Ilirjeta Gashi | Vlora Prenaj*![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Public procurement is a critical aspect of economic growth in today's world, particularly in developing countries. The aim of this research is to analyze the National Audit Office's findings of irregularities in public sector institutions regarding public procurement and demonstrate the importance of auditing in improving the public procurement process, especially in public enterprises. Specifically, this study examines how auditing can enhance the quality of public procurement in the Republic of Kosovo, where it is used in public enterprises. The researcher obtained information from the auditor's report on the National Audit Office's annual financial statements and the annual reports on the annual financial statements of public enterprises. Through data analysis and statistical evaluation methods based on the findings and the implementation of the auditor's recommendations related to the findings in the public procurement process, the study concludes that auditing has a positive impact on improving the quality of public procurement.

public procurement, public enterprises, audit, National Audit Office

Public procurement constitutes a significant part of European Union spending. In Kosovo, public procurement started after the end of the war and is still a new field. Public procurement is a very important issue from a socio-economic point of view, its importance is also shown by its participation in the country's GDP. Through public procurement in Kosovo in 2020, the value of signed contracts was calculated as a percentage of 7.50% of GDP [1].

In Kosovo, the Auditor General of the Republic of Kosovo is the highest institution of economic and financial control. The organization, operation, and powers of the Auditor General of the Republic of Kosovo are determined by the Constitution and by special laws [2]. The Auditor General is functionally, financially, and operationally independent and is not subject to orders or influence from any other person or institution. As the head of the National Audit Office (NAO), the Auditor General is responsible to the Assembly for carrying out the duties and powers set out in the Constitution, the law, by-laws, and internationally recognized standards for auditing the public sector [3]. The NAO conducts regularity audits and performance audits. When conducting performance audits or other types of audits, the NAO, in accordance with internationally recognized public sector auditing standards, evaluates the efficiency, effectiveness, and/or economy of a particular aspect of the operations in whole or in part of any institution, program, or activity [3].

Public procurement refers to public purchases made by the government, municipalities, district councils, and public companies, as well as associations and foundations, in order to carry out their various activities [4]. Every legislation on public procurement, which has been in force in Kosovo from 1999 to 2012, places a significant importance on the basic principles of public procurement. The basic principles, which are prioritized according to the public procurement legislation in Kosovo, are transparency, equality in treatment/non-discrimination, competition, economy and efficiency, professionalism, integrity, and value for money.

The audit of the annual financial statements carried out by the NAO in public procurement makes a great contribution to economic development. The more financial controls are carried out by the State Audit Office, the greater the control over the spending of public funds through public procurement procedures [5]. Public procurement has an impact on the economy [6], the market, public institutions, individuals, and enterprises [7]. The role of auditing in improving the public procurement process has been explored in several cases. Public service agencies strive to maximize overall "value for money" for citizens. This requires consideration of issues such as customer satisfaction, public interest, fair play, fairness, justice, and equity [8]. Regardless of whether the audit report is about providing a fair and honest presentation of the financial situation, auditing the public sector requires an exercise of professional judgment [9].

Despite the fact that government organizations and public procurement professionals have worked extensively to enhance public procurement methods, public procurement has received little attention from academics [10]. The importance of public procurement affects many different areas of an economy. All contracting authorities are obliged to ensure that public funds are used in the most economical way, taking into consideration the purpose and subject of the procurement. Public funds that have been provided under a public contract may be used only by that contract and only for the same purposes [11].

Public procurement is also a key way for governments to directly or indirectly affect all parts of public and economic life and work toward national strategic goals, such as economic growth [12]. Even though the International Auditing Standards (ISA) for Supreme Audit Institutions (SAI) apply to different types of public financial operations, there is currently no International Organization of Supreme Audit Institutions (INTOSAI) standard for auditing public procurement. So, when auditing these cases, public sector auditors must rely on the ISSAI's very general requirements and their own experience, which is often different from the ISA's.

The audit of public procurement is one area of auditing that lets us give the most thorough assessment and understanding of the factors that affect the efficient use of budget funds, as well as audit procedures that will prevent large losses in the future by changing the way the public procurement industry grows [13]. Using a method that takes into account both the quantitative and qualitative parameters of procurement risks, an audit of the effectiveness of the use of public funds for each procurement must be done, and areas of cost-effectiveness for state budget funds must be found [14]. Lastly, we know that the purpose of auditing in the public procurement process is to increase accountability and transparency, to encourage improvement and trust in the right use of public funds, to make management and oversight bodies more effective, and to encourage change [12]. Public procurement is receiving more attention now than ever before [15]. But shortcomings in this field still persist [12]. Public procurement is receiving more attention now than ever before [15]. But shortcomings in this field still persist [16].

In this research, we try to examine the findings of irregularities in institutions in the public sector. The purpose of this paper is to look at the role of auditing in improving the quality of the public procurement process, especially in Kosovo.

The paper is structured as follows: section 2 theoretical approach and literature review, section 3 research methodology, section 4 presents results and discussions. Finally, in the last section, the conclusions and recommendations.

2.1 Auditing as an important process in the control of public money

Auditing is an additional inspection in professional work based on existing documents, and it has a corrective nature as opposed to a type of control [17]. Auditing represents a method of inspecting accounting reports, data from the main books, and other documents to obtain authentic information about the economic and financial condition of an enterprise [18]. Auditing is an important process for controlling public funds and implementing internal control procedures for public money [18]. Auditing as a process should be based on acceptable standards, such as the INTOSAI standards and the applicable legislation in force. The INTOSAI acts as an umbrella organization for the external government audit community [19].

Harmonizing standards in each country is a constant trend, which leads to the creation of international standards that many countries agree on. In 1998, the Auditing Standards Committee released the Code of Ethics of the International Organization of Supreme Audit Institutions at the XIX Congress of INTOSAI in Montevideo, Uruguay [20]. These International Standards on Auditing (ISA), which were suggested by INTOSAI, have been accepted by Kosovo and put into place by the State Audit Agency in the Regulation of State Auditing Standards and the ISA of the International Federation of Accountants (IFAC). With this step, Kosovo is one of the countries that has started to harmonize the practices and protocols used around the world and set up an audit system that is the same as the ones used in developed countries. The INTOSAI standards are a way for states to set their own auditing standards, and they don't go against the IFAC standards [20].

The SAI must do the external audit, while licensed, independent auditors must do the same for private sector businesses. The SAI must be established and determined by the legislation of the respective country, respectively by the Constitution of the country [2].

During the financial year, the NAO does interim audits to check on how the recommendations from previous audits are being used and to see if these recommendations have been used as a basis. The NAO, while conducting performance audits or other audits in accordance with ISA in the public sector, evaluates the efficiency, effectiveness, and/or economy of a particular aspect of the operations in whole or in part of any institution, program, or activity [3]. Procurement efficiency and procurement effectiveness of the purchasing function are measures of procurement performance [21]. Effective auditing of public procurement ensures that public entities achieve the best value for money and honesty, and in doing so, secure public trust [22]. We think that making audit standards for public procurement would make the work of the auditors easier and would help improve the quality of public procurement and get more for the money.

2.2 Public procurement process, legal framework, and its operationalization

Procurement is an essential part of public service delivery for contracting authorities, public procurement refers to the process by which public authorities buy works, goods, or services, efficient and cost-effective procurement is essential to good governance.

When auditing public procurement, the auditor must take into account the nature and purpose of the EU public procurement regime. Although it is still rooted in budget law, the EU regime is nevertheless supposed not only to save public money, but also to build the European common market. Three basic principles derive precisely from this nature and the underlying legislation: competition, non-discrimination/equal treatment, and transparency. The auditor is advised to first verify whether the contracting authority has adhered to the spirit of these principles and not just the wording of the detailed regulations. But this doesn't mean that a contracting authority doesn't have to follow the detailed rules. Even though breaking these rules seems like a small mistake that often leads to the rejection of the most economically advantageous bid, it is important to note that meeting these often formal requirements helps ensure that all bidders are treated the same. The internal context due to various corrupt activities involving public tenders, public procurement has long been one of the most criticized sectors in Kosovo by civil society and the media. However, after the creation of the electronic procurement system, Kosovo has taken a step forward in increasing transparency and accountability [11]. Kosovo has tried to change the Law on Public Procurement [11] through changes aimed at advancing the transparency and accountability of public officials, contracting authorities, and economic operators.

Legal framework: public procurement in Kosovo is regulated by the Public Procurement Law (PPL), (Law, No. 04/l-042), which entered into force on October 5, 2011 and was amended twice in 2016 [11]. It is largely compliant with the EU Public Procurement Directives of 2004, but the provisions of the EU Public Sector Directive 2014/24 and the EU Utilities Sector Directive 2014/25 have not yet been transposed completely.

Institutional framework: the institutional structure is determined by Law No. 04/L-042, amended from time to time, and consists of the Public Procurement Regulatory Commission (PPRC), the Procurement Review Body (PRB), and the Central Procurement Agency (CPA).

Procurement Departments of Contracting Authorities: each contracting authority in Kosovo is obliged to establish the procurement department/division/unit within that authority. The procurement department/division/unit of a contracting authority under the Law on Public Procurement is completely independent in conducting procurement activities. In 2018, 165 contracting authorities, divided according to the following types, were subject to the provisions of the Law on Public Procurement [22]: 63 central-level institutions, 74 local-level institutions, 16 public enterprises owned by the government, 10 public enterprises owned by municipalities, and 2 social enterprises under the administration of the Kosovo Privatization Agency.

Electronic audit of the procurement system: genuine auditing plays a unique role in promoting accountability and making better use of public funds. This has made institutions more open, effective, and accountable. Reforms in public procurement and reporting systems, digitization of procurement processes, and the opening of procurement data have made it possible to have more information available, which has facilitated the work of public officials, civil society organizations, and active citizens and empowered them to hold the government accountable.

Today, all tenders are managed digitally through the electronic procurement platform, and, in the same way, the audit of this process is also carried out electronically. This enables a much higher degree of transparency and accountability in procurement processes, as well as shrinks the scope for human discretion, error, or abuse [23].

Electronic auditing of procurement systems has many benefits that work well together. For example, it saves time, cuts down on travel (which is important in emergencies like the COVID-19 pandemic), improves accuracy, and makes it possible to track audits in real time. It is important to teach public officials how to use the tools and systems that are put in place. With the help of USAID, the PPRC has created many ways for procurement and audit officials, the civil society, and other groups to get training. Until a few years ago, PPRC itself had started its path towards self-sustainability by replacing the classical classroom method with an e-learning experience for e-procurement training programs. PPRC developed four e-Learning materials for economic operators, as well as four more for contracting authorities instructing them to use the e-procurement platform. This journey culminates with the event in which the PPRC launches new e-Learning videos for public sector auditors [23].

This new form of training is designed to cover the auditors of public institutions, including those at the local and central levels, and these e-Learning materials will help users complete their tasks through an online experience that can be created at the convenience of the user, eliminating the need to hold refresher training for new entrants. The e-Learning materials are available on the e-Procurement platform and in the training section of the PPRC website. These developments and reforms have been achieved with the support of USAID through the activities of transparent, effective, and profitable municipalities. Anyway, the Government of Kosovo has already taken the leading position when it comes to the operation, maintenance, and improvement of the national procurement system, but also in national level auditing, as well as internal auditing, which proves the sustainability of the systems established [23].

The degree to which public procurement practitioners are trustworthy is reflected in their integrity, as bidders and other stakeholders require assurance that they can rely on any information distributed by the procurement entity, whether formally or informally [24]. But, in our opinion, changes and improvements to the procurement system should always be followed by a process of analysis so that actions can be prioritized and the best use can be made of people, money, and other resources in a planned and coordinated way.

2.3 The role of public procurement audit and the field of its application

Public auditing and control work done by the SAI often involves cases of public procurement and is affected by the complexity mentioned. Even though ISA for the International Standards of Supreme Audit Institutions (ISSAI) applies to different types of public financial operations, there is currently no INTOSAI standard for auditing public procurement. So, when auditing these cases, public sector auditors must rely on the ISSAI's very general requirements and their own, often different, internal experience [18].

The main objectives of the public procurement audit are to assess how efficiently and effectively, in accordance with the requirements of the law and the established ethical standards, the contracting authorities are implementing their public procurement function and then to provide all interested users with information and independent, objective, and reliable conclusions and opinions based on sufficient and appropriate evidence.

Public Procurement Audit Subjects: the audited subjects are state institutions and agencies, as well as other subjects as defined by national laws governing public procurement audit.

Fields of Public Procurement Audit: we suggest that the field of audit should be understood as an integration of audit subjects whose similar features allow the use of common methodological audit techniques and tools in the audit framework.

Public procurement audit objectives: in general, public sector auditing is described as a systematic process of objectively obtaining and evaluating evidence to determine whether information or actual conditions are consistent with established criteria. Information disclosure also brings higher value to companies [25]. The purpose of the public procurement audit will be to provide all interested parties with independent, objective, reliable information, conclusions, and opinions, based on sufficient and appropriate evidence, to answer the identified fundamental questions. Public sector audits also aim to increase accountability and transparency, to encourage improvement and confidence in the proper use of public funds, to strengthen the effectiveness of management and supervisory bodies, and to promote change. These general goals will influence the approach to be used.

Public sector audits can be categorized into one or more of three main types: financial statement audits, regulatory compliance audits, and performance audits. ISAs can do audits or other work on any relevant topic, such as reporting on the results and quantitative results of the entity's service delivery activities, sustainability reports, future resource needs, compliance with standards of internal control, real-time project audits, or other issues. ISAs may also conduct combined audits including financial, performance, and/or compliance aspects [19].

The audit can start when the procurement procedure is at a more or less advanced stage of preparation or after it has already been completed. The mandate of some ISAs includes auditing procedures at both stages. It goes without saying that the earlier the audit begins, the greater the potential impact. However, any risk of seeing the auditor as a participant in the process should be avoided. Audit of procurement procedures include both compliance audit and performance audit in most cases. The compliance criteria against which the process will be assessed are based on the applicable legal framework in the country's particular context. This context can vary significantly from country to country, and therefore the relevant context for the purpose of this summary is considered to be the EU procurement regime [19].

2.4 The operation of public enterprises in the Republic of Kosovo

Based on the statistics of the Unit for Policy and Monitoring of Public Enterprises, there are 17 central public enterprises and 43 local public enterprises in Kosovo. Local and central public enterprises are generally characterized by large technical and commercial losses as well as stagnation or small improvements. Public enterprises in Kosovo perform important services for citizens such as electricity production, water supply, waste collection, transport, etc. But many of these public enterprises are losing money, either technically or financially.

Public enterprises in Kosovo date back to the time of communism, and as part of that system, they were destined to meet most of the social and economic needs. In this regard, it should be noted that, due to the communist system's characteristics, all products and services had to be produced within the country and by public or social enterprise, excluding foreign trade. Starting from this, we have a wide range of products or services offered by public enterprises today without considering quantity, quality, market coverage, potential exports, or even the generation of innovative products or services, but only the importance and territorial extent of the products or services. Public enterprises are divided into [26]:

(1) Central Public Enterprises;

(2) Local Public Enterprises.

This study will analyze the role of auditing in improving quality in the public procurement process, namely in public enterprises in the Republic of Kosovo, using data from sources obtained from reports published by the NAO. The secondary data used, such as the auditor's report of the annual financial statements of the NAO and the annual reports of the annual financial statements of public enterprises.

3.1 The hypotheses that this paper tests

H1: The audit of the annual financial statements performed by the NAO has essential importance in the public procurement process.

H2: The audit of the annual financial statements performed by the NAO has an impact on the effectiveness and efficiency of the public procurement process.

H3: The audit results have shown that the existing controls in the field of public procurement are implemented with deficiencies in all phases.

H4: The number of recommendations related to public procurement in relation to the total number of recommendations has a linear relationship.

3.2 Data

In this research, we analyzed the annual reports of the NAO, namely the part related to public enterprises in Kosovo. In this research, five reports from 2016–2020 and 10 annual reports of public enterprises are included: annual reports of the financial statements of KRM Pastrimi Sh.a. 2018-2019; Annual reports of the financial statements of KMDK Sh.a. 2018-2019; Annual reports of the financial statements of KRU Prishtina Sh.a. 2018-2019; annual reports of the financial statements of Trainkos Sh.a. 2018-2019; and annual reports of the financial statements of Hidroregjioni Jugor Prizren Sh.a. 2018-2019. From these reports, I received an overview of the opinions given for annual reports of the financial statements, the number of recommendations given, and found recommendations related to procurement in public enterprises, as well as an overview of the recommendations of the NAO for the above-mentioned five public enterprises for the past five years, including how many of them have been implemented, how many are in the process of implementation, and how many have not been implemented.

The analysis of the research part was done by combining quantitative and qualitative methods. Quantitative research methods are used for mathematical data. This method was used in a smaller setting to provide some conditions related to the audit with public procurement issues, the results of which served to address the questions and validate the conclusions. Theoretical methods such as theories, hypotheses, various explanations, and concepts are developed using qualitative research methods and sources from literature research. The theoretical method has helped to build a framework based on existing, researched theories that will serve as a tool for improving the public procurement audit by adding value for money, which is related to effectiveness and efficiency. In the end, the method used presents an analysis of the audit of the public procurement system in Kosovo and identifies weaknesses in the implementation of the law.

4.1 The importance of the audit of the annual financial statements performed by the NAO in the public procurement process

The importance of auditing financial statements related to the public procurement process is directly related to the principles and standards of public procurement. From the analysis of the audit reports of the annual financial statements carried out by the NAO, the results have shown that we have five main categories related to public procurement issues for which the auditor has given recommendations.

These are:

Category 1. Weak management of contracts according to the Law on Public Procurement;

Category 2: Identification of needs by requesting units for procurement planning was not based on proper analysis;

Category 3: Division of tenders and non-application of the open procedure;

Category 4: Purchase of goods and services without procurement procedures;

Category 5: Delay in the execution of the contract.

From these results, we understand that categories such as: poor management of contracts, identification of needs by requesting units for procurement planning that was not based on proper analysis, the allocation of tenders and non-application of the open procedure, purchase of goods and services without following procurement procedures, and the delay in the realization of the contract are related to the principle of public procurement: value for money. Value for money represents one of the most important and complex principles in public procurement, since the value for money in public procurement has no measurement unit. Therefore, we can conclude that the audit of the annual financial statements carried out by the NAO is of fundamental importance in the public procurement process, and we prove that H1: The audit of the annual financial statements performed by the NAO has essential importance in the public procurement process. Accepted. Analyzing the audit results related to the auditor's findings in the field of public procurement. The procurement process at the public enterprise is carried out according to the rules and procedures defined in the Law on Public Procurement in Kosovo. The auditor's office has brought out some issues related to public procurement; however, the NAO emphasizes that the Public Enterprise should work further to advance the current system to ensure that public money is used economically, efficiently, and effectively. Based on the data analysis of the annual audit reports of enterprises for the years 2016–2020, from the audit results, we will prove that the existing controls in the field of public procurement are carried out with deficiencies in all stages of public procurement, and we will show the main issues related to public procurement each year. From these reports, we have defined five categories.

The results showed that the main categories are:

Category 1: Poor contract management;

Category 2: Identification of needs by requesting units for procurement planning was not based on proper analysis;

Category 3: Division of tenders and non-application of the open procedure;

Category 4: Purchase of goods and services without procurement procedures;

Category 5: Delay in the execution of the contract.

The results have shown that the findings identified in relation to public procurement refer to several categories of findings, which include all phases from procurement planning to poor contract management.

So based on these hypotheses, the results H3: The audit shows that the existing controls in the field of public procurement are implemented with deficiencies in all phases. Accepted.

From Figure 1, we can see that the number of findings in these five categories makes up about 10–15 percent of the total number of findings. This is because, in the NAO's annual reports, a large part of the rest of the percentage is made up of other irregularities.

Figure 1. Findings identified by the auditor related to public procurement

Sources: Authors

4.2 The impact of the audit of the annual financial statements carried out by the NAO on the effectiveness and efficiency of the public procurement process

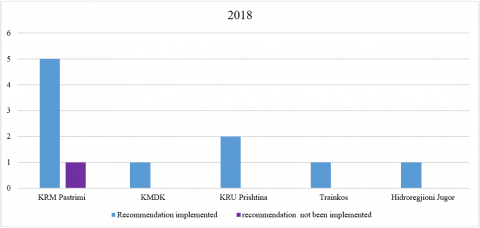

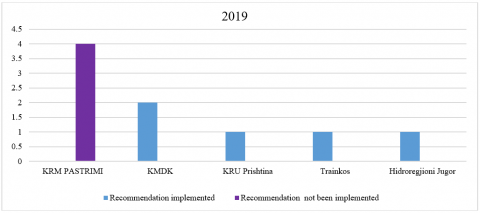

In order to develop this analysis and come to the results, we have selected five public enterprises for the case study: KRM Pastrimi Sh.a., KMDK Sh.a., Regional Water Company "Prishtina" Sh.a., Trainkos Sh.a., and KRU Hidroregjioni Jugor Prizren Sh.a. Their audit reports of the financial statements for two years (2018-2019) have been analyzed in relation to the recommendations for public procurement, whether the recommendations have been implemented, while the data were obtained from the reports in the following years. From this analysis, we derived the impact of the audit of the annual financial statements of public enterprises on the effectiveness and efficiency of the public procurement process. The recommendation has been implemented (during the 2019 audit, we did not encounter such cases) or recommendation has not been implemented (improvement measures have not been taken). Below, we have presented the implementation of the recommendations for the years 2018 and 2019 for the five cases that we have taken as a case study.

In Figure 2, we see that, for 2018, only one of the five public enterprises that we took as a case study had recommendations related to public procurement that had not been implemented. From this, we understand that a large percentage of the recommendations have been implemented, and we prove that the recommendations from the NAO in the annual financial statement reports have influenced the efficiency and effectiveness of public procurement.

In Figure 3 for 2019, we see that of the five public enterprises that we have taken as a case study, only one of them has recommendations related to public procurement that have not been implemented. From this, we understand that a large percentage of the recommendations have been implemented. And we confirm that the recommendations from the NAO in the reports of the annual financial statements have influenced the efficiency and effectiveness of public procurement. The results have shown that the findings of the general auditor have influenced an increase in the efficiency and effectiveness of procurement for the benefit of improved services and citizen funds.

So based on these hypothesis results, H2: The audit of the annual financial statements performed by the NAO has an impact on the effectiveness and efficiency of the public procurement process. Accepted.

Figure 2. Implementation of recommendations in 2018

Sources: Authors

Figure 3. Implementation of recommendations in 2019

Sources: Authors

4.3 The relationship between the number of recommendations related to public procurement in relation to the total number of recommendations

The results showed that in 2016, the total number of recommendations for four public enterprises was 21, while for public procurement there were only 3 recommendations. In 2017, the total number of recommendations for public enterprise was 83, while for public procurement there were only 6 recommendations. In 2018, there were 143 recommendations for eleven public enterprises, but only 9 for public procurement. In 2019, the total number of recommendations for eleven public enterprises was 265, while for public procurement, there were only 11. In 2020, the total number of recommendations for twelve public enterprises was 264, but for public procurement, there were only 10 recommendations.

Below we have presented the total number of recommendations related to public procurement in the audit reports of the financial statements issued for public enterprises by year, for the years 2016-2020.

Figure 4 shows the curve that refers to the total number of recommendations in audit reports of financial statements issued for public enterprises by year, for the years 2016–2020. Of course, the number of recommendations in audit reports of financial statements issued by the NAO is influenced by many factors, such as the type of audits performed that year, the size of entities covered by the NAO's annual program, etc. The opportunities for improving enterprise by implementing the recommendations are different [27].

The data show that there has been an increase in the number of recommendations from the auditor general issued annually from 2016 to 2020. It can be noted that in 2016, the smallest number of recommendations related to public procurement were issued, while in 2020, the highest number of audit reports were issued. But every year, the number of public enterprises that have been audited has also increased, which means that with the increase in audit subjects, the number of findings related to the public procurement process has also increased.

Figure 5 shows the curve for the total number of recommendations in audit reports of financial statements for public enterprises from 2016 to 2020 compared to the total number of recommendations related to public procurement.

Figure 4. The total number of recommendations related to public procurement from the NOA in the years 2016-2020

Sources: Authors

Figure 5. Linear relationship of total recommendations with recommendations related to public procurement in Pes

Sources: Authors

In Table 1, the results show that the correlation between the number of financial audit reports issued and the number of public procurement findings found is based on a five-year series: 2016, 2017, 2018, 2019 and 2020. Calculating the simple linear correlation, in which the number of audit reports issued is the variable X and the number of confirmed findings related to public procurement is the variable Y, we obtained the result that the coefficient of determination is R squared=0.90.

Table 2 shows a direct and positive correlation. The purpose of this test is to show whether the variation between the observed variables exists quantitatively and how intense it is. Both observed variables are treated as random. The research shows that there is a linear relationship between the number of issued financial statement audit reports and the number of identified public procurement findings. If we note the time series for these variables, this is a logical result, i.e., their positive correlation is the result of an increase or decrease in the number of audit reports, and financial statements will lead to an increase or decrease in the number of identified public procurement findings.

From these results, we prove that the hypothesis H4: The number of recommendations related to public procurement in relation to the total number of recommendations has a linear relationship. Accepted.

Table 1. Statistical regression

|

SUMMARY OUTPUT |

|

|

Regression Statistics |

|

|

Multiple R |

0.949308 |

|

R Square |

0.901186 |

|

Adjusted R Square |

0.868248 |

|

Standard Error |

1.187325 |

|

Observations |

5 |

|

ANOVA |

df |

SS |

MS |

F |

Significance F |

|

Regression |

1 |

38.57078 |

38.57078 |

27.36018 |

0.013596 |

|

Residual |

3 |

4.229223 |

1.409741 |

||

|

Total |

4 |

42.8 |

We used scientific and empirical data to look at the role of auditing in the public procurement process while writing this paper. In the Republic of Kosovo, auditing the public procurement process is a new field, but it is very important for managing public money because the public procurement process is where public money is filtered. The public's familiarity with how state bodies spend public funds distinguishes the audit of the public procurement process.

In this paper, we used literature about auditing, the public procurement process, and the connection between the audit and the public procurement process. The purpose of this paper was to explain the audit process in the public procurement process and its role in raising the quality of public procurement. The annual audit reports of the annual financial statements by the NOA for public enterprises in the Republic of Kosovo for the past five years (2016–2020) were analyzed, and in this way, the issues related to public procurement and the recommendations of the NOA for these issues were identified. Through various analyses, the essential importance of the audit in the public procurement process was elaborated, as were the main findings of the auditors in the public procurement process, the impact of the audit on the effectiveness and efficiency of the public procurement process, and the relationship between the findings in the public procurement process and the total findings of all issues.

From these analyses, we came to the conclusion that:

From these analyses, we came to the conclusion that the audit of the annual financial statements is of fundamental importance and affects the raising of the quality of public procurement, and all hypotheses were accepted.

Recommendations:

Based on the findings, the audit will focus on the following key points to improve the quality of public procurement:

Even though there was a lot of effort put into making this research happen, it did not happen without limitations. One of the limitations worth mentioning is data collection. We have not been able to provide data for public enterprises for the 10-year period (2010-2020), because in public enterprises, the recommendations related to public procurement started in 2016, so we only got 5 years.

[1] Report on public procurement activities in Kosovo. (2021). https://e-prokurimi.rks-gov.net/.

[2] The Constitution of Kosovo. (2008). https://gzk.rks-gov.net/ActDetail.aspx?ActID=3702.

[3] Law, No. 05/L-055. (2016). https://gzk.rks-gov.net/ActDetail.aspx?ActID=12517.

[4] Sundstrand, A. (2009). Public procurement - Procurment outside the EC-directives. Conference paper presented at the 4th Public Procurement.

[5] Dionysiev, I. (2020). The role of the state audit in the public procurement process - Case of the Republic of North Macedonia, University St. Cyril and Methodius in Skopje. http://hdl.handle.net/20.500.12188/14536.

[6] Fourie, D., Malan, C. (2020). Public procurement in the South African economy: Addressing the systemic issues. Sustainability, 12(20): 8692. https://doi.org/10.3390/su12208692

[7] Grandia, J. (2018). Public Procurement in Europe. The Palgrave handbook of public administration and management in Europe, pp. 363-380. https://doi.org/10.1057/978-1-137-55269-3_19

[8] Bartle, J.R., Korosec, R.L.C. (2003). A review of state procurement and contracting. Journal of Public Procurement, 3(2): 192-214. https://doi.org/10.1108/JOPP-03-02-2003-B003

[9] Ismajli, H., Perjuci, E., Prenaj, V. (2019). The importance of external audit in detecting abnormalities and fraud in the financial statements of public enterprises in Kosovo. Ekonomika, 98(1): 124-134. https://doi.org/10.15388/Ekon.2019.1.8

[10] Thai, K.V. (2001). Public procurement re-examined. Journal Public Procurement, 1(1): 9-50. https://doi.org/10.1108/JOPP-01-01-2001-B001

[11] Law, no. 05/L-092. (2016). https://gzk.rks-gov.net/ActDetail.aspx?ActID=11332.

[12] Public Procurement Audit Practical Guide. (2016). INTOSAI. https://www.intosaicommunity.net.

[13] Isroilov, B.I., Abduganiyev, U.K., Ibragimov, B.B. (2020). Financial control of public procurement to prevent corruption in the development of digital economy. In 2nd International Scientific and Practical Conference “Modern Management Trends and the Digital Economy: from Regional Development to Global Economic Growth”(MTDE 2020), pp. 546-552. https://doi.org/10.2991/aebmr.k.200502.089

[14] Drozd, I., Pysmenna, M., Pohribna, N., Zdyrko N., Kulish, A. (2021). Audit assessment of the effectiveness of public procurement procedures. Independent Journal of Management & Production, 12(3): 85-107. https://doi.org/10.14807/ijmp.v12i3.1522

[15] Knight, L., Harland, C., Telgen, J., Thai, K.V., Callender, G., McKen, K. (2007). Public Procurement. London: Routledge. https://doi.org/10.4324/NOE0415394048

[16] Jones, D.S. (2007). Public procurement in southeast Asia: Challenge and reform. Journal of Public Procurement, 7(1): 3-33. https://doi.org/10.1108/JOPP-07-01-2007-B001

[17] Filipova, L. (2015). Competence of the State Audit office of the Republic of Macedonia and review of the INTOSAI standards and reports of the State Audit. Journal of Process Management and New Technologies, 3(3): 61-68. https://scindeks-clanci.ceon.rs/data/pdf/2334-735X/2015/2334-735X1503061F.pdf.

[18] Stanoevski, S. (1998). Control and audit. Faculty of Economics, Skopje.

[19] INTOSAI. International Organization of Supreme Audit Institutions. (2023). https://www.intosai.org/.

[20] Stevkovski, D. (2011). State Audit Office as a controller of the spending budget funds. Master'sthesis, Skopje: St, Faculty of Law "Justinian I.

[21] Kakwezi, P., Nyeko, S. (2019). Procurement processes and performance: Efficiency and effectiveness of the procurement function. International Journal of Social Sciences Management and Entrepreneurship (IJSSME), 3(1): 172-182. http://www.sagepublishers.com/.

[22] Audit of Public Procurement. (2016). SIGMA https://www.sigmaweb.org/publications/Public-Procurement-Policy-Brief-28-200117.pdf.

[23] PPRC. Public Procurement Regulatory Commission. (2023). https://e-prokurimi.rks-gov.net/.

[24] Khan, N. (2018). Public Procurement Fundamentals. USA: Emerald Publishing Limited.

[25] Nguyen, V.T.H. (2022). Factors affecting information disclosure: Evidence from vietnamese listed companies. International Journal of Sustainable Development and Planning. 17(5): 1653-1658. https://doi.org/10.18280/ijsdp.170531

[26] Law, no. 03/L-087. (2008). https://gzk.rks-gov.net/ActDetail.aspx?ActID=2547.

[27] Turkalj, Ž., Mahaček, D. (2015). Procedurement procedures in the function of improving company business conduct. In 15th international scientific conference Business Logistics in Modern Management, pp. 67-78.