Indra Siswanti*![]() | Hosam Alden Riyadh

| Hosam Alden Riyadh![]() | Embun Prowanta

| Embun Prowanta![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This investigation explores the moderating role of digital transformation on the impact of financing and capital quality on the sustainability of business practices within Islamic rural banks in Indonesia. Data were collected from the financial and annual reports of 165 Islamic rural banks across the nation, with a focused sample of 30 banks in the West Java region, spanning the years 2016 to 2021. The analysis, conducted through EViews version 10, employed multiple linear regression analysis on panel data to ascertain the relationships in question. It was found that non-performing financing (NPF) exerts a significant adverse effect on the sustainability of these banks' operations, whereas a positive influence is observed in the case of the capital adequacy ratio (CAR). Furthermore, digital transformation was identified as a critical moderating factor, enhancing the negative impact of NPF and bolstering the positive impact of CAR on business sustainability. The findings suggest that Islamic rural banks in Indonesia embarking on digital transformation initiatives must prioritize information transparency, financial stability, and the cultivation of innovative capabilities. Additionally, the selection of digital transformation strategies should be tailored to the banks' unique characteristics, including property rights, operational scale, and growth potential. This study contributes to the literature by providing empirical evidence of the significant role digital transformation plays in influencing the relationship between financial health indicators and sustainability in the context of Islamic rural banking.

green business, digital transformation, financing quality, capital quality

Data from the Financial Services Authority indicate that as of June 2022, Indonesia’s total number of rural banks was 1,453. In comparison, the number of Islamic rural banks in Indonesia was only 165. Hence, the proportion of all Islamic rural banks is only 11.35%. According to statistical data for 2021, it is revealed that with 231 million Muslims, Indonesia has the biggest Muslim population in the world. Thus, given that Muslims make up the vast majority and most Indonesians live in rural areas, Islamic rural banks should have the opportunity and potential for further development. Only then can Islamic rural banks serve as the cornerstone of the people's economy in the regions.

Nevertheless, several issues have hindered Indonesia's growing network of Islamic rural banks from developing swiftly, including a lack of socialization efforts by the government, the banks themselves, and other stakeholders. At present, nearly all financial transactions are conducted digitally. Inadequate technological advancements and a lack of innovation in products also affect the growth of Islamic rural banks in Indonesia, even though their market share differs from that of the banking sector as a whole. However, as the driving force of sustainable business, the quality and quantity of human resources have not received much attention from Islamic rural banks up until this point.

Digital transformation data on Islamic rural banks in Indonesia was obtained from investment costs, which were used for information technology (IT) upgrades to support the digitalization program at Islamic rural banks. The following is the evolution of investment data to boost digital transformation:

It is evident from Table 1 that IT investment in Islamic rural banks consistently rises every year. This is due to the fact that digital transformation is crucial for fierce competition in the banking industry, particularly since these banks must contend with a plethora of new financial technologies that may pose a threat to them. Islamic rural banks must constantly upgrade their IT (digital transformation).

Table 1. IT Investment in Islamic Rural Banks (in millions of rupiah)

|

Year |

Amount (Rupiah) |

|

2016 |

155,074 |

|

2017 |

258,780 |

|

2018 |

267,785 |

|

2019 |

330,438 |

|

2020 |

349,728 |

|

2021 |

433,482 |

Source: Data processed (2023)

Further, boosting business tactics to boost company profitability continues to be a top priority for many firms today. They believe they are capable of anything, even retaining customers with higher profits. They should be informed that strong corporate profits do not guarantee a company's existence, as this is wholly untrue. It should be mentioned that social, environmental, and economic issues are always important for a sustainable business. Three pillars, namely, people, planet, and profit, i.e., the 3Ps, are required to sustain this process for the company's survival. The corporation operates along these three pillars to address societal requirements without jeopardizing the needs of future generations. Thus, companies design products that take advantage of the current environment and use renewable resources. In addition, 3P is an effective business strategy that can build a company's competitiveness.

Related to sustainable business in Islamic banks, Siswanti [1] revealed that financial and non-financial factors affected the ability of Islamic banks to engage in sustainable business. Siswanti et al. [2] also uncovered that the sustainable business of Islamic banks in Indonesia was still dominated by financial performance.

Instead of being a dream, digitalization is a reality that must be experienced, particularly in light of the global COVID-19 pandemic. The pandemic has brought about huge changes. Competition, market needs, the advent of new technologies, and new rules and regulations from authorities all contributed to earlier changes. The pandemic has added to the known factors driving the current alterations. Human migration is restricted by pandemic conditions, which exacerbate the existing changes.

Even while technology is used to change current business processes or launch new ventures, digital transformation will fundamentally alter how an organization operates and what kind of value it offers to its clients. Another shift known as digital transformation is revamping conventional procedures using digital technologies to make them more successful and efficient. In this sense, the banking industry relies heavily on technology, and practically every bank strives to keep up with and advance technical advancements. It is common knowledge that nearly all bank services and products, including SMS banking, e-banking, and m-banking, may now be accessible via technology. Given Islamic rural banks' competition from financial technology (Fintech), online lending, and conventional rural banks, technological advancements are also critical to their success. As a result, Islamic rural banks risk losing their clients over time if they do not advance technologically.

Due to digital transformation, the way a company generates value for its customers and other stakeholders can change. At the level of the business model, digital transformation occurs most effectively. Because of the possibility of winner-take-all market outcomes, network effects can be a significant force in digital business models. They do this by generating large-gets-larger reinforcing feedback loops. Network effects are demand-side economies of scale; as a product's user base grows, its value rises. Owing to high switching costs, a huge network can charge high prices, draw in new subscribers, and enjoy protection from competition. The big network generates substantial revenues and profits because of the cheap operational expenses that come with scale (supply-side economies of scale). To sum up, strong network effects indicate a commercial possibility. Managers, however, cannot understand that a network effect is a two-sided phenomenon that can work for or against a company, slowing growth or speeding decline [3].

Regarding the effect of digital transformation on sustainable businesses, Oktavenus [4] reported that digital transformation had a significant positive effect on sustainable businesses. When carrying out digital transformation, it is important to migrate data to the new system, though employees need time to adapt to this. This greatly helps the security and management of corporate data. Whatever the company's reasons for migrating to digital transformation, whether due to market demand or modernization, digital transformation is crucial for optimizing company profits, and digital transformation is the key to a company's progress today, including in the banking industry.

Again, the increase in NPF will make banks improve their business capital structure and reduce their ability to expand credit to the real sector automatically, posing difficulty for every industry sector to borrow credit. This bad credit condition will cause banks to lack funds, injuring the course of business activities carried out by the bank. Thus, it is vital for banks to always maintain the quality of financing provided to the public, considering that high levels of NPF affect the financial performance of Islamic rural banks and the sustainability of their businesses. As for financing quality for sustainable businesses, Kurniawansyah and Mutmainah [5] stated that NPF affected the sustainable banking business in Indonesia. In contrast, Masrurroh and Mulazid [6] affirmed that the NPF did not affect the sustainable business of Islamic banks.

Moreover, the CAR indicates the soundness of a bank's capital. The CAR measures a bank's ability to fund risky assets, including the loans it has made. A capital assessment evaluates the bank's ability to cover existing risks and foresee future hazards with sufficient capital. The CAR, which measures how well a bank's capital has surpassed its requirements, can be used to gauge the likelihood of its continued operation. The resilience of the bank in question in managing the decline in the value of bank assets brought on by problem assets increases with the CAR. Johnson et al. [7] asserted that capital has several functions, including a buffer against operational losses, and capital became the basis for investors to evaluate a company's ability to generate profits. With sufficient capital, the company's business can be sustainable. The study's findings addressed how capital quality affected sustainable business. Rahmi and Anggraini [8] indicated that the CAR significantly positively affected Islamic banks' sustainability, which contrasts with the research results by Masrurroh and Mulazid [6], which stated that the CAR did not affect sustainable business at a Sharia commercial bank.

Considering that Islamic rural banks face competition from both commercial rural banks and Fintech institutions, they face quite difficult challenges in implementing digital transformation. Therefore, Islamic rural banks always improve services through IT improvements (digital transformation) so that customers do not switch to commercial rural banks or other Fintech institutions. In addition, those banks always maintain the financing quality to keep it below 5%. According to the regulations of the Financial Services Authority (OJK), the maximum level of NPF is 5%. For this reason, the financing quality, as reflected in NPF, must always focus on the principles of providing credit known as the 5Cs, namely, character, capacity, capital, collateral, and condition. According to these five principles, banks analyze and decide whether their prospective debtors/customers will receive credit approval. By maintaining the 5C principles, the financing quality of Islamic rural banks can always be maintained. As institutions that collect public funds, they must have strong capital so that all bank operations run properly.

Further, the most important function of bank capital is to absorb losses caused by failures in bank operations. The main purpose of capital is to protect customers from losses that occur. If the capital owned by banks cannot be sufficient to absorb losses, they cannot operate properly, which reduces their image in the eyes of the public. This leads to a decline in their profits, and people no longer trust them and switch to other banks. Moreover, Islamic rural banks need to maintain their capital quality. According to the regulations of OJK, Islamic rural banks are required to maintain their capital quality, which is reflected in a CAR of at least 8%.

This study proposes the following questions: (i) Do quality financing and capital affect sustainable business in Islamic rural banks in Indonesia? (ii) Does digital transformation moderate the effect of quality financing and capital on sustainable business in Islamic rural banks in Indonesia? Therefore, this study aims to: (i) test and analyze the effect of quality financing and capital on the sustainable business of Islamic rural banks in Indonesia; (ii) test and analyze the digital transformation, which moderates the effect of quality financing and capital on sustainable business in Islamic rural banks in Indonesia.

2.1 Sustainable business

A sustainable or green business refers to an enterprise, which has little or no negative impact, or may even positively affect the local or global environment, community, society, or economy. It attempts to achieve the triple bottom line (TBL). Rashid et al. [9] defined a sustainable business as any company engaging in environmentally friendly or green activities to ensure that all procedures, goods, and manufacturing activities adequately addressed current environmental concerns while maintaining a profit. That is, it is a company that meets the needs of the present world without impairing the capacity of future generations to meet its own needs.

The TBL, also known as the 3P, was created by Elkington [10]. According to the author, businesses that want to be sustainable must focus on the 3Ps and pursue profits. The 3P concept is regarded as the main pillar in creating a sustainable business. The corporation must now base its corporate obligations on the TBL, which includes financial, social, and environmental considerations rather than the single bottom line, a corporate value represented in its financial position.

The sustainable business of Islamic rural banks can be measured in the three aspects of economic, social and environmental performance as follows:

2.2 Digital transformation

According to Westerman et al. [11], digital transformation is an organizational change process, which involves people, strategy, and structure using digital technology and business models that adapt to improve organizational performance. Digital transformation is a matter of using technology to transform or change analog or traditional processes into digital ones that are more efficient and effective. It covers many technologies and will certainly evolve. Digital transformation is not only about technology but also occurs at the intersection of people, business, and technology under the guidance of a broader business strategy. In today's digital era, consumer behavior has undergone significant changes, and digital platforms have become a source of information for the public to make decisions [12]. Organizational management incorporates IT, including leadership, data structure, and organizational processes [13, 14]. As a result, it is guaranteed that IT organizations can be used to uphold and further corporate strategies and objectives.

Market behavior has changed due to digital transformation and technological advancements [4]. The majority of consumers are now more likely to conduct business online. Consumers can only buy their various needs without visiting an outlet if they have a smartphone connected to the internet. This convenience must be offered in the workplace if businesses are to continue competing in the digital age. The digital transformation is measured as follows:

DT= Ln. Information technology investment (1)

2.3 Quality financing

The financing quality of Islamic rural banks is measured by the NPF. According to Dendawijaya [15], NPF refers to the case, where the debtor cannot make the agreed-upon principal installment payments. As defined by Siamat [16], NPF is a loan with difficulty repaying due to internal factors, such as intention, and external ones, i.e., an event beyond the creditor's control.

NPF consists of loans that are classified as substandard, doubtful, or even losses. The number of non-performing loans is one of the key factors which determines the performance of banking and other financial institutions. NPF provides an overview of the capital owned by the bank. Quality financing in Islamic rural banks can be reflected in the NPF, which is an instrument for assessing problematic financing. The higher the NPF, the higher the risk the bank faces. A high NPF affects the bank’s capital. The maximum NPF ratio that Bank Indonesia allows for Islamic rural banks is 5%. The NPF is calculated as follows:

$\mathrm{NPF}=\frac{\text { Non-performing financing } \times\, 100 \%}{\text { Total financing }}$ (2)

2.4 CAR

The CAR shows a bank’s ability to maintain current capital to protect against possible losses in loans, investments, securities, and claims from other banks. It is a certain proportion of the total risk-weighted assets used to identify, measure, monitor, and control the risks that arise, affecting the amount of bank capital. The minimum capital provision set by the government in assessing the soundness of a bank varies according to the level of need that is deemed most appropriate.

The CAR also demonstrates how well the bank’s capital has satisfied its requirements, providing a foundation for evaluating the likelihood of its continued operation. The resilience of the bank in question in dealing with the decline in the value of bank assets brought on by problem assets increases with the CAR. The Financial Services Authority regulates the minimum CAR value of Islamic rural banks at 8%. CAR is measured by the following formula:

CAR = (Total capital/ATMR) $\times$ 100 % (3)

2.5 Research hypotheses

2.5.1 Quality financing and sustainable business

Quality financing is an assessment tool used by a bank to assess the collectability or ability of customers to pay for financing. The criteria for assessing the financing quality are based on business prospects, customer performance, and the ability to pay. The better the financing quality of a bank, the more sustainable its business is. Islamic rural banks must always maintain their financing quality, bearing in mind that a high NPF affects their financial performance.

Kurniawansyah and Mutmainah [5] did research on Indonesian commercial banks listed on the Jakarta Stock Exchange for 2009-2011. Totally, 29 commercial banks were used as samples through saturated/census sampling. The research results demonstrated that NPF significantly negatively affected sustainable banking businesses in Indonesia. Jathurika [17] demonstrated that only a few listed commercial banks in Sri Lanka were affected. The analyzed non-performing loan indicator included the non-performing loan ratio, while the financial performance indicator covered ROA and equity. The research proved that non-performing loans significantly negatively affected financial performance, ultimately affecting the sustainable business of banks in Sri Lanka. Based on this description, the following hypothesis is proposed:

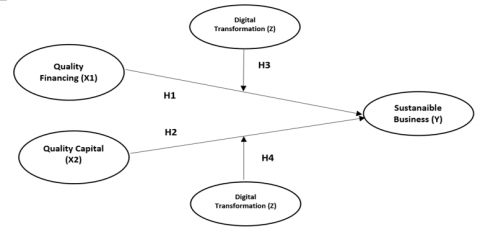

H1: Quality financing has a significant negative effect on sustainable business.

2.5.2 Quality capital and sustainable business

According to Johnson et al. [7], capital has several functions, such as a buffer against operational losses, and capital becomes the basis for investors to evaluate a company's ability to generate profits. With sufficient capital, the company's business can be sustainable. Rahmi and Anggraini [8] stated that the CAR significantly impacted the sustainable operation of Islamic banks. Kipruto et al. [18] conducted research at 14 commercial banks in Kenya using five-year financial data from 2013 to 2016. Therefore, it was recommended that CBK regularly monitor commercial banks by ensuring the release of their quarterly results to the public. The research results stated that the CAR had a considerable favorable impact on financial performance, affecting the long-term sustainability of Kenyan banks' businesses. Based on this description, the following hypothesis is derived:

H2: Quality capital has a significant positive effect on sustainable business.

2.5.3 Digital transformation in moderating the effect of quality financing on sustainable business

Yanti et al. [19] found that micro, small and medium enterprises (MSME) were not so competitive, and one of the causes was limited mastery of information and communications technology (ICT). To have competitiveness and business sustainability, MSME must respond to rapid changes in technological innovation and the efficient use of technology. Research results stated that innovation and technological development significantly affected the sustainability of microenterprises. Likewise, Oláh et al. [20] stated that Industry 4.0 significantly affected environmental sustainability. Moreover, Do et al. [21] investigated the impact of digital transformation on the performance of conventional Vietnamese banks at different scales and the policy implications of digital transformation to improve their performance. Specifically, they applied the system generalized method of moments (SGMM) of Blundell and Bond to joint-stock commercial banks in Vietnam. Then the outcome disclosed that the digital transformation positively impacted the performance of Vietnamese commercial banks. Besides, they also discovered that the larger the banks, the greater the positive impact of digital transformation on bank performance. Therefore, the efficiency of digital transformation depends on the bank scale.

Siswanti et al. [2] presented a green business model for Islamic rural banks in Indonesia through the role of digital banking in moderating the influence of corporate governance on the sustainable business of those banks. They asserted that digital transformation significantly affected the banks’ sustainable business. Based on this explanation, the following hypothesis is put forward:

H3: Digital transformation moderates the effect of quality financing on sustainable business.

2.5.4 Digital transformation in moderating the effect of quality capital on sustainable business

Digital transformation is revolutionizing how people and businesses operate, significantly improving customer service, business operations, and new business models [22]. Vial [23] provided a more detailed explanation of transformation. Digital transformation is a process that tries to improve an entity by significantly altering its properties by combining information, processing, and communication with networking technologies. This definition exemplifies how modern technology can fundamentally change how businesses operate. Given that the concept of digital transformation has advanced, it makes sense that organizations would modify and diversify their operational processes. Siswanti et al. [2] presented a green business model for Islamic rural banks in Indonesia through the role of digital banking in moderating the influence of corporate governance on their sustainable business, and stated that digital transformation played a significant role. Based on this description, the following hypothesis is offered:

H4: Digital transformation moderately affects quality capital for sustainable business.

Based on the description of the hypotheses above, the conceptual framework is made, as shown in Figure 1.

Figure 1. Conceptual framework

This study examined the disclosure of the role of digital banking in moderating the impact of financing and capital quality on the sustainable business of Islamic rural banks in Indonesia. Thus, it can be said that this type of investigation is explanatory, i.e., explaining the variables studied and their relationship to one another. The positivist paradigm was employed, because this research was carried out quantitatively by measuring the variables of the model and analyzing the effect of one variable on another. The sample size was 165 Islamic rural banks in Indonesia, while 30 were selected. The selection criteria were Islamic rural banks with total assets of more than IDR 100 billion, which continuously reported annual reports and always generated profits during the research period, due to the concentration of Indonesia's money velocity in these four cities. The research data were secondary to the financial and annual reports for 2016-2021, and they were obtained via the website of www.ojk.go.id. Table 2 shows the operational definition and measurement.

Each research variable is measured as follows:

(i) The sustainable business variable is measured in the three aspects of economic, social and environmental performance as follows: (a) economic performance is measured by ROA; (b) social performance is measured by self-assessment through ten questions concerning the GRI-G4; (c) environmental performance is measured by self-assessment through eight questions concerning the GRI-G4.

(ii) The digital transformation variable is measured by the total investment value, which is standardized via Eq. (1), for IT development.

(iii) The quality financing variable is divided into several groups in banking practice, namely, Group I (the current group), Group II (the group for special attention), Group III (the substandard group), Group IV (the doubtful group), and Group V (the non-performing group). To measure the financing quality, the NPF was calculated using Eq. (2). It should be noted that special financing for Groups III, IV, and V is included in the NPF.

(iv) The quality capital variable shows the bank's ability to maintain existing capital and cover possible losses in providing financing/credit. The capital quality is measured using the CAR, which is an indicator of the health of bank capital. Eq. (1) was used to measure the adequacy of capital owned by the bank to support assets containing risk, such as credit/financing.

Table 2. Operational definition and measurement

|

Variable |

Operational Definition |

Measurement |

|

Quality Financing |

The ratio used to measure a bank's ability to bear the risk of default on credit repayments from debtors |

NPL = (Non-performing loan/ total loan) $\times$ 100% |

|

Quality Capital |

A financial ratio that shows how a bank can provide funds to protect against possible business losses |

CAR = (Total equity/ATMR) $\times$ 100% |

|

Transformation Digital |

Digital transformation is using technology to transform analog processes into digital ones. |

Investment costs Information technology |

|

Sustainable Business |

Sustainability in business refers to a company's strategy to reduce the negative environmental impact of its operations in a particular market. |

Profit (Economic performance) People (Social performance) Planets (Environmental performance) |

3.1 Data processing and analysis and discussion

Data were processed and analyzed using EViews 10, aiming for the significance of multiple linear regression analysis of panel data. The stages of data processing techniques using EViews 10 are described below. Basuki and Prawoto [24] claimed three techniques to determine the model estimation method using panel data:

(i) Common effect model

This model technique is the simplest because it combines the time series and the cross-section data. Instead of paying attention to the dimensions of time or individuals, company data are assumed to be the same in various periods.

(ii) Fixed effect model

The model technique assumes different effects between individuals. The difference is accommodated by the difference in the intercept, which means the difference between managerial and intensive work cultures.

(iii) Random effect model

This model estimates panel data for disturbance variables, which are likely to determine the relationship between individuals and time. This model removes heteroscedasticity, which is its benefit.

3.2 Tests

Then the testing stages using EViews 10 are divided as follows:

(i) Chow test

This test chooses the best model from the fixed-effect and common-effect models based on the data. The testing aims to determine which fixed and common effect model techniques to use. In this instance, the significance threshold of 0.05 yields the F-count value, supporting the following hypotheses:

H0: Common effect

H1: Fixed effect

H0 is rejected if F-count < 0.05, indicating that the fixed effect model was applied. In the meantime, H0 is acceptable if F-count > 0.05, suggesting that the common effect model was employed.

(ii) Hausman test

It is a statistical assessment to identify the right model between the fixed and random effect models. The hypotheses are as follows:

H0: Random effect

H1: Fixed effect

A probability value can be obtained by testing these two models. If the probability value is greater than 0.05, H0 is accepted, suggesting that the random effect model is the more appropriate one. On the other hand, H1 is accepted, and the fixed effect model is the appropriate one if the probability value is less than 0.05.

(iii) Lagrange multiplier (LM) test

A statistical test is used to select the best model from the common and random effect models. The following are the hypotheses:

H0: Common effect

H1: Random effect

The test results between these two models are shown by the probability value. The random effect model is the appropriate one, and H0 is rejected if the probability value is less than 0.05. The common effect model is the appropriate one, and H1 is rejected if the value is greater than 0.05.

4.1 Descriptive statistics

The descriptive analysis provides a comprehensive overview of the study data, encompassing several statistical measures, such as the quantity of data, lowest and maximum values, mean, and standard deviation. Table 3 displays the findings of the study's descriptive statistics.

Table 3. Descriptive statistics

|

|

Y |

X1 |

X2 |

Z |

|

Mean |

0.384111 |

7.850833 |

23.61617 |

22.17122 |

|

Median |

1.930000 |

5.475000 |

19.96500 |

22.03500 |

|

Maximum |

409.2000 |

50.76000 |

92.83000 |

25.17000 |

|

Minimum |

83.54000 |

0.040000 |

8.960000 |

19.61000 |

|

Std.Dev |

65.53551 |

7.476189 |

12.10085 |

1.302816 |

|

Skewness |

1.393548 |

2.068792 |

2.480614 |

0.205347 |

|

Kurtosis |

9.776873 |

9.332805 |

11.73182 |

2.578898 |

|

Jarque-Bera |

402.7044 |

429.1801 |

756.4383 |

2.594980 |

|

Probability |

0.000000 |

0.000000 |

0.000000 |

0.273217 |

|

Sum |

69.14000 |

1413.150 |

4240.910 |

3990.820 |

|

Sum Sq.Dev |

768787.5 |

10004.92 |

26211.09 |

304.2887 |

|

Observation |

180 |

180 |

180 |

180 |

Note: Y: Sustainable business; X1: Quality financing; X2: Quality capital; Z: Digital transformation

Source: data processed (2023)

Table 3 shows the descriptive statistics of the variables employed in this investigation. The business sustainability variable of Islamic rural banks ranged from 83.54 to 409.20 in value, with an average of 0.384111 and a standard deviation of 65.53551, as shown in the above table. The standard deviation is higher than the average value, indicating a fairly significant difference between the lowest and greatest business sustainability values.

According to Table 3, the non-performing finance variable has an average value of 7.85 and a standard deviation of 7.4761. Its lowest value is 0.040, and its largest value is 50.760. Moreover, its value ranges from 7.85 to 50.760. These results imply little discernible difference between the highest and lowest non-performing financial scores, with the standard deviation value nearly matching the average.

With the minimum and maximum values of 8.960 and 92.83, the CAR variable ranges between 8.960 and 92.83, and has an average of 23.616 and a standard deviation of 12.10. These results suggest a significant disparity between the lowest and highest values of the CAR, with the standard deviation value being lower than the average value.

Table 3 displays that the digital transformation variable has a standard deviation of 1.3028 and an average of 22.17, with values ranging from 19.61 to 25.17. With the standard deviation number being lower than the average value, it can be concluded that there is a considerable difference between the lowest and greatest levels of digital transformation.

4.2 Panel data regression model

Table 4 shows the EViews 10 testing process.

Table 4. Selection of data regression model

|

Method |

Test |

Result |

|

Chow Test |

OLS>< Fixed Effect |

Fixed Effect |

|

Hausman Test |

Fixed Effect ><Random Effect |

Fixed Effect |

|

Lagrange Test |

Common Effect >< Random Effect |

Common Effect |

Source: data processed (2023)

Then the LM test was performed to identify which common and random effect models had the better fit. It was discovered that the common effect model was the one that was employed in this investigation. Table 5 below displays the findings of the panel data regression for the common effect model.

Table 5. Common effects model

|

Variable |

Coefficient |

Std. Error |

t-Statistic |

Prob |

|

C |

10.38306 |

10.56929 |

-0.982381 |

0.3273 |

|

X1 |

-2.54576 |

0.642898 |

-3.959819 |

0.0001 |

|

X2 |

1.269693 |

0.397197 |

3.196631 |

0.0016 |

|

M1 |

0.597364 |

0.505876 |

-1.180851 |

0.0239 |

|

M2 |

0.123061 |

0.261914 |

0.469853 |

0.0390 |

|

R-Squared |

0.627293 |

Mean dependent var |

0.384111 |

|

|

Adjusted R-squared |

0.612418 |

S.D. dependent var |

65.53551 |

|

|

S.E. of regression |

61.74204 |

Akaike info criterion |

11.10578 |

|

|

Sum squared resid |

670926.0 |

Schwarz criterion |

11.17673 |

|

|

Log-likelihood |

-995.5201 |

Ahnnan-Quinn criteria |

11.13455 |

|

|

F-statistic |

8.557147 |

Durbin-Watson stat |

1.242375 |

|

|

prob (F-statistic) |

0.000025 |

|||

Source: data processed (2023)

4.3 Hypothesis test

Table 4 shows the EViews 10 testing process.

4.3.1 F-test

The F-test was used to evaluate the simultaneous impact of the independent variables in the regression model on the dependent variable. The confidence level for hypothesis testing is 95%, or 0.05 (5%).

Table 6. F-test

|

Coefficient |

|

Coefficient |

|

|

R-Squared |

0.627293 |

Mean dependent var |

0.384111 |

|

Adjusted R-squared |

0.612418 |

S.D. dependent var |

65.53551 |

|

S.E. of regression |

61.74204 |

Akaike info criterion |

11.10578 |

|

Sum squared resid |

670926.0 |

Schwarz criterion |

11.17673 |

|

Log-likelihood |

-995.5201 |

Ahnnan-Quinn criteria |

11.13455 |

|

F-statistic |

8.557147 |

Durbin-Watson stat |

1.242375 |

|

prob (F-statistic) |

0.000025 |

Source: data processed (2023)

Based on Table 6 above, the results for a prob (F-statistic) of 0.000025 can be obtained. It can be concluded that the prob value (F-statistic) is smaller compared to the five percent alpha. Due to the rejection of H0 and the acceptance of Ha, it can be inferred that the NPF and the CAR simultaneously affect the business sustainability of Islamic rural banks.

4.3.2 Partial test (t-test)

With a significance level of α = 5%, the t-test was utilized to partially test the hypothesis and demonstrate the impact of each independent variable separately on the dependent variable. In this research, the significance threshold of 0.05 was frequently utilized [25].

Table 7. t-test

|

Variable |

Coefficient |

Std. Error |

t-Statistic |

Prob |

|

C |

10.38306 |

10.56929 |

-0.982381 |

0.3273 |

|

X1 |

-2.54576 |

0.642898 |

-3.959819 |

0.0001 |

|

X2 |

1.269693 |

0.397197 |

3.196631 |

0.0016 |

|

M1 |

0.597364 |

0.505876 |

-1.180851 |

0.0239 |

|

M2 |

0.123061 |

0.261914 |

0.469853 |

0.0390 |

Source: data processed (2023)

As for the impact of the independent variables on the dependent variable, the following conclusions can be drawn from the t-test results in Table 7.

To answer the research questions and hypotheses, all hypotheses were tested for requirement satisfaction or statistical use as a measurement model in this study, based on the statistical test results. The F-test was conducted to determine the simultaneous effect of the independent variables on the dependent variable. The confidence level for hypothesis testing is 95%, or a = 0.05 (5%). Based on Table 7, the prob (F-statistics) result is 0.00000. Thus, it can be concluded that the prob value (F-statistics) is < 5%.

The first hypothesis predicts the impact of the NPF on the business sustainability of Islamic rural banks (X1). The result shows that t-statistics > a = 5%, indicating NPF’s impact on business sustainability. Based on the empirical result of the t-test, the influence of NPF on sustainability is 3.959819, and the probability value is 0.00000.05. Thus, it means that, for the first hypothesis, NPF has a materially adverse and significant impact on the sustainability of the operations of those banks.

The second hypothesis posits that quality capital has a significant positive effect on sustainable business (X2). The outcome shows that quality capital considerably benefits sustainable business, as indicated by t-statistics > a = 5%. The CAR has a substantial impact on sustainable business, as evidenced by the t-test results. The effect of the CAR on sustainability is 3.196631, and the probability value is 0.0000<0.05, supporting the second hypothesis.

According to the third hypothesis, digital transformation moderates the effect of quality financing on sustainable business (M1). The result shows that digital transformation moderates the effect of quality financing on sustainable business, as indicated by t-statistics > a = 5%. As determined by a t-statistic examination, the role of digital transformation in reducing NPF's impact on the sustainability of Islamic rural banks has a probability value of 0.0239<0.05 and a t-statistic value of 2.282216. Thus, the third hypothesis is accepted, which describes that NPF's impact on the banks' sustainability business is moderated by digital transformation.

The fourth hypothesis anticipates that digital transformation moderately affects quality capital for sustainable business (M2). The result exhibits that digital transformation moderately affects quality capital for sustainable businesses, with t-statistics > a = 5%. The t-test results have a probability value of 0.0390<0.05 and a t-statistic value of 2.469853. As a result, the fourth hypothesis is supported, which states that the influence of digital transformation might help the business operations of those banks remain viable by reducing the impact of their CAR.

4.3.3 Coefficient of determination (R2) test

The extent to which the model accounts for the variation in the dependent variable is indicated by the coefficient of determination, R2. The coefficient is between 0 and 1. The low adjusted R2 value indicates that the independent variable's capacity to explain variation in the dependent variable is severely constrained. If the adjusted R2 value gets closer to 1, the greater the variation in the independent variables, the greater the variation in the dependent variable [26]. The coefficient was performed using EViews 10.0, which yielded the findings below. Table 8 shows the coefficient of the determination test.

Table 8. Coefficient of determination test

|

|

Coefficient |

|

Coefficient |

|

R-Squared |

0.627293 |

Mean dependent var |

0.384111 |

|

Adjusted R-squared |

0.612418 |

S.D. dependent var |

65.53551 |

|

S.E. of regression |

61.74204 |

Akaike info criterion |

11.10578 |

|

Sum squared resid |

670926.0 |

Schwarz criterion |

11.17673 |

|

Log-likelihood |

-995.5201 |

Ahnnan-Quinn criteria |

11.13455 |

|

F-statistic |

8.557147 |

Durbin-Watson stat |

1.242375 |

|

prob (F-statistic) |

0.000025 |

Source: data processed (2023)

Assuming the above processing results, the adjusted R2 came out to 0.612418. This value can be explained by the fact that the non-performing financing (NPF) and capital adequacy ratio (CAR) variables could explain the sustainability business variable of Islamic rural banks by 61.24%. In comparison, other variables outside the research explained the remaining 38.76%.

The discussion section discusses the hypotheses' results and the findings' implications for theory, practice, and future research. First, theoretically, the concept of digital transformation may be understood as a multidimensional domain, encompassing several segments. Various definitions have been proposed by scholars in response to the distinctions between digitalization and digital transformation. In general, Do et al. [27] claimed that digital transformation included the utilization of IT in the daily operations and management of organizations with the aim of enhancing the efficiency of operations. However, it is obvious that the advent of artificial intelligence and big data has facilitated the digitalization of other sectors, such as the banking industry. Islamic rural ranks in Indonesia are a traditional industry and a non-pioneer of IT. Second, practically, these findings consolidate the market position and achieve overtaking in corners of digital transformation, and numerous financial institutions have begun the process of digital transformation. For instance, in China, banks were asked to accelerate their digital transformation. Therefore, digital transformation needs to be performed actively.

However, the digital transformation of banks differs from that of other industries. Thus, this study makes a valuable contribution to existing knowledge by providing a theoretical framework and utilizing relevant data sources to examine the digital transformation of commercial banks. Specifically, the study focuses on the sub-dimensional assessment of this transformation process. The impact of the digital transformation on banking efficiency is still relatively new. The current research results show that the digital transformation enhances the effectiveness of Islamic rural ranks in Indonesia. This is analyzed from the perspective of Fintech and its effects. The effects of digital transformation on Islamic rural banks in Indonesia are evident in both their internal operations, performance and long-term business sustainability. Therefore, there is a certain research gap in the digital transformation of the business sustainability of Islamic rural banks. This study, thus, focuses on the impact of bank digital transformation on bank efficiency. At the same time, it also focuses on the business sustainability of Islamic rural banks. The findings of this study have the potential to contribute to the existing studies of the digital transformation of banks, as well as the research on the business sustainability of Islamic rural banks.

5.1 The effect of NPF on the sustainable business of Islamic rural banks

Based on the t-test results, it can be stated that NPF significantly negatively affects the sustainable business of Islamic rural banks. Considering that a high-level NPF affects the sustainable business of those banks, they must always maintain the quality of their financing, which is reflected in their NPF. NPF is a very important matter for all banks to pay attention to, including Islamic banks. Therefore, Islamic rural banks should take into account that a high NPF affects their liquidity and profitability, ultimately affecting their sustainable business. Given the high value of NPF, the allowance for possible write-offs of earning assets increases, which erodes or reduces bank capital and revenue, and makes banks insolvent.

The findings of this hypothesis are confirmed and consistent with the research of Kurniawansyah and Mutmainah [5], who stated that NPF affected the sustainable Islamic banking business in Indonesia. Meanwhile, Oganda et al. [28] stated that NPF significantly negatively affected commercial bank business in Kenya. In addition, Chege and Bichanga [29] asserted that NPF significantly negatively affected commercial bank business in Kenya. However, the outcomes of this study differ from those of Masrurroh and Mulazid [6], who stated that NPF did not affect sustainable business.

5.2 The effect of CAR on the sustainable business of Islamic rural banks

According to the t-test results, the CAR has a significant positive effect on the sustainable business of Islamic rural banks. Capital is an essential factor in developing businesses and obtaining profits, and all company activities are highly dependent on the existence and adequacy of capital. The size of the business is closely related to the capital owned by the company. Thus, it can be concluded that if the CAR of Islamic rural banks is sufficient, this affects their performance, thereby influencing their sustainable business.

Thus, the findings of the second hypothesis verify and are consistent with those of Okoye et al. (2017), who reported that CAR had a significant positive effect on the financial performance of commercial banks in Nigeria, leading to an impact on the business sustainability of commercial banks in Nigeria. Likewise, Dao and Nguyen [30] stated that CAR significantly positively affected bank performance in Vietnam. Sumiati and Karmila [31] also stated that the quality of capital reflected in CAR significantly affected the financial performance of banks. Besides, Sukmadewi [32] stated that CAR significantly affected banks’ financial performance. All the results of these studies show that CAR ultimately affects the sustainability of banks.

5.3 The effect of CAR on the sustainable business of Islamic rural banks

The study results show that digital transformation moderates the effect of NPF on the sustainable business of Islamic rural banks. Bearing in mind that a high-value NPF disrupts the performance of those banks, the level of NPF must always be maintained to not exceed a predetermined limit, thereby not affecting the sustainable business of those banks in Indonesia. Further, digital transformation is expected to strengthen the influence of NPF on their sustainable business. As is known, today's technology continues to develop rapidly, including technology in banking and finance, and technological developments are expected to provide solutions to help facilitate business affairs. There is no business that is not in contact with technology, especially the banking business, including the Islamic rural banking business. As such, Islamic rural banks must change as the business environment changes with digitalization. Islamic rural banks must also improve themselves following the big currents of change, namely digitization. Recently, competitors have emerged from digital banks, especially not only on the savings side but also on the credit side. Especially since the COVID-19 pandemic, the digital economy is growing rapidly. Since everything is suddenly digital, the steps that Islamic rural banks take are to collaborate well with various bank and non-bank financial institutions, which at least increases the market share, expands the economic sector and business models, and, most importantly, improves the efficiency and effectiveness of the lending business.

The results of the third hypothesis support and are consistent with the research of Koetter and Noth [33], stating that digital transformation resolves information asymmetry and helps reduce competitive pressures. IT contributes to increasing the productivity and competitiveness of banks, thereby increasing their sustainability. The research results of Kleis et al. [34] also stated that the use of IT in innovation and knowledge creation processes increased the success of companies in the long term, and IT contributed to the development of innovations, thereby increasing the company's business sustainability. A study by Yanti et al. [19] found that innovation and technological development significantly affected the sustainability of microenterprises. Likewise, Oláh et al. [20] revealed that Industry 4.0 significantly affected environmental sustainability.

5.4 Digital transformation in moderating the effect of the CAR on sustainable business

The study results demonstrate that digital transformation moderates the effect of the CAR on the sustainable business of Islamic rural banks. As is known, capital adequacy for those banks needs to be maintained, considering that all their activities are highly dependent on capital adequacy. If their capital level is strong, their business continues.

Results of the fourth hypothesis corroborate and are consistent with those of Okoye et al. [35], stating that CAR has a significant positive effect on the financial performance of commercial banks in Nigeria, thereby affecting the business sustainability of commercial banks in Nigeria. Also, Dao and Nguyen [30] stated that the CAR significantly positively affected bank performance in Vietnam. Berger and Bouwman [36] asserted that the capital factor helped small banks increase their chances of survival during a crisis and improved their performance in both the medium and long terms. As for digital transformation, Beccalli [37] stated that investment in IT affected bank performance to the point where the business sustainability of banks was affected.

Four main findings can be drawn from this study: i) The NPF significantly negatively affects the sustainability business of Islamic rural banks; ii) The CAR significantly positively affects their sustainability business; iii) Digital transformation moderates the NPF's effect on the sustainability business of those banks; iv) Digital transformation moderates the CAR's influence on the banks’ sustainability business. Therefore, Islamic rural banks must always maintain their financing quality, which is reflected in a high-level NPF, considering that high levels of NPF affect their sustainability business.

Thus, as is known, capital is an important factor in developing businesses and obtaining profits, and all company activities are very dependent on the existence and adequacy of capital. Likewise, the NPF level must always be maintained so that it does not exceed a predetermined limit, bearing in mind that high NPF values disrupt the performance of Islamic rural banks, thereby affecting their sustainability business. Finally, the capital adequacy of those banks needs to be maintained, considering that all their activities are highly dependent on capital adequacy. If Islamic rural banks have a strong level of capital adequacy, their business will continue. The practical contribution of this research provides evidence that digital transformation enhances the business sustainability of Islamic rural banks within the context of the rapid changes in the digital economy and technology. Moreover, the digital transformation of banks has been getting more attention, but mostly at a macro level, as these findings demonstrate that digital transformation is a kind of market value management.

Furthermore, this research provides a reference for digital transformation firms to accelerate their business sustainability. This study answers all four research questions. However, perhaps more related questions will be raised in the future, such as the level of implementation of digital transformation in the banking industry.

This research has two main limitations: i) the samples used were specific to Islamic rural banks located on the largest island called Java Island in Indonesia. However, Indonesia is a large country with seven main islands; ii) data about all banks in Indonesia cannot be accessed and collected, which might slightly affect the interpretation of the findings. Accordingly, there are several suggestions for the research as follows:

[1] Siswanti, I. (2019). Determination of sustainable business factors of Islamic banks in Indonesia. The International Journal of Accounting and Business Society, 27(2): 137-158. https://doi.org/10.21776/ub.ijabs.2019.27.2.7

[2] Siswanti, I., Imaningsih, E.S., Yusoff, Y.M., Prowanta, E. (2022). The role of Islamic intellectual capital and financial performance on sustainability business Islamic banks in Indonesia. Seybold, 17(7): 1187-1206. https://doi.org/10.5281/zenodo.6938193

[3] Katsamakas, E. (2022). Digital transformation and sustainable business models. Sustainability, 14(11): 6414. https://doi.org/10.3390/su14116414

[4] Oktavenus, R. (2019). Analisis pengaruh transformasi digital dan pola perilaku konsumen terhadap perubahan bisnis model perusahaan di Indonesia. Jurnal Manajemen Bisnis dan Kewirausahaan, 3(5): 44. https://doi.org/10.24912/jmbk.v3i5.6080

[5] Kurniawansyah, D., Mutmainah, S. (2013). Analisis hubungan financial performance dan corporate social responsibility. Diponegoro Journal of Accounting, 2(2): 676-687.

[6] Masrurroh, D.A., Mulazid, A.S. (2017). Analisa pengaruh size perusahaan, capital adequacy ratio (CAR), non perfoming financing (NPF), return on asset (ROA), financing deposit ratio (FDR) terhadap pengungkapan corporate social responsibility (CSR) bank umum syariah di Indonesia periode 2012-201. Human Falah, 4(1): 1-18. http://doi.org/10.30829/hf.v4i1.622

[7] Johnson, D.W., Johnson, R.T., Stanne, M.B. (2000). Cooperative learning methods a meta-analysis. Minneapolis: University of Minnesota.

[8] Rahmi, N., Anggraini, R. (2013). Pengaruh car, bopo, npf, dan csr disclosure terhadap profitabilitas perbankan syariah. Urnal Ilmiah Wahana Akuntansi, 8(2): 171-187.

[9] Rashid, A., Asif, F.M.A., Krajnik, P., Nicolescu, C.M. (2013). Resource conservative manufacturing: An essential change in business and technology paradigm for sustainable manufacturing. Journal of Cleaner Production, 57: 166-177. https://doi.org/10.1016/j.jclepro.2013.06.012

[10] Elkington, J. (1998). Cannibals with Forks: The Triple Bottom Line of 21st Century Business. New Society Publishers.

[11] Westerman, G., Bonnet, D., McAfee, A. (2011). Leading Digital: Turning Technology into Business Transformation. Harvard Business Review Press.

[12] Nugroho, L. (2021). The role of information for consumers in the digital era (Indonesia case). Artvin Çoruh Üniversitesi Uluslararası Sosyal Bilimler Dergisi, 7(2): 49-59. https://doi.org/10.22466/acusbd.1017850

[13] Riyadh, H.A., Sultan, A.A., Abdurahim, A., Sofyani, H. (2020). The effect of Iraq’s dinar exchange rate against UK pound on Iraq’s export to UK. Journal of Critical Reviews, 7(2): 51-55. https://doi.org/10.31838/jcr.07.02.12

[14] Utami, W., Nugroho, L., Mappanyuki, R., Yelvionita, V. (2020). Early warning fraud determinants in banking industries. Asian Economic and Financial Review, 10(6): 604-627. https://doi.org/10.18488/journal.aefr.2020.106.604.627

[15] Dendawijaya, L. (2005). Manajemen Perbankan (2nd ed.). Ghalia Indonesia.

[16] Siamat, D., Kusumawardhani, P.N., Agustin. (2005). Manajemen Lembaga Keuangan (2nd ed.). Lembaga Penerbit Fakultas Ekonomi Universitas Indonesia.

[17] Jathurika, M. (2019). Impact of non-performing loans on financial performance: A case of Sri Lankan listed commercial banks. International Journal of Accounting and Business Finance, 5(1): 86. https://doi.org/10.4038/ijabf.v5i1.41

[18] Kipruto, J.J., Wepukhulu, J.M., Osodo, O.P. (2017). The influence of capital adequacy ratio on the financial performance of second-tier commercial banks in Kenya. International Journal of Business and Management Review, 5(10): 13-23. https://doi.org/10.37745/ijbmr.2013

[19] Yanti, V.A., Amanah, S., Muldjono, P., Asngari, P. (2018). Faktor yang mempengaruhi keberlanjutan usaha mikro kecil menengah di bandung dan bogor. Jurnal Pengkajian dan Pengembangan Teknologi Pertanian, 20(2): 137-148.

[20] Oláh, J., Aburumman, N., Popp, J., Khan, M.A., Haddad, H., Kitukutha, N. (2020). Impact of industry 4.0 on environmental sustainability. Sustainability, 12(11): 4674. https://doi.org/10.3390/su12114674

[21] Do, T.D., Pham, H.A.T., Thalassinos, E.I., Le, H.A. (2022). The impact of digital transformation on performance: Evidence from Vietnamese commercial banks. Journal of Risk and Financial Management, 15(1): 21. https://doi.org/10.3390/jrfm15010021

[22] Jathurika, M. (2019). Impact of non-performing loans on financial performance: A case of Sri Lankan listed commercial banks. International Journal of Accounting and Business Finance, 5(1): 86. https://doi.org/10.4038/ijabf.v5i1.41

[23] Oláh, J., Aburumman, N., Popp, J., Khan, M.A., Haddad, H., Kitukutha, N. (2020). Impact of industry 4.0 on environmental sustainability. Sustainability, 12(11): 4674. https://doi.org/10.3390/su12114674

[24] Do, T.D., Pham, H.A.T., Thalassinos, E.I., Le, H.A. (2022). The impact of digital transformation on performance: Evidence from Vietnamese commercial banks. Journal of Risk and Financial Management, 15(1): 21. https://doi.org/10.3390/jrfm15010021

[25] Abdulquadri, A., Mogaji, E., Kieu, T.A., Nguyen, N.P. (2021). Digital transformation in financial services provision: A Nigerian perspective to the adoption of chatbot. Journal of Enterprising Communities: People and Places in the Global Economy, 15(2): 258-281. https://doi.org/10.1108/JEC-06-2020-0126

[26] Vial, G. (2019). Understanding digital transformation: A review and a research agenda. The Journal of Strategic Information Systems, 28(2): 118-144. https://doi.org/10.1016/j.jsis.2019.01.003

[27] Basuki, A.T., Prawoto, N. (2017). Analisis Regresi Dalam Penelitian Ekonomi & Bisnis: (Dilengkapi Aplikasi SPSS & Eviews) (2nd ed.). Jakarta RajaGrafindo Persada.

[28] Ghozali, I. (2016). Aplikasi analisis Multivariate Dengan Program SPSS. Badan Penerbit UNDIP.

[29] Ghozali, I. (2013). Aplikasi Analisis Multivariat Dengan Program IBM SPSS (7th ed.). Penerbit Universitas Diponegoro.

[30] Do, T.K., Lai, T.N., Tran, T.T.C. (2020). Foreign ownership and capital structure dynamics. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4306100

[31] Oganda, A.J., Mogwambo, V.A., Otieno, S. (2018). Effect of cash reserves on performance of commercial banks in Kenya: A comparative study between national bank and equity bank Kenya limited. International Journal of Academic Research in Business and Social Sciences, 8(9). https://doi.org/10.6007/IJARBSS/v8-i9/4648

[32] Chege, L.M., Bichanga, J. (2017). Non-performing loans and financial performance of banks: An empirical study of commercial banks in Kenya. International Journal of Management and Commerce Innovations, 4(2): 909-916.

[33] Dao, B.T.T., Nguyen, K.A. (2020). Bank capital adequacy ratio and bank performance in Vietnam: A Simultaneous equations framework. The Journal of Asian Finance, Economics and Business, 7(6): 39-46. https://doi.org/10.13106/jafeb.2020.vol7.no6.039

[34] Sumiati, A., Karmila, E. (2016). The effect of CAR and non performing loan (NPL) on conventional commercial bank financial performance for 2013-2015 Period. Jurnal Ilmiah Wahana Akuntansi, 11(2): 1-16.

[35] Sukmadewi, R. (2020). The effect of capital adequacy ratio, loan to deposit ratio, operating-income ratio, non performing loans, net interest margin on banking financial performance. ECo-Buss, 2(2): 1-10. https://doi.org/10.32877/eb.v2i2.130

[36] Koetter, M., Noth, F. (2013). IT use, productivity, and market power in banking. Journal of Financial Stability, 9(4): 695-704. https://doi.org/10.1016/j.jfs.2012.06.001

[37] Kleis, L., Chwelos, P., Ramirez, R.V., Cockburn, I. (2012). Information technology and intangible output: the impact of IT investment on innovation productivity. Information Systems Research, 23(1): 42-59. https://doi.org/10.1287/isre.1100.0338