Galad Mohamed Barre* | Abdimalik Ali Warsame | Hassan Abdikadir Hussein![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Climate change has received substantial attention from policymakers and academicians; hence, demonstrating the importance of environmental conservation. Fossil fuel energy use for industrialization and urbanization curtails environmental quality. This highlights the urgent need for green financing in green technologies and clean energy to preserve environmental quality. Contrary to the previous attempts that focus on the importance of green finance for mitigating climate change without examining how well-versed people are in the idea of green finance; however, this study aims to examine the awareness and preference for green finance among staff of commercial banks in Mogadishu, Somalia using a descriptive statistics research design. The results indicate more than 75% of the respondents are very familiar or familiar with green finance. However, less than 25% are unfamiliar with green finance. the result also indicates that the majority of the respondents prefer green finance more than 65% and just over 14% said they do not prefer green finance. Therefore, policymakers should implement policies aimed at reducing uncertainty and providing the banks with a conducive environment in green financing.

awareness of environmental finance, sustainable finance, commercial banks, Somalia, Sub-Saharan Africa

Environmental issues have received more attention in recent years as a result of ongoing global warming and increased energy production and consumption [1, 2]. Climate disasters including droughts, storms, coastal flooding, rising sea levels, and tsunamis affect the entire planet [3]. Because these climate changes jeopardize the world's sustainable way of life, and the economy as a whole aggregate [4]. Since it aids in the transition to a green economy for better management of issues like climate change, environmental catastrophes, and energy efficiency, the financial sector needs to develop green financing [5].

Green finance is a concept that integrates the financial and economic fields with ethical behavior toward the environment [6]. Furthermore, green finance may be motivated by financial incentives, a desire to preserve the environment, or a combination of both, depending on the participant. Banking and financial institutions in particular have an impact on an economy through their funding of various operations, which will have an impact on the general economy and ultimately have an impact on the real-world mitigation of environmental concerns [7, 8]. These financial intermediaries might actively support the cause for a greener environment, implement a "green" policy, and help customers' enterprises use clean technology. Hence, to maintain overall sustainability, each and every financial institution needs to develop a long-term strategy to monitor the environmental impact of their clients' initiatives. This tends to reduce costs and support the development of new enterprises [4]. Therefore, least developed countries, such as Somalia, requires more assistance for climate change adaptation and mitigation issues compared other developing nations since it is one of the most exposed countries to climate change in the world.

To ensure green safety and long-term ecological balances, green banking makes industries more environmentally friendly and preserve environmental quality [9]. A corporation is only granted a loan under the green banking concept if all environmental safety regulations are upheld [8]. Green banking can play a key role in ensuring other businesses behave responsibly since banks, as financiers of initiatives, have a significant impact on the greening of other industries in the economy [6, 10]. Commercial banks are interested in green financing for much more than just the potential financial rewards; rather, they have a more general interest. Promoting and guiding green financing is without a doubt one of commercial banks' most important social responsibilities [6].

Globally, When forests are lost, fossil fuels are burned, and other non-renewable energy sources are used in a range of industrial activities, the concentration of carbon dioxide and other greenhouse gases in the atmosphere is rising [11, 12]. Global food security is being threatened by climate change [13]. Hence, to address this issue, researchers and practitioners have proposed fostering and investing in the manufacture of green technologies.

In the context of Sub-Saharan African countries, the livelihoods of the population are severely affected by the scourge of climate change via decreasing farm production [14, 15]; livestock production [16]. According to other studies, the amount of arable land per capita in densely populated East African regions is diminishing [13, 17]. In the Horn of Africa region, in recent decades, climate change and severe environmental deterioration of forest regions have had a substantial impact on the livestock and agricultural subsectors [12]. Due to their limited ability to adapt to the changing environment and their subpar political systems, Sub-Saharan African countries (SSA) are more vulnerable to it than other regions [18]. Notably, Africa contributes a tiny fraction of the global greenhouse gase emissions (GHGs) but bear the largest burden of the climate change consequences.

Somalia has been ravaged by civil conflicts and political instability for the last three decades. Consequently, it encountered recurrent natural disasters and depleted natural resources [19, 20]. Pastoralists and agro-pastoralists in the country are extremely susceptible to weather and climatic extremes. At times of food shortage, for example, selling livestock to buy food and cereals from smallholder communities provides a feasible safety net [21]. This is commonly practiced by the Somali pastoral communities whose life mainly relies on rain-fed crops. Severe weather variations may obliterate this buffering mechanism, making rural communities more vulnerable to shocks. Major flooding occurrences in the country reduce agricultural land productivity owing to soil logging, causing loss of fertile topsoil and deforestation [22]. The loss of fertile topsoil through soil erosion has also been accelerated by strong winds, which in turn reduces land productivity. High temperatures have caused the failure of agricultural harvests as a result of higher evapotranspiration, reduced water availability, and increased insect invasion [22]. By the late 1980s, nearly all of Somalia's floodplain woods had been eradicated to make way for irrigated agriculture. In 2014, only 10% of the nation's surface area was covered by forests, down from 62% in 1980. Forest cover in Somalia has decreased by 1% year on average since 1990 [23]. On the other hand, one of the most important elements of environmental deterioration that endangers the development of sustainable agriculture is deforestation [24]. Forests help to provide food, reduce pollution, stop soil erosion, fight global warming, and improve the water cycle [25]. The ability and effectiveness of green finance and sustainable finance to lessen the severe effects of climate change are not well understood in the Somali context. It is limited to the Somali context, but it also has similarities with other emerging countries, particularly those in Sub-Saharan Africa (SSA), which have not gotten as much attention from the empirical literature.The Somali people mainly participate in climate change via degrading forest deforestation. Thus, the purpose of this study is to investigate the awareness and willingness of Somali commercial bank employees toward green financing. The results of this study will help Somali commercial banks' top management better prepare and educate their staff about green finance so they can fight climate change. Since banks are among the largest entities that potentially contribute to the reduction of climate change, this study will also be helpful to policymakers in their efforts to regulate private banks' ability to mitigate the effects of climate change. There is no empirical evidence of green finance awareness and preference in Somali commercial banks. Thus, this study is an effort to fill this knowledge gap.

The concept of green finance is becoming more and more popular as the economy grows, and many studies are currently concentrating on that area, notably as a social responsibility from the companies [6]. Yet, both developed and developing countries make up the majority of these studies. Green finance is the financial innovation that occurred as a result of people seeking out methods of environmental protection and seeing it as a link between the financial and environmental industries [26]. So, green credit funds are likely to invest more in companies who reveal such information since green finance policies compel financial institutions to carefully analyze environmental protection information of enterprises before lending them [27]. In the financial sector, a variety of green finance solutions are emerging, each with its own brands, terms, and conditions [28]. Banks use strategy to find market pertinent green financing products that put them ahead of rivals in the market [29].

The banks have been identified as offering the following green finance products: green traded equities and bonds, green long-term investment accounts, carbon finance, and climate finance. Green infrastructure financing and green bank assurance [28]. These products are provided by the banking sector in an effort to increase environmental production and generate profits from investments of environmentally friendly. Green loan or credit: is a unique form of short- to medium-term financing provided by banks to start-ups, small firms, and multinational enterprises to fund their product development and research efforts [30, 31]. In particular, it offers green innovation start-up capital, making them competitive, especially among high-tech enterprises [32]. Also, green loans, which are available to small firms at low interest rates, reinforce their capital structures to protect them from financial trouble [28]. Another study highlighted the enormous benefits of green credits for corporate performance [33]. Furthermore, banks agree to the Equator Principles, which guarantee preferential treatment for environmentally beneficial projects, while lending to small businesses. These banks are required by the Equator Principles to expand the volume of loans to be disbursed, lower the interest rates, and lengthen the payback terms [34].

Green long-term investment account: Green long-term investment accounts, also known as sustainable investment accounts, are a banking product that enables consumers to save enough money to support long-term investment activities in agriculture and other sectors of the economy that are ecologically conscious [35]. Current data indicates that investment in renewable energy is rising, and banks enable this by allowing businesses and people to fund this project [35]. Making sure that sponsoring programs have adequate funding to address the economic challenges faced by minorities and older adults (pension), to ensure social cohesion and integration, sound corporate governance, and to improve labor relations is another aspect of banks' long-term investments in the environment [36].

Carbon finance: The banking industry finances various projects like the construction of tunnels and zigzag kilns, as well as biogas plants, solar power plants, waste disposal facilities, and energy treatment facilities [37, 38]. This financial product is crucial for lowering greenhouse gas emissions caused by carbon emissions from fossil fuels, industrial waste, and manufacturing-related pollution. It helps recycle garbage, enhance cooking, and provide access to clean water [29]. To lessen the damaging effects of carbon emissions on the environment, several banks in coal-exporting countries are issuing more carbon finance and fewer conventional loans on fossil fuel (coal) [39, 40].

Climate finance: Banks' efforts to address the climate crisis, including greenhouse gas emissions from industry and all human undertakings, aim to raise funds in order to preserve weather resilience and improve people's well-being [41, 42]. Also, the product will support initiatives, organizations, and advocacy groups aimed at reducing adverse weather changes [43]. There are many different perspectives on climate finance from banks, making it broad and complex [44].

Green traded stocks and bonds: Typically, "green securities" are described as bank securities that are primarily used to finance green sector projects, such as exchange-traded green indexes and green funds [41, 45]. The function of maximizing the resource allocation in the capital market and supporting the real economy is made possible by the development of green stocks and bonds [46]. China's stock market and banks, in particular, are pioneers in promoting green securities, which encourage the growth and innovation of listed firms [47]. Stock markets place a strong emphasis on creating green bonds, advancing the development of green index products, and strengthening global collaboration in green finance [28].

Green bancassurance: Everyone faces risks, and purchasing insurance is one method to manage these risks. Offering carbon-neutral underwriting protections for green vehicles, buildings, and other insurable assets or liabilities, green bancassurance [48]. The environment, humans, and animals directly benefits from these products. Providing eco-friendly policies with alternatives like premium discounts for carbon-neutral cars, certified green dwellings (buildings), and properties to homeowners, car owners, etc, banks work with insurers to promote sustainable activities [49]. Green banking encourages green invention supplying effective ways to prevent insurance-coverable hazards [50].

Green infrastructural finance: Green infrastructure financing is a cutting-edge method of funding that supports and improves ecological civilisation in development initiatives. It uses sustainable financing techniques to construct large-scale infrastructure projects like roads, schools, railroads, and hospitals [51, 52]. Marks on green infrastructure bonds have a significant impact on the subscription cost [53]. This draws in private investors and vehicles with specific functions to acquire financing for infrastructure. Because these bonds are typically sold at a premium, borrowers can benefit. Additionally, numerous studies show that financing green infrastructure has resulted in infrastructures with favorable environmental effects worldwide [54]. This supports sustainable growth and the global climate. Thus, this study comes to the conclusion that providing green infrastructure financing has the ability to improve climate conditions brought on by public buildings and stimulate further investment in green initiatives [55, 56].

In terms of green finance in african context, the Africa will need to invest around \$100 billion year to deal with the effects of climate change [57, 58] and over US\$600 billion to cover the costs for implementing the SDGs [59]. While it may be difficult to raise the full amount of financial and non-financial resources required to realize the SDGs' ambitions, given that public financing and traditional aid cannot fully fund the SDGs' implementation, the challenge is arguably even greater in Africa and the continent's energy sector because reaching universal access in Africa before 2030 is a prerequisite to achieving the majority of the SDGs by that same year [59]. Approximately 635 million people in Sub-Saharan Africa (SSA) lack access to electricity due to the region's low electrification rate of 32–35%, and 80% of people still rely on traditional biomass use for their energy needs [59]. Moreover, sixteen of the world's most major energy deficits are located in Sub-Saharan Africa (SSA), which also accounts for 57% of the global shortfall in electricity availability [60-62]. The funding needed to implement green programs and projects is insufficient [63]. This has resulted in a massive financial shortfall [61], can be satisfied by a further contribution from the business sector. Just 10% of Africa's energy financing comes from private sources, with the rest going toward climate finance [60]. With the increasing need for energy across the continent, Sub-Saharan Africa is well positioned to profit from the socio-economic and environmental advantages of renewable resources as well as energy efficiency measures. In order to facilitate the mobilization of financial flows into sectors, an evaluation of the financing potential and associated barriers for the financing deployment of renewable energy and energy efficiency sector mapping will be a positive step [60]. About half (49%) of the region's approved funding is held by the top ten recipient countries, while more fragile and war-torn nations like Liberia, Chad, Burundi, and Somalia, which are more vulnerable to climate change, receive less climate finance. Approximately 43 countries in SSA have received some climate finance [62]. The green finance investments in SSA are very low. Thus this study examines the awareness and preference of green finance in Somalia.

A convenient random sample of 530 employees of Somali banks is used in this study to collect data. This sampling technique is widely used for primary data sets and is a cost-effective method for collecting the data. The survey was chosen because the researchers saw it as the most effective method to understand and comprehend the awareness and preference for green finance by Somali bank employees. This study has used descriptive statistics as a method for data analysis the main reason is that is the most appropriate method as long as this study wants to find out number of people who prefer or aware the green finance practices in Somalia and other study uses same data analysis method as follows study [6]. The confidentiality of the survey responders is ensured to guarantee the survey's quality; filter questions are used. These filter questions are primarily used to determine whether respondents meet the three prerequisites – the respondents must be above 18 years of age, and they should be an employee of one of the banks in Somalia. The questionnaires are distributed in person; the researchers respectfully speak with employees who are present at the Islamic financial institutions’ counters to hand them out. The questionnaires, which are written in English, including the cover page and the contents, are given to the responders. Mogadishu, the capital of Somalia, serves as the location where the study's data is gathered. All Somali banks have their headquarters in this city, or at least have a branch there, which was a major factor in the decision to choose it as the location. Somalia has thirteen Islamic banks and two Takaful insurance businesses [56]. In order to reduce any potential bias caused by the large concentration of bank staff during specific hours of the day or days of the week, the surveys are presented during the banks' working hours as well as on different days of the week. The data was collected in June and July of 2023. Just 530 of the 600 surveys that the authors distributed were actually collected and returned, but they are all valid. The rate of collection is 88.33%. The questionnaire is structured as follows.

Question 1 aims to ascertain respondents' opinions on the significance of green finance in terms of commercial banks' social responsibility. Questions 2 to 6, the goal is to evaluate their familiarity with the meaning, methods, intentions, and well-known ideas in order to learn about the overview of green finance. Question 7 to 8 is to determine why people who respond negatively to the question of whether they prefer green financing when given the opportunity. Question 9 asks respondents their opinions on the relationship between promoting green financial knowledge and the cause of environmental conservation. The questionnaire was distributed using Google document form and spread on social media such as WhatsApp and Facebook, as well as email. In this study, all the variables are adopted from previous studies on related on green finance, enviromental protection and all instruments has been validated [6].

In order to learn how the employees, feel about environmental protection and how familiar they are with green finance, the researchers distributed questionnaires to 600 respondents who work in Somalia's banking sector. According to the studies, bank staffs are more knowledgeable about green money than the general public. This is why the writers decided to use them as the responses. The surveys are randomly distributed to various kinds of employees at each bank in order to produce a more convincing result, with each bank receiving a quarter of the total questionnaires.

Table 1 outlines the paper's demographic section. The data indicates that men make up 67.0% of the sample's responders while women make up 33.0% of them. The majority of respondents were between the ages of 18 and 25, which accounted for 64.2% of the total, followed by the 25 to 35 age range, which accounted for 32.3%. The majority of respondents (55.8%) are graduates, followed by undergraduates (36.4%) in terms of educational attainment. 23.4% of respondents reported are married, leaving 76.6% of them single. Finally, when it comes to the respondents' working experience in the banking sector in Somalia, the majority of them are in-between one and three years' worth of experience, accounting for up to 40.2%, while those with less than one-year experience is the second which accounted up to 39.2%.

Table 1. Background of the respondents

|

Variable |

Frequency |

Percent |

|

Gender |

||

|

Male |

355 |

67.0 |

|

Female |

175 |

33.0 |

|

Age |

||

|

18 - 25 years |

340 |

64.2 |

|

26 – 35 years |

171 |

32.3 |

|

above 35 |

19 |

3.6 |

|

Total |

530 |

100.0 |

|

Level of Education |

||

|

Graduate |

296 |

55.8 |

|

Undergraduate |

193 |

36.4 |

|

High school |

21 |

4.0 |

|

Other |

20 |

3.8 |

|

Total |

530 |

100.0 |

|

Marital Status |

||

|

Single |

406 |

76.6 |

|

Married |

124 |

23.4 |

|

Expreince |

||

|

Less than 1 year |

208 |

39.2 |

|

Between 1-3 years |

213 |

40.2 |

|

Between 3-5 years |

56 |

10.6 |

|

Above 5 years |

53 |

10.0 |

|

Total |

530 |

100.0 |

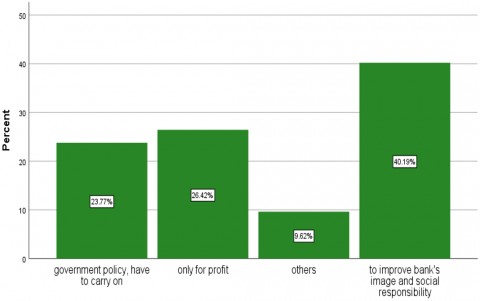

Figure 1. Importance of green finance

Figure 1 depicts the respondents' perceptions of the importance of green finance for Somalia's commercial banks. 38.87% of them chose “supporting the development of charity and protecting the vulnerable group” as the most important green finance for commercial banks. 27.55% considered “allocating capital to the areas the protect the environment and social resources” is the most significant one. The result of this study is consistent with [6], who finds similar results. Another 25.85% understood “responsible the shareholders’ employees and customer” are more significant. the least significant one is “others” which only accounted 7.74%. Therefore, the result indicates that the respondents have different views about the important of green finance.

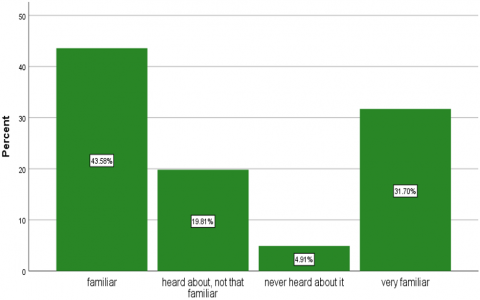

Figure 2. Familiarity with green finance

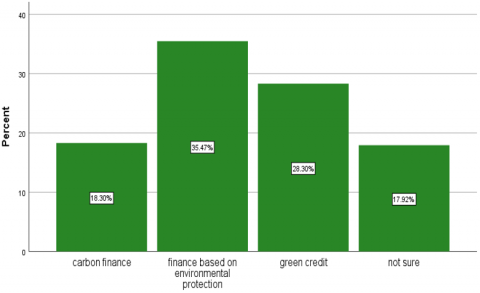

Figure 3. Familiarity with the connotation

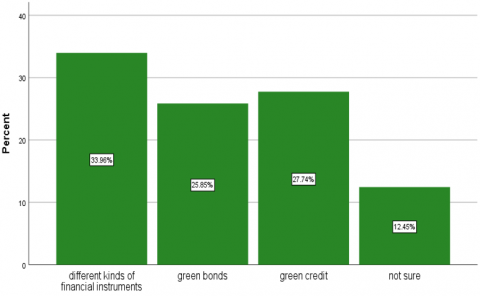

Figure 4. Familiarity with the methods

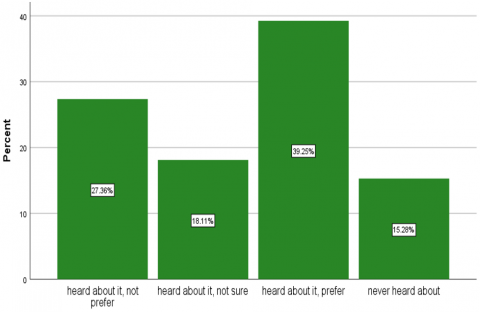

Figure 5. Familiarity with the Equator Principles and preference

Figure 6. Familiarity with the purpose

Figure 2 demonstrates how familiar with the idea of green finance the respondents are. In terms of familiarity with green financing, 75.28% are familiar or very familar with green financing. The result of this study is contradicting to the findings of study [6] who finds that majority of the respondents heard about the concept but did not have deeper understanding about green finance. The main reason about this difference maybe is the different context between China and Somalia as Somalia people are more information oriented people. 19.81% of respondents claimed they had heard of the idea but lacked a thorough understanding of what it actually entailed. Finally, only 4.91% of respondents stated they had never heard of green finance. Thus, the results show that the majority of the respondents are familiar with the idea of green finance. The Somali people are reading or seen the devastation of climate change on their communities.

Figure 3 answers what respondents understand about the connotation of finance in terms of commercial banks. 35.47% regard it as finance based on environmental protection. This result is contrading to the findings of study [6] who finds that carbon finance is the most familar one and second is environmental protectio. 28.30 % thought it is green credit. 18.30% viewed it as carbon finance and the rest were not sure about the connotation of it. Therefore, the vast majority of respondents concurred that green finance is a form of financing focused on environmental protection, demonstrating that they are familiar with the term becuase Somalis are very concern about the impact of climate change on their lives as long as they do not have much protection from their goverment or any other organization and climate are changing rapidly [15].

Figure 4 illustrates the methods of green finance in terms of commercial banks in the respondent’s opinions in Somalia. 33.96% selected different kinds of financial instruments which is similary to the findings of study [6], whereas 27.74% chosen green credit, and 25.85% believed that the methods of green finance are green bonds. Lastly, only 12.45% are not sure what kind of methods belong to green finance. Hence, the majority of the respondents indicated that green finance methods are different kinds of financial instruments including green bonds, green credit and much more. Thefore, this study concludes the true method of green finance are not clear for the respondents as long as different products have been choisen by the respondents.

Figure 5 shows whether the respondents have heard about the Equator Principles or not and whether they will prefer to choose the banks that practice this principle or not. The result shows that majority 39.25% had “heard about it, prefer” the principle which is contrading to the findings of study [6] who finds that never heard about the principle, whereas the number of respondents choosing “heard about it, not prefer” is 27.36%. Second, 18.11% choose “heard about it, not sure”. Finally, only 15.28% selected “never heard about”. That shows the most of the respondents have heard the Equator Principles and preferred the green finance. Therefore, the results indicate the most of the respondents have understood and prefer the Equator Principle in green finance.

Figure 6 summarizes what the respondents regard as purpose of practice in green finance. 40.19% believed the banks chose it for the reason of shouldering their corporate social responsibility in order to increase its image and by doing this, improve their reputations which is similary to the findings of study [6]. Second, “only for profit” is 26.42%, then “following the government’s policy” and “others” by 23.77% and 9.62% respectively. Thefore, the majority of respondents viewed that the purpose of green finance practices by the banks are for purpose to improve banks' reputations and social responsibility.

Figure 7. Preference in green finance

Figure 8. Reason for not choosing

Figure 7 and Figure 8 both are discussing preference in green finance and the answer whether the respondents will choose green finance instruments or not if the return on investment is exactly the same as the time deposit rate. Figure 7 indicates that the majority of the respondents 65.47% prefer green finance which is contrading to the findings of study [6] who finds that majority of the respondents are not sure whether they prefer or not for green finance and only 14.34% they are not preferring green finance. Therefore, this results demonstrate that the vast majority of the respondents prefer green finance which is good indication for the future. Hence, it very crucial for somalis to prefer green finance in order to adopt climate change that effects badly [15]. The Figure 8 also shows that the most respondents are not choosing green finance because they are afraid of trouble 31.51% which is similary to the findings of study [6]. and it followed by the respondents who said they afraid of uncertainty by 27.35%. lastly, not familiar green finance took third position 21.70%. finally, other factors are causing why I am not choosing green finance is only 19.43%. therefore, this study shows that the main reason that respondents are not choosing green finance is because they afraid trouble or uncertainty. The idea of green finance do not exist or new in Somalia that is why majority are afraid or uncertain to use green finance.

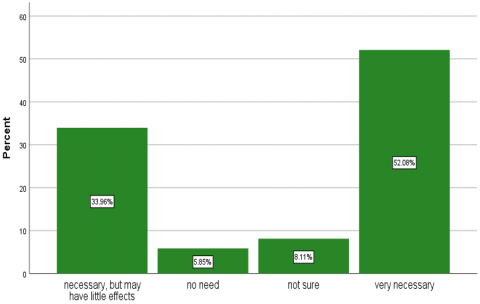

Figure 9. Necessity of popularizing green finance

Figure 9 shows the respondents' opinion on whether popularizing green finance is necessary for promoting the environmental protection. 86.04% stated its very necessity or necessary, but may have little effects which is similary to the findings of study [6]. Finally, only 8.11% and 5.85% choose not sure and no need respectively. Thus, large majority of the respondents agreed that it is necessary to promote green finance in order enhance environmental protection becuase Somalia is one of the most effected countries by climate change [15].

First, the significance of green finance. When asked why green finance is important, the majority of respondents in Somalia's commercial banks employees selected "supporting the growth of charity and protecting the vulnerable group." Most of the country's bank employees also place a high value on using green finance to assist and protect vulnerable groups. While the respondents ranked "allocating cash to the areas that protect the environment and social resources" in second position, but other studies have given it the first position [6]. Because they do not practice green finance and the vast majority of their funding is tied to Murabaha financing for autos and other goods that might be contributing to climate change issues, Somali commercial banks do not recognize the importance of green finance [57, 58]. Therefore, as the climate change problem is increasing the commercial banks should give great attention to green finance since Somalia is vulnerable to climate change consequences.

In terms of the awareness of green finance, the result demonstrated that respondents have familiar with the concept of green as more than 75% agreed they are familiar or very familiar and only less than 5% said they never heard about the concept of green finance. The results are unexpected because we were assuming that respondents do not have any concept about green finance, but many efforts are still required to be made to improve the awareness of the commercial banks to finance climate change and increase the awareness of the public.

The respondents who think green finance has a connotation of being green, which is akin to green, came in second with more than one third of the respondents believing that it is financing based on environmental protection [6]. There is also a small part of respondents who have misunderstanding about the relationship between carbon finance and green finance or had no idea about what the connotation was. Green credit has a rather long history and has accounted for a sizable portion of green finance in commercial banks, as shown by the theoretical framework. For instance, the Agricultural Bank of China has green credit projects totaling 472.45 billion CNY, greatly exceeding the amount of other green finance products. However, it is undeniable that there are some additional types of green financing instruments [6].

Regarding green financing strategies, the majority of respondents thought there were several different types, and a tiny percentage said they were just unsure. Recent years, the instruments of green financing have seen a sharp rise; as an example, bank industry has introduced low-carbon credit cards and green bonds.

The Equator Principles are the next topic, and roughly 40% of respondents had heard of the idea, with only 15% saying they have never heard of it. This demonstrates that the majority of bank employees in Somalia at least understand the notion of the equator. The Equator Principles were created in 2002 at a gathering of some highly regarded commercial institutions. It is the guiding philosophy that was developed when those cutting-edge financial institutions looked for a more effective approach to fulfill their social obligations. Finally, more than 40% of respondents think that green financing for social responsibility can help commercial banks' reputations.

Moreover, choice of green financing; More than two thirds of the respondents would say they prefer green finance, and nearly 60% of the respondents say they would never choose green finance because they are afraid of trouble or afraid of uncertainty. The respondents had the option to invest in time deposit or green finance instruments with the same return on capital as time deposit. The fact that they were unfamiliar with the idea of green finance, worried that the return on their investment might change, or chose to avoid problems is the likely cause. This indicates that more respondents will accept green finance instruments as one of their options for managing their finances if the public awareness of green finance is increased.

Finally, more than 85% of respondents believe that the popularization of green finance is essential, indicating that most of them are aware of the risks associated with climate change and the potential role that green money could play in reducing those risks. Less than 6%, on the other side, said it was not vital for the advancement of environmental preservation. Most of the respondents feel that the deal will have a favorable impact on environmental protection.

The result of this study indicates that the respondents have different views about the important of green finance, although majority of them seen as essential for their lives. The result also shows that respondents are familiarity with green finance, although large number of the respondents are not choosing green finance because they are afraid of trouble or uncertainty. In addition, the employees of Somali banks are preferring green finance mainly 65.47%. this study will help the Somali bank managements to educate their employees and clients for the benefits of using green finance. The findings of this study will also help policy makers to push the usage of green finance to tackle the impact of climate challenge. Lastly, this study will help the future researchers, academicians as a guideline for the future studies and will contribute to the body of knowledge in this field.

The majority of bank industry employees acknowledge the value of using green finance to address issues related to climate change, but they have only a limited understanding of its idea, connotation, methodology, and key concepts. Nonetheless, they frequently express the goal of using green financing more explicitly. They also know less about how various commercial bank types conduct their green finance business, and the majority of them acknowledge the significance of spreading awareness of green finance to safeguard the environment.

The banks in Somalia are not offering any green finance investments, there are notable differences between the staff's beliefs and the actual reality in some areas, such as "supporting the growth of charity and protecting the vulnerable group" and the real practice of commercial banks. As a matter of fact, it is important for Somali banks to offer green finance investments in order to contribute to the mitigation of climate change because if the banks provide more financing to the businesses, those businesses will be more environmentally friendly, which will help mitigating climate change. The employee of Somali banks more than 75% are aware with green finance. Thus, the results show that the majority of the respondents are familiar with the idea of green finance. In terms of motivation to provide green finance, the majority of respondents 65% said they are motivated or prefer to offer green finance.

The implications of this study: First, as the vast majority of respondents prefer green finance, it is suggested that the commercial banks of Somalia should start providing green finance to their clients in order to participate tackling the climate change, since Somalia is considered one of the vulnerable countries to climate change in the world. Second, as this study found that the majority of respondents are not choosing green finance because they are afraid of trouble or uncertainty, it is recommended to increase the awareness of green finance in order to easily enhance the adoption or the usage of green finance by the clients in Somali banks. Third, the large part of the respondents think green finance is necessary offer. Hence the commercial banks of Somalia should offer green finance to increase the potential customers and to safeguard the previous customers. Lastly, as large part of respondents’ familiarity with green financing, it is suggested that the policy makers should make compulsory for the private banks to offer green finance to reduce the impact of climate change. The study adds to the body of knowledge in service marketing literature in the following ways. In terms practical of knowledge, this study finding provide a significant contribution to the current knowledge of sustainable environmental protection by the banks. Second, this study is the first attempt to examine the awareness and preference of green finance in Somalia. Finally, this study fills the gap which previous studies left since green finance is new in Somalia.

6.1 Limitations and future research of the study

There are some limitations related to this study that give direction to potential researchers in this field. Firstly, the researcher conducted this empirical study in Mogadishu city. Therefore, it has geographical limitations. Future studies can be conducted targeting other cities in Somalia as well as rural areas to get more insightful results pertaining to awareness and preference of green finance. Secondly, the primary data source of this study is collected only from employees of Somali banks. Future research should be included both Somali bank staff and clients to see their preference of green finance. Finally, a questionnaire instrument was used in this study to collect data. Future studies should be considered using other data collection tools, such as interviews.

[1] Akhtar, S., Martins, J.M., Mata, P.N., Tian, H., Naz, S., Dâmaso, M.,Santos, R.S. (2021). Assessing the relationship between market orientation and green product innovation: The intervening role of green self-efficacy and moderating role of resource bricolage. Sustainability, 13(20): 11494. https://doi.org/10.3390/su132011494

[2] Jewell, J., McCollum, D., Emmerling, J., Bertram, C., Gernaat, D.E., Krey, V., Keppo, I. (2018). Limited emission reductions from fuel subsidy removal except in energy-exporting regions. Nature, 554(7691), 229-233. https://doi.org/10.1038/nature25467

[3] Zhang, X., Wang, Z., Zhong, X., Yang, S., Siddik, A.B. (2022). Do green banking activities improve the banks’ environmental performance? The mediating effect of green financing. Sustainability, 14(2): 989. https://doi.org/10.3390/su14020989

[4] Zheng, G.W., Siddik, A.B., Masukujjaman, M., Fatema, N., Alam, S.S. (2021). Green finance development in Bangladesh: The role of private commercial banks (PCBs). Sustainability, 13(2): 795. https://doi.org/10.3390/su13020795

[5] Zheng, G.W., Siddik, A.B., Masukujjaman, M., Fatema, N. (2021). Factors affecting the sustainability performance of financial institutions in Bangladesh: The role of green finance. Sustainability, 13(18): 10165. https://doi.org/10.3390/su131810165

[6] Zhu, W., Zhu, Z., Fang, S., Pan, W. (2017). Chinese students’ awareness of relationship between green finance, environmental protection education and real situation. Eurasia Journal of Mathematics, Science and Technology Education, 13(7): 3753-3769. https://doi.org/10.12973/eurasia.2017.00757a

[7] Akter, N., Siddik, A., Mondal, M.A. (2018). Sustainability reporting on green financing: A study of listed private sustainability reporting on green financing: A study of listed private commercial banks in Bangladesh. Journal of Business and Technology, 12: 14-27.

[8] Hoque, N., Mowla, M., Uddin, M.S., Mamun, A., Uddin, M.R. (2019). Green banking practices in Bangladesh: A critical investigation. International Journal of Economics and Finance, 11(3): 58-68. https://doi.org/10.5539/ijef.v11n3p58

[9] Bhardwaj, B.R., Malhotra, A. (2013). Green banking strategies: Sustainability through corporate entrepreneurship. Greener Journal of Business and Management Studies, 3(4): 180-193. https://doi.org/10.15580/GJBMS.2013.4.122412343

[10] Nisha, N. (2017). Green investments and returns: A developing country perspective. In Measuring Sustainable Development and Green Investments in Contemporary Economies, USA, pp. 1-21. https://doi.org/10.4018/978-1-5225-2081-8.ch001

[11] Bekun, F.V. (2022). Mitigating emissions in India: Accounting for the role of real income, renewable energy consumption and investment in energy. International Journal of Energy Economics and Policy, 12(1): 188-192. https://doi.org/10.32479/ijeep.12652

[12] Pickson, R.B., He, G., Ntiamoah, E.B., Li, C. (2020). Cereal production in the presence of climate change in China. Environmental Science and Pollution Research, 27: 45802-45813. https://doi.org/10.1007/s11356-020-10430-x

[13] Warsame, A.A., Mohamed, J., Ali, A. (2023). The relationship between environmental degradation, agricultural crops , and livestock production in Somalia. Environmental Science and Pollution Research, 30(3): 7825-7835.. https://doi.org/10.1007/s11356-022-22595-8

[14] Abdi, A.H., Warsame, A.A., Sheik-Ali, I.A. (2022). Modelling the impacts of climate change on cereal crop production in East Africa: Evidence from heterogeneous panel cointegration analysis. Environmental Science and Pollution Research, 30(12): 35246-35257, https://doi.org/10.1007/s11356-022-24773-0

[15] Warsame, A.A., Sheik-Ali, I.A., Ali, A.O., Sarkodie, S.A. (2021). Climate change and crop production nexus in Somalia: An empirical evidence from ARDL technique. Environmental Science and Pollution Research, 28(16): 19838-19850. https://doi.org/10.1007/s11356-020-11739-3

[16] Warsame, A.A., Sheik-Ali, I.A., Hassan, A.A., Sarkodie, S.A. (2022). Extreme climatic effects hamper livestock production in Somalia. Environmental Science and Pollution Research, 29(27): 40755-40767. https://doi.org/10.1007/s11356-021-18114-w

[17] Lal, R., Singh, B. (1998). Effects of soil degradation on crop productivity in East Africa. Journal of sustainable agriculture, 13(1): 15-36. https://doi.org/10.1300/J064v13n01_04

[18] Barrios, S., Ouattara, B., Strobl, E. (2008). The impact of climatic change on agricultural production: Is it different for Africa? Food policy, 33(4): 287-298. https://doi.org/10.1016/j.foodpol.2008.01.003

[19] Warsame, A.A., Sheik-Ali, I.A., Jama, O.M., Hassan, A.A., Barre, G.M. (2022). Assessing the effects of climate change and political instability on sorghum production in Somalia. Journal of Cleaner Production, 360: 131893. https://doi.org/10.1016/j.jclepro.2022.131893

[20] Jama, O.M., Liu, G., Diriye, A.W., Yousaf, B., Basiru, I., Abdi, A.M. (2020). Participation of civil society in decisions to mitigate environmental degradation in post-conflict societies: Evidence from Somalia. Journal of Environmental Planning and Management, 63(9): 1695-1715. https://doi.org/10.1080/09640568.2019.1685957

[21] Hussein, M., Law, C., Fraser, I. (2021). An analysis of food demand in a fragile and insecure country: Somalia as a case study. Food Policy, 101: 102092. https://doi.org/10.1016/j.foodpol.2021.102092

[22] Warsame, A.A., Sarkodie, S.A. (2022). Asymmetric impact of energy utilization and economic development on environmental degradation in Somalia. Environmental Science and Pollution Research, 29(16): 23361-23373. https://doi.org/10.1007/s11356-021-17595-z

[23] Warsame, A.A., Sheik-Ali, I.A., Mohamed, J., Sarkodie, S.A. (2022). Renewables and institutional quality mitigate environmental degradation in Somalia. Renewable Energy, 194: 1184-1191. https://doi.org/10.1016/j.renene.2022.05.109

[24] Urban, M. A., Wójcik, D. (2019). Dirty banking: Probing the gap in sustainable finance. Sustainability, 11(6): 1745. https://doi.org/10.3390/su11061745

[25] Tan, D., Adedoyin, F.F., Alvarado, R., Ramzan, M., Kayesh, M.S., Shah, M.I. (2022). The effects of environmental degradation on agriculture: Evidence from European countries. Gondwana Research, 106: 92-104. https://doi.org/10.1016/j.gr.2021.12.009

[26] Salazar, J. (1998). Environmental finance: Linking two world. In a Workshop on Financial Innovations for Biodiversity Bratislava, 1: 2-18.

[27] Yu, C.H., Wu, X., Zhang, D., Chen, S., Zhao, J. (2021). Demand for green finance: Resolving financing constraints on green innovation in China. Energy Policy, 153: 112255. https://doi.org/10.1016/j.enpol.2021.112255

[28] Akomea-Frimpong, I., Adeabah, D., Ofosu, D., Tenakwah, E.J. (2022). A review of studies on green finance of banks, research gaps and future directions. Journal of Sustainable Finance & Investment, 12(4): 1241-1264. https://doi.org/10.1080/20430795.2020.1870202

[29] Raberto, M., Ozel, B., Ponta, L., Teglio, A., Cincotti, S. (2019). From financial instability to green finance: The role of banking and credit market regulation in the Eurace model. Journal of Evolutionary Economics, 29: 429-465. https://doi.org/10.1007/s00191-018-0568-2

[30] Díaz-García, C., González-Moreno, Á., Sáez-Martínez, F.J. (2015). Eco-innovation: Insights from a literature review. Innovation, 17(1): 6-23. https://doi.org/10.1080/14479338.2015.1011060

[31] Islam, M.A., Yousuf, S., Hossain, K.F., Islam, M.R. (2014). Green financing in Bangladesh: Challenges and opportunities-a descriptive approach. International Journal of Green Economics, 8(1): 74-91. https://doi.org/10.1504/IJGE.2014.064469

[32] Chen, S., Huang, Z., Drakeford, B.M., Failler, P. (2019). Lending interest rate, loaning scale, and government subsidy scale in green innovation. Energies, 12(23): 4431. https://doi.org/10.3390/en12234431

[33] Cullen, J. (2018). After ‘HLEG’: EU banks, climate change abatement and the precautionary principle. Cambridge Yearbook of European Legal Studies, 20: 61-87. https://doi.org/10.1017/cel.2018.7

[34] Verma, M.K. (2012). Green banking: A unique corporate social responsibility of India Banks. International Journal of Research in Commerce & Management, 3(1): 110-114.

[35] He, L., Liu, R., Zhong, Z., Wang, D., Xia, Y. (2019). Can green financial development promote renewable energy investment efficiency? A consideration of bank credit. Renewable Energy, 143: 974-984. https://doi.org/10.1016/j.renene.2019.05.059

[36] Julia, T., Rahman, M.P., Kassim, S. (2016). Shariah compliance of green banking policy in Bangladesh. Humanomics, 32(4): 390-404. https://doi.org/10.1108/H-02-2016-0015

[37] Da, B., Liu, C., Liu, N., Xia, Y., Xie, F. (2019). Coal-electric power supply chain reduction and operation strategy under the cap-and-trade model and green financial background. Sustainability, 11(11): 3021. https://doi.org/10.3390/su11113021

[38] Esposito, L., Mastromatteo, G., Molocchi, A. (2019). Environment–risk-weighted assets: Allowing banking supervision and green economy to meet for good. Journal of Sustainable Finance & Investment, 9(1): 68-86. https://doi.org/10.1080/20430795.2018.1540171

[39] Ganda, F. (2018). The influence of carbon emissions disclosure on company financial value in an emerging economy. Environment, Development and Sustainability, 20: 1723-1738. https://doi.org/10.1007/s10668-017-9962-4

[40] Glomsrød, S., Wei, T. (2018). Business as unusual: The implications of fossil divestment and green bonds for financial flows, economic growth and energy market. Energy for Sustainable Development, 44: 1-10. https://doi.org/10.1016/j.esd.2018.02.005

[41] D’Orazio, P., Popoyan, L. (2019). Fostering green investments and tackling climate-related financial risks: Which role for macroprudential policies? Ecological Economics, 160: 25-37. https://doi.org/10.1016/j.ecolecon.2019.01.029

[42] D’Orazio, P., Valente, M. (2019). The role of finance in environmental innovation diffusion: An evolutionary modeling approach. Journal of Economic Behavior & Organization, 162: 417-439. https://doi.org/10.1016/j.jebo.2018.12.015

[43] Urban, M.A., Wójcik, D. (2019). Dirty banking: Probing the gap in sustainable finance. Sustainability, 11(6): 1745. https://doi.org/10.3390/su11061745

[44] Buchner, B., Herve-Mignucci, M., Trabacchi, C., Wilkinson, J., Stadelmann, M., Boyd, R., Micale, V. (2014). Global landscape of climate finance 2015. Climate Policy Initiative, 32: 1-38.

[45] Ziolo, M., Filipiak, B. Z., Bąk, I., Cheba, K. (2019). How to design more sustainable financial systems: The roles of environmental, social, and governance factors in the decision-making process. Sustainability, 11(20): 5604. https://doi.org/10.3390/su11205604

[46] Yuan, F., Gallagher, K.P. (2018). Greening development lending in the Americas: Trends and determinants. Ecological Economics, 154: 189-200. https://doi.org/10.4324/9780429330193-3

[47] Taghizadeh-Hesary, F., Yoshino, N. (2019). The way to induce private participation in green finance and investment. Finance Research Letters, 31: 98-103. https://doi.org/10.1016/j.frl.2019.04.016

[48] Wang, C., Nie, P.Y., Peng, D.H., Li, Z.H. (2017). Green insurance subsidy for promoting clean production innovation. Journal of Cleaner Production, 148: 111-117. https://doi.org/10.1016/j.jclepro.2017.01.145

[49] Green, T.L., Kronenberg, J., Andersson, E., Elmqvist, T., Gomez-Baggethun, E. (2016). Insurance value of green infrastructure in and around cities. Ecosystems, 19: 1051-1063. https://doi.org/10.1007/s10021-016-9986-x

[50] Mills, E. (2012). The greening of insurance. Science, 338(6113): 1424-1425. https://doi.org/10.1126/science.1229351

[51] Falcone, P.M., Sica, E. (2019). Assessing the opportunities and challenges of green finance in Italy: An analysis of the biomass production sector. Sustainability, 11(2): 517. https://doi.org/10.3390/su11020517

[52] La Rocca, R., Baietti, A. (2012). Green infrastructure finance: Framework report. World Bank Publications, USA.

[53] Gianfrate, G., Peri, M. (2019). The green advantage: Exploring the convenience of issuing green bonds. Journal of Cleaner Production, 219: 127-135. https://doi.org/10.1016/j.jclepro.2019.02.022

[54] Tolliver, C., Keeley, A.R., Managi, S. (2020). Drivers of green bond market growth: The importance of Nationally Determined Contributions to the Paris Agreement and implications for sustainability. Journal of Cleaner Production, 244: 118643. https://doi.org/10.1016/j.jclepro.2019.118643

[55] Flaherty, M., Gevorkyan, A., Radpour, S., Semmler, W. (2017). Financing climate policies through climate bonds–A three stage model and empirics. Research in International Business and Finance, 42: 468-479. https://doi.org/10.1016/j.ribaf.2016.06.001

[56] Central bank of Somalia. (2023). SUPERVISION AND LICENSING. Retrieved from https://centralbank.gov.so/licensing-supervision-department/

[57] Barre, G.M. (2023). Tawarruq as an alternative product for bai al-inah within the Islamic banking system: A case study of Somali Islamic banks. Asian Economic and Financial Review, 13(1): 85-97. https://doi.org/10.55493/5002.v13i1.4697

[58] Hallegatte, S. (2016). Shock waves: Managing the impacts of climate change on poverty. World Bank Publications, USA.

[59] Chirambo, D. (2018). Towards the achievement of SDG 7 in Sub-Saharan Africa: Creating synergies between Power Africa, Sustainable Energy for All and climate finance in-order to achieve universal energy access before 2030. Renewable and Sustainable Energy Reviews, 94: 600-608. https://doi.org/10.1016/j.rser.2018.06.025

[60] Mungai, E.M., Ndiritu, S.W., Da Silva, I. (2022). Unlocking climate finance potential and policy barriers—A case of renewable energy and energy efficiency in Sub-Saharan Africa. Resources, Environment and Sustainability, 7: 100043. https://doi.org/10.1016/j.resenv.2021.100043

[61] Chirambo, D. (2016). Addressing the renewable energy financing gap in Africa to promote universal energy access: Integrated renewable energy financing in Malawi. Renewable and Sustainable Energy Reviews, 62: 793-803. https://doi.org/10.1016/j.rser.2016.05.046

[62] Watson, C., Schalatek, L. (2019). Climate finance fundamentals 3: Thematic briefing-adaptation finance. Overseas Development Institute and Heinrich Böll Stiftung North America.

[63] Fagbemi, F., Osinubi, T.T. (2020). Leveraging foreign direct investment for sustainability: An approach to sustainable human development in Nigeria. Resources, Environment and Sustainability, 2: 100005. https://doi.org/10.1016/j.resenv.2020.100005