence of an influential relationship of EA in SD can be judged. It can be noted from the results of the previous models that the mediation of the relationship has contributed with an effect of 11% when mediating the relationship of MS between EA and SD. This means that the fourth model reflects the best combination of the relationship between the variables compared to the three models, and this indicates the effective role of MS in the influential relationship to the role of EA in achieving SD.

The past decades have witnessed major violations in the field of the emission of pollutants of various types resulting from the increasing number and size of population. International reports indicate that Iraq is among the countries that are mostly affected by global warming and the subsequent increase in the number of factories and human exploitation of natural resources exported by fossil fuels and their multiple operations starting from exploration, drilling, extraction, then storage, transportation, refining, and finally use, and the great risks these operations cause, which have led to an increase in the phenomenon of global warming. All of these reasons call for attention to sustainability issues to ensure that future generations’ share of living in a clean environment. In addition, as regulated society continues to expect an increase in environmental issues related to regulation, it is the suitable time to apply risk-management tools to have protection against potential liabilities and to ensure compliance with environmental laws and regulations and to develop a reliable program of environmental compliance which includes regular internal EA of the business unit and its operations. Therefore, we are interest was based on what was stated before concerning the role that EA plays in monitoring and reducing greenhouse gases.

EA is one of the tools for implementing environmental management concepts. EA procedures are mandatory for activities that might likely not comply with environmental requirements. Despite the important status of EA in the Environmental Management Law, it is a means of implementing the law, and even though EA essentially evaluates the environmental performance of the refinery. Because it is the process by which EA can be conducted on specific operational areas to assess their effectiveness and compliance with environmental rules and regulations. EA are conducted to ensure that companies are doing what they can to preserve the environment. It has been concluded that EA, represented by the procedures undertaken by the audit committees of the Federal Office of Financial Supervision at Baiji Refinery in following up on the procedures to reduce carbon dioxide emissions. Submitting reports concerning this to government agencies, contributes effectively to reducing pollutants, and thus contributes to achieving SD. It has been noted, via reviewing the reports that the number of emissions increased even though they were among the environmental limits according to the Iraqi laws. The reason here is due to the impact of fuel combustion processes from refining furnaces and other industrial activities. Therefore, the government is required to reconsider the formulation of the laws and update them due to the damage caused by the refinery.

[1] Barton, H., Bruder, N. (2014). A Guide to Local Environmental Auditing. Routledge.

[2] Jamtsho, C. (2005). Environmental auditing and sustainable development from the perspective of a government auditing. Doctoral dissertation, School of Environmental Sciences, University of East Anglia.

[3] Mavengere, N.B. (2013). Information technology role in supply chain’s strategic agility. International Journal of Agile Systems and Management, 6(1): 7-24. https://doi.org/10.1504/IJASM.2013.052209

[4] Maseer, R.W., Zghair, N.G., Flayyih, H.H. (2022). Relationship between cost reduction and reevaluating customers’ desires: The mediating role of sustainable development. International Journal of Economics and Finance Studies, 14(4): 330-344. https://doi.org/10.34109/ijefs.20220116

[5] Hadi, H.A., Flayyih, H.H. (2024). Analysis of the accounting financial performance of private listed banks in the emerging market for the period 2010-2022. Corporate and Business Strategy Review, 5(1): 8-15. https://doi.org/10.22495/cbsrv5i1art1

[6] Dulias, R. (2022). Anthropogenic and natural factors influencing African World Heritage sites. Environmental & Socio-Economic Studies, 10(3): 67-84.

[7] Abdulzahra, A.N., Al-shiblawi, G.A.K., Flayyih, H.H., Elaigwu, M., Abdulmalik, S.O., Talab, H.R., Audu, F. (2023). Corporate governance towards sustainability performance quality: A case of listed firms in Malaysia. Journal of Information Systems Engineering and Management, 8(4): 22882. https://doi.org/10.55267/iadt.07.14051

[8] Huss, A., Spoerri, A., Egger, M., Röösli, M., Group, S.N.C.S. (2010). Aircraft noise, air pollution, and mortality from myocardial infarction. Epidemiology, 21(6): 829-836. https://doi.org/10.1097/EDE.0b013e3181f4e634

[9] Baumbach, G. (2012). Air Quality Control: Formation and Sources, Dispersion, Characteristics and Impact of Air Pollutants—Measuring Methods, Techniques for Reduction of Emissions and Regulations for Air Quality Control. Springer Science & Business Media.

[10] Hansen, J., Johnson, D., Lacis, A., Lebedeff, S., Lee, P., Rind, D., Russell, G. (1981). Climate impact of increasing atmospheric carbon dioxide. Science, 213(4511): 957-966. https://doi.org/10.1126/science.213.4511.957

[11] Akbaş, H.E., Canikli, S. (2018). Determinants of voluntary greenhouse gas emission disclosure: An empirical investigation on Turkish firms. Sustainability, 11(1): 107. https://doi.org/10.3390/su11010107

[12] Hansen, J., Sato, M., Kharecha, P., et al. (2008). Target atmospheric CO2: Where should humanity aim? arXiv preprint arXiv:0804.1126. https://doi.org/10.2174/1874282300802010217

[13] Lewis, L. (2000). Environmental audits in local government: A useful means to progress in sustainable development. Accounting Forum, 24(3): 296-318. https://doi.org/10.1111/1467-6303.00043

[14] Sakhr, N.H., Hamad, M.K. (2019). The role of environmental auditing in achieving the sustainable development goals-a suggested model. AL-Anbar University Journal of Economic and Administration Sciences, 11(27): 474-494.

[15] Hakim, W., Yunus, A. (2017). Environmental audit as instrument for environmental protectioan and management. The Business & Management Review, 9(2): 228-232.

[16] Maria, R. (2012). Corporate governance, internal audit and environmental audit-the performance tools in Romanian companies. Accounting and Management Information Systems, 11(1): 112.

[17] Shariqi, O., Brahimi, L. (2017). The role of environmental auditing in achieving sustainable development goals. Journal of Development Studies and Research, 4(1): 107-124.

[18] Hasan, S.I., Saeed, H.S., Al-Abedi, T.K., Flayyih, H.H. (2023). The role of target cost management approach in reducing costs for the achievement of competitive advantage as a mediator: An applied study of the iraqi electrical industry. International Journal of Economics and Finance Studies, 15(2): 214-230. https://doi.org/10.34109/ijefs.202315211

[19] Welford, R. (2004). Corporate social responsibility in Europe and Asia: Critical elements and best practice. Journal of Corporate Citizenship, 13: 31-47.

[20] Flayyih, H.H., Khiari, W. (2023). Empirically measuring the impact of corporate social responsibility on earnings management in listed banks of the Iraqi stock exchange: The mediating role of corporate governance. Industrial Engineering & Management Systems, 22(3): 273-286. https://doi.org/10.7232/iems.2023.22.3.273

[21] Hillary, R. (1998). Environmental auditing: Concepts, methods and developments. International Journal of Auditing, 2(1): 71-85. https://doi.org/10.1111/1099-1123.00031

[22] Hussein, A.W.G.M. (2014). The role of environmental accounting and environmental audit in the activation of sustainable development (Study of the views of a sample of accountants and auditors. Tikrit Journal of Administration and Economics Sciences, 10(32): 304-318.

[23] Thabit, T.H., Ibraheem, L.K. (2019). Implementation of environmental management accounting for enhancing the sustainable development in Iraqi oil refining companies introduction. https://ssrn.com/abstract=3401086.

[24] Wanyonyi, A.W. (2020). An insight into the emerging issues, challenges and future prospects in environmental audit. https://ssrn.com/abstract=3628412.

[25] Younas, A., Younas, R. (2020). Regulations for environmental audit and artificial intelligence: A strategic perspective for central Asia.

[26] Xu, Z., Dai, Y., Liu, W. (2022). Does environmental audit help to improve water quality? Evidence from the China national environmental monitoring centre. Science of the Total Environment, 823: 153485. https://doi.org/10.1016/j.scitotenv.2022.153485

[27] Lagoarde-Segot, T. (2020). Financing the sustainable development goals. Sustainability, 12(7): 2775. https://doi.org/10.3390/su12072775

[28] Abdel, N.H.G.R.A. (2021). Evaluate the sustainable development agenda 2030 in Iraq for the period 2018-2020. Journal of Sustainable Studies, 3(3(3)): 20-45.

[29] Dohadailo, Y., Kyrchata, I., Kovalova, T., Dmytriiev, I., Lošonczi, P. (2021). Continuous CVP-analysis as a key tool of anti-crisis management of an enterprise in the conditions of sustainable development in the VUCA-world. In Problems and Prospects of Development of the Road Transport Complex: Financing, Management, Innovation, Quality, Safety - Integrated Approach, pp. 81-95. https://doi.org/10.15587/978-617-7319-45-9.CH6

[30] Dhar, B.K., Sarkar, S.M., Ayittey, F.K. (2022). Impact of social responsibility disclosure between implementation of green accounting and sustainable development: A study on heavily polluting companies in Bangladesh. Corporate Social Responsibility and Environmental Management, 29(1): 71-78. https://doi.org/10.1002/csr.2174

[31] Pisciella, A., Melloni, G. (2023). Accounting for sustainable development goals: Evidence on environmental performance of European companies.

[32] Ozili, P.K. (2023). Earnings management for sustainability: The surplus income model of sustainable development. In Smart Analytics, Artificial Intelligence and Sustainable Performance Management in a Global Digitalised Economy, pp. 145-158. https://doi.org/10.1108/S1569-37592023000110B009

[33] Ahmad, S.A., Sulaiman, G.A. (2023). The role of attributes based costing technology in achieving sustainable development goals. International Journal of Professional Business Review, 8(2): 8. https://doi.org/10.26668/businessreview/2023.v8i2.1105

[34] Cash, D.W., Clark, W.C., Alcock, F., et al. (2003). Knowledge systems for sustainable development. Proceedings of the National Academy of Sciences, 100(14): 8086-8091. https://doi.org/10.1073/pnas.1231332100

[35] Guarini, E., Mori, E., Zuffada, E. (2022). Localizing the sustainable development goals: A managerial perspective. Journal of Public Budgeting, Accounting & Financial Management, 34(5): 583-601. https://doi.org/10.1108/JPBAFM-02-2021-0031

[36] Popescu, L., Iancu, A., Avram, M., Avram, D., Popescu, V. (2020). The role of managerial skills in the sustainable development of SMEs in Mehedinti County, Romania. Sustainability, 12(3): 1119. https://doi.org/10.3390/su12031119