Maksym Dubyna*![]() | Olena Panchenko

| Olena Panchenko![]() | Tetiana Shpomer

| Tetiana Shpomer![]() | Olena Shyshkina

| Olena Shyshkina![]() | Iryna Kosach

| Iryna Kosach![]() | Olena Bazilinska

| Olena Bazilinska![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The article attempts to justify the importance of ensuring the stable development of the payment infrastructure in crisis conditions, which are formed by unpredictable and turbulent processes in the development of the financial system. It was determined that in the modern conditions of active digitization of the activities of financial institutions, their leading role in making settlements between economic entities, the emergence of destructive processes in the functioning of these institutions may have a negative impact on the functioning of the national economy, the state of its economic security, especially as a result of complex political and social events in the country. During the research, a range of general and special research methods were used, among which content analysis, statistical methods, and methods of generalization and abstraction played an important role. The article describes the theoretical provisions of the influence of the payment infrastructure on the state of economic security of the country, substantiates the main transformational processes that are taking place with such infrastructure today as a result of the development of information and communication technologies. To confirm the formulated theoretical provisions, the case of Ukraine was considered as a country that periodically finds itself in difficult socio-political conditions of its own functioning, and today the war with the Russian Federation has already led to colossal economic losses and a significant decrease in the level of economic security. In this way, the macroeconomic development of Ukraine during 2010-2022 was analyzed. Important attention is focused on the analysis of the state of the payment infrastructure in the country, how its development changed during the outlined period, and what transformations took place in its functioning since the beginning of Russia's military aggression against Ukraine. The results of the study made it possible to confirm the assumption about the important role of the payment infrastructure in ensuring the economic security of the country and the importance of ensuring the stable functioning of such infrastructure even in difficult political, social and economic conditions. It was also established that in the era of the development of the digital economy, it is the payment infrastructure that can minimize the destructive consequences of turbulent economic processes and ensure the availability of financial services.

payment infrastructure, economic security of the state, digitalization, financial services market, financial institutions, infrastructure

Ensuring the economic security of the state is one of the most difficult tasks. In modern conditions, taking into account the dynamism of the world economy, close interaction between the governments of different countries, their economic systems, a significant number of factors are formed in the external environment, which can have a destructive effect on economic relations and lead to deterioration of the economic development of countries. Accordingly, in this context, the state regulation system of economic relations is changing today, the methods and tools used by state authorities to influence the activities of economic entities in order to ensure the stability of the national economy functioning are becoming more complicated.

The economic security of the country is an integral component of the formation of a solid foundation for the development of economic entities. This is a multifaceted and complex concept, which includes a number of components that reflect the stability level in various directions of the development of economic relations. It is this multi-structuredness of this concept that complicates the process of ensuring the economic security level in the long term. It is especially difficult to carry out in the conditions of complex socio-economic shocks that governments may face in a specific period of the state's functioning. The imbalance of the economic development occurs in such cases due to many reasons, but the consequences of the recovery of the national economy and its stability can last for years.

The financial system is an integral component of the economic development of countries and today plays a key role in ensuring stable functioning of economies in all developed countries. This type of security is primarily related to the ability to produce necessary resources for the economy development, the activities of economic entities in the long term. However, history proves that it is within the financial system that critical situations often arise, which quickly spread to the functioning of economic systems, lead to economic crises and thereby reduce the economic security level to a critical value for the country.

Ensuring the country's financial security also requires governments and central banks to implement a complex financial policy, the implementation of which allowed, on the one hand, to prevent potential fluctuations within the country's economy and its financial system, and on the other hand, to create opportunities to counter crisis situations and reduce their impact on economic and financial relations.

Directly in the modern world of the wide-spread of digital technologies, the payment system plays an important role in the formation of the country's financial system. In general, this system today is an integral component of the development of the country's financial system, ensuring the normal functioning of the entire banking system. In today's world, payment instruments play a key role in shaping the economic behavior of economic entities. It should be noted that digitization processes had a significant and positive impact on the payment system functioning and led to its radical transformation, which contributed to the increase in the convenience of making payments, circulation of financial resources between economic agents, etc.

The payment infrastructure is an integral part of the payment system and provides the possibility of its development in the long term. A significant deterioration in this infrastructure functioning immediately negatively affects the operation of the banking system, which in turn quickly creates the conditions for deterioration of the level of financial and economic security of the country. That is why the development of payment infrastructure in the modern world is an important element of ensuring the accelerated development of economic relations. This is especially important for the countries in which the financial system is at an insufficiently high level of its own development, or those countries that are facing complex socio-political upheavals caused by internal and external factors.

In today's world, the role of digital technologies in the development of payment infrastructure is enormous, and such technologies actually change the established models of the functioning of such infrastructure. It is the virtualization of the payment infrastructure, the expansion of the possibilities of Internet technologies in making settlements between economic entities that makes it possible to level the influence of physical branches of financial institutions on the timeliness of such settlements and makes it possible to increase the flexibility of banking and non-banking institutions in providing settlement services to clients as a result of disruption of their own activities , the emergence of deep crisis phenomena in the functioning of the country's economy. At the same time, from a macroeconomic point of view, it is the virtualization of the payment infrastructure that should provide an opportunity for financial institutions to ensure the stable functioning of the national payment system and thereby contribute to avoiding the stoppage of settlement operations in the country as a result of the onset of socio-political shocks.

The outlined actualizes the study of the role of the payment infrastructure in the financial system development, ensuring financial, as well as economic, security in the conditions of complex dissipative processes that arise within the functioning of economic systems. At the same time, the issues of analyzing the impact of digitalization on the development of the payment infrastructure, its role in modern development, are becoming relevant.

Thus, the purpose of the article is the theoretical substantiation of the role of the payment infrastructure in ensuring the level of economic security of the country in the conditions of socio-economic shocks.

To achieve this goal, the following tasks are set: to determine the essence of the payment infrastructure and its role in the functioning of the country's financial system; identify and specify the negative consequences of an inefficiently functioning payment infrastructure to ensure the economic security of the state; describe the modern transformations of the payment infrastructure, which are taking place as a result of the influence of information and communication technologies; justify the importance of digital technologies in the development of the payment infrastructure and ensuring the economic security of the country; to investigate the real case of Ukraine regarding the role of the payment infrastructure in the stability of the functioning of the national economy in the conditions of social and political shocks.

The study of issues of the digital payment infrastructure is gaining more and more relevance. Many publications by scientists are devoted to various aspects of digitization and the role of these processes in the development of regions and the country as a whole, as well as the impact and provision of the economic security [1-3].

The authors of articles [4-6] researched that at the current stage there is no effectively functioning global payment system, however, they note that mobile payments are one of the fastest growing mobile services and emphasize the analysis of the problems of modernizing the financial market infrastructure. According to the paper [4], despite the narrative of a globalized economy, there is no effectively functioning global payment system. The researchers point out that while the infrastructure exists to transmit global payment data, the movement of actual money is done indirectly, making it an unpredictable task. The reason, as noted in the study, is that money is not just data, but a complex bundle of rights closely tied to the nation-state. Within article [5], mobile payments are proven to be one of the fastest growing mobile services available today, and are widely used by smartphones for utility payments, bill payments, and online shopping, among other applications. According to Auto, mobile payments play a vital role in the rapid growth of online markets and revolutionize the supply chain of enterprises and industries; are becoming dominant over traditional offline payment channels and electronic online channels such as ATM, e-check and e-card payments. Scholars [6] explore initiatives and challenges for modernizing a financial market infrastructure in Japan. The authors note that countries and regions around the world are accelerating their efforts to develop and improve the financial market infrastructure, so they believe the Japan's Zengin system must go beyond simply offering a 24/7 real-time payment infrastructure.

A group of scientists [7-9] examines the peculiarities of forming a micropayment infrastructure based on blockchain technology, studies the possibilities of using payment tools to create programmed money and increase the energy efficiency of the payment infrastructure. The authors of the study [7] believe that sustainable micropayment infrastructures are critical assets for the digital economy as they help secure transactions and facilitate micropurchases. Scientists will propose a micropayment infrastructure based on the blockchain technology, which is able to reduce the complexity of transaction verification, reduce losses and protect against various cyber-attacks. The authors [8], pointing to various innovations developed and implemented by the payments industry over the past decade, argue that instead of waiting for digital currencies to reach maturity, it makes sense to explore how existing payment instruments can be used to create programmable money. Researchers note, that using instant payments, open banking APIs and payment requests, the industry can already create programmable money with the added benefit of speed to the market. Within the study [9], an assessment of the chain of time and energy losses, financial losses, which occur due to the imperfection of the payment infrastructure and tools, was made using the data of cashiers' working hours. The empirical results of the study provide valuable information on how best to organize payment in retail trade in order to reduce energy costs and improve the energy efficiency of the payment infrastructure.

In scientific works [10-12], the role of digital technologies in the transformation of the financial behavior of households was investigated, as well as modeling of the financial influence of political-oligarchic interests of state enterprises on the formation and implementation of the financial policy in the state was carried out.

Scientific works are of practical importance [13-16], within which developed an intelligent payment scheme for energy infrastructure based on blockchain, analyzed achievements in payment infrastructure and promising new technologies, and also analyzed the successful experience of banks. The study [13] notes that today the government actively supports the construction of intelligent networks and new digital infrastructure, so the energy infrastructure is gradually developing in the direction of intelligence and digitalization. In order to increase the timeliness and accuracy of payments to the energy infrastructure fund, to increase the reliability of data, as well as to improve the quality and efficiency of supervision and verification, the authors propose an intelligent payment scheme for the energy infrastructure based on the blockchain. The purpose of the study [14] is to analyze the transactions taking place along the border between Hong Kong and mainland China, which has experienced a sudden “tightening” due to travel restrictions imposed after the COVID-19 outbreak. Referring to the "digital transitions" notion, the authors argue that the use of the digital money infrastructure to manage such transactions should serve as a reminder to scholars to productively engage with the various forms of borders and boundaries that emerge in online spaces. It has been studied that countries and regions around the world are improving their financial market infrastructure at an accelerated pace [15]. The authors are convinced that these efforts go beyond initiatives to provide a 24/7 real-time payment infrastructure to completely new areas of innovative value-added services. Scholars examine advances in the payment infrastructure, promising new technologies, new service providers, and the relationship between inherent new value and associated risk. The authors [16] demonstrate the practical experience of a large Brazilian bank that used a very important payment application. As transactions increased, the program began to show some limitations, generating unavailability. The challenges have been overcome by distributed systems concepts such as middleware architecture; parallel processing; database and programmed procedures in operating systems.

Given a critical role of fthe inancial market infrastructures for the economy functioning, the financial stability and the monetary policy conduct, it is vital for central banks and other relevant authorities to monitor and maintain the financial market infrastructure during and after a crisis, according to scholars [17], to ensure their safe and efficient operation. The authors highlight the key issues for the infrastructure of financial markets and consider various prospective scenarios and related issues. The article [18] analyzes the factors that have led to the popularity of mobile payments in China and explains how companies in other countries can follow in the China's footsteps and benefit from this technology. The researchers describe some of the challenges that companies and other businesses may face when implementing mobile payments, and further demonstrate the risks. The study [19] discusses the Japan's payment infrastructure and the opportunities that new technology and innovation can bring to the nation's banking industry and payment services sector. The authors [20] made an attempt to compare the development of the payment card market infrastructure in Poland and China. The researchers considered the two most important components of the payment card infrastructure: the number of merchant terminals serving payment cards (POS) and the number of automated teller machines (ATMs). The empirical econometric model allows to describe the mechanisms of the payment card market infrastructure and can be used to build short-term forecasts.

Within the framework of the article [21], it was investigated that the development of the digital infrastructure and organization takes place with the help of three causal mechanisms of development: architectural, institutional and functional. According to scientists, each mechanism reveals a clear path of the digital infrastructure development based on the structure formation, behavior formation and service formation. The scientific paper [22] demonstrates critical success factors (CSFs) for implementing digital payments in India. There are several studies of the CSFs literature for the digital payment system adoption in the Indian context. The authors consider the Interpretative Structural Modeling (ISM) methodology and develop a model for effective implementation of the digital payments system in India.

Despite a significant number of publications, the issue of the digitalization role in the payment infrastructure to ensure the economic security of the state in the conditions of socio-political shocks requires further analysis and detailed study, which determined the choice of the research direction.

The article uses a wide range of scientific methods and approaches to conduct a study of the role of digitalization in the development of payment infrastructure in ensuring the economic security of the state in conditions of socio-economic shocks. The choice of methods is determined by the specifics of the researched objects and the peculiarities of their functioning. Directly with the help of a set of theoretical methods (content analysis, abstraction methods, systemic approach), the essence of the payment infrastructure was substantiated and its main types (institutional, physical payment, technological, auxiliary) were specified, the main destructive consequences for the stable functioning of the national economy were identified and systematized. ineffective functioning of the payment infrastructure, its role in ensuring the appropriate level of economic security of the country is described. The use of the historical method and statistical methods made it possible to conduct a retrospective analysis of the economic development of Ukraine, to identify periods of socio-political shocks that occurred in the country's history and affected its economic condition. The application of statistical methods also made it possible to analyze the current state of the payment infrastructure in Ukraine, to reveal the impact of digitalization on the development of such infrastructure. Based on the use of the index approach, a methodology for calculating the payment infrastructure development index was formulated, which is proposed to be determined based on the following formula:

ІIDP = (IATM + ISTC+ IPTT + I PBT)/4

where, ІIDP – index of the payment infrastructure development in the t period;

IATM – index of changes in the number of ATMs in the t period;

ISTC – index of changes in the number of self-service software and technical complexes in the t period;

IPTT – index of changes in the number of payment trading terminals in the t period;

IPBT – index of changes in the number of payment bank terminals in the t period.

In turn, the outlined indices were determined on the basis of such a formula:

It = Int/Int-1

where, It– index of the indicator in the t period;

Int – absolute value of the indicator in the t period;

Int-1 – absolute value of the indicator in the t-1 period.

The application of content analysis and methods of generalization, analysis and synthesis also made it possible to describe the main trends in the functioning of the payment infrastructure during the period of military aggression and other socio-political shocks that were and are occurring in Ukraine, to identify the main risks that may arise within the financial system from inefficient work of such infrastructure.

The data of the National Bank of Ukraine, the State Statistics Service of Ukraine, which were used to conduct a macroeconomic analysis of the dynamics of the country's economic development in the long term, and an analysis of the current state of the payment infrastructure in the country served as the information base of the scientific research. To perform calculations, all statistical information was used from the official websites of the outlined state institutes.

All calculations during the research were carried out using Microsoft Excel. At the same time, additional checks of the obtained data were also carried out, which was carried out through the empirical analysis of the parameters obtained as a result of the calculations of the annual indicators determined for the analysis.

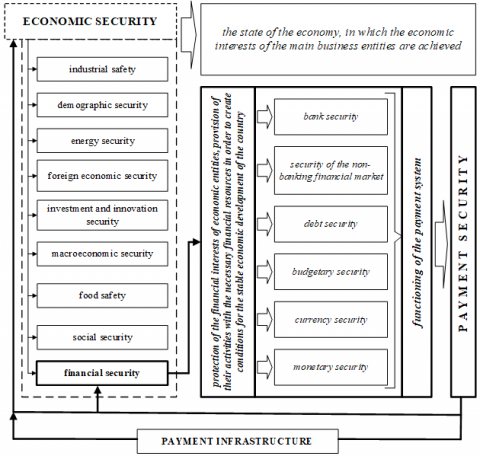

Today, the payment system is an integral part of the financial system development of any country and is a set of telecommunication technologies, business entities, rules, regulations and norms, based on which the process of the financial resources movement between various consumers of financial services takes place. Accordingly, in order for such a system to work and perform the functions assigned to it, it needs an infrastructure, that is, a complex of technical and organizational institutions that create the conditions and take an active role in the movement of the specified relations. The issue of specifying the components that should be attributed to the payment infrastructure, and which in general to the payment system is quite debatable, taking into account the constant increase in the number of different entities that participate in the organization of financial settlements in the modern conditions of the financial market functioning. However, it is quite logical that the payment infrastructure today is an integral part of the functioning of the entire payment system. In Figure 1, a conceptual diagram of the payment infrastructure functioning in the modern conditions of the financial system operation of any of the developed countries is presented.

Today, the payment infrastructure is an integral part of the financial infrastructure system, which plays a key role in the development of the country's financial system. At the same time, in the current conditions of the financial relations digitalization, the role of such infrastructure is only increasing, and its importance is only increasing not only for carrying out financial transactions, but also in general for accelerating the economic development of the country. At the same time, such infrastructure already plays an important role in ensuring the financial security of the country, and, in general, in the formation of an effectively functioning system of the national economic security.

The economic security is an important component of ensuring the conditions for the stable development of the national economy. On the other hand, it is the result of deliberate and consistent actions of governments as a result of using a successful model of the state economic policy, the implementation of which made it possible to create an appropriate level of the economic security in society.

The economic security is the state of the national economy in a static dimension, during which there is a steady increase in the rate of the national economy development, which is realized based on meeting the economic needs of business entities, stability of the macroeconomic situation, and the growth of the country's level of competitiveness in the global markets of goods and services. The GSDI provides this definition of the essence of economic security – the ability of individuals, households and communities to meet sustainably their basic and essential needs; including food, shelter, clothing, health care, education information, livelihoods, and social protection [23].

Figure 1. Theoretical provisions of the payment infrastructure functioning

Source: compiled by the authors

The complexity of the study of the economic security as an economic category and generally a mandatory component of the country's economic development lies in the fact that the stability of such development is always influenced by a significant number of different factors that can exert both positive and negative influence on the functioning of various types of business entities . Such processes occur constantly in macroeconomic systems, that is, they are always characterized by a certain level of fluctuations. Accordingly, the economic security of the country is also such a state of the national economy, in which the negative impact of these fluctuations can be quickly reduced as a result of making appropriate decisions. That is, a certain level of strength is inherent in any national economy, which determines its ability to counteract internal and external factors.

The payment infrastructure mediates the relations between various economic entities, and therefore, is an important component of the country's financial system, partially determines the stability of such system functioning and affects the level of economic turbulence in the country and, accordingly, its national economic security. The magnitude of the impact of the payment infrastructure and its irreplaceability for stable functioning of economic entities determines its important role in the formation of stable conditions for the economic growth. In Figure 2, a conceptual model of the influence of the payment infrastructure on the economic security level of the country is presented.

Figure 2. The role of the payment infrastructure in ensuring the economic security of the state

Source: compiled by the authors

In modern conditions, the destructive influence of an inefficiently functioning payment infrastructure on the national economy development and ensuring the country's economic security can be manifested in the following:

– violation of stable conditions of the business entities functioning due to delayed payments;

- untimely execution of calculations by business entities, partial breach of obligations to their partners, additional fines;

- deterioration of the interaction with financial institutions and the impossibility of obtaining credit services on time, which affects the financial condition of enterprises, especially those that have a constant need for borrowed funds to ensure the stability of their activities;

– payment discipline is deteriorating and international settlements are becoming more complicated, which affects business reputation of business entities;

- citizens' access to cash decreases, which affects their financial stability;

– queues at branches of banking institutions for citizens to carry out cash operations may grow;

- decrease in the development rate of the credit services market, which is caused by the deterioration of the situation with obtaining and issuing credit cards;

– process of making social payments deteriorates, especially for vulnerable segments of the population, which negatively affects their quality of life;

- growth in the amount of receivables and payables within the national economy, etc.

Deterioration of the payment infrastructure functioning in the country leads, first of all, to the restriction of access of all business entities to their funds and subsequently, in the long term, leads to an increase in the volume of cash transactions and, accordingly, cash and circulation. This, as evidenced by the experience of developed countries, does not contribute to the growth of financial stability in the country and thereby negatively affects the financial security level, which ultimately has a destructive effect on the resistance of the national economy to new external and internal threats.

The development of the payment infrastructure today is also important for the economic development of the country, as well as the development of individual industries and spheres of the national economy. In modern realities, such development takes place in the conditions of the digitalization of financial relations and, in general, active use of information and communication technologies by business entities, especially financial institutions.

Digitization is a complex process of gradual use of modern information technologies by various subjects in their own activities. Active use of such technologies today has led to the formation of a new type of economy - the digital economy, within which an alternative concept of ensuring development exclusively through the use of digital technologies has already been formed.

Today, digitalization is already having a significant impact on the payment system development. Gradual introduction by financial institutions of new information and communication technologies into their own activities radically changed the basic principles and mechanisms of providing payment services to economic entities, and today the payment infrastructure system continues to change actively in accordance with the new opportunities of such technologies. First of all, the following changes have already taken place in its functioning:

– share of online payments made by business entities has increased;

– new industry of online payments was formed, which are provided not only by banking, but also by non-banking financial institutions;

– there was a significant attraction of investment resources to the payment system development based on the introduction of modern digital technologies;

- there was a multiple increase in transfers of financial resources between individuals;

– digitalization of the interaction between financial institutions and their clients in the provision of payment services took place;

– availability of payment services for all business entities has increased significantly;

– increased requirements to ensure cyber security of settlement operations, protection of individual customer information;

– number of frauds and the amount of financial losses suffered by financial institutions increased;

- availability of credit resources for business entities increased, which contributed to the development of electronic credit services;

– number of types of payment services provided today by banking and non-banking institutions has increased;

– digitalization of the payment sphere ultimately led to the gradual digitalization of the operation of financial institutions, their implementation of modern information and communication technologies in virtually all spheres of their own activity;

– digitalization of payment services contributed to the emergence of virtual financial institutions that do not provide customer services in physical branches;

- digital technologies fundamentally changed the organization of work of banking institutions in terms of providing payment services, which led to the decrease in the branches of these institutions, a decrease in the number of cash registers in them, and accordingly, the number of employees.

In general, worldwide, the digitalization of payment services contributed to the development of the FinTech industry, creation of new global financial companies in the field of payment services, and contributed to the competition growth between financial institutions in the financial services market.

Digitization of the payment system creates a number of both positive and negative consequences for its development in the future, but from the standpoint of speeding up settlements between economic entities, control over the movement of financial funds, organization of payment services, the use of information and communication services allows obtaining a significant number of advantages. Especially such advantages are best manifested in periods of significant stochastic processes in the national economy development, which arise in the conditions of socio-political shocks. Any negative fluctuations in the economy undoubtedly affect the functioning of the financial system, the stability of which is significantly determined by the ability of the payment system to perform the functions assigned to it and the ability to make settlements between business entities even in difficult periods of economic turbulence in the country.

To determine and justify the applied provisions of the impact of the payment infrastructure on ensuring the economic security of the country, we will analyze the experience of the functioning of such infrastructure in Ukraine in the conditions of the war with the Russian Federation. To do this, from the beginning, we will analyze the current state of the country's development and the level of its economic security.

The invasion of Russia in 2022 led to complex consequences for the economy of Ukraine, namely:

– a significant part of the country was occupied, which affected economic relations between business entities;

– migration of a significant number of citizens abroad, closure of a large number of small enterprises;

– large number of internally displaced persons in the country;

– destruction of a large number of enterprises; the destruction and suspension of work of large enterprises, which employed thousands of workers, had a particularly negative impact on the economy development;

- constant missile attacks and blackouts, which significantly slow down the pace of the economic recovery and ensuring the stable operation of the country's industry, even in such difficult times;

- destruction of the national economy infrastructure, the destruction of a large number of bridges, the decrease in the efficiency of seaports in the country due to a difficult security situation in the Black Sea;

– occupation of significant agricultural territories in the south of the country, which had a destructive effect on the agricultural industry development;

- looting of the state institutions, hospitals, educational institutions, private enterprises by Russian troops in the territories that were liberated from occupation, etc.

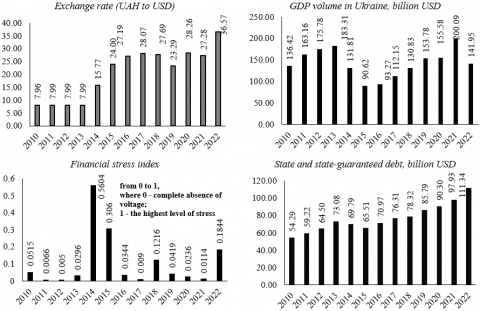

All of the above naturally affected the economic security level of the country, the stability of the national economy development. In Figure 3, individual indicators of such development in Ukraine are presented.

Thus, as a result of the aggression, the economic situation in the country became difficult and unpredictable, the functioning of the financial system and the stability of the national currency became dependent on external borrowings, loans from international financial organizations and governments. This is clearly confirmed by the data of Figure 3.

In particular, from 2010 to 2022, the rate of the national currency hryvnia decreased in Ukraine from UAH 7.96 per USD to UAH 36.57 per USD. That is, the decrease occurred almost five times. The biggest decrease occurred, first of all, in 2014-2016 and in 2022 - periods of socio-economic shocks for Ukraine. It was in 2014 that the Revolution of Dignity took place, the annexation of Crimea, the capture of the eastern regions of the country, and the Anti-Terrorist Operation. The consequences of the internal political crisis for the country were extremely complex and negative, which was reflected in macroeconomic indicators.

Figure 3. Macroeconomic indicators of Ukraine's development

Source: compiled by the authors based on data from the State Statistics Service of Ukraine

In 2022, the economic development of the country was significantly complicated by the start of the war started by the Russian Federation. The active phase of the war, millions of internally displaced persons and migrants had a destructive effect on the country's economic situation. Constant shelling of the regions of the country, large areas of the occupied territories, creation of blackouts, undermining of the Kakhovskaya HPP continued to destabilize the national economy functioning.

All destructive consequences of the impact of the outlined unpredictable and complex factors were immediately reflected in the country's GDP. Compared to 2014-2015, at the beginning of 2022, Ukraine had a greater reserve of financial strength and a more stably functioning banking system. Thanks to this and a number of adequate and correct decisions of the National Bank of Ukraine in 2022, the economy recession was not so deep. However, by the end of 2022, the Ukraine's GDP has fallen to the same level as in 2018. It should be noted that after the recession in 2014, the country's economy took eight years to reach the GDP of 2013.

The general economic condition in the country is always reflected in the financial system functioning and vice versa. Based on the analysis of the Financial Stress Index, it can be stated that the most destructive processes in the formation of the country's financial system were observed in 2014, 2015 and 2022. This, in turn, affected the stable economic development and was caused by a significant shortage of financial resources to ensure the national economy development. At the same time, from the data in Figure 3 it is shown that during the entire period for which the analysis is carried out, the volumes of the state and state-guaranteed debt have been constantly growing. If in 2010 this indicator was 54.29 billion USD, then in 2022 it will be 111.3 billion USD. In twelve years, the amount of debt has more than doubled, and this is when it is defined in USD. The national currency grew even more.

Throughout the war, Ukraine received financial assistance from the governments of other countries and international organizations. Sometimes this is on a free and non-refundable basis, but sometimes such assistance relates to the national debt and will contribute to its growth. From the economic point of view, it is difficult for Ukraine to oppose Russia with its several times larger national economy and financial capabilities. However, it is precisely at the expense of the assistance of Western countries that such countermeasures are possible. Attracting external resources also plays a key role in the purchase of weapons, payment of salaries to the military, etc.

After the start of the war, Ukraine found itself in a rather difficult and difficult economic situation, which was accompanied by a deep shock to the entire Ukrainian society. During February-March 2022, the country simply stopped economically, especially in the regions that were occupied or were on the front line. However, after the first victories in the war and the retreat of the aggressor from the north of the country (Kyiv, Chernihiv regions), business entities gradually resumed their work.

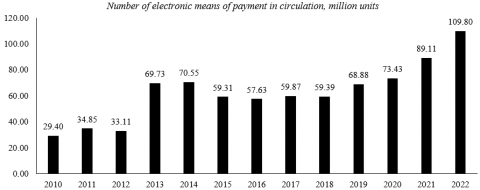

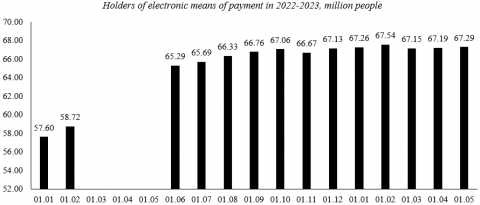

From April-May 2022, the country's banking system also began to resume its work. In the regions that were not in the combat zone, banking institutions continued their work, but within the limits established by the National Bank of Ukraine since the beginning of the war. At the same time, the payment infrastructure performed its functions. In Figure 4, information on the state of electronic payment means in Ukraine is presented.

Figure 4. Analytical information on the state of electronic payment means in Ukraine

Source: compiled by the authors based on data from the National Bank of Ukraine

Thus, at the end of 2022, the number of electronic devices in circulation in Ukraine amounted to 109.8 million units, which is significantly more than the similar indicator of 2021 and all previous periods. The sharp increase in the number of such instruments can be explained by the effects of the war on the card business. In particular, the issuance of new electronic means of payment to military personnel, internally displaced persons, citizens who have lost their documents due to the destruction of their homes, emergency relocation and departure from the residence territory. Also, a significant number of citizens opened accounts for transactions with foreign counterparties. It should be noted that the banking system (banking institutions are monopolists in Ukraine in the settlement and cash services) coped with new complex tasks and was able to fully satisfy the needs of citizens and business entities in financial services.

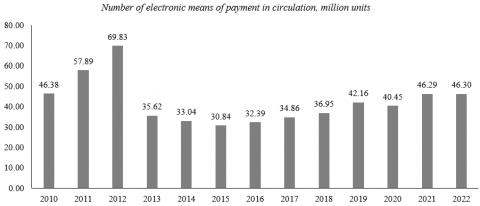

However, the number of electronic means of payment, with which at least one spending transaction was carried out during the reporting period, did not increase at a significant pace, and at the end of 2022 amounted to 46.3 million units, which is one of the highest indicators for the entire period, according to which is being researched. The highest value of this indicator was recorded in 2012 – 69.83 million units. A sharp decrease in the number of electronic means of payment, with which at least one spending transaction was carried out during the reporting period in 2013, is associated with the deterioration of the banking system functioning with the future closure of a significant number of banking institutions in the country.

Also in Figure 4, the data on the number of holders of electronic means of payment in Ukraine in 2022 (monthly information) is presented. During this period, we can observe how this indicator changed, starting from January 2022 - a period of peace and normal functioning of the financial system, ending in May 2023 - when the war had already lasted more than a year. From the data in this figure, we can see that during the outlined period, the number of holders of electronic payment means increased from 57.6 million people to 67.29 million people, almost 10 million people more. This means that the number of payment means at the disposal of many citizens in the country has increased.

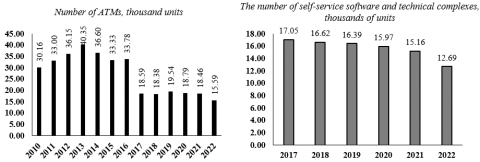

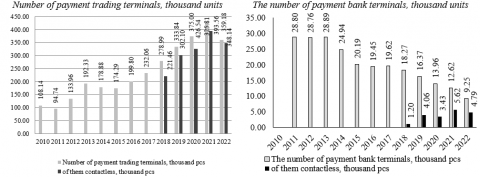

At the same time, the payment system functioning remained at a stable level in the country. In Figure 5, information on the payment infrastructure development in Ukraine is presented.

At the end of 2022, there were 15.59 thousand units in Ukraine. ATMs, 12.69 million units of self-service software and technical complexes, 359.18 thousand units payment trading terminals, of which 348.14 units were contactless. There were also 9.25 thousand pcs. payment bank terminals, of which 4.79 thousand units - contactless. Statistical data on the payment infrastructure development in the country reflect the two biggest trends in its functioning:

1) digitization of the entire financial services industry, which is reflected in the following:

- decrease in cash in circulation, which is confirmed by a decrease in the number of ATMs and payment terminals;

– growth in the number of contactless payment trading and banking terminals, which indicates the involvement of modern information and communication technologies in the financial sphere;

2) impact of the war on the payment infrastructure functioning, namely:

– accelerated decrease in the number of ATMs (from 18.46 thousand units to 15.59 thousand units) and self-service software and technical complexes (from 15.16 thousand units to 12.69 thousand units), which is explained by the destruction loss of a significant number of them in the occupied territories;

- decrease in the number of payment and banking terminals, which is again explained by a significant number of destroyed business entities, loss of their own business, closure of shopping centers and stores, the suspension of their service by Ukrainian banking institutions;

- decrease in the activity of financial companies that serviced software and technical self-service complexes, their relocation to territories under the control of the Ukrainian authorities.

- revocation by the National Bank of Ukraine of some financial institutions' licenses for conducting business activities in the field of financial services due to the deterioration of their financial condition.

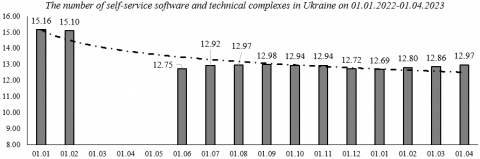

Also in Figure 5, the data on the payment infrastructure development in Ukraine in 2022-2023 is presented. Accordingly, we can state a decrease during this period in the number of both ATMs and software and technical complexes. At the same time, for March-May, information on the number of these institutions was not provided, as its collection was complicated by military actions. However, already in June 2022, a sharp decline in the number of ATMs (decrease by 18%), the software and technical self-service complexes (decrease by 16%) was recorded. During 2022, a part of these devices was restored, which was realized due to the start of work of financial institutions in the de-occupied territories and the growth of their number in regions where military operations were not carried out. However, even despite the sharp reduction of these institutions, the payment infrastructure fully satisfied the needs of economic entities in the relevant financial services.

In Figure 6, the results of the index analysis of the payment infrastructure development in Ukraine is presented, and the overall index of its development in 2010-2022 is determined.

So, in 2022, as already mentioned, a decrease in the number of the physical payment infrastructure occurred for all its types. Accordingly, the vast majority of all intermediate indices of the development of certain types of such infrastructure testify to a gradual decrease in this number, and certain indices of changes in the number of payment trading enterprises. According to this index, a decline is observed only in 2022.

The cumulative index of the payment infrastructure development shows that during 2020-2022, it is gradually decreasing. At the same time, in 2018-2019, there was a slight increase in the number of physical payment means for making payments. This growth occurred solely due to the increase in the number of payment trading terminals, which is associated with both the gradual growth of cashless payments in the country and changes in Ukrainian legislation.

It is safe to say that the gradual increase in cashless transactions will lead to a decrease in the number of physical objects of the payment infrastructure and their further virtualization. These processes are already being observed in the country today, which is possible based on the active development of the digital economy. The use of information and communication technologies by financial institutions forms a new ecosystem of payment settlements, in which a large number of banking institutions and other financial companies are already involved. In fact, it also forms a more stable basis for the payment system functioning in the country.

However, the active use of online payments, as the experience of Ukraine once again proves, is possible in the country if the normal functioning of mobile communications and the Internet is ensured. In difficult conditions of social and political shocks, this is not always possible. Accordingly, it is the combination of virtual and physical infrastructure facilities in the difficult conditions of the country's economic development that is the most optimal way to meet the needs of all categories of citizens in financial services.

Figure 5. Development of payment infrastructure in Ukraine

Source: compiled by the authors

Figure 6. Development index of the payment infrastructure

Source: compiled by the authors

The peculiarities of the payment infrastructure development of Ukraine in the conditions of military aggression and subsequent socio-political shocks that occurred in the country include the following:

- provision of online payments by financial institutions in the entire territory where there was access to the Internet, the possibility of using only a smartphone for this;

- possibility of making mutual settlements between business entities by transferring funds to accounts;

– creation of the NBU network of bank branches (Power Banking) to provide financial services to clients during the blackout period;

– quick restoration of access to credit resources for citizens, which allowed them to use credit cards during the economic crisis;

- active use of the payment system for quick and round-the-clock collection of charitable funds for military needs, support of military formations in different parts of the country;

- ability to quickly transfer funds between citizens of Ukraine and other countries;

- use for payment of social assistance, support of internally displaced persons, payment of aid to citizens from international organizations;

- ability to pay wages to employees who are located in different regions of the country or abroad, but work online;

– destruction of a significant number of financial institutions and their physical payment infrastructure in the occupied territories;

- stability of settlements by banking institutions, despite all challenges they face today in terms of providing financial services to their clients.

It is worth noting that the rapid pace of digitization of economic relations in Ukraine, which was observed during the last years before the military aggression and was partly due to COVID-19, had a positive effect on the development of the country's payment system, contributed to the active implementation of information and communication technologies by financial institutions in their activities. This, in turn, made it possible to respond more flexibly to the challenges that banking and other financial companies received as a result of the start of military aggression, since they were able to provide a significant part of their operational activities at an appropriate level from those regions of Ukraine where military operations are not taking place.

The stable functioning of the payment infrastructure in the conditions of the digital economy formation in Ukraine ensured the possibility of avoiding such systemic crisis phenomena in the functioning of the country's financial system in the difficult conditions of the development of its economy:

- impossibility to make calculations between business entities;

- the difficulty of paying pensions, scholarships, and wages to employees of state institutions;

– difficulty with paying salaries to military personnel, taking into account their mobility, variability of the situation on the fronts;

- deterioration of the financial condition of households due to the lack of funds to support life activities and the impossibility of obtaining them from other persons in a non-cash form;

- stoppage of work of financial institutions, inability to provide loans;

- inability to effectively organize the process of paying taxes, fees, etc.

The specified destructive consequences of the destruction of the payment infrastructure in the country, in turn, could deepen the crisis processes in the functioning of the country's financial system, primarily its financial market, and, as a result, further reduce the level of its economic security.

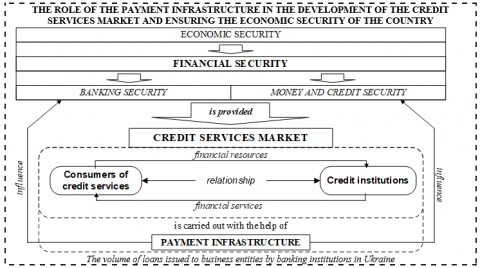

The payment infrastructure plays an important role in the development of the credit services market. In fact, the digital development of the payment infrastructure stimulates the development of the credit services. It was the virtualization of such services and settlement and cash transactions that contributed to the creation of new credit products (online loans, credit cards, and NFC services), which allowed financial institutions to significantly increase the volume of loans issued and ensure the digital transformation of their own activities. Accordingly, the relationship between the development of the credit services market and the functioning of the payment infrastructure is quite close, which undoubtedly affects the banking and monetary security of the country.

In Figure 7, information about the role of the payment infrastructure in the development of the credit services market and ensuring financial and economic security is presented.

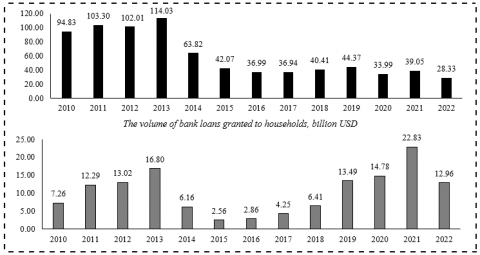

The functioning of the credit services market in Ukraine today is not possible without the payment infrastructure development. Accordingly, the credit services market itself has the ability to form both incentives for the national economy development and create destructive factors for the further emergence of new crisis phenomena in general in the national financial system. The experience of this market development in Ukraine proves that it is credit relations that have the ability to quickly spread crisis phenomena within the financial services market and gradually extrapolate them to the real sector of the national economy.

Information on the development of the credit services market in Ukraine (Figure 7) shows that after the crisis period of social and political shocks in 2014-2015, lending to the national economy in the country did not recover to the pre-crisis (2013) level. We will observe an even greater decline in 2022. All this has a destructive effect not only on the general economic development of the country, but also lowers the threshold of the economic strength of the state, its level of economic security. In modern conditions, this indicator is at a low level for Ukraine. It is only the normalization of the development of the credit services market that is a solid basis for the economic development of the country in general and for the gradual improvement of its capabilities to counteract complex crisis phenomena that permanently arise within the limits of the global financial system.

However, the payment infrastructure plays a special role today in the development of the credit services market, which are provided specifically to households. In fact, the entire payment infrastructure system functions to increase access to financial resources for their owners, borrowers. That is why the development of this market strongly depends on the state of the payment infrastructure in the country and vice versa, credit relations between citizens and financial institutions stimulate the payment infrastructure development, especially in the conditions of a stably functioning national economy. The data of Figure 7 testify that in Ukraine, after a sharp decline in lending to individuals in 2014-2015, banking institutions subsequently restored it to the pre-crisis level in 2021. However, the war had a significant impact on the volume of such lending. At the same time, the decline in 2022 is an order of magnitude smaller than it was in 2014-2015.

The development of credit relations was partially based on the active involvement of digital technologies by financial institutions to update the payment infrastructure and create new opportunities for customers. Directly in the lending sphere, the use of such technologies made it possible to simplify the process of obtaining loans; get a loan at any time of the day; check own accounts and control the movement of cash resources; understand the amount of personal debt and accrued interest; significantly increase the transparency level of credit relations; reduce the time of receiving credit funds; get credit cards and use borrowed funds if necessary, etc.

Thus, the results of the study prove that in unstable conditions, ensuring the stable functioning of the payment infrastructure becomes critical for the national economy. The stoppage, violation of the time frame for making settlements between economic entities leads to the deterioration of the financial condition of all economic entities, and it is a difficult period for the country. The lack of proper functioning of the payment infrastructure creates prerequisites for instability in society in general, reduces the level of accessibility of financial institutions, and blocks the flow of funds to business entities. Accordingly, the virtualization of calculations contributes to their stability, the possibility of providing appropriate services by financial institutions regardless of the peculiarities of their functioning in different regions of the country. Moreover, the digitalization of financial services contributes to a significant increase in their accessibility for citizens, despite the work of physical branches of such institutions.

Figure 7. The role of the payment infrastructure in the development of the credit services market and ensuring the country's financial security

Source: compiled by the authors

The experience of the functioning of the payment system of Ukraine in the conditions of military aggression proves that even during periods of significant destruction and occupation, there is an opportunity for citizens and military personnel to make the necessary calculations, transfer funds, and use credit resources. However, for this, the payment infrastructure must work efficiently. Within the country, it played an important role in ensuring the further functioning of economic entities, the opportunity for some of them to carry out their own activities, in particular in the field of production of goods for the military.

Therefore, the issue of ensuring conditions for the development of payment infrastructure is relevant for most developed countries, especially now, in the era of active use of digital technologies by financial institutions in the process of providing their own services to economic entities. Accordingly, to ensure such development, it is important to clearly understand the main threats that these institutions may face in the process of building their own information systems for customer service. Accordingly, their information protection today is an important component of ensuring the reliability of payment systems, which requires the implementation of a number of complex tasks in this direction both at the level of the state and at the level of the financial institutions themselves.

So, within the framework of the research, its main goal was achieved - the theoretical provisions of the influence of the payment infrastructure on the stability of the national economy, the stability of the functioning of the financial system in the conditions of socio-economic shocks were deepened. It has been established that such an influence is powerful, and the specified type of infrastructure based on the digitalization of the entire payment system plays an important role in the stable functioning of the country's financial system, the timeliness of payments and increasing the availability of financial resources for economic entities, which are key to supporting the country's economic development in complex conditions of its existence.

It has been established that in modern realities the payment system is developing in the conditions of the digital economy formation, which is carried out based on the use of modern information and communication technologies by banking and non-banking institutions in their own activities. It is also determined that the current trend in the functioning of the modern financial services market is the maximum possible virtualization of settlements between economic agents, which undoubtedly affects the interaction of these institutions with their clients, including and when performing settlement operations.

The article substantiates that the maximum digitization of the payment infrastructure in compliance with all security conditions for the use of information and communication technologies contributes to increasing the level of economic security of the country, which occurs on the basis of the availability of financial services, the ability of economic agents to carry out settlement operations and thereby fulfill their own obligations to each other one The stable operation of the payment infrastructure contributes to the reduction of tensions in society, between economic entities regarding the availability of financial resources for use in the stochastic conditions of the socio-political life of the country, the unfolding of crisis and unpredictable events.

To analyze the applied experience of the payment infrastructure development in the conditions of complex challenges to the financial system, the experience of Ukraine as a state that is permanently faced with complex external challenges was used. The analysis of such experience allows us to state that the payment infrastructure digitalization increases its stability level in difficult conditions of the socio-economic development of the country. It has been established that shock challenges to the financial system, which may be associated with the physical destruction of financial institutions, their seizure and loss to their owners, can be partially leveled by the functioning of the virtual payment space. This makes it possible for such institutions to perform their functions stably and to prevent the formation of crisis phenomena within the national economy, avoiding the outflow of customers, closing accounts and a significant loss of their own competitiveness in the conditions of the instability of the economic environment in which they develop.

The main recommendations for ensuring the stable and innovative development of the payment infrastructure and, accordingly, its positive impact on the level of economic security of the state include the following: support at the state level for the digitalization processes of financial institutions (training of relevant personnel, promotion of competition, support in terms of importing relevant equipment), active involvement relevant state institutions to the processes of their own digital transformation, implementation of national programs in society to increase the level of digital literacy, financial culture, training citizens to use virtual financial services, development of regulations regarding the security of the use of virtual payment infrastructure by financial institutions, development of programs at the state level to ensure the growth of information security of the national economy, economic entities, including and financial institutions and their clients, creation of mechanisms for detecting and countering cyber fraud in the financial sphere, coordination of actions of individual countries in this direction, etc.

Further research in this direction may be related to the search for scientific approaches to assessing the crisis resistance of the national payment infrastructure to new socio-political shocks, the development of regulations regarding the actions of financial institutions, state authorities as a result of unforeseen events in order to maintain the stability of the payment infrastructure, safe use digital technologies, blocking business entities that support stochastic processes in society and the national economy.

This research is carried out within the framework of the scientific project “A model of the post-war development of credit institutions based on the artificial intelligence: customization of financial services and prudent supervision” with the support of the Ministry of Education and Science of Ukraine.

[1] Tulchynska, S., Popelo, O., Krasovska, G., Kistiunik, O., Raichava, L., Mykhalchenko, O. (2023). The impact of the national economy digitalization on the efficiency of the logistics activities management of the enterprise in the conditions of intensifying international competition. Journal of Theoretical and Applied Information Technology, 101(1): 123-134.

[2] Popelo, O., Shaposhnykov, K., Popelo, O., Hrubliak, O., Malysh, V., Lysenko, Z. (2023). The influence of digitalization on the innovative strategy of the industrial enterprises development in the context of ensuring economic security. International Journal of Safety and Security Engineering, 13(1): 39-49. https://doi.org/10.18280/ijsse.130105

[3] Revko, A., Popelo, O., Tulchynska, S., Butko, M., Derhaliuk, M. (2022). Methodological approaches to the evaluation of innovation in polish and Ukrainian regions, taking into account digitalization. Comparative Economic Research. Central and Eastern Europe, 25(1): 55-74. https://doi.org/10.18778/1508-2008.25.04

[4] Brandl, B., Dieterich, L. (2023). The exclusive nature of global payments infrastructures: The significance of major banks and the role of tech-driven companies. Review of International Political Economy, 30(2): 535-557. https://doi.org/10.1080/09692290.2021.2016470

[5] Bojjagani, S., Sastry, V.N., Chen, C., Kumari, S., Khan, M.K. (2023). Systematic survey of mobile payments, protocols, and security infrastructure. Journal of Ambient Intelligence and Humanized Computing, 14(1): 609-654. http://doi.org/10.1007/s12652-021-03316-4

[6] Yanagawa, E. (2022). The dawn of next-generation payment infrastructure: The future of zengin and financial services in Japan. Journal of Payments Strategy and Systems, 16(4): 409-427.

[7] Youssef, S.B.H., Boudriga, N. (2022). A resilient micro-payment infrastructure: An approach based on blockchain technology. Kuwait Journal of Science, 49(1): 1-27. http://doi.org/10.48129/KJS.V49I1.10578

[8] Kulk, E., Plompen, P. (2021). Demystifying programmable money: How the next generation of payment solutions can be built with existing infrastructure. Journal of Payments Strategy and Systems, 15(4): 445-454.

[9] Melnychenko, O. (2021). Energy losses due to imperfect payment infrastructure and payment instruments. Energies, 14(24): 8213. http://doi.org/10.3390/en14248213

[10] Tkachuk, І., Kobelia, М., Popelo, О., Zhavoronok, А., Vinnychuk, О. (2023). Modelling financial influence of political and oligarchic interests of governed-sponsored enterprises on the creation and implementation of the financial policy in the state. Journal of Hygienic Engineering and Design, 42: 271-279.

[11] Zhavoronok, A. Popelo, O., Shchur, R., Ostrovska, N., Kordzaia, N. (2022). The role of digital technologies in the transformation of regional models of households’ financial behavior in the conditions of the national innovative economy development. Ingénierie des Systèmes d’Information, 27(4): 613-620. https://doi.org/10.18280/isi.270411

[12] Dubyna, M., Popelo, O., Zhavoronok, A., Lopashchuk, I., Fedyshyn, M. (2023). Development of the credit market of Ukraine under macroeconomic instability. Public and Municipal Finance, 12(1): 33-47. http://doi.org/10.21511/pmf.12(1).2023.04

[13] Wu, W., He, H., Chu, Z., Liu, Y., Shi, L., Gu, M., Yang, L. (2021). Blockchain-based smart payment scheme of power infrastructure funds. Energy Reports, 7: 725-733. http://doi.org/10.1016/j.egyr.2021.09.199

[14] McDonald, T., Shum, H.H., Wong, R. (2021). Payments in the pandemic: Orchestrating and imagining cross-boundary digital money infrastructures in China during COVID-19. Media International Australia, 181(1): 44-56. http://doi.org/10.1177/1329878X211024265

[15] Yanagawa, E. (2021). Payment infrastructure trends in Japan: Emerging technologies and alternative infrastructures. Journal of Payments Strategy and Systems, 15(2): 134-149.

[16] Moreira, F.R., Nunes, R.R., Giozza, W.F., Nze, G.A. (2020). Optimization of the performance of an online payment application by the improviment of its infrastructure. Paper presented at the Iberian Conference on Information Systems and Technologies, CISTI, Seville, Spain. http://doi.org/10.23919/CISTI49556.2020.9140895

[17] Löber, K., Papsdorf, P. (2020). The COVID-19 pandemic: Implications for financial market infrastructures and the payments ecosystem in the euro area. Journal of Payments Strategy and Systems, 14(3): 202-206.

[18] Bhatt, M.S., Md Daud, M.A.S., Aminosharei, R., Wong, K.M. (2020). A new dawn of mobile payments: Infrastructure, challenges, risks and mitigating factors. In Ethics, Governance and Risk Management in Organizations. Accounting, Finance, Sustainability, Governance & Fraud: Theory and Application. Springer, Singapore. https://doi.org/10.1007/978-981-15-1880-5_11

[19] Yanagawa, E. (2019). Payment infrastructure initiatives in Japan: Extended operating hours and the zengin electronic data interchange system (ZEDI). Journal of Payments Strategy and Systems, 13(4): 357-367.

[20] Witold, W.J., Ewelina, S., Jinghua, W. (2019). The mechanisms of changes in the infrastructure of the payment card Market—A comparative analysis of Poland and China. In Springer Proceedings in Business and Economics, pp. 457-471. http://doi.org/10.1007/978-3-030-21274-2_31

[21] Giraldo-Mora, J.C., Avital, M., Hedman, J. (2019). Development dynamics of digital infrastructure and organization: The case of global payments innovation. In the 40th International Conference on Information Systems, ICIS 2019, Munich.

[22] Singh, N.K., Sahu, G.P., Rana, N.P., Patil, P.P., Gupta, B. (2019). Critical success factors of the digital payment infrastructure for developing economies. In Smart Working, Living and Organising. TDIT 2018. IFIP Advances in Information and Communication Technology. Springer, Cham. http://doi.org/10.1007/978-3-030-04315-5_9

[23] GSDI. (n.d.). Economic security. https://gsdi.unc.edu/our-work/economic-security/#:~:text=GSDI%20defines%20Economic%20Security%20as,%2C%20livelihoods%2C%20and%20social%20protection.