Roni Andespa![]() | Yulia Hendri Yeni*

| Yulia Hendri Yeni*![]() | Yudi Fernando

| Yudi Fernando![]() | Dessy Kurnia Sari

| Dessy Kurnia Sari![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This article delves into sustainable growth strategies for Islamic banks, focusing on expanding and developing Islamic branding. Overcoming challenges and outlining an essential strategy, the research, conducted using the PRISMA model, reviews articles from various academic databases. The findings emphasize Sharia compliance as a critical strategy for sustainable development, ensuring strict adherence to Islamic principles in all financial products and services. This approach builds trust within the Muslim community, distinguishing Islamic banks from conventional institutions and establishing a foundation rooted in commitment to Islamic values. The research underscores the ethical principles of Islamic banking, emphasizing risk-sharing and social justice, and highlights the significance of Islamic branding in reinforcing moral foundations and attracting ethically conscious customers. The study highlights how effective branding enhances trust, facilitating financial inclusion and social responsibility. It implies a need for regulatory frameworks supporting standardized Islamic branding, consumer education, and incentives for ethical practices, positioning Islamic banking as a valuable contributor to the financial landscape.

sustainable development, Islamic banks, Islamic branding, challenges, importance, strategies

The growth of the Muslim population worldwide has become a significant phenomenon in the last few decades [1]. According to the Pew Research Center, approximately 1.8 billion of the world’s population, or 24.1% of global citizens, adhered to Islam. The Muslim population is projected to increase to 2.2 billion by 2030 [2]. These data carry substantial implications for the market of Islamic products and services. In this regard, there will be a rapid surge in demand for products and services that align with Sharia principles. For instance, the halal industry and Islamic finance will experience extraordinary growth.

The Islamic banking sector has emerged as one of the most benefited sectors from the growing Muslim population worldwide, experiencing steady growth in recent years [3]. However, a robust Islamic branding strategy is essential to ensure the sustainable development of Islamic banks [4]. Islamic branding will enable these banks to distinguish themselves in an increasingly competitive market and foster greater customer trust. It will be crucial in supporting sustainable development worldwide by catering to financial needs using Sharia principles.

The Islamic branding strategy fundamentally differs from conventional branding in several ways. One key distinction is the emphasis on Sharia compliance within the management [5]. It means that the branding efforts prioritize aligning with Islamic principles and values. In contrast, conventional branding may not necessarily have a religious or ethical focus, and its strategies might be driven by different considerations, such as market trends and consumer preferences [6]. Islamic branding, therefore, reflects a commitment to adhering to Sharia principles, setting it apart from the more secular and diverse approaches of conventional branding [7].

The growth of Islamic banking assets from 2015 to 2021 has been quite promising. In 2015, Islamic banking assets were recorded at US\$1.603 billion. A positive growth trend occurred every year, reaching its peak in 2021 with asset values amounting to US\$2.765 billion. Projections for 2026 indicate a highly optimistic forecast, estimating Islamic banking assets to reach US\$4.025 billion. This data reflects the success and consistent growth in the Islamic banking industry during this period, providing a solid foundation for a better future in an economy based on Sharia principles [8]. The impact of the development of Islamic banks has prompted several countries to implement policies related to sustainable development. For instance, the Saudi Arabian government has committed to specific goals by 2025, including allocating 22.5% of global Islamic financial assets, increasing the number of Sharia scholars, and increasing publications on Islamic finance. It aims to achieve three strategic objectives: governance, positioning and international education, research and development, and innovation. In Labuan, Islamic finance is planned to support education, enhance global Islamic infrastructure, and institutionalize social Islamic finance through digitization. Brunei Darussalam is constructing a Sharia-compliant financial and digital economic zone through public-private partnerships involving environmentally conscious companies [8].

Sustainable development undertaken by Islamic banks constitutes a crucial aspect of the global financial landscape [9]. With an increasing emphasis on ethically sound and socially responsible financial practices, Islamic financial institutions have garnered significant attention from numerous stakeholders [10]. These institutions operate based on Sharia principles, adhering to Islamic ethics prohibiting interest-based transactions and investments in activities deemed morally or socially detrimental [11]. In this context, Islamic branding emerges as a vital tool to foster public trust, credibility, and differentiation in the market [12]. The effectiveness of Islamic branding in ensuring the sustainability and growth of Islamic banks is a subject that necessitates thorough examination [9].

Despite the increasing importance of Islamic financial institutions for sustainable development, there is still a lack of comprehensive research addressing the strategic implementation of Islamic branding in financial institutions. This study aims to fill this void by examining Islamic banks’ challenges in formulating and implementing effective Islamic branding strategies. Identified issues include the complex interplay between Islamic financial principles, modern marketing practices, and unique cultural and religious considerations underlying the branding process. Therefore, creating Islamic bank branding can be aligned with sustainable development.

Islamic branding in Islamic banks refers to marketing strategies and brand identity that align with Islamic principles and values, encompassing various elements such as communication, products, services, and images designed to attract and retain customers seeking Sharia-compliant financial alternatives [13]. As a result, the primary objective of this research is to provide a comprehensive framework for sustainable development in Islamic banking through implementing Islamic branding strategies. It involves a multifaceted approach, including developing crucial branding challenges, exploring best practices, and devising tailored Islamic branding strategies. Furthermore, this research aims to ensure the impact of branding success on Islamic banks’ financial performance and societal acceptance [14].

Several previous studies have examined the relationship between sustainable development and Islamic branding. For example, research has identified that branding development in Islamic banks can be achieved by strongly applying Islamic principles in their operations and services [15]. This branding activity encompasses transparency, justice, and social accountability. Other studies highlight the importance of collaboration between Islamic banks and other Sharia financial institutions in building a strong and mutually supportive ecosystem toward sustainable development goals [16].

Furthermore, research has found that one of the main challenges in branding Islamic banks is overcoming the negative perceptions or stereotypes associated with Islamic finance [17]. This study identifies effective strategies, including marketing campaigns, to educate the public and provide tangible evidence of the positive impact generated. Several previous studies highlight the importance of handling Sharia compliance issues rigorously and consistently to build public trust and strengthen the branding of Islamic banks [18]. Several other studies indicate that Islamic branding can be crucial in distinguishing Islamic banks from conventional financial institutions. A strong branding strategy has the potential to enhance public trust and expand the customer base [19].

Furthermore, previous research emphasizes that a strong Islamic branding approach can assist banks in attracting investors and strategic partners committed to Islamic principles [20]. Subsequently, previous research provides practical guidelines on strategies banks can apply to develop and enhance Islamic branding [21]. These strategies focus on public education and awareness, collaboration with Islamic organizations, and leveraging technology to improve transparency. In addition, several studies emphasize the importance of maintaining consistent communication and implementing Sharia principles across all aspects of the bank’s operations to strengthen its branding efforts [22].

This research explores Islamic branding strategies that can be applied to Islamic banks in various global contexts. The study aims to gain insights from theoretical frameworks and practical case studies, thus offering a holistic perspective on the challenges and opportunities in this field. Additionally, this research will incorporate feedback and perspectives from industry experts and practitioners to ensure diverse and applicable approaches.

Previous studies were more focused on discussing the theories and basic concepts of Islamic branding, but they were less exploratory in examining its practical implementation in Islamic banks. Limitations hindered some earlier research in gathering the necessary empirical data to measure the effectiveness of Islamic branding in Islamic banking [23]. Furthermore, previous studies did not emphasize explaining how Islamic branding can serve as a tool for achieving sustainable development goals within Islamic banking [24].

Therefore, current and relevant research is required to address the present circumstances. In the era of globalization and economic complexity, there is an urgent requirement for novel research that accommodates changes in the business environment and meets the needs of society. The public’s increasing interest in Islamic banking underscores the significance of in-depth analysis to fully utilize the potential of Islamic branding in supporting the growth of the Islamic finance sector [25]. In facing the challenges of sustainable development, concrete strategies that Islamic banks can adopt through the development of Islamic branding are needed [26].

This research’s social and practical relevance is emphasized by the increasing importance of Islamic finance in the global financial ecosystem. Sharia-compliant banking institutions play a crucial role in the international financial system, embodying an ethical and inclusive financial approach [27]. By enhancing the understanding of academics and practitioners regarding Islamic branding strategies, this research can significantly contribute to these institutions’ sustainability and growth.

This study makes a groundbreaking contribution to the field of Islamic finance by merging the principles of Sharia with contemporary branding strategies. This synthesis creates a new framework that effectively allows Islamic banks to communicate their values and offerings to a diverse clientele [28]. Furthermore, this research has the potential to develop innovative branding techniques tailored explicitly to Islamic finance’s unique cultural and ethical considerations.

Given the recent global shift towards sustainable and ethical finance, the choice to research sustainable development and Islamic branding is highly pertinent. The ESG criteria (Environmental, Social, and Governance) are a crucial benchmark for financial institutions, aligning seamlessly with the fundamental principles of Islamic finance [29]. This research endeavours to position Islamic branding as a strategic tool for Islamic banks to thrive in the ever-evolving financial landscape.

In summary, this research tackles the urgent requirement for a holistic framework promoting sustainable development within Islamic banks by strategically implementing Islamic branding. By identifying challenges, delineating optimal practices, and crafting a customized branding strategy, this study aims to substantially influence Islamic financial institutions’ growth and societal acceptance. With its innovative approach, this research strives to connect Islamic finance with contemporary branding practices and contribute meaningfully to the broader conversation surrounding ethical and sustainable finance. As a result, the problems addressed in this article are as follows:

RQ1: How can Islamic branding be developed in Islamic banks to attain sustainable development?

RQ2: What challenges do Islamic banks face in establishing their brand?

RQ3: Why is Islamic branding significant for Islamic banks?

RQ4: What strategies can be employed to create Islamic branding for Islamic banks?

2.1 The sustainable development concept for business

Sustainable development is a comprehensive approach to fostering the progress of society, the economy, and the natural environment through the harmonious balance of economic growth, social justice, and environmental protection [30]. This overarching concept also applies within the business realm, which seeks to generate enduring value for the company, society, and the environment. As a guiding principle, Sustainable Development aids businesses in incorporating economic, social, and environmental considerations into their operations and decision-making processes [31]. By adhering to these principles, businesses can actively contribute to the overarching objective of sustainable development, striving to achieve sustainable economic growth while avoiding practices that could harm the environment or society [32].

Such initiatives may involve investments in green technologies, implementing more efficient supply chain management, and creating decent job opportunities. Businesses are encouraged to innovate new products, services, and technologies that align with the principles of sustainable development [33]. It involves adopting practices that benefit the community, environment, employees, and other relevant stakeholders, showcasing a broader commitment to accountability beyond mere financial gains [34]. Sustainable businesses seamlessly integrate social responsibility into their core values, actively prioritizing the well-being of the community, including employees, local communities, and the environment, alongside their financial objectives [35]. Islamic banks embed sustainability practices and social responsibility into their operations to align with ethical, social, and environmental considerations [36]. Consequently, Islamic banks are pivotal in advancing broader sustainability and social responsibility objectives, ultimately fostering a more balanced and inclusive approach to finance and economic development [37].

2.2 Islamic branding concept

Branding is the creation of a distinctive and easily recognizable identity for a product, service, or organization. Creating branding involves shaping how customers perceive and connect with the brand, influencing their thoughts and feelings towards it [38]. This identity sets the brand apart from competitors and helps build trust and customer loyalty. It entails crafting cohesive messages, visual elements, and an overall experience to leave a lasting impression on consumers [39]. Islamic branding, also known as Muslim branding, is a unique approach to the branding process that aligns with the principles and values of Islam. It ensures that offerings meet Muslim consumers’ specific needs and preferences while respecting their culture and religion [40]. The portrayal of Islamic brands involves carefully considering factors such as halal certification, modesty in advertising, and alignment with Islamic values, making it a crucial strategy for businesses targeting the Muslim market [41].

By adhering to the principles of Islam, companies can cultivate a positive brand image among Muslim customers, demonstrating a commitment to shared values, which ultimately leads to increased brand loyalty and affinity [42]. To implement Islamic branding effectively, companies must steer clear of the perception of exploiting religious beliefs for commercial gain, and this entails the company’s engagement with Islamic values being genuine rather than mere marketing tactics [43]. Avoiding shallow Islamic branding without sincere dedication to upholding Islamic principles is crucial in maintaining respect for the Muslim community [44]. It means a brand should not merely use Islamic symbols or references for marketing purposes but demonstrate genuine dedication [45].

2.3 Previous study

Several studies have explored the field of Islamic branding, specifically focusing on its influence on customer satisfaction and loyalty in banks [46]. This research suggests that Islamic branding has a favourable and notable impact on customer loyalty, mediated through the satisfaction of Islamic bank customers. Moreover, empirical findings explore the factors leading to and outcomes of brand image in Islamic banks. The study identifies three categories of brand image antecedents: functional, emotional, and spiritual attributes.

Several previous studies have also identified crucial aspects of Islamic branding among Muslims and determined which aspects of Islamic brands motivate consumers to purchase those products. Research findings reveal that the motivating factors for Muslims to buy Islamic brands are primarily based on the brand’s origin, followed by customer-centric and compliance-oriented brands [47]. Then, a study found that product quality, Islamic physical attributes, and Islamic beliefs significantly influence brand image and consumer satisfaction. This finding emphasizes that product quality, Islamic physical characteristics, and Islamic beliefs play crucial roles in shaping brand image, ultimately leading to the satisfaction of Muslim consumers regarding Islamic travel packages [48].

Research to understand the influence of electronic word-of-mouth (e-WoM) behaviour on social media among Muslims in shaping the halal brand image and its impact on purchase intention has been conducted by researchers in the past. It was found that altruism and moral obligation within the Muslim community positively influence e-WoM behaviour [49]. A past study examined the relationship between the brand image and the intention to revisit a halal restaurant. It was confirmed that the halal restaurant brand image positively impacts customers’ intention to review [50].

However, contrasting findings suggest that implementing Islamic branding may face challenges related to cultural nuances and varying interpretations of Sharia principles [51]. These challenges can result in inconsistencies in portraying a unified Islamic identity, potentially undermining the effectiveness of branding efforts [52]. Additionally, the literature reveals divergent opinions on the significance of incorporating environmental and social responsibility in Islamic branding. Some researchers argue that integrating these aspects is crucial for aligning with the broader principles of sustainable development. In contrast, others contend that emphasizing environmental and social responsibility may divert attention from the core financial services of Islamic banks, potentially hindering their competitiveness [53].

Research with a Systematic Literature Review (SLR) will provide valuable insights into the impact of Islamic branding on sustainable development and consumer behavior. Considering the findings from previous research on challenges in implementing Islamic branding and differing opinions on environmental and social responsibility, it becomes evident that a more careful and systematic approach is needed to review the existing literature. A Systematic Literature Review using the PRISMA model is required to synthesize diverse findings, evaluate the methodological accuracy of each study, and identify gaps or inconsistencies in the current body of knowledge. This systematic approach ensures a comprehensive and unbiased analysis, contributing to a more robust understanding of the dynamics and complexity surrounding Islamic branding. Unlike the research methods employed by previous researchers, the common thread in this study is the need for a more comprehensive discussion and transparency regarding the research methodology used.

While existing research has contributed valuable insights into understanding Islamic branding, a Systematic Literature Review using the PRISMA model is crucial to consolidate findings, critically evaluate methodologies, and guide future research directions in this evolving field. These studies employ varied research methodologies regarding the differing methods used by these researchers. Although they share a common focus on Islamic branding, each study adopts a different approach to data collection, sampling methods, and analytical techniques. Some studies may use qualitative methods like interviews or content analysis to explore consumer or stakeholder perceptions and attitudes. Others may use quantitative methods like surveys or experiments to gather numerical data and test hypotheses.

In conclusion, the proposed systematic literature review addresses this variation by providing a comprehensive and structured analysis of various studies. It involves synthesizing diverse findings, evaluating the methodological accuracy of each study, and identifying potential gaps or inconsistencies in the current knowledge base. SLR facilitates a more integrated understanding of the research landscape, contributing to a stronger foundation for future studies in Islamic branding.

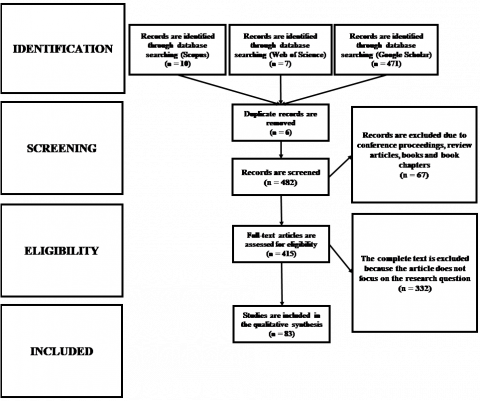

This Systematic Literature Review (SLR) research employs the PRISMA model as its primary method. A systematic literature review is a research method used to identify, evaluate, and synthesize all relevant empirical evidence from various sources to address specific research questions [54]. This method has gained significant popularity in academic research due to its systematic, objective, and comprehensive approach to gathering and processing information from existing literature. The main objective of an SLR is to provide a comprehensive overview of a particular topic based on existing empirical evidence. The stages in the Systematic Literature Review process include identification, screening, and eligibility assessment of previous research articles [55]. In this study, the authors will analyze previous literature regarding the steps in developing Islamic branding for Islamic banks with the aim of sustainable development, the importance of Islamic branding for banks, challenges in Islamic branding, and strategies for creating Islamic branding. The researchers review articles published from 2018 to 2023.

3.1 Identification stage

In a Systematic Literature Review (SLR) context, the identification stage is the initial phase where researchers search for relevant previous studies to be included in the literature review. This stage ensures that all prior research on the investigated topic can be incorporated into further analysis. The search database includes Scopus, Web of Science, and Google Scholar. Harzing’s Publish or Perish is the tool employed for article searches.

The selection of these three academic databases is a strategic decision aimed at enhancing the comprehensiveness and reliability of the literature review. Scopus and Web of Science were chosen for their reputation for hosting high-quality, peer-reviewed academic content, ensuring the review is grounded in credible sources. These databases’ comprehensive indexing systems further facilitate a systematic and thorough exploration of articles related to Islamic branding and sustainable development. Complementing these reputable databases, Google Scholar is included to capture a broader spectrum of scholarly materials, going beyond traditional journal articles to encompass theses, conference papers, and various sources. Google Scholar is a supplementary tool that ensures the inclusivity necessary for a well-rounded understanding of the research landscape.

Harzing’s Publish or Perish is an efficient article search tool that seamlessly enables researchers to conduct cross-database searches. This tool simplifies the identification of relevant articles across various academic databases, encouraging more in-depth searches and mitigating limitations associated with relying on a single database. Researchers use this tool to expand their network and ensure comprehensive scholarly works are considered. The collective use of three academic databases simultaneously, with Harzing’s Publish or Perish tool, forms a comprehensive strategy to ensure that the literature review is conducted meticulously and covers all aspects. The diverse strengths of each component contribute to a holistic understanding of Islamic banking branding and sustainable development, enriching the scholarly foundation of this research.

3.2 Screening stage

The second stage in the Systematic Literature Review with the PRISMA model is the screening stage, which is a crucial process in conducting a systematic literature review as it requires an examination of articles relevant to the research question. The purpose of this stage is to identify and select articles or sources that are pertinent to the research topic. Therefore, during the screening stage, researchers must be cautious and meticulous in obtaining reliable insights from previous studies [56].

3.3 Eligibility stage

The eligibility step in SLR is determining whether an article meets the inclusion criteria in the current literature research. The eligibility process in the SLR aims to ensure that only quality articles are included in the analysis; this seeks to achieve high reliability and validity in synthesizing the literature.

4.1 Identification

In the initial stage, the researcher utilized keywords and synonyms extracted from previous literature to ensure information regarding the development of Islamic branding in Islamic banks for sustainable development. This process encompassed understanding the significance of Islamic branding, the challenges faced in Islamic bank branding, and strategies for establishing Islamic branding. The search results were recorded in Table 1, with ten articles retrieved from Scopus, seven from the WoS database, and 471 from Google Scholar, resulting in 488 articles identified.

Table 1. The articles found in the database

|

Database |

Found Articles |

|

Scopus |

10 |

|

Web of Science |

7 |

|

Google Scholar |

471 |

|

Total |

488 |

4.2 Screening

Table 2. Exception articles

|

Article Type |

Exception |

|

Duplicate records |

6 |

|

Conference proceedings, review articles, books, and book chapters |

67 |

Table 2 presents the investigation results identifying six duplicate articles, thus bringing the total down to 482 (488-6). Additionally, there are 67 articles categorized under conference proceedings and others. Consequently, 415 articles are scheduled for review in the next stage (482-67).

4.3 Eligibility stage

The primary step in this research process is identifying articles that suit the research questions and ensuring that the articles reviewed meet the criteria the researcher desires to be suitable for use as sources in the literature review [57]. Previous articles were evaluated to address the research questions, and it was determined whether these articles focused on the following topics: RQ1: How can Islamic branding be developed in Islamic banks to achieve sustainable development? RQ2: What challenges do Islamic banks face in building their brand? RQ3: Why is Islamic branding important for Islamic banks? and RQ4: What strategies can be applied to create an Islamic brand? From the eligibility process, 332 articles focused on other aspects outside the research questions. The research flow depicted in Figure 1, following the PRISMA model, illustrates the research process consisting of identification, screening, and eligibility determination, resulting in a total of 83 articles that can be included in the final stage of the study (415 - 332).

Figure 1. The research flows

After completing the eligibility criteria, the systematic literature review using the PRISMA model approach reveals how Islamic branding can be developed in Islamic banks to achieve sustainable development. It explores the challenges Islamic banks face in building their brand, elucidates the significance of Islamic branding for these banks, and outlines the strategies that can be employed to establish an Islamic brand. The explanation is as follows:

4.3.1 Developing Islamic branding for Islamic banks with the goal of sustainable development

Developing Islamic branding in Islamic banks to achieve sustainable development requires a comprehensive strategy [20]. First, the management aligns the operational activities of Islamic banks with Islamic principles and values [23]. These activities encompass ensuring that all bank products and services comply with Sharia law, abstain from interest-based transactions, and adhere to ethical investment guidelines [58]. In addition, such initiatives must establish financial transparency, ultimately bolstering public trust in Islamic banks [59]. The conclusion is that the managers of Islamic banks must guarantee that all operational activities align with Islam’s principles and values, including compliance with Sharia law, avoiding interest-based transactions, and adhering to ethical investment guidelines.

Secondly, effective communication is essential in building a solid Islamic brand [43]. Banks must clearly articulate their commitment to Islamic values through marketing campaigns, website content, and customer interactions [60]. It educates customers about the bank’s ethos and fosters a sense of belonging and trust among customers [61]. Furthermore, providing educational materials on Islamic finance can empower customers to make informed decisions that align with their beliefs [62]. The conclusion is that clear and effective communication of Islamic values through marketing efforts, website content, and customer interactions is crucial in building a strong Islamic brand, as it aims to educate customers about the bank’s ethos and foster their trust.

Moreover, partnerships and collaborations with Islamic scholars and institutions can significantly bolster the credibility of an Islamic bank [63]. The bank can demonstrate its commitment to upholding Islamic principles by seeking guidance and endorsements from reputable religious authorities [64]. These partnerships can also lead to the development of innovative financial products that cater specifically to the needs and preferences of the Islamic market [65, 66]. In conclusion, building partnerships and collaborations with Islamic scholars and institutions enhance Islamic banks’ credibility. It demonstrates Islamic bank managers’ dedication to upholding Islamic principles, ultimately fostering the development of innovative financial products designed to cater to Muslim customers’ needs.

In addition, incorporating philanthropy and social responsibility into the bank’s operations is crucial for sustainable development [67]. Establishing zakat and sadaqah programs and investing in community development projects fulfill religious obligations and foster a positive image of the bank in the broader community [68]. Demonstrating a genuine concern for the welfare of society further solidifies the Islamic bank’s commitment to ethical and sustainable practices [69]. It can be concluded that philanthropy, social responsibility, zakat, sadaqah programs, and investment in community development projects are essential for sustainable development because Islamic banks can fulfill religious obligations, foster a positive image, and strengthen their commitment to ethical and sustainable practices.

Furthermore, technological innovation plays a vital role in advancing Islamic branding. Islamic banks should leverage digital platforms to enhance accessibility and convenience for their customers [70]. It includes offering Sharia-compliant online banking services and developing user-friendly mobile applications for seamless transactions [71]. Embracing fintech solutions can also lead to the creation of cutting-edge Islamic financial products [72]. The conclusion is that technological innovation plays a crucial role in advancing Islamic branding. It encourages Islamic banks to leverage digital platforms to enhance customer accessibility and convenience, encompassing services like online banking and mobile applications.

Additionally, continuous training and development for staff members are essential [73]. Ensuring employees have a deep understanding of Islamic finance principles enables them to serve customers effectively and with integrity [24]. It includes regular workshops, seminars on Islamic finance, and ongoing professional development opportunities [74]. The conclusion is that ongoing training and development for staff members are essential to ensure that employees possess a profound understanding of Sharia finance principles, enabling them to serve customers effectively and with integrity.

Furthermore, conducting regular audits and assessments is crucial to maintain compliance with Islamic principles and ensure transparency [64]. Implementing robust monitoring mechanisms and appointing Sharia compliance officers can help promptly identify and rectify deviations from ethical standards [75]. It safeguards the bank’s reputation and reinforces customer trust [10]. It can be concluded that audits, regular assessments, and the implementation of monitoring mechanisms are essential for maintaining compliance with Islamic principles. Ensuring transparency and correcting deviations from ethical standards will uphold the reputation of Islamic banks and enhance customer trust.

Moreover, managers of Islamic banks should actively solicit feedback from customers, who can offer valuable insights for system enhancements [40]. The system was established as a platform for customers to express their opinions regarding the bank’s dedication to ongoing improvement [76]. Feedback from customer input can enhance existing products and new offerings that align with Muslim customers’ preferences [77]. The conclusion is that Islamic bank managers must proactively seek customer feedback to improve the system. This feedback serves as a continuous improvement tool aimed at refining existing products and introducing new ones that align with the preferences of Muslim customers.

In conclusion, developing Islamic branding in Islamic banks for sustainable development requires a multifaceted approach. Aligning operations with Islamic principles, effective communication, strategic partnerships, philanthropy, technological innovation, staff training, compliance monitoring, and customer feedback all play integral roles in building a solid and sustainable Islamic brand. By prioritizing these aspects, Islamic banks can thrive in the competitive financial industry and contribute positively to the broader community and economy.

4.3.2 Challenges in Islamic Bank branding

Establishing an Islamic brand poses several challenges for Islamic banks. Firstly, one major hurdle is aligning their operations strictly with Sharia principles [78]. It requires meticulous adherence to Islamic finance principles governing all banking activities [79]. From investment decisions to profit-sharing arrangements, the bank must comply with Sharia law [80]. Achieving this level of consistency can be demanding, as it necessitates a thorough understanding of Islamic financial concepts [81].

Secondly, Islamic banks face the challenge of educating the public about their unique financial offerings [82]. Unlike conventional banks, Islamic banks operate on profit-and-loss sharing models and abstain from interest-based transactions [83]. Communicating these differences effectively to potential customers is crucial for building trust and attracting a customer base that values Islamic finance principles [84]. In conclusion, Islamic banks must effectively communicate profit-sharing models and avoid interest-based transactions to educate the public, build trust, and attract a customer base aligned with Islamic financial principles.

Many Muslim scholars and intellectuals also believe Islamic banks share similarities to conventional ones [85]. This perception may arise from the resemblance in their operational procedures, which is apparent from an external standpoint. However, fundamentally, Islamic bank’s function based on distinct Sharia principles. Hence, although Islamic and conventional banks exhibit external similarities, the fundamental principles they uphold differ significantly [86]. Islamic banks aim to establish a financial system that aligns more closely with Islamic values, emphasizing sustainability and avoiding usury practices.

Apart from that, compliance with financial regulations in a country is also another critical issue. In some countries, legal and regulatory systems may not be aligned with Sharia principles [87]. As a result, Islamic banks must adapt to financial regulations that may not suit their business model [88]. Islamic bank managers must continue to ensure that their operations meet these standards while complying with Sharia principles, which require a delicate balance [89]. It includes developing innovative financial products and services that comply with both regulations.

In addition, to establish a distinctive Islamic brand, it is essential to undertake marketing efforts and activities that effectively engage with the community [43]. Islamic banks must formulate marketing strategies that align with their target markets, emphasizing their dedication to ethical and socially responsible banking practices [40]. Subsequently, the Islamic bank executed a campaign that spotlighted its adherence to Islamic values and societal contributions [90]. In conclusion, managers of Islamic banks must implement marketing strategies tailored to their target market, underscoring their commitment to ethical and socially responsible banking practices.

Another challenge stems from the need for a robust infrastructure that supports Islamic banking operations, and it encompasses building a comprehensive Sharia-compliant auditing, risk management, and governance system [91]. It also involves developing skilled personnel well-versed in Islamic finance principles, from frontline staff to top-level management [92]. In addition, Islamic banks face the challenge of building a diverse portfolio of Sharia-compliant investment opportunities [93]. A deep understanding of various industries and sectors that align with Islamic finance principles is required.

Lastly, maintaining competitive rates of return can be a challenge for Islamic banks [94]. While complying with Sharia principles, bank managers must also guarantee that their financial products remain competitive [95]. Striking this balance requires innovative approaches to investment and profit-sharing arrangements [96]. Furthermore, global economic fluctuations also present a challenge for Islamic banks. Islamic bank manager must be agile in responding to changing market conditions while upholding their commitment to ethical financial practices [97]. It requires a proactive approach to risk management and a keen understanding of global economic trends [95].

4.3.3 The importance of Islamic branding for Islamic banks

Islamic branding plays a crucial role in the success and credibility of Islamic banks [98]. Firstly, it establishes a distinct identity for these financial institutions within the global market [99]. Through specific symbols, logos, and communication strategies, Islamic banks convey their adherence to Sharia-compliant principles, setting them apart from conventional banks [62]. Clear differentiation is essential as it enables customers, particularly those seeking financial services in line with their religious beliefs, to quickly identify and choose Islamic banks [28].

Secondly, Islamic branding reinforces trust and confidence among the bank’s clientele [100]. Prominently featuring Islamic values and ethics in their branding efforts, these banks signal their commitment to ethical and responsible financial practices [67]. This assurance resonates strongly with customers prioritizing transparency, fairness, and compliance with Islamic principles when managing their finances [101]. It, in turn, fosters long-lasting relationships and enhances customer loyalty, crucial components for any thriving banking institution [102].

Furthermore, a robust Islamic brand can draw in customers from both domestic and international markets [103]. It is a distinctive indicator for individuals searching for banking services that resonate with their religious principles and ethos [104]. A well-executed branding initiative can potentially engage prospective clients across diverse geographical areas, bolstering the growth and extending the reach of the Islamic bank beyond its primary target demographic [13]. Its expanded outreach augments the bank’s financial performance and supports economic progress in regions with a substantial Muslim populace [105].

Moreover, Islamic branding is integral in educating the public about the principles and benefits of Islamic finance [16]. Through clear and consistent messaging, Islamic banks can demystify the concept of Sharia-compliant banking, making it more accessible and understandable for a wider audience [62]. This educational aspect of branding contributes to the overall development of Islamic finance, promoting financial literacy and enabling individuals to make informed decisions about their banking choices [106].

A well-crafted Islamic brand also shields against negative perceptions or misconceptions regarding Islamic finance [107]. It provides a platform for Islamic banks to proactively address potential customers’ concerns or doubts regarding the compatibility of Islamic banking practices with modern financial requirements [19]. This proactive approach safeguards the reputation of Islamic banks and contributes to the broader acceptance and integration of Islamic finance into the global financial system [52].

In summary, Islamic branding plays a pivotal role in ensuring the success and legitimacy of Islamic banks. It establishes a distinct global market identity through symbols, logos, and communication strategies that effectively convey compliance to Sharia-compliant principles. Furthermore, it enhances trust and confidence by prominently featuring Islamic values, resonating with individuals prioritizing ethical financial practices, and fostering enduring customer relationships. Additionally, a robust Islamic brand attracts a diverse clientele, expanding the bank’s reach and supporting economic progress in Muslim-majority regions. Ultimately, this safeguards the reputation of Islamic banks and facilitates their seamless integration into the global financial system.

4.3.4 Strategy to create Islamic branding for Islamic banks

A thoughtful approach involving various strategies is essential to create a distinctive Islamic branding for Islamic banks. Firstly, emphasizing Sharia compliance is crucial, ensuring that all financial products and services strictly adhere to Islamic principles [21]. It builds trust within the Muslim community and sets the bank apart from conventional institutions [49]. By prioritizing Sharia compliance, the bank establishes a vital foundation based on adherence to Islamic principles, further distinguishing itself from traditional financial institutions [108].

Secondly, effective communication is pivotal as the bank must articulate its dedication to Islamic principles through lucid and transparent messaging across all marketing materials [109]. This approach underscores its commitment to particular financial protocols, including abstaining from interest-based transactions and removing investments in prohibited industries [110]. Therefore, the bank’s ability to convey its allegiance to Islamic values and emphasize its adherence to specific financial practices, such as avoiding interest-based transactions and investments in prohibited industries, hinges on achieving effective communication through clear and transparent messaging in all marketing materials [25].

Moreover, fostering community engagement plays a significant role in establishing Islamic branding [43]. Banks can organize events, seminars, and workshops on Islamic finance, creating a platform for education and discussion [37]. It demonstrates the bank’s dedication to the community and helps establish a loyal customer base [111]. In conclusion, by cultivating community involvement through hosting events, seminars, and workshops on Islamic finance, the Islamic bank is constructing its Islamic branding, showing dedication to the community, and nurturing a loyal customer base.

Furthermore, incorporating Islamic aesthetics into branding elements such as logos, colour schemes, and interior design can visually represent the identity of an Islamic bank [112]. These visual cues serve as a reminder of the institution’s values and principles [113]. By integrating Islamic aesthetics into branding elements like logos, colour schemes, and interior design, this bank effectively showcases its Islamic identity, continuously reinforcing the core values and principles of Islamic banking [114].

The managers of Islamic banks can provide innovative and Sharia-compliant financial products, distinguishing them from their competitors [115]. The development of unique and innovative services tailored to meet the needs of the Muslim community reflects the bank’s dedication to sustainable Islamic finance development [25]. This Islamic bank’s unique financial services and products should be user-friendly and easily accessible to the public [116]. Offering easily accessible and user-friendly banking services will significantly enhance Islamic banks’ value and volume of financial transactions [117].

In addition, partnering with prominent Islamic scholars and organizations can enhance the bank’s credibility and bolster the authenticity of its Islamic branding [118]. Pursuing endorsement or certification from a reputable authority within Islamic finance provides customers with assurance regarding the bank’s adherence to Sharia principles [119]. In conclusion, the collaboration with Islamic scholars and organizations significantly elevates the credibility of the Islamic branding for Islamic banks. These financial institutions can actively seek backing or certification from established authorities within a given jurisdiction, thereby solidifying customer confidence in the bank’s commitment to Sharia principles and fostering sustainable development within the financial institution [65, 120].

Finally, maintaining a robust online-based service and utilizing effective digital marketing strategies is imperative in today’s interconnected world [121]. Engaging with target markets through social media platforms, blogs, and interactive websites enables banks to reach a broader audience and effectively communicate the values of Islamic finance [122]. In this scenario, Islamic banks also offer a platform for continuous dialogue and feedback, thus fortifying the positive relationships between banks and customers [123]. The conclusion is that transitioning services online enables banks to engage the wider community, providing a platform to convey the principles of Islamic finance and fostering ongoing dialogue and feedback for enhanced customer relationships.

Practical and effective strategies for establishing impactful Islamic branding for Islamic banks arise from various findings. A key strategy involves emphasizing Sharia compliance and ensuring strict adherence to Islamic principles in all financial products and services. It builds trust within the Muslim community and sets the bank apart from conventional institutions. Clear and transparent communication is crucial, requiring consistent messaging across all marketing materials to express the bank’s dedication to Islamic principles and specific financial protocols.

Community engagement is a significant aspect, with recommendations to organize events, seminars, and workshops on Islamic finance. It educates the community and showcases the bank’s commitment, fostering a loyal customer base. Integrating Islamic aesthetics into branding elements, such as logos and interior design, visually represents the Islamic bank’s identity and constantly reminds it of its values. Offering innovative, Sharia-compliant financial products that are user-friendly and easily accessible helps distinguish the bank from competitors, thereby enhancing the value and volume of financial transactions.

Collaboration with Islamic scholars and organizations is identified as a means to enhance credibility and authenticity. Seeking endorsement or certification from reputable authorities within Islamic finance provides customers with assurance regarding the bank’s commitment to Sharia principles. Finally, maintaining a robust online presence and employing effective digital marketing strategies are essential. Engaging with target markets through social media platforms, blogs, and interactive websites facilitates broader outreach and effective communication of Islamic finance values, fostering positive relationships between banks and customers. In conclusion, the holistic implementation of these strategies is vital for Islamic banks, contributing to developing a solid and sustainable Islamic branding while reinforcing their commitment to Sharia principles.

The sustainable development of Islamic banks by creating Islamic branding has several theoretical and managerial implications. Islamic banking operates based on the principles of Islamic law, which emphasize ethical and moral considerations in financial transactions. Establishing strong Islamic branding for these banks involves addressing challenges, acknowledging the significance of these challenges, and implementing effective strategies.

Theoretically, this research contributes to the theory and knowledge that Islamic banking is founded on ethical principles, prohibiting interest and promoting risk-sharing and social justice. Developing Islamic branding reinforces the moral foundation and emphasizes alignment with Islamic values in financial practices. Building an Islamic brand requires strict adherence to Sharia principles, and this compliance can lead to greater transparency and accountability, which are crucial in attracting customers seeking ethically sound financial solutions. Branding an Islamic image assists Islamic banks in projecting a clear religious identity, which can appeal to customers prioritizing faith-based values in their financial choices and foster customer loyalty.

Managerially, this research contributes to the notion that Islamic branding enhances the trust and credibility of Islamic banks among Muslims and non-Muslims. It is particularly crucial in an industry frequently afflicted by scandals and a lack of transparency. Through effective branding, Islamic banking can reach out to segments of the population that harbor ethical reservations about conventional banking practices. It facilitates financial inclusion by providing options to individuals previously excluded from the banking system. Islamic banks are anticipated to play a role in promoting social welfare and philanthropy. An Islamic branding strategy can underscore a bank’s dedication to social responsibility and ethical investment, attracting socially conscious customers.

The study implies the importance of regulatory frameworks recognizing and reinforcing the ethical foundation of Islamic banking through adherence to Sharia principles. Policymakers should promote the implementation of Islamic branding standards across the entire industry, aiming to establish honest and transparent practices for bank management. Crucially, consumer education is needed to raise awareness of Islamic banking’s ethical principles. Policymakers can encourage socially responsible practices by providing recognition and financial incentives to Islamic banks involved in philanthropy and ethical investments. Supporting financial inclusion and industry collaboration is vital for extending banking services to marginalized populations. Establishing effective monitoring mechanisms is also advised to ensure ongoing compliance with Sharia principles and ethical standards. Governments should actively endorse ethical finance, acknowledging the societal benefits of Islamic banking’s commitment to ethical practices and social responsibility and positioning it as a valuable contributor to the broader financial landscape.

This literature study delves into the development of Islamic branding for Islamic banks, with the fundamental purpose of achieving sustainable growth. The article underscores the importance of Islamic branding, delineates the existing challenges, and elucidates strategies for building a robust Islamic brand. This research employs the Systematic Literature Review methodology using the PRISMA model. The dataset comprises articles published between 2018 and 2023. In total, 83 articles have been meticulously reviewed, all directly addressing the research questions. Through this comprehensive review, researchers unearthed crucial insights regarding the development of Islamic branding in Islamic banking, with a steadfast focus on sustainable development [20, 61, 66, 67].

Furthermore, this research highlights substantial challenges in branding Islamic banks [78, 83, 95]. It, therefore, underlines the crucial role of Islamic branding in the overall success of financial institutions [13, 16, 98]. Finally, this article outlines essential strategies for creating an appealing Islamic brand in Islamic banking [37, 64, 111].

The findings of this research can be implemented in the broader financial industry and non-Islamic markets. For instance, the identified strategies for creating an appealing Islamic brand, such as emphasizing ethical principles and community engagement, can be adopted by conventional banks aiming to enhance their public image and attract a broader customer base [124]. Furthermore, the research’s emphasis on the crucial role of Islamic branding in the success of financial institutions raises questions about whether similar branding principles can be applied in diverse cultural and economic contexts [125]. Concrete examples could include analyzing how non-Islamic financial institutions prioritizing ethics have successfully implemented branding strategies inspired by Islamic principles [11]. It might involve examining case studies or industry reports that showcase instances where banks, regardless of their religious orientation, have incorporated ethical considerations into their branding to resonate with socially conscious consumers.

The limitations of this research are twofold. Firstly, the available literature is restricted due to the specificity or limited prior exploration of the research topic. Secondly, as the research pertains to Islamic branding, a relatively nascent and evolving field, no comprehensive literature exists. Therefore, future researchers can study the following topics for their future research:

[1] Hadiz, V.R. (2018). Imagine all the people? Mobilizing Islamic populism for right-wing politics in Indonesia. Journal of Contemporary Asia, 48(4): 566-583. https://doi.org/10.1080/00472336.2018.1433225

[2] Alam, N., Zameni, A. (2019). Existing regulatory frameworks of cryptocurrency and the Shari’ah alternative. In Halal Cryptocurrency Management. Cham: Springer International Publishing. pp. 179-194. https://doi.org/10.1007/978-3-030-10749-9_12

[3] Naz, S.A., Gulzar, S. (2022). Impact of Islamic finance on economic growth: An empirical analysis of Muslim countries. The Singapore Economic Review, 67(1): 245-265. https://doi.org/10.1142/S0217590819420062

[4] Al-Haija, E.A., Kolsi, M.C., Kolsi, M.C.C. (2021). Corporate social responsibility in Islamic banks: To which extent does Abu Dhabi Islamic bank comply with the global reporting initiative standards? Journal of Islamic Accounting and Business Research, 12(8): 1200-1223. https://doi.org/10.1108/JIABR-11-2020-0346

[5] Ab Ghani, N.L., Mohd Ariffin, N., Abdul Rahman, A.R. (2023). The extent of mandatory and voluntary Shariah compliance disclosure: Evidence from Malaysian Islamic financial institutions. Journal of Islamic Accounting and Business Research. https://doi.org/10.1108/JIABR-10-2021-0282

[6] Ab Hamid, S.N., Maulan, S., Wan Jusoh, W.J. (2022). Brand attributes, corporate brand image and customer loyalty of Islamic banks in Malaysia. Journal of Islamic Marketing, 14(10): 2404-2428 https://doi.org/10.1108/JIMA-09-2021-0309

[7] Fatmawati, D., Ariffin, N.M., Abidin, N.H.Z., Osman, A.Z. (2022). Shariah governance in Islamic banks: Practices, practitioners and praxis. Global Finance Journal, 51: 100555. https://doi.org/10.1016/j.gfj.2020.100555

[8] Islamic Corporation for Development of The Private Sector. (2022). Refinitiv Islamic finance development report 2022: Embracing change. ICD.

[9] Jan, A.A., Lai, F.-W., Tahir, M. (2021). Developing an Islamic corporate governance framework to examine sustainability performance in Islamic Banks and Financial Institutions. Journal of Cleaner Production, 315: 128099. https://doi.org/10.1016/j.jclepro.2021.128099

[10] Alam, Md.K., Islam, F.T., Runy, M.K. (2021). Why does Shariah governance framework important for Islamic banks? Asian Journal of Economics and Banking, 5(2): 158-172. https://doi.org/10.1108/AJEB-02-2021-0018

[11] Hidayah, N.N., Lowe, A., De Loo, I. (2021). Identity drift: The multivocality of ethical identity in Islamic financial institution. Journal of Business Ethics, 171(3): 475-494. https://doi.org/10.1007/s10551-020-04448-x

[12] Junaidi, J., Wicaksono, R., Hamka, H. (2022). The consumers’ commitment and materialism on Islamic banking: the role of religiosity. Journal of Islamic Marketing, 13(8): 1786-1806. https://doi.org/10.1108/JIMA-12-2020-0378

[13] Kartika, T., Firdaus, A., Najib, M. (2019). Contrasting the drivers of customer loyalty; financing and depositor customer, single and dual customer, in Indonesian Islamic bank. Journal of Islamic Marketing, 11(4): 933-959. https://doi.org/10.1108/JIMA-04-2017-0040

[14] Andespa, R., Yeni, Y.H., Fernando, Y., Sari, D.K. (2023). A systematic review of customer Sharia compliance behaviour in Islamic banks: Determinants and behavioural intention. Journal of Islamic Marketing. https://doi.org/10.1108/JIMA-06-2023-0181

[15] Ridwan, R., Mayapada, A.G. (2022). Does sharia governance influence corporate social responsibility disclosure in Indonesia Islamic banks? Journal of Sustainable Finance & Investment, 12(2): 299-318. https://doi.org/10.1080/20430795.2020.1749819

[16] Utomo, S.B., Sekaryuni, R., Widarjono, A., Tohirin, A., Sudarsono, H. (2021). Promoting Islamic financial ecosystem to improve halal industry performance in Indonesia: A demand and supply analysis. Journal of Islamic Marketing, 12(5): 992-1011. https://doi.org/10.1108/JIMA-12-2019-0259

[17] Aysan, A.F., Disli, M., Duygun, M., Ozturk, H. (2018). Religiosity versus rationality: Depositor behavior in Islamic and conventional banks. Journal of Comparative Economics, 46(1): 1-19. https://doi.org/10.1016/j.jce.2017.03.001

[18] Hatta, I.H., Baharuddin, G., Hilmiyah, N. (2022). Empirical analysis of branding perception on Islamic banks in Indonesia. Quality-Access to Success, 23(189): 95-106. http://doi.org/10.47750/QAS/23.189.12

[19] Said, L.R., Bilal, K., Aziz, S., et al. (2022). A comparison of conventional versus Islamic banking customers attitudes and judgment. Journal of Financial Services Marketing, 27(3): 206-220. https://doi.org/10.1057/s41264-021-00113-0

[20] Sarker, M.N.I., Khatun, M.N., Alam, G.M. (2019). Islamic banking and finance: Potential approach for economic sustainability in China. Journal of Islamic Marketing, 11(6): 1725-1741. https://doi.org/10.1108/JIMA-04-2019-0076

[21] Mohd Haridan, N., Sheikh Hassan, A.F., Mohammed Shah, S., Mustafa, H. (2023). Financial innovation in Islamic banks: Evidence on the interaction between Shariah board and FinTech. Journal of Islamic Accounting and Business Research, 14(6): 911-930. https://doi.org/10.1108/JIABR-11-2022-0305

[22] Georgiadou, E., Nickerson, C. (2022). Marketing strategies in communicating CSR in the Muslim market of the United Arab Emirates: Insights from the banking sector. Journal of Islamic Marketing, 13(7): 1417-1435. https://doi.org/10.1108/JIMA-09-2020-0274

[23] Jan, M.T., Shafiq, A. (2021). Islamic banks’ brand personality and customer satisfaction: An empirical investigation through SEM. Journal of Islamic Accounting and Business Research, 12(4): 488-508. https://doi.org/10.1108/JIABR-05-2020-0149

[24] Ab Shatar, W.N., Hanaysha, J.R., Tahir, P.R. (2021). Determinants of cash waqf fund collection in Malaysian Islamic banking institutions: Empirical insights from employees’ perspectives. ISRA International Journal of Islamic Finance, 13(2): 177-193. https://doi.org/10.1108/IJIF-06-2020-0126

[25] Alhammadi, S. (2023). Expanding financial inclusion in Indonesia through Takaful: Opportunities, challenges and sustainability. Journal of Financial Reporting and Accounting. https://doi.org/10.1108/JFRA-05-2023-0256

[26] Bukhari, S.A.A., Hashim, F., Amran, A.B. (2020). Determinants and outcome of Islamic corporate social responsibility (ICSR) adoption in Islamic banking industry of Pakistan. Journal of Islamic Marketing, 12(4): 730-762. https://doi.org/10.1108/JIMA-11-2019-0226

[27] Habib, F. (2023). Islamic finance and sustainability: The need to reframe notions of Shariah compliance, purpose, and value. In Islamic Finance, FinTech, and the Road to Sustainability, Cham: Springer International Publishing pp. 15-40. https://doi.org/10.1007/978-3-031-13302-2_2

[28] Ullah, K., Ashfaque, M., Atiq, M., Khan, M., Hussain, A. (2023). Shariah capabilities and value propositions of Islamic banking. International Journal of Islamic and Middle Eastern Finance and Management, 16(4): 701-715. https://doi.org/10.1108/IMEFM-12-2019-0518

[29] Liu, F.H., Lai, K.P. (2021). Ecologies of green finance: Green Sukuk and development of green Islamic finance in Malaysia. Environment and Planning A: Economy and Space, 53(8): 1896-1914. https://doi.org/10.1177/0308518X211038349

[30] Khan, I., Zakari, A., Dagar, V., Singh, S. (2022). World energy trilemma and transformative energy developments as determinants of economic growth amid environmental sustainability. Energy Economics, 108: 105884. https://doi.org/10.1016/j.eneco.2022.105884

[31] Ghosh, S., Mandal, M.C., Ray, A. (2022). Green supply chain management framework for supplier selection: An integrated multi-criteria decision-making approach. International Journal of Management Science and Engineering Management, 17(3): 205-219. https://doi.org/10.1080/17509653.2021.1997661

[32] Raihan, A., Muhtasim, D.A., Pavel, M.I., Faruk, O., Rahman, M. (2022). Dynamic impacts of economic growth, renewable energy use, urbanization, and tourism on carbon dioxide emissions in Argentina. Environmental Processes, 9(2): 38. https://doi.org/10.1007/s40710-022-00590-y

[33] O’Neill, E.A., McKeon Bennett, M., Rowan, N.J. (2022). Peatland-based innovation can potentially support and enable the sustainable development goals of the United Nations: Case study from the Republic of Ireland. Case Studies in Chemical and Environmental Engineering, 6: 100251. https://doi.org/10.1016/j.cscee.2022.100251

[34] Baid, V., Jayaraman, V. (2022). Amplifying and promoting the “S” in ESG investing: The case for social responsibility in supply chain financing. Managerial Finance, 48(8): 1279-1297. https://doi.org/10.1108/MF-12-2021-0588

[35] Barauskaite, G., Streimikiene, D. (2021). Corporate social responsibility and financial performance of companies: The puzzle of concepts, definitions and assessment methods. Corporate Social Responsibility and Environmental Management, 28(1): 278-287. https://doi.org/10.1002/csr.2048

[36] Bhuiyan, Md.A.H., Darda, Md.A., Hossain, Md.B. (2022). Corporate social responsibility (CSR) practices in Islamic banks of Bangladesh. Social Responsibility Journal, 18(5): 968-983. https://doi.org/10.1108/SRJ-07-2020-0280

[37] Julia, T., Kassim, S. (2020). Exploring green banking performance of Islamic banks vs conventional banks in Bangladesh based on Maqasid Shariah framework. Journal of Islamic Marketing, 11(3): 729-744. https://doi.org/10.1108/JIMA-10-2017-0105

[38] Chen, X., Qasim, H. (2021). Does E-Brand experience matter in the consumer market? Explaining the impact of social media marketing activities on consumer-based brand equity and love. Journal of Consumer Behaviour, 20(5): 1065-1077. https://doi.org/10.1002/cb.1915

[39] Ratnasari, R.T., Gunawan, S., Mawardi, I., Kirana, K.C. (2021). Emotional experience on behavioral intention for halal tourism. Journal of Islamic Marketing, 12(4): 864-881. https://doi.org/10.1108/JIMA-12-2019-0256

[40] Abbas, A., Nisar, Q.A., Mahmood, M.A.H., Chenini, A., Zubair, A. (2019). The role of Islamic marketing ethics towards customer satisfaction. Journal of Islamic Marketing, 11(4): 1001-1018. https://doi.org/10.1108/JIMA-11-2017-0123

[41] Zaki, R.M., Elseidi, R.I. (2023). Religiosity and purchase intention: An Islamic apparel brand personality perspective. Journal of Islamic Marketing. https://doi.org/10.1108/JIMA-09-2022-0257

[42] Osman, I., Junid, J., Ali, H., Buyong, S.Z., Syed Marzuki, S.Z., Othman, N. (2023). Consumption values, image and loyalty of Malaysian travellers towards Muslim-friendly accommodation recognition (MFAR). Journal of Islamic Marketing. https://doi.org/10.1108/JIMA-09-2022-0245

[43] Yasin, M., Liébana-Cabanillas, F., Porcu, L., Kayed, R.N. (2020). The role of customer online brand experience in customers’ intention to forward online company-generated content: The case of the Islamic online banking sector in Palestine. Journal of Retailing and Consumer Services, 52: 101902. https://doi.org/10.1016/j.jretconser.2019.101902

[44] Aman, A. (2019). Islamic marketing ethics for Islamic financial institutions. International Journal of Ethics and Systems, 36(1): 1-11. https://doi.org/10.1108/IJOES-12-2018-0182

[45] Shah, S.A., Bhutto, M.H., Azhar, S.M. (2021). Integrative review of Islamic marketing. Journal of Islamic Marketing, 13(6): 1264-1287. https://doi.org/10.1108/JIMA-07-2020-0216

[46] Wadud, A.M.A., Layaman (2023). The impact of Islamic branding on customer loyalty with customer satisfaction as an intervening variable. In Islamic Sustainable Finance, Law and Innovation, Cham: Springer Nature Switzerland pp. 95-104. https://doi.org/10.1007/978-3-031-27860-0_8

[47] Jumani, Z.A., Muhamad, N. (2022). Development and validation of key antecedents of religious brand attitude: A cross-cultural quantitative analysis using smart PLS. Journal of Islamic Marketing. https://doi.org/10.1108/JIMA-06-2022-0177

[48] Nawi, N.B.C., Al Mamun, A., Nasir, N.A.M., Abdullah, A., Mustapha, W.N.W. (2019). Brand image and consumer satisfaction towards Islamic travel packages: A study on tourism entrepreneurship in Malaysia. Asia Pacific Journal of Innovation and Entrepreneurship, 13(2): 188-202. https://doi.org/10.1108/APJIE-02-2019-0007

[49] Fachrurazi, F., Silalahi, S.A.F., Hariyadi, H., Fahham, A.M. (2023). Building halal industry in Indonesia: The role of electronic word of mouth to strengthen the halal brand image. Journal of Islamic Marketing, 14(8): 2109-2129. https://doi.org/10.1108/JIMA-09-2021-0289

[50] Wardi, Y., Trinanda, O., Abror, A. (2022). Modelling halal restaurant’s brand image and customer’s revisit intention. Journal of Islamic Marketing, 13(11): 2254-2267. https://doi.org/10.1108/JIMA-01-2021-0034

[51] Kateb, I., Nafti, O., Zeddini, A. (2023). How to improve the financial performance of Islamic banks in the MENA region? A Shariah governance perspective. International Journal of Emerging Markets. https://doi.org/10.1108/IJOEM-03-2023-0434

[52] Muflih, M. (2021). The link between corporate social responsibility and customer loyalty: Empirical evidence from the Islamic banking industry. Journal of Retailing and Consumer Services, 61: 102558. https://doi.org/10.1016/j.jretconser.2021.102558

[53] Ur Rehman, Z., Zahid, M., Rahman, H.U., et al. (2020). Do corporate social responsibility disclosures improve financial performance? A perspective of the Islamic banking industry in Pakistan. Sustainability, 12(8): 3302. https://doi.org/10.3390/su12083302

[54] Paul, J., Barari, M. (2022). Meta-analysis and traditional systematic literature reviews—What, why, when, where, and how? Psychology & Marketing, 39(6): 1099-1115. https://doi.org/10.1002/mar.21657

[55] Joseph, C., Janang, J.T., Yusuf, S.N.S., Rahmat, M. (2023). Factors influencing corporate ethical values disclosures: A systematic literature review. International Journal of Business and Society, 24(1): 219-236. https://doi.org/10.33736/ijbs.5613.2023

[56] Kim, S.H., Jung, Y.J., Choi, G.W. (2022). A systematic review of library makerspaces research. Library & Information Science Research, 44(4): 101202. https://doi.org/10.1016/j.lisr.2022.101202

[57] Ishak, M.S.I. (2019). The principle of maṣlaḥah and its application in Islamic banking operations in Malaysia. ISRA International Journal of Islamic Finance, 11(1): 137-146. https://doi.org/10.1108/IJIF-01-2018-0017

[58] Ullah, S., Harwood, I.A., Jamali, D. (2018). ‘Fatwa Repositioning’: The hidden struggle for shari’a compliance within Islamic financial institutions. Journal of Business Ethics, 149(4): 895-917. https://doi.org/10.1007/s10551-016-3090-1

[59] Platonova, E., Asutay, M., Dixon, R., Mohammad, S. (2018). The impact of corporate social responsibility disclosure on financial performance: Evidence from the GCC Islamic banking sector. Journal of Business Ethics, 151(2): 451-471. https://doi.org/10.1007/s10551-016-3229-0

[60] Rehman, F.U., Zeb, A. (2023). Translating the impacts of social advertising on Muslim consumers buying behavior: The moderating role of brand image. Journal of Islamic Marketing, 14(9): 2207-2234. https://doi.org/10.1108/JIMA-07-2021-0231

[61] Riaz, U., Burton, B., Fearfull, A. (2023). Emotional propensities and the contemporary Islamic banking industry. Critical Perspectives on Accounting, 94: 102449. https://doi.org/10.1016/j.cpa.2022.102449

[62] Junaidi, J., Anwar, S.M., Alam, R., Lantara, N.F., Wicaksono, R. (2022). Determinants to adopt conventional and Islamic banking: Evidence from Indonesia. Journal of Islamic Marketing, 14(3): 892-909. https://doi.org/10.1108/JIMA-03-2021-0067

[63] Khurram, S., Khurram, A., Memon, M.A. (2019). Stakeholder salience and collaboration decisions in microfinance organizations: Evidence from developing Islamic country’s context. Strategic Change, 28(6): 479-497. https://doi.org/10.1002/jsc.2300

[64] Haridan, N.M., Hassan, A.F.S., Karbhari, Y. (2018). Governance, religious assurance and Islamic banks: Do Shariah boards effectively serve? Journal of Management and Governance, 22(4): 1015-1043. https://doi.org/10.1007/s10997-018-9418-8

[65] Abasimel, N.A. (2023). Islamic mibanking and econocs: Concepts and instruments, features, advantages, differences from conventional banks, and contributions to economic growth. Journal of the Knowledge Economy, 14(2): 1923-1950. https://doi.org/10.1007/s13132-022-00940-z

[66] Miah, M.D., Suzuki, Y. (2020). Murabaha syndrome of Islamic banks: A paradox or product of the system? Journal of Islamic Accounting and Business Research, 11(7): 1363-1378. https://doi.org/10.1108/JIABR-05-2018-0067

[67] Hanic, A., Smolo, E. (2023). Islamic approach to corporate social responsibility: An international model for Islamic banks. International Journal of Islamic and Middle Eastern Finance and Management, 16(1): 175-191. https://doi.org/10.1108/IMEFM-07-2021-0284

[68] Larouche, C. (2023). Autonomous care? Muslim transnational giving networks and perceptions of welfare responsibilities in India. Ethnography, 24(3): 389-406. https://doi.org/10.1177/14661381221134417

[69] Alotaibi, K.O., Helliar, C., Tantisantiwong, N. (2022). Competing logics in the Islamic funds industry: A market logic versus a religious logic. Journal of Business Ethics, 175(1): 207-230. https://doi.org/10.1007/s10551-020-04653-8

[70] Mohd Nor, S., Abdul-Majid, M., Esrati, S.N. (2021). The role of blockchain technology in enhancing Islamic social finance: The case of Zakah management in Malaysia. Foresight, 23(5): 509-527. https://doi.org/10.1108/FS-06-2020-0058

[71] Rabbani, M.R., Bashar, A., Nawaz, N., et al. (2021). Exploring the role of Islamic fintech in combating the aftershocks of COVID-19: The open social innovation of the Islamic financial system. Journal of Open Innovation: Technology, Market, and Complexity, 7(2): 136. https://doi.org/10.3390/joitmc7020136

[72] Chong, F.H.L. (2021). Enhancing trust through digital Islamic finance and blockchain technology. Qualitative Research in Financial Markets, 13(3): 328-341. https://doi.org/10.1108/QRFM-05-2020-0076

[73] Ali, M.M., Devi, A., Furqani, H., Hamzah, H. (2020). Islamic financial inclusion determinants in Indonesia: An ANP approach. International Journal of Islamic and Middle Eastern Finance and Management, 13(4): 727-747. https://doi.org/10.1108/IMEFM-01-2019-0007

[74] Muhammad, R., Nugraheni, P. (2022). Sustainability of Islamic banking human resources through the formulation of an Islamic accounting curriculum for higher education: Indonesian perspective. SAGE Open, 12(1). https://doi.org/10.1177/21582440221079838

[75] Kismawadi, E.R. (2023). Improving Islamic bank performance through agency cost and dual board governance. Journal of Islamic Accounting and Business Research. https://doi.org/10.1108/JIABR-01-2023-0035

[76] Oladapo, I.A., Hamoudah, M.M., Alam, M.M., Olaopa, O.R., Muda, R. (2022). Customers’ perceptions of FinTech adaptability in the Islamic banking sector: Comparative study on Malaysia and Saudi Arabia. Journal of Modelling in Management, 17(4): 1241-1261. https://doi.org/10.1108/JM2-10-2020-0256

[77] Amin, H. (2022). Maqasid-based consumer preference index for Islamic home financing. International Journal of Ethics and Systems, 38(1): 47-67. https://doi.org/10.1108/IJOES-07-2020-0117

[78] Mukhibad, H., Nurkhin, A., Anisykurlillah, I., Fachrurrozie, F., Jayanto, P.Y. (2023). Open innovation in Shariah compliance in Islamic banks - Does Shariah supervisory board attributes matter? Journal of Open Innovation: Technology, Market, and Complexity, 9(1): 100014. https://doi.org/10.1016/j.joitmc.2023.100014

[79] Jatmiko, W., Iqbal, A., Ebrahim, M.S. (2023). On the ethicality of Islamic banks’ business model. British Journal of Management: 1467-8551.12703. https://doi.org/10.1111/1467-8551.12703

[80] Rouetbi, M., Ftiti, Z., Omri, A. (2023). The impact of displaced commercial risk on the performance of Islamic banks. Pacific-Basin Finance Journal, 79: 102022. https://doi.org/10.1016/j.pacfin.2023.102022

[81] Relano, F. (2023). Ethical and Islamic banking compared from a time-based perspective. Journal of Business Ethics. https://doi.org/10.1007/s10551-023-05497-8

[82] Akbar, M., Akbar, A., Yaqoob, H.S., Hussain, A., Svobodová, L., Yasmin, F. (2023). Islamic finance education: Current state and challenges for Pakistan. Cogent Economics & Finance, 11(1): 2164665. https://doi.org/10.1080/23322039.2022.2164665

[83] Anjum, M.I. (2022). An Islamic critique of rival economic systems’ theories of interest. International Journal of Ethics and Systems, 38(4): 598-620. https://doi.org/10.1108/IJOES-08-2021-0155

[84] Khan, S.M., Ali, M., Puah, C.-H., Amin, H., Mubarak, M.S. (2023). Islamic bank customer satisfaction, trust, loyalty and word of mouth: The CREATOR model. Journal of Islamic Accounting and Business Research, 14(5): 740-766. https://doi.org/10.1108/JIABR-01-2022-0017

[85] Harahap, B., Risfandy, T. (2022). Islamic organization and the perception of riba (Usury) and conventional banks among Muslims: Evidence from Indonesia. SAGE Open, 12(2): 215824402210979. https://doi.org/10.1177/21582440221097931

[86] Ghoniyah, N., Hartono, S. (2020). How Islamic and conventional bank in Indonesia contributing sustainable development goals achievement. Cogent Economics & Finance, 8(1): 1856458. https://doi.org/10.1080/23322039.2020.1856458

[87] Bananuka, J., Katamba, D., Nalukenge, I., Kabuye, F., Sendawula, K. (2020). Adoption of Islamic banking in a non-Islamic country: Evidence from Uganda. Journal of Islamic Accounting and Business Research, 11(5): 989-1007. https://doi.org/10.1108/JIABR-08-2017-0119

[88] Louhichi, A., Louati, S., Boujelbene, Y. (2020). The regulations-risk taking nexus under competitive pressure: What about the Islamic banking system? Research in International Business and Finance, 51: 101074. https://doi.org/10.1016/j.ribaf.2019.101074

[89] Saeed, S.M., Abdeljawad, I., Hassan, M.K., Rashid, M. (2023). Dependency of Islamic bank rates on conventional rates in a dual banking system: A trade-off between religious and economic fundamentals. International Review of Economics & Finance, 86: 1003-1021. https://doi.org/10.1016/j.iref.2021.09.013

[90] Ramli, H.S., Abdullah, Md.F., Alam, Md.K. (2023). Islamic crowdfunding practices in Malaysia: A case study on Nusa Kapital. Asian Journal of Accounting Research, 8(2): 145-156. https://doi.org/10.1108/AJAR-11-2021-0248

[91] Muhammad, R., Azlan Annuar, H., Taufik, M., Nugraheni, P. (2021). The influence of the SSB’s characteristics toward Sharia compliance of Islamic banks. Cogent Business & Management, 8(1): 1929033. https://doi.org/10.1080/23311975.2021.1929033

[92] Hidayat, S.E., Rafiki, A., Svyatoslav, S. (2020). Awareness of financial institutions’ employees towards Islamic finance principles in Russia. PSU Research Review, 4(1): 45-60. https://doi.org/10.1108/PRR-08-2019-0026