Monu Bhargava* | Ashish Sharma | Birajit Mohanty | Moon Moon Lahiri

© 2022 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Advancements in financial system and technology, enlarged individual responsibility for financial decisions, and rapid information expansion, have fundamentally transformed women's need to be functionally literate and financially capable, especially after the COVID-19 pandemic. The personality also has long term implications on financial well-being. The aim of the paper is to study the dominating role of financial attitude, financial awareness & skills, and financial behaviour on financial competence and the moderating role of personality on financial knowledge, financial behaviour, financial attitude, and financial capability. Multi stage stratified random sampling has been used to collect data from 530 urban working women in both the Public and Private sectors, self-employed professionals, and entrepreneurs. Smart-PLS is used by applying Structure Equation Modelling (SEM) to study the moderating role of personality on financial attitude, behaviour, knowledge, and capability. Further the Chi-square test and Tukey test and Kruskal Wallis Test are used to test the hypothesis. The study found that Financial Knowledge of working women with gold personalities influences their financial capability (Beta, 0.578) the most, While, Financial Behaviour is the primary influencer having green (Beta, 0.396) & blue (Beta, 0.638) personalities. Working women having Green Personality are found to be superior with respect to Financial Behaviour, Financial Capability and Financial Knowledge. It is also observed that working women having blue personality characteristics, have comparatively better financial attitude.

personality, financial capability, financial behaviour, financial attitude, financial knowledge & skills

The COVID-19 epidemic has altered the global landscape, wreaking havoc on human and economic conditions that strengthened the need of becoming financially knowledgeable, stable and competent [1]. Financial capability is a decisive step toward financial stability. A financially capable person employs money management tactics and savings strategies on a regular basis to avoid budgetary constraints or financial problems and attain higher financial stability [2]. To make effective financial decisions and attain financial capacity, a blend of awareness, knowledge, skill, attitude, and conduct is required [3]. Financial capability is also affected by individual’s experience, condition and the personality [4]. The personality has strong relationship with financial decision making [5]. Greater level of financial capable behaviour is not just because of high level of financial knowledge or high degree of attitude, but also significantly associated with personality, which includes positive and impulsive behaviour to face challenges and to take accurate financial decisions [6]. The personality has long-term implications on financial well-being.

Women make up 41% of the global workforce. Even after playing the significant role in the society and performing dual responsibilities as home-maker and working women, a global gender wage gap is of 23% [7]. Women are underrepresented in the majority of economic activity. They are still reliant on their male counterpart or the father. Women have lower level of financial literacy and financial capability than do men have in most countries or cultural differences [8]. By increasing their financial engagement could result in annual economic gains of trillions of dollars.

In this research paper, the aim is to compare the level of financial knowledge, financial attitude, financial behaviour and financial capability among working women belonging to different personality category and the moderating role of personality is also examined on financial knowledge, attitude, behaviour and financial capability.

2.1 Financial capability

Financial capability is defined as, “the ability to apply financial information and abilities to achieve financial well-being while maintaining a positive attitude. Financial capability is divided into four components: money management, staying informed, selection of the product and future planning” [9]. Financial capability can be revealed by a specific degree of financial knowledge and skills and execution of advantageous financial behaviour. Therefore, it can be said that financial knowledge & skills, financial attitude and financial behaviour are firmly connected with financial capacity to attain financial strength [10]. Financial capability need not only financial knowledge but also financial attitude and financial behaviour [11].

2.2 Financial knowledge & skills

Financial knowledge is an analytical comprehension of financial concepts, products and services that is essential to apply the information in day- to-day life to become financially capable [12]. It refers to the process through which people improve their financial abilities and confidence by becoming more aware of financial hazards and possibilities, making informed decisions, knowing where to get assistance, and taking effectual steps to boost their financial competence [13].

H1: Financial Knowledge affects Financial Capability.

2.3 Financial behaviour

Financial behaviour is the positive behaviour that enhances the financial capability of the individual [14]. It comprises of planning for expenditures, quick payment of bills, making of budgets, regular savings [15].

H2: Financial Behaviour affects Financial Capability.

2.4 Financial attitude

Financial attitude can be characterized as the inclination of the person in relation to financial matters. It is the skill to make plans for future and track financial transactions. It is the result of financial behaviour of a person to take financial decision and deep-rooted through his economic and non-economic beliefs [16]. Without strong financial attitudes, gaining financial profit for the future would be difficult, as these two characteristics are linked to achieving short and long-term life goals [17]. Routine actions can shape financial attitudes.

H3: Financial Attitude affects Financial Capability.

2.5 Personality

Financially capable behaviour is not only about the financial knowledge and attitude one has attained but also strongly influenced by personality of the person [6]. Personality traits are a blend of emotive, cognitive and motivational characteristics that influence the individuals’ response to the environment, and the decision making under certain circumstances [18]. The person can be categorized as either 'logical' or 'emotional.' Emotional investors make investment decisions based on their emotional motivation, whereas rational investors make judgments based on the data they have [19]. In this research paper, true color personality test is used to study the role of personality of financial capability. The test categorizes women into one of four personality types: blue, green, orange, or gold [20, 21]. Green personality women have a stronger desire to learn new things from existing material, and they are more likely to have an analytical mind and good research skills. They make decisions based on data and statistics, and they work hard to encourage intelligent considerations. Women of this category have a conscientious personality [22]. 'Conscientiousness' refers to an individual's cognitive and analytical abilities when making decisions [19]. Blue Colored personality women are more sensitive, unselfish, compassionate, and make decisions based on emotions. These women have a Neuroticism personality type [23]. 'Neuroticism' refers to a person's emotional stability when making an investing decision [19]. Gold personalities are dependable, decisive, organized, and have a strong sense of safety and security. These women have Agreeable personality [24]. The attribute of 'Agreeability' describes how people react to new information. Orange personality women with orange personalities are risk-takers, fun-lovers, carefree, and brave. Individuals with orange personalities are known for their business acumen. These women are of Extroversion personality type [25]. Individuals' behaviour toward others is referred to as 'extraversion.' Extroverts are assertive and prefer to move around with others. High levels of financial capability indicate greater level of control over finances and ability to use the knowledge, plan and act on them, which can lead to better mental well-being [25].

In this study, the researchers have attempted to

4.1 Variables studied

|

Financial Literacy |

|

|

Financial Knowledge [26-30] |

|

|

Financial Behaviour [31-33] |

|

|

Financial Attitude [34, 35] |

|

|

Financial Capability |

|

|

Managing Money [36-39] |

Making End Meets

Budget to cover heavy expenditures |

|

Planning Ahead [40, 41] |

|

|

Choose Products [42, 43] |

|

|

Staying Informed [44, 45] |

|

4.2 Sample

This particular research work is solely based on primary data. Multi stage stratified random sampling has been used to collect data from urban working women in both the Public and Private sectors, self-employed professionals, and entrepreneurs. 600 urban working women from Jaipur were approached with a standard questionnaire. 535 filled questionnaires were returned in which 530 were properly filled. Thus, the sample size of this study is 530. Thus, response rate was 88.33% approximately.

4.3 Measures

Partial Least Square (PLS) analysis is used as an analytical tool in this study. PLS is a powerful analytical tool since it does not require many assumptions and can explain the relationship between latent variables [46].

4.4 Theoretical framework

The theoretical framework (Figure 1) shows the way through which the study is being organized to achieve the research objectives. It explains the relationship between financial behaviour, financial knowledge& skills, financial attitude and financial capability along with the moderating role of personality.

Figure 1. Author’s compilation

The measurement model and the structural model are both evaluated using PLS-SEM. Convergent validity, discriminant validity, and construct reliability are used to evaluate the measurement models [47].

5.1 Assessment of measurement model

Measurement models are used in assessing validity & reliability of constructs [48]. Latent variable’s internal consistency is usually examined by using “Cronbach's Alpha” and “Composite Reliability” [47]. 0.7 or higher Cronbach alpha values signify acceptable internal consistency.

Table 1. Validity and reliability of constructs

|

Cronbach's Alpha |

rho_A |

CR |

AVE |

|

|

Financial Knowledge |

0.952 |

0.956 |

0.958 |

0.657 |

|

Financial Behaviour |

0.957 |

0.957 |

0.965 |

0.822 |

|

Financial Attitude |

0.755 |

0.807 |

0.842 |

0.578 |

|

Financial Capability |

0.973 |

0.974 |

0.975 |

0.651 |

The Table 1 shows that the The value of Cronbach's Alpha for each construct is observed greater than 0.7; therefore, these constructs meet the criterion of internal consistency. Apart from it, obtained values of rho_A and Composite Reliability for each latent variable is more than 0.7 and respectively values of AVE are more than 0.5 which fulfills criterion of convergent validity [49].

Table 2. Fornell-larcker criterion

|

Financial Attitude |

Financial Behaviour |

Financial Capability |

Financial Knowledge |

|

|

Financial Attitude |

0.677 |

|||

|

Financial Behaviour |

0.677 |

0.907 |

||

|

Financial Capability |

0.733 |

0.851 |

0.779 |

|

|

Financial Knowledge |

0.637 |

0.886 |

0.833 |

0.811 |

Table 3. Heterotrait - monotrait ratio (HTMT)

|

Original Sample (O) |

Sample Mean (M) |

2.5% |

97.5% |

|

|

Financial Knowledge -> Financial Behaviour |

0.921 |

0.921 |

0.896 |

0.943 |

|

Financial Knowledge -> Financial Attitude |

0.810 |

0.810 |

0.739 |

0.873 |

|

Financial Knowledge -> Financial Capability |

0.858 |

0.858 |

0.823 |

0.890 |

|

Financial Behaviour -> Financial Attitude |

0.851 |

0.852 |

0.783 |

0.909 |

|

Financial Capability -> Financial Behaviour |

0.877 |

0.877 |

0.840 |

0.910 |

|

Financial Capability -> Financial Attitude |

0.875 |

0.875 |

0.800 |

0.938 |

Table 4. One-sample Kolmogorov-Smirnov test

|

Financial Knowledge |

Financial Behaviour |

Financial Attitude |

Financial Capability |

||

|

N |

530 |

530 |

530 |

530 |

|

|

Normal Parameters a,b |

Mean |

530 |

-.0001 |

.0001 |

.0000 |

|

Std. Dev. |

.0000 |

1.00091 |

1.00084 |

1.00090 |

|

|

Most Extreme Differences |

Absolute |

1.00091 |

.139 |

.172 |

.128 |

|

+ive |

.105 |

.139 |

.133 |

.120 |

|

|

-tive |

.105 |

-.126 |

-.172 |

-.128 |

|

|

Kolmogorov-Smirnov Z |

2.407 |

3.198 |

3.966 |

2.954 |

|

|

|

|

|

|

|

|

|

Asymp. Sig. (2-tailed) |

.000 |

0.000 |

0.000 |

.000 |

|

|

a. Test distribution is Normal. |

|||||

|

b. Calculated from data. |

|||||

Through employing both “Fornell-Larcker Criterion” & “Heterotrait-Monotrait Ratio (HTMT)”, discriminant validity is assessed for constructs. As per Fornell-Larcker criterion the sq. root of AVE for every construct (displayed in Table 2) are greater than that construct’s correlation with the other ones [50], therefore fullfills the discriminate validity criteria. On the other side, HTMT is used to check external consistency of constructs [51] which is helpful in overcoming inadequacy in cross loadings & Fornell-Larcker Criterion [52] The permissible value for HTMT is anything less than 1 [51]. Since, all values (shown in Table 3) are found less than threshold value, all constructs are valid enough to meet criteria of suitability.

5.2 Test of normality of data

Data normality is a mandatory requirement that must be fulfilled in every parametric test. The normality test can be done using various methods, one of them using the Kolmogorov-Smirnov method. A data can be said to be normal if it has a significance value of more than 0.05 (sig.> 0.05). Conversely the data is said to be abnormal if it has a significance value of less than 0.05 (sig. <0.05). Normality test was done for all selected models before framing hypothesis testing. The results of the normality test with Kolmogorov-Smirnov can be seen in the Table 4.

Normality test results obtained from above Table 4 can be seen that all variable data have a significance value of less than 0.05 so that the whole can be concluded that the data distribution is not normal. Testing the hypothesis can be done using the non-parametric test.

5.3 Status of financial attitude, behaviour, knowledge and capability in working women with different personalities

William Cooper and Lowry [53] developed a personality profiling technique and he classified personality of person into four categories (i.e., orange, gold, green and blue). Different colored personality consists of significant number of characters [53]. Kruskal-Wallis test was applied to understand the significance of difference in Financial Attitude, Behaviour, Knowledge and Capability in working women with different personalities.

Table 5. Results of Kruskal Wallis test

|

Ranks |

|||

|

Personality Type |

N |

Mean Rank |

|

|

Financial Knowledge |

Orange |

199 |

240.89 |

|

Green |

68 |

303.46 |

|

|

Blue |

122 |

291.20 |

|

|

Gold |

141 |

259.69 |

|

|

Total |

530 |

|

|

|

Financial Behaviour |

Orange |

199 |

237.95 |

|

Green |

68 |

297.06 |

|

|

Blue |

122 |

288.54 |

|

|

Gold |

141 |

269.23 |

|

|

Total |

530 |

|

|

|

Financial Attitude |

Orange |

199 |

231.28 |

|

Green |

68 |

294.76 |

|

|

Blue |

122 |

307.48 |

|

|

Gold |

141 |

263.36 |

|

|

Total |

530 |

|

|

|

Financial Capability |

Orange |

199 |

231.36 |

|

Green |

68 |

306.56 |

|

|

Blue |

122 |

297.93 |

|

|

Gold |

141 |

265.82 |

|

|

Total |

530 |

||

Table 6. Chi-Square test

|

Test Statistics |

|||

|

Financial Knowledge |

Financial Behaviour |

Financial Attitude |

|

|

Chi-Square |

12.968 |

12.429 |

22.269 |

|

df |

3 |

3 |

3 |

|

Asymp. Sig. |

.005 |

.006 |

.000 |

|

a. Kruskal Wallis Test b. Grouping Variable: personality Type |

|||

As per the results of Kruskal Walis test, it is found that the mean scores of Financial Behaviour, Financial Capability and Financial Knowledge for the green personality women are the highest, that shows that the working women having Green Personality are found superior. While, working women having blue personality characteristics, have comparatively better financial attitude (Table 5).

As per Table 6 it is revealed that at 5% significance level Financial Attitude, Financial Behaviour, Financial Capability and Financial Knowledge of working women having different personalities differ significantly.

5.4 Interaction between FK, FB, FA, FC with personalities

In order to achieve final outcomes of hypothesis testing of structural equation model is required subsequently the assessment of PLS algorithm. In order to validate connection amongst constructs path coefficient are often used. Simply Partial Least Square (PLS) is a regression model in a form of path model that is capable of managing number of dependent variables with one/more dependent variables [54].

Model fit:

Table 7. Fitness test of proposed model

|

Saturated Model |

|

|

SRMR |

0.072 |

|

Chi-Square |

9551.540 |

|

NFI |

0.884 |

The Chi-square (9551.540) is found significant at 5% level of significance (p value, 0.00), according to the data displayed in Table 6. The proposed research model's approximation model fit is measured using SRMR (standardized root mean square residual). A model is considered to have an adequate fitness of model whenever “SRMR” is < 0.08 [54]. Value of SRMR =0.072< 0.08 (shown in Table 7). Therefore, the proposed model is suitable for analysis of data.

Impact of Financial Knowledge (p value, 0.00), Financial Behaviour (p value, 0.00) and Financial Attitude (p value, 0.00) upon Financial Capability is found significant since the p value are found less than significant level at 5% level of confidence and t statistics value for these three constructs (Financial Knowledge, Financial Behaviour and Financial Attitude) is found greater than 1.96 [55] (shown in Table 8).

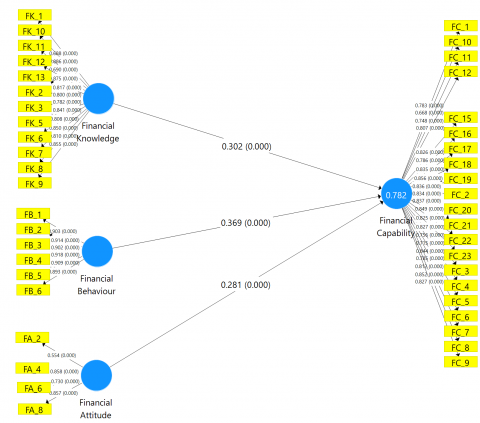

Thus, Financial Knowledge, Financial Behaviour and Financial Attitude of a working woman altogether has significant impact of 78.2% (shown in Figure 2) on their Financial Capabilities.

5.5 Influence of ‘FK’, ‘FB’, and ‘FA’ on the ‘FC’ of female employees with divergent personalities

Since the pervious results through SEM modelling have proven that Financial Attitude, Financial Behaviour, Financial Capability and Financial Knowledge altogether impact Financial Capability of working women having different personalities. Furthermore, to establish this framework for working women with different personalities, multiple regression method was employed.

Figure 2. Measurement model

Table 8. Result of hypothesis

|

Hypothesis |

Path Coefficient |

P Values |

Hypothesis Result |

|

|

H1 |

Financial Knowledge -> Financial Capability |

0.302 |

0.000 |

H1 Accepted |

|

H2 |

Financial Behaviour -> Financial Capability |

0.369 |

0.000 |

H2 Accepted |

|

H3 |

Financial Attitude -> Financial Capability |

0.281 |

0.000 |

H3 Accepted |

Table 9. Results of regression analysis

|

Model Summary b |

|||||||||||

|

Personality Type |

R |

R2 |

Adj. R2 |

Standard Error of estimate |

Change Statistics |

Durbin-Watson |

|||||

|

R2 Change |

F Change |

df1 |

df2 |

Sig. F Change |

|||||||

|

Orange |

1 |

.949a |

.901 |

.900 |

.37004 |

.901 |

594.490 |

3 |

195 |

.000 |

2.025 |

|

Green |

1 |

.780a |

.608 |

.590 |

.59889 |

.608 |

33.078 |

3 |

64 |

.000 |

1.523 |

|

Blue |

1 |

.866a |

.751 |

.744 |

.47866 |

.751 |

118.360 |

3 |

118 |

.000 |

1.881 |

|

Gold |

1 |

.789a |

.622 |

.614 |

.45363 |

.622 |

75.200 |

3 |

137 |

.000 |

1.500 |

|

a. Predictors: (Constant), Financial Knowledge, Financial Attitude, Financial Behaviour |

|||||||||||

|

b. Dependent Variable: Financial Capability |

|||||||||||

Table 10. ANOVA

|

ANOVAa |

|||||||

|

Personality Type |

Sum of Squares |

df |

Mean Square |

F |

Sig. |

||

|

Orange |

1 |

Regression |

244.205 |

3 |

81.402 |

594.490 |

.000b |

|

Residual |

26.701 |

195 |

.137 |

||||

|

Total |

270.906 |

198 |

|||||

|

Green |

1 |

Regression |

35.592 |

3 |

11.864 |

33.078 |

.000b |

|

Residual |

22.955 |

64 |

.359 |

||||

|

Total |

58.546 |

67 |

|||||

|

Blue |

1 |

Regression |

81.356 |

3 |

27.119 |

118.360 |

.000b |

|

Residual |

27.036 |

118 |

.229 |

||||

|

Total |

108.392 |

121 |

|||||

|

Gold |

1 |

Regression |

46.425 |

3 |

15.475 |

75.200 |

.000b |

|

Residual |

28.192 |

137 |

.206 |

||||

|

Total |

74.617 |

140 |

|||||

|

a. Dependent Variable: Financial Capability |

|||||||

|

b. Predictors: (Constant), Financial Knowledge, Financial Attitude, Financial Behaviour |

|||||||

Table 11. Personality-wise regression analysis

|

personality Type |

Unstandardized Coefficients |

Standardized Coefficients |

t |

Sig. |

Correlations |

Collinearity Statistics |

||||||

|

B |

Std. Error |

Beta |

Zero-order |

Partial |

Part |

Tolerance |

VIF |

|||||

|

Orange |

1 |

(Constant) |

-.023 |

.027 |

-.876 |

.382 |

||||||

|

Financial Knowledge |

.305 |

.062 |

.291 |

4.953 |

.000 |

.901 |

.334 |

.111 |

.146 |

6.837 |

||

|

Financial Behaviour |

.275 |

.076 |

.256 |

3.634 |

.000 |

.920 |

.252 |

.082 |

.102 |

9.808 |

||

|

Financial Attitude |

.434 |

.050 |

.440 |

8.590 |

.000 |

.917 |

.524 |

.193 |

.192 |

5.200 |

||

|

Green |

1 |

(Constant) |

.100 |

.075 |

1.334 |

.187 |

||||||

|

Financial Knowledge |

.161 |

.150 |

.170 |

1.074 |

.287 |

.695 |

.133 |

.084 |

.245 |

4.075 |

||

|

Financial Behaviour |

.363 |

.155 |

.396 |

2.342 |

.022 |

.742 |

.281 |

.183 |

.215 |

4.662 |

||

|

Financial Attitude |

.290 |

.106 |

.294 |

2.748 |

.008 |

.667 |

.325 |

.215 |

.536 |

1.866 |

||

|

Blue |

1 |

(Constant) |

.019 |

.045 |

.413 |

.681 |

||||||

|

Financial Knowledge |

.152 |

.087 |

.153 |

1.749 |

.083 |

.774 |

.159 |

.080 |

.276 |

3.622 |

||

|

Financial Behaviour |

.610 |

.085 |

.638 |

7.198 |

.000 |

.851 |

.552 |

.331 |

.269 |

3.720 |

||

|

Financial Attitude |

.164 |

.059 |

.153 |

2.776 |

.006 |

.579 |

.248 |

.128 |

.692 |

1.446 |

||

|

Gold |

1 |

(Constant) |

.032 |

.038 |

.835 |

.405 |

||||||

|

Financial Knowledge |

.514 |

.088 |

.578 |

5.811 |

.000 |

.774 |

.445 |

.305 |

.279 |

3.584 |

||

|

Financial Behaviour |

.112 |

.090 |

.127 |

1.238 |

.218 |

.708 |

.105 |

.065 |

.264 |

3.789 |

||

|

Financial Attitude |

.144 |

.068 |

.148 |

2.137 |

.034 |

.579 |

.180 |

.112 |

.579 |

1.727 |

||

|

a. Dependent Variable: Financial Capability |

||||||||||||

In Table 10, at 5% level of significance; Financial Attitude, Financial Behaviour, Financial Capability and Financial Knowledge have significant impact on Financial Capability of working women having different personalities.

Mostly Financial Attitude, Financial Behaviour, Financial Capability and Financial Knowledge of working women with orange personality have 90.1% impact on their financial capability (Table 9). Financial Knowledge of working women with gold personality influences their financial capability (Beta, 0.578) most. While, Financial Behaviour is the major influencer of financial capability of working women with green (Beta, 0.396) & blue (Beta, 0.638) personalities. Financial Attitude of working women with orange personality influences their financial capability (Beta, 0.44) most (Table 11).

Financial Attitude, Financial Behaviour & Financial Knowledge have a positive effect on Financial Capability of working women. Higher the Financial Attitude, Financial Behaviour & Financial Knowledge, the higher Financial Capability of working women will be. The appropriate attitude, behaviour and knowledge about monetary management influences how a working woman manages her finances and enhances financial capability. This study backs up earlier studies [35, 56, 57]. From daily and regular expenses to long-term budget projections, financial knowledge is vital for working women to manage both domestic & professional life. Sound financial knowledge laid a profound impact and improves the skills to stipulate security & prosperity in the life. Financial knowledge refers to an individual's basic understanding of financial concepts, which allows them to better manage their financial challenges and safeguard their financial strength and progress [58, 59].

Financial behaviour is a critical factor in determining financial capability [60, 61]. Higher financial capability is associated to more favorable and risk-less financial behaviour. Higher level of knowledge leads to better financial behaviour, which in turn leads to greater financial competence and regulation. With superior capability, an individual can upgrade financial plans, financial obligations, and cash flows [16]. It is discussed that Financial attitude expresses implicit beliefs, which can influence behavioural intentions. While, it is discussed in the context of finance, attitude is defined as an opinion and an approach about how an individual manages his financial affairs and makes sound and improved financial decisions [62]. Attitude refers to one's confidence in making sound financial decisions, and it influences one's financial capability [63]. It is also proved that improved attitudes boost financial capability [64]. A working woman is financially capable if she can make value-added financial decision. It was discovered that improving working women's financial knowledge, financial behaviour, and financial attitude can improve their financial capability.

Since the findings suggested that financial knowledge, behaviour, attitude and capability are significantly different for working women with different personalities. Furthermore, it was also discovered that the out-tern of financial knowledge, behaviour and, attitudinal-perspective on the financial capability significantly vary for working women of divergent personalities (gold, orange, green and blue). Therefore, it can be concluded that personality of working women has mediating role on their financial capability. Working women having different personalities would have different spending/ savings habits, their attitude towards financial decisions might not be that much similar and all might not have same level of knowledge to take financial decisions. Thus, for working women having traits of different personalities would not be similarly financially capable. In generally persons with green personality have more affinity to discover new insights from available information, they mostly have analytical mind and good research skills. They take decisions based on facts & figures and they majorly strive to foster thoughtful considerations [22]. Persons who come under blue color personality category, are more emotional, noble, and sympathetic and mostly take emotion driven decisions [65]. Apart from it, Financial Attitude was found most appropriate for working women having gold personality and blue personality. Individuals with traits blue personality, are more concerned and patient in nature. While, persons with traits green personality are more practical thinker which appears prominently on their behaviour [53]. Individuals with orange personalities are renowned as risk-takers and have good entrepreneurial skills [24].

The impetus of this research is to investigate the effect of ‘financial knowledge’, ‘financial behaviour’ and, ‘financial attitude’ upon ‘financial capability’ and the moderating role of personality on working women. Three important findings from this study are highlighted based on the conceptual framework that includes financial knowledge, behaviour attitude capability and personality traits. Firstly, Financial Attitude, Financial Behaviour, and Financial Knowledge have a favorable impact on working women's financial capability. Secondly, financial behaviour is a critical aspect that forms financial competence, and third, the impact of financial knowledge, conduct, and attitude on financial capability differs considerably across working women with varied personalities. (gold, orange, green and blue). As a result, it may be concluded that working women's personalities play a moderating role in their financial potential. The study is limited to a group of urban working women in the state of Rajasthan only. The moderating role of digital financial awareness can be analyzed on financial knowledge, financial attitude, financial behaviour and financial capability.

[1] Strategies, A.N. (2021). Advancing national strategies for financial education. Economic Survey, RBI. https://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/NSFE202020251BD2A32E39F74D328239740D4C93980D.

[2] Shephard, D.D., Bailey, S. The psychological dimensions of financial capability discussion paper beyond financial literacy: The psychological dimensions of financial capability. https://think.ing.com/uploads/reports/Beyond-financial-literacy_The-psychological-dimensions-of-financial-capability_Summary-paper.pdf, accessed on May 16, 2022.

[3] Agarwalla, S.K., Barua, S.K., Jaco, J., Varma, J.R. (2015). Financial Literacy among Working Young in Urban India. World Development, 67: 101-109. https://doi.org/10.1016/j.worlddev.2014.10.004

[4] Authority, F.S. (2005). Measuring financial capability: An exploratory study. Prepared for the Financial Services Authority by Personal Finance Research Centre, University of Bristol.

[5] Németh E., Zsoter, B. (2017). Personality, attitude and behavioural components of financial literacy: A comparative analysis. Journal of Economics and Behavioral Studies, 9(2): 46-57. https://doi.org/10.22610/jebs.v9i2.1649

[6] Shephard, D.D., Bailey, S. (2017). The psychological dimensions of financial capability’ discussion paper beyond financial literacy: The psychological dimensions of financial capability.

[7] World employment social outlook, 2018. https://www.ilo.org/wcmsp5/groups/public/---dgreports/---dcomm/---publ/documents/publication/wcms_615594.pdf, accessed on May 16, 2022.

[8] Cabeza-García, L., Del Brio, E.B., Oscanoa-Victorio, M.L. (2019). Female financial inclusion and its impacts on inclusive economic development. Women's Studies International Forum, 77: 102300. https://doi.org/10.1016/j.wsif.2019.102300

[9] Cabeza-García, L., Del Brio, E.B., Oscanoa-Victorio, M.L. (2019). Female financial inclusion and its impacts on inclusive economic development. Women's Studies International Forum, 77: 102300. https://doi.org/10.1016/j.wsif.2019.102300

[10] Brown, E. (2015). OECD working papers on finance, insurance and private pensions No. 14 empowering women through financial awareness and education Angela Hung, Joanne Yoong. https://www.researchgate.net/publication/254439241_Empowering_Women_Through_Financial_Awareness_and_Education.

[11] Teravainen-Goff, A. (2019). Literacy and financial capability an evidence review. National Literacy Trust Research Report (1116260).

[12] Xiao, J.J., O’Neill, B. (2016). Consumer financial education and financial capability. International Journal of Consumer Studies, 40(6): 712-721. https://doi.org/10.1111/ijcs.12285

[13] Hinz, R. et al. (2013). Financial capability in low-and middle-income countries: measurement and evaluation a report on the world bank’s research program and the knowledge from the Russia Financial Literacy and Education Trust Fund. https://www.researchgate.net/publication/332070873_Financial_capability_in_low-and_middle-income_countries_measurement_and_evaluation_A_REPORT_ON_THE_WORLD_BANK'S_RESEARCH_PROGRAM_AND_THE_KNOWLEDGE_FROM_THE_RUSSIA_FINANCIAL_LITERACY_AND_EDUCATION_TRUS.

[14] Hung, A., Yoong, J., Brown, E. (2012). Empowering women through financial awareness and education. OECD Working Papers on Finance, Insurance and Private Pensions. http://www.finlitedu.org/team-downloads/evaluation/hung-yoong-brown-2012pdf.pdf.

[15] Bhushan, P., Medury, Y. (2014). An empirical analysis of inter linkages between financial attitudes, financial behaviour and financial knowledge of salaried individuals. Indian Journal of Commerce & Management Studies, 5(3): 1161-1201. www.scholarshub.net.

[16] Banerjee, A.N., Hasan, I., Kumar, K., Philip, D. (2021). The power of a financially literate woman in intra-household financial decision-making. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3246314%0Ahttps://www.researchgate.net/profile/Dennis-Philip-2/publication/345808151_The_Power_of_a_Financially_Literate_Woman/links/5fdb653d92851c13fe92f219/The-Power-of-a-Financially-Literate-Woman.pdf.

[17] Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2): 179-211. https://doi.org/10.1016/0749-5978(91)90020-T

[18] Yap, R.J.C., Komalasari, F., Hadiansah, I. (2018). The effect of financial literacy and attitude on financial management behavior and satisfaction. Bisnis & Birokrasi Journal, 23(3): 3-5. https://doi.org/10.20476/jbb.v23i3.9175

[19] Fan, L., Chatterjee, S., Kim, J. (2021). An integrated framework of young adults’ subjective well-being: The roles of personality traits, financial responsibility, perceived financial capability, and race. Journal of Family and Economic Issues, 43: 66-85. https://doi.org/10.1007/s10834-021-09764-6

[20] Cooper, W.H., Withey, M.J. (2009). The strong situation hypothesis. Personality and Social Psychology Review, 13(1): 62-72. https://doi.org/10.1177/1088868308329378

[21] Weber, M.R., Dennison, D. (2014). An exploratory study into the relationship between personality and student leadership. Journal of Hospitality & Tourism Education, 26(2): 55-64. https://doi.org/10.1080/10963758.2014.900374

[22] Pinjisakikool, T. (2017). The effect of personality traits on households’ financial literacy. Citizenship, Social and Economics Education, 16(1): 39-51. https://doi.org/10.1177/2047173417690005

[23] Ferwerda, B., Schedl, M., Tkalcic, M. (2015). Predicting personality traits with instagram pictures. ACM International Conference Proceeding Series, 2015-Septe, 7-10. https://doi.org/10.1145/2809643.2809644

[24] Taylor, M.P., Jenkins, S.P., Sacker, A. (2011). Financial capability and psychological health. Journal of Economic Psychology, 32(5): 710-723. https://doi.org/10.1016/j.joep.2011.05.006

[25] OCDE and INFE. (2015). Core competencies framework on financial literacy for youth. 1-36. https://www.oecd.org/finance/Core-Competencies-Framework-Youth.pdf, accessed on May 16, 2022.

[26] Organisation for Economic and Cooperation and Development. (2011). Measuring financial literacy: Questionnaire and guidance notes for conducting an internationally comparable survey of financial literacy. Oecd, p. 31. https://www.oecd.org/finance/financial-education/49319977.pdf.

[27] Gera Prerna, A.N., Pamarthy, H. (2012). Financial Literacy as a tool for financial inclusion and client protection. United Nations Development Programme, p. 283.

[28] OECD. (2020). OECD/INFE 2020 international survey of adult financial literacy, 78. https://www.oecd.org/financial/education/oecd-infe-2020-international-survey-of-adult-financial-literacy.pdf, accessed on May 16, 2022.

[29] NISM. (2014). Financial Literacy and Inclusion in India: Final Report - India’, p. 48. https://ncfe.org.in/reports/nflis, accessed on May 16, 2022.

[30] OECD. (2020). Financial literacy of adults in south east Europe. https://www.oecd.org/finance/Financial-Literacy-of-Adults-in-South-East-Europe.pdf, accessed on May 16, 2022.

[31] Grohmann, A. (2018). Financial literacy and financial behavior: Evidence from the emerging Asian middle class. Pacific-Basin Finance Journal, 48: 129-143. https://doi.org/10.1016/j.pacfin.2018.01.007

[32] Dickason, Z., Ferreira, S. (2018). Establishing a link between risk tolerance, investor personality and behavioural finance in South Africa. Cogent Economics and Finance, 6(1): 1-13. https://doi.org/10.1080/23322039.2018.1519898

[33] Agnew, S., Harrison, N. (2015). Financial literacy and student attitudes to debt: A cross national study examining the influence of gender on personal finance concepts. Journal of Retailing and Consumer Services, 25: 122-129. https://doi.org/10.1016/j.jretconser.2015.04.006

[34] Rai, K., Dua, S., Yadav, M. (2019). Association of financial attitude, financial behaviour and financial knowledge towards financial literacy: A structural equation modeling approach. FIIB Business Review, 8(1): 51-60. https://doi.org/10.1177/2319714519826651

[35] Financial Capability Index a Toolkit for Use What is Financial Capability? Micro finance opportunities. https://microfinanceopportunities.org/fci-portal/FinancialCapabilityIndexToolkit.pdf, accessed on May 16, 2022.

[36] Bmrb, T.N.S. (2015). Financial Capability and Wellbeing’, Money Advice Service (March). https://moneyandpensionsservice.org.uk/wp-content/uploads/2021/03/financial-capability-and-wellbeing.pdf, accessed on May 16, 2022.

[37] Financial Capability in the United States 2016’ FINRA Investor Education Foundation (2016), (July). https://finrafoundation.org/sites/finrafoundation/files/NFCS-2015-Report-Natl-Findings.pdf, accessed on May 16, 2022.

[38] Schürz, M., Wagner, K. (2006). Financial capability of Austrian households. Monetary Policy & the Economy, 3: 50-67.

[39] Dvorak, T., Hanley, H. (2010). Financial literacy and the design of retirement plans. Journal of Socio-Economics, 39(6): 645-652. https://doi.org/10.1016/j.socec.2010.06.013

[40] Van Rooij, M., Lusardi, A., Alessie, R. (2009). Financial literacy and retirement planning in the Netherlands. DNB Working Paper, Journal of Economic Psychology, 32(4): 593-608. https://doi.org/10.1016/j.joep.2011.02.004

[41] Mccrae, R.R., Costa, P.T. (1997). Personality trait structure as a human universal. American Psychologist, 52(5): 509-516. https://doi.org/10.1037//0003- 066x.52.5.509

[42] Kempson, E., Perotti, V., Scott, K. (2013). Capability: A new instrument and results from low- and middle-income countries. Understanding Financial Well-Being. https://www.researchgate.net/publication/327155464_Measuring_financial_capability_a_new_instrument_and_results_from_low-_and_middle-income_countries.

[43] Kida, T., Moreno, K.K., Smith, J.F. (2010). Investment decision making: Do experienced decision makers fall prey to the paradox of choice? Journal of Behavioral Finance, 11(1): 21-30. https://doi.org/10.1080/15427561003590001

[44] Wilson, R.M.S. (1983). A concise guide to the literature of personal investment and financing. Managerial Finance, 9(3/4): 47-51. https://doi.org/10.1108/eb013529

[45] Mishra, D.L. (2012). Finance education is imperative for enhancing financial capability of Indian citizens. IOSR Journal of Business and Management, 5(5): 1-10. https://doi.org/10.9790/487x-0550110

[46] Hair, J.F., Ringle, C.M., Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2): 139-152. https://doi.org/10.2753/MTP1069-6679190202

[47] Hair, J.F., Hult, G., Tomas, M., Ringle, C.M., Sarstedt, M., Thiele, K.O. (2017). Mirror, mirror on the wall: a comparative evaluation of composite-based structural equation modeling method. Journal of the Academy of Marketing Science, 45(5): 616-632. https://doi.org/10.1007/s11747-017-0517-x

[48] Sarstedt, M., Hair, J.F., Ringle, C.M., Thiele, K.O., Gudergan, S.P. (2016). Estimation issues with PLS and CBSEM: Where the bias lies! Journal of Business Research, 69(10): 3998-4010. https://doi.org/10.1016/j.jbusres.2016.06.007

[49] Leguina, A. (2015). A primer on partial least squares structural equation modeling (PLS-SEM). International Journal of Research & Method in Education, 38(2): 220-221. https://doi.org/10.1080/1743727x.2015.1005806

[50] Fornell, C., Larcker, D. (1994). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Journal of marketing research. Advances Methods of Marketing Research, 18(3): 382-388. https://doi.org/10.2307/3150980

[51] Henseler, J., Hubona, G., Ray, P.A. (2016). Using PLS path modeling in new technology research: Updated guidelines. Industrial Management and Data Systems, 116(1): 2-20. https://doi.org/10.1108/IMDS-09-2015-0382

[52] Henseler, J., Ringle, C.M., Sarstedt, M. (2016). Testing measurement invariance of composites using partial least squares. International Marketing Review, 33(3): 405-431. https://doi.org/10.1108/IMR-09-2014-0304

[53] Cooper, W., Lowry, D. (2009). True colors personality test assessment analysis paper for EDF 6432. http://wmacooper.pbworks.com/f/WillCooper-True+Colors.pdf.

[54] Oliver, G., Liehr-gobbers, K., Krafft, M. (2010). Handbook of Partial Least Squares, 691-692. https://doi.org/10.1007/978-3-540-32827-8

[55] Streukens, S., Leroi-Werelds, S. (2016). Bootstrapping and PLS-SEM: A step-by-step guide to get more out of your bootstrap results. European Management Journal, 34(6): 618-632. https://doi.org/10.1016/j.emj.2016.06.003

[56] Radianto, W.E.D. (2020). The role of financial attitude in the relationship between financial knowledge and financial behavior. Journal of Xi’an University of Architecture & technology, XII(Xii): 374-385.

[57] Sherlyani, M., Pamungkas, A.S. (2020). Pengaruh financial behavior, risk tolerance, dan financial strain terhadap financial satisfaction. Jurnal Manajerial Dan Kewirausahaan, 2(1): 272. https://doi.org/10.24912/jmk.v2i1.7468

[58] Hilgert, M.A., Hogarth, J.M., Beverly, S.G. (2003). Household financial management: The connection between knowledge and behavior. Federal Reserve Bulletin, 106: 309-322.

[59] Huston, S.J. (2010). Measuring financial literacy. Journal of Consumer Affairs, 44(2): 296-316. https://doi.org/10.1111/j.1745-6606.2010.01170.x

[60] Potocki, T., Cierpiał-Wolan, M. (2019). Factors shaping the financial capability of low-income consumers from rural regions of Poland. International Journal of Consumer Studies, 43(2): 187-198. https://doi.org/10.1111/ijcs.12498

[61] Arifin, A.Z. (2018). Influence factors toward financial satisfaction with financial behavior as intervening variable on Jakarta area workforce. European Research Studies Journal, 21(1): 90-103.

[62] Shim, S., Serido, J., Bosch, L., Tang, C.Y. (2013). Financial identity-processing styles among young adults: A longitudinal study of socialization factors and consequences for financial capabilities. Journal of Consumer Affairs, 47(1): 128-152. https://doi.org/10.1111/joca.12002

[63] Batty, M., Collins, J.M., Odders-White, E. (2015). Experimental evidence on the effects of financial education on elementary school students’ knowledge, behavior, and attitudes. Journal of Consumer Affairs, 49(1): 69-96. https://doi.org/10.1111/joca.12058

[64] Freeman, V., Jung, C. Blue & C - Personality Traits of Leaders, 1-4. https://files.eric.ed.gov/fulltext/EJ1068487.pdf, accessed on May 16, 2022.

[65] Hartsfield, L. (2008). The effect of color on personality traits. http://www.drspeg.com/research/2008/personalitycolor.pdf, accessed on May 16, 2022.