Bile Abdisalan Nor*![]() | Husein Osman Abdullahi

| Husein Osman Abdullahi![]() | Hussein Abdi

| Hussein Abdi![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Somalia has a large mobile money user base, with over 83% of mobile phone users using mobile money services. Compare this to the penetration rate of financial services, which is just 5% among rural populations and 1% among internally displaced people. This paper seeks to determine the factors influencing mobile banking adoption in Somalia Through a comprehensive survey involving 130 participants, integrating online as well as face-to-face approaches was employed. The data that was collected that subsequently assessed employing the SPSS software, facilitating a thorough investigation into the subject. This research reveals that perceived ease of use, perceived usefulness, and trust significantly influence individuals' intentions to adopt mobile banking services in Somalia. Focusing on enhancing the user experience, emphasizing practical benefits, and fostering trustworthiness emerges as crucial strategies for boosting mobile banking adoption rates. Notably, perceived cost and risk play a lesser role, possibly owing to cost- effective transaction options and high trust in the reliability of mobile money services. These findings emphasize actionable steps for mobile banking stakeholders in Somalia, pointing towards the importance of user-centric enhancements, clear communication of practical advantages, and continued efforts to build and maintain trust in the mobile banking ecosystem. Based on these findings, a recommendation would be to focus on improving the user experience of mobile banking applications in Somalia. Furthermore, collaboration between mobile network operators, financial institutions, and the government could foster a supportive environment for mobile banking adoption, leading to increased accessibility and usage for the broader population in Somalia.

mobile banking adoption, financial inclusion, Somalia, quantitative analysis, user perceptions

Mobile banking refers to the capability of performing financial activities through a mobile platform using a mobile device [1]. This explanation considers not only fundamental services such as fund transfers as well as bank account statements but also digital payment options. It also covers financial services reliant on information, for instance, real-time updates on account limits and balances, as well as access to stock brokerage information. As pointed out by study [2], mobile banking is a pivotal instrument driving advancement, fostering development, stimulating innovation as well as enhancing business competitiveness.

Analysts need to know a lot about M-banking because it helps banks and other financial service providers to gain a competitive benefit by gaining knowledge of the primary factors that influences the desire to use Mobile banking. Apps also reduce the cost of mobile banking. Mobile banking's facilities make it easier for families to budget, especially when things aren't going well. Asongu and Nwachukwu [3] state that mobile banking allows women to start and run their own businesses while also saving money on transportation and transaction costs.

In Somalia, a country still recovering from years of conflict and facing challenges in its financial sector development, mobile banking holds immense potential to address the needs of unbanked and underbanked populations. However, mobile banking has not yet achieved widespread adoption and factors influencing individuals' intention to use mobile banking remain understudied.

Previous studies, exemplified by study [4], have diligently investigated factors influencing individuals' attitudes towards mobile banking. Notably, Akturan and Tezcan [4] revealed that perceived social risk, perceived performance risk, perceived benefit, as well as Perceived Usefulness (PU), directly influence individuals' attitudes towards mobile banking. Building upon these foundational insights, the current study aims to extend and refine these findings within the specific context of Somalia. It acknowledges the unique socio-economic, cultural, and infrastructural factors inherent to Somalia, shaped by post-conflict recovery and a distinct financial landscape. In doing so, this research recognizes the potential introduction of additional factors or alterations in the significance of existing ones that may influence individuals' attitudes towards mobile banking in Somalia. The study seeks to provide a comprehensive understanding of these dynamics, contributing valuable insights to the nuanced interplay of factors shaping the intention to use mobile banking in Somalia.

The availability and use of mobile phones have grown rapidly in Somalia, with more than two-thirds of the population having access to a mobile device. This presents a favourable environment for the adoption as well as utilization of mobile banking services. Mobile banking can provide financial inclusion to those who are outside the traditional banking system, improve access to credit, and enable secure and efficient transactions.

Somalia has a large mobile money user base, with over 83% of mobile phone users using or subscribing to mobile money services. Compare this to the penetration rate of financial services, which is just 5% among rural populations and 1% among internally displaced people [5]. Mobile money is used for a wide range of transactions, from paying for education fees, disbursing donations/charity, receiving vouchers from the government, shopping online, receiving cash transfers from NGOs, and paying government taxes. The high penetration of mobile money in Somalia is caused by a number of issues, such as the lack of access to standard banking services, the high cost of transfers, and the ease of mobile money.

Somalia experiences a high mobile phone penetration rate of 70% [6], indicating widespread mobile technology access. However, this technological advancement contrasts sharply with the country's limited financial inclusion. As per the data obtained from the World Bank, merely 15.5% of the Somali population can access banking services and owns a bank account. This indicates the possibility for mobile banking to tackle the matter of financial inclusion. Nevertheless, the current uptake of mobile banking in Somalia remains limited. This prompts an inquiry into the factors that impact the intention to utilize mobile banking in the region.

Even though some study has already been done on mobile banking adoption in a number of countries, including developing countries, there is a gap regarding the factors that influences the intention to use mobile banking specifically in Somalia. Existing research may not fully capture the unique socio-economic, cultural, as well as infrastructural context of Somalia, which could significantly impact the utilization of mobile banking services. Hence, there is a need for comprehensive research specifically focused on understanding the factors that influences the intention to use mobile banking in Somalia. Such study would contribute to bridging the existing knowledge gap and provide valuable insights for policymakers, mobile network operators and financial institutions to drive the usage of mobile banking services in the country. The aim of this paper is to identify the factors influencing the intention to use mobile banking in Somalia.

2.1 Mobile banking

Mobile banking is the ability to do financial activities through a mobile platform using a mobile device [1]. Asfaw [2] disputes that mobile banking is a leading tool for pushing progress, helping establishment, encouraging creativity, and making businesses more competitive. Mobile technology has spread more quickly and widely in the developing world than any other technology ever made by humans. As a result, there is a huge flow of text messages that goes far beyond what an individual needs for conversation. Also, people who don't have access to traditional services are increasingly being told that they need custom-made services like mobile banking [7]. Banking through a mobile platform is made possible by the bizarre growth of networks for mobile devices. for instance, phones in growing economies. This makes it possible to use virtual bank accounts on a mobile device, like a phone.

The Technology Adoption Model (TAM) created by Davis and Bagozzi seems to be the most popular framework for promoting the spread of new ideas. Many researchers have utilised this framework to investigate what variables influence people's adoption of new technologies for example [8]. As per [9], TAM's sequential connection between attitudes, beliefs, intentions, as well as actions allows us to predict how individuals will utilize new technology. Furthermore, TAM states that an individual's attitude towards their intention to utilize an innovation is determined by their perception with regard to the innovation's usefulness as well as perceived ease of use (PEoU), having the intention serving as a mediator between the perception along with the actual use of the innovation.

PEoU has been shown to affect PU [10]. According to this theory, PU as well as PEoU are crucial factors in determining whether to embrace and utilise it. As a result, several studies on MB adoption include additional factors, such as perceived cost of use, perceived risk, compatibility with lifestyle [10].

3.1 Perceived usefulness (PU)

The term "perceived usefulness" denotes to the degree to which consumers feel that utilising mobile banking would enhance their overall banking experience and make it easier to complete their financial tasks. Some previous studies consistently found a positive relationship between PU as well as intention to use mobile banking. As per [11]. PU as well as PEoU significantly influence the intention to use mobile banking.

Similarly, Akturan and Tezcan [4] revealed that perceived social risk, perceived performance risk, perceived benefit, as well as PU directly influence individuals' attitudes towards mobile banking. According to study [12], PU, as well as risk are substantial indicators for using mobile banking services.

Riquelme and Rios [13] discovered that the factors with the most impact on the intention to use mobile banking services are social risk, social norms, as well as PU. For study [11], the perceived cost, perceived risk, PU, and compatibility of mobile banking all influence customer adoption mobile banking.

H1: There is a relationship between perceived usefulness and intention to use mobile banking.

3.2 Perceived ease of use (PEoU)

Davis [9] defines the PEoU as the extent to which the M-banking use is effortless. It is an individual's evaluation of the effort expended as a result of utilising a technology [9]. PEOU may also be defined as the belief that using technology will not be mentally taxing and will not require a significant amount of effort as well as time. According to study [14], their study found that PEoU is positively connected to both PU as well as attitude towards mobile banking. Additionally, PU was discovered to possess a positive and substantial connection with attitude and intention towards adopting mobile banking.

H2: There is a relationship between PEoU and intention to use mobile banking.

3.3 Perceived cost

Perceived costs encompass the financial, time, and effort-related expenses associated with adopting and using mobile banking services. Studies have shown that perceived costs serve a substantial role in shaping individuals' intention to use mobile banking. As per [11] the perceived risk, PU, perceived cost, and compatibility of mobile banking all influence customer adoption mobile banking. Additionally, the results lend credence to a mediation hypothesis, according to which customers' attitudes mediate the impact of various consumer perceptions on their intentions towards the usage of mobile banking. According to study [15], their study found that several factors significantly influence consumers' attitude towards mobile banking utilization, which, in turn, influences their intention to use mobile banking. Moreover, these factors comprise perceived cost, PU, perceived risk, perceived interactivity, relative advantage, as well as easefulness. Perceived monetary cost influences behavioural intention to utilise mobile banking [16].

H3: There is a relationship between perceived cost and intention to use mobile banking.

3.4 Perceived risk

Perceived risk resembles individuals' subjective assessment with respect to potential negative outcomes or uncertainties correlated with utilizing mobile banking services. Perceived risk can stem from concerns related to privacy and security, technical issues, and potential financial losses. Research suggests that perceived risk has an influence on individual's intention to use mobile banking. Li [17] found that perceived risk significantly influences individuals' attitude towards utilizing online banking. When individuals perceive higher levels of risk associated with online banking, it can negatively impact their attitude towards using it. Koenig-Lewis et al. [12] identified PU as well as perceived risk as substantial indicators with regard to the mobile banking services use. If individuals perceive mobile banking as useful and beneficial, it positively influences their intention to use it. However, if individuals perceive higher levels of risk associated with mobile banking, it can hinder their intention to use the services. Hsieh [18] revealed that perceived risk significantly predicts the intention of the physicians to utilize such a system. Greater levels of perceived risk are likely to reduce the physicians’ intention to adopt and utilize an electronic medical records exchange system.

H4: There is a relationship between perceived risk and intention to use mobile banking.

3.5 Perceived trust

In the framework of mobile banking, "trust" expresses the extent to which the customer has confidence in the service. Trust exists when a user perceives the service they are using can be relied on. Some Scholars have examined customers' usage of mobile banking. According to research by study [19] there is a negative correlation between perceived risk as well as trust, suggesting that higher levels of trust may lower this barrier to mobile banking adoption. Perceived trust and purchase intention are both negatively affected by perceived risk [20]. In line with study [21] research, it was observed that perceived security risk as well as perceived privacy were associated negatively with the establishment of trust in electronic commerce websites in Saudi Arabia. However, Tiwari and Tiwari [22] discovered that perceived trust exhibits a noteworthy positive impact on the intention to adopt mobile banking.

H5: There is a relationship between perceived trust and intention to use mobile banking.

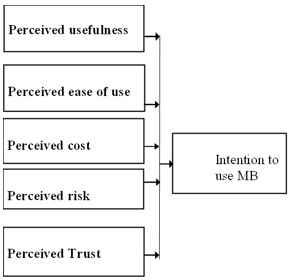

In Figure 1, we present the conceptual framework guiding this survey, illustrating the interconnected relationships and key factors influencing the intention to use mobile banking.

Figure 1. Conceptual framework

This research utilized a quantitative research approach employing a descriptive research design. Here, the quantitative approach was chosen as it allows for the statistical and numerical analysis of the impact of independent variables (PU, PEoU, Perceived risk, Perceived cost as well as Perceived trust) on the dependent variable (Intention to use mobile banking) in Somalia. The research population for this research comprises individuals from Somalia.

The data collection aspect was performed by the researchers through face to face and an online self-administered questionnaire which can be filled out by respondents from various backgrounds. For sampling design, the method chosen was purposive sampling, where respondents are chosen based on participants who are most likely able to understand the specific goals this research seeks to uncover. Purposive sampling was deemed the most appropriate method for this study based on the specific goals and characteristics of the research in the context of Somalia. In purposive sampling, participants are deliberately selected based on specific criteria that align with the objectives of the study. Given the unique socio-economic, cultural, and infrastructural factors in Somalia, the researchers aimed to ensure that the selected participants were those most likely to provide valuable insights into the factors influencing the intention to use mobile banking in this particular context. In a diverse setting like Somalia, where accessibility to certain demographics or populations might be challenging, purposive sampling allows for a targeted and strategic selection of participants who possess the relevant experiences and perspectives related to mobile banking.

A sum of 130 respondents participated in the research by completing the questionnaire. The data collection aspect was carried out by the researchers through face-to-face and an online self-administered questionnaire, which can be filled out by respondents based on a judgemental sampling method. It is a non-random sampling method whereby the respondents are chosen based on their knowledge of the subject matter for research. The collected quantitative data was then processed using SPSS for further analysis. Exploratory Factor Analysis (EFA) was employed to classify the data based on their corresponding variables. This kind of analysis helped us learn more about the connection between the variables under investigation.

4.1 Model specification

This study utilizes cross-sectional data collected at a single point in time. The linear regression method, specifically Ordinary Least Squares (OLS), is employed to define the model in this study. OLS is considered one of the most robust methods in regression analysis, and it is depending on certain assumptions. The regression model employed in this research is as follows:

Y= α +β1X1 +β2X2+β3X3+β4X4+β5X5+e

where,

Y= Intention to use mobile banking

α = constant term

X1- Perceived ease of use

X2- Perceived usefulness

X3- Perceived cost

X4- Perceived risk

X5- Perceived trust

Β1, β2, β3, β4, β5 = Beta coefficients that indicate the weight of every factor

4.2 Results

This paper aims to find out factors influence the intention of the people to use mobile banking in Somalia A sum of 130 participants was acquired for the purpose of analysis.

In Table 1, we present a comprehensive overview of the demographic characteristics of our survey respondents in Somalia. Notably, the survey reveals that most of our respondents were male (91.5%), whereas 8.5% were female. These findings can be attributed to the prevailing trend observed in Somalia, where the male gender monopolizes the workforce, education, as well as distinct life aspects. The overwhelming majority of male respondents (91.5%) likely mirrors a broader trend where men monopolize key aspects of life, including employment opportunities and educational access. This imbalance can significantly impact the survey results, as the experiences and perspectives of women, who constitute only 8.5% of the respondents, may be marginalized or overlooked. The underrepresentation of women limits the depth of insights into their unique challenges, aspirations, and needs. Consequently, the survey's applicability and generalizability to the entire population are compromised, particularly in areas where gender dynamics play a pivotal role. Approximately 60.2 per cent of our respondents were in the age range of 25 to 34, highlighting a significant representation of the youthful population among Somalis. This finding suggests that the majority of Somalis are relatively young. As for education, the majority of the respondents (62.3%) are postgraduate level, followed by 59.6% at is undergraduate level. Furthermore, regarding monthly income, the highest percentage of respondents (43.8%) have an income of 100-300. The next highest percentage (28.5%) have an income of 301-600. for household size, the largest percentage of households (49.2%) have 5 or fewer people. The next largest percentage (38.5%) have 6-10 people. The remaining households are more evenly distributed, with 12.3% having 11 or more people. Finally, the data obtained reveal that the majority of respondents have less than 5 years of experience.

Table 1. Demographic characteristics of the respondents

|

Factors |

Percentage (%) |

|

Gender |

|

|

Male |

91.5 |

|

Female |

8.5 |

|

Total |

100 |

|

Age |

|

|

18-24 |

22.2 |

|

25-34 35-44 |

66.2 10.8 |

|

45 and above |

0.8 |

|

Total |

100 |

|

Educational background |

|

|

Primary school Secondary school |

0 5.4 |

|

Diploma |

0 |

|

Batchelor degree |

56.9 |

|

Postgraduate degree |

62.3 |

|

Total |

100 |

|

Monthly Income |

|

|

$100-300 $301-600 $601-900 $901 and more |

43.8 28.5 13.1 14.6 |

|

Total |

100 |

|

Household size |

|

|

5 or less 6-10 11 and more |

49.2 38.5 12.3 |

|

Total |

100 |

|

Level of experience |

|

|

Less than one year 1-2 years 3-4 years 5 years or more |

9.2 25.4 26.9 38.5 |

|

Total |

100 |

Table 2. Reliability

|

Variables |

Cronbatch’s Alpha |

|

Preceived ease of use |

0.800 |

|

Preceived usefulness |

0.599 |

|

Preceived cost |

0.686 |

|

Preceived risk |

0.784 |

|

Preceived trust |

0.564 |

|

Intention to use MB |

0.737 |

4.3 Reliability test

In this study, the reliability of the instruments was assessed through the utilization of Cronbach's alpha. Cronbach's alpha serves as a commonly employed assessment to gauge the internal consistency and dependability of a scale or measurement. An alpha value exceeding 0.6 is typically interpreted as indicative of strong reliability. The alpha coefficient spans from 0 to 1, with values approaching 1 indicating greater uniformity among the items in the measurement. Based on Table 2 indicated that the variables PU, PEoU, Perceived cost, Perceived respectively.

4.4 Correlation test

The correlation between variables indicates the direction and strength of the relationship between them. Table 3 displays Pearson's correlation coefficients for the four constructs, encompassing values from 0.092 to 0.580 The Pearson's correlation coefficients provided in Table 3 indicate the strength and direction of the relationships between the four constructs studied. A correlation coefficient ranges from -1 to 1, where -1 signifies a perfect negative correlation, 1 denotes a perfect positive correlation, and 0 indicates no correlation. In this study, the positive correlation coefficients suggest that as one variable changes, the other tends to change in the same direction. The values range from 0.092 to 0.580, reflecting varying degrees of correlation strength. Specifically, the highest correlation coefficient of 0.580 is observed between perceived usefulness and perceived risk. This indicates a moderately strong positive correlation, suggesting that as perceived usefulness increases, there tends to be a consistent increase in perceived risk and vice versa. This relationship may have implications for decision-making processes related to the subject of your study. It's worth exploring the nature of this correlation further to understand how perceptions of usefulness might be interconnected with perceptions of risk. Conversely, the lowest correlation coefficient of 0.092 is found between intention to use and perceived risk. This suggests a weak positive correlation, indicating that changes in perceived risk have a relatively weak association with changes in intention to use. The weak correlation implies that perceived risk may not be a strong determinant of the intention to use in your study context.

Table 3. Correlation

|

Pearson Correlation |

|

Perceived Ease of Use |

Perceived Usefulness |

Perceived Cost |

Perceived Risk |

Perceived Trust |

Intention to Use MB |

|

Perceived ease of use |

1 |

.189* |

.451** |

0.095 |

.361** |

.347** |

|

|

Perceived usefulness |

.189* |

1 |

.518** |

.580** |

.303** |

.273** |

|

|

Perceived cost |

.451** |

.518** |

1 |

.458** |

.277** |

.227** |

|

|

Perceived risk |

0.095 |

.580** |

.458** |

1 |

.248** |

0.092 |

|

|

Perceived trust |

.361** |

.303** |

.277** |

.248** |

1 |

.470** |

|

|

Intention to use MB |

.347** |

.273** |

.227** |

0.092 |

.470** |

1 |

|

|

**. Correlation is significant at the 0.01 level (2-tailed). |

|||||||

4.5 Estimation of model parameters

To demonstrate the relationship between our variables, this research used OLS. The methodology section outlines the specifics of the model, while the outcomes of the model parameters are exhibited in the subsequent Table 4.

Table 4. Unstandardized coefficients

|

Unstandardized Coefficients |

||||

|

Variable |

Beta |

Std. Error |

t-Statistic |

Prob. |

|

(Constant) |

7.071 |

1.941 |

3.644 |

0.000 |

|

Perceived ease of use |

0.173 |

0.083 |

2.084 |

0.039 |

|

Perceived usefulness |

0.211 |

0.103 |

2.051 |

0.042 |

|

Perceived cost |

-0.006 |

0.097 |

-0.060 |

0.952 |

|

Perceived risk |

-0.114 |

0.082 |

-1.399 |

0.164 |

|

Perceived trust |

0.399 |

0.090 |

4.425 |

0.000 |

According to the data shown above, PU, PEoU as well as perceived trust possess a positive and significant impact on the intention to use mobile banking in Somalia, with significance at a 5% level of analysis. The findings indicate that factors like PU, PEoU as well as perceived trust serve a crucial role in shaping the intention to use mobile banking in Somalia. Users who perceive mobile banking as easy to use, useful, and trustworthy are more inclined to adopt as well as use it. Thus, Hypotheses H1, H2, and H5 are accepted, confirming the relationship between these variables. However, H3 and H4 are rejected as perceived cost and perceived risk are insignificant with a p-value of 0.952 and 0.164 respectively which are greater than 5% significant level. This proposes that these factors do not have substantial effects on users' willingness to accept mobile banking services. With an R-squared value of 62%, the model shows that it fits well in estimating the parameter, meaning that the variance in the dependent variable can be accounted for by the independent variables up to 62%. Additionally, the F-statistics test holds significance at the 1% level, signifying the collective significance of the variables. To ensure the absence of multicollinearity among the independent variables, collinearity tolerance and VIF statistics were examined. All variables exhibited collinearity tolerance values below one and VIF values below 3, indicating no significant multicollinearity issues. Additionally, the condition index was below 30, further supporting the absence of multicollinearity. A serial correlation was assessed through the Durbin-Watson test, which indicated that the data did not suffer from serial correlation problems, as the Durbin-Watson value was neither below 1.5 nor above 2.5.

Mobile banking is becoming increasingly popular in Somalia as a convenient way for people to manage their money. Since traditional banks are not easily accessible, mobile banking has become an effective solution to close the financial gap. Over 83% of mobile phone users in Somalia use or subscribe to mobile money services, compared to only 5% among rural communities and 1% among displaced people who use traditional financial services.

This research aims to find factors that influences the intention to use mobile banking in Somalia. The research found that PEoU possess a positive and significant impact on the intention to use mobile banking in Somalia. When users find mobile banking easy to use and navigate, they are more inclined to adopt it. This means that if the mobile banking system is user-friendly, more people will use it. Making the mobile banking experience simpler and more convenient can lead to more people using it. People also feel more confident using mobile banking when they discover it easy to use, which is important for gaining their trust [14]. Mobile banking can be beneficial in places like Somalia, where people lack access to financial services.

Moreover, PEoU enhances trust and confidence in the mobile banking platform. It is more likely that users will have a favorable attitude towards using a service if they are happy with its features and functions. The result is that more people will intend to use it, leading to actual usage [23]. In a context like Somalia, mobile banking offers an opportunity for financial inclusion, especially for underserved or remote populations. Thus, H1 is accepted, which aligns with study [14].

Furthermore, PU possesses a significant as well as positive impact on the intention to use mobile banking in Somalia. When users find mobile banking useful for their financial needs, they are more likely to use it. Highlighting these benefits could boost adoption rates. Additionally, PU refers to a crucial factor influencing users' intentions to utilize online management systems. An adopter's intentions to adopt and use a system increase when they believe it offers clear benefits aligns with their goals, boosts productivity, and provides a more effective way to accomplish the tasks [24, 25]. Thus, H2 is accepted, which is consistent with the results of study [4].

Trust also plays a vital role. The study also revealed that perceived trust is a substantial factor that influences people's decision to use mobile banking in Somalia. People are more inclined to use mobile banking when they feel it is secure and reliable for their financial transactions. The finding that perceived trust is a substantial factor influencing people's decision to use mobile banking in Somalia has significant implications for financial institutions and mobile operators in the region. Understanding the importance of trust can guide the development of strategies to enhance user confidence and promote the adoption of mobile banking services. Financial institutions and mobile operators should prioritize investments in robust security measures to ensure the safety and confidentiality of users' financial information. This may involve implementing encryption technologies, multi-factor authentication, and continuously updating security protocols to stay ahead of emerging threats. By focusing on these security enhancements, they can address user concerns and establish a foundation of trust that is crucial for the success and widespread acceptance of mobile banking in Somalia. Thus, H2 is accepted, which aligns with study [22].

However, the perceived cost of using mobile banking does not seem to be a substantial factor that influences people's decision to use it in Somalia. This could be because mobile banking services in Somalia are affordable or free, reducing cost concerns. This could be due to the competition among mobile money providers. It is important to note that individual perspectives and circumstances can vary. While perceived cost might not be a primary factor, it could still influence some individuals' decisions regarding mobile banking in Somalia. Thus, H3 is rejected, and this result aligns with study [22].

Finally, the perceived risk of using mobile banking also does not seem to be a significant factor influencing people's decision to use it in Somalia. This could be because Mobile money providers in Somalia might have established a strong reputation for secure and reliable services, leading to lower perceived risk among users. Additionally, mobile money providers in Somalia might have a good reputation for delivering secure and reliable services, reducing the perceived risk for users. Cultural and Societal Factors could also play a role. Cultural attitudes and societal norms can heavily influence people's behaviours. In some cases, individuals in Somalia might prioritize community recommendations and social connections over perceived risks associated with mobile banking. Thus, so H4 is rejected, and this result aligns with study [26]. This result regarding the perceived risk of using mobile banking in Somalia aligns with the findings of the study on mobile banking adoption in Pakistan in certain aspects. Both studies highlight the potential insignificance of perceived risk as a determining factor in users' decisions to adopt mobile banking services. In the case of the Pakistan study, perceived risk was identified as an insignificant factor in the diffusion of mobile banking adoption. Similarly, in Somalia, our result suggests that the perceived risk might not be a significant factor influencing people's decisions to use mobile banking. One potential commonality is the notion that mobile money providers in both contexts have established a strong reputation for secure and reliable services. This positive reputation could contribute to lower perceived risk among users, making it a less influential factor in their adoption decisions. User Moreover, cultural and societal factors influencing mobile banking adoption in Somalia resonates with the broader understanding that cultural attitudes and societal norms play a crucial role in shaping individuals' behaviors. This aligns with the acknowledgment in the Pakistan study that contextual factors, such as socio-economic conditions, can significantly impact technology adoption.

Mobile banking is becoming increasingly popular in Somalia as a convenient way for people to manage their money. This study aimed to find out factors influence the intention of the people to use mobile banking in Somalia. Through a comprehensive survey involving 130 participants, integrating online as well as face-to-face approaches was employed. The gathered data was subsequently assessed employing the SPSS software, facilitating a thorough investigation into the subject. This research reveals that perceived ease of use (PEoU), perceived usefulness (PU), and trust significantly influence individuals' intentions to adopt mobile banking services in Somalia. Focusing on enhancing the user experience, emphasizing practical benefits, and fostering trustworthiness emerges as crucial strategies for boosting mobile banking adoption rates. Notably, perceived cost and risk play a lesser role, possibly owing to cost-effective transaction options and high trust in the reliability of mobile money services. These findings emphasize actionable steps for mobile banking stakeholders in Somalia, pointing towards the importance of user-centric enhancements, clear communication of practical advantages, and continued efforts to build and maintain trust in the mobile banking ecosystem.

Based on these findings, a recommendation would be to focus on improving the user experience with respect to mobile banking applications in Somalia. This could involve simplifying the interface, providing clear instructions, and offering convenient features that cater to the needs of the users. Additionally, building trust through transparent security measures, privacy policies, and customer support would be essential to encourage more people to embrace mobile banking. Furthermore, efforts can be made to create awareness and educate the public regarding the perks and advantages of mobile banking, emphasizing its convenience, efficiency, and safety.

Lastly, Government of Somalia should consider implementing financial literacy programs to educate citizens about the benefits and functionalities of mobile banking. By enhancing understanding and awareness, policymakers can alleviate concerns, particularly around perceived risk and cost, thus contributing to higher adoption rates.

The study acknowledges a potential limitation in the representativeness of the sample, as it may not fully capture the diversity within the entire population of mobile banking users in Somalia. The disproportionate inclusion of specific demographics, such as certain age groups or urban populations, raises concerns about the generalizability of the findings. To improve the robustness of future studies, researchers could consider adopting more inclusive sampling methods that ensure a broader representation across various regions and demographic segments.

Finally, this study marks an important step in understanding mobile banking adoption in Somalia. To further deepen our insights into the dynamics at play, we propose specific directions for future research. Firstly, we advocate for the implementation of qualitative studies, employing methodologies such as in-depth interviews and focus group discussions. These qualitative approaches hold the promise of uncovering a more nuanced understanding of the socio-cultural factors influencing mobile banking adoption. By delving into contextual nuances, user perceptions, and behavioral patterns, qualitative insights can complement the quantitative data collected, providing a more holistic comprehension of the multifaceted factors shaping adoption. Secondly, we recommend the adoption of longitudinal analyses to track changes over time and unveil the evolving trends in mobile banking adoption. Such longitudinal studies present a valuable opportunity to observe shifts in user attitudes, preferences, and behaviors. By offering a more comprehensive view of the long-term impact of mobile banking initiatives, these analyses can contribute to a deeper understanding of the trajectory and sustainability of mobile banking adoption in Somalia. These proposed avenues for further exploration aim to build on the foundations laid by this study, fostering a more comprehensive understanding of mobile banking adoption dynamics in Somalia.

[1] Chitungo, S.K., Munongo, S. (2013). Extending the technology acceptance model to mobile banking adoption in rural Zimbabwe. Journal of business administration and education, 3(1): 1-6.

[2] Asfaw, H.A. (2015). Financial inclusion through mobile banking: Challenges and prospects. Research Journal of Finance and Accounting, 6(5): 98-104.

[3] A. Asongu, S., Nwachukwu, J.C. (2018). Comparative human development thresholds for absolute and relative pro-poor mobile banking in developing countries. Information Technology & People, 31(1): 63-83. https://doi.org/10.1108/ITP-12-2015-0295

[4] Akturan, U., Tezcan, N. (2012). Mobile banking adoption of the youth market: Perceptions and intentions. Marketing Intelligence & Planning, 30(4): 444-459. https://doi.org/10.1108/02634501211231928

[5] World Bank. (2017). Mobile Money in Somalia - Household Survey and Market Analysis. April, 1, p. 27.

[6] World Bank Group. (2018). Somalia Economic Update, August 2018: Rapid Growth in Mobile Money--Stability or Vulnerability? World Bank.

[7] Ogetange, Z.K. (2014). The effect of agency banking on financial performance of commercial banks in Kenya. University of Nairobi, Kenya.

[8] Venkatesh, V., Davis, F.D. (2000). A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science, 46(2): 186-204. https://doi.org/10.1287/mnsc.46.2.186.11926

[9] Davis, F.D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3): 319-340. https://doi.org/10.2307/249008

[10] Hanafizadeh, P., Keating, B.W., Khedmatgozar, H.R. (2014). A systematic review of Internet banking adoption. Telematics and informatics, 31(3): 492-510. https://doi.org/10.1016/j.tele.2013.04.003

[11] Wessels, L., Drennan, J. (2010). An investigation of consumer acceptance of M-banking. International Journal of bank marketing, 28(7): 547-568. https://doi.org/10.1108/02652321011085194

[12] Koenig-Lewis, N., Palmer, A., Moll, A. (2010). Predicting young consumers' take up of mobile banking services. International Journal of Bank Marketing, 28(5): 410-432. https://doi.org/10.1108/02652321011064917

[13] Riquelme, H.E., Rios, R.E. (2010). The moderating effect of gender in the adoption of mobile banking. International Journal of Bank Marketing, 28(5): 328-341. https://doi.org/10.1108/02652321011064872

[14] Raza, S.A., Umer, A., Shah, N. (2017). New determinants of ease of use and perceived usefulness for mobile banking adoption. International Journal of Electronic Customer Relationship Management, 11(1): 44-65. https://doi.org/10.1504/IJECRM.2017.086751

[15] Krishanan, D., Khin, A.A., Teng, K.L.L., Chinna, K. (2016). Consumers' perceived interactivity & intention to use mobile banking in structural equation modeling. International Review of Management and Marketing, 6(4): 883-890.

[16] Tung, F.C., Yu, T.W., Yu, J.L. (2014). An extension of financial cost, information quality and IDT for exploring consumer behavioral intentions to use the internet banking. International Review of Management and Business Research, 3(2): 1229.

[17] Li, C.F. (2013). The revised technology acceptance model and the impact of individual differences in assessing internet banking use in Taiwan. International Journal of Business & Information, 8(1).

[18] Hsieh, P.J. (2015). Physicians’ acceptance of electronic medical records exchange: An extension of the decomposed TPB model with institutional trust and perceived risk. International Journal of Medical Informatics, 84(1): 1-14. https://doi.org/10.1016/j.ijmedinf.2014.08.008

[19] Al-Jabri, I.M. (2015). The intention to use mobile banking: Further evidence from Saudi Arabia. South African Journal of Business Management, 46(1): 23-34. https://doi.org/10.4102/sajbm.v46i1.80

[20] Chen, Y.S., Chang, C.H. (2012). Enhance green purchase intentions: The roles of green perceived value, green perceived risk, and green trust. Management Decision, 50(3): 502-520. https://doi.org/10.1108/00251741211216250

[21] Eid, M.I. (2011). Determinants of e-commerce customer satisfaction, trust, and loyalty in Saudi Arabia. Journal of Electronic Commerce Research, 12(1): 78-93.

[22] Tiwari, P., Tiwari, S.K. (2020). Integration of technology acceptance model with perceived risk, perceived trust and perceived cost: Customers’ adoption of m-banking. International Journal on Emerging Technologies, 11(2): 447-452.

[23] Ali, A.Y.S., Dhaha, I.S.Y. (2014). Factors influencing mobile money transfer adoption among Somali. International Journal of Business and Economic Law, 4(1): 180-188.

[24] Šumak, B., Pušnik, M., Heričko, M., Šorgo, A. (2017). Differences between prospective, existing, and former users of interactive whiteboards on external factors affecting their adoption, usage and abandonment. Computers in Human Behavior, 72: 733-756. https://doi.org/10.1016/j.chb.2016.09.006

[25] Abdullahi, H.O., Mohamud, A.H., Ali, A.F., Hassan, A.A. (2023). Determinants of the intention to use information system: A case of SIMAD University in Mogadishu, Somalia. International Journal of Advanced and Applied Sciences, 10(4): 188-196. https://doi.org/10.21833/ijaas.2023.04.023

[26] Abbas, M., Zaman, U., Ahmad, J., Nawaz, M.S., Ahraf, M. (2019). Diffusion of mobile banking in Pakistan. SMART Journal of Business Management Studies, 15(1): 10-19. https://doi.org/10.5958/2321-2012.2019.00002.2