Theresia Woro Damayanti*![]() | Supramono Supramono

| Supramono Supramono![]() | Ika Kristianti

| Ika Kristianti![]() | Dhian Adhitya

| Dhian Adhitya![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study examines the effect of entrepreneurial capacity, both directly and indirectly, through entrepreneurial characteristics on the performance recovery speed of Micro, Small, and Medium Enterprises (MSME) due to the COVID-19 pandemic. The entrepreneurial capacity consists of financial access and market access. Meanwhile, entrepreneurial characteristics include the need for achievement, risk-taking propensity, and internal locus of control. The data were obtained through a field survey of MSME entrepreneurs engaged in the food and beverage sector in three cities including; Semarang, Surakarta, and Salatiga, Indonesia. The total sample was 397 respondents and used SEM-PLS analysis to test the hypothesis. This study shows that financial access, the need for achievement, and the internal locus of control positively affect MSMEs' performance recovery speed after the COVID-19 pandemic. Furthermore, the mediating effect testing demonstrates that the need for achievement and internal locus of control mediate the effect of financial access on the performance recovery speed of MSMEs. Therefore, stakeholders interested in developing the MSMEs are suggested to intensify their efforts to increase their ability to access finance and strengthen the entrepreneurial characteristics among the MSME entrepreneurs.

performance recovery speed, entrepreneurial capacity, entrepreneurial characteristics, MSME, pandemic impact

The COVID-19 pandemic caused an economic downturn, which harmed the business world, particularly MSMEs, as they have lower cost resilience and flexibility than big companies [1], limited cash reserves, and the absence of risk management systems in place [2]. Many MSMEs closed their business due to the COVID-19 pandemic [3, 4]. However, several MSMEs can still sustain themselves despite various issues such as decreased income [5] and liquidity difficulties [6].

The issue of accelerating the recovery of MSME performance due to the impact of the COVID-19 pandemic is a serious concern for developing countries, including Indonesia. The MSMEs in Indonesia account for 99.99% of total business units, absorb 96.92% of the workforce, and contribute 60.51% to the gross domestic product (GDP). COVID-19 has had a significant impact on the performance of MSMEs in Indonesia. For example, in 2020, 55.2% of MSMEs in Indonesia experienced a decline in sales, 36.7% experienced no sales during the pandemic [7] and there was a decline in income of around 30%-50% [8].

The Indonesian government has implemented various policies, including health and economic policies, both fiscal and monetary [9]. The speed of efforts to restore MSME performance certainly does not only depend on the measures taken by the government but also may be inseparable from the entrepreneurial capacity of the MSME entrepreneurs themselves, which is indicated, among other things, by their abilities to access finance [10, 11] and market [12]. To the best of our knowledge, there have been no studies that have paid attention to the determinants of the speed of recovery in MSME performance. Previous studies examining MSMEs as objects paid more attention to examining the impact of the COVID-19 pandemic [3, 4, 13] and the strategies used to deal with the COVID-19 pandemic [14, 15].

MSMEs currently lack the availability of financing because of their limited financing access [16]. Meanwhile, prior studies in some countries, such as Malaysia, Tanzania, and South Eastern Europe, demonstrate that financing access positively affects MSMEs’ performance [17-19]. Further, MSMEs’ entrepreneurial capacity to maintain their consumers by expanding their markets through innovative marketing (e.g., e-commerce and digital marketing) is equally essential for MSMEs' performance [11]. Hence, it is crucial to analyze how MSMEs' entrepreneurial capacity, such as financing and market access, contribute to the speed of their performance recovery.

Prior studies also showed that entrepreneurial capacity is associated with entrepreneurial characteristics. The MSME entrepreneurs’ entrepreneurial characteristics include the need for achievement, risk-taking propensity, and internal locus of control [20]. For example, Ahmad et al. [21] and Firnalista et al. [22] observe that access to finance is related to entrepreneurial characteristics. Another study documents that market access, like innovative marketing, is associated with entrepreneurial characteristics [23]. Therefore, entrepreneurial capacity is arguably associated with the speed of MSMEs’ performance recovery directly and indirectly through entrepreneurial characteristics.

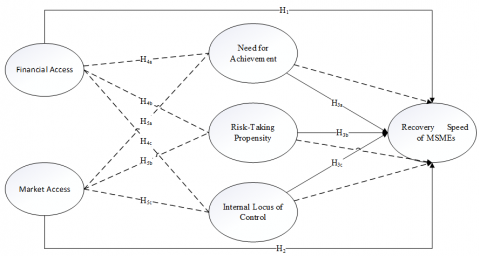

This present study aims to develop a model for the performance recovery speed of MSME based on entrepreneurial capacity and entrepreneurial characteristics by responding to the following research questions: (a) Does financial access and market access affect the performance recovery speed of MSME?; (b) Do the need for achievement, risk-taking propensity, and internal locus of control affect performance recovery speed of MSME?; and (c) Can the need for achievement, risk-taking propensity, and internal locus of control mediate the effect of financial access and market access on performance recovery speed of MSME?

This study contributes to the development literature in three ways. First, initiate a study of the performance recovery speed of MSMEs after the COVID-19 pandemic. Second, this study combines entrepreneurial capacity and entrepreneurial characteristics, while previous studies explain separately entrepreneurial capacity [24, 25] and entrepreneurial characteristics [26, 27]. Third, this present study investigates the previously unstudied mediating effect of entrepreneurial characteristics on the influence of entrepreneurial capacity on the performance recovery speed of MSMEs.

The entrepreneurial capacity is frequently referred to as the key to successful company performance, including the MSMEs [28]. It is related to individual abilities [29], entrepreneurial skills, and professional competence [30] and is a source that keeps the entrepreneurial spirit alive [31]. Furthermore, according to the resources and capability theory, entrepreneurial capacity is a corporate asset that can be the foundation for long-term competitive advantage. Financial access and market access are entrepreneurial capacities that the MSME entrepreneurs must possess in the context of MSMEs, given that the main constraints to MSME growth frequently raised in the literature are related to aspects of financing and marketing.

In this context, financial access refers to the entrepreneurs' ability to obtain financial institution services [32], particularly for the benefit of financing sources. It has been shown to boost the growth of MSMEs. Adequacy of financial resources influences the sustainability and growth of SMEs. Especially at the start of a business or SME development, financial resources are an essential basis for ensuring the performance and success of SMEs [33]. Furthermore, it enables the MSMEs in developing countries to invest and expand their businesses, allowing them to adopt cutting-edge technology to boost competitiveness and encourage innovation [34], job creation, profitability, efficiency, exports, productivity, and return on assets [35]. Thus, MSMEs with better financial access can continue operating normally and conducting marketing activities during the COVID-19 pandemic. As a result, their performance, which has suffered due to the COVID-19 pandemic, is expected to improve more quickly. Therefore, the first hypothesis is formulated as follows:

H1: Financial access has a positive effect on the performance recovery speed of MSME

During the COVID-19 pandemic, MSMEs need to develop their dynamic capability consisting of sensing, seizing opportunities, and transforming resource configurations [36]. The dimensions of sensing include being able to seek new market segments and business opportunities. Further, seizing opportunities is related to the ability to produce something according to consumer needs. Meanwhile, transforming resource configurations is related to managing the business adaptively to changes, including innovative marketing [37, 38]. This innovative marketing is closely related to the access to the market – the MSME entrepreneurs' ability to communicate their products and deliver them quickly. Amid shifts in market behavior characterized, among others, by a significantly increased preference for online shopping and speed of delivery, digital technology-based market access is required. According to previous studies, using digital technology and internet resources will help the industry survive and grow [36, 39]. MSMEs that innovate and invest in digital development have a higher level of performance compared to MSMEs that do not invest in innovation [40]. In addition, a healthy lifestyle has also become another shift so that MSMEs in the food and beverage industries can produce hygienic products [41]. Thus, the MSMEs that gain market access through digital marketing, which potentially experience a decline in their performance due to COVID-19, will experience faster recovery and improvement. For this reason, the second hypothesis is formulated as follows:

H2: Market access has a positive effect on the performance recovery speed of MSME

The MSME entrepreneurs have distinctive characteristics that distinguish them from one another [20]. Psychologists say distinct psychological characteristics differ in cognitive and entrepreneurial values [42]. This study focuses on the following psychological characteristics commonly associated with entrepreneurial characteristics: the need for achievement, risk-taking propensity, and internal locus of control [20]. These entrepreneurial characteristics can be innate in an entrepreneur, but they can also be learned and developed through education and training [43].

Need for achievement refers to the extent to which individuals set their goals and put their efforts into achieving these objectives and the extent to which they work hard and are satisfied with their results [44]. An increase in the desire to succeed will boost business performance [45]. Meanwhile, the risk-taking propensity is related to an individual’s willingness to take risks that may result in a loss [20]. Previous studies have found a positive association between the need for achievement, risk-taking propensity, and MSME performance [46].

Furthermore, the internal locus of control is another entrepreneurial characteristic, referring to a psychological characteristic related to the individual's belief that he can control the causes of events in his life [47]. If a person's achievements and failures in life are more controlled by his behavior (internal factors) instead of external factors such as the influence of other people, chances, luck, and fate [48], then he has a high internal locus of control. Psychology literature mentions that the internal locus of control describes how individuals associate results with their internal factors, like efforts and talents, or external ones, like luck [49]. People with an internal locus of control believe they can control their fate and environment [50]. Individuals with an external locus, on the other hand, are susceptible to external influences [50]. Previous studies also documented the significant positive association between the internal locus of control and business performance [45]. Considering the above elaboration, the three entrepreneurial characteristics are also thought to have the potential to accelerate the recovery of MSME performance. Therefore, the sub-hypotheses are formulated as follows:

H3a: The need for achievement has a positive effect on the performance recovery speed of MSME

H3b: The risk-taking propensity has a positive effect on the performance recovery speed of MSME

H3c: The internal locus of control has a positive effect on the performance recovery speed of MSME

The main issue impeding the MSMEs' progress, as frequently mentioned in the financial literature, is a lack of internal financing [9, 34, 51]. As a result, the MSMEs require financial access to improve their internal financial conditions [52]. The MSME entrepreneurs, who believe they have good financial access, are likely to be dissatisfied with what has been accomplished and should be challenged to continue to increase their business growth, dare to incur losses while operating during a pandemic, and have the self-confidence to succeed. Several studies have also shown that financial access improves these entrepreneurial characteristics [22, 53]. The entrepreneurial characteristics, in turn, are expected to positively affect the speed at which MSMEs recover from the COVID-19 pandemic. For this reason, financial access can influence the performance recovery speed of MSMEs through entrepreneurial characteristics. Thus, the sub-hypotheses that can be proposed are as follows:

H4a: The need for achievement mediates the positive effect of financial access on the performance recovery speed of MSME

H4b: The risk-taking propensity mediates the positive effect of financial access on the performance recovery speed of MSME

H4c: The internal locus of control mediates the positive effect of financial access on the performance recovery speed of MSME

In reality, MSMEs face several market-related challenges, including increased competition, rapid changes in market tastes, and the use of technology for marketing activities [54]. Several innovative marketing communication media, such as digital marketing [55] and social media, have proven effective in improving MSME performance. Previous studies showed that market access has a positive relationship with entrepreneurial characteristics [23], which is expected to affect the performance recovery speed of MSMEs due to the COVID-19 pandemic. For this reason, market access is likely to influence MSME performance through entrepreneurial characteristics.

H5a: The need for achievement mediates the positive effect of market access on the performance recovery speed of MSME

H5b: The risk-taking propensity mediates the positive effect of market access on the performance recovery speed of MSME

H5c: The internal locus of control mediates the positive effect of market access on the performance recovery speed of MSME

Figure 1. Conceptual model

3.1 Measurement

This study has one exogenous variable: the performance recovery speed of MSME measured by the time it took to recover the number of customers, sales turnover, and profit. A question was posed: "Has the business recovered in terms of sales?" There were eight possible answers: (a) recovered six months ago; (b) recovered 6-12 months ago; (c) recovered 1-1.5 years ago; (d) recovered early in the pandemic; (e) will recover in the next six months; (f) will recover in the next 6-12 months; (g) will recover in the next 1-1.5 years; and (h) do not know yet. A similar question was applied to the sales turnover and profit. Furthermore, there are five endogenous variables for entrepreneurial capacity, including financial and market access variables. Meanwhile, variables of the need for achievement, risk-taking propensity, and internal locus of control comprised entrepreneurial characteristics. All endogenous variables were measured with seven-point intervals, where '1' denotes strongly disagree and '7' denotes strongly agree.

This study attempts to develop the measure of financial access as a variable based on the definition of [32]. The financial access was measured by six questionnaire items emphasizing whether the participants have a relationship with a banking institution, are frequently visited by financial institutions, have sufficient credit guarantee, have enough amount of income to repay, have no difficulties in obtaining credit, and have an understanding of credit terms. Similarly, the market access variable must also be measured. Market access refers to the ability to communicate product values and deliver the products to consumers through innovative marketing. This study was measured by six questionnaire items emphasizing whether the participants can provide delivery services through digital platforms or outside the digital platforms, the ability to provide e-money payment services, employ online promotions, and the ability to use social media and instant messaging applications (such as WhatsApp) in marketing.

Several alternative constructs for measuring entrepreneurial characteristics have been developed in previous studies. However, to our best knowledge, none focuses on MSMEs' performance during the COVID-19 pandemic. Hence, this study also aims to develop its measure based on the existing definitions. The need for achievement, operationally defined as the entrepreneurs' desire to set high targets and work hard to achieve them, was measured through questionnaire items asking the participants whether they are satisfied/dissatisfied with current turnover are challenged to keep the business open during the pandemic condition; still have a turnover target despite limitations; make efforts to find innovations; make efforts so that the sales do not decline; and try to catch up on the sales turnover. Furthermore, the measurement of the risk-taking propensity operationally defined as the extent to which the entrepreneurs are willing to take the risk of loss [20] was reduced to four questionnaire items, asking the participants whether they experienced a drastic decrease in the sales turnover; have additions of variations of goods that are not accepted by the market; make promotions that result in losses; have a higher fixed cost. Meanwhile, the measurement of the internal locus of control operationally defined as the extent to which the entrepreneurs believe in their ability to develop their business [50] was measured by five questionnaire items, asking the participants about their business progress; post-COVID-19 pandemic business recovery; durability during the COVID-19 pandemic; business failure; and creative ability and the ability to seek innovations and business development.

3.2 Sample

Samples of this study consisted of MSMEs in the food and beverage industry in three cities in Indonesia, including the cities of Semarang, Surakarta, and Salatiga. Semarang City and Surakarta City were selected considering that they were designated culinary tourism destinations by the Indonesian Ministry of Tourism and Creative Economy. Meanwhile, the City of Salatiga was selected because UNICEF designated it as the City of Gastronomy. The sample size of this study was determined by using the Slovin formula with an e value of 5%, while the total number of MSMEs in the food and beverage industry in the three cities was 10,113, consisting of 5,651 MSMEs from Semarang City, 1,729 MSMEs from Salatiga City, and 2,733 MSMEs Surakarta City.

The required sample size is 384 MSMEs. To ensure that the data meets the minimum requirements for the number of respondents required, 15% was added to the total number of respondents in field research, making the total number of respondents 450. Respondents are owners of food and beverage MSMEs located in these three cities and are not franchise businesses. The selection of MSMEs is based on (a) the length of time (> one year) to see the ability of MSMEs to handle the crisis resulting from COVID-19, (b) the distribution of business locations, and (c) the willingness of MSME owners to be interviewed. The field survey via face-to-face interviews was carried out between July and August 2022.

Before conducting field research, a pilot test with 60 respondents was conducted to ensure the quality of the construction measurements. The pilot test results indicate that there are a total of six items omitted – consisting of one item on the financial access variable, two items on the need for achievement variable, two items on the risk-taking propensity, and one item on the internal locus of control – because its convergent validity test indicates that it does not have a loading factor of > 0.70. The test reliability indicates that it does not have a Cronbach's alpha (C.A.) value of > 0.70 and a composite reliability (C.R.) value of > 0.80.

Considering the completeness and consistency of instrument filling, from the 450 questionnaires obtained during field research, only 397 instruments were used for analysis. However, this study has met the minimum sample size requirements used. Table 1 describes the profile of respondents in terms of age, educational background, and business characteristics.

Table 1. Respondent profile

|

Profile |

N (%) |

|

Gender |

|

|

Female |

161 (40.55) |

|

Male |

236 (59.45) |

|

Age |

|

|

Up to 30 years old |

80 (20.15) |

|

Between 30-50 years old |

212 (53.40) |

|

Over 50 years old |

105 (26.45) |

|

Education |

|

|

Does not attend school / Does not graduate from Elementary School |

15 (3.78) |

|

Elementary School |

89 (22.42) |

|

Junior High School |

86 (21.66) |

|

Senior High School / Vocational High School |

169 (42.57) |

|

College |

38 (9.57) |

|

Business Age |

|

|

Up to 5 years |

152 (38.29) |

|

Between 5-10 years |

73 (18.39) |

|

Over 10 years |

172 (43.32) |

|

Asset Value |

|

|

Up to IDR 50 million |

391 (98.49) |

|

Between IDR 50-500 million |

5 (1.26) |

|

Over IDR 500 million |

1 (0.25) |

The validity, reliability, and goodness of fit model were measured before testing the hypotheses. Table 2 displays the results of the validity and reliability test. The convergent validity test reveals that all indicators have a loading value greater than 0.70, and the correlation values for all constructs are greater than the AVE value. As a result, the indicators can be declared valid for convergent and discriminant functions. The test also demonstrates that the constructs are reliable, as evidenced by the C.A. and C.R. values greater than 0.70 and 0.80, respectively.

Table 2. Validity and reliability assessment

|

Latent Construct |

Item |

Loading |

CA |

CR |

AVE |

|

Financial Access |

FA1 |

0.885 |

0.942 |

0.956 |

0.814 |

|

FA2 |

0.852 |

||||

|

FA3 |

0.909 |

||||

|

FA4 |

0.930 |

||||

|

FA5 |

0.931 |

||||

|

Market Access |

MA1 |

0.896 |

0.928 |

0.944 |

0.736 |

|

MA2 |

0.894 |

||||

|

MA3 |

0.870 |

||||

|

MA4 |

0.802 |

||||

|

MA5 |

0.876 |

||||

|

MA6 |

0.806 |

||||

|

Need for Achievement |

NA1 |

0.781 |

0.882 |

0.919 |

0.740 |

|

NA2 |

0.861 |

||||

|

NA3 |

0.904 |

||||

|

NA4 |

0.890 |

||||

|

Risk-taking Propensity |

RP1 |

0.891 |

0.766 |

0.895 |

0.810 |

|

RP2 |

0.909 |

||||

|

Internal Locus of Control |

LC1 |

0.866 |

0.917 |

0.939 |

0.754 |

|

LC2 |

0.770 |

||||

|

LC3 |

0.908 |

||||

|

LC4 |

0.916 |

||||

|

LC5 |

0.876 |

||||

|

Speed of Recovery |

SR1 |

0.984 |

0.985 |

0.990 |

0.990 |

|

SR2 |

0.980 |

||||

|

SR3 |

0.991 |

The goodness of fit test was measured based on the Standardized Root Mean Square Residual (SRMR) value of 0.08 and the Normed Fit Index (NFI) value of > 0.80. Table 3 shows the SRMR has a value of 0.062 – less than 0.08 – and the NFI value is 0.821 – higher than 0.80. Thus, the model is considered fit.

Table 3. Goodness of fit

|

Criteria |

Parameter |

Rule of Thumb |

Decision |

|

Standardized Root Mean Square Residual (SRMR) |

0.062 |

< 0.08 |

Fit |

|

Normed Fit Index (NFI) |

0.821 |

> 0.80 |

Fit |

The structural model assessment was performed to examine both direct and indirect effects through the mediating variable. The results of direct effect testing in Table 4 show that only three variables were proven to have a significant effect on recovery speed. Financial access significantly positively affects the speed of MSME performance recovery (β = 0.168, p < 0.01), indicating that H1 can be supported empirically. This demonstrates that the MSMEs with better financial access would recover faster due to the COVID-19 pandemic. It also documents that better financing access affects not only MSMEs' growth and, productivity and asset returns [35] but also the speed of post-COVID-19 performance recovery. The results are in line with the results of a study from [33] that financial resources are an essential basis for SME performance and also the results of a study from [35] that good financial access can increase profitability and accelerate performance recovery due to the COVID-19 pandemic. Observing that financial access is a determinant of the speed of MSME performance after the COVID-19 pandemic, credit relaxation can be used as a policy instrument to accelerate the recovery of MSME performance during an economic crisis.

Furthermore, the findings also reveal that the need for achievement significantly positively influences the performance recovery speed of MSME (β = 0.355, p < 0.01), indicating that H3a can be supported empirically. Thus, the MSMEs with a high need for achievement – such as setting and attempting to achieve goals, working hard, and being satisfied with their work – would recover faster post-COVID-19 pandemic. This finding aligns with Sidek and Zainol [45], who confirmed that increasing the need for achievement would improve business performance, as evidenced by the recovery speed after the COVID-19 pandemic. Thus, MSME entrepreneurs need to be encouraged always to set challenging goals and try hard to achieve these goals.

In a similar vein, the result of testing H3c reveals that the internal locus of control has a positive and significant effect on the performance recovery speed of MSME (β = 0.351, p < 0.01). The MSME entrepreneurs with a high internal locus of control or confidence in their ability to control destinies and environment would recover faster, especially after the COVID-19 period. The findings of this study support [45], who observed that the internal locus of control could affect the business performance, as measured by MSMEs’ performance recovery in this study. In adverse conditions such as the COVID-19 pandemic, the internal locus of control of food and beverage MSME entrepreneurs needs to be fostered so that they can grow optimism that the businesses they manage will experience a faster recovery in performance.

The findings of this study demonstrate no effect of market access on the recovery speed. Therefore, H2 cannot be supported empirically. As a result, the MSMEs with the ability to expand their market, as evidenced by their ability to engage in innovative marketing such as e-commerce and digital marketing, could not accelerate the post-COVID-19 pandemic recovery. Thus, the study results from [36, 39] do not apply to conditions during the COVID-19 pandemic. Similarly, the result of H3b testing, which cannot be supported empirically in this study, implies that the risk-taking propensity does not affect recovery speed. The MSME entrepreneurs with a high risk-taking propensity or willingness to take risks with potential losses appeared unable to accelerate the post-COVID-19 pandemic recovery. Thus, the results of a previous study [46], which found that risk-taking propensity can improve performance, only sometimes apply, mainly when studied in crisis conditions due to the COVID-19 pandemic.

Table 5 shows that the need for achievement is confirmed to mediate the effect between financial access and recovery speed (β = 0.099, p < 0.01), indicating that H4a is confirmed empirically. Similarly, the result of H4c testing reveals that the internal locus of control can mediate the effect between financial access and recovery speed (β = 0.129, p < 0.01). Therefore, the MSME entrepreneurs with good financial access were motivated to achieve goals, worked hard to achieve them, and strongly believed in their ability to control their destinies and external factors. This, in turn, would result in a faster recovery of MSME performance.

In terms of indirect effect testing of the market access on the recovery speed, it is proven that the need for achievement (H5a) and internal locus of control (H5c) are both able to mediate the effect of market access on the recovery speed (β = 0.256, p < 0.01; β = 0.157, p < 0.01). Thus, the MSME entrepreneurs with better market access would be motivated to try to achieve goals, work hard to achieve goals, and be more self-confident in their ability, which would speed up the MSME recovery.

However, the results of this study can not confirm the mediation of risk-taking propensity (H5b) on the effects of financial access and market access on the speed of MSMEs’ performance recovery, as indicated by the significance values that are higher than 0.10 (β = 0.006 p = 0.420; β = 0.059 p = 0.244).

Table 6 reveals that the mediation of the need for achievement and internal locus of control in the influence between financial access and recovery speed is only partial. This emphasized that financial access could affect the recovery speed, whether or not the need for achievement and internal locus of control were present. Further, it is also found that the need for achievement and internal locus of control fully mediate the influence of market access and recovery speed. Thus, market access affects the recovery speed only if mediated by the need for achievement and internal locus of control.

Table 4. Result of hypothesis testing – direct effect

|

Hypothesis |

Relationship |

Path Coefficient |

P-Value |

Decision |

|

H1 |

FA -> SR |

0.168 |

0.004*** |

Supported |

|

H2 |

MA -> SR |

-0.064 |

0.449 |

Not supported |

|

H3a |

NA -> SR |

0.355 |

0.000*** |

Supported |

|

H3b |

RP -> SR |

0.090 |

0.152 |

Not supported |

|

H3c |

LC -> SR |

0.351 |

0.001*** |

Supported |

Notes: *** indicates significance at α of 0.01

Table 5. Result of hypothesis testing – mediating effect

|

Hypothesis |

Relationship |

β |

P-Value |

Decision |

|

H4a |

FA -> NA -> SR |

0.099 |

0.000*** |

Supported |

|

H4b |

FA -> RP -> SR |

0.006 |

0.420 |

Not supported |

|

H4c |

FA -> LC -> SR |

0.129 |

0.000*** |

Supported |

|

H5a |

MA -> NA -> SR |

0.256 |

0.000*** |

Supported |

|

H5b |

MA -> RP -> SR |

0.059 |

0.244 |

Not supported |

|

H5c |

MA -> LC -> SR |

0.157 |

0.000*** |

Supported |

Notes: *** indicates significance at α of 0.01

Table 6. Result of hypothesis testing – direct VS indirect effect

|

Hypothesis |

Relationship |

Direct Effect |

Indirect Effect |

Partially/ Fully Mediated |

||

|

β |

P-Value |

β |

P-Value |

|||

|

H4a |

FA -> NA -> SR |

0.168 |

0.004*** |

0.099 |

0.000*** |

Partially |

|

H4c |

FA -> LC -> SR |

0.168 |

0.004*** |

0.129 |

0.000*** |

Partially |

|

H5a |

MA -> NA -> SR |

-0.064 |

0.449 |

0.256 |

0.000*** |

Fully |

|

H5c |

MA -> LC -> SR |

-0.064 |

0.449 |

0.157 |

0.000*** |

Fully |

Notes: *** indicates significance at α of 0.01

The direct effect testing results show that financial access, need for achievement, and internal locus of control positively affect the performance recovery speed of MSMEs after the COVID-19 pandemic. Furthermore, the mediation effect test also demonstrates that the need for achievement and internal locus of control mediate the effect between financial access and performance recovery speed of MSMEs. Although market access has not been proven to affect the recovery speed directly, our findings confirm an effect between market access and the recovery speed. Regarding the risk-taking propensity, this study cannot confirm whether it affects the recovery speed as an independent or mediating variable.

This present study offers two policy implications so that MSMEs, especially in Indonesia, can recover quickly and operate sustainably after the COVID-19 pandemic. First, financial access is critical to the performance recovery speed of MSME following the COVID-19 pandemic, which has been shown to have both a direct and indirect effect on recovery speed. Hence, the Indonesian government still needs to maintain its credit relaxation policies to increase MSMEs' financial access, special credit packages for MSMEs, and affordable interest rates. Second, banking institutions should help MSME entrepreneurs to be able to access banking credit by banking officers visiting MSME entrepreneurs to provide banking literacy, offering credit schemes that are not burdensome, and helping to fill out forms that MSME entrepreneurs consider complicated by MSME entrepreneurs. Third, parties interested in the development of MSMEs, such as local governments, non-profit organizations, and college institutions, should increase their efforts to help MSME entrepreneurs to be able to prepare for various needs to meet external funding access requirements. Apart from that, it also provides training and assistance to the MSME entrepreneurs, particularly to foster entrepreneurial capacity, which has been shown to contribute to the performance recovery speed of MSME.

This research was funded by the Ministry of Research and Technology/ National Research and Innovation Agency of the Republic of Indonesia (Grant No.: 033/E5/PG.02.00/2022).

|

MSME |

Micro, Small, and Medium Enterprises |

|

GDP |

Gross Domestic Product |

|

SEM PLS |

Structural Equation Modelling - Partial Least Squares |

|

AVE |

Average Variance Extracted |

|

CA |

Cornbach's alpha |

|

CR |

Composite Reliability |

|

SRMR |

Standardized Root Mean Square Residual |

|

NFI |

Normed Fit Index |

[1] Assefa, M., Yadavilli, J. (2020). Financial supporting mode for small businesses to coup with COVID-19 lockdown restrictions. Journal of Emerging Technologies and Innovative Research, 7(10): 496-506. https://doi.org/10.6084/m9.figshare.JETIR2010058

[2] Morgan, T., Anokhin, T., Ofstein, T., Friske, W. (2020). SME response to major exogenous shocks: The bright and dark sides of business model pivoting. International Small Business Journal: Researching Entrepreneurship, 38(5): 369-379. https://doi.org/10.1177/026624262093659

[3] Bartik, A.W., Bertrand, M., Cullen, Z., Glaeser, E.L., Luca, M., Stanton, C. (2020). The impact of COVID-19 on small business outcomes and expectations. Proceedings of the National Academy of Sciences of the United States of America, 117(30): 17656-17666. https://doi.org/10.1073/pnas.2006991117

[4] Fairlie, R. (2020). The impact of COVID-19 on small business owners: Evidence from the first three months after widespread social-distancing restrictions. Journal of Economics and Management Strategy, 29(4): 727-740. https://doi.org/10.1111/jems.12400

[5] Jordà, O., Singh, S.R., Taylor, A.M. (2022). Longer-run economic consequences of pandemics. The Review of Economics and Statistics, 104(1): 166-175. https://doi.org/10.1162/rest_a_01042

[6] Famiglietti, M., Leibovici, F. (2020). COVID-19’s shock on firms’ liquidity and bankruptcy: Evidence from the Great Recession. Economic Synopses, 7: 1-21. https://doi.org/10.20955/es.2020.7

[7] Wulandari, W.E. (2021). Lelang dan UMKM: representasi kolaboratif inovatif serta berdaya guna. Kementerian Keuangan Republik Indonesia. https://www.djkn.kemenkeu.go.id/artikel/baca/14186/Lelang-dan-UMKM-Representasi-Kolaborasi-Inovatif-Serta-Berdaya-Guna.html.

[8] Setyoko, P.I., Kurniasih, D. (2022). Impact of the covid 19 pandemic on Small and Medium Enterprises (SMEs) performance: A qualitative study in Indonesia. Journal of Industrial Engineering & Management Research, 3(3): 315-324. https://doi.org/10.7777/jiemar.v3i3.406

[9] Hidayati, R., Rachman, N.M. (2021). Indonesian government policy and SMEs business strategy during The COVID-19 pandemic. Niagawan, 10(1): 1-9. https://doi.org/10.24114/niaga.v10i1.21813

[10] Svotwa, T.D., Jaiyeoba, O., Mornay, R.L., Makanyeza, C. (2022). Perceived access to finance, entrepreneurial self-efficacy, attitude toward entrepreneurship, entrepreneurial ability, and entrepreneurial intentions: A Botswana youth perspective. Sage Open, 10(4): 1-18. https://doi.org/10.1177/21582440221096437

[11] Khan, U., Salamzadehh, Y., Kawamorita, H., Rethi, G. (2021) Entrepreneurial orientation and small and medium-sized enterprises’ performance; Does access to finance’ moderate the relation in emerging economies?. Vision The Journal of Business Perspective, 25(1): 88-102. https://doi.org/10.1177/0972262920954604

[12] Shelton, L.M., Minniti, M. (2018). Enhancing product market access: Minority entrepreneurship, status leveraging, and preferential procurement programs. Small Business Economics, 50(3): 481-498. https://doi.org/10.1007/s11187-017-9881-7

[13] Dai, R., Feng, H., Hu, J., Jin, Q., Li, H., Wang, R.R., Wang, R.X., Xu, L., Zhang, X. (2021). The impact of COVID-19 on small and medium-sized enterprises (SMEs): Evidence from two-wave phone surveys in China. China Economic Review, 67: 101607. https://doi.org/10.1016/j.chieco.2021.101607

[14] Marjański, A., Sułkowski, Ł. (2021).Consolidation strategies of small family firms in Poland during COVID-19 crisis. Entrepreneurial Business and Economics Review, 9(2): 167-182. https://doi.org/10.15678/EBER.2021.090211

[15] Stępień, B., Światowiec-Szczepańska, J. (2022). The role of public aid and restrictions’ circumvention in SMEs’ pandemic survival strategies. Entrepreneurial Business and Economics Review, 3(1): 23-36. https://doi.org/10.15678/EBER.2022.100402

[16] Tambunan, T. (2019). Recent evidence of the development of micro, small, and medium enterprises in Indonesia. Journal of Global Entrepreneurship Research, 9(1): 1-15. https://doi.org/10.1186/s40497-018-0140-4

[17] Badi L., Ishengoma, E. (2021). Access to debt finance and performance of small and medium enterprises. Journal of Financial Risk Management, 10(3): 241-259. https://doi.org/10.4236/jfrm.2021.103014

[18] Khan, M.A., Asima, S., Zahid, S., Le, T.M.H., Qaiser, N. (2020). Determinants of entrepreneurial small and medium enterprises performance with the interaction effect of commercial loans. Asia Pacific Journal of Innovation and Entrepreneurship, 14(2): 161-173. https://doi.org/10.1108/apjie-11-2019-0079

[19] Nizaeva, M., Ali, C. (2019). Investigating the relationship between financial constraint and growth of SMEs in South Eastern Europe. Sage Open, 9(3): 1-15. https://doi.org/10.1177/2158244019876269

[20] Ndofirepi, T.M. (2020). Relationship between entrepreneurship education and entrepreneurial goal intentions: Psychological traits as mediators. Journal of Innovation and Entrepreneurship, 9(1): 1-20. https://doi:10.1186/s13731-020-0115-x

[21] Ahmad, S., Tahar, T., Sahibzada, G.H., Wangari, W., Fawad, A. (2022). Entrepreneurial-specific characteristics and access to finance of SMEs in Khyber Pakhtunkhwa, Pakistan. Sustainability, 14(16): 1-14. https://doi.org/10.3390/su141610189

[22] Firnalista, N., Nofialdi, Azriani, Z. (2020). Impact of entrepreneurial characteristics and access to credit on business performance of the small business (Case: Brown sugar processing in Agam District). Indonesian Journal of Agricultural Research, 3(1): 56-64. https://doi.org/10.32734/injar.v3i1.4289

[23] Absah, Y., Muchtar, Y.C., Qamariah, I. (2016). The influence of entrepreneurial characteristics and marketing on business performance is mediated by competitive advantage. Proceedings Universitas Sumatra Utara.

[24] Tóth-Pajor, Á., Bedő, Z., Csapi, V. (2023). Digitalization in entrepreneurship education and its effect on entrepreneurial capacity building. Cogent Business & Management, 10(2): 1-22. https://doi.org/10.1080/23311975.2023.2210891

[25] López, A.R., Souto, J.E. (2020). Empowering entrepreneurial capacity: Training, innovation and business ethics. Eurasian Business Review, 10: 23-43. https://doi.org/10.1007/s40821-019-00133

[26] Oginni, B.O., Omoyele, S.O., Ayantunji, I.O., Larnre-Babalola, F.O., Balogun, R.A. (2023). Nexus between entrepreneurial characteristics and small business productivity in Nigeria. Journal of Enterprise & Development, 5(2): 238-256. https://doi.org/10.20414/jed.v5i2.6835

[27] Georgakalou, M., Kamariotou, M., Kitsios, F. (2023). Evaluating leaders’ strategic thinking and entrepreneurial characteristics using semantic analysis, Analysis/ Businesse, 3(1): 181-197. https://doi.org/10.3390/businesses3010013

[28] Teruel-Sanchez, R., Briones-Penalver, A.J., Bernal-Conesa, J.A., Nieves-Nieto, C. (2021). Influence of the entrepreneur's capacity in business performance. Business Strategy and The Environment, 30(5): 2453-2467. https://doi.org/10.1002/bse.2757

[29] Hu, W., Liu H., Tian, Y., Zhang, X., Mao, Y. (2022) Entrepreneurial capability, career development, and entrepreneurial intention: Evidence from China's HR survey data. Frontiers in Psychology, 13: 870706. https://doi.org/10.3389/fpsyg.2022.870706

[30] Popova, M.V., Rozhdestvenskaya, E.I. (2020). The impact of the coronavirus pandemic (COVID-19) consequences on phonetic aspect of a foreign language teaching in specialized linguistic specialties at universities. Proceeding Advances in Social Science, Education and Humanities Research, 486: 293-298. https://doi.org/10.2991/assehr.k.201105.052

[31] Yusi, M.S. (2022) The relationship between entrepreneurial spirits and entrepreneurial value in improving business self-reliance: A proposed model. Jurnal Riset Bisnis dan Investasi, 8(1): 1-11. https://doi.org/10.35313/jrbi.v8i1.3698

[32] Giang, M.H., Bui, H.T., Yuichiro, Y., Tran, D.X., Mai, T.Q. (2019). The causal effect of access to finance on productivity of small and medium enterprises in Vietnam. Sustainability, 11: 1-19. https://doi.org/10.3390/su11195451

[33] Gumel, B.I., Bin Bardai, B. (2023). A review of critical success factors influencing the success of SMEs. Business Review, 3(1): 37-61. https://doi.org/10.33215/sbr.v3i1.906

[34] Lee, N., Sameen, H., Cowling, M. (2015) Access to finance for innovative SMEs since the financial crisis. Research Policy, 44(2): 370-380. https://doi.org/10.1016/j.respol.2014.09.008

[35] Beck, T., Demirgüç-Kunt, A., Maksimovic, V. (2008). Financing patterns around the world: Are small firms different? Journal of Financial Economics, 89(3): 467-487. https://doi.org/10.1016/j.jfineco.2007.10.005

[36] Clampit, J.A., Melanie, P.L., John. E.G., Jim, L. (2021). Performance stability among small and medium-sized enterprises during COVID-19: A test of the efficacy of dynamic capabilities. International Small Business Journal: Researching Entrepreneurship, 40(3): 403-419. https://doi.org/10.1177/02662426211033270

[37] Garbellano, S., Da Veiga, M.R. (2019). Dynamic capabilities in Italian leading SMEs adopting industry 4.0’. Measuring Business Excellence, 23(4): 472-483. https://doi.org/10.1108/MBE-06-2019-0058

[38] Kumar, A., Syed, A.A., Pandey, A. (2020). How adoption of online resources can help Indian SMEs in improving performance during COVID-19 pandemic. Test Engineering and Management Journal, 6(3): 137-144. https://doi.org/10.24083/apjhm.v16i3.1009

[39] Kumar, A., Ayedee, N. (2021). Technology adoption: A solution for SMEs to overcome problems during COVID-19. Academy of Marketing Studies Journal, 25(1): 1-16.

[40] Fanggidae, H.C., Sutrisno, S., Fanggidae, F.O., Permana, R.M. (2023). Effects of social capital, financial access, innovation, socioeconomic status and market competition on the growth of Small and Medium Enterprises in West Java Province. The ES Accounting and Finance, 1(2): 104-112. https://doi.org/10.58812/esaf.v1i02.69

[41] Fatimah, F., Fikri, P., Jane, S.T., Sanusi, G., Trina, E.T. (2021). Perbaikan produksi, promosi dan pemasaran pada UKM pengrajin kue di kotamobagu Sulawesi Utara dalam menghadapi masa pandemi COVID-19. Solidaritas: Jurnal Pengabdian, 1(2): 55-64. https://doi.org/10.24090/sjp.v1i2.5465

[42] Hernandez, M.A., Perez, C.P. (2019). Psychological characteristics analysis that define a disabled entrepreneur. Suma de Negocios, 10(22): 9-18. https://doi.org/10.14349/sumneg/2019.V10.N22.A2

[43] Selamat, F., Hetty, K.T., Chairy, C., Didi, W.U. (2018). Entrepreneurial characteristics amongst different professional backgrounds: Evidence from Indonesia. International Journal of Business, 2(1): 25-32. https://doi.org/10.32924/IJBS.V2I1.30

[44] Tessema Gerba, B. (2012). Impact of entrepreneurship education on entrepreneurial intentions of business and engineering students in Ethiopia. African Journal of Economic and Management Studies, 3(2): 258-277. https://doi.org/10.1108/20400701211265036

[45] Sidek, S., Zainol, F.A. (2011). Psychological traits and business performance of entrepreneurs in small construction Industry in Malaysia. International Business and Management, 2(1): 170-185.

[46] Alam, K., Mohammad, A.A., Michael, O.E., Peter, A.M., Retha, W. (2022). Digital transformation among SMEs: Does gender matter? Sustainability, 14(1): 1-20. https://doi.org/10.3390/su14010535

[47] Rokhman, W., Ahamed, F. (2015). The role of social and psychological factors on entrepreneurial intention among islamic college students in Indonesia. Entrepreneurial Business and Economics Review, 3(1): 29-42. https://doi.org/10.15678/EBER.2015.030103

[48] Uysal, Ş.K., Karadağ, H., Tuncer, B., Şahin, F. (2022). Locus of control, need for achievement, and entrepreneurial intention: A moderated mediation model. The International Journal of Management Education, 20(2): 100560. https://doi.org/10.1016/j.ijme.2021.100560

[49] Annisa, N.N., Ginarti, S. (2023). Employee performance: Self-efficacy and locus of control. International Journal on Social Science Economics and Art, 12(4): 200-206. https://doi.org/10.35335/ijosea.v12i4.181

[50] Arkorful, H., Hilton, S.K. (2021). Locus of control and entrepreneurial intention: A study in a developing economy. Journal of Economic and Administrative Sciences, 38(2): 333-344. https://doi.org/10.1108/jeas-04-2020-0051

[51] Bakhtiari, S., Breunig, R., Magnani, L., Jacquelyn, Z. (2020). Financial constraints and small and medium enterprises: A review. The Economic Record, The Economic Society of Australia, 96(315): 506-523. https://doi.org/10.1111/1475-4932.12560

[52] Kong, X., Deng-Kui, S., Haiyang, L., Dongmin, K. (2021). Does access to credit reduce SMEs’ tax avoidance? Evidence from a regression discontinuity design. Financial Innovation, 7(1): 1-23. https://doi.org/10.1186/s40854-021-00235-3

[53] Elahi, H., Ahmad, H., Shamas, M., Haq, U.L., Saleem, A. (2021). The impact of operating cash flows on financial stability of commercial banks : Evidence from Pakistan. Journal of Asian Finance, Economics and Business, 8(11): 223-234. https://doi.org/10.13106/jafeb.2021.vol8.no11.0223

[54] Yoshino, N., Taghizadeh-Hesary, F. (2016). Major challenges facing small and medium-sized enterprises in Asia and solutions for mitigating them. SSRN Electronic Journal, ADBI Working Paper 564. https://doi.org/10.2139/ssrn.2766242

[55] Elbannan, M.A., Farooq, O. (2020). Do more financing obstacles trigger tax avoidance behavior? Evidence from Indian SMEs. Journal of Financial Economics, 44: 161-178. https://doi.org/10.1007/s12197-019-09481-9

[56] Beck, T., Demirguc-Kunt, A. (2006). Small and medium-size enterprises: Access to finance as a growth constraint. Journal of Banking & Finance, 30(11): 2931-2943. https://doi.org/10.1016/j.jbankfin.2006.05.009